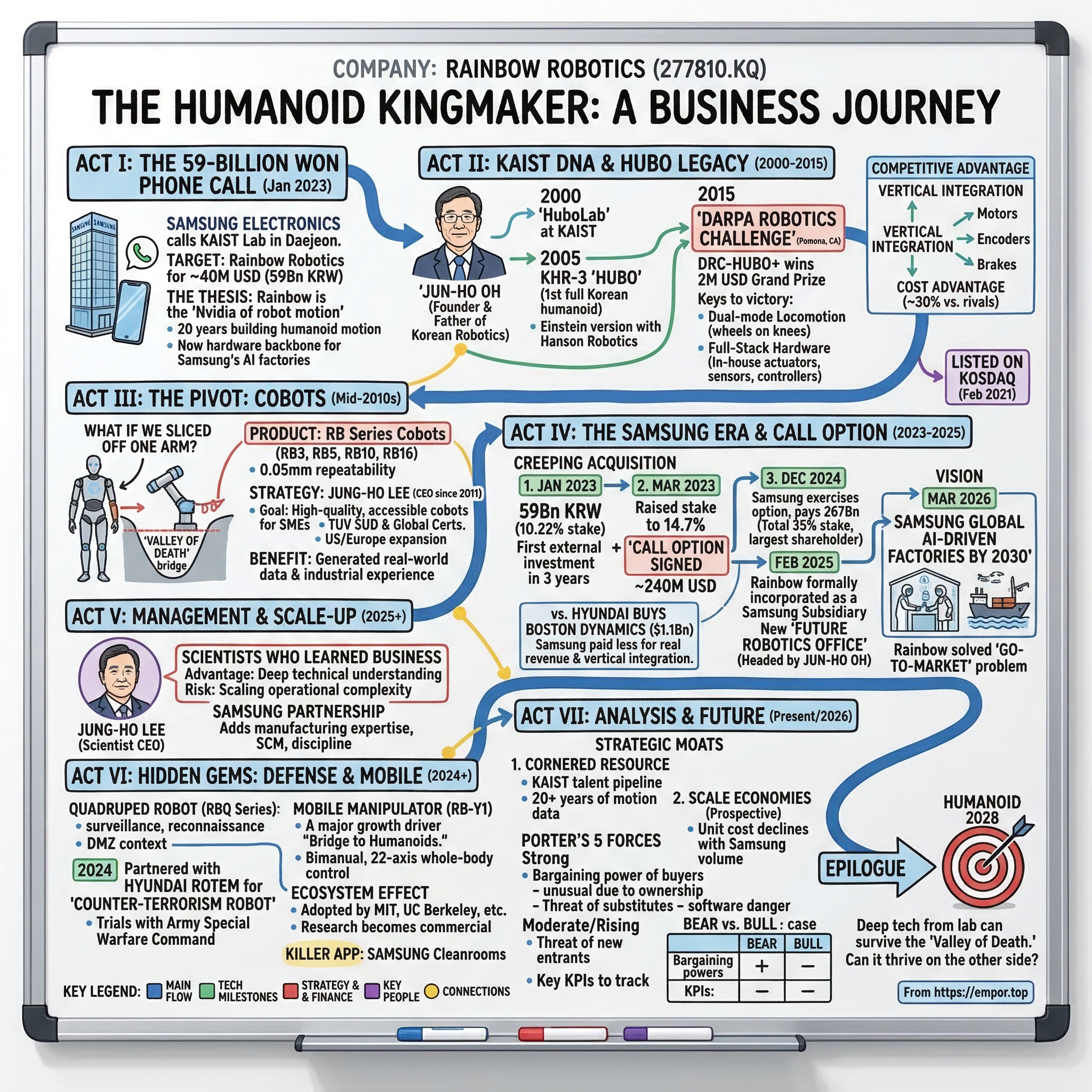

Rainbow Robotics: The Humanoid Kingmaker

I. Introduction: The 59-Billion Won Phone Call

Picture this: it is January 2023, and somewhere inside the glass towers of Samsung Electronics' Suwon campus, a decision has been made that will rewrite the future of South Korean robotics. Samsung, the largest conglomerate in the world by revenue, a company that had been conspicuously silent on external M&A for nearly three years, picks up the phone. The call does not go to a chip designer in Austin or a software unicorn in San Francisco. It goes to a modest research lab in Daejeon, a city best known for hosting KAIST, Korea's answer to MIT.

The target: Rainbow Robotics Co., Ltd. The price: 59 billion Korean won, roughly $40 million. For Samsung, this was pocket change—less than what they spend on semiconductor R&D in a single day. But for Rainbow Robotics, it was existential. It was the moment a small team of roboticists, who had spent two decades building humanoid robots that could walk, talk, and win global competitions, finally got the backing they needed to go from science project to industrial platform.

The thesis here is deceptively simple. Rainbow Robotics is not just another robotics startup riding the AI hype cycle. They are the "Nvidia of robot motion"—the company that spent twenty years building the hardest part of robotics (making a machine move like a human) and is now positioned to become the hardware backbone for the largest electronics manufacturer on the planet. While the world obsesses over Tesla's Optimus and Boston Dynamics' viral videos, Rainbow has been quietly building something that may matter more: the ability to mass-produce the actuators, controllers, and motion systems that make robots actually work in a factory.

This is a story that moves through three distinct acts. First, the origin myth: how a university professor's obsession with making a robot walk led to a $2 million DARPA prize and a generation of Korean robotics talent. Second, the pivot: how Rainbow realized that humanoids were a decade away from profitability and made the clever decision to "slice off" a humanoid arm and sell it as a collaborative robot. And third, the Samsung era: the creeping acquisition that turned Rainbow from an independent research lab into the cornerstone of Samsung's vision for AI-driven factories by 2030.

The roadmap is clear. From the DARPA Robotics Challenge in the California desert to the cleanrooms of Samsung's semiconductor fabs, Rainbow Robotics has been playing a longer game than almost anyone in the industry. And the game is just getting started.

II. The KAIST DNA and The HUBO Legacy

To understand Rainbow Robotics, you first have to understand Jun-Ho Oh. In the world of Korean robotics, Oh is not just a professor—he is the founding father, the man who convinced an entire country that building a walking, talking humanoid robot was not a fantasy but a national priority.

Oh's path to robotics was anything but direct. He earned his bachelor's and master's degrees in mechanical engineering from Yonsei University, one of Korea's elite institutions, then spent time at the Korea Atomic Energy Research Institute before heading to the University of California, Berkeley for his Ph.D. He returned to Korea in 1985 and joined KAIST's Department of Mechanical Engineering, where he would spend the next four decades. But it was in the late 1990s, as Honda's ASIMO and Sony's QRIO were capturing global headlines, that Oh became consumed by a singular question: could Korea build a humanoid robot that could compete with—and beat—the best in the world?

The answer began taking shape in 2000, when Oh established the Humanoid Robot Research Center at KAIST, known simply as HuboLab. The first prototype, KHR-0, was little more than a pair of mechanical legs on a tethered platform—no torso, no arms, no head. It was crude, but it walked. By 2003, the team had progressed to KHR-1, a 21-degree-of-freedom robot with legs, a torso, and rudimentary arms. The Korean government, recognizing the strategic importance of the work, began funding the project at roughly $500,000 per year—a modest sum by global standards, but enough to keep the lab running.

The breakthrough came on January 6, 2005, when KAIST unveiled KHR-3, renamed HUBO (short for "humanoid robot"). HUBO was the first full Korean humanoid—41 degrees of freedom, a human-like appearance, and the ability to walk, grasp objects, and even gesture. Later that year, Oh partnered with David Hanson of Hanson Robotics to create Albert HUBO, the world's first walking android with a realistic human face—an Einstein replica, no less—mounted on a bipedal frame. The stunt generated global headlines and established Korea as a serious player in humanoid robotics.

But the real test came a decade later, in the blistering heat of Pomona, California. The DARPA Robotics Challenge, launched in the wake of the Fukushima nuclear disaster, was designed to push the boundaries of what robots could do in disaster scenarios. Twenty-four teams from six countries converged for the finals in June 2015, each tasked with completing eight grueling tasks: driving a vehicle, opening a door, turning a valve, drilling through a wall, navigating debris, and climbing stairs, among others.

The competition was stacked. Boston Dynamics had entered their Atlas robot, backed by Google's deep pockets. NASA fielded Valkyrie. Carnegie Mellon, MIT, and a host of other elite institutions had poured millions into their entries. Team KAIST, led by Oh, arrived with DRC-HUBO+, a 5-foot-9, 176-pound humanoid that looked modest by comparison. But HUBO had a secret weapon—a "Transformer" trick that no other robot could match. When walking was too risky or too slow, DRC-HUBO dropped to its knees, where concealed wheels on its ankles and kneecaps allowed it to glide across flat surfaces with speed and stability. This was not elegance for elegance's sake. In a competition where a single fall could cost minutes, HUBO's dual-mode locomotion was a masterstroke of pragmatic engineering.

DRC-HUBO completed all eight tasks with a perfect score in 44 minutes and 28 seconds. Three teams achieved perfect scores, but HUBO's time was the fastest by a decisive margin. Team KAIST took home the $2 million grand prize, and Jun-Ho Oh became a national hero. The Korean government awarded him the Changjo Medal for Science and Technology and the prestigious Ho-Am Prize in Engineering. More importantly, the victory proved something that the Korean robotics community had long believed: that deep, vertically integrated hardware expertise—building your own actuators, sensors, and controllers from scratch rather than assembling off-the-shelf parts—was the path to building robots that actually worked in the real world.

This "full-stack" hardware philosophy would become Rainbow Robotics' defining competitive advantage. Unlike competitors who relied on third-party servo motors and commercial sensors, Oh's team designed and manufactured every critical component in-house. The actuators that powered HUBO's joints, the encoders that tracked its movements, the real-time controllers that coordinated dozens of motors simultaneously—all of it was proprietary. This was not just a matter of pride. It meant that Rainbow understood the physics of robot motion at a level that companies buying components from catalogs simply could not match. And it meant that their cost structure was fundamentally different: no markup from suppliers, no dependency on third-party lead times, and the ability to optimize every component for the specific demands of their robots.

The transition from lab to company had actually begun four years before the DARPA triumph. In 2011, Oh and his protégé Jung-Ho Lee formally incorporated Rainbow Robotics—the name stands for "Robot for Artificial Intelligence and Boundless Walking"—after receiving simultaneous commercial inquiries from U.S. universities and the Singapore government for HUBO2 units. But in those early years, building humanoids for research clients did not pay the bills. To keep the lights on, Rainbow sold an unlikely product: astronomical mounts, the precision tracking systems used to stabilize telescopes. It was an odd business for a robotics company, but the engineering overlap was real—both applications required extreme precision in motor control and positioning. The astronomical mount business generated just enough revenue to fund continued R&D on the humanoid platform.

The company listed on the KOSDAQ exchange on February 3, 2021, at a market capitalization of approximately 405 billion Korean won, roughly $350 million. At the time, the IPO was a bet on the future—Rainbow's revenue was just 5.4 billion won the prior year, and the company was deeply unprofitable. But the KOSDAQ investors who bought in were not paying for current earnings. They were paying for twenty years of accumulated expertise in making machines move like humans, and for the option value of what that expertise could become if the right partner came along.

That partner was about to make a phone call.

III. The Pivot: Collaborative Robots (Cobots)

There is a classic dilemma in deep tech: you can build something extraordinary, but if the market is not ready, brilliance does not pay rent. By the mid-2010s, Rainbow Robotics faced this dilemma in its purest form. They had the world's most advanced humanoid robot platform. They had won the DARPA prize. They had a team of engineers who understood bipedal locomotion better than almost anyone on the planet. And they had almost no revenue.

The humanoid market, to put it bluntly, did not exist. There was no factory ordering humanoid robots for production lines. No logistics company deploying them in warehouses. The technology was extraordinary, but the applications were still a decade away from commercial viability. Oh and Lee knew this. The question was what to do about it.

The answer was elegantly simple, and it reveals a strategic instinct that separates companies that survive the "Valley of Death" from those that become footnotes in academic journals. Rainbow looked at their humanoid and asked: what if we sliced off just one arm?

A humanoid robot is, at its core, a collection of subsystems—legs for locomotion, arms for manipulation, a torso for coordination, a head for perception. Each subsystem is an engineering marvel on its own. The arm, in particular, is where most of the practical value lies for industrial applications. A robotic arm that can grip, place, weld, or assemble components is useful in a factory today. A walking, talking humanoid is useful in a science fiction movie. Rainbow made the pragmatic choice: they took their humanoid arm technology—the same actuators, the same controllers, the same motion-planning algorithms that powered HUBO's precise movements—and packaged it into a standalone collaborative robot, or "cobot."

The result was the RB series, Rainbow's line of collaborative robots designed to work alongside human workers in manufacturing environments. The lineup spans multiple payload classes: the RB3 handles 3 kilograms with either 730mm or 1,200mm reach, the RB5 manages 5 kilograms, the RB10 lifts 10 kilograms with an impressive 1,300mm reach, and the RB16 handles 16 kilograms. All achieve a repeatability of plus or minus 0.05 millimeters—a level of precision that puts them on par with the best cobots in the world.

The competitive benchmarking tells a compelling story. The global cobot market has been dominated for years by Universal Robots, the Danish company acquired by Teradyne in 2015. Universal Robots has sold over 37,000 units and enjoys the kind of brand recognition in industrial automation that iPhone has in smartphones. But Universal Robots has a structural disadvantage: they buy their actuators and sensors from third-party suppliers, which means their cost of goods sold includes significant markups from the component supply chain.

Rainbow, by contrast, manufactures all essential cobot components in-house: actuators, encoders, brakes, controllers, and motor drivers. This vertical integration gives them an estimated 30 percent cost advantage over comparable Universal Robots models. For a factory manager evaluating cobots, this is not a trivial difference. A cobot that costs $25,000 instead of $35,000, with equivalent performance and reliability, is a compelling value proposition—especially for the small and medium-sized manufacturers that represent the fastest-growing segment of the cobot market.

The gross margins reflect this advantage. While exact figures for the cobot segment alone are not broken out, Rainbow's overall gross profit margin has been running around 32-33 percent, and the cobot business is believed to be materially higher, likely approaching 50 percent, due to the absence of third-party component costs. For context, Universal Robots' parent Teradyne reports gross margins of roughly 55-60 percent for the overall company, but Universal Robots itself is widely believed to operate at lower margins because of its reliance on external suppliers.

Product-market fit came through a series of real-world deployments that demonstrated the RB series was not just a cheaper alternative but a genuinely versatile tool. Rainbow's cobots found their way into welding cells, CNC machine tending operations, grinding and polishing stations, assembly lines, and palletizing systems. One of the more visible applications was coffee-making—Rainbow deployed barista robots that could prepare and serve drinks autonomously, a crowd-pleasing demonstration that doubled as a proof of concept for the precision and reliability of their motion control systems.

CEO Jung-Ho Lee, who had been with the company since its founding, drove the commercialization strategy with a clear-eyed focus on accessibility. His vision was to make high-quality cobots available to small and mid-sized companies that had traditionally been priced out of automation. This was not just a sales pitch—it was a genuine market insight. The vast majority of the world's manufacturing is done by companies with fewer than 500 employees, and these companies have been dramatically underserved by the industrial robotics incumbents like FANUC, ABB, and KUKA, whose products are designed for large-scale production lines and priced accordingly.

Rainbow also certified their cobots through TUV SUD, earning CE (European), NRTL (North American), and KCs (Korean) certifications—a necessary but expensive step that signaled their intent to compete globally, not just in the Korean domestic market. By 2023, the company had established a U.S. subsidiary in Schaumburg, Illinois, and set up two distributors in Germany to access the European market.

The cobot pivot was more than just a revenue strategy. It was a bridge. Every cobot sold was generating real-world data on actuator performance, controller reliability, and customer requirements. Every deployment was training Rainbow's engineering team on the practical challenges of industrial automation—challenges that would prove essential when Samsung came calling with a much bigger vision. The cobot business was not the endgame. It was the proving ground.

IV. The Samsung Era: Capital Deployment and the Call Option

The Samsung investment in Rainbow Robotics was not a single event. It was a three-year campaign of capital deployment that, in retrospect, looks like one of the most disciplined "creeping acquisitions" in recent Korean corporate history. To understand why it matters, you need to understand both the mechanics of the deal and the strategic logic behind it.

In January 2023, Samsung Electronics made its first move: a 59 billion won investment (approximately $40 million) for a 10.22 percent stake. For Samsung, this was a rounding error—the company's annual capital expenditure runs north of $30 billion. But the signal was unmistakable. Samsung had not made a significant external investment in nearly three years. The fact that they chose a small robotics company from Daejeon, rather than a semiconductor equipment maker or an AI software firm, told the market something important about Samsung's strategic priorities.

Two months later, in March 2023, Samsung made a second move that was far more consequential than the initial investment. They purchased additional shares to bring their stake to approximately 14.7 percent, and—crucially—they signed a call option agreement. The call option gave Samsung the right to purchase shares held by Rainbow's largest shareholders and related parties if those shares were ever put up for sale. In financial terms, this was Samsung planting a flag: they were telling the market, and telling Rainbow's other shareholders, that they intended to be the controlling owner of this company. The question was not if, but when.

The "when" came on December 30, 2024. Samsung exercised the call option, paying 267 billion won (approximately $181 million) to acquire additional shares and bring their total stake to 35 percent, making them Rainbow's largest shareholder. The total investment across all three tranches came to roughly 354 billion won, or about $240 million.

To appreciate the brilliance of this approach, compare it to the most famous robotics acquisition of the decade: Hyundai's purchase of Boston Dynamics. In 2020, Hyundai Motor Group paid $1.1 billion for an 80 percent stake in Boston Dynamics, a company renowned for its viral YouTube videos of parkour-performing robots but notorious for its inability to generate meaningful commercial revenue. Boston Dynamics had been passed around like a hot potato—acquired by Google's parent Alphabet in 2013, sold to SoftBank in 2017, and then sold again to Hyundai. Despite billions of dollars in cumulative investment, Boston Dynamics' commercial robot, Spot, had generated only modest sales.

Samsung's approach was the opposite. Instead of paying a billion-dollar premium for brand recognition and YouTube views, they paid a fraction of that amount for a company with actual revenue, actual products in customer factories, and actual vertical integration in the components that matter most. Samsung's total investment in Rainbow, including the call option exercise, was less than a quarter of what Hyundai paid for Boston Dynamics. Yet Rainbow arguably had a clearer path to commercial viability, thanks to its established cobot business and its full-stack hardware capabilities.

The strategic implications of the deal extended far beyond the financial terms. In February 2025, Rainbow Robotics was formally incorporated as a Samsung subsidiary under Samsung Electronics' consolidated financial statements. Samsung established a Future Robotics Office reporting directly to the Samsung CEO, and appointed Jun-Ho Oh—Rainbow's founder and the godfather of Korean robotics—as the head of this new office and a special advisor to Samsung.

This was the moment the deal's true purpose became clear. Samsung was not buying Rainbow Robotics for its cobot revenue, which at roughly 19 billion won in 2024 was negligible by Samsung standards. Samsung was buying the team, the technology, and the twenty-year head start in robot motion control. The objective was nothing less than transforming Samsung's global manufacturing operations.

On March 1, 2026, Samsung announced its plan to convert all of its global production facilities into "AI-driven factories" by 2030, using humanoid robots and agentic AI systems. Rainbow Robotics' cobots, mobile manipulators, and eventually humanoid robots would be at the center of this transformation. For Rainbow, the Samsung deal instantly solved the single biggest problem facing any hardware startup: go-to-market. Samsung operates semiconductor fabs, display factories, appliance plants, and shipyards on nearly every continent. Each one of these facilities is a potential deployment site for Rainbow's products. There is no need to build a sales team, no need to establish distribution channels, no need to convince skeptical factory managers to take a chance on an unknown brand. Samsung is both the customer and the owner.

This dynamic—where the acquirer is also the primary customer—creates a powerful flywheel. Samsung deploys Rainbow robots in its factories. The deployment generates performance data and customer feedback. Rainbow uses that data to improve its products. The improved products get deployed more widely. And with each cycle, Rainbow's unit costs decline as production scales up. It is a classic example of what Hamilton Helmer would call "Scale Economies"—the more robots Samsung deploys, the cheaper each additional robot becomes, and the harder it is for any competitor to match Rainbow's cost structure.

But the Samsung deal also carried risks. The most obvious was the "captive supplier" problem. If Rainbow becomes entirely dependent on Samsung for revenue, it loses the incentive and the ability to innovate for the broader market. A robot optimized for Samsung's semiconductor fabs may not be the best robot for a German automotive plant or a Japanese food processing facility. The deal structurally ties Rainbow's fate to Samsung's, for better and for worse.

V. Management: The Scientists Who Became CEOs

In most technology companies, there is a moment where the founders step aside and "professional management" takes over. The engineers who built the product give way to the MBAs who know how to scale it. At Rainbow Robotics, that moment never came—and the company is arguably better for it.

Jung-Ho Lee has been CEO of Rainbow Robotics since the company's incorporation in February 2011, making him one of the longest-tenured CEOs in the Korean robotics industry. Lee earned his Ph.D. in Robotics from KAIST, where he was a researcher at the Humanoid Robot Research Center under Jun-Ho Oh. He is not a business school graduate who was parachuted in to "professionalize" a research lab. He is a roboticist who learned business by necessity, because someone had to sell astronomical mounts and cobot arms to keep the lights on while the humanoid dream incubated.

This background matters more than it might seem. In hardware companies, the distance between the CEO's office and the engineering floor can determine whether products ship on time, whether quality is maintained, and whether the company pursues technically feasible ambitions rather than PowerPoint fantasies. Lee understands the physics. When a customer reports a vibration issue with an RB10 cobot at a specific joint velocity, Lee does not need an engineer to translate the problem for him. He can diagnose the issue himself, trace it to the actuator design, and make informed decisions about whether the fix requires a firmware update or a hardware revision.

Jun-Ho Oh, the founder, occupied a different role. After spending decades as the intellectual engine of the company—the man who conceived HUBO, won the DARPA prize, and built the technical team from scratch—Oh moved into an advisory role at Rainbow and took on a new mandate as the head of Samsung's Future Robotics Office. This transition, which coincided with Samsung's consolidation of its Rainbow stake in early 2025, was significant. It signaled that Oh's expertise was now being applied at Samsung scale, overseeing the integration of Rainbow's technology into Samsung's broader manufacturing and product strategy.

Oh's credentials are staggering. Beyond his Berkeley Ph.D. and four decades at KAIST, he served as a robotics policy consultant for the Korean Ministry of Commerce, Industry, and Energy. He is a member of the Korea Academy of Science and Technology. His awards—the Changjo Medal, the Ho-Am Prize, KAIST Distinguished Professor, "Top 10 Scientists of the Year," a Presidential Citation—read like a greatest-hits album of Korean scientific recognition. In interviews, Oh has described himself as driven by a simple conviction: that Korea must build the world's best humanoid robot, and that the way to do it is to control every piece of the technology stack, from the smallest bearing in an actuator to the highest-level motion-planning algorithm.

The ownership structure reinforces alignment. Oh retained a significant stake in Rainbow post-Samsung, and lock-up agreements tied to the Samsung deal ensure that the founding team's interests remain aligned with the long-term integration strategy rather than short-term stock price movements. The management team is incentivized to make Samsung's AI-driven factory vision a reality, not to chase flashy R&D projects that generate headlines but no revenue.

There is a broader lesson here about what kind of leadership a company like Rainbow needs at this stage of its evolution. The conventional wisdom says that you need a "business person" to commercialize deep tech—someone who can talk to customers, manage supply chains, and navigate corporate partnerships. But Rainbow's experience suggests otherwise. The technical credibility of the leadership team was arguably what attracted Samsung in the first place. Samsung did not need a slick sales pitch. They needed to know that the people running Rainbow understood robot motion at a fundamental level, and that the products they were buying were not assemblages of off-the-shelf parts dressed up with marketing.

The risk, of course, is that a scientist-led company may struggle with the operational challenges of scaling production. Building ten cobots for a research lab is a fundamentally different challenge than building ten thousand for Samsung's global factory network. This is where the Samsung partnership becomes critical: Samsung brings world-class manufacturing expertise, supply chain management, and operational discipline. Rainbow brings the technology and the talent. Whether this combination can work at scale is one of the central questions facing the company.

VI. Hidden Gems: Defense and The Mobile Manipulator

Beyond the cobot business and the Samsung integration, Rainbow Robotics has been quietly building capabilities in two areas that rarely get attention from analysts but could prove transformative: defense robotics and mobile manipulation.

The defense story starts with legs, not arms. Rainbow's quadruped robot program—the RBQ series—grew directly out of the bipedal locomotion expertise that the team developed for HUBO. If you can make a robot walk on two legs over uneven terrain, making one walk on four legs is, in some ways, a simpler problem (though still fiendishly difficult by any normal engineering standard). The RBQ-3 and RBQ-10 are four-legged robots designed for surveillance, reconnaissance, patrol, and search missions—the kind of tasks that are too dangerous for human soldiers but too complex for wheeled drones.

In 2024, Rainbow partnered with Hyundai Rotem—the defense arm of Hyundai Motor Group—to develop a multi-legged walking robot specifically for counter-terrorism operations. The project was part of a state-led fast-track R&D program, the kind of government-backed initiative that signals serious intent rather than speculative research. The two companies spent two years developing the platform, which can be equipped with a robotic arm, a remote weapon system, and a tear gas sprayer.

The Defense Acquisition Program Administration, South Korea's equivalent of the Pentagon's procurement office, launched a six-month operational trial of the quadruped with the Army Special Warfare Command in August 2024. The trial was designed to evaluate the robot's effectiveness in real-world counter-terrorism scenarios—border patrol, building clearance, and hostage situations where sending a human first is unacceptably dangerous.

South Korea's defense context makes this particularly relevant. The Korean Demilitarized Zone, the most heavily fortified border in the world, stretches 250 kilometers along the 38th parallel. The Korean military has long sought autonomous systems for border surveillance, and a quadruped robot that can navigate the rugged, mountainous terrain of the DMZ without roads or flat surfaces is a compelling solution. The classified nature of some of these collaborations means that the full scope of Rainbow's defense business is not publicly known, but the Hyundai Rotem partnership and the Army trial suggest meaningful revenue potential.

Then there is the product that could be Rainbow's most important: the RB-Y1, a bimanual mobile manipulator that represents the bridge between today's stationary cobots and tomorrow's humanoid robots.

Think of it this way. A cobot is an arm bolted to a table. It can do extraordinary things within its reach, but it cannot move to a different workstation. A humanoid is a full-body robot that can walk, reach, and manipulate objects anywhere. But humanoids are expensive, complex, and years away from reliable industrial deployment. The mobile manipulator sits in the sweet spot: it puts a pair of robotic arms on a wheeled base, giving it the dexterity of a cobot and the mobility of an autonomous vehicle.

The RB-Y1 is Korea's first bimanual mobile manipulator, and its specifications are impressive. It features two 7-degree-of-freedom arms (for comparison, a human arm has seven degrees of freedom), a 6-axis single leg, and a wheeled mobile platform. It stands 1.4 meters tall, weighs 131 kilograms, and each arm can lift 3 kilograms. Its 20-axis whole-body control system manages the robot's center of gravity dynamically, allowing it to perform tasks that require coordination between both arms while moving.

Rainbow priced the RB-Y1 research platform at $80,000 and the commercial platform at $120,000 to $150,000—aggressive pricing that has attracted attention from top AI research labs. MIT, UC Berkeley, the University of Washington, and Georgia Tech have all adopted the RB-Y1 as a research platform, which means that the next generation of AI-powered robot control algorithms is being developed on Rainbow's hardware. This has echoes of how Nvidia's GPUs became the default platform for AI research and then rode that research ecosystem to commercial dominance.

The "killer app" for the mobile manipulator, however, is not in research labs. It is in Samsung's semiconductor cleanrooms. These environments require extreme precision, minimal contamination, and the ability to move materials between workstations without human intervention. A mobile manipulator that can navigate a cleanroom autonomously, pick up wafer carriers with precise dual-arm coordination, and deliver them to the next processing step is worth far more than a stationary cobot. This is the "hidden" business that analysts are only beginning to model, and it could dwarf the standalone cobot market in revenue terms if Samsung deploys these systems across its global fab network.

Rainbow also has a nascent medical robotics program. In February 2025, a company called Erop completed preclinical trials for laparoscopic cholecystectomy—gallbladder removal surgery—in collaboration with Rainbow Robotics. The surgical robotics market is dominated by Intuitive Surgical's da Vinci system, a multi-billion dollar franchise with formidable competitive moats. Rainbow is not positioned to challenge Intuitive directly, but the underlying technology—precise, multi-degree-of-freedom manipulation with force feedback—is closely related to their core competency. Medical robotics is better understood as a long-term option embedded in Rainbow's technology platform rather than a near-term revenue driver.

VII. The Playbook: Strategic Moats and Competitive Positioning

To evaluate Rainbow Robotics as an investment, it helps to apply two of the most rigorous frameworks in business strategy: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. Together, they reveal a company with genuine competitive advantages but also significant structural vulnerabilities.

Start with Helmer's framework. The most obvious power Rainbow possesses is what Helmer calls a "Cornered Resource"—an asset that competitors cannot replicate or acquire. In Rainbow's case, this is the twenty-plus years of humanoid motion data, proprietary actuator designs, and accumulated engineering know-how that emerged from the HUBO program. You cannot buy this on the open market. You cannot recruit a few engineers from Rainbow and replicate it at a new company. The knowledge is distributed across the entire organization, embedded in thousands of design decisions, test results, and iterative refinements that were made over two decades. When Rainbow designs an actuator for a cobot joint, they are drawing on data from humanoid gait-balancing experiments that no other commercial robotics company has ever conducted.

The KAIST talent pipeline reinforces this cornered resource. KAIST is the undisputed center of Korean robotics research, and Rainbow has been the primary destination for KAIST robotics graduates for over a decade. This is not unlike how Nvidia's proximity to Stanford and Berkeley created a self-reinforcing loop of talent acquisition. The best robotics students in Korea want to work at Rainbow because Rainbow is where the most interesting problems are. And because Rainbow has the best talent, they produce the best technology, which attracts the next generation of the best talent.

The second power is Scale Economies, though this one is more prospective than realized. As Samsung deploys Rainbow robots across its global factory network, the unit economics should improve dramatically. Fixed R&D costs get amortized over a much larger production base. Component costs decline as suppliers offer volume discounts (or as Rainbow's in-house manufacturing achieves economies of scale). Service and support costs per unit drop as the installed base grows. If Samsung's 2030 vision for AI-driven factories materializes, Rainbow could achieve unit costs that no global competitor can match—not because their technology is inherently cheaper, but because their captive customer is orders of magnitude larger than any competitor's.

The third potential power is what Helmer calls "Process Power"—advantages that emerge from doing something in a specific way that is embedded in organizational culture and cannot be easily copied. Rainbow's full-stack hardware approach, where they design and manufacture actuators, encoders, brakes, controllers, and motor drivers in-house, qualifies. This is not a strategy that a competitor can adopt overnight. It requires years of investment in manufacturing capabilities, deep expertise in multiple engineering disciplines, and an organizational culture that values vertical integration over speed-to-market.

Now turn to Porter's 5 Forces, which paint a more nuanced picture.

The bargaining power of buyers is perhaps the most unusual dynamic in the robotics industry. Samsung is simultaneously Rainbow's largest shareholder and its most important customer. In a normal buyer-supplier relationship, the buyer's bargaining power is a threat—they can demand lower prices, better terms, or switch to a competitor. But when the buyer owns 35 percent of the supplier, the incentives are fundamentally different. Samsung has no interest in squeezing Rainbow's margins to zero, because Samsung benefits from Rainbow's profitability and long-term health. This creates an unusually stable demand environment, but it also raises the question of whether Rainbow can negotiate effectively with its controlling shareholder on pricing and terms.

The threat of new entrants is moderate and rising. The global excitement around humanoid robots has attracted enormous capital—Figure AI, backed by Microsoft and OpenAI, has raised hundreds of millions. Tesla has committed significant resources to Optimus. Chinese companies like Unitree are pushing aggressive pricing on quadruped robots. However, the barrier to entry in the specific niche where Rainbow operates—vertically integrated motion control hardware with two decades of proprietary data—remains extremely high. A well-funded startup can build a impressive-looking humanoid prototype in two years. Building the actuators, controllers, and motion systems to the level of reliability required for industrial deployment in a Samsung semiconductor fab takes much longer.

The threat of substitutes is where things get interesting. The most significant competitive threat to Rainbow does not come from other hardware companies. It comes from software. If Tesla or another AI-first company develops control algorithms that can make a cheap, commodity humanoid perform reliably in industrial settings, the value of Rainbow's proprietary hardware could erode. This is the "Nvidia risk" in reverse: Nvidia's moat is in hardware that makes AI software run fast, but if someone develops AI chips that are "good enough" at a fraction of the cost, Nvidia's premium evaporates. Similarly, if AI software becomes sophisticated enough to compensate for inferior hardware, Rainbow's full-stack hardware advantage becomes less valuable.

The intensity of rivalry in the cobot market is high and increasing. Universal Robots, Doosan Robotics, FANUC, ABB, and Techman Robot all compete aggressively on price, features, and distribution. Doosan Robotics, Rainbow's most direct domestic competitor, went public on the KOSDAQ in October 2023 and has a market capitalization of roughly 5.3 trillion won. Doosan has sold over 2,000 cobots and is aggressively expanding internationally. The cobot market is growing fast—estimated to exceed $10 billion by 2030—but the number of well-funded competitors is growing even faster.

For investors tracking Rainbow's trajectory, three KPIs matter most. First, the cobot order backlog and unit shipment growth, which is the clearest indicator of commercial traction independent of Samsung. Second, the revenue concentration ratio with Samsung—specifically, what percentage of total revenue comes from Samsung-related deployments versus third-party customers. A healthy company should see Samsung revenue growing in absolute terms while declining as a percentage of total revenue, indicating that external demand is scaling even faster. Third, the gross margin trend, which reflects whether vertical integration is delivering the cost advantage that the thesis depends on, or whether competitive pressure and scaling challenges are compressing margins.

VIII. Analysis: Bear vs. Bull Case

Every investment thesis needs a devil's advocate, and Rainbow Robotics' bull case is aggressive enough to warrant a serious examination of what could go wrong.

The bear case begins with the "captive supplier" risk. Rainbow Robotics is, as of early 2026, effectively a Samsung subsidiary. Samsung owns 35 percent of the company, the founder has moved to Samsung's Future Robotics Office, and Samsung's AI-driven factory vision is the primary demand driver for Rainbow's products. If Samsung's factory automation plans are delayed, scaled back, or redirected toward different technology, Rainbow has limited ability to pivot. The company's go-to-market outside Samsung—a U.S. subsidiary and two German distributors—is embryonic relative to the scale of the Samsung relationship.

There is a historical pattern worth noting. Samsung has a long track record of building capabilities internally rather than nurturing acquisitions. Samsung SDI, Samsung Electro-Mechanics, and Samsung SDS are all examples of subsidiaries that were absorbed into Samsung's ecosystem and optimized for Samsung's needs rather than the external market. If Rainbow follows this pattern, it could become a highly profitable captive supplier to Samsung but lose the ability to compete for—and win—global customers. A robot optimized for Samsung's semiconductor fabs may not be the best robot for a BMW assembly line or an Amazon warehouse.

The valuation amplifies this risk. As of March 2026, Rainbow Robotics trades at a market capitalization of roughly 13.9 trillion won (approximately $9.5 billion) against trailing revenue of just 34 billion won. That is a price-to-sales ratio of over 300 times. Even by the generous standards of high-growth robotics companies, this is stratospheric. Doosan Robotics, with higher revenue and a more established distribution network, trades at a fraction of Rainbow's valuation. The stock price, which hit an all-time high of 934,000 won on March 3, 2026, is pricing in not just Samsung's factory automation plans but the entire humanoid robot future—a future that is still years away from generating meaningful revenue.

The second bear argument is execution risk. Scaling from dozens of cobots per year to thousands requires a fundamentally different manufacturing operation. Rainbow had approximately 75 employees as recently as 2024. Even with Samsung's manufacturing expertise, the transition from artisanal production to industrial scale involves new supply chains, new quality control processes, new hiring, and new operational challenges. Companies that make this transition successfully—think Tesla ramping Model 3 production—typically go through a prolonged period of pain that the market does not fully appreciate in advance.

The third bear argument is competitive convergence. The humanoid robot space is attracting unprecedented capital. Tesla, Figure AI, Boston Dynamics, Agility Robotics, and multiple well-funded Chinese companies are all racing to develop commercially viable humanoid robots. If the humanoid platform becomes commoditized—if the "intelligence" is in the AI software rather than the hardware—then Rainbow's decades of motion-control expertise may prove less valuable than the market assumes. Tesla, with its massive AI infrastructure and billions of miles of real-world data from its autonomous driving program, could potentially leapfrog Rainbow's hardware advantage by developing software that makes a cheaper robot perform just as well.

Now the bull case.

The strongest argument for Rainbow Robotics is the simplest: if Samsung wants a humanoid robot in every factory—and eventually in every home—Rainbow is the only company that can build the limbs. Samsung's March 2026 announcement that it intends to convert all global factories to AI-driven operations by 2030 was not a press release puff piece. It was a corporate commitment from a company that spends over $30 billion per year on capital expenditure and has a track record of executing on ambitious manufacturing transformations. Samsung built the world's most advanced semiconductor fabs. They built the world's largest shipyard (through Samsung Heavy Industries). When Samsung says they are going to automate their factories, the probability of execution is meaningfully higher than when a startup says the same thing.

Rainbow is the hardware "shell" for Samsung's AI brain. Samsung's expertise in AI and semiconductor design provides the intelligence; Rainbow provides the physical embodiment. This is a complementary relationship, not a competitive one. Samsung does not need to build its own actuators and motion controllers from scratch—it has a subsidiary that has spent twenty years perfecting them. Similarly, Rainbow does not need to develop its own AI capabilities—it has a parent company that designs the chips those AI models run on.

The RB-Y1 mobile manipulator represents a second growth vector that is independent of the humanoid timeline. If Rainbow can establish the RB-Y1 as the default research platform for academic robotics—and with MIT, Berkeley, University of Washington, and Georgia Tech already on board, they are well on their way—the company benefits from a powerful ecosystem effect. Researchers who develop algorithms on RB-Y1 hardware will naturally prefer to deploy those algorithms on RB-Y1 hardware in commercial settings. This is exactly how Nvidia built its AI dominance: by becoming the default platform for research and then riding the research ecosystem into commercial deployment.

The humanoid commercialization target of 2028 is aggressive but not unrealistic, given that Rainbow has been building humanoids since 2001. This is not a company that is starting from a clean sheet of paper. They have seven successive generations of bipedal humanoid experience, proprietary actuators and controllers that have been refined over two decades, and a controlled deployment environment—Samsung's own factories—where they can iterate rapidly without the risks of public-facing consumer products.

The financial trajectory, while still early, is encouraging. Revenue grew 76 percent in 2025 to 34 billion won, and the company maintains a pristine balance sheet with 81.5 billion won in cash and virtually zero debt. The cash position, boosted by Samsung's investments, gives Rainbow the runway to invest aggressively in R&D and manufacturing scale-up without the dilution or debt burden that typically constrains hardware startups.

Finally, there is an intangible factor that is difficult to quantify but should not be ignored: national strategic importance. South Korea views robotics as a critical technology for its economic future, alongside semiconductors and batteries. Rainbow Robotics, as the company that won the DARPA prize and is now backed by Samsung, occupies a unique position in this national strategy. Government R&D funding, favorable regulatory treatment, and defense contracts are all more likely to flow to a company that is seen as a national champion. This does not guarantee success, but it creates a structural tailwind that competitors in other countries may not enjoy.

IX. Epilogue: The Future of the Humanoid

In the spring of 2026, the trajectory of Rainbow Robotics feels both inevitable and precarious. Inevitable because the convergence of Samsung's capital, Rainbow's technology, and the global demand for automation is a powerful combination. Precarious because the valuation leaves no room for disappointment, and the competitive landscape is evolving at a pace that would have been unimaginable even three years ago.

The company's near-term roadmap is anchored by two milestones. First, the continued deployment of cobots and mobile manipulators in Samsung's facilities, which will generate the revenue growth needed to justify the current valuation. Second, the development of a next-generation humanoid robot targeted for commercial deployment by 2028, which will be the ultimate test of whether Rainbow's two decades of research can translate into a product that works reliably outside a controlled laboratory environment.

The deployment at Samsung Heavy Industries' Geoje Shipyard is particularly telling. Shipbuilding is one of the most physically demanding and dangerous industrial environments in the world—a far cry from the clean, controlled conditions of a semiconductor fab. If Rainbow's robots can operate effectively in a shipyard, they can operate almost anywhere. This deployment, if successful, would be the strongest possible proof point for the company's technology.

There is a broader question embedded in Rainbow's story that extends beyond any single company or stock. The question is whether the "deep tech" model—twenty years of patient university research, followed by commercialization through a dominant corporate partner—is a viable path for building enduring technology companies. The conventional Silicon Valley playbook says no: move fast, ship products, iterate based on customer feedback, and worry about deep technology later. But Rainbow's journey suggests an alternative model, one that is more common in Korea, Japan, and Germany than in the United States: build the technology first, achieve genuine technical superiority, and then find a partner with the scale and capital to take it to market.

Jun-Ho Oh spent twenty years in a KAIST laboratory building robots that could walk. Jung-Ho Lee spent fifteen years turning that research into products that factories would buy. Samsung spent three years methodically acquiring the option to deploy those products at global scale. Each of these timelines would be considered unacceptably long by Silicon Valley standards. But the result—a company with proprietary hardware, a captive customer with unlimited deployment potential, and a twenty-year head start on the competition—is the kind of competitive position that cannot be replicated by throwing money at the problem.

The question for investors is not whether Rainbow Robotics has built something extraordinary. They have. The question is whether the market has already priced in that extraordinary potential, and whether the execution challenges ahead—scaling production, navigating the Samsung relationship, and staying ahead of a rapidly evolving competitive landscape—are fully appreciated at a $9.5 billion valuation for a company that generated $23 million in revenue last year.

Rainbow Robotics proved that deep tech from a university lab can survive the Valley of Death. The next chapter will determine whether it can thrive on the other side.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube