WuXi AppTec: The Operating System for Drug Discovery

I. Introduction: The "Amazon of R&D"

Picture the year 2000. A pharmaceutical chemist at Pfizer or Merck wants to test a new molecule. The process is almost medieval in its scale. He fills out an internal requisition. He waits weeks for an in-house team to synthesize the compound. He shares lab benches with hundreds of colleagues across a corporate campus the size of a small university. The all-in cost of bringing a single drug to market hovers above one billion dollars, and it takes ten to fifteen years. Drug discovery is the exclusive domain of giants—a world of glass towers in New Jersey, Connecticut, and Basel, where the only way to play is to already be enormous.

Now jump to today. A two-person biotech startup in Boston—maybe a former academic and a venture associate with a thesis on a particular kinase—signs a contract over a video call. Within weeks, a facility somewhere in Suzhou or Shanghai is synthesizing their candidate molecules at industrial scale. The same facility runs the toxicology, files the regulatory paperwork, and eventually manufactures the commercial product. The startup never owns a single beaker. They never hire a single chemist. They raise $30 million in Series A money and operate with the optionality of a company a hundred times their size.

That transformation—the unbundling of pharmaceutical R&D—did not happen by accident. It was engineered, deliberately, over twenty-five years, primarily by one company. Its name does not appear on any pill bottle. Its logo is not in any television commercial. But it is, by some measures, the most important infrastructure company in modern medicine.

WuXi AppTec employs more than 41,000 people. Its client roster includes essentially every meaningful pharmaceutical company on Earth—the top twenty global pharma firms are all customers. In 2024, it served over 6,000 active clients across more than thirty countries. Roughly one in every four small-molecule drugs cleared by the U.S. FDA in recent years has, somewhere in its supply chain, touched a WuXi facility. And yet, ask the average investor on Wall Street to name the company, and you will get a blank stare.

This is the story of how a chemist named Ge Li, returning home from a New Jersey research lab with a singular thesis about cost structure, built what amounts to the cloud infrastructure layer of the global pharmaceutical industry. We are going to walk through the business model they invented—the so-called CRDMO, for Contract Research, Development, and Manufacturing Organization. We are going to look at the audacious financial engineering that took them off the New York Stock Exchange in a $3.3 billion privatization and then re-floated them across two Asian exchanges into something that, at peak, carried over $60 billion in combined market value.

And we are going to confront the elephant in the room: the geopolitical avalanche now rolling down the mountain in the form of the U.S. BIOSECURE Act, a piece of legislation that has, in the span of eighteen months, transformed WuXi from the unquestioned leader of global pharma services into the central case study of de-risking from China.

This is, in many ways, the perfect Acquired episode. It has a brilliant founder. It has an industry-defining business model. It has a financial engineering masterstroke. It has a competitive moat made of human capital and regulatory paperwork. And it has an existential, narrative-bending threat. The most important company in healthcare that the average person has never heard of—and the company whose fate may now be decided as much in the U.S. Senate as in any laboratory.

Let us begin where most great company stories begin: with one person, one small room, and one heretical idea.

II. Founding & The "Succinct" Early Years

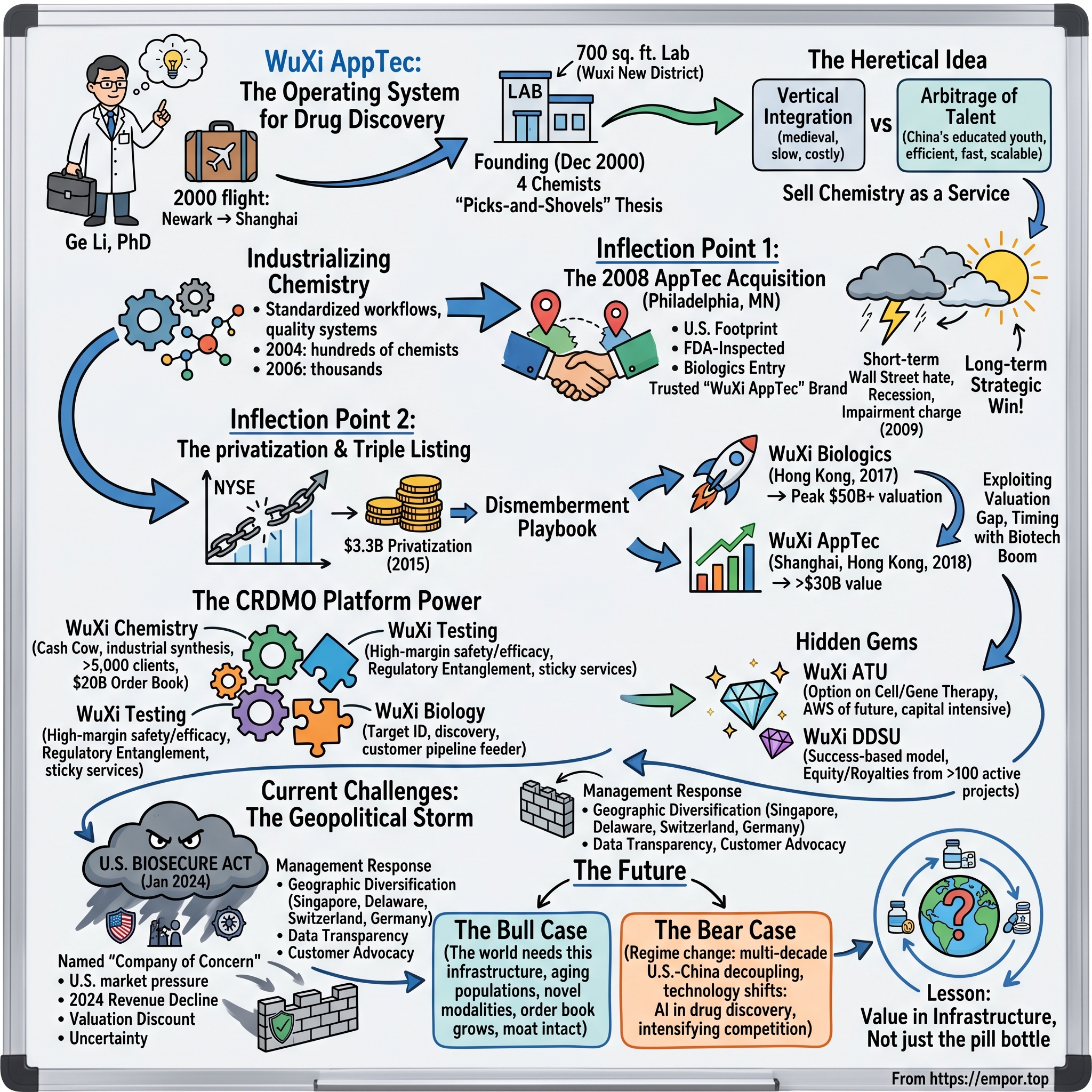

In December 2000, a thirty-three-year-old chemist named Ge Li boarded a flight from Newark to Shanghai. In his luggage were a few suits, a laptop, and the formative work experience of his career—several years at Pharmacopeia, a Princeton-area combinatorial chemistry firm that had captured the imagination of late-1990s biotech investors with the promise of industrializing molecule design. Ge Li had earned his PhD in organic chemistry from Columbia under the legendary Koji Nakanishi. He was, by any reasonable definition, a member of the global scientific elite.

He was also, increasingly, a man with a thesis that did not fit American pharmaceutical orthodoxy. At Pharmacopeia, he had watched as drug companies poured staggering sums into building captive chemistry teams. He had watched as those same teams worked at a pace dictated by the vacation schedules, real estate constraints, and middle-management politics of vast corporate research divisions. And he had begun to suspect that something fundamental was broken—that the pharmaceutical industry had confused vertical integration with competence, and that there was a vast and unexploited arbitrage hiding in plain sight.

That arbitrage was talent. China, in the year 2000, was in the early years of an enormous demographic and educational expansion. Tens of thousands of chemistry students were graduating from universities in Shanghai, Beijing, Tianjin, and Wuhan every year. Many of them had been trained in laboratories that, while not the equal of Harvard or MIT, were perfectly capable of executing the kind of bench chemistry that constituted the daily reality of drug discovery. And they were available at salary structures that, charitably, were a small fraction of what an equivalent chemist would cost in New Jersey.

Ge Li landed in Shanghai with his wife and a small group of co-founders, including a few colleagues from his Pharmacopeia days. He set up shop in a 700-square-foot lab in the Wuxi New District—a then-obscure development zone in Jiangsu Province whose name, by accident of geography, would become the company's brand. The team was four chemists, including Ge Li himself. The thesis, even in those earliest weeks, was crystal clear: do not build a drug company. Build the picks-and-shovels infrastructure that drug companies need. Sell chemistry as a service.

This was, at the time, a heretical idea. The dominant business model in pharmaceutical R&D was integration. Charles River Laboratories, founded in 1947, did some of this work, but largely in animal models and toxicology, not in the chemistry that lay at the heart of drug discovery. Covance, the other major Western contract research player, was similarly tilted toward clinical and preclinical services rather than the molecule-design front end. The chemistry itself was assumed to be the proprietary core that no serious pharma company would ever outsource.

Ge Li's bet was that this assumption was wrong, and that the right way to attack it was through a service model so disciplined and so reliable that it would be cheaper, faster, and ultimately better than the in-house alternative. The early years were a grind. The team took on small custom synthesis contracts—a few grams of this intermediate, a few hundred milligrams of that screening compound. They charged a fraction of what a U.S. CRO would charge. They turned around results in weeks rather than months. And they built, slowly, a reputation among Western biotech and pharma chemists as a place where things actually got done.

The early pivot, by most accounts, came around 2002 to 2003. The original concept had included some discussion of WuXi developing its own intellectual property—perhaps licensing molecules to larger players. Ge Li reportedly killed that idea. The conflict of interest was lethal. If WuXi was going to be the trusted partner of every major pharma firm, it could not simultaneously be a competitor. The pure-service model became the strategic constitution of the company, and it has never wavered.

By 2004, WuXi had several hundred chemists. By 2006, more than a thousand. The growth rate was almost exponential. And the company had begun to do something that the Western contract research industry had structurally failed to do: it had begun to industrialize chemistry. Workflows were standardized. Throughput was measured. Quality systems were built to FDA-grade specifications. The labor cost advantage was real—roughly one-fifth of comparable U.S. chemistry costs in the early years—but the more durable advantage was process. WuXi was iterating on the actual production of molecules at a pace that the Western incumbents, encumbered by legacy real estate and unionized lab staff, simply could not match.

In August 2007, less than seven years after that 700-square-foot start, WuXi PharmaTech listed its American Depository Shares on the New York Stock Exchange. The IPO raised roughly $185 million and valued the company at well over $1 billion. The "small chemistry shop in Wuxi" had, in less than a decade, become a publicly traded American company. And it was about to make a bet that would, in retrospect, define everything that came after.

III. Inflection Point 1: The 2008 AppTec Acquisition

In January 2008, Ge Li sat in a conference room in Philadelphia across from the management of AppTec Laboratory Services. AppTec was, at the time, a respectable but not glamorous American contract research firm headquartered in St. Paul, Minnesota, with operations in Philadelphia, Atlanta, and a few other locations. Its specialties were biologics testing, medical device validation, and the kind of regulated quality work that constituted the unglamorous backbone of FDA submissions. Revenue was modest by Big Pharma standards—roughly $69 million the prior year. Profitability was, by AppTec's own admission, recovering rather than thriving.

The deal that emerged from that room was, by every conventional metric of the time, expensive. WuXi PharmaTech paid $151 million in cash and stock for AppTec, representing roughly a 30% premium over recent comparable contract research transactions. This was the largest acquisition WuXi had ever attempted. It was funded with a combination of IPO proceeds and debt at a moment when global credit markets were beginning to seize. By the time the transaction closed in January 2008, Bear Stearns was weeks away from collapse, and the broader financial system was sliding toward the worst crisis since the Great Depression.

Wall Street, as Wall Street tends to do, hated it. WuXi's NYSE-listed shares fell sharply in the months following the announcement. The bear case was immediate and articulate: a Chinese chemistry shop had paid a premium for a sleepy American testing business at the worst possible moment in the credit cycle. The synergies were unclear. The integration risk was real. The cultural gap between a young Shanghai-based services company and a Minneapolis-based regulated lab business was enormous. And as the Great Recession deepened in late 2008 and 2009, AppTec's underlying business itself came under pressure. By early 2009, WuXi was forced to take an impairment charge against the acquisition, a public admission that the deal had not gone according to plan in its first year.

This is the moment where the conventional analysis stops. And it is where the Acquired analysis starts to get interesting. Because what looked, in 2009, like a financial blunder, in retrospect looks like one of the most strategically important transactions in the company's history.

Consider what AppTec actually gave WuXi. First, it gave them a U.S. footprint. Not a sales office. Not a token presence. A real, functioning, FDA-inspected operational presence on American soil, complete with biologics testing capabilities, medical device expertise, and a roster of U.S. clients who suddenly became cross-sell opportunities for the China-based chemistry business. Second, and more importantly, it gave them a brand. The company renamed itself WuXi AppTec. That single naming choice—putting an American name alongside the Chinese one—was an act of strategic positioning that paid dividends for the next fifteen years.

Because here is the central thing to understand about the global pharmaceutical industry: trust is the entire game. Pharma companies do not, under any circumstances, take risks on suppliers they do not implicitly trust. The cost of switching is too high. The regulatory consequences of a quality failure are too severe. The reputational damage of a recall is too painful. A Chinese contract research firm, in 2008, faced an enormous trust deficit. The AppTec acquisition was, in significant part, a purchase of trust. It transformed WuXi from "the cheap Chinese option" into "a global services partner with regulated U.S. operations."

The third thing the deal gave them, less obvious at the time, was an entry point into biologics. The pharmaceutical industry of 2008 was in the early stages of a structural shift away from small-molecule chemistry and toward biologic drugs—proteins, antibodies, and eventually cell and gene therapies. AppTec's biologics testing business was a foothold in a market that, over the subsequent decade, would grow into the largest single growth category in global pharma. Without that 2008 acquisition, WuXi's pivot into biologics in the 2010s would have been much harder, much slower, and possibly impossible.

By 2011 and 2012, the financial logic of the deal had reasserted itself. The integrated business was growing. The cross-sell was working. The brand had landed. And the impairment of 2009, in retrospect, looked less like a strategic failure and more like the predictable cost of buying a real asset at the wrong moment in a credit cycle. The strategic asset was intact.

The transaction also taught Ge Li something important about himself as a capital allocator. He had moved decisively, when the industry consensus was conservative. He had taken short-term pain in the form of an impairment without abandoning the long-term thesis. And he had used a moment of broader market distress to acquire something that, in a normal cycle, would have been priced beyond his reach. These would be the defining moves of the next chapter, when he made an even more audacious bet—this time, on the company itself.

IV. Inflection Point 2: The Privatization & The Triple Listing

By 2014, Ge Li had a problem that, on the surface, looked like an enviable one. WuXi PharmaTech was a profitable, growing, NYSE-listed company with annual revenues approaching $700 million and a market capitalization of around $2 billion. The business was throwing off cash. The client roster was the envy of the industry. By any conventional measure, the company was a success.

And yet, when Ge Li looked at the share price, he saw something that infuriated him. The market was valuing WuXi at a multiple consistent with a low-margin labor arbitrage business—something between a staffing agency and a low-end contract manufacturer. American investors, conditioned by years of skepticism toward U.S.-listed Chinese companies after a wave of accounting scandals at smaller firms, were applying a discount that bore no resemblance to the strategic position WuXi had built. The company was, Ge Li believed, being priced as a cost-saving service when it had become something fundamentally more valuable: a technology platform.

The decision he made next was one of the boldest in modern healthcare capital markets history. In April 2015, WuXi announced that a consortium led by Ge Li and including New G.P. Limited, Ally Bridge Group, Boyu Capital, Temasek, and Hillhouse Capital would take the company private at $46 per ADS, valuing the equity at approximately $3.3 billion. The transaction closed in December 2015. WuXi PharmaTech, after eight years on the New York Stock Exchange, went dark.

To understand the audacity of this move, you have to understand the playbook it implied. Ge Li was not taking the company private to keep it private. He was taking it private to break it apart and re-list the pieces on Asian exchanges, where investors—he believed—would understand the platform thesis and pay the multiple it deserved. This was financial engineering of a kind that, in healthcare, had essentially no precedent at this scale.

The dismemberment proceeded in stages over the following two and a half years. First, in June 2017, the company spun out its biologics business as WuXi Biologics, which listed on the Hong Kong Stock Exchange. The IPO was an instant sensation. WuXi Biologics opened trading at a market cap of roughly $4.5 billion. By 2018, that figure had crossed $10 billion. By the peak of the biotech bull market in 2021, WuXi Biologics carried a market capitalization above $50 billion in its own right.

Second, in May 2018, WuXi AppTec—the rump small-molecule chemistry, testing, and contract manufacturing business—listed on the Shanghai Stock Exchange. The Shanghai listing was massively oversubscribed; the shares more than tripled within their first weeks of trading. Then, in December 2018, WuXi AppTec completed its dual listing on the Hong Kong Stock Exchange under the ticker 2359.HK, raising additional capital and creating a fully convertible structure between the A-shares and H-shares.

The arithmetic, by the end of 2018, was breathtaking. A consortium that had paid roughly $3.3 billion to take WuXi private in 2015 was, three years later, sitting on a combined market capitalization across WuXi AppTec and WuXi Biologics that exceeded $30 billion. By the peak of the biotech cycle in mid-2021, that combined figure was well above $60 billion. This was, depending on how one measures, somewhere between a five-times and ten-times return in a span of half a decade—achieved not through operating performance alone, but through a deliberate exploitation of the valuation gap between American and Asian capital markets.

Two things made this work. The first was the sheer narrative quality of WuXi's positioning. Hong Kong and Shanghai investors, looking at a Chinese company providing critical infrastructure to the global pharmaceutical industry, did not see "labor arbitrage." They saw national champion. They saw the picks-and-shovels of biotech. They saw a story consistent with the broader narrative of Chinese industrial sophistication. The price-to-earnings multiple they were willing to pay was, in some periods, three to four times what U.S. investors had been paying for the same business.

The second was timing. The 2018 to 2021 window happened to coincide with one of the largest biotech bull markets in history. A wave of small biotech IPOs in the U.S., a flood of cheap capital into early-stage drug development, and the COVID-19 pandemic's acceleration of vaccine and therapeutic development all combined to push contract research demand to historic highs. WuXi's revenue in 2021 grew over 38% year-on-year. WuXi Biologics grew over 80% in some quarters. The numbers justified the multiple. For a moment, at least.

Ge Li's privatization-and-re-listing was, in retrospect, one of the most successful capital allocation moves in healthcare history. It demonstrated that a founder with conviction in his own asset, and a willingness to use cross-border capital markets as a strategic tool, could create enormous shareholder value without changing a single thing about the underlying operating business. The factories were the same. The chemists were the same. Only the listing venue had changed. And yet the value-creation was real, measured in tens of billions of dollars.

The cost of this maneuver, of course, was that WuXi AppTec became, structurally, a Chinese-listed company at the precise moment when being a Chinese-listed company was about to become a strategic vulnerability rather than a strategic asset. But that storm was still gathering. In the meantime, Ge Li had his platform, his multiple, and his capital. The next question was what to build with it.

V. The Business Units & "Hidden" Gems

Walk into a typical WuXi facility today—say, the massive small-molecule complex in Changzhou or the integrated campus in Wuxi itself—and what you see does not look like a research lab at all. It looks like a factory. Robotic synthesizers run twenty-four hours a day. Conveyor systems move trays of compounds between stations. Quality control technicians in cleanroom suits monitor data feeds on banks of screens. The aesthetic is closer to a semiconductor fab than to the chaotic, professor-driven academic chemistry labs that most people imagine when they think of drug discovery.

This industrial aesthetic is the visible expression of WuXi's central insight: that drug discovery, when subjected to engineering rigor, can be made to look much more like manufacturing than like research. And the company has organized its business units around that principle, each of them a different layer in what Ge Li and his team have begun calling, internally and externally, the CRDMO platform.

The CRDMO acronym—Contract Research, Development, and Manufacturing Organization—is itself worth pausing on. The traditional industry framework distinguished between CROs (Contract Research Organizations, which did discovery and clinical work) and CMOs (Contract Manufacturing Organizations, which made the final pills). WuXi's strategic insight was that this division was artificial, expensive, and slow. By integrating research, development, and manufacturing under a single roof and a single contractual relationship, they could compress timelines, reduce hand-off friction, and—most importantly—lock customers into a multi-year relationship that would be excruciating to unwind.

The largest single business unit, and the engine of cash flow, is WuXi Chemistry. This is the original business, scaled to industrial proportions. WuXi Chemistry serves more than 5,000 active customers globally and operates at a scale that simply does not exist anywhere else. Its order book at the start of 2024 stood at approximately $20 billion in committed future revenue, including a multi-billion-dollar GLP-1 weight-loss manufacturing contract that has been the subject of intense investor speculation. Chemistry contributed roughly three-quarters of WuXi AppTec's total revenue in 2024 and an even larger share of its operating profit. This is the cash cow. Without it, none of the other businesses would exist.

The second pillar is WuXi Testing, which combines safety and efficacy testing services with clinical trial support. This business, anchored partly in the assets acquired through AppTec back in 2008, is what Acquired listeners would recognize as the "sticky" services layer. Once a customer has its safety testing protocols validated at a specific WuXi facility, switching to another vendor involves not just signing a new contract but re-validating every protocol with the FDA, EMA, and other regulators. The switching cost is measured not in dollars but in years of regulatory delay. This is high-margin, high-retention work, even though it grows more slowly than chemistry.

The third pillar is WuXi Biology, which provides target identification, screening, and biology services—essentially, the front end of drug discovery. This is a smaller, faster-growing segment that serves both the platform's own integrated discovery customers and standalone academic and biotech clients. It is also the entry point through which most new biotech customers begin their relationship with WuXi: a startup typically engages WuXi Biology for a screen, then graduates to WuXi Chemistry for synthesis, and eventually to WuXi Testing and WuXi Manufacturing for the later stages.

But the most interesting parts of the business, from a long-term investment perspective, are the segments that most casual observers overlook. These are the "hidden" gems—businesses that are currently small, currently low-margin, and currently capital-intensive, but that represent options on entire categories of future medicine.

The first of these is WuXi ATU, the Advanced Therapies Unit. ATU is the company's bet on cell and gene therapy—the manufacturing of CAR-T treatments, viral vectors for gene therapy, and the next generation of personalized medicines. The economics of cell and gene therapy manufacturing are notoriously difficult. Each CAR-T treatment is, in some sense, a bespoke product made from a specific patient's own cells. The manufacturing infrastructure required is enormous, the regulatory complexity is extreme, and the unit economics, for now, are challenging. ATU has been a drag on WuXi AppTec's consolidated margins for several years.

But the strategic logic of ATU is impeccable. If cell and gene therapy delivers on its long-term promise—if, in fifteen or twenty years, a meaningful fraction of cancer treatment is a CAR-T variant and a meaningful fraction of rare-disease treatment is a gene therapy—then the contract manufacturing infrastructure for these modalities will be one of the most valuable categories in healthcare. WuXi ATU is positioning to be the AWS of that future. The company is, in effect, paying today for an option on tomorrow.

The second hidden segment is the DDSU, or Drug Discovery Services Unit. DDSU is among the most innovative business model experiments in the contract research industry. Rather than charging customers a flat fee for discovery services, DDSU operates on a success-based model: WuXi performs early-stage discovery work on behalf of a partner—often a smaller biotech or even an academic group—and in exchange takes an equity stake or a milestone-and-royalty share in any drug that reaches commercialization. WuXi, in effect, becomes part venture capitalist, part service provider.

The DDSU portfolio now includes more than 100 active projects, with several molecules in late-stage clinical trials. The first commercial royalties from DDSU drugs began flowing in 2023 and 2024, marking the long-awaited validation of a business model that took the better part of a decade to mature. If even a small fraction of DDSU's pipeline reaches blockbuster status, the segment could eventually contribute hundreds of millions of dollars in high-margin royalty income—a stream of revenue that bears no resemblance to the cost-plus economics of traditional contract research.

What makes the WuXi business architecture so powerful is not any single one of these units. It is the combination. A biotech customer who starts with a screening project in WuXi Biology can graduate, over a period of years, into chemistry, into testing, into clinical trial support, and ultimately into commercial manufacturing. By the time that customer has a marketed drug, they are bound to WuXi by dozens of regulatory filings, hundreds of validated protocols, and a level of operational dependence that simply cannot be replicated by any competitor in any reasonable time frame. This is what the Acquired playbook would call platform power. And it explains why, even amid the geopolitical storm of the past two years, the company's order book has continued to grow.

VI. Management & Ownership

If you have ever watched a Ge Li speech—and there are not many publicly available, because he is famously reserved with the press—you notice quickly that he does not sound like a typical CEO. He does not talk about market share or quarterly guidance. He talks about chemistry. He talks, with the precision of someone who has spent thirty years thinking about it, about reaction yields, about throughput, about the molecular complexity that distinguishes truly valuable medicinal chemistry from commodity work. The man on stage is, recognizably, still the chemist who landed in Shanghai in 2000 with a thesis and a laptop.

That continuity matters more than it might seem. Ge Li is one of the relatively rare cases in modern global business of a founder-CEO who has remained operationally engaged across more than two decades and through a complete transformation of his industry. He is not a hands-off chairman who has delegated to professional managers. He is, by all accounts of those who have worked with him, deeply involved in technical strategy, capital allocation, and the cultural architecture of the company.

Ge Li was born in 1967 in Anhui Province, in central China. His path is, in retrospect, almost archetypally that of the post-1978 Chinese scientific elite. Undergraduate work at Peking University. PhD in organic chemistry at Columbia. Postdoctoral work at the University of Cincinnati. Industrial experience at Pharmacopeia in New Jersey. By the time he returned to China at age thirty-three, he had absorbed the methodological rigor of American industrial chemistry and begun to see, with increasing clarity, the structural opportunity hiding in the cost differential between Chinese and Western scientific labor.

What is less well-documented, but consistently described by people who have worked with him, is his almost obsessive operational orientation. Ge Li is, by reputation, a man who reads the operational reports. Who walks the labs. Who personally interviews senior scientific hires. The "WuXi Way," as the internal culture is sometimes called, is recognizably his: high pressure, high efficiency, technically demanding, with a flat-ish reporting structure that more closely resembles a Silicon Valley engineering organization than a traditional pharmaceutical company. Bonuses are tied to throughput, error rates, and customer satisfaction metrics. Career progression is meritocratic in a way that is not always characteristic of either Chinese or pharmaceutical industry norms.

The ownership structure reflects the founder's continued centrality. Ge Li, together with his co-founders and family-related entities, controls approximately 20% of WuXi AppTec's outstanding shares—a large enough stake to ensure de facto strategic control, but small enough that the public float remains liquid and the company is, for practical purposes, governed as a publicly accountable enterprise. Institutional ownership is dominated by global asset managers including BlackRock, Vanguard, and a number of large Asian sovereign wealth and pension funds. Hillhouse Capital and Boyu Capital, the partners who supported the 2015 privatization, retain meaningful stakes through related vehicles.

The senior management team beneath Ge Li is, for the most part, a group of highly technical executives, many of them with Western pharmaceutical backgrounds. The CFO, Edward Hu, is a long-tenured executive who has steered the company through the privatization, re-listings, and most recently through the geopolitical turbulence of the BIOSECURE Act. Steve Yang, the chief operating officer, is a former Pfizer executive who joined WuXi in 2009 and has been instrumental in the operational scale-up of the past decade. The CEO of WuXi Biologics, Chris Chen, is similarly a Pfizer alumnus with deep biologics manufacturing expertise. The pattern across the senior team is consistent: technical credentials, multinational experience, and a willingness to operate at the scale and pace that Ge Li demands.

Compensation, for the senior team, is heavily weighted toward equity-based incentives—primarily restricted stock units that vest against multi-year revenue and return-on-equity targets. This is not a place where executives are paid for showing up. The sums involved are not, by U.S. CEO standards, extravagant—Ge Li himself takes a relatively modest base salary—but the equity participation has, over the past decade, made many of the senior team into significant individual shareholders. Their incentives are, in a meaningful sense, aligned with long-term shareholders.

The succession question, as is true of every founder-led company, is the question that most thoughtful long-term investors keep returning to. Ge Li is, as of this writing, fifty-eight years old. He has shown no public indication of stepping back, and the company's operational complexity—particularly the navigation of the BIOSECURE Act and the ongoing global capacity expansion—seems to demand his continued attention. The bench, however, is deep. Hu, Yang, and the CEOs of the various business units constitute a credible succession pipeline. The cultural risk of a founder transition is real, but it is not, on present evidence, imminent.

What is perhaps the most important thing to understand about WuXi's management is the cultural posture toward customers. The company has, from its earliest days, treated the customer relationship as the absolute fulcrum of its strategy. Confidentiality is taken with an almost religious seriousness. Conflicts of interest are policed obsessively. The decision, made in the early 2000s, to never compete with customers by developing proprietary drugs has been honored without exception. In an industry where trust is the most valuable currency, WuXi has accumulated, over twenty-five years, an enormous balance of it. That balance is not a line item on any financial statement. But it is, arguably, the most valuable asset the company owns.

VII. The Playbook: 7 Powers & 5 Forces

For a long-term investor trying to understand whether WuXi AppTec is a durable, defensible business or a temporary beneficiary of an arbitrage that may close, the most useful framework is Hamilton Helmer's Seven Powers. Helmer's argument—that durable competitive advantage comes from a small number of specific structural conditions—maps unusually well onto the WuXi story. Let us work through the powers that apply.

The first and most distinctive is Cornered Resource. WuXi's cornered resource is human: an enormous pool of highly trained Chinese chemistry, biology, and pharmaceutical PhDs that the company has assembled at a scale and at a cost structure that Western competitors simply cannot match. Some industry analysts have begun calling this the "Engineer Dividend"—the structural advantage that flows to any enterprise that can deploy world-class technical labor at a fraction of the Western cost. WuXi did not invent this dividend, but it has industrialized the harvest of it more effectively than any other company in pharmaceutical services.

The numbers are staggering. WuXi employs more than 41,000 people, the vast majority of them in China, and the majority of those are scientists with at least a master's-level technical training. The cost per scientist, even after years of wage inflation in tier-one Chinese cities, remains a fraction of the U.S. equivalent. And the supply pipeline is, if anything, deepening: China graduates more chemistry PhDs each year than any other country in the world. This is a cornered resource that took two decades to assemble and that no Western competitor can replicate without rebuilding the underlying educational system.

The second power, and perhaps the most important from a customer-retention perspective, is Switching Costs. Once a pharmaceutical customer files with the FDA using a specific WuXi facility as the manufacturing site for a particular molecule, the regulatory machinery closes around that arrangement like a vault door. Changing manufacturers requires a new filing, a new validation, often a new round of clinical comparability studies. Timelines for switching are typically measured in two to four years. For a marketed drug generating hundreds of millions of dollars in annual revenue, that is a non-starter. The customer is, for practical purposes, locked in for the life of the patent.

This is not a switching cost that WuXi imposes; it is a switching cost that the regulatory environment imposes on behalf of patient safety. But the company has, very deliberately, structured its commercial relationships to maximize the depth of these regulatory entanglements. Every additional protocol filed, every additional manufacturing process validated, every additional analytical method qualified deepens the lock-in. By the time a typical late-stage customer has been with WuXi for five years, the cost of disentanglement is essentially prohibitive.

The third power is Scale Economies, but with a twist. The conventional understanding of scale economies in pharmaceutical services would focus on the unit cost advantages of running a large facility. WuXi has those advantages in spades. But the more interesting scale story is what one might call the "long-tail" strategy. WuXi's enormous capacity allows it to serve thousands of small and mid-sized biotech customers that would be uneconomic for a smaller competitor. A large pharma customer might generate $100 million in annual revenue for WuXi; a small biotech might generate $500,000. Most contract research organizations cannot afford to take on the small biotech, because the customer-acquisition and onboarding costs swamp the revenue. WuXi can, because its enormous scale amortizes those costs across thousands of relationships.

This long-tail dynamic is, in turn, a forward feeder of large-customer relationships. The biotech that engages WuXi for a $500,000 discovery contract may, in five years, be a billion-dollar company with a marketed drug—and that drug will be manufactured at WuXi, because the relationship and the regulatory filings are already in place. The company has effectively positioned itself at the absolute earliest stage of the customer lifecycle, and it captures the value as customers grow.

The fourth power, less central but still meaningful, is Process Power. The operational discipline that WuXi has built over twenty-five years—the standardization of synthesis protocols, the throughput optimization, the integrated quality systems—is genuinely difficult to replicate. A new entrant cannot simply hire a few experienced managers and run the same playbook. The institutional knowledge is distributed across thousands of scientists and embedded in tens of thousands of standard operating procedures. This is a moat made of organizational learning, and it does not show up on any balance sheet.

Now turn to Porter's Five Forces, which provides the complementary view of industry structure. The most acute force, in WuXi's case, is the bargaining power of buyers. Big Pharma customers are massive, sophisticated, and price-sensitive. They negotiate hard, they multi-source where possible, and they have the in-house capability to take work back if they choose to. In a normal contract research market, this buyer power would be an enormous constraint on supplier margins.

WuXi has counteracted buyer power through the depth of its integration. By being the only realistic vendor that can take a customer from molecule design through clinical trial manufacturing and into commercial production—all under one quality system, one project manager, one contractual umbrella—WuXi has made itself harder to commoditize. The integrated relationship, once established, becomes the customer's path of least resistance, and the customer's negotiating leverage erodes accordingly.

The other forces are, on balance, favorable. The threat of new entrants is constrained by the capital intensity, the regulatory complexity, and the human-capital depth required to operate at WuXi's scale. The threat of substitutes—primarily, customers building or rebuilding in-house capacity—has been declining for two decades, as the economic logic of outsourcing has become increasingly compelling. Supplier power, in the form of laboratory equipment, raw materials, and specialty reagents, is moderate but manageable. Internal industry rivalry exists but is fragmented; no single competitor can match WuXi's breadth.

The single most important KPI to watch as a long-term investor in WuXi is the order book or backlog—specifically, the dollar value of contracted future revenue. This number tells you, with much greater accuracy than any quarterly revenue print, what the next two to three years of revenue will look like. The second most important KPI is the customer count, segmented by category. A growing count of small and mid-sized biotech customers indicates that the long-tail engine is still feeding. A flat or declining count of large pharma customers would be an early warning that the geopolitical narrative is biting harder than the order book suggests. These are the two numbers that, if you were limited to two, would tell you most of what you needed to know.

VIII. M&A Strategy & Benchmarking

In March 2021, WuXi Biologics announced the acquisition of OXGENE, a UK-based biotechnology firm specializing in viral vector and gene therapy technologies. The deal price was modest by big-pharma M&A standards—approximately $135 million in cash—but the strategic significance was substantial. OXGENE brought proprietary technologies for designing adeno-associated virus and lentiviral vectors, which are the delivery mechanisms at the heart of most modern gene therapies. The acquisition gave WuXi a meaningful presence in the UK gene therapy ecosystem and accelerated the buildout of the company's cell and gene therapy manufacturing capabilities.

The OXGENE deal is a useful illustration of the WuXi M&A philosophy, which differs in important ways from the pharmaceutical industry's general acquisition playbook. Big Pharma tends to do mega-deals: $50 billion acquisitions of clinical-stage companies, often justified by the late-stage pipeline of a single molecule. WuXi, by contrast, has consistently done smaller, technologically targeted acquisitions, each of which adds a specific capability to the platform. The OXGENE deal was not about acquiring revenue. It was about acquiring intellectual property, technology, and a team in a category—gene therapy vectors—where building from scratch would have taken years longer.

This pattern is consistent across the company's M&A history. The 2008 AppTec deal added U.S. testing capabilities and a regulated brand. A series of smaller acquisitions in the 2010s added specific service lines: drug product manufacturing, formulation development, advanced analytical capabilities. The 2017 acquisition of HD Biosciences in Shanghai added in vitro biology and target identification. Each transaction, taken individually, was modest. Cumulatively, they have built out the breadth of the platform with much lower execution risk than a single large acquisition would have entailed.

The benchmarking question—how does WuXi compare to its peers—is one of the most contested topics in the contract research investment community. The most relevant comparators are Lonza Group, the Swiss-headquartered contract development and manufacturing organization; Samsung Biologics, the South Korean biologics manufacturing specialist; Catalent, the U.S.-based drug development services firm acquired by Novo Holdings in 2024; and Charles River Laboratories, the original American CRO franchise.

On revenue, WuXi AppTec generated approximately RMB 39.2 billion (roughly $5.5 billion) in 2024, making it comparable in size to Lonza but smaller than the post-acquisition Catalent. On growth, WuXi has historically grown revenue in the 20% to 35% annual range, well above the typical 5% to 10% growth posted by Lonza and Charles River. On operating margin, WuXi sits in the upper range of the comparables, in the high twenties, despite the drag from its still-developing cell and gene therapy and DDSU segments.

Where WuXi diverges most sharply from its peers is on EV/EBITDA multiple. At the peak of the biotech bull market in 2021, WuXi traded at multiples north of 30x EBITDA, comparable to Samsung Biologics and well above Lonza. By early 2026, after the BIOSECURE Act overhang and the broader correction in biotech valuations, WuXi's EV/EBITDA multiple had compressed dramatically, trading at a meaningful discount to Lonza despite materially superior growth and margin profiles. This is, in some sense, the defining valuation puzzle of the company today: is the discount appropriate given geopolitical risk, or is it an overreaction that will normalize as the BIOSECURE situation clarifies?

The capital allocation framework that Ge Li and CFO Edward Hu have articulated is, by industry standards, unusually clear. Free cash flow from the mature businesses—primarily Chemistry and Testing—is reinvested in three categories: capacity expansion in existing businesses to support backlog growth, geographic diversification into Singapore, the United States, and Europe, and selective acquisitions to extend platform capabilities. Dividends have been modest. Share repurchases have been used opportunistically, particularly during periods of share price weakness driven by macro or geopolitical concerns. The company has been notably restrained in undertaking large strategic acquisitions, preferring to build organically wherever feasible.

One particularly notable capital deployment of the past two years has been the buildout of the Singapore campus. WuXi announced in early 2023 a multi-year, multi-billion-dollar investment in a new integrated services and manufacturing site in Singapore, with the explicit goal of providing customers with a non-China-based alternative for sensitive work. The Singapore campus is expected to become operational in stages from 2026 onward and represents, in many ways, the company's most important strategic insurance policy against the geopolitical risks discussed in the next section.

A second-layer diligence note worth flagging: the Singapore expansion, while strategically necessary, will be margin-dilutive in its early years. New facilities anywhere in the world, but especially in higher-cost jurisdictions like Singapore, take three to five years to reach mature utilization rates. Investors should not expect the Singapore investment to contribute meaningfully to operating profit before the late 2020s, and may see margin pressure in 2026 and 2027 as the capacity comes online ahead of the revenue.

Alongside Singapore, WuXi has expanded its U.S. footprint through investments in sites in Middletown, Delaware, and outside Philadelphia, and its European footprint through facilities in Couvet, Switzerland, and Leverkusen, Germany. The aim, articulated repeatedly in management commentary, is to be able to credibly tell any customer in any geography that their work can be performed at a non-China location if the customer's risk tolerance requires it. This is not a rhetorical commitment. It is being built, brick by brick, around the world.

Whether the geographic diversification is sufficient to defuse the geopolitical risk is the question that now dominates every conversation about the company. To understand that question, we have to confront the storm directly.

IX. Current Challenges: The Geopolitical Storm

In late January 2024, a previously obscure piece of legislation called the Biosecure Act was introduced in the U.S. Senate. The bill, in its original form, named several Chinese biotechnology companies—including WuXi AppTec and WuXi Biologics—as "companies of concern" and proposed to prohibit U.S. federal agencies, federal contractors, and recipients of federal funding from contracting with these named entities. It was, in effect, a piece of industrial sanctions legislation aimed directly at the largest contract research organization in the world.

The market reaction was immediate and brutal. WuXi AppTec's Hong Kong-listed shares fell more than 30% in the days following news of the legislation, and WuXi Biologics fell similarly. Tens of billions of dollars of combined market capitalization evaporated in the span of two weeks. Customer phone calls flooded into WuXi's commercial offices. Boards of directors at U.S. biotech firms suddenly demanded contingency planning for the loss of their primary contract research partner. The narrative around the company shifted, almost overnight, from "global platform leader" to "the central case study of U.S.-China decoupling in biotech."

To understand what happened, you have to understand both the substance of the U.S. concerns and the political dynamics that propelled the legislation. The substantive concern, as articulated by the bill's sponsors, was that contract research organizations like WuXi handle enormous volumes of sensitive intellectual property and biological data on behalf of their U.S. pharmaceutical customers. The bill's proponents argued that this data could, in principle, be subject to compulsory disclosure to the Chinese state under various Chinese national security and data laws. The concern, in its strongest form, was that critical pharmaceutical IP was being exposed to a foreign state actor.

WuXi has consistently and forcefully denied the underlying premise. The company has stated, repeatedly and in detailed regulatory filings, that it does not transfer customer data to the Chinese government, that it has implemented industry-standard data security and confidentiality protocols, and that the structure of its customer contracts contains explicit prohibitions on the kind of IP transfer that the bill's proponents allege. The company has not, on any public record, ever been credibly accused of an actual breach. The case against it, in the substantive sense, is largely speculative.

The political dynamics, however, are largely independent of the substantive merits. The BIOSECURE Act emerged at a moment of broad bipartisan consensus in Washington that the U.S. needed to reduce its strategic dependence on Chinese supply chains in critical industries—semiconductors, pharmaceuticals, critical minerals, advanced manufacturing. Once a piece of legislation acquires that kind of bipartisan momentum, the substantive arguments matter less than the political alignment. The bill passed the U.S. House of Representatives in September 2024 by a wide bipartisan margin. It stalled in the Senate through the end of 2024 and into 2025, but versions have been re-introduced in subsequent sessions, and the underlying political dynamic has not abated.

As of April 2026, the BIOSECURE Act has not been enacted into law in its original form. But the practical effect on WuXi's commercial position has been significant regardless. Several large U.S. pharmaceutical customers have begun, quietly, to move incremental work to non-WuXi vendors or to non-China WuXi facilities. New customer wins in the U.S. have slowed. The company's revenue from the U.S. market grew at a notably reduced pace in 2024 and 2025 compared to historical trend. The "China discount" in the company's valuation has become a permanent feature rather than a temporary anomaly.

Management's response has been threefold. First, geographic diversification, which we discussed in the previous section: the Singapore, U.S., and European campus investments are explicitly designed to give customers a non-China execution option. Second, customer engagement, including extensive direct outreach by Ge Li and the senior team to U.S. customers, regulators, and policymakers. Third, transparency around data security, including the publication of detailed white papers on the company's IP protection protocols and the commissioning of independent third-party audits.

The financial impact, to date, has been more visible in valuation than in operating results. Revenue in 2024 came in at RMB 39.2 billion, representing a year-over-year decline of roughly 2%, the first revenue decline in the company's history. Management attributed the decline to a combination of the BIOSECURE overhang, the unwinding of COVID-era manufacturing contracts, and the broader weakness in early-stage biotech funding that has reduced demand from small biotech customers. The order book, however, remained robust at over $48 billion in committed future revenue at year-end 2024, suggesting that the underlying customer relationships have not, in the main, been severed.

The most thoughtful analysis of the geopolitical risk, in the view of long-term investors, distinguishes between three scenarios. In the first scenario, the BIOSECURE Act or some equivalent passes in a form that materially restricts WuXi's access to the U.S. market. Revenue would compress meaningfully, but the company's geographic diversification would mitigate the worst outcomes, and the existing order book would provide a multi-year revenue cushion. In the second scenario, the legislation continues to languish or is enacted in a watered-down form that creates ongoing uncertainty without an outright ban. This appears to be the current trajectory, and the financial impact—a permanent valuation discount, a slower growth rate, but continued operational viability—is roughly what we are observing today. In the third scenario, the geopolitical environment normalizes, the legislation fails entirely, and WuXi's exceptional growth profile reasserts itself. This is the bull case, and it is not the consensus expectation, but it is also not implausible if the broader U.S.-China relationship shifts.

What is striking, in conversations with industry participants, is the degree to which WuXi's customers themselves have become advocates for the company. The Biotechnology Innovation Organization, the major U.S. industry trade association, has expressed concerns about the BIOSECURE Act's potential impact on the broader U.S. biotech ecosystem—the argument being that if you remove WuXi's services from the U.S. market overnight, you do not improve U.S. biotech competitiveness; you cripple it. The transition costs for U.S. biotech customers, in the form of delayed clinical trials and extended drug development timelines, would run into the tens of billions of dollars. This customer advocacy is not a guarantee of any particular legislative outcome, but it is a meaningful counterweight to the political pressure for action.

The company's central asset—its customer relationships—has not, on present evidence, been catastrophically damaged. The order book is intact. The customer count continues to grow. But the strategic landscape has changed permanently. WuXi will, for the foreseeable future, operate in a world where geopolitics is a first-order strategic variable rather than a background condition. That is the new reality, and the bull and bear cases must be assessed against it.

X. The Bull vs. Bear Case

The bull case for WuXi AppTec rests on a simple proposition: as long as humans want new medicines, the world needs the infrastructure that WuXi has built, and there is no credible alternative at scale.

Look at the underlying demand drivers. Global pharmaceutical R&D spending is projected to grow from approximately $260 billion in 2025 to over $350 billion by 2030. The aging populations of the developed world, the rising middle class of the emerging world, and the explosion of novel modalities—antibody drug conjugates, GLP-1 agonists, cell and gene therapies, RNA therapeutics—are all creating structural demand for the kind of integrated services that WuXi specializes in. The early-stage biotech funding environment has been weak in 2023 through 2025, but every credible long-term observer of the industry expects a recovery as interest rates normalize and as the next wave of novel mechanisms enters clinical development.

Within that demand environment, WuXi sits at the intersection of all the relevant secular trends. Its small-molecule chemistry business is benefiting from the GLP-1 boom, which has created multi-billion-dollar manufacturing contracts that will run for years. Its biologics affiliate is positioned for the structural shift toward antibody therapeutics. Its ATU business is the most credible pure-play option on the cell and gene therapy market. And its geographic diversification, while costly in the short term, is creating a hedge against the geopolitical risk that has compressed the multiple.

The Helmer power analysis, recall, identified four distinct sources of competitive advantage: cornered resource, switching costs, scale economies, and process power. None of these powers have been meaningfully eroded by recent events. The pool of Chinese chemistry talent is, if anything, growing. The regulatory switching costs around existing customer programs are unchanged. The scale economies of WuXi's manufacturing platform remain unmatched. And the process discipline, embedded in twenty-five years of organizational learning, is intact. Multiple compression has occurred, but moat erosion has not. For a long-term investor, this distinction is the entire story.

The bear case is different in character. It is not that WuXi is a fundamentally broken business. It is that the structural environment in which WuXi operates may be undergoing a one-way regime change, and that the company's historical advantages may, in the new regime, count for less.

The first bear pillar is geopolitics. The BIOSECURE Act, even in its current unenacted form, has demonstrated that U.S. policy can move suddenly and decisively against China-based suppliers in strategic industries. The bear argument is that this is not a passing storm but a structural shift, that the U.S. and China are entering a multi-decade period of strategic competition, and that any business model premised on Chinese cost arbitrage serving U.S. end markets is fundamentally exposed. Geographic diversification, in this view, is partial mitigation but not a solution: it costs money, it dilutes margins, and it may not be sufficient if U.S. policy moves toward broader restrictions on Chinese pharmaceutical engagement.

The second bear pillar is technological. The bull case for AI-driven drug discovery, which has exploded into pharmaceutical industry consciousness over the past three years, posits that the entire economics of medicinal chemistry may be on the verge of dramatic change. If AI models can predict molecular properties, optimize synthesis routes, and design novel chemical entities with much greater accuracy than human chemists, the demand for the "army of chemists" that constitutes WuXi's cornered resource may decline. The most pessimistic version of this argument suggests that within ten to fifteen years, drug discovery may require an order of magnitude fewer chemistry hours than it does today.

WuXi has, to its credit, invested aggressively in AI tools and in computational chemistry capabilities. The company would argue that AI augments rather than replaces its chemistry workforce, and that the integrated platform is, if anything, better positioned to deploy AI at scale than fragmented competitors. But the bear case has substance: a technological shift that materially reduces the value of human chemistry labor would, in the long run, undermine one of WuXi's foundational sources of competitive advantage.

The third bear pillar is industry structure. The contract research industry is becoming more competitive. Samsung Biologics has expanded aggressively in biologics. Lonza has invested billions in capacity. A wave of Indian contract research firms—Syngene, Aragen, and others—are positioning themselves as the preferred non-China alternatives. Even within China, WuXi faces increasing competition from peers like Asymchem and Pharmaron. The combination of geopolitical de-risking and aggressive competitor investment may erode WuXi's pricing power even in segments where the underlying demand remains strong.

The Porter's Five Forces analysis, applied with bear-case assumptions, reads differently than the bull case. Buyer power, in a world of intensified competition for non-China supply, becomes more acute. The threat of substitutes becomes more meaningful as customers actively cultivate alternative vendors. Internal industry rivalry intensifies as competitors scale into the markets WuXi has historically dominated. None of these forces is destructive on its own, but the cumulative effect could meaningfully compress the margin profile that has historically made WuXi such a compelling business.

The honest assessment, for a long-term investor, is that both the bull and bear cases have substance. The company's underlying competitive position remains strong. Its order book continues to grow. Its customer relationships, though stressed, have not fractured. At the same time, the geopolitical environment is genuinely hostile, the competitive set is genuinely intensifying, and the technological landscape is genuinely shifting. The valuation multiple compression of the past two years reflects, in some sense, an honest market reckoning with this changed environment.

The KPIs to watch—because they will tell you which case is winning—are not particularly mysterious. First, the order book. If contracted future revenue continues to grow, the customer base is voting with its checkbook that WuXi remains essential. If the order book begins to decline, the bear case is materializing. Second, U.S. revenue as a percentage of total revenue. If this percentage stabilizes or recovers, geopolitics is being managed. If it declines persistently, the geopolitical risk is materializing. Third, operating margin. If margin holds in the high twenties despite the geographic diversification spending, operational excellence is intact. If margin compresses below the mid-twenties on a sustained basis, either the cost base is rising or pricing power is eroding. These three numbers, taken together, will tell most of the story over the next three to five years.

XI. Epilogue & Playbook Lessons

There is a moment, in every great Acquired episode, where the hosts step back from the granular operational and financial detail and ask the larger question: what was the founding insight that made this company possible, and what does its trajectory tell us about how value gets created in the modern economy?

For WuXi AppTec, the founding insight was deceptively simple. Ge Li looked at the pharmaceutical industry of the late 1990s and saw an industry that had vertically integrated for the wrong reasons. Drug companies owned their chemistry teams not because internal chemistry was strategically essential, but because there was no credible alternative. The captive model was a default, not a choice. And captive models, in industries where the captive function is not actually a source of competitive advantage, are always vulnerable to disaggregation.

What WuXi did, over the subsequent twenty-five years, was create the credible alternative. It built a chemistry platform that was, on every measurable dimension, faster, cheaper, and more flexible than the captive alternative. It then extended that platform into testing, into biology, into manufacturing, into cell and gene therapy. At each step, the offer to customers was the same: stop owning the function. Let us own it for you. Free up your capital and your management attention for the things that actually matter—the molecules, the clinical strategy, the commercial execution.

This is, structurally, the same playbook that Amazon Web Services ran on enterprise IT, that Foxconn ran on consumer electronics manufacturing, that Taiwan Semiconductor Manufacturing Company ran on chip fabrication. In each case, an incumbent industry operated on the assumption that a particular function had to be owned in-house. In each case, a focused outsider built a platform that proved the assumption wrong. And in each case, once the platform was built, the disaggregation became irreversible. No serious cloud-native startup today builds its own data centers. No serious consumer electronics brand today builds its own assembly lines. And no serious modern biotech startup today builds its own chemistry team. The captive model has been outcompeted, structurally and permanently, by the platform model.

WuXi did not just sell chemistry. It sold time. The most precious resource in pharmaceutical research is not capital and not even talent; it is the calendar. Every month that a drug spends in development is a month closer to patent expiry, a month later to market, a month longer that patients wait for treatment. WuXi's central value proposition, beneath all the technical detail, was that customers who used its platform could get to clinical trials faster than customers who did not. In an industry where each successful drug represents a window of patent-protected revenue measured in years, the compression of timelines is worth far more than the cost savings on the chemistry itself. This is why the customer relationships, once established, have proven so durable. WuXi was not selling commodity service; it was selling the most valuable resource in the customer's economic universe.

The democratization implication of this platform is, in many ways, the most consequential part of the WuXi story. Twenty-five years ago, drug discovery was the exclusive domain of large pharmaceutical companies because only large pharmaceutical companies could afford the captive infrastructure required. Today, a two-person biotech startup can credibly attempt to discover a drug, raise venture capital around the attempt, and reach clinical proof-of-concept without ever owning a laboratory. That shift has produced an explosion of biotech innovation, an expansion of the medicines pipeline, and a structural change in the industrial organization of pharmaceutical research that we are only beginning to understand. WuXi did not produce this shift by itself, but no other single company contributed more to it.

What is the larger lesson for thoughtful long-term investors? Perhaps it is this: the most valuable companies of the modern era are often not the companies that make the consumer-facing products. They are the companies that build the infrastructure that everyone else depends on. The cloud, the chips, the assembly lines, the chemistry. These businesses are quieter, less glamorous, and harder to understand than the consumer brands that capture popular attention. But they are, in many ways, the more durable franchises. They benefit from secular tailwinds in the industries they serve. They accumulate switching costs that protect their relationships. They build process advantages that compound over decades. And, when they reach sufficient scale, they become close to irreplaceable.

The WuXi story, at this moment in early 2026, is unfinished. The geopolitical challenges are real and may intensify. The competitive landscape is more crowded than it has ever been. The technological shifts in AI-driven discovery may, in the long run, require a meaningful reimagining of the underlying business model. None of this is small. The company that emerges from the next five years may look meaningfully different from the company that exists today.

But the underlying franchise—the platform, the customer relationships, the cornered resource of human capital, the regulatory switching costs, the institutional learning embedded across thousands of standardized protocols—is intact. The Acquired playbook, applied to WuXi AppTec, returns a company that built one of the most powerful infrastructure positions in modern healthcare, that exploited a generational arbitrage in cross-border capital markets to extract enormous shareholder value, and that now faces, with characteristic operational discipline, the most serious external challenge of its history.

There is a phrase in the Chinese pharmaceutical industry that captures, perhaps better than any Western framework, what Ge Li built. Ren cai—talent—is the foundation of any scientific enterprise. Pingtai—platform—is the architecture that transforms talent into compounding value. WuXi AppTec is, fundamentally, a story about the deliberate construction of pingtai on top of the systematic mobilization of ren cai. Whether that construction proves durable in a more hostile geopolitical environment is the question of the next decade.

For now, twenty-five years after Ge Li boarded that flight from Newark with a thesis and a laptop, the most important infrastructure company in modern medicine continues to operate at industrial scale across three continents, serving thousands of customers, processing millions of compounds, and quietly enabling an enormous fraction of the new medicines that the world will see in the coming decade. The most important company in healthcare that the average person has never heard of remains, on present evidence, very much itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube