Dah Sing Banking Group: The Last Independent Fortress of Hong Kong

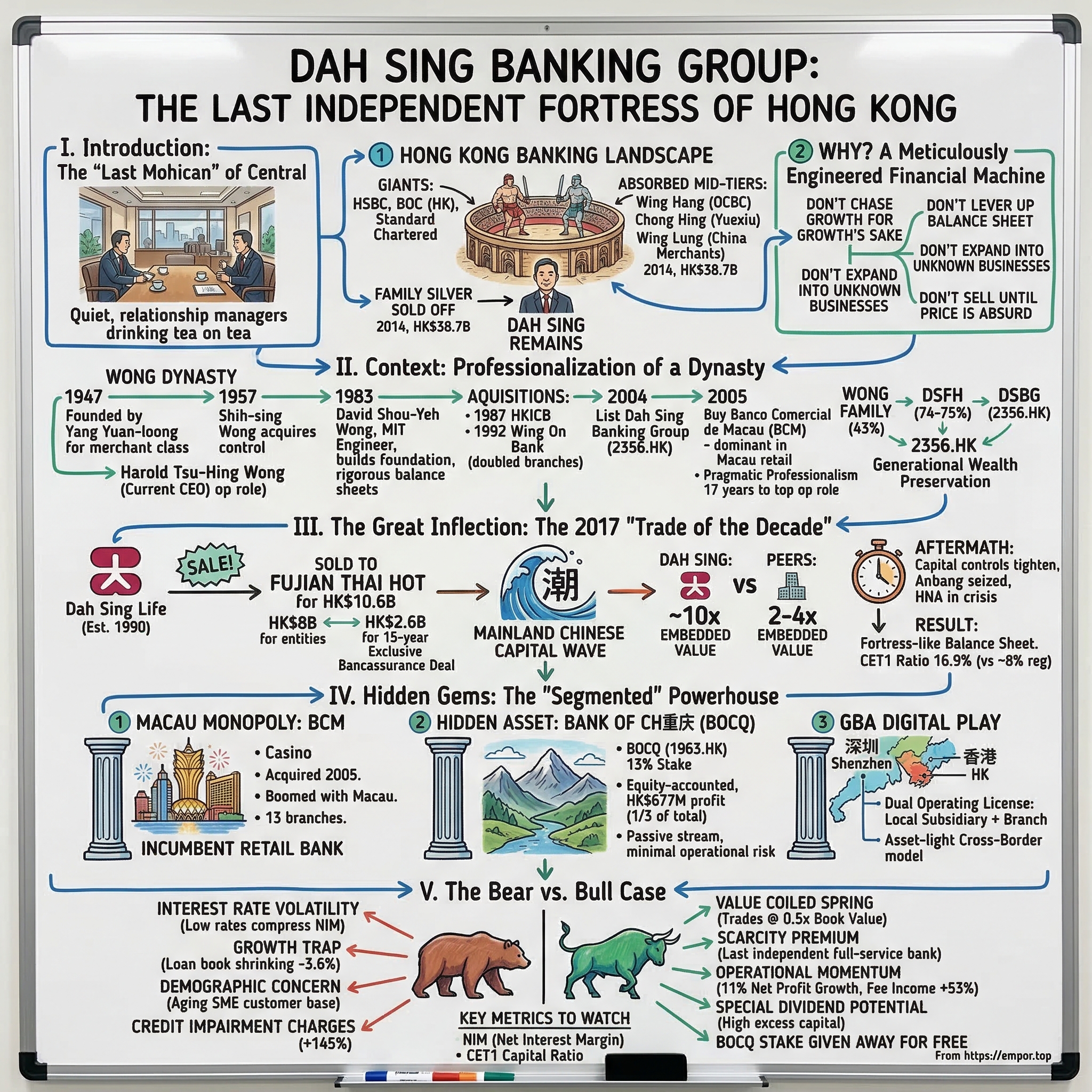

I. Introduction: The "Last Mohican" of Central (00:00 – 08:00)

Walk into the gleaming lobby of Dah Sing Financial Centre in Wan Chai — the bank's new headquarters, opened in 2021 — and you will notice something immediately different from the towering palaces of HSBC or Standard Chartered a few blocks away. There are no crowds. No tourist queues at the ATMs. No line of retail customers stretching to the door. Instead, there is a quiet, deliberate calm. A handful of relationship managers sit with clients over tea. The building itself is sleek but understated, much like the institution it houses. This is a bank that has spent nearly eight decades perfecting the art of being invisible — and profiting enormously from it.

Hong Kong's banking landscape is, on the surface, a gladiatorial arena. Three giants — HSBC, Bank of China (Hong Kong), and Standard Chartered — control the lion's share of deposits, mortgages, and corporate lending. Below them, a cluster of mid-tier local banks have, one by one, been absorbed into larger entities over the past two decades. Wing Hang Bank fell to Singapore's OCBC in 2014 for HK$38.7 billion. Chong Hing Bank was swallowed by Guangzhou's Yuexiu Financial Holdings the same year. Wing Lung Bank went to China Merchants Bank back in 2008. Each sale followed a familiar script: the founding family decides the next generation isn't interested, or that the regulatory burden is too heavy, or that the premium being offered is simply too juicy to refuse. And so, one by one, the "family silver" of Hong Kong banking was sold off.

Yet Dah Sing remains. It is, by most measures, the last truly independent, family-controlled, full-service commercial bank headquartered in Hong Kong. And the question that animates everything about this story is deceptively simple: why?

The easy answer is that the Wong family — now in its third generation of control — simply doesn't want to sell. But the deeper answer is far more interesting. Dah Sing Banking Group, listed on the Hong Kong Stock Exchange under ticker 2356.HK, is not just a survivor. It is a meticulously engineered financial machine built on a philosophy that runs counter to nearly every instinct in modern banking: the belief that the best thing a bank can do, in most environments, is nothing at all. Don't chase growth for growth's sake. Don't lever up the balance sheet to goose returns on equity. Don't expand into businesses you don't understand. And above all, don't sell — until the price is so absurd that only a fool would say no.

That last principle was demonstrated in spectacular fashion in 2017, when Dah Sing sold its life insurance subsidiary for HK$10.6 billion to a Chinese conglomerate at a valuation so rich it made the entire Hong Kong insurance industry do a double-take. It was the most expensive insurance transaction in Hong Kong history, executed at the absolute peak of the mainland Chinese outbound capital wave. The proceeds transformed Dah Sing's already-strong balance sheet into one of the most over-capitalized banking entities in Asia — a CET1 capital ratio of 16.9% as of the most recent filing, compared to a regulatory minimum of roughly 8%, meaning the bank holds more than twice the capital regulators require.

Today, Dah Sing Banking Group operates roughly 64 locations across Hong Kong, Macau, and mainland China. Its market capitalization sits at approximately HK$17 billion — a fraction of its HK$33.8 billion in total equity book value. That means the stock trades at roughly half of book value. For context, if you could buy every share of Dah Sing at today's price, you'd be acquiring HK$256 billion in total assets — including a pristine Hong Kong loan book, a dominant Macau retail bank, and a strategic stake in a major mainland Chinese bank — for the price of a mid-range Hong Kong apartment tower.

The thesis of this deep dive is straightforward: Dah Sing isn't just a bank. It is a masterclass in counter-cyclical capital harvesting — buying when others are panicking, selling when others are euphoric, and hoarding capital in the interstitial periods when everyone else is reaching for yield. It is the story of a family that understood, long before it became fashionable, that in banking, the ultimate competitive advantage isn't growth. It's survival.

II. Context: The Professionalization of a Dynasty (08:00 – 18:00)

The origin story of Dah Sing Bank begins on May 1, 1947, in a Hong Kong that barely resembled the gleaming financial capital it would become. The city was still recovering from Japanese occupation. The banking sector was rudimentary. A group of local entrepreneurs, led by Yang Yuan-loong, established the bank to serve the emerging merchant class — traders, small manufacturers, and importers who needed a Chinese-owned institution they could trust. The name itself, "Dah Sing," translates roughly to "great prosperity" — an aspiration as much as a description.

The bank's early years were unremarkable. It was one of dozens of small Chinese banks jostling for position in post-war Hong Kong. The pivotal moment came a decade later, in 1957, when businessman Shih-sing Wong acquired the controlling interest. This was the beginning of the Wong dynasty, and it established a pattern that would repeat itself across three generations: a single family acquiring control of a mid-tier institution and then, with extraordinary patience, building it into something far more valuable than its size would suggest.

Shih-sing Wong's son, David Shou-Yeh Wong, took the reins as Chairman in 1983, and it is under David's stewardship that the modern Dah Sing was truly forged. David is a fascinating figure — an MIT-educated engineer who brought a quantitative rigor to banking that was unusual for his era and his market. Where many Hong Kong bank chairmen of his generation were deal-makers and networkers, David was a builder. He understood balance sheets the way an architect understands load-bearing walls: every number had to carry its weight, and nothing extraneous was tolerated.

Under David's leadership, Dah Sing executed a series of acquisitions that quietly doubled the bank's scale without ever stretching its resources. In 1987, the bank acquired Hong Kong Industrial and Commercial Bank, and the parent entity, Dah Sing Financial Holdings (DSFH), was listed on the Hong Kong Stock Exchange under code 440. In 1992, the acquisition of Wing On Bank and its 16 branches effectively doubled the branch network overnight. These weren't glamorous deals. They didn't make front-page news. But each one was executed at a disciplined price, integrated cleanly, and immediately accretive to the group's franchise.

In 2004, the group carved out its banking operations into a separately listed entity — Dah Sing Banking Group Limited (2356.HK) — giving investors direct access to the core banking business while the parent DSFH retained its broader financial services portfolio. A year later came perhaps the most strategically significant acquisition of them all: Banco Comercial de Macau (BCM), purchased from Portugal's Banco Comercial Portugues. This gave Dah Sing a dominant position in the Macau retail banking market — a franchise that would prove remarkably valuable as Macau's economy boomed alongside its casino industry.

But if David Wong built the foundation, it is his son Harold who represents the professionalization of the dynasty — the transition from "founder's instinct" to "institutional competence" that is the make-or-break moment for every family-controlled enterprise.

Harold Tsu-Hing Wong is, by all accounts, an unusual banker. Educated in law at King's College London and in business at Harvard Business School, he joined Dah Sing Bank in 2000 — not through the front door of the chairman's office, but through the operational trenches. He was appointed Executive Director in 2005, Vice Chairman in March 2010, and finally Managing Director and CEO of Dah Sing Bank in August 2017. That timeline is worth noting: it took Harold seventeen years to ascend to the top operational role, an eternity by the standards of family-business succession in Asia, where sons and daughters are often parachuted into corner offices within months of graduating.

Harold's management philosophy can be summed up in a phrase that would make most growth-oriented investors cringe: pragmatic professionalism. He doesn't chase league table rankings. He doesn't announce grand five-year transformation plans. He doesn't give keynote speeches at Davos. In 2013, he was named Executive of the Year at the Hong Kong Business Awards — a recognition that came not for any single bold stroke but for the quiet accumulation of competence across lending, risk management, and customer relationships.

The incentive structure matters enormously here. David Wong's family holds approximately 43% of Dah Sing Financial Holdings, which in turn controls roughly 74-75% of Dah Sing Banking Group. This is not a situation where management owns a token 0.5% stake and is playing with other people's money. The Wongs are, in effect, managing their own family's single largest asset. Every loan approved, every risk taken, every acquisition considered is filtered through the lens of generational wealth preservation. It is the difference between a renter and a homeowner: the homeowner fixes the roof before it leaks.

This matters because it inoculated Dah Sing against the "empire building" trap that destroyed so many of its mid-tier peers. When Chong Hing Bank expanded aggressively into mainland China lending in the early 2010s, racking up credit losses that eventually contributed to its sale, Dah Sing held back. When Wing Lung Bank stretched for yield in its investment portfolio, Dah Sing stayed conservative. The pattern is unmistakable: at every junction where peers reached for growth, the Wongs chose restraint. Not out of timidity, but out of a deeply ingrained understanding that in banking, the institution that survives the cycle is the institution that wins.

David Wong, now approximately 84 years old, remains Executive Chairman. Harold, in his mid-fifties, runs day-to-day operations. The generational handshake between founder and successor is still in progress, and how it resolves — whether David eventually steps back fully, whether Harold's eventual successors have the same instincts — is one of the most important variables in Dah Sing's long-term story.

III. The Great Inflection: The 2017 Thai Hot "Trade of the Decade" (18:00 – 35:00)

To understand why the sale of Dah Sing Life deserves the label "trade of the decade," you first need to understand the market environment that made it possible.

In 2015 and 2016, a tidal wave of mainland Chinese capital was crashing over Hong Kong's financial sector. Chinese insurers, flush with cash from a booming domestic market and under pressure to diversify internationally, were desperate for Hong Kong footholds. The logic was straightforward: Hong Kong insurance policies denominated in US dollars or Hong Kong dollars offered Chinese consumers a way to diversify out of the renminbi, access international investment returns, and — not incidentally — move capital offshore in a period of rising anxiety about the Chinese economy. Mainland visitors were crossing the border in droves to purchase Hong Kong insurance policies, and the premiums flowing into Hong Kong-based life insurers were growing at extraordinary rates.

This created a seller's market of historic proportions. Chinese conglomerates — many of them real estate developers, investment firms, and industrial groups with no prior insurance experience — were bidding aggressively for any Hong Kong insurance platform they could find. Prices detached from fundamentals. Valuations that would have been considered absurd two years earlier became table stakes. The embedded value of a life insurance book — essentially, the present value of future profits from existing policies — was being marked up to levels that veteran insurance executives found bewildering.

Dah Sing had established its life insurance arm, Dah Sing Life Assurance, in 1990. Over 26 years, it had grown into a respectable mid-tier insurer, deeply integrated with the bank's distribution network. For most family-owned banking groups, the insurance subsidiary would have been considered part of the permanent furniture — a steady fee generator that complemented the core lending business. Selling it would be like selling the family silver.

Unless, of course, someone offered you ten times what the silver was worth.

On June 2, 2016, Dah Sing announced the sale of Dah Sing Life Assurance Company and its Macau insurance subsidiary to Fujian Thai Hot Investment — later renamed Tahoe Investment Group — for a total consideration of HK$10.6 billion in cash. The deal structure was elegant in its construction. Fujian Thai Hot paid approximately HK$8 billion for the insurance entities themselves. Separately, Dah Sing Life and Macau Insurance Company paid HK$2.6 billion back to the banking group in exchange for 15-year exclusive bancassurance distribution agreements. In other words, Dah Sing sold the insurance business but retained the right to distribute insurance products through its branch network for a decade and a half — keeping the fee income while shedding the capital requirements and underwriting risk.

The valuation was staggering. Industry observers estimated the sale price at roughly 10 times the embedded value of the insurance book — a multiple that was, at the time, an industry outlier. To put this in context, typical insurance M&A transactions in Hong Kong at the time were closing at 2-4 times embedded value. Dah Sing got more than double the high end of the range.

The deal closed on June 19, 2017. The insurance business was rebranded as Tahoe Life. And Dah Sing Banking Group was suddenly sitting on a mountain of cash that would transform its balance sheet for years to come.

The timing, in retrospect, was almost eerily perfect. Within months of the deal closing, the Chinese government began aggressively tightening capital controls, cracking down on the very outbound investment flows that had fueled the buying frenzy. Anbang Insurance — one of the most aggressive mainland acquirers — was seized by Chinese regulators in early 2018. HNA Group, another serial acquirer, spiraled into a debt crisis. The window of mainland Chinese capital flooding into Hong Kong insurance assets didn't just close; it slammed shut.

Dah Sing had sold at the absolute peak. Not because they had a crystal ball, but because they understood a principle that is easy to articulate and extraordinarily difficult to execute: when someone offers you a price that is far above intrinsic value, you take it. You don't agonize about the growth you might be leaving on the table. You don't worry about what analysts will say about your "shrinking" revenue base. You take the cash, say thank you, and wait for the next opportunity.

The proceeds didn't disappear into some ill-conceived acquisition spree. A special dividend was paid to shareholders. The remainder was deployed to strengthen the bank's capital base and fund its ongoing operations. The banking group's capital adequacy ratios, already strong, became fortress-like. By the most recent filing, the CET1 ratio stood at 16.9% and the total capital adequacy ratio at 21.0% — numbers that place Dah Sing among the most over-capitalized banks in the Asia-Pacific region.

In 2023, the original 15-year bancassurance deal with Tahoe Life was replaced by a new exclusive partnership with Sun Life — the Canadian insurance giant — extending the arrangement for another 15 years. Dah Sing had essentially sold the insurance manufacturing business at a generational peak, retained the distribution economics, and then renegotiated the distribution deal with a stronger, better-capitalized partner. The entire sequence, viewed end-to-end, is a clinic in value extraction.

This single transaction redefined Dah Sing's financial profile and set the stage for everything that followed — a banking group with more capital than it knows what to do with, trading at half its book value, waiting patiently for the next dislocation.

IV. Hidden Gems: The "Segmented" Powerhouse (35:00 – 50:00)

Most investors who glance at Dah Sing see a mid-tier Hong Kong bank. That's like looking at an iceberg and seeing only the tip. Beneath the surface of the core Hong Kong lending business are three distinct assets that, if properly understood and valued, fundamentally change the calculus of what this group is worth.

The Macau Monopoly: Banco Comercial de Macau

When Dah Sing acquired Banco Comercial de Macau from Portugal's Banco Comercial Portugues in December 2005, the deal barely registered on most investors' radar. Macau was still primarily known as a sleepy former Portuguese colony that happened to have some casinos. The territory's GDP was a rounding error compared to Hong Kong's.

What followed was one of the most dramatic economic transformations in modern Asian history. Macau's gaming revenue exploded from about US$5.6 billion in 2005 to a peak of over US$45 billion in 2013, making it the single largest gambling market on Earth — seven times the size of the Las Vegas Strip. And while the casino operators captured the headlines and the tourist dollars, someone had to bank the territory. Someone had to hold the deposits of the tens of thousands of workers who flooded into Macau to staff the hotels, restaurants, and gaming floors. Someone had to finance the infrastructure — the bridges, roads, and residential developments — that supported the boom. That someone, in large part, was BCM.

Today, BCM operates 13 branches and self-service banking centres across Macau, Taipa, and Coloane. It is one of the leading locally incorporated banks in the territory, offering the full spectrum of commercial banking services: deposits, credit cards, foreign exchange, securities trading, trade finance, wealth management, and insurance distribution. It is supervised by the Monetary Authority of Macao (AMCM) and led by CEO Pak-Hung Lau.

The strategic value of BCM extends beyond its current profitability. Macau's economy is diversifying beyond gaming — the government has been pushing aggressively into conventions, tourism, and fintech — and BCM is positioned as the incumbent retail bank for that transition. More importantly, Macau's integration into the Greater Bay Area economic zone means BCM serves as Dah Sing's natural bridge between Hong Kong and mainland China, handling cross-border payments, trade finance, and wealth management flows that are only going to grow as the GBA matures.

The Hidden Asset: Bank of Chongqing

If BCM is the hidden gem that savvy investors eventually discover, the Bank of Chongqing stake is the one that most never even look for.

Dah Sing Bank acquired a strategic shareholding in Bank of Chongqing (BOCQ, listed on the Hong Kong Stock Exchange under code 1963.HK) in 2006-2007, initially taking a 17% position. Over time, through dilution from subsequent share issuances by BOCQ, the stake has come down to approximately 13%. It is accounted for as an associate under the equity method — meaning Dah Sing records its proportional share of BOCQ's profits in its income statement but doesn't consolidate BOCQ's full balance sheet.

This accounting treatment has a practical consequence: most retail investors, and even some institutional analysts, effectively ignore the BOCQ stake when valuing Dah Sing. It shows up as a single line item — "share of profits of associates" — buried in the middle of the income statement. In fiscal 2024, that line item was HK$677 million. Not a trivial number — it represented roughly a third of Dah Sing Banking Group's total net profit.

Think about what this means. Dah Sing owns a meaningful stake in a mid-tier Chinese bank with a presence across the Chongqing municipality — one of China's fastest-growing economic regions — without bearing any of the direct operational risk of running hundreds of branches in mainland China. No regulatory headaches with the PBOC. No direct credit exposure to the Chinese property market. No need to hire thousands of mainland staff. Just a passive, equity-accounted stream of profits that shows up every quarter like clockwork.

There was a period, particularly during 2022-2023, when the Bank of Chongqing investment required meaningful impairment charges — reflecting concerns about Chinese banking sector asset quality amid the property downturn. But in fiscal 2024, impairment losses on the associate collapsed by 97% year-on-year to just HK$16 million, suggesting the worst of the write-down cycle may be behind them. In the first half of 2025, BOCQ contributed HK$443 million in profit — a healthy annualized run rate.

The GBA Digital Play

The third hidden asset is less tangible but potentially the most transformative: Dah Sing's positioning in the Greater Bay Area.

In a move that attracted relatively little attention, Dah Sing Bank became the first foreign bank in mainland China to be granted a "dual operating license." This means it can simultaneously operate a locally incorporated wholly-owned subsidiary — Dah Sing Bank (China) Limited, established in Shenzhen in 2008 — and a local branch under its Hong Kong parent license. The practical significance is that Dah Sing can offer a full range of RMB lending, deposit, and remittance services to corporate customers in the GBA without the capital and regulatory burden of building out a massive mainland branch network.

This is the "asset-light" model applied to cross-border banking: minimal brick-and-mortar investment, maximum optionality on cross-border wealth management and trade finance flows. The bank co-publishes an annual Greater Bay Area Industry Development Index with Our Hong Kong Foundation, positioning itself as a thought leader in GBA economic integration. It runs SME support programs, online seminars, and research surveys focused on helping Hong Kong businesses navigate mainland opportunities.

The GBA strategy is still early-stage, and its financial contribution to the group is modest. But it represents exactly the kind of patient, low-cost positioning that has characterized Dah Sing's approach throughout its history: plant the flag early, invest modestly, build relationships, and wait for the opportunity to scale when the economics are right. If cross-border wealth management between Hong Kong and the mainland accelerates — and most observers believe it will — Dah Sing will already be there.

Taken together, these three assets — BCM's Macau franchise, the Bank of Chongqing equity stake, and the GBA digital positioning — represent a geographically diversified, capital-light exposure to three of the most important economic corridors in southern China. None of them require significant incremental capital. None of them carry the operational complexity of running a mainland Chinese bank branch network. And none of them are fully reflected in Dah Sing's stock price.

V. The 7 Powers Analysis (50:00 – 1:05:00)

Hamilton Helmer's "7 Powers" framework identifies the durable sources of competitive advantage that allow a business to sustain superior returns over time. Applied to Dah Sing Banking Group, three of the seven powers are particularly relevant — and they explain why this seemingly unexciting mid-tier bank has survived when so many of its peers have been absorbed.

Switching Costs: The Relationship Lock-In

In consumer banking, switching costs are notoriously low. A retail depositor can open a new savings account at HSBC in thirty minutes on a smartphone. But Dah Sing's core franchise isn't built on retail depositors queuing at ATMs. It is built on relationships with Hong Kong's small and medium enterprise community — the traders, manufacturers, property owners, and family businesses that form the backbone of the city's economy.

For an SME customer, switching banks is not a matter of downloading a new app. It involves transferring credit lines, renegotiating loan covenants, reassigning security interests over properties and receivables, and — most critically — rebuilding a relationship with a new loan officer who understands your business. Many of Dah Sing's SME relationships span decades. The loan officer who approved a customer's first trade finance facility twenty years ago may still be managing that account today. That kind of institutional memory and personal trust is extraordinarily difficult for a competitor to replicate, whether that competitor is a global bank with an impersonal credit scoring model or a virtual bank with an algorithm.

This is the kind of switching cost that doesn't show up in any financial metric but is the single most important reason Dah Sing's loan book has historically exhibited lower loss rates than its peers. When you've banked a family business for thirty years, you understand the real risks in ways that no credit model can capture. You know when the owner is overextended. You know when the industry is turning. You know when to say yes and, more importantly, when to say no.

Cornered Resource: The Banking License

In Hong Kong, a full banking license is what economists call a "Veblen good" in the regulatory sense — they aren't making any more of them, and the existing ones only become more valuable over time. While there are approximately 163 licensed banks operating in Hong Kong, this number is somewhat misleading: the vast majority are branches or subsidiaries of foreign institutions operating under a different regulatory category. The number of truly independent, locally incorporated, full-service licensed banks with deep retail and SME franchises in Hong Kong can be counted on one hand. Dah Sing is one of them.

The HKMA's three-tier banking system — licensed banks, restricted license banks, and deposit-taking companies — creates a regulatory moat around full-service banking licenses. Only licensed banks can accept deposits of any size and maturity, and only they are permitted to use the word "bank" in their name. The Deposit Protection Scheme covers deposits up to HK$800,000 at licensed banks, providing a government-backed trust advantage that virtual banks and other non-bank financial institutions cannot easily replicate.

When Wing Hang Bank was acquired by OCBC in 2014, the premium paid reflected not just the value of the loan book or the branch network but, fundamentally, the value of the license itself — the right to operate as a full-service bank in one of the world's most important financial centres. Dah Sing's license carries the same scarcity value, and it is an asset that appreciates every time a competitor exits the market.

Counter-Positioning: The Anti-Virtual Bank

Since 2019, Hong Kong has licensed eight virtual banks: ZA Bank, Airstar Bank, WeLab Bank, Livi Bank, Mox Bank, Ant Bank, PAO Bank, and Fusion Bank. These digital-only institutions arrived with bold ambitions to disrupt traditional banking through lower fees, higher deposit rates, and frictionless digital experiences. The results, seven years later, have been modest at best.

Virtual banks have collectively amassed approximately 2.2 million users — an impressive headline number until you examine the economics underneath. Their aggregate deposits of roughly HK$32.2 billion represent just 0.2% of Hong Kong's HK$15.4 trillion deposit base. The average customer deposit at a virtual bank is approximately 30 times smaller than at a traditional bank. Most virtual banks remain unprofitable.

The fundamental problem for virtual banks is one of counter-positioning. They compete effectively on price and convenience for simple, commoditized products — savings accounts, small personal loans, payment cards. But Dah Sing's core franchise operates in a segment that algorithms cannot yet serve: the high-touch, relationship-driven world of SME lending and wealthy-merchant banking. When a garment manufacturer in Sham Shui Po needs a HK$50 million revolving credit facility secured against his factory inventory and receivables from buyers in three countries, he doesn't open an app. He calls his banker at Dah Sing.

This is counter-positioning in its purest form. Dah Sing isn't trying to beat the virtual banks at their own game. It is serving a customer segment that the virtual banks, by their very architecture, cannot effectively reach. The high-touch, judgment-intensive nature of SME lending — where the relationship manager's understanding of the borrower's character and business is as important as the financial statements — is precisely the kind of service that resists digitization. Dah Sing's response to the virtual bank threat has been measured: they launched 24-hour US stock trading capabilities in late 2025 and continue to invest in their mobile banking platform. But they haven't panicked. They haven't slashed fees to compete. They haven't launched a "digital-first" strategy that would cannibalize their existing franchise. They have, characteristically, done nothing dramatic — and that restraint is itself a strategic choice.

Beyond Helmer's framework, a quick scan through Porter's Five Forces reinforces the picture. The threat of new entrants is low — banking licenses are scarce and capital requirements are high. Supplier power (depositors) is moderate — Hong Kong depositors are sticky but rate-sensitive in HIBOR environments. Buyer power (borrowers) is moderate for large corporates but low for SMEs who value relationship continuity. The threat of substitutes (virtual banks, fintech) is real but, as discussed, limited in Dah Sing's core niche. And competitive rivalry among incumbent mid-tier banks has actually decreased as consolidation has thinned the field. Dah Sing, as the last independent, now faces less direct competition from peers of similar size and character than at any point in its history.

VI. Playbook: The Art of Saying "No" (1:05:00 – 1:20:00)

There is a particular species of management genius that receives almost no attention in business schools or on conference stages. It is the genius of restraint. The genius of the deal not done, the expansion not pursued, the trend not followed. In an industry that glorifies growth, leverage, and "bold strategic vision," Dah Sing Banking Group has built its entire playbook around a single, deeply unfashionable idea: the most important word in banking is "no."

Lesson 1: Liquidity Is a Strategy

Ask any bank analyst what they think about excess capital, and you will hear a familiar refrain: it's a "drag on ROE." Return on equity — the ratio of profits to shareholders' equity — is the metric by which bank management teams are judged, compensated, and promoted. And the easiest way to boost ROE is to reduce the denominator: lever up the balance sheet, deploy excess capital into loans or investments, return it to shareholders through buybacks and dividends. In theory, every dollar of equity sitting idle on a bank's balance sheet is a dollar not earning a return.

Dah Sing's management team has heard this argument a thousand times. They understand the math. And they have, consistently and deliberately, rejected it.

With a CET1 ratio of 16.9% and a total capital adequacy ratio of 21.0%, Dah Sing holds roughly twice the regulatory minimum capital requirement. By the standards of most bank analysts, this is "inefficient." The group's return on equity, at approximately 6.2%, is well below the double-digit returns that more aggressively managed banks target. If you're a portfolio manager whose bonus depends on hitting a 15% ROE hurdle, Dah Sing's conservatism looks like a vice.

But the Wongs don't think about capital the way most bank management teams do. They don't see excess capital as a drag on returns. They see it as dry powder for the next systemic crisis. When the 1997 Asian financial crisis devastated Hong Kong's banking sector, Dah Sing was strong enough to acquire competitors at distressed prices. When the 2008 global financial crisis froze interbank lending markets, Dah Sing never had to worry about liquidity. When the COVID-19 pandemic cratered economic activity in 2020-2021, Dah Sing's capital buffers meant it could continue lending to its SME clients without pulling credit lines or tightening covenants.

This is the "insurance premium" model of capital management: you accept lower returns in normal times in exchange for resilience — and opportunity — in crisis times. The historical record suggests that banking crises occur with depressing regularity, roughly once every 10-15 years. A bank that is "inefficiently" capitalized during the calm periods is, by definition, the bank that is "optimally" capitalized when the storm arrives.

Lesson 2: Don't Compete with Giants

The second lesson embedded in Dah Sing's playbook is an understanding of where they can and cannot win. HSBC has a balance sheet of approximately US$3 trillion. Standard Chartered and Bank of China (Hong Kong) are not far behind in terms of their Hong Kong operations. Dah Sing's HK$256 billion in total assets makes it roughly 1/100th the size of HSBC.

In any industry, competing head-to-head with players that are 100 times your size is a recipe for destruction. Yet many mid-tier Hong Kong banks attempted exactly this — expanding into investment banking, proprietary trading, offshore lending, and cross-border structured finance in an effort to "grow into" the big leagues. The results were predictable: they overextended, took risks they didn't fully understand, and ultimately either failed or were forced to sell at distressed valuations.

Dah Sing chose a different path. Rather than trying to be a smaller version of HSBC, they positioned themselves as the specialist for the Hong Kong merchant class — the garment traders of Sham Shui Po, the electronics wholesalers of Sham Shui Po, the property owners of the New Territories, the family businesses that have been operating in Hong Kong for two or three generations. These are customers that HSBC considers too small for its corporate banking division but too complex for its retail banking platform. They fall into a gap that only a mid-tier, relationship-driven bank like Dah Sing can effectively serve.

This is not a glamorous niche. It doesn't generate headlines or awards or invitations to World Economic Forum panels. But it is extraordinarily defensible. The Hong Kong SME community is large, profitable, and loyal. These customers don't switch banks because a competitor offers them 10 basis points more on their deposit rate. They stay because their banker understands their business, their family, and their ambitions. Dah Sing has been cultivating these relationships for decades, and the cumulative value of that institutional knowledge is essentially impossible for a new entrant to replicate.

Lesson 3: The "Wait and See" M&A Approach

The perennial question surrounding Dah Sing is: why haven't they been acquired? The stock trades at half of book value. The family controls the parent company with a 43% stake. The market cap of roughly HK$17 billion is well within the financial capacity of any number of potential acquirers — Chinese banks, Southeast Asian banking groups, even private equity firms with an appetite for financial services.

In 2013, when rival Chong Hing Bank disclosed it had been approached by potential buyers, Dah Sing Banking issued a statement saying it was "open-minded about the possibility of a merger or sale" but was not in active discussions. That phrase — "open-minded" — is a masterpiece of strategic ambiguity. It signals to potential bidders that the door is not closed while simultaneously declining to initiate any process.

The most likely explanation for why Dah Sing hasn't sold is simply arithmetic. The Wong family's 43% stake in DSFH, which controls 74-75% of DSBG, means a full acquisition would need to be priced high enough to make the Wongs willing to give up not just an income stream but a family legacy spanning nearly seven decades. At half of book value, the current stock price implies an enterprise value that the family almost certainly considers inadequate. A credible bid would likely need to come at a significant premium to book value — perhaps 1.2-1.5 times — which at current equity levels would imply a price tag of HK$40-50 billion or more for the banking group alone.

There is also a generational dimension. David Wong, at approximately 84, remains Executive Chairman. Harold, as Managing Director and CEO, is the heir apparent but not yet the sole decision-maker. The transition of power between generations is often the moment when family-controlled businesses become most receptive to acquisition offers — either because the next generation doesn't share the founder's attachment to the business, or because the estate planning considerations of a generational transfer create tax and liquidity pressures that a sale can solve. Whether this dynamic plays out at Dah Sing remains to be seen, but it is the single most important variable that potential acquirers are watching.

VII. The Bear vs. Bull Case (1:20:00 – 1:35:00)

Every investment thesis, no matter how compelling, must be stress-tested against the arguments for why it might be wrong. Dah Sing Banking Group is no exception, and the bear case is worth taking seriously before examining why the bulls remain convinced.

The Bear Case

The most immediate concern is interest rate volatility in Hong Kong. Because the Hong Kong dollar is pegged to the US dollar under the Linked Exchange Rate System, Hong Kong's monetary policy effectively follows the US Federal Reserve. When the Fed raises rates, HIBOR (the Hong Kong Interbank Offered Rate) typically follows, which expands bank net interest margins. But when rates fall, margins compress — and for a bank like Dah Sing that relies heavily on net interest income (HK$5.29 billion in fiscal 2024, representing the vast majority of operating income), a sustained period of low rates can meaningfully impact profitability. The bank's net interest margin expanded to 2.17% in 2024 from 2.01% in 2023, but this improvement is partially a function of the rate cycle and could reverse if global rates decline.

The second bear argument is the "growth trap" — or rather, the absence of growth. Dah Sing's gross advances (total loan book) actually declined 3.6% in fiscal 2024 to HK$139.9 billion. Total assets shrank modestly from HK$260.7 billion to HK$256.3 billion. For a bank trading at half of book value, the absence of loan growth means there is no catalyst to close the valuation gap through earnings expansion. If the loan book isn't growing, and margins are at the mercy of the rate cycle, then book value grows only through retained earnings — a slow, incremental process that may not be enough to attract the kind of institutional investor attention that would re-rate the stock.

Third, there is a demographic concern embedded in Dah Sing's core franchise. The Hong Kong SME community that forms the backbone of the bank's loan book is aging. The garment traders, electronics wholesalers, and family-business owners who have banked with Dah Sing for decades are, in many cases, approaching retirement. Their children may not want to continue the family business. Their industries may be in structural decline as manufacturing migrates to Southeast Asia and e-commerce disrupts traditional wholesale trade. If Dah Sing's core customer base is shrinking, the switching costs that protect the franchise today may be irrelevant tomorrow.

Fourth, credit impairment charges surged 145% year-on-year in fiscal 2024 to HK$1.79 billion — a significant jump that reflects stress in the Hong Kong and mainland China property markets. While the Bank of Chongqing impairment charges declined dramatically, the core Hong Kong loan book showed elevated losses. If the property market downturn deepens, Dah Sing's conservative underwriting may be tested in ways it hasn't been before.

The Bull Case

The bull case begins with the observation that Dah Sing is, in essence, a "value coiled spring" — a term used to describe companies whose intrinsic value significantly exceeds their market price, with multiple potential catalysts to close the gap.

The most obvious catalyst is the "special dividend" potential. With HK$33.8 billion in total equity and a CET1 ratio of 16.9% — more than double the regulatory minimum — Dah Sing has enormous capacity to return capital to shareholders. The regular dividend of HK$0.66 per share in fiscal 2024 represents a yield of approximately 5.5% at the current stock price, but this barely scratches the surface of what the bank could theoretically distribute. Even a modest reduction in the CET1 ratio from 16.9% to, say, 13% — still well above regulatory minimums and peer averages — would free up billions of Hong Kong dollars for extraordinary distributions.

The second bull argument is the scarcity premium. As the last independent, family-controlled, full-service bank in Hong Kong, Dah Sing occupies a unique position in the M&A landscape. Every other bank of similar character has been acquired — and acquired at significant premiums to prevailing market prices. Wing Hang Bank was bought at roughly 2.1 times book value by OCBC. Chong Hing Bank was acquired at approximately 1.8 times book value by Yuexiu. If Dah Sing were to be acquired at even 1.0 times book value — a modest premium by historical standards — the stock would roughly double from current levels.

Third, the 2024 financial results demonstrated meaningful operational momentum. Net profit grew 11% year-on-year to HK$2.06 billion. Net interest margin expanded 16 basis points. Fee and commission income surged 53%, suggesting the bancassurance partnership with Sun Life and the bank's wealth management initiatives are gaining traction. The bank's cost-to-income ratio of approximately 48% is competitive with peers, indicating operational efficiency despite the conservative posture.

Fourth, the Bank of Chongqing stake — worth approximately HK$3-4 billion at current market prices for a 13% position in a listed entity — is essentially being given away for free in Dah Sing's current valuation. When you subtract the market value of the BOCQ stake and the excess capital above regulatory minimums from Dah Sing's market cap, the implied value of the core Hong Kong and Macau banking operations approaches zero. That is either an extraordinary mispricing or a market judgment that those operations are worth nothing — a conclusion that the bank's consistent profitability directly contradicts.

The Key Metrics to Watch

For investors tracking Dah Sing's trajectory, two KPIs matter above all others.

The first is net interest margin (NIM). At 2.17% in fiscal 2024, NIM is the single most important driver of Dah Sing's revenue and profitability. It captures the spread between what the bank earns on its loans and investments and what it pays on deposits and funding — and it is highly sensitive to the interest rate cycle. A sustained NIM above 2.0% signals a healthy earnings environment; a compression below 1.8% would signal margin pressure that could weigh on profitability.

The second is the CET1 capital ratio. At 16.9%, this metric tells you how much excess capital the bank is hoarding — capital that could be returned to shareholders, deployed into acquisitions, or used to absorb credit losses. If CET1 starts declining meaningfully, it could signal either that management is finally deploying capital (bullish) or that credit losses are consuming the buffer (bearish). The direction and velocity of CET1 movement is the clearest signal of management's intentions and the bank's financial trajectory.

VIII. Conclusion: The Narrative Finality (1:35:00 – 1:45:00)

Dah Sing Banking Group is not a story about disruption, transformation, or exponential growth. It is not a company that will ever be featured on the cover of a technology magazine or celebrated at a Silicon Valley conference. It will never have an "iPhone moment" or a "pivot to AI." And that, paradoxically, is precisely what makes it remarkable.

In a financial landscape that rewards boldness, leverage, and speed, Dah Sing has built an enduring franchise by practicing the opposite virtues: patience, conservatism, and restraint. The Wong family's stewardship across three generations has produced an institution that is, by almost any measure, one of the most resilient mid-tier banks in Asia. It survived the 1997 Asian financial crisis. It navigated the 2008 global financial meltdown without breaking a sweat. It emerged from the COVID-19 pandemic with its capital base intact and its customer relationships strengthened. And it executed, in the 2017 insurance sale, what may be remembered as one of the shrewdest asset disposals in Hong Kong corporate history.

The question of whether Dah Sing is a "category king" — to use the Silicon Valley parlance — has a simple answer: no. It is not the dominant player in any single market. It is not the largest, the fastest-growing, or the most technologically advanced bank in Hong Kong. But ask a different question — is it the most "anti-fragile" bank in Asia? — and the answer becomes more interesting. Nassim Taleb coined the term "anti-fragile" to describe systems that actually benefit from disorder, volatility, and stress. Dah Sing's mountain of excess capital, its conservative loan book, its relationship-driven franchise, and its history of counter-cyclical capital deployment suggest an institution that doesn't just survive crises but actively profits from them.

The stock trades at roughly 0.50 times book value. The dividend yield exceeds 5%. The capital ratios would be the envy of any bank in the region. And the family that controls it has demonstrated, over and over, that they know how to wait for the right moment to act.

When the next financial storm hits Hong Kong — and in a city tied to the US dollar, exposed to Chinese economic cycles, and sitting at the geopolitical crosshairs of US-China competition, the question is when, not if — David and Harold Wong will not be the ones looking for a bailout. They will be the ones looking at what to buy.

IX. Further Reading

- The 2017 Dah Sing Life Sale Prospectus: The anatomy of a high-premium exit, available through the Hong Kong Stock Exchange disclosure archive

- HKMA Annual Banking Report: Comprehensive data on Hong Kong's three-tier banking system and the evolution of mid-tier banks

- Harold Wong's 2013 Hong Kong Business Awards Executive of the Year profile and subsequent interviews on the future of Hong Kong banking

- Bank of Chongqing (1963.HK) annual reports: Essential reading for understanding the equity-accounted "hidden asset" within Dah Sing's portfolio

- Hamilton Helmer's "7 Powers: The Foundations of Business Strategy": The theoretical framework for understanding Dah Sing's durable competitive advantages in switching costs, cornered resources, and counter-positioning

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube