China Life Insurance: The Story of China's Sovereign Financial Giant

I. Introduction & Episode Roadmap

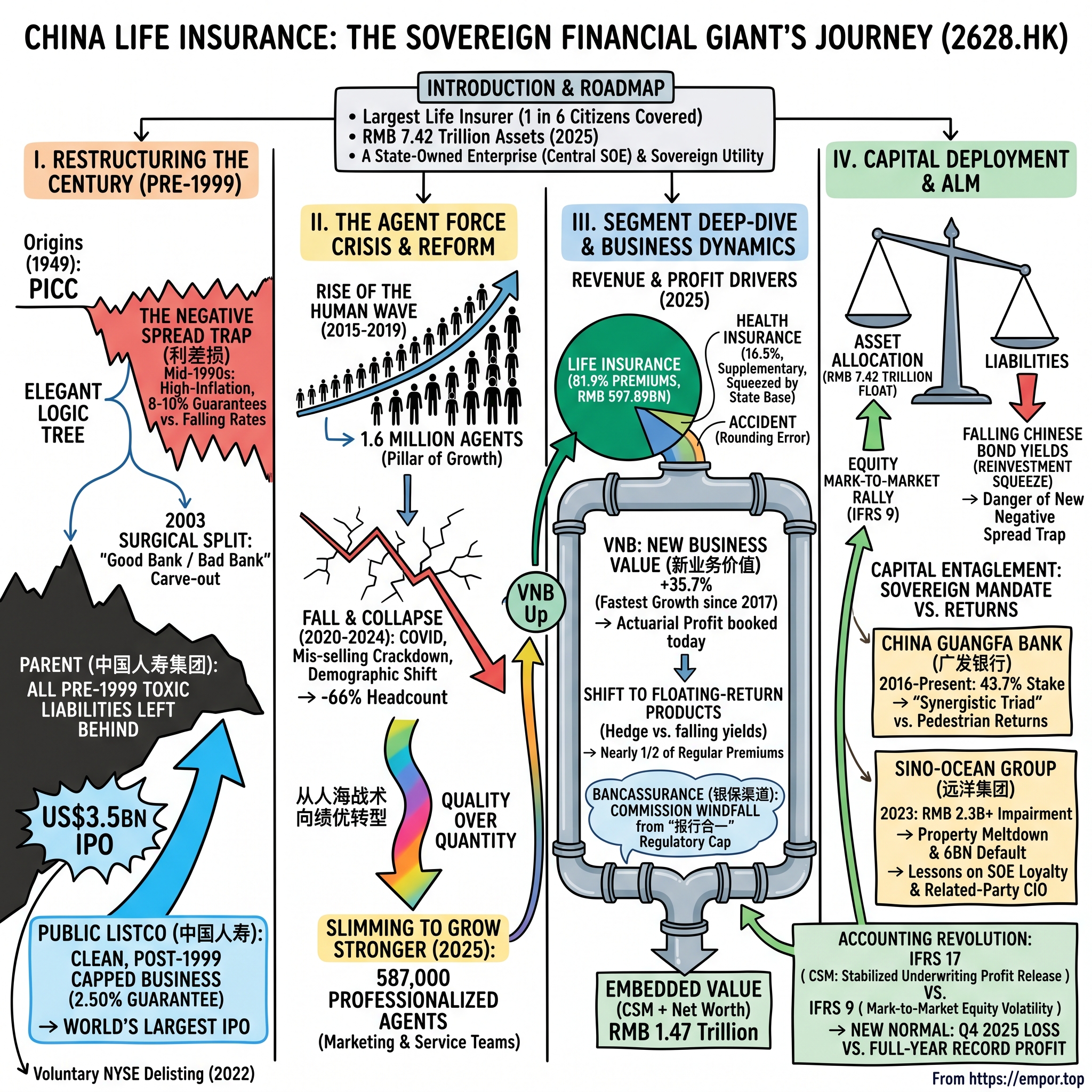

Picture the arithmetic for a moment. There is a single company in China that collects premiums from roughly one in six of the country's citizens, sits on an investment portfolio larger than the annual economic output of most nations on earth, and yet trades on the Hong Kong Stock Exchange at a fraction of the value of the future profits it has already booked. That company is 中国人寿保险股份有限公司 China Life Insurance Company Limited, listed in Hong Kong as 2628.HK and in Shanghai as 601628.SS. It is the largest life insurer in the People's Republic, and it is not really a private enterprise at all. It is a central State-Owned Enterprise — a sovereign financial utility wearing the costume of a listed insurance company.

The scale is genuinely difficult to hold in your head. In its 2025 financial year, China Life reported total premiums of RMB 729.89 billion, crossing RMB 700 billion for the first time in its history.12 Its total investment assets reached RMB 7.42 trillion, and its embedded value — the actuarial present value of profits already locked into policies on the books — stood at just under RMB 1.47 trillion.1 Net profit attributable to shareholders came in at a record RMB 154.08 billion, up 44.1% from RMB 106.94 billion the year before.12 For a sense of proportion: that single-year profit figure is larger than the entire market capitalisation of many companies people consider large.

And here is the central hook of this story. How does an institution charged with the retirement, health, and savings of hundreds of millions of people generate a record profit and, in the very same year, post a loss of more than RMB 13.7 billion in a single quarter?3 How does a company built on the most low-tech distribution engine imaginable — a foot army of insurance agents knocking on doors in provincial China — reinvent itself while that army shrinks by two-thirds? And how should a minority shareholder in Hong Kong think about owning a sliver of an enterprise whose ultimate boss is the Chinese state, and whose loyalties, when push comes to shove, may not be to them?

This is a story with four spines running through it. The first is the restructuring of the century: how a structurally insolvent state monolith used a "good bank / bad bank" split in 2003 to pull off the largest initial public offering in the world that year. The second is the agent force crisis: the rise and painful collapse of a distribution machine that once numbered in the millions. The third is capital allocation under a sovereign mandate: the story of a bank stake, 广发银行 China Guangfa Bank, and a property disaster, 远洋集团 Sino-Ocean Group. And the fourth is the accounting revolution — the arrival of IFRS 17 and IFRS 9, which rewired the company's reported earnings and tied them, for the first time, to the daily mood swings of the Chinese stock market.

Before we begin, it's worth puncturing the two consensus narratives that cling to this company, because both are half-truths. The first myth is that China Life is a straightforward "reopening" play on Chinese consumption — buy the biggest insurer, ride the growth of the middle class. The reality is far more textured: this is a mature, slow-growing, capital-intensive institution whose fortunes are dominated less by how many policies it sells and more by two forces largely outside its control, the level of Chinese interest rates and the direction of the domestic stock market. The second myth runs the opposite way — that China Life is simply a "value trap," a cheap stock that stays cheap because the state milks it for policy purposes. There is real truth in that, as we'll see, but it ignores that the company is genuinely well-capitalised, throws off a rising dividend, and sits on a demographic tailwind that few businesses on earth can match. The interesting version of China Life lives between those two myths, and getting there requires understanding how it was built. Let's start where the modern company was born: in the wreckage of a crisis that nearly sank the entire Chinese life insurance industry.

II. Pre-1999: The Negative Spread Trap & Restructuring of the Century

To understand why China Life exists in its peculiar present form, you have to go back to a boardroom problem so severe it required an act of state to solve. But first, the origins. The lineage traces to 1949, when the newly founded People's Republic established the People's Insurance Company of China — 中国人民保险公司 PICC — which absorbed the country's insurance interests and, after domestic insurance was suspended in 1959, effectively became a department of the central bank.5 Insurance in China went dark for two decades. It was only in the reform era that the business was revived, and in 1996 PICC was reorganised into a holding structure and split into three pieces: PICC Life, PICC Property, and PICC Reinsurance.5 The life arm was the direct ancestor of the company we are telling you about today.

Now to the crisis. In the mid-1990s, China was a high-inflation, high-interest-rate economy. Bank deposits paid double-digit yields, and to compete for household savings, insurers sold long-dated policies promising guaranteed returns — on the richest products, guarantees that ran as high as 8% to 10%, and on the company's own account as high as 6.5%.5 This is the oldest and most dangerous mistake in the insurance business: promising a fixed return for thirty years without knowing what you will be able to earn on the money. The Chinese term for the trap is elegant and ominous — 利差损, the negative spread loss, the gap between what you pay policyholders and what your assets earn.

The trap sprang shut with brutal speed. Between 1996 and 1999 the central bank slashed interest rates again and again — several cuts in 1996–97, several more through 1998–99 — as inflation collapsed and the economy cooled.5 Suddenly an insurer contractually obligated to pay 8% could reinvest maturing money only at 2%. Multiply that spread across billions of RMB of thirty-year liabilities and you get a structural hole in the balance sheet measured in the tens of billions. On June 10, 1999, the regulator drew a line in the sand and capped the guaranteed pricing rate on all new policies at 2.50%.5 But that only stopped the bleeding on new business. The old policies — the poisoned ones — were still there, and they would haunt the balance sheet for decades.

Here is where the financial engineering became genuinely elegant. If you wanted to raise international capital against China's rising middle class, no global investor would touch a company sitting on a multi-decade negative-spread bomb. So the State Council performed a surgical split. Every long- and medium-term policy issued before June 10, 1999 — the toxic, high-guarantee legacy — was left behind in the state parent, 中国人寿保险(集团)公司 China Life Insurance (Group) Company. Every clean policy issued on or after that date, capped at the new 2.5% ceiling, together with the premier nationwide branch network and brand, was transferred into a freshly incorporated joint-stock listco: China Life Insurance Company Limited.56 It was a good bank / bad bank carve-out a decade before that phrase entered the Western financial vocabulary during the 2008 crisis. The parent kept the garbage; the listco got the crown jewels.

The payoff came in December 2003. China Life listed simultaneously in Hong Kong and New York, its American Depositary Shares trading under the ticker "LFC" from December 17, and raised roughly US$3.5 billion including the over-allotment — the largest IPO anywhere in the world that year, eclipsing the runners-up.57 International investors, hungry for exposure to Chinese consumption and reassured by the absence of the negative-spread liability, oversubscribed the deal many times over. It was a triumph of structuring. But it also planted a seed that every minority shareholder should remember: the state had just demonstrated, in the most vivid way possible, that it could decide which assets and which liabilities belonged to public shareholders and which belonged to the parent. That power cuts both ways, as we'll see.

The New York chapter, notably, did not last. Nearly two decades later, in August 2022, China Life announced it would file a Form 25 with the U.S. Securities and Exchange Commission to voluntarily delist its ADSs from the New York Stock Exchange, with the last day of trading expected on or around September 1, 2022.23 The company's stated rationale was pragmatic: the trading volume of its ADSs was tiny relative to the worldwide volume of its Hong Kong H-shares, and maintaining the U.S. listing carried considerable administrative and compliance cost.23 It later moved to deregister entirely. The delisting was part of a broader retreat of Chinese state enterprises from U.S. exchanges amid escalating audit-oversight and geopolitical tensions between Washington and Beijing — a reminder that for a company this closely tied to the Chinese state, the listing venue itself is subject to forces well beyond ordinary corporate finance. Hong Kong, closer to home and beyond the reach of American securities regulators, became the center of gravity for the H-share investor base. For now, though, the newly cleaned-up company of 2003 had a growth engine to build — and it built it out of people.

III. The Core Engine: Rise, Fall, and Reform of the Agent "Great Wall"

If you had walked into a China Life recruitment meeting in 2015, you would have witnessed something closer to a revival tent than a corporate onboarding. Rows of hopeful recruits, many of them relatives and neighbours of existing agents, being told that anyone could sell insurance, that the product sold itself, that all you had to do was start with the people you knew. This was the engine that built modern China Life: the individual agent channel, 个险, a human wall of salespeople that blanketed the country down into Tier 3 and Tier 4 cities, county towns, and rural villages where no foreign insurer and no fintech app could economically reach.

The logic was pure scale. In a country the size of a continent, physical trust is distributed door to door. A farmer in Henan does not buy a thirty-year annuity from a slick app; he buys it from someone he knows, ideally someone the whole village knows works for the big state insurer. China Life turned this into an industrial machine. By 2019, at the peak of the "human wave" model, its individual agent force had swelled to something on the order of 1.6 million people — one of the largest private sales forces on the planet.8 The catch, which management downplayed for years, was that this was a high-volume, high-churn model. Recruit a huge cohort, have each new agent sell a policy or two to their immediate circle, and count on a fraction sticking around after the friends-and-family well ran dry.

Then the machine broke. Between 2020 and 2024, the entire Chinese life insurance industry watched its agent armies evaporate. The reasons stacked on top of one another: COVID lockdowns made face-to-face selling impossible, a more sophisticated urban consumer stopped buying from untrained relatives, the population itself began to age and shrink, and — crucially — regulators launched aggressive campaigns against mis-selling, the practice of dressing up savings products as something they weren't.9 S&P Global captured the mood of the period in the title of one research note: China Insurance: Change Is Painful.8 For China Life the contraction was staggering in scale. The individual agent headcount fell from its roughly 1.6-million peak to 615,000 by the end of 2024, and settled at 587,000 through 2025.14 Two out of every three agents were simply gone.

Now, a naïve reading of that number is catastrophe — the sales force collapsed. But watch what happened to the economics, because this is the heart of management's thesis. As the low-productivity agents washed out, the ones who remained were, by definition, the professionals. China Life reorganised the survivors into a 371,000-strong general marketing team and a 216,000-strong specialised service-and-collection team, the 收展队伍, which focuses on servicing and cross-selling to existing policyholders.1 And the value of what they sold went up, not down. This is the "slimming to grow stronger" argument — 从人海战术向绩优转型, from human-wave tactics to a high-performer transition — and the evidence for it lives in a single number that we will spend the next section unpacking: new business value.

To grasp why the old model was doomed, it helps to understand the perverse incentive at its core. Under the human-wave approach, an insurer earns handsomely on a new agent's first few sales — typically to that agent's own family and close friends — because first-year commissions and the associated new business are front-loaded. The company therefore had every reason to recruit relentlessly, churn through cohorts, and treat each new hire as a fresh pool of warm leads regardless of whether that person had any aptitude or intention to build a career. It was, in effect, a recruiting machine dressed as a sales force. When the supply of naïve recruits and untapped family networks finally ran dry — accelerated by demographics, urbanization, and a public that had grown wise to the pitch — the whole model lost its fuel. This was not a China Life-specific stumble; it was an industry-wide reckoning that McKinsey and others had been warning about for years, arguing that the agency channel had to be rebuilt around professionalism, training, and productivity rather than sheer numbers.9

The honest analytical read is that management is largely winning this argument, but the win deserves scrutiny rather than applause. A shrinking headcount that produces rising value per agent is genuinely a healthier business than a bloated one selling low-margin junk. But some of the recent productivity surge also reflects a product mix shift and a favourable regulatory tailwind that lowered costs across the whole industry — tailwinds China Life did not create. There is also a survivorship question hiding in the data: when you cut a sales force by two-thirds, per-capita productivity mechanically rises simply because the least productive people are the ones who left, not necessarily because the survivors got better at their jobs. Disentangling genuine skill improvement from pure composition effect is nearly impossible from the outside. The durable question, which no single year answers, is whether 587,000 agents is a stable floor or a way station to something smaller still, and whether the professionalized core can keep growing value once the easy gains from purging deadweight are exhausted. For now, the force has stopped shrinking, and the numbers it produces are the best evidence we have. Let's size them.

IV. Segment Deep-Dive: Sizing the Revenue, Profit, and Value Drivers

Every insurance company is really two businesses stapled together: an underwriting business that collects premiums and promises to pay claims, and an investment business that manages the float in between. China Life's underwriting mix is dominated, overwhelmingly, by one line. Of the RMB 729.89 billion in 2025 gross premiums, life insurance — the long-term savings, annuity, and endowment contracts that are the company's reason for being — generated RMB 597.89 billion, or 81.9% of the total, and it grew 11.0% year on year.1 This is where the profit and the long-duration liabilities both live.

The second line, health insurance, contributed RMB 120.22 billion, about 16.5% of premiums, but it is a structurally harder business.1 Chinese commercial health insurance competes against a vast, state-backed basic medical insurance system that covers most of the population, so private insurers are squeezed into the supplementary layer — critical illness cover, higher-end reimbursement — where margins are thinner and competition fiercer. Worth noting is that this segment barely grew in 2025, edging up from RMB 119.14 billion the year before, a near-flat performance that quietly underscores the ceiling on commercial health cover in a country where the state provides the base layer.1 The proliferation of cheap, government-endorsed city-level supplementary schemes — the so-called 惠民保 huimin bao products sold for a few dozen yuan a year — has further commoditised the entry-level end of the market, leaving traditional insurers to compete on service and higher-end coverage rather than price. The strategic read is that health is a business China Life must be in for completeness and cross-sell, but it is not where the value is created. The third line, accident insurance, at RMB 11.77 billion and 1.6% of premiums, is a rounding error to the investment case; it actually shrank year on year, and we mention it and move on.1

But premiums are a vanity metric in life insurance, and here is why. When you sell a thirty-year annuity, the cash arrives over decades, and whether the policy is profitable depends entirely on its pricing, its costs, and how long the customer keeps paying. So the metric that actually matters — the one every serious insurance analyst watches first — is the value of new business, 新业务价值 or VNB: the actuarial present value of all future profit from the policies sold this year. It is the closest thing an insurer has to same-store sales growth. In 2025, China Life's VNB grew 35.7% to RMB 45.75 billion, its fastest growth since 2017.12 That is the single most important number in this section, because it validates the entire "quality over quantity" gamble: fewer agents, selling higher-margin regular-premium long-term contracts instead of cheap single-premium savings products, generating far more value per policy.

What does that surge actually mean, stripped of the cheerleading? It means the product restructuring is real and it is working, but it also means you should watch for how much of the gain is repeatable. Part of the VNB jump came from selling more protection-and-long-term-savings business and less low-value single-premium volume — that is durable. Part came from a regulatory change that mechanically lowered the industry's customer-acquisition costs. That change is worth understanding on its own, because it quietly rewrote the economics of Chinese insurance distribution.

There is one more product shift buried in the 2025 results that deserves a spotlight, because it is arguably the most strategically important thing the company did all year. China Life pushed hard into what it calls floating-return business, and by year-end that category accounted for nearly half of its first-year regular premiums.2 Decode the jargon and this is a quiet revolution in who bears the risk. A traditional policy hands the customer a fixed guaranteed return, which means the insurer eats the entire burden of finding assets that beat that guarantee — the exact mechanism that created the 1990s negative-spread disaster. A floating-return or participating product, by contrast, shares the investment outcome with the policyholder: when returns are good, the customer participates in the upside; when they are poor, the customer absorbs part of the shortfall. In an era of relentlessly falling bond yields, shifting the product mix toward floating returns is the single most effective defense management has against a repeat of 利差损. It lowers the guaranteed liability the company must out-earn, and it is no accident that this push accelerated precisely as long-term Chinese yields kept sinking. Whether customers keep buying products that offer them less certainty, and whether the shift is fast enough to outrun the yield decline, are open questions — but the direction of travel is exactly what a prudent actuary would order.

The first-year regular premium figure itself — RMB 116.2 billion — matters because "regular premium" means the customer commits to paying every year for years or decades, versus a single lump sum.1 Regular-premium business is worth far more to an insurer: it locks in recurring cash flow, it embeds higher lifetime value, and it is the raw material from which VNB is manufactured. The steady tilt from single-premium volume toward first-year regular premium is the unglamorous plumbing behind the headline VNB growth, and it is the kind of mix improvement that compounds quietly for years rather than flattering a single reporting period.

For years, the 银保渠道 bancassurance channel — selling insurance through bank branches — was a nightmare of hidden costs. Insurers desperate for volume paid banks fat under-the-table commissions to push their products, and the banks, holding the customer relationship, extracted the lion's share of the economics. Then the regulator, the 国家金融监督管理总局 National Financial Regulatory Administration (NFRA), imposed a policy called 报行合一 — literally "integration of reporting and execution" — first issued in August 2023.10 The rule was deceptively simple: the commission you actually pay must match the commission you filed with the regulator. No more secret side payments. Fitch estimated the change cut the industry's average bancassurance commission rate by roughly 30%.11 For a giant like China Life, with the scale to command bank shelf space regardless, this was a windfall: acquisition costs fell, the banks lost their pricing leverage, and VNB margins across the bancassurance book structurally widened. Embedded value, meanwhile, climbed to RMB 1.467 trillion by the end of 2025, from RMB 1.401 trillion a year earlier — the compounding reservoir of profit already earned but not yet released.1 Now, that reservoir has to be invested somewhere. And that is where the story gets complicated.

V. Capital Deployment: The Guangfa Bank Triad and the Real Estate Debt Trap

Managing RMB 7.42 trillion is not a portfolio problem; it is a sovereign-scale asset-allocation problem, and it is conducted under strict asset-liability management rules in a macro environment where safe yields keep falling.1 The temptation for any insurer sitting on that much money is to reach for yield — to buy something that pays more than a government bond. China Life made two famous reaches in the last decade. One was a bank. The other was a property developer. Together they are a near-perfect case study in what happens when a sovereign insurer's capital allocation gets entangled with the state's broader agenda.

Start with the bank. In 2016, China Life deployed RMB 23.31 billion — about US$3.58 billion — to buy out the stakes that Citigroup and IBM Credit held in 广发银行 China Guangfa Bank, a national commercial lender.12 The agreements were signed on February 29, 2016 and completed that August, lifting China Life's holding to 43.686% and making it CGB's single largest shareholder.1213 The strategic pitch was the "synergistic triad": China Life would own a bank, cross-sell insurance to the bank's credit-card and deposit customers, and lock in a captive bancassurance funnel. On paper, a vertically integrated financial powerhouse.

In practice, the deal illustrates the difference between strategic logic and shareholder returns. A 43.686% stake is large enough to consolidate capital demands and reputational risk, but it is a minority position that does not give full operational control, and a mid-sized Chinese commercial bank is precisely the kind of asset that has struggled through the era of compressing net interest margins and rising capital-adequacy requirements. The bancassurance funnel is real, but the capital it ties up has, on the available evidence, delivered returns that look pedestrian next to what the same capital might have earned deployed straight into the core insurance franchise. This is an analytical judgement rather than a figure China Life breaks out — the company does not publish a clean standalone return on its CGB investment — but the pattern of a capital-heavy bank stake dragging on a group's blended returns is a familiar one.

There is a deeper strategic critique here too, one that value investors call "diworsification." The valuation at the time — roughly one times book value, in line with historical Chinese bank deals — was not obviously excessive, so this was not a case of wild overpayment.12 The problem is conceptual: an insurer's core skill is pricing and managing long-duration liabilities and matching them with assets, while a commercial bank's core skill is credit underwriting and deposit gathering. These are different businesses with different risk profiles, and stapling them together in pursuit of "synergy" often produces a conglomerate that trades at a discount to the sum of its parts rather than a premium. The cross-selling dream — turning CGB's card and deposit customers into China Life policyholders — is the kind of synergy that is easy to pitch and hard to prove, and China Life has never disclosed hard numbers demonstrating that the funnel generates value exceeding the capital cost of owning nearly half a bank. A skeptic would file CGB under "empire-building that a state conglomerate can afford but a return-focused allocator might not have chosen."

The second reach was far more painful. China Life became the largest shareholder of 远洋集团 Sino-Ocean Group (3377.HK), holding roughly 29.59% of a developer it evidently regarded as a safe, state-adjacent, asset-backed source of long-term yield.1415 For a while the logic held: property developers threw off high returns, and a state-linked one seemed to carry an implicit backstop. Then China's property sector imploded. Sino-Ocean swung to a net loss of RMB 15.9 billion in 2022, with its auditor openly questioning its ability to continue as a going concern, and the losses widened further into 2023.14 It defaulted on roughly US$6 billion of offshore debt and entered a grinding multi-year restructuring.16 In a landmark moment, an English court sanctioned Sino-Ocean's restructuring plan on February 3, 2025 using a cross-class cramdown — forcing dissenting creditors to accept the deal — with the parallel Hong Kong scheme sanctioned weeks later; it was the first mainland Chinese developer to restructure through the English courts.16

For China Life shareholders, the cost showed up as a gaping hole in investment income. The company does not ring-fence a precise "Sino-Ocean impairment" line, but the direction is unmistakable: for the first nine months of 2023, China Life's investment income collapsed to RMB 22.58 billion, from RMB 156.92 billion a year earlier, with impairment losses accounting for the majority of the damage.17 This is the episode that should give every minority investor pause. A profit-maximising insurer would likely have exited or written down a distressed developer far faster; a sovereign insurer, whose CIO once sat on that developer's board (more on that shortly), was arguably slower to cut, and became entangled in a rescue that served a broader policy goal of stabilising the property sector.

Put the two case studies side by side and a single pattern emerges. Both the bank stake and the property stake were large, illiquid, capital-heavy positions in exactly the kinds of assets a Chinese state financial giant is expected to support — a national commercial bank and a state-adjacent property developer. Both were defensible on paper at the time of purchase. And both ended up tying capital into low- or negative-return outcomes that a purely return-driven allocator might have avoided or exited sooner. This is the connective tissue of the whole China Life investment case: the company's scale and sovereign backing are simultaneously its greatest asset and the source of its most expensive mistakes, because the same institution that enjoys the state's implicit support is also expected to answer the state's implicit calls. The lesson is stark: when the state needs someone to absorb economic stress, a central SOE with RMB 7 trillion of assets is a very convenient balance sheet. Which raises the obvious question — who, exactly, is running this balance sheet, and whom do they answer to?

VI. Technocratic Leadership & Corporate Governance: The Cai Xiliang & Li Mingguang Era

There is a revealing ritual in Chinese state finance: the leadership reshuffle. Senior executives at the largest SOEs are not recruited by headhunters or elevated by founders; they are rotated in by the organization department of the state, often arriving from a different corner of the financial system entirely, and they can be moved on with equal suddenness. To read China Life's C-suite is therefore to read a map of the Chinese state's priorities, and the map redrew itself sharply in 2023 and 2024, right as the company hit its most turbulent stretch since the IPO.

The people who run China Life are not entrepreneurs, founders, or celebrity CEOs. They are senior technocrats rotated through the upper reaches of the Chinese state financial apparatus, and understanding what motivates them is essential to understanding the stock. The current leadership took the helm during the most turbulent stretch the company has faced since its IPO — the agent collapse, the property crisis, and the accounting overhaul all at once. What is telling about the specific individuals chosen is that they map almost perfectly onto the three crises: a Chairman schooled in cross-asset investment for the portfolio problem, a career actuary as CEO for the liability problem, and an investment chief steeped in the property world for the real-estate cleanup. Whether by design or coincidence, the bench was assembled for exactly the fights the company now has on its hands.

At the top sits Chairman 蔡希良 Cai Xiliang, born in 1966, a master's graduate in economics from the Shanghai University of Finance and Economics.18 His résumé is a tour of the commanding heights of Chinese state finance. From 2016 to 2022 he was a member of the Party Committee and Deputy General Manager of 中信集团 CITIC Group, one of China's largest state conglomerates, while simultaneously serving as Vice Chairman and General Manager of 中国信保 SINOSURE, the state export-credit insurer.18 He became Party Secretary of the China Life Group in August 2024, and was formally elected Chairman of the listco's board on October 30, 2024, with his term commencing December 4, 2024 pending regulatory approval.19 His CITIC background matters: it brings a sophisticated, cross-asset investment sensibility to a company whose central challenge is investing a sovereign-scale portfolio. On the 2025 results, Cai declared the company had achieved a "full harvest" with "stronger growth momentum" — the kind of triumphant framing that is worth reading against the volatility lurking underneath the headline profit.2

If Cai is the strategist, the President and CEO, 利明光 Li Mingguang, is the technician. Appointed President effective August 4, 2023, Li is an actuary to his core.20 He joined China Life in 1996 — meaning he has spent essentially his entire career inside the company — and is a fellow of both the China Association of Actuaries and the UK's Institute and Faculty of Actuaries.20 (For the record, and contrary to some circulating summaries, his degrees are in computer science from Shanghai Jiao Tong University and a master's from the Central University of Finance and Economics, capped by a Tsinghua EMBA, and he rose to Chief Actuary around 2012, not earlier.) His decades of underwriting and actuarial discipline are exactly what you want continuity on when the core question is whether long-term liabilities are priced to survive falling yields. Notably, it was Li — not the Chairman — who fronted the awkward part of the 2025 results, explaining the Q4 loss as the direct consequence of a capital-market "structural adjustment" hitting the company's stock and fund holdings.3

The third figure worth knowing is the Chief Investment Officer, 刘晖 Liu Hui, born in February 1970, appointed CIO in December 2023.21 Her background is the tell. From 2014 to 2022 she was concurrently an Executive Director and Vice President of Sino-Ocean Group, President and Chairman of China Life Capital Investment, and General Manager of China Life Real Estate.21 In other words, the executive now charged with cleaning up and reallocating the portfolio was, until recently, on the board of the very property developer that inflicted the biggest impairment. Whether you read that as deep domain expertise or as an uncomfortable conflict is a matter of judgement, but a skeptical investor should note it.

Here is the governance crux, and it is genuinely different from a Western insurer. As a central SOE, China Life's top executives hold no personal shareholding in the company and receive no stock options; the HKEX filings explicitly confirm that the Chairman receives no director's fee or remuneration from the listco and that directors hold no interests in its shares.1821 So what drives them? Not share-price appreciation. They are measured on state-directed mandates: maintaining solvency under the 中国二代偿付能力监管规则 C-ROSS Phase II regime, growing VNB, ensuring social stability, and — always — regulatory compliance. On the credibility ledger, this management deserves some genuine marks: it addressed the Sino-Ocean damage without hiding it, avoided throwing further capital into the sinking asset, and executed the agent stabilisation it promised. But the incentive structure means that when minority-shareholder returns collide with a state objective, no one at the top has a personal financial reason to fight for the minority. Keep that in mind as we turn to the machinery that now governs how all of this shows up in the reported numbers.

VII. The Accounting Revolution: Demystifying IFRS 17 & IFRS 9 Volatility

In January 2023, Chinese insurers walked through an accounting doorway from which there is no return, adopting two new global standards simultaneously: IFRS 17 for insurance contracts and IFRS 9 for financial instruments.22 Investors who ignore this as mere bookkeeping will badly misread China Life's earnings, because these standards fundamentally changed what "profit" even means for the company.

Start with IFRS 9, because it is the source of the drama. The old world let an insurer hold a portfolio of stocks and recognise gains only when it chose to sell, smoothing results across good years and bad. The new world forces a large share of equity and fund holdings into a bucket called Fair Value Through Profit or Loss — FVTPL — where every tick of the market flows straight into the income statement, realised or not. Think of it as marking your entire stock portfolio to market every quarter and running the result through your net profit. In the first half of 2025, an estimated 77.4% of China Life's stock holdings sat in this FVTPL bucket.3 That is a colossal amount of equity exposure wired directly into reported earnings.

This single mechanism explains the paradox we opened with. When the A-share market rallied hard from late 2024 through much of 2025, those unrealised gains poured into the P&L, and total investment income surged 25.8% to RMB 387.69 billion, with the gross investment yield jumping 59 basis points to 6.09% — driving that record RMB 154.08 billion net profit.13 It was not, for the most part, an underwriting triumph. It was a stock-market rally showing up on an insurer's income statement. And what the market gives, the market takes away: in the fourth quarter of 2025, Chinese equities corrected, some indices sharply, and China Life swung from RMB 167.8 billion of cumulative profit through nine months to a RMB 13.73 billion loss in the final quarter alone.3 Same company, same portfolio, opposite sign — purely because of where the market closed on December 31. This volatility is the new normal, and it makes quarter-to-quarter earnings a poor guide to the underlying business. It also complicates management's ability to give clean guidance, because a huge swing factor is literally outside its control.

If IFRS 9 injects volatility, IFRS 17 tries to impose discipline, through a concept worth learning: the Contractual Service Margin, or CSM. When China Life sells a profitable long-term policy, IFRS 17 does not let it book the profit up front. Instead the expected profit is parked in the CSM — think of it as an "unearned profit reserve" — and released gradually into earnings over the decades the company actually provides coverage.22 The elegance is that this shields reported underwriting profit from short-term swings in premium volume: a bad sales year does not crater earnings, because the profit engine is the slow release of a reservoir built over many prior years. The CSM is, in effect, a truer picture of the durable value of the underwriting book than premiums or one year's profit could ever be.

There is a subtlety here that separates the insurers who understand IFRS 17 from the ones who merely comply with it. Because the CSM is the store of future profit, the single most important thing an insurer can do is grow it — and the way to grow it is to write high-VNB new business, since a profitable new policy adds to the reservoir while an unprofitable one does not. This is why VNB and CSM are two views of the same underlying truth: VNB is the profit added to the tank this year, and the CSM is the tank's total level. It also means that the switch away from low-margin single-premium products toward high-margin regular-premium and protection business, described earlier, is not just a sales-mix story — it is directly the mechanism by which China Life refills its long-term profit reserve. A company that grew premiums while shrinking its CSM would be liquidating its future; one that grows both is genuinely building value. The uncomfortable irony of the dual transition is that IFRS 17 stabilised the underwriting line just as IFRS 9 destabilised the investment line — leaving China Life with reported earnings arguably more volatile overall than before, even as the underlying economics became more transparent to anyone willing to look past the headline number. For long-term investors, the practical takeaway is to anchor on VNB, embedded value, and the CSM balance, and to treat any single quarter's net profit with deep suspicion. Beyond the core insurance-and-investment machine, though, China Life has been quietly building adjacencies — and it's worth asking whether they matter.

VIII. Strategic Ecosystems: Hidden Value or Core Support?

Walk into one of China Life's 国寿嘉园 retirement communities and you are not looking at a real-estate flip. You are looking at a customer-retention device dressed as a building. This is the most important thing to understand about the company's senior-care push under the 国寿大养老 banner: unlike the property developers it invested in and got burned by, these assets are not built to be sold. They are built to be lived in — by the company's own policyholders.

The value mechanism is a closed loop, and it is genuinely clever. A high-net-worth customer signs a large, multi-decade pension annuity, and in return is promised a guaranteed place in a premium China Life retirement facility. The insurance product and the physical service reinforce each other: the annuity funds the retirement, and the retirement locks in the annuity. It raises switching costs — you are not going to surrender a policy that comes with your future home attached — and it deepens the relationship with exactly the affluent, long-duration customers an insurer most wants. In an aging society, owning both the financial product and the physical care infrastructure is a structural advantage that a pure product-seller cannot easily replicate. The honest caveat is that these communities are capital-intensive and slow to scale, and China Life does not disclose them as a material standalone profit centre; their value today is strategic and prospective rather than a needle-mover on the P&L.

The demographic backdrop is what makes this bet rational rather than vain. China's population has begun to shrink and to age with startling speed; the cohort entering retirement over the next two decades is enormous, and the state pension system alone cannot carry the load. That is simultaneously the great opportunity and the great risk for China Life — opportunity because it creates structural demand for exactly the annuity, health, and elder-care products the company sells, and risk because longer lifespans mean the company must pay those annuities for longer than it might have priced for, the actuarial hazard known as longevity risk. Owning the retirement communities is, in part, a hedge and a differentiator in that landscape: it converts an abstract financial promise into a tangible, emotionally resonant benefit — a specific apartment in a specific building where a customer will actually spend their final decades. It is worth being clear-eyed, though, that senior-care real estate is a notoriously difficult business globally, with long payback periods, heavy operating costs, and thin margins. China Life is betting that the strategic value — customer acquisition, retention, and the premium annuity sales the communities anchor — outweighs the modest standalone economics of running the facilities. That is a defensible bet, but it is a bet, not a proven profit engine, and investors should size it as optionality rather than as a core earnings driver.

The other adjacency is technology, marketed as "Digital China Life": AI-assisted claims processing, automated underwriting, and digital servicing tools. It is important to size this correctly and not get carried away. China Life is not trying to monetise a tech platform or spin out a fintech unicorn. The purpose is narrow and defensive — drive down the expense ratio, speed up claims, and support the leaner agent force with better tools. It is an operational cost-saver, appropriately sized as a supporting act rather than a growth story in its own right. With the adjacencies in proportion, we can step back and ask the question that ultimately decides the investment case: what, if anything, actually protects this business from competition?

IX. Playbook & The Competitive Moat: Porter's 5 Forces & Hamilton Helmer's 7 Powers

Let's war-game this. Imagine you are 平安人寿 Ping An Life, China's formidable private-sector insurer, or 太保寿险 CPIC, and you want to take share from China Life. Where do you attack? Running the company through Hamilton Helmer's 7 Powers framework reveals why that attack is harder than it looks — and where the moat is thinner than the bulls claim.

The first genuine power is scale economies in distribution. China Life's physical branch and agent network reaches into remote towns, counties, and rural regions where the cost of acquiring each customer is low precisely because the infrastructure is already sunk and already national. A private competitor trying to replicate that rural footprint would have to spend enormous sums to serve customers who each generate modest premiums — the economics simply do not work at China Life's cost base. This is a real, durable advantage in the Tier 3 / Tier 4 / rural segment, even as it matters less in the affluent coastal cities where Ping An competes hardest with technology and brand.

The second, and arguably the deepest, power is branding built on sovereign trust. This is subtle, so it's worth dwelling on. A thirty-year insurance policy is a promise, and a promise is only worth the credibility of the institution making it. In a market that has lived through wealth-management-product defaults, shadow-banking scares, and a property collapse, ordinary Chinese savers place an enormous premium on safety. As the flagship central-state-owned insurer, China Life carries an implicit sovereign association — the sense, rightly or wrongly, that the state stands behind it — that no private or foreign insurer can manufacture. When a farmer or a retiree is choosing where to park thirty years of savings, that perception of a state backstop is worth more than a slightly higher illustrated return. The third power, switching costs, is common to the whole industry: long-term policies carry steep surrender penalties, locking in capital and customers for decades.

It is worth pausing on the head-to-head with 平安人寿 Ping An Life, because the contrast sharpens what China Life is and is not. Ping An, the crown jewel of privately controlled 中国平安 Ping An Group, has spent a decade and enormous sums building a technology-and-ecosystem model — health platforms, an army of digitally-enabled agents, and a data-driven approach to a wealthier, more urban customer. Ping An generally runs a leaner, higher-productivity agent force and has historically commanded richer new-business margins and a higher return on equity than China Life, and the market has rewarded it with a higher valuation multiple. Where China Life wins is breadth and trust: it reaches the rural and lower-tier hinterland Ping An finds uneconomic, and its state pedigree resonates most powerfully with exactly the risk-averse, safety-first saver. The honest framing is that these two are not really fighting over the same customer at the same moment — Ping An optimizes for the affluent coastal upgrader, China Life for the mass-market saver who wants the biggest, safest name in the country. China Life is the Costco of Chinese insurance: enormous scale, thin-margin trust, and a defensive position that is hard to dislodge but structurally lower-return than a premium specialist. (Precise side-by-side unit economics are not something China Life discloses in a form clean enough to compare line-for-line, so treat the productivity and margin comparison as directional rather than exact.)

Now Porter's 5 Forces, which sharpen where the pressure comes from. The bargaining power of buyers is low to medium — customers are price-conscious, but for multi-decade contracts, reliability outweighs a few basis points of yield, which is why the brand power above translates into pricing resilience. The most interesting shift is in the bargaining power of intermediaries, specifically banks. Historically the banks held enormous leverage, extracting fat commissions to sell insurance through their branches. The regulator's 报行合一 rule, described earlier, broke that leverage almost overnight, handing pricing power back to insurers and structurally widening margins — a rare case of a regulation strengthening the incumbents' moat rather than eroding it. Rivalry among the big insurers is intense but disciplined, new entrants face prohibitive capital and licensing barriers, and substitutes — bank deposits, wealth products, government pension schemes — compete for the same savings but lack insurance's tax treatment and guarantees.

So what is the honest verdict on the moat? It is real, and it is strongest exactly where it is least glamorous: rural scale and sovereign-trust branding. But it is not the moat of a high-return compounder. Scale in low-premium rural markets is a defensive advantage, not a profit geyser, and sovereign trust is inseparable from sovereign obligation. The same state association that wins the customer's trust also means the state can direct the company's capital. That duality is the pivot from the bull case to the risks, and it is where a skeptical investor earns their keep.

X. Risk Radar & The Skeptical Investor Stress Test

There is one risk that towers over all the others for China Life, and it is not the stock market or the property crisis. It is the slow, grinding descent of Chinese long-term interest rates. This is the ghost of 1999 threatening to return, and it deserves to be understood clearly.

Here is the mechanism, in plain terms. China Life sells policies with guaranteed minimum returns — even at today's lower caps, it has promised policyholders a floor. It then has to invest RMB 7.42 trillion, plus the torrent of new premiums arriving every year, in assets that earn more than those guarantees.1 As long as long-term government bond yields comfortably exceed the guaranteed rates, the spread is positive and the company earns its margin. But Chinese ten-year and thirty-year government bond yields have been falling for years, and every time a bond matures, the proceeds must be reinvested at the new, lower rate. If yields keep sliding toward the guaranteed floor, the spread compresses toward zero — and if they fall through it, China Life faces a fresh, modern version of the 利差损 negative-spread trap on its new book of business. This is not a tail risk; it is the central actuarial challenge of the entire Chinese life industry, and it is the reason the regulator keeps cutting the maximum guaranteed pricing rate. Asset-liability management — matching the duration of a thirty-year promise with assets that actually pay for it — is the whole game, and it gets harder every year yields fall.

There is a second, sneakier layer to the problem called duration mismatch, and it is worth making concrete. China Life's liabilities — thirty-year annuities and endowments — are extremely long-duration. But the Chinese bond market has historically offered relatively few genuinely long-dated, high-quality assets to match them, which means the company's asset duration has typically fallen short of its liability duration. In a falling-rate world, that gap is toxic: the liabilities are locked in at their guaranteed cost, but the assets keep rolling over into lower-yielding replacements faster than the liabilities reprice. The 6.09% gross investment yield reported for 2025 looks comfortably above any guaranteed liability cost, but remember how much of that yield came from a one-off equity rally flowing through FVTPL rather than from durable bond coupons.13 Strip out the volatile mark-to-market equity gains and the underlying fixed-income engine is where the reinvestment squeeze actually bites. This is precisely why the pivot to floating-return products and the regulator's repeated cuts to guaranteed rates matter so much: they are the two levers — one commercial, one regulatory — being pulled in tandem to keep the guaranteed cost of liabilities descending in step with asset yields. If asset yields fall faster than the industry can reprice its liabilities and re-mix its products, the spread inverts, and no amount of sales growth fixes a business that loses money on every new policy. That is the nightmare scenario, and it is the single most important thing to model for any long-term owner of this stock.

The second material risk we have already met: IFRS 9 earnings volatility. Because reported profit now rides the stock market, a bad year for Chinese equities can turn a record profit into a loss, complicating guidance and unnerving investors who mistake accounting noise for business deterioration. Management can explain it, but it cannot control it.

Now the stress test that a skeptical long-short investor or activist would run — and here we confront the elephant in the valuation. China Life has historically traded at a deep discount to its embedded value, often at a fraction of the value of profits it has already booked. Why? Part of the answer is the volatility and the interest-rate overhang above. But the larger part is what we might call the SOE discount, and it is rational. A minority shareholder in China Life must accept that the company's ultimate controller is the Chinese state, and that when a policy objective and shareholder returns diverge, the state's agenda comes first. The evidence is not hypothetical: the willingness to buy low-yield local-government and infrastructure bonds to fund national priorities, the capital tied up in China Guangfa Bank, and above all the entanglement in the Sino-Ocean rescue all point to a balance sheet that can be directed to absorb national economic stress. An activist could rightly challenge the portfolio complexity, the related-party proximity of the CIO to the impaired developer, the capital-heavy bank stake, and the absence of management skin in the game. There is no realistic path to "unlocking value" by pressuring this board, because the board does not answer to minority holders. The discount, in other words, is not a mispricing waiting to be corrected; it is the market pricing the reality of who is in charge. That sober framing sets up the balanced case.

XI. The Balanced Investment Spine: Bull vs. Bear Case & KPIs

So why might China Life win from here, and what could break it? Let's take both sides seriously, because a company this size rewards neither cheerleading nor reflexive cynicism.

The bull case rests on three pillars. First, demographics: China is aging fast, the state pension system is visibly strained, and there is a historic, multi-decade tailwind behind private commercial pension, annuity, and health products — precisely China Life's core. As the population grays, demand for exactly what this company sells should structurally rise. Second, the regulatory moat: 报行合一 and the capital demands of C-ROSS Phase II squeeze weaker, under-capitalised private insurers, and a well-capitalised sovereign giant is positioned to absorb the share they cede, at structurally higher margins than before. Third, the agency stabilisation: the headcount collapse appears to have bottomed, and the professionalised force is delivering that 35.7% VNB growth — evidence, not just narrative, that the quality transition is producing value.1 Layer on a solvency position that looks robust — a comprehensive solvency ratio of 174.01% and a core ratio of 128.77% at the end of 2025, both comfortably above regulatory minimums — and a dividend the company raised to a total RMB 8.56 per 10 shares, up 31.7% in aggregate payout, and you have a case for a well-capitalised, cash-generative, dividend-paying franchise riding a demographic wave.1

The bear case is equally coherent. The low-yield trap is the existential threat: if Chinese rates stay depressed or fall further, the asset-liability mismatch grinds down the spread and erodes embedded value from underneath, no matter how well the agents sell. The burden of the state is the second pillar: continued exposure to directed capital deployment — into infrastructure, banks, and distressed rescues — dilutes returns on equity and caps the multiple the market will pay. And the earnings volatility means the reported profit can lurch violently, making the stock a rough ride even if the underlying franchise is sound. The bear does not need China Life to fail; the bear only needs it to remain a low-return sovereign utility that the market keeps valuing at a discount, which is exactly what it has been.

The synthesis that an honest analyst reaches is that the bull and bear cases are not really in conflict — they describe the same company at different time horizons and through different lenses. Over the next few years, the demographic tailwind and the regulatory margin boost are real and should support VNB and embedded value; over the long arc, the interest-rate trap and the sovereign-mandate drag are equally real and cap how much of that value ever compounds into shareholder returns. This is why the reported 27.81% return on equity for 2025 must be read with care: it was inflated by the equity rally flowing through the income statement and is not a normalised, repeatable figure.1 The durable return on equity of this business is far more modest, and pretending otherwise — in either direction — is the mistake. The company is neither the growth story the bulls occasionally spin nor the terminal value trap the bears assume; it is a large, defensive, dividend-paying financial utility whose intrinsic value grows steadily but whose market value will lurch with rates and equities. An activist hoping to force a re-rating would find no lever to pull, because the controlling shareholder is the state and the state is not for turning. The rational posture, then, is to judge the company on the slow-moving fundamentals rather than the noisy price — which points directly to the metrics that matter.

Which brings us to what actually matters to track. Forget the noisy quarterly net profit. Three KPIs tell the real story. First, VNB growth and VNB margin — the truest read on whether the company is selling profitable new business or just volume. Second, the solvency ratios, core and comprehensive, under C-ROSS Phase II — the measure of capital adequacy and the constraint on both growth and dividends. Third, and most fundamental, the gross investment yield measured against the average guaranteed cost of liabilities — the investment spread, which is the entire economic engine and the early-warning system for any return of the negative-spread trap. Watch those three and you understand China Life; watch the headline profit and you understand mostly the stock market. That distinction is the crux of the final lesson.

XII. Outro & Lessons for Long-Term Investors

Strip away the trillion-RMB figures and the accounting machinery, and China Life resolves into a single, clarifying idea: it is a sovereign utility disguised as an insurance company. It is not a nimble, high-return compounder in the mold of a great private financial franchise, and pretending otherwise leads investors astray. It is the state's chosen instrument for managing the savings, retirement, and health protection of a vast population — an institution whose scale and trust are genuine competitive powers, and whose ownership is a genuine constraint on how much of that value ever reaches a minority shareholder.

That framing resolves the paradox we opened with — record profit and a quarterly loss in the same twelve months. Both are true, and neither is the point. The record profit was mostly a stock-market rally passing through a newly transparent income statement; the quarterly loss was that same rally reversing. The real business underneath moved far less than either number suggests, which is precisely why the disciplined investor learns to look past the reported net profit to the slow-moving fundamentals of new-business value, capital strength, and the spread between what the assets earn and what the policies promise.

Three lessons endure from this story. The first is the elegance and the warning of the 2003 good bank / bad bank carve-out — a blueprint for rescuing a distressed financial system by separating the poison from the crown jewels, but also a permanent reminder that the state decides who holds which. The second is the illusion of headcount-driven growth: China Life's agent force fell by two-thirds, and the business got healthier, proving that unit economics and structural efficiency ultimately override the vanity of sheer scale — a lesson that applies far beyond insurance. The third is how to think about the SOE discount honestly: it is not a mispricing to be arbitraged but a rational reflection of divided loyalties, and the intelligent way to own such a company is to value it for asset preservation, solvency, and dividend durability rather than to dream of aggressive capital appreciation. There is a fourth lesson, quieter than the others but perhaps the most useful. It is that accounting rules are not neutral plumbing; they shape how a business is perceived, valued, and even managed. The arrival of IFRS 9 did not change a single policy China Life had sold or a single yuan it had invested, yet it transformed the company from a smooth-earnings compounder into a market-sensitive weathervane, and it will do so again and again in the years ahead. Investors who understand the accounting see through the noise; those who do not will be whipsawed by it. In a company this large and this entwined with the state, the ability to read the numbers for what they actually mean — rather than what the headline proclaims — is the whole of the analytical edge.

China Life will be here in thirty years, paying the claims it promised. Whether it rewards the minority shareholder as richly as it serves the state is the question every investor in 2628.HK must answer for themselves.

References

-

Announcement of Results for the Year Ended 31 December 2025 — China Life Insurance Company Limited, HKEXnews, 2026-03-25 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

China Life Insurance records sharp jump in annual profit — China Daily, 2026-03-28 ↩↩↩↩↩

-

China Life Insurance Reports Record 2025 Profit of 154 Billion Yuan, Q4 Market Correction Leads to Single-Quarter Loss Over 13.7 Billion Yuan — BigGo Finance, 2026 ↩↩↩↩↩↩

-

China Life Insurance's 2025 profit surges 44pc to 154.1 billion yuan — The Standard (Hong Kong), 2026-03 ↩

-

China Life Insurance Company Limited History — FundingUniverse ↩↩↩↩↩↩↩

-

China Life raises US$3.5bn in world's largest IPO of 2003 — Taipei Times, 2003-12-13 ↩

-

China Insurance: Change Is Painful — S&P Global Ratings, 2023-06-21 ↩↩

-

Life insurance in China: Four priorities to transform the agency channel — McKinsey & Company ↩↩

-

Annual Report on Financial Law and Regulation — Fangda Partners ↩

-

Chinese life insurers to benefit from bancassurance commission restriction (citing Fitch Ratings) — Intelligent Insurer, 2024 ↩

-

China Life in Purchase of Citi's and IBM Credit's Stake in CGB — Cleary Gottlieb ↩↩↩

-

China Life Insurance Co Ltd completed the acquisition of 23.69% stake in China Guangfa Bank — MarketScreener, 2016-08 ↩

-

China's Sino-Ocean reports $2.3B loss as auditor questions financial future — Mingtiandi ↩↩

-

Sino-Ocean selling stake in Beijing tower to China Life — Mingtiandi ↩

-

English Court Sanctions Sino-Ocean Group Restructuring Plan — Sidley Austin, 2025-02 ↩↩

-

China Life and China Pacific report declines in investment income — Beinsure ↩

-

Announcement — Election of Executive Director and Biography of Cai Xiliang — China Life Insurance Company Limited, HKEXnews, 2024-09-30 ↩↩↩

-

Announcement — Election of Chairman and Board Changes — China Life Insurance Company Limited, HKEXnews, 2024-10-30 ↩

-

China Life Insurance Company Limited — Change of President (Li Mingguang) — PR Newswire, 2023 ↩↩

-

Circular — Election of Executive Director and Biography of Liu Hui — China Life Insurance Company Limited, HKEXnews, 2023-11-08 ↩↩↩

-

China Life Insurance Company Limited Announces 2023 Interim Results (H Shares) — PR Newswire, 2023 ↩↩

-

China Life Insurance Company Limited — Voluntary Delisting of ADSs from the NYSE — PR Newswire, 2022-08 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube