BOC Aviation Limited: The $26 Billion Flying Balance Sheet

I. Introduction & Episode Roadmap

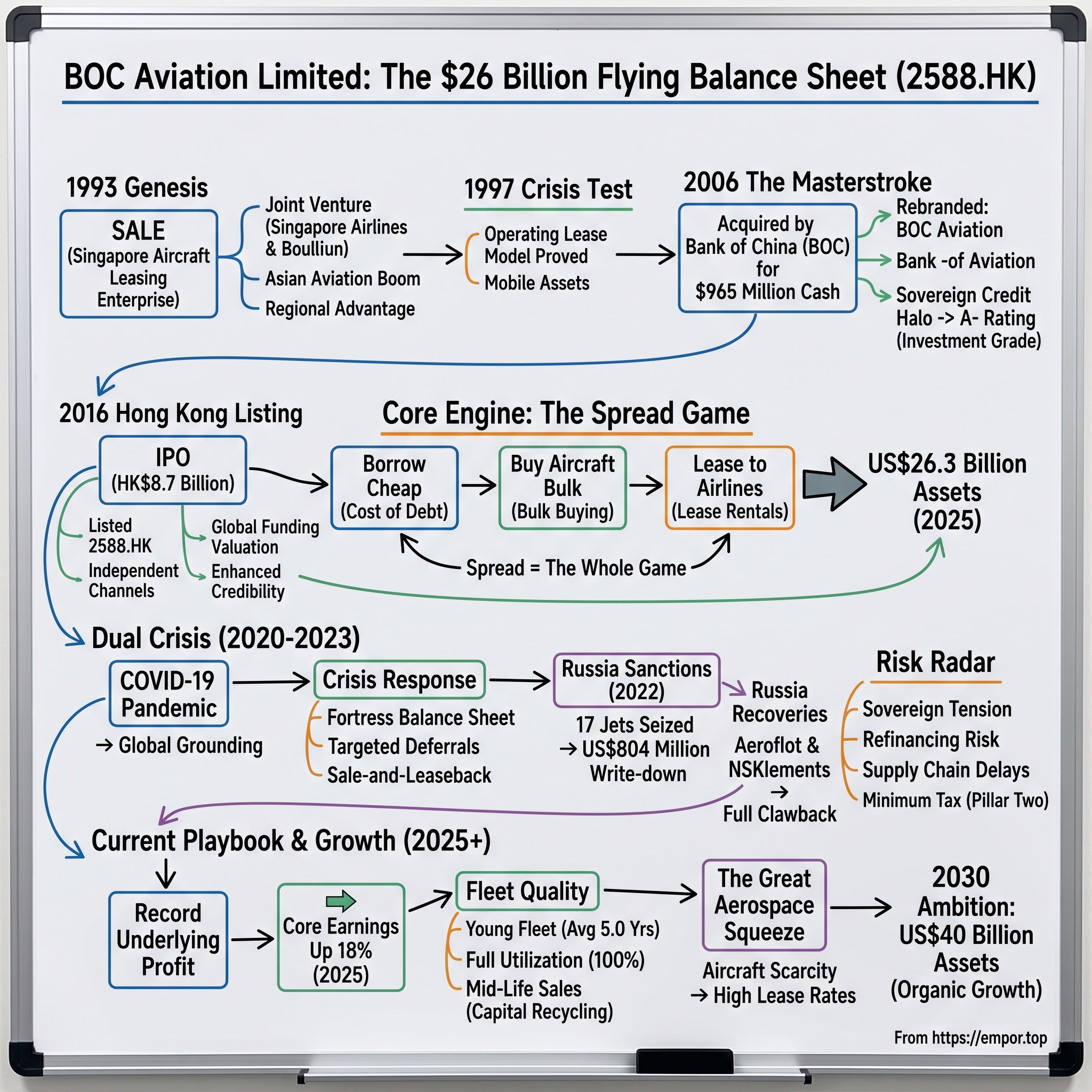

Picture the busiest air corridors on earth — Singapore to Shanghai, London to Dubai, São Paulo to Lisbon — and the hundreds of narrowbody jets threading them at any given moment. Most passengers assume the airline whose logo is painted on the tail actually owns the aluminum tube they are strapped into. Increasingly, it does not. More than half of the world's commercial fleet is now leased rather than owned outright, and behind that quiet structural shift sits a class of financial institutions that own the skies without ever selling a ticket, staffing a gate, or de-icing a wing. They are aircraft operating lessors, and among the largest and most consistently profitable is a company headquartered not in Dublin or Los Angeles, but in Singapore: 中银航空租赁 BOC Aviation Limited, listed on the 香港交易所 Hong Kong Stock Exchange under the ticker 2588.HK.

BOC Aviation is, in the most literal sense, a flying balance sheet. As of the end of 2025 it owned, managed, or had on order a portfolio of 815 aircraft and engines, and its total assets had swelled to a record US$26.3 billion.1 Its owned aircraft are leased to 87 airlines across 46 countries and regions — a spread of counterparties so wide that no single carrier's failure can sink it.1 The business it runs is deceptively simple to describe and fiendishly difficult to execute well: borrow money as cheaply as possible, buy aircraft in bulk at prices no individual airline can command, and lease them out on long-dated contracts to carriers all over the world. The gap between the cost of the borrowing and the yield on the lease — the spread — is the whole game. Everything else is detail.

What makes BOC Aviation worth a long look is not merely its scale. It is the peculiar identity at the company's core. This is a Singaporean enterprise, born in 1993 of a joint venture between an airline and an American lessor, that was bought outright in 2006 by 中国银行 Bank of China — one of the four great state-owned commercial banks of the People's Republic.2 Bank of China still owns roughly 70% of the equity today.[^3] That parentage is the source of the company's single most valuable asset, and it is not an airplane. It is a credit rating. BOC Aviation carries an investment-grade A- rating, affirmed with a stable outlook, and that rating — underwritten in large part by the market's belief that a sovereign Chinese bank stands behind it — grants the company a cost of capital that most independent lessors can only envy.3 Understand that one fact and you understand the entire business.

Three themes will run through this story like a narrative spine, and it is worth planting them before we begin.

The first is the spread game — the deceptively boring arithmetic of leasing, where fortunes are made not on any single deal but on the persistent, compounding gap between borrowing cost and lease yield. We will demystify how a lessor actually earns money, why aircraft are unusually good collateral, and why the whole model lives or dies on the cost of debt rather than on any cleverness with airplanes themselves.

The second is organic discipline. The modern leasing industry was built largely by consolidation. AerCap swallowed International Lease Finance Corporation and then GE's GECAS to become a colossus; SMBC Aviation Capital bought Goshawk. BOC Aviation, by contrast, grew almost entirely by placing its own orders directly with Airbus and Boeing, taking delivery, leasing, and eventually selling mid-life jets to recycle its capital. It is a story of patience over dealmaking — and we will test whether that discipline is a genuine, durable edge or simply a slower road to the same destination the acquirers reached by shortcut.

The third is sovereign tension. BOC Aviation is a Chinese state-linked enterprise that funds itself overwhelmingly in US dollars, buys American Boeings and European Airbuses, and leases them to Western and emerging-market carriers alike. That straddle has been enormously profitable. It is also the company's defining vulnerability, and the Russia sanctions saga of the last four years was a live-fire test of exactly how fragile a globe-spanning, dollar-funded, state-adjacent lessor can become when great-power politics turns hostile. Management, for its part, is not thinking small: it has publicly set a target of growing the asset base to US$40 billion by 2030, a roughly 50% expansion from today.4 Whether that ambition is realistic, and what it would cost to achieve, is a question we will hold up to the light. Let us begin where the company itself began — not in Beijing, but in Singapore.

II. Genesis: The Singapore Aircraft Leasing Enterprise (SALE) Era (1993–2006)

In 1993, the center of gravity of the aircraft leasing world sat firmly in the West. The two dominant names were Steven Udvar-Házy's International Lease Finance Corporation in Los Angeles and GPA Group, the Irish pioneer whose spectacular near-collapse that very year — a failed IPO that nearly took the company down and shook the entire industry — served as a vivid reminder of how brutally cyclical this business could be. Asia, meanwhile, was on the cusp of the greatest aviation boom in history. Incomes were rising across the region, deregulation was loosening the grip of state-owned flag carriers, and a generation of low-cost carriers was about to teach hundreds of millions of first-time flyers that a plane ticket could cost less than a long-distance train fare. Somebody was going to have to finance all those airplanes, and the Western incumbents were an ocean and a culture away.

Into that gap stepped Singapore Aircraft Leasing Enterprise — SALE — founded in 1993 as a 50:50 joint venture between シンガポール航空 Singapore Airlines, one of the most admired flag carriers in the world, and Boullioun Aviation Services, a US-based operating lessor.2 The logic was elegant, almost obvious in hindsight. Singapore Airlines brought deep aviation credibility, a gilt-edged reputation, and a front-row seat to Asian demand. Boullioun brought the technical machinery of leasing — how to structure a lease, value a residual aircraft a decade out, and manage a fleet across borders. And Singapore itself brought something no other Asian financial center could quite match: political stability, English common law, a pro-business tax regime, a world-class banking system, and a geographic position within a few hours' flight of the fastest-growing air markets on earth.

SALE positioned itself as the first institutional aircraft lessor native to the Asia-Pacific region, and that word "native" carried more weight than it might appear. A lessor's core skill is not owning airplanes — anyone with capital can do that. Its core skill is underwriting airline credit: deciding which carriers will still be reliably paying their monthly lease rentals in five, ten, or twelve years, and which will quietly stop. A firm run out of Los Angeles or Shannon could read a Lufthansa's or a United's balance sheet fluently. But how do you underwrite a scrappy Indonesian start-up, a Chinese provincial carrier, or a newly deregulated Indian airline with a two-year operating history? Physical and cultural proximity gave SALE an information advantage in exactly the markets that were growing fastest and that Western lessors found hardest to read. In the language of Hamilton Helmer's 7 Powers, this was an early form of counter-positioning: SALE occupied a regional niche the global incumbents could not easily contest without physically relocating and rebuilding their credit judgment from scratch — something no established Western lessor was going to do to chase a joint venture in Singapore.

The model's resilience was stress-tested almost immediately, and violently. In 1997, GIC and Temasek Holdings — Singapore's twin sovereign investment arms — joined SALE's shareholder register, deepening the enterprise's institutional and sovereign backing.2 That same year, the Asian Financial Crisis detonated across the region. Currencies collapsed, airlines that had gorged on dollar-denominated debt suddenly could not service it, and the very demand story SALE had bet its existence on looked, for a terrifying few months, like it might unravel entirely.

Here the structural genius of the operating lease revealed itself, and it is worth pausing on because it is the foundation of everything that follows. Unlike a bank that has lent money against an aircraft — and, when the borrower goes bankrupt, is left holding a claim in a courtroom and a queue of other creditors — an operating lessor owns the metal outright. When an airline fails, the lessor repossesses the jet and re-leases it to someone else, ideally a stronger carrier in a stronger market. Aircraft are mobile, standardized, and dollar-denominated assets. A Boeing 737 grounded in Jakarta by a bankrupt operator can, with the right team, be repainted and flying for a carrier in Turkey or Mexico within months. That mobility is the lessor's insurance policy against the airline cycle. SALE emerged from the 1997–98 crisis with its fleet largely intact and its underwriting reputation enhanced rather than damaged.

The episode hardened into culture a lesson that would define the company for the next thirty years: in leasing, survival is a function of discipline in the good years, not heroics in the bad ones. You underwrite conservatively when everyone is euphoric, keep your leverage sane, and hold enough liquidity that a downturn is an opportunity rather than an emergency. By the mid-2000s SALE had built a respectable, profitable, conservatively run fleet — modest by the standards of the giants, but clean. And it had caught the eye of a suitor with far deeper pockets and a far grander ambition than a regional joint venture could ever satisfy on its own.

III. The Masterstroke: China's Sovereign Bank Enters the Leasing Game (2006–2015)

By 2006, Beijing had a problem that was really an opportunity. China was on its way to becoming the largest aircraft market on the planet — its airlines would need thousands of new jets over the coming decades — yet almost all of that metal was being financed and leased by foreign firms who captured the economics and the expertise. China's state banks, flush with deposits and under a national directive to build globally competitive financial champions, saw a chance to plant a flag in an industry that combined hard assets, dollar cash flows, structural growth, and strategic importance to the country's aviation future. 中国银行 Bank of China, historically the most internationally minded of the four big state lenders, went shopping.

In December 2006, Bank of China acquired 100% of SALE for approximately US$965 million in cash.2 For a business of SALE's quality, that price was strikingly disciplined — a multiple close to book value, a world away from the frothy premiums that would later change hands as the industry consolidated. This is a detail worth dwelling on, because it establishes the character of the whole enterprise. Bank of China was not buying a hot growth story at a hot growth price. It was buying a well-run platform at a sober valuation and intending to grow it with the one ingredient SALE had always lacked: a truly world-class balance sheet standing behind every deal. In 2007 the company was rebranded BOC Aviation.2 The Singaporean bones remained — the Singapore headquarters, the Asia-Pacific underwriting culture, much of the management — but the muscle was now sovereign Chinese.

What Bank of China conferred was less tangible than an airplane but ultimately far more valuable: the sovereign credit halo. Following the acquisition, the company's credit standing climbed toward the investment-grade A- tier where it sits today, rated by both S&P and Fitch.3 To understand why that single notch of rating is the beating heart of this entire business, you have to understand what a lessor actually sells. It does not, fundamentally, sell airplanes — Airbus and Boeing sell airplanes. What a lessor sells is access to cheap capital, wrapped around an aircraft and delivered to an airline that either cannot or does not want to fund the plane itself.

Here is the mechanism, stripped to its essentials. A lessor buys a US$50 million jet using mostly borrowed money. If it can borrow at, say, 4% and lease the plane out at an implied yield of 7%, it pockets the three-point difference on the full value of the aircraft, every year, for the life of the lease. Now notice what leverage does to that arithmetic. Because the lessor funds the great majority of the aircraft's cost with debt and only a sliver with its own equity, that three-point gross spread translates into a much larger return on the equity actually invested. Shave a single percentage point off the borrowing cost and, because the business is enormously leveraged, the return on equity leaps. This is why the cost of debt is not one variable among many — it is the variable. Bank of China's implicit support let BOC Aviation issue bonds and draw bank facilities at spreads that independent, unbacked competitors simply could not match, and that funding advantage flows straight through to the bottom line.

It is worth sitting with why aircraft make such unusually good collateral for this borrow-cheap-and-lease model, because it is the reason lenders are willing to fund lessors so generously in the first place. A commercial jet is a globally standardized, dollar-denominated asset with a deep secondary market and a useful life measured in decades. A Boeing 737 or Airbus A320 is essentially the same machine whether it flies for a carrier in Chile or Vietnam, which means a lender financing that aircraft knows that even in a default it is secured against something liquid and relocatable rather than a factory bolted to one spot. That collateral quality lets a lessor borrow a large fraction of each aircraft's value at attractive rates — and the better the lessor's own credit, the better those rates still. Stack a top-tier borrower's credit on top of top-tier collateral, as BOC Aviation does, and you arrive at about the cheapest secured financing available anywhere in corporate finance. This is the deep structural reason the leasing model works at all, and why the cost-of-capital advantage compounds rather than erodes.

That advantage was thrown into sharp relief during the 2008 Global Financial Crisis. As credit markets froze and funding evaporated for leveraged financial firms of every kind, several aircraft lessors found themselves starved of the debt that was their lifeblood. GE's GECAS and AIG's ILFC — the two biggest names in the industry — were both tethered to parents in acute distress, and ILFC in particular nearly became collateral damage in AIG's implosion. BOC Aviation, tethered instead to a sovereign bank whose deposit base was rock-solid, kept its funding taps open when others' ran dry. And crucially, it could keep buying aircraft precisely when prices were softest and airlines were most desperate to raise cash by selling their fleets and leasing them straight back. The firm that can still write checks in a crisis gets to choose the best deals at the best prices — a pattern that would repeat, almost note for note, during the pandemic a dozen years later.

That funding edge fed directly into a second, reinforcing advantage: scale economies in purchasing. Armed with cheap, reliable capital, BOC Aviation began placing large direct orders with Airbus and Boeing — committing to fifty or a hundred aircraft at a time rather than picking up jets one by one. Bulk buyers of narrowbody aircraft negotiate discounts off manufacturers' list prices that are famously steep; industry practice is that large lessors and major airlines routinely secure discounts far exceeding anything a carrier ordering a handful of planes could ever obtain. Those discounts became the raw material of BOC Aviation's spread. Buy the asset well below list, finance it more cheaply than your rivals, lease it at the market rate, and the economics compound quietly in your favor on every single aircraft. Between the Bank of China acquisition and the middle of the 2010s, the company did exactly that — year after year, jet after jet, growing its fleet and its earnings with the metronomic consistency that would become its signature. By 2015 it had comfortably outgrown its private, wholly-owned structure. It was time to show the world the numbers, and to let a public market put a price on the sovereign halo.

IV. Going Public: The 2016 Hong Kong Listing

On June 1, 2016, BOC Aviation's shares began trading on the Main Board of the 香港交易所 Hong Kong Stock Exchange under the ticker 2588, the company having converted weeks earlier from a private company to a public one and adopted the name BOC Aviation Limited.4 The initial public offering raised roughly HK$8.7 billion, or about US$1.1 billion — one of the more substantial financial-sector listings in Hong Kong that year.4 For a company that had spent more than two decades as a low-profile subsidiary — first of a Singaporean airline, then of a Chinese bank — stepping onto a public exchange was a coming-out party with a very specific guest list in mind: global bond investors, international airline customers, and the ratings agencies whose opinions underwrote the whole business.

The structure of the deal told you everything about its purpose. Bank of China deliberately retained a controlling stake of roughly 70%, floating only about 30% of the equity to the public.[^3] This immediately raises the obvious question a skeptical investor should ask: why bother listing at all if the parent keeps three-quarters of the company and cedes no real control? A minority holder in a 70%-controlled company has essentially no ability to force change; the parent decides. So what was the point?

The answer is that the IPO was never primarily about raising equity capital. It was about plumbing and credibility. Consider what a public listing bought BOC Aviation that a private structure could not. First, an independent, market-tested valuation — a transparent share price that anchored the company's cost of equity and gave it a currency it could use in the future. Second, a genuine diversification of funding channels away from near-total reliance on parent-adjacent bank debt, opening the door to deep public bond markets and a far broader base of investors around the world. Third, and most subtly, the disciplines that come with a public listing: audited disclosure to an exchange standard, a board with independent directors, semi-annual scrutiny from analysts and investors, and adherence to international corporate governance norms.

That last point carried real, quantifiable commercial value, and it connects directly to the sovereign-tension theme. When a lessor asks a Lufthansa, an American Airlines, or an Emirates to sign a twelve-year lease and entrust it with tens of millions of dollars of rent, the airline is underwriting the lessor as much as the reverse — it needs confidence that its counterparty will honor purchase agreements, deliver aircraft on spec, and behave predictably for over a decade. A transparent, exchange-listed, well-governed counterparty is simply easier and safer to do business with than an opaque state subsidiary. For a Chinese-owned firm courting Western customers and Western bondholders, that reassurance was worth more than the cash the IPO raised.

The prospectus itself was a study in how a leasing business wants to be seen. It emphasized not aggressive growth but quality: a consistent record of profitability through cycles, a young fleet with an average age of well under four years at the time, and a shareholder-friendly dividend policy targeting a payout of up to 40% of net profit after tax.4 That trinity — durable profitability, fleet youth, and disciplined capital return — was a deliberate rebuttal to the boom-and-bust reputation that had shadowed the leasing industry since the GPA collapse of the early 1990s. The message to prospective investors was unmistakable: we are not a leveraged bet on the aviation cycle; we are a steady compounder that happens to own airplanes, and we will hand you back a defined share of the profits every year.

For a while, reality obliged. In the years after listing, BOC Aviation compounded its fleet and earnings much as it had before, and the shares developed a following among investors who wanted exposure to structural aviation growth without the operational chaos, fuel-price exposure, and thin margins of owning an airline. This is the quiet pitch of the whole asset class: a lessor captures the growth of global air travel while shedding most of the operational risk. It does not fly the plane, hedge the jet fuel, staff the cabin, or fill the seats — it simply owns the aircraft and collects a contracted rent whether the flight is full or empty, whether fuel is cheap or dear. The airline bears the volatility; the lessor holds the asset. In good times the airline keeps the upside of a booming route, but in bad times it is the airline, not the lessor, that absorbs the shock — and even then the lessor's aircraft, being mobile and re-leasable, tends to survive the airline that fails. That structural insulation is why a well-run lessor can post steadier returns through the cycle than almost any airline ever manages, and it is what BOC Aviation put on display in its first years as a public company. But a prospectus is a promise made in fair weather. Whether the quality it advertised was real would be tested not by a routine downturn but by two of the most extreme shocks the aviation industry had ever faced, arriving almost back to back — a global grounding of the entire air-travel system, followed by an assault on the one assumption every lessor's model quietly depends on. The pristine young fleet and fortress balance sheet the prospectus advertised were about to be run through a wringer no prospectus could have modeled.

V. The Dual Crisis: Grounded Planes, Stolen Jets, and the Russian Showdown (2020–2023)

In the spring of 2020, the unthinkable happened to the airline industry: demand went to essentially zero. As COVID-19 swept the world and borders slammed shut within days of one another, global passenger traffic collapsed by more than 90% almost overnight. Fleets that had been flying at near-full utilization in January were parked wingtip to wingtip in desert boneyards by April. Airlines that had carried investment-grade credit ratings at the start of the year were queueing for government bailouts by spring. For an aircraft lessor — whose entire business rests on airlines around the world reliably paying their monthly rent — this was the nightmare scenario made real: thousands of leases, spread across dozens of countries, all coming under pressure at exactly the same moment.

BOC Aviation's response revealed the temperament its prospectus had advertised. Rather than panic — accelerating repossessions, suing struggling customers, or dumping aircraft into a market with no buyers and no lease demand — management leaned on the fortress balance sheet and played for the long term. It granted targeted lease deferrals to core airline customers, effectively extending them short-term credit to bridge the worst of the shutdown, and it used its cheap, still-available funding to keep transacting when much of the market was frozen solid. A key tool was the sale-and-leaseback. Cash-strapped airlines sold aircraft they already owned outright to BOC Aviation and leased them straight back, converting metal into desperately needed liquidity to survive the drought. For the airline it was oxygen; for the lessor it was a chance to acquire young, in-demand aircraft — often on attractive terms — with a long-term lease already attached and a customer motivated to keep paying. Once again, the firm that could still write checks in a crisis got to choose the best deals.

The pandemic was a shock the entire industry shared, and BOC Aviation weathered it better than most precisely because of the discipline it had banked in the good years. The second crisis was more sinister, because it struck not at demand but at the one assumption underpinning the whole model: that you own your airplanes and can, when you must, get them back. In February 2022, Russia invaded Ukraine. Western sanctions followed within days, legally requiring lessors to terminate their leases with Russian airlines and repossess their aircraft. Russia's response was to effectively nationalize the foreign-owned jets sitting on its soil — hundreds of aircraft across the industry, collectively worth on the order of US$10 billion, simply seized, re-registered onto the Russian aircraft registry, and kept flying for domestic carriers in open defiance of their legal owners.

BOC Aviation had 17 aircraft trapped in Russia when the door slammed. In August 2022 it took a pre-tax write-down of approximately US$804 million against those jets, effectively marking the stranded fleet down to nothing — one of the largest single hits in the company's history.5 For a business whose entire identity had been built on the certainty of asset ownership and the mobility of collateral, watching US$804 million of aluminum vanish behind a geopolitical iron curtain was an existential insult, not merely a financial one. This was the sovereign-tension theme made brutally concrete: a globe-spanning, dollar-funded lessor discovering that in a world of hard sanctions and counter-sanctions, physical possession by a hostile state can override legal title, and that the "mobility" of aircraft collateral is only as reliable as the geopolitics of where the aircraft happens to be parked.

What happened next is the part of the story that separates BOC Aviation from a firm that simply eats its losses and moves on. Rather than write off the Russian fleet and blame the macro gods, management pursued recovery on two fronts at once. It litigated aggressively — including proceedings in the Irish High Court and substantial claims against the aviation insurers who had underwritten the aircraft — and it negotiated pragmatically with the Russian side for direct settlements. These were, in effect, two levers on the same problem: extract value from the seized assets by whatever route paid out first, whether an insurer's check or a Russian buyout.

The settlements came steadily over the following two years. In late 2023, BOC Aviation reached agreements with Аэрофлот Aeroflot Group covering aircraft operated by its carriers.6 Then, in a settlement finalized around November 2024, the Russian insurer НСК NSK Insurance paid roughly US$208 million in cash to take ownership of eight Boeing 737-800s that had been leased to Aeroflot's low-cost unit Победа Pobeda, plus a further aircraft under management.7 Layered on top of the earlier recoveries, these deals ultimately allowed BOC Aviation to recover effectively the entire US$804 million it had written down. With its claims substantially satisfied, the company withdrew its remaining Irish High Court action against insurers in early 2025.[^9]

This full recovery deserves interrogation rather than mere applause, because how you read it shapes how you value the company. On one interpretation, it is a genuine demonstration of what Helmer would call process power — legal and commercial execution that a less capable or less patient competitor could not have matched, turning an US$804 million crater into a full clawback while many peers were still mired in litigation. On a more skeptical interpretation, the recovery also reflected BOC Aviation's uniquely useful position: as a Chinese state-linked lessor rather than a Western one, it may simply have found Russian counterparties, insurers, and airlines more willing to settle than they were with firms domiciled in sanctioning jurisdictions. Both things can be true at once, and an honest analysis holds them together. Either way, the recoveries flattered the reported results substantially. They contributed to a record net profit after tax of US$924 million in FY2024, up 21% on the prior year's US$764 million.8 But that headline was inflated by one-off insurance recoveries — a nuance that matters enormously for understanding what came next, when the tailwind faded and the market got its first clean look at the underlying engine.

VI. The Current Playbook: Operating Economics and the Great Aerospace Supply Squeeze

When BOC Aviation reported its full-year 2025 results in March 2026, the headline looked, at first glance, like a step backward: net profit after tax of US$787 million, down from the record US$924 million of 2024.1 A casual reader might see a company sliding into reverse. A careful one sees very nearly the opposite. The 2024 figure had been juiced by the Russian insurance recoveries; strip those one-off items out, and underlying net profit rose 18% in 2025, to US$746 million — a genuine record for the core business.1 Management leaned hard on that distinction, deliberately headlining the release "record underlying profit," and in this instance the framing is defensible rather than promotional: the recurring operating engine actually got stronger even as the one-time tailwind disappeared. It is a useful reminder always to separate a lessor's durable lease economics from the lumpy, non-recurring gains — insurance settlements, large trading gains, write-backs — that periodically flatter or depress the reported number in any single year.

That same lesson had played out visibly at the half-year. In the first half of 2025, reported NPAT fell to US$342 million from US$460 million a year earlier — but the prior-year figure had included roughly US$175 million of non-recurring write-backs, and on a clean core basis, first-half earnings actually grew 20% to a record.9 On the results call, CEO Steven Townend framed it plainly, noting the company had recorded its "highest ever core first-half earnings, driven by rising demand in all our key businesses."9 For an investor, the takeaway is not the noisy headline in either direction but the trajectory of the core: two consecutive records, driven by the fundamentals of the business rather than by settlements.

Underneath the headline, the machine looks formidable. For the full year, total revenues and other income rose 2% to US$2.6 billion, while total assets reached the record US$26.3 billion.1 Operating free cash flow climbed 17% to a record US$2.2 billion, and the company sat on US$6.9 billion of total liquidity at year-end — a deliberately oversized war chest for a business whose whole edge depends on being able to buy aggressively when others cannot.1 Critically for a company that has staked its reputation on capital-return discipline, it stuck to its word on dividends, declaring a total 2025 payout equivalent to 40% of net profit — the top of its stated range, and a step up from the 35% distributed for 2024.18 A management team that hits, and then raises to the top of, its own dividend policy year after year is quietly compounding a different kind of asset: credibility.

Fleet quality is the quiet KPI that underwrites everything else. By the end of 2025 the portfolio comprised 815 aircraft and engines — of which the owned fleet numbered around 462, with roughly 16 managed and an order book of 337 aircraft still to be delivered.10 Set that against the end of 2024, when the total portfolio stood at 709 aircraft with 435 owned and a 232-aircraft order book, and you can see the organic growth engine at work: the fleet expanded meaningfully in a single year without a single acquisition, funded by orders and purchase-and-leasebacks rather than by buying a rival.8 Through all of it, the owned fleet's average age held near 5.0 years — among the youngest of any major lessor — with an average remaining lease term of roughly eight years, and utilization at effectively 100%.108

Those three fleet numbers together tell a coherent and important story. Young aircraft are cheaper to maintain, more fuel-efficient (and so more attractive to cost-conscious airlines), and hold their residual value far better than older jets. A long average remaining lease term — close to eight years — locks in a river of contracted cash flow that does not depend on next year's market. And full utilization means no expensive jets sitting idle in storage burning money and insurance premiums. A young, fully-leased, long-dated fleet is the physical embodiment of the discipline the company has preached since the SALE days, and it is the thing that lets management sleep through the aviation cycle.

Now to the economics that actually matter, drawn from the company's most recent detailed disclosures. The recurring core is lease rental income — the monthly rent airlines pay — which drives the large majority of revenue. Around it sit interest and fee income from finance leases and management services, and the more opportunistic gains on aircraft sales, which function as the trading desk of the operation. That trading line is strategically revealing and worth explaining. When BOC Aviation sells a mid-life aircraft for more than its carrying value, it proves two things simultaneously: that its assets are conservatively booked on the balance sheet, and that there is deep, liquid buyer demand for young jets. In the first half of 2025, for example, the company sold 18 aircraft and booked gains at a healthy margin, part of a deliberate program of selling mid-life metal to recycle capital into new deliveries.9 This is the compounding flywheel in motion: buy new, lease long, sell mid-life at a gain, and roll the proceeds into the next order — which is precisely how the fleet stays young without a single dilutive acquisition.

The spread economics reached a genuinely favorable place. On its interim disclosures, BOC Aviation's net lease yield advanced to around 7.5%, up from 7.0% a year earlier, while its cost of debt sat in the mid-4% range and its lease rate factor — a measure of monthly rent relative to aircraft cost — rose to 10.3% from 9.8%.11 The reason those numbers are climbing brings us to the defining feature of the current market: the great aerospace supply squeeze. Boeing, hobbled by the 737 MAX crises, quality-control scandals, and a bruising 2024 labor strike, has been unable to deliver jets on schedule for years; Airbus has wrestled with its own engine and supply-chain constraints. New-aircraft delivery slots are backed up well into the next decade. In a world where airlines cannot get the planes they need, existing aircraft — and firm order positions — become scarce and precious. Lease rates rise, and lessors holding young fleets and confirmed delivery slots find themselves holding something close to gold. Bloomberg captured the moment aptly, reporting that lessors were riding high on record lease rates driven directly by the manufacturers' production shortfalls.12

Behind those spreads sits the capital-markets machine that makes them possible, and 2025 showed it running at full tilt. The company deployed roughly US$4.2 billion of new capital expenditure into aircraft during the year and raised about US$4.3 billion of fresh debt financing to fund it — a near one-for-one match that tells you how tightly the funding engine is calibrated to the buying engine.1 It carried committed capital expenditure of around US$19 billion against its order book, an obligation that only a firm confident in its continued access to cheap debt would take on.1 Net assets per share rose to US$9.86 and total equity to US$6.8 billion, the retained-earnings ballast that lets the company keep levering into new aircraft without straining the rating.1 For a business whose product is cheap capital, the ability to raise billions of dollars of debt on demand, at tight spreads, through a year of elevated interest rates, is not a footnote — it is the operating system working exactly as designed.

All of which feeds an explicit and unusually concrete ambition. Management has publicly targeted growing the asset base to roughly US$40 billion by 2030 — a step up of about 50% from the current US$26 billion, to be reached organically through deliveries and purchase-and-leasebacks rather than acquisition.4 That target is worth holding management to, because a stated numerical goal with a date attached is exactly the kind of promise against which credibility is later scored. It is ambitious but not fanciful: the 337-aircraft order book already contains much of the metal required to get there, provided Boeing and Airbus deliver. The risk is not that the target is dishonest but that it is hostage to the very supply squeeze currently inflating the company's margins — a tension we will return to. For now, the more telling credibility signal is the smaller promise the company keeps every six months: a dividend policy honored and then raised to the top of its range, and a growth story delivered without the write-downs and broken forecasts that so often accompany rapid expansion.

Steering the company through this uniquely favorable window is a relatively new chief executive, and the handover is itself a study in the company's culture. On December 31, 2023, Robert Martin — who had run BOC Aviation and its predecessor for the better part of three decades and was the human embodiment of its patient, cycle-tested temperament — stepped down as managing director and CEO, remaining on the board as a non-executive director to preserve institutional memory.13 On January 1, 2024, Steven Townend took the controls.13 Townend was no outsider parachuted in to shake things up. He was a firm veteran of more than two decades who had served as chief financial officer and deputy managing director — meaning the person now setting strategy is the very one who spent years engineering the balance sheet and funding structure that are the company's core weapon.13 The message was continuity, not disruption, which is exactly the right message for a business whose entire edge is its refusal to do anything sudden. Alongside him, the CFO role passed to Wu Jianguang, who came from Bank of China's own financial-management department — a thread that keeps the parent close to the company's purse strings.13

That continuity extends to how the leadership is paid, which a skeptical investor should always inspect. Executives are incentivized through a Restricted Share Unit long-term incentive plan whose performance metrics are tied to net profit after tax, return on equity, and collection rates, and which carries clawback provisions.10 The design is telling. By anchoring pay to profitability, returns on capital, and — crucially — collection rates rather than to raw fleet growth or headline revenue, the plan is structured to discourage the single greatest temptation every lessor faces in a hot market: chasing market share by buying too many aircraft and leasing them to weak, low-quality airlines at thin margins that look fine until a downturn exposes them. Whether the plan genuinely restrains that impulse can only be proven across a full cycle, but the intent is consistent with the organic-discipline story the company has told for thirty years. And that discipline is best understood not in isolation, but by contrast — against rivals who chose a dramatically different path to the same scale.

VII. Competitive Landscape: Organic Discipline vs. Mega-M&A Giants

To war-game BOC Aviation's competitive position, it helps to sort the top tier of the leasing industry into two tribes with fundamentally different philosophies about how to grow: the mega-M&A integrators, who bought their way to scale, and the organic compounders, who built it order by order, jet by jet.

The undisputed titan of the first tribe is AerCap, the Dublin-based giant that assembled its roughly 1,500-plus aircraft empire through a series of blockbuster acquisitions — buying International Lease Finance Corporation from a crippled AIG in 2014, and then GE Capital Aviation Services in 2021 to become, by a very wide margin, the largest aircraft lessor on earth. AerCap competes through sheer scale, deep and sophisticated access to global corporate debt markets, and the negotiating heft that comes from ordering aircraft by the many hundreds. Alongside it sits SMBC Aviation Capital, backed by the Japanese megabank 三井住友銀行 Sumitomo Mitsui Banking Corporation, which vaulted up the rankings by acquiring Goshawk Aviation in 2022 and now operates a fleet of comparable size to BOC Aviation's. These are the consolidators — the firms that bought growth and then set about digesting it.

BOC Aviation and Air Lease Corporation sit firmly in the second tribe. Air Lease, the roughly 450-plane lessor founded in 2010 by the legendary Steven Udvar-Házy after he left ILFC, is independent and founder-led — but crucially lacks a bank parent, and therefore lacks the rating halo a sovereign owner confers, funding itself instead purely on its own corporate credit. BOC Aviation is arguably the purest expression of organic discipline in the entire industry. With an owned fleet in the mid-400s and an order book of 337 aircraft, it has grown almost entirely through direct manufacturer orders and purchase-and-leaseback deals rather than corporate M&A.10 In the first half of 2025 alone it committed to what it described as the largest aircraft order in its history — 70 Airbus A320neo-family jets and 50 Boeing 737 MAX aircraft — a single pen-stroke that speaks to both its confidence and its access to delivery slots that rivals covet.914

Which philosophy is better? The honest answer is that each carries a distinct and opposite risk, and the industry has not settled the debate. The integrators bought their scale instantly, but inherited integration friction, mixed-age and mixed-quality fleets, and the heavy write-downs that inevitably come with absorbing other companies' aircraft and legacy lease books. The organic compounders avoid all of that friction and keep their fleets pristine, but they grow more slowly and remain hostage to the manufacturers' ability to actually deliver the jets they have ordered — a dependency that, as we will see, cuts in surprising directions. BOC Aviation's whole bet is that in leasing, as in compounding generally, the tortoise's steady asset rotation beats the hare's episodic dealmaking across a full cycle. The pristine 5.0-year average fleet age, achieved without a single acquisition, is Exhibit A that the strategy is at least working on its own terms.

Run the situation through Porter's five forces and the picture sharpens considerably. Supplier power is extreme. Commercial aircraft manufacturing is a duopoly of Boeing and Airbus, and in the current squeeze the two manufacturers hold the whip hand on both price and timing — there is nowhere else to buy a modern narrowbody at scale. Yet here BOC Aviation's order book flips a weakness into a genuine advantage — what Helmer would call a cornered resource. With deliveries backlogged for years, a firm order slot for a new narrowbody is itself a scarce, valuable asset, and BOC Aviation holds 337 of them.10 Airlines that cannot secure their own delivery positions must come to lessors who already have them, handing real pricing power to whoever controls the pipeline.

The other forces reinforce the position. Buyer power is moderate and heavily fragmented across 87 airline customers in 46 countries, no one of which is remotely indispensable to the company — a deliberate diversification that is itself a form of risk management.1 The threat of substitutes — airlines simply buying their own planes with their own cash instead of leasing — actually recedes precisely when capital is expensive and aircraft are scarce, which is exactly today's environment; a cash-strapped airline in a high-rate world is more likely to lease, not less. And the threat of new entrants is blunted by the single hardest barrier in this business: you cannot conjure an A- credit rating, a two-decade underwriting track record, and relationships with the manufacturers deep enough to command hundreds of delivery slots overnight. Capital alone does not buy your way in; several well-funded new lessors have tried and struggled.

One further competitive nuance deserves attention, because it complicates the tidy two-tribe picture: BOC Aviation is not the only bank-backed lessor with a sovereign halo. It shares that structural advantage with a cluster of Chinese peers spun out of the country's other state financial giants — notably 工银租赁 ICBC Leasing, the aircraft-leasing arm of 中国工商银行 Industrial and Commercial Bank of China, and 国银租赁 CDB Aviation, backed by China Development Bank. These firms enjoy their own versions of cheap, state-adjacent funding, and they have grown into meaningful players in the global leasing market. What separates BOC Aviation from them is less the funding advantage — which they broadly share — than the operating track record: BOC Aviation's decades of Western-standard governance, its Hong Kong listing, its diversified international customer base, and its demonstrated ability to place aircraft with the world's premier airlines rather than primarily with Chinese carriers. The sovereign halo, in other words, is necessary but not sufficient; the durable edge is the halo plus thirty years of disciplined underwriting and global relationships that a newer state-backed rival cannot simply purchase.

That barrier is the company's deepest moat, and it maps directly onto Helmer's scale economies and, above all else, its cost position. Its investment-grade rating keeps its average cost of debt anchored in the mid-4% range even as broader interest rates have risen sharply from the lows of the last decade, while its net operating lease yield has climbed toward 7.5%.311 The gap between those two figures — a net interest spread comfortably above 5% — is the entire investment case expressed as a single number. Because BOC Aviation borrows more cheaply than almost any independent competitor, it can win deals at lease rates that would be marginal or unprofitable for a higher-cost rival, or pocket a fatter margin on the identical deal. The rating, in other words, is not a footnote to the business. It is the business. And that realization frames the central debate every prospective investor must resolve for themselves.

VIII. The Investor's Stress Test: Bull vs. Bear and Risk Radar

Myth vs. Reality

Before stress-testing the case, it is worth clearing away three consensus narratives that do not survive contact with the disclosures.

Myth: BOC Aviation is a Chinese company leasing Chinese planes to Chinese airlines. The ownership is Chinese, but almost nothing else about the operation is. The company is headquartered and managed in Singapore, keeps its books in US dollars, buys exclusively from Boeing and Airbus, and leases to 87 airlines spread across 46 countries and regions.1 Its customer base is a map of global aviation, not of the mainland. The Chinese connection is a funding and ownership fact, not a commercial concentration — which is precisely why the geopolitical risk, when it bites, would bite at the funding and ownership level rather than through customer concentration.

Myth: profits fell in 2025, so the business is deteriorating. This is the most common misreading of the company, and it is simply an artifact of comparing a settlement-inflated year to a clean one. Reported profit did decline, but the underlying business posted its best year ever, with core earnings up 18%.1 Anyone reading only the headline number would draw exactly the wrong conclusion about the direction of the operating engine — a reminder that with lessors, one-off items routinely swamp the signal in any given twelve months.

Myth: rising interest rates are bad for leveraged lessors. Intuitively this seems obvious — a highly leveraged business borrowing at higher rates should suffer. In practice the relationship is more subtle, and for a low-cost borrower it can invert. Higher rates make aircraft ownership more expensive for airlines, pushing more of them toward leasing; they also lift lease rates across the market. A lessor with an unusually cheap and stable funding base can therefore see its spread widen as rates rise, which is broadly what the recent yield and lease-rate-factor data show.11 The genuine risk is not the level of rates but the convergence of the two curves — and that is a very different thing to monitor.

Every compelling investment case has a bull argument and a bear argument that are, on close inspection, the same fact viewed from opposite ends. For BOC Aviation, that fact is its parentage. Turn it one way and it is the source of the cheapest capital in the entire industry; turn it the other and it is a concentration of geopolitical risk unlike anything its Western peers carry on their books. A serious investor has to hold both views in mind at once and decide which one the future will vindicate.

Why they win, from here. The bull case is the yield-to-cost spread play operating in something close to its ideal habitat. In an environment of higher-for-longer interest rates and acute aircraft scarcity, lease rates are rising across the whole industry — and because BOC Aviation funds itself more cheaply than nearly anyone, rising rates can actually widen its net margins rather than compress them, as older low-rate debt rolls off and new leases get priced at today's elevated rents. Crucially, the evidence for this is not management rhetoric but observable operating data: a net lease yield climbing toward 7.5%, a lease rate factor at 10.3%, an order book of 337 delivery slots functioning as scarce cornered assets, a fleet age of 5.0 years, full utilization, and two consecutive records in core earnings.10119 Layer on the complete Russia recovery as a demonstration of execution credibility under fire, and the bull thesis is that this is a structurally advantaged compounder catching a once-in-a-generation supply cycle at exactly the right moment — with a stated ambition to grow the asset base to US$40 billion by 2030 to press the advantage.4

Why the case could break. The bear case starts with that same celebrated balance sheet and asks a harder question about who, ultimately, stands behind it. BOC Aviation is roughly 70% owned by 中国银行 Bank of China, itself an instrument of the Chinese state.[^3] The company funds itself overwhelmingly in US dollars raised in Western capital markets, buys Boeing and Airbus aircraft, and leases them to carriers around the globe. That straddle has been a genuine superpower for two decades — but the Russia episode proved, in the most concrete way imaginable, that when great-power politics turns hostile, the ground can shift with terrifying speed and legal ownership can count for nothing. The activist-style stress test almost writes itself: if US-China tensions were ever to escalate toward the kind of sweeping sanctions regime imposed on Russia, could Western and allied airlines continue leasing from a Chinese state-owned lessor? Could the company keep issuing dollar bonds to Western investors on whom its funding advantage depends? Its entire cost-of-capital edge, and a meaningful slice of its customer base, rest on a geopolitical status quo that is, by any honest reading, less stable than it was a decade ago. This is not a risk the company can hedge or diversify away — it is embedded in the ownership structure that is also its greatest strength.

Between those two poles sit several more concrete, mechanical risks that belong on any serious risk radar.

The first is refinancing and cost-of-capital risk. The company's celebrated mid-4% cost of debt is a blended figure that still includes a great deal of cheap borrowing locked in during the ultra-low-rate years. As that vintage debt matures and must be rolled over at today's materially higher rates, the average cost will drift upward almost mechanically. The entire bull case depends on lease yields rising fast enough to preserve or widen the spread. If funding costs climb faster than lease rates — or if the aircraft-scarcity dynamic currently lifting lease rates eventually eases as Boeing and Airbus finally clear their backlogs later this decade — that spread could narrow. It is the spread, not the absolute level of either rate, that must be defended, and it is under continuous, quiet pressure.

The second is manufacturer execution risk, which cuts in a genuinely double-edged way that many observers miss. The same Boeing and Airbus delays that are inflating today's lease rates also mean BOC Aviation frequently cannot take delivery of its own ordered aircraft on schedule. Its growth model — and its US$40 billion ambition — depends on converting that 337-aircraft order book into delivered, leased, cash-generating metal on something like the planned timetable. Every slipped delivery keeps rates high on the existing fleet (good for near-term earnings) but pushes the company's own growth-on-delivery pipeline to the right (bad for the growth story), while leaving it dependent on two chronically troubled suppliers to execute. The supply squeeze is simultaneously the tailwind lifting current earnings and the headwind delaying future growth — a tension that will define the next several years.

A third, quieter risk has recently arrived on the scene and deserves a mention because it directly touches the company's core arithmetic: tax. The global minimum tax regime — the OECD's Pillar Two framework, mandating an effective minimum corporate rate — began flowing through BOC Aviation's earnings in 2025, lifting its effective tax rate sharply (in the first half, to 15.8% from 9.7% a year earlier) and shaving a meaningful amount off net profit, with management flagging that the higher rate will persist.9 For a company long domiciled in low-tax Singapore, this is a structural, permanent nick to the after-tax spread that no amount of operational excellence can undo. It is not existential, but it is real, and it quietly raises the bar the operating business must clear.

There is also a subtler tension buried inside the growth ambition itself, and it is the kind of thing an activist investor would press on. The US$40 billion-by-2030 target implies steady, aggressive buying over the next several years — but the company's entire brand, and much of its rating, rests on not buying indiscriminately. Growth and discipline are not natural allies in leasing; the fastest way to grow an aircraft portfolio is to relax your underwriting and pay up for volume, which is exactly the behavior the incentive plan is designed to prevent. Management is therefore threading a genuine needle: it must expand the balance sheet by half within five years while keeping the fleet young, the credit quality high, and the spread wide. History suggests it can — the fleet grew meaningfully in 2025 without any deterioration in age or utilization — but the tension is real, and the moment the numbers show the company chasing growth at the expense of margin or credit quality is the moment the investment case should be re-examined.

Finally, there is a governance point a diligent investor should log rather than lose sleep over. With Bank of China controlling roughly 70% of the votes and supplying senior executives — the current CFO came directly from the parent's financial-management department — minority shareholders are, in the end, passengers on a controlled company, reliant on management's demonstrated discipline rather than on any ability of their own to force change.[^3]13 The historical record on that discipline — the steady fleet, the honored dividend policy, the clean recovery from Russia — is genuinely reassuring. But the structural dependence on it is simply a permanent fact of this particular investment, not something that will ever be resolved.

IX. Playbook & Key Takeaways

Step back from the quarter-to-quarter numbers and BOC Aviation offers two durable business lessons that travel far beyond the narrow world of aircraft leasing.

The first: in financial leasing, the credit rating is the product. It is tempting to think a lessor's product is the airplane, but the airplane is a commodity available to anyone with a purchase order and access to Toulouse or Seattle. What BOC Aviation actually sells is access to capital cheaper than its own customers or its competitors can source, wrapped around that commodity and delivered on a twelve-year contract. This reframes entirely what "success" looks like for the business. Protecting the A- rating — through conservative leverage, disciplined underwriting, ample liquidity, and the sovereign parentage that anchors it — matters more than winning any individual deal or grabbing a point of market share. A lessor that chases growth by loosening its credit standards or over-levering its balance sheet is quietly cannibalizing the only thing that makes it special. The entire visible edifice of young fleets, full utilization, and fat spreads rests, invisibly, on that one notch of investment-grade credit.

The second: organic asset rotation can beat M&A integration. The industry's giants bought their scale in a hurry and then inherited the friction — the integration headaches, the aging and mismatched fleets, the write-downs that come with digesting other companies' aircraft and lease books. BOC Aviation instead kept its fleet at a pristine 5.0-year average age through the unglamorous, endlessly repeatable discipline of buying new, leasing long, selling mid-life, and recycling the proceeds into the next order — letting compounding, not dealmaking, do the heavy lifting. It is slower and far less dramatic than a mega-merger, and it surrenders the instant scale that acquisitions deliver. But it also sidesteps the value destruction that so often follows the champagne of a deal announcement, and over a full cycle the tortoise's steady rotation has kept the fleet younger and the balance sheet cleaner than the hare's episodic buying spree. Whether that patience continues to pay as the company reaches for US$40 billion in assets — a stretch that may test the discipline that got it here — is the open question of the next five years.

For an investor tracking this company over time — without ever needing to calculate anything, simply reading what management discloses each half — three KPIs capture almost the entire story, and they should be read together rather than in isolation, because any one of them alone can mislead.

Net operating lease yield. Currently around 7.5%, and rising on the back of aircraft scarcity.11 This is the "revenue" side of the spread — how much rent the fleet earns relative to what it cost. As long as the supply squeeze persists, the direction should be upward; a sustained reversal would be the first hard sign that the scarcity cycle inflating today's lease rates has begun to turn.

Average cost of debt. Currently in the mid-4% range.11 This is the single best barometer of the parent's credit halo actually working in practice. If it drifts materially higher as cheap legacy debt matures — or, more ominously, if it ever decouples upward from where peers are funding — that is the market quietly repricing the sovereign backstop, which would be the most important and most easily missed way the moat could erode.

Net interest spread. The gap between the two, comfortably above 5%. This is the investment case distilled to a single figure. It must stay wide to justify the equity. If lease yields and funding costs both rise but the spread holds, the model is working exactly as designed; if the spread compresses even as headline profit looks impressive in some settlement-flattered year, the compounding engine is losing power beneath the surface, and that is what an owner should watch above all else.

BOC Aviation is, in the end, precisely what its balance sheet says it is — a disciplined, sovereign-backed spread machine, catching a supply-constrained aviation cycle at a fortunate moment, throwing off record underlying cash flow, and carrying one enormous, unhedgeable question about the geopolitics of its own ownership. The operating story is about as clean as the leasing industry produces, and the management team has, so far, done what it said it would do. Whether that is enough for the decade ahead depends less on the company's execution, which has been excellent, than on whether the world stays open enough for a Chinese-owned, dollar-funded, globe-spanning lessor to keep quietly flying above the fray.

References

-

BOC Aviation Reports Record Underlying Profit for Full Year 2025 — BOC Aviation, 2026-03-19 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Fitch Affirms BOC Aviation's Credit Rating at 'A-' with Stable Outlook — Fitch Ratings, 2025-06-22 ↩↩↩

-

BOC Aviation Reports Robust Growth in First Half 2025 — BOC Aviation, 2025-08-21 ↩↩↩↩↩↩

-

Factbox — Aviation Lessor Settlements With Russia Over Trapped Planes — Insurance Journal, 2024-06-21 ↩

-

Aeroflot Group settles aircraft claims with lessor BOC Aviation — FlightGlobal, 2023-11 ↩

-

Aeroflot Group, BOC ink $208mn settlement over nine aircraft — ch-aviation, 2024-11 ↩

-

BOC Aviation Reports Record Profit for Full Year 2024 — BOC Aviation, 2025-03-13 ↩↩↩↩

-

BOC Aviation Reports Robust Growth in First Half 2025 — BOC Aviation, 2025-08-21 ↩↩↩↩↩↩

-

BOC Aviation delivers 51 aircraft in 2025, expands orderbook to 337 jets — Aviation24.be, 2026 ↩↩↩↩↩↩

-

Global Aircraft Lessors Benefit From Squeezed Fleet Supply and Record Lease Rates — Bloomberg, 2025-10-14 ↩

-

BOC Aviation Announces Steven Townend as Managing Director and Chief Executive Officer from 1 January 2024 — BOC Aviation, 2023-11-08 ↩↩↩↩↩

-

BOC Aviation places order for 70 Airbus A320neo family aircraft — Airbus Pressroom, 2025-07-28 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube