WuXi Biologics: The Global Biotech Foundry

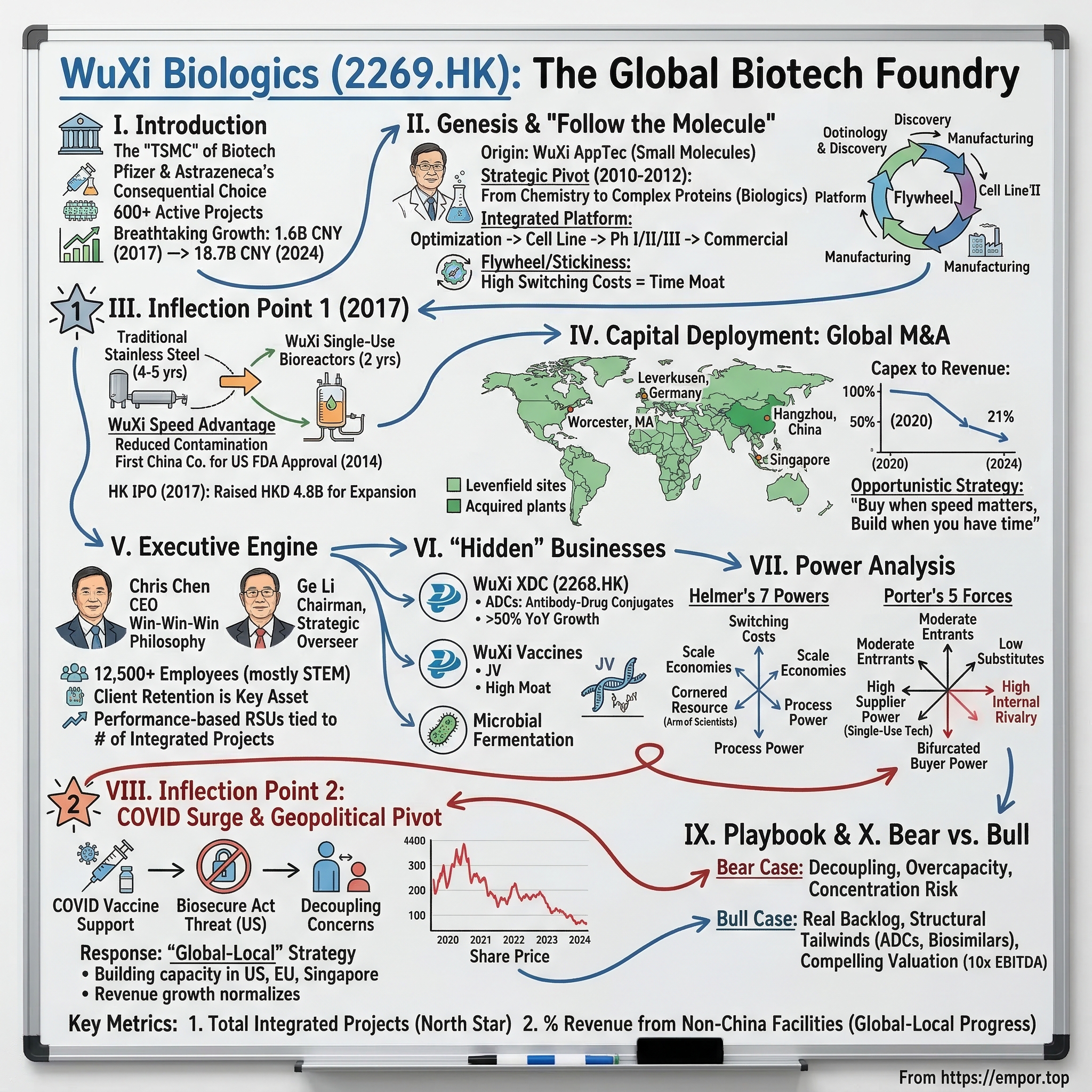

I. Introduction: The "TSMC" of Biotech

Picture a conference room at Pfizer's headquarters in Manhattan, sometime in early 2020. The world's largest pharmaceutical company is about to make one of the most consequential supply chain decisions in modern medicine. The question on the table is not which drug to develop next, or which clinical trial to fund. It is something far more fundamental: who is going to actually make the drug? The answer, for Pfizer and for dozens of the world's most powerful pharma companies, increasingly points to a single city in eastern China—Wuxi, population seven million, home to a company that most people outside the biotech industry have never heard of.

WuXi Biologics is not a household name. It does not sell drugs to patients. It does not run television advertisements or sponsor sports stadiums. Yet it sits at the very center of the global pharmaceutical supply chain in a way that few companies in any industry can match. When AstraZeneca needed billions of COVID-19 vaccine doses manufactured at unprecedented speed, it turned to WuXi. When small biotechs with promising cancer therapies need to go from a molecule in a petri dish to a vial of medicine ready for human trials, the fastest path runs through WuXi's facilities. The company's client list reads like a who's who of global pharma: more than six hundred active projects spanning the full lifecycle of biologic drug development and manufacturing.

The analogy that has stuck—and for good reason—is TSMC. Just as Taiwan Semiconductor Manufacturing Company became the indispensable fabrication partner for the world's chip designers, WuXi Biologics has positioned itself as the indispensable manufacturing partner for the world's drug developers. The company does not invent the drugs. It builds them. And just like TSMC, WuXi has discovered that being the factory—the infrastructure layer—can be an extraordinarily powerful business position, one that generates deep switching costs, massive scale economies, and a kind of quiet strategic leverage that only becomes visible when you try to imagine the world without it.

The numbers tell a story of breathtaking growth. In 2017, the year of its Hong Kong IPO, WuXi Biologics reported revenue of roughly 1.6 billion Chinese yuan. By 2024, that figure had grown to 18.7 billion yuan—a more than tenfold increase in seven years. The company went from a small department within a larger parent organization to a publicly traded entity with a market capitalization that has at times exceeded two hundred billion Hong Kong dollars. Today, it employs over twelve thousand people, operates manufacturing sites across China, Ireland, Germany, the United States, and Singapore, and manages a pipeline backlog that represents one of the largest concentrations of biologic drug manufacturing capacity on earth.

But this is not simply a story about growth. It is a story about strategy—about how a company built in the shadow of China's manufacturing miracle learned to apply the principles of speed, scale, and relentless cost optimization to one of the most technically demanding industries in the world. It is a story about geopolitical risk, about what happens when the factory the world depends on sits in a country that is increasingly at odds with its largest customers. And it is a story about a business model so elegantly designed that once a client enters the WuXi ecosystem, leaving becomes an exercise in regulatory pain that few are willing to endure.

This is the story of how WuXi Biologics became the most important company in biotech that most people have never heard of.

II. Genesis and The "Follow the Molecule" Strategy

To understand WuXi Biologics, you first have to understand its parent—or more precisely, its origin species. The story begins not with biologics at all, but with a chemist named Ge Li and a bet on small molecules.

Ge Li was born in 1967 in China, trained as a chemist, and earned his PhD in organic chemistry from Columbia University in New York. He worked briefly in the pharmaceutical industry in the United States before returning to China in 2000 with a vision that was, at the time, borderline audacious: he would build a world-class pharmaceutical services company in China, offering Western drugmakers high-quality research and manufacturing at a fraction of the cost. The company he founded was WuXi AppTec, and it focused on small molecule chemistry—the traditional pills and tablets that had dominated pharmaceutical development for decades.

WuXi AppTec grew rapidly through the 2000s, riding a wave of pharmaceutical outsourcing from the West to China. The value proposition was straightforward: China had an enormous pool of well-trained chemists who could be hired at a fraction of American or European salaries, and Ge Li was meticulous about building facilities and processes that met Western regulatory standards. By the late 2000s, WuXi AppTec had established itself as one of the leading contract research organizations in the world.

But Ge Li and his team saw a shift coming. The pharmaceutical industry was undergoing a fundamental transition—from small molecules to large molecules, from chemistry to biology. Small molecules are relatively simple chemical compounds that can be manufactured through traditional chemical synthesis. Biologics, by contrast, are large, complex proteins produced by living cells—think monoclonal antibodies, the blockbuster drugs behind treatments for cancer, autoimmune diseases, and increasingly, a wide range of other conditions. The manufacturing process for biologics is orders of magnitude more complex than for pills. Instead of mixing chemicals in a reactor, you are essentially farming living cells in massive bioreactors, carefully controlling temperature, pH, nutrient feeds, and a hundred other variables to coax those cells into producing the precise protein you need.

Between 2010 and 2012, WuXi made what would prove to be its defining strategic pivot. A small team within WuXi AppTec began building out capabilities in biologic drug development and manufacturing. This was not a trivial decision. Biologics manufacturing requires entirely different facilities, equipment, expertise, and regulatory know-how. It was, in essence, starting a new company within the old one. The team was small—fewer than a hundred people—and the skeptics were many. China had virtually no track record in biologic manufacturing. The established players were companies like Lonza in Switzerland, Samsung Biologics in South Korea, and Boehringer Ingelheim in Germany—firms with decades of experience and billions of dollars in installed capacity.

What WuXi brought to the table was not experience in biologics. It was a business model innovation that would prove to be its most important strategic asset: "Follow the Molecule."

The concept is deceptively simple but profoundly powerful. Traditional contract manufacturers operate as point-in-time service providers. A biotech company might hire one firm to help with early-stage research, another to produce material for clinical trials, and yet another for commercial manufacturing. Each handoff introduces delays, regulatory risk, and the possibility of failure. WuXi's insight was to offer an integrated platform that could take a biologic molecule from its earliest stage of discovery all the way through commercial manufacturing—and to structure its business so that it had every incentive to capture and retain that molecule at every stage.

Here is how the flywheel works in practice. A small biotech company comes to WuXi with a promising antibody candidate. WuXi's scientists help optimize the cell line—the living factory that will produce the drug. They develop the manufacturing process at laboratory scale, then scale it up for Phase I clinical trials. If the drug succeeds in Phase I, WuXi scales up again for Phase II, then Phase III. And if the drug ultimately wins regulatory approval, WuXi manufactures it at commercial scale. At each stage, the relationship deepens. The institutional knowledge accumulated by WuXi's team—the specific quirks of that particular cell line, the process parameters that were painstakingly optimized over years of development—becomes an asset that is extraordinarily difficult and expensive to replicate elsewhere.

This is the "stickiness" that traditional contract manufacturers lack. When you are simply filling vials at the end of the process, you are a commodity. When you have been with a molecule since its birth, you are a partner—and replacing you means, in practical terms, re-doing years of development work and re-filing regulatory submissions with agencies like the FDA. The switching costs are not just financial; they are temporal. In an industry where a year of delay can mean hundreds of millions of dollars in lost revenue, time is the ultimate moat.

By 2013, the biologics team within WuXi AppTec had grown large enough and promising enough to merit its own identity. The subsidiary that would become WuXi Biologics was formally incorporated in the Cayman Islands in 2014, setting the stage for what would come next: a bet on a specific manufacturing technology that would give the company its signature speed advantage, and an IPO that would provide the capital to turn a regional player into a global force.

III. Inflection Point 1: The First 1,000L and The 2017 IPO

In the early 2010s, the biologics manufacturing industry was dominated by a single paradigm: stainless steel. Massive, gleaming bioreactors—some holding fifteen thousand liters or more—were the standard. These reactors were permanent installations, custom-built into facilities that took four to five years to construct and cost hundreds of millions of dollars. Cleaning and validating a stainless steel bioreactor between production runs was itself a weeks-long process. The industry had been built this way for decades, and the established players saw little reason to change.

WuXi Biologics saw things differently. The company made an early and aggressive bet on single-use bioreactors—essentially, large disposable plastic bags that serve as the vessel for cell culture. Instead of cleaning and re-sterilizing a stainless steel tank between runs, you simply remove the plastic liner and install a new one. The concept was not entirely new—several equipment suppliers had been developing single-use technology—but WuXi was among the first to build its entire manufacturing strategy around it.

The advantages were transformative. Single-use bioreactors dramatically reduced the risk of cross-contamination between products, a critical concern when a facility is manufacturing drugs for multiple clients simultaneously. They slashed turnaround times between production campaigns. And most importantly, they allowed WuXi to build new manufacturing facilities in roughly two years instead of the four to five years required for traditional stainless steel plants. In an industry where speed to market can determine whether a drug generates billions in revenue or gets beaten by a competitor, this time advantage was worth far more than the modest per-unit cost premium of disposable equipment.

This decision gave birth to what the company would eventually brand "WuXi Speed"—the ability to move faster than any competitor from process development to GMP manufacturing. It was not just a marketing slogan. It was an operational reality that became the company's primary competitive differentiator.

The early validation came in 2014, when WuXi Biologics became the first company in China to support a client's biologic drug through to US FDA approval for manufacturing. This was a watershed moment. It demonstrated that a Chinese facility could meet the exacting quality standards of the world's most demanding regulatory agency. For the global biotech industry, which had long viewed Chinese manufacturing with skepticism, it was a signal that the rules of the game were changing.

By 2016, the biologics operation had grown to the point where it was ready to stand on its own. WuXi Biologics had over a hundred active projects, revenue was approaching one billion yuan, and the company was investing aggressively in expanding its manufacturing capacity. The decision was made to take the company public on the Hong Kong Stock Exchange.

The IPO, which took place on June 13, 2017, was a landmark event for the Hong Kong capital markets and for the Chinese biotech industry. WuXi Biologics raised approximately HKD 4.8 billion, giving the company a valuation that reflected the market's growing appreciation for the CDMO model—Contract Development and Manufacturing Organization, the industry term for what WuXi does. The capital raised in the IPO was not for dividends or executive bonuses. It was fuel for an expansion strategy that was about to shift into overdrive.

The timing proved fortuitous. The global biologics industry was entering a period of unprecedented demand growth, driven by the explosion of monoclonal antibody therapies, the emergence of biosimilars, and the growing pipeline of novel biologic modalities. Manufacturing capacity was becoming scarce. Companies that had spent decades building their own facilities were discovering that they could not keep up with demand. And companies that had never built a factory—the hundreds of small biotech firms emerging from the venture capital ecosystem—needed someone to manufacture their drugs for them.

WuXi Biologics, freshly capitalized and armed with its speed advantage, was perfectly positioned to capture this demand. In the year of its IPO, the company reported revenue of 1.6 billion yuan and net income of 253 million yuan. The gross margin was a healthy 41 percent, reflecting the premium that clients were willing to pay for speed and integrated services. But the real story was in the project pipeline: the number of active integrated projects was growing at a pace that suggested the "Follow the Molecule" flywheel was working exactly as designed. Each new project that entered the system at the discovery stage represented years of future revenue as it progressed through clinical trials and, potentially, to commercial manufacturing.

The stage was set for the next phase: a global expansion that would take WuXi Biologics from a China-based operation to a truly worldwide manufacturing network.

IV. Capital Deployment: Global M&A and Benchmarking

If the 2017 IPO gave WuXi Biologics the capital to dream big, the years that followed revealed a management team with a sophisticated and unusually disciplined approach to deploying that capital. The strategy can be understood through a simple framework: when speed matters more than price, buy; when you have time, build.

The biologics CDMO industry has a structural challenge that makes organic growth alone insufficient for any company with global ambitions. Building a new manufacturing facility from scratch—even with WuXi's single-use technology advantage—takes roughly two years. Securing regulatory approvals for that facility takes additional time. And in those two to three years, client projects are moving through clinical trials and reaching milestones where they need manufacturing capacity now, not in twenty-four months. The opportunity cost of not having capacity available when a client needs it is enormous. A large commercial manufacturing contract can be worth hundreds of millions of dollars per year, and if you cannot serve it, a competitor will.

This is why WuXi Biologics pursued what might be called an "opportunistic acquisition" strategy—buying existing facilities that came with built-in regulatory approvals, trained staff, and immediate manufacturing capacity. The math, when you work it out, is compelling. If acquiring a facility costs fifty percent more than building one from scratch, but it gives you access to that capacity two to three years earlier, the premium effectively "pays for itself" through the revenue you can capture during those years.

The most significant of these acquisitions came in quick succession. In 2020, WuXi acquired a biologics manufacturing facility in Leverkusen, Germany, from Bayer. The plant came with established GMP capabilities, European regulatory approvals, and a trained workforce—all things that would have taken years to build from scratch. The acquisition gave WuXi an immediate manufacturing footprint in the European Union, the world's second-largest pharmaceutical market. It also sent a signal to European pharmaceutical companies that WuXi was serious about being a local partner, not just a distant Chinese supplier.

The following year, in 2021, WuXi acquired Pfizer's biologics manufacturing assets in Hangzhou, China. This was a different kind of deal—buying surplus capacity from a major pharma company that was rationalizing its manufacturing network. The Hangzhou facility came with Pfizer-grade quality systems and processes, which in the biologics world is about as good a stamp of approval as you can get. Industry analysts estimated that both acquisitions were completed at roughly 1.5 to 2 times book value—a premium, certainly, but one that looked modest when measured against the alternative of building equivalent capacity from the ground up over three to five years.

Alongside the acquisitions, WuXi was building at a furious pace. New facilities went up in Wuxi and Shanghai, adding tens of thousands of liters of bioreactor capacity to the Chinese network. But the most strategically significant greenfield investments were happening outside China. In Ireland, WuXi built a major manufacturing campus in Dundalk, taking advantage of Ireland's favorable corporate tax regime, its established pharmaceutical workforce, and its position as a hub for pharmaceutical manufacturing within the EU. In the United States, the company invested in a facility in Worcester, Massachusetts—a decision that would take on much greater strategic significance as US-China tensions escalated. And in Singapore, WuXi began building what it positioned as its Asia-Pacific hub outside of China, a facility designed to serve clients who wanted WuXi's capabilities but preferred a manufacturing location with less geopolitical risk.

By the mid-2020s, the result of this build-and-buy strategy was a global manufacturing network of more than fifteen sites spanning four continents. This network itself became a competitive advantage. A client working with WuXi could have its drug manufactured in China for early-stage clinical trials (where cost matters most), then shift production to Ireland or the US for commercial manufacturing in Western markets (where regulatory proximity matters most). No boutique CDMO could offer this kind of geographic flexibility. The network effect meant that WuXi could "swap" capacity between sites to accommodate fluctuations in client demand—a capability that is extraordinarily valuable in an industry where production timelines are notoriously unpredictable.

The financial results reflected the payoff. Revenue grew from 5.6 billion yuan in 2020 to 15.3 billion yuan in 2022—nearly tripling in just two years. Gross margins held steady in the low-to-mid forties, suggesting that the company was not buying revenue at the expense of profitability. The capital expenditure was enormous—WuXi spent roughly the equivalent of its annual revenue on capex during the peak expansion years of 2020 and 2021—but this was investment in long-lived manufacturing assets that would generate returns for decades.

The question that investors had to grapple with was whether the return on this massive capital deployment would justify the investment. By 2024, with revenue at 18.7 billion yuan and the global network largely built out, WuXi Biologics was entering a new phase—one where the focus would shift from building capacity to filling it, from capital expenditure to free cash flow generation. The capex-to-revenue ratio had already begun declining meaningfully, from over 100 percent in 2020 to roughly 21 percent in 2024. The biological factory had been built. Now it needed to be fed.

V. Current Management and The "Executive Engine"

Walk into WuXi Biologics' headquarters on Meiliang Road in Wuxi, and the first thing that strikes you is the contrast between the setting and the ambition. Wuxi is not Shanghai or Beijing. It is a mid-sized Chinese city in Jiangsu province, known historically for its ceramics industry and its proximity to Taihu Lake. The headquarters itself is functional rather than flashy—a campus of modern but unremarkable buildings set among the manufacturing facilities that are the company's true showpieces. This is not a company that spends money on marble lobbies. The money goes into bioreactors.

At the center of the operation is Zhisheng Chen, known universally in the industry as Chris Chen. Born in 1973, Chen is a product of the first generation of Chinese scientists who built careers in Western pharmaceutical companies before returning to China. His formative professional years were spent at Eli Lilly, one of the world's largest and most respected drugmakers, where he absorbed the quality systems, manufacturing discipline, and regulatory rigor that define Western pharmaceutical operations. When he joined WuXi Biologics, he brought that institutional knowledge with him—and it became the foundation on which the company's credibility was built.

Chen's leadership style is often described in terms of a philosophy he calls "Win-Win-Win"—an outcome where the client wins (through speed and quality), WuXi wins (through revenue and growth), and patients win (through faster access to medicines). It sounds like corporate boilerplate, but people who have worked with Chen describe a genuine obsession with client satisfaction that permeates the organization. In an industry where manufacturing delays and quality failures can literally kill patients and destroy companies, reliability is not just a selling point—it is an existential requirement. Chen has built a culture where delivering on time and on spec is treated as a non-negotiable obligation.

Above Chen in the organizational hierarchy sits founder Ge Li, who remains Chairman and the company's largest individual shareholder. Li's role has evolved over the years from hands-on founder to strategic overseer. The transition from a founder-centric model to a professionalized management structure is one of the most important—and most difficult—milestones for any growing company. WuXi Biologics appears to have navigated it relatively well. Li sets the strategic direction and maintains relationships with the Chinese government and regulatory establishment. Chen runs the day-to-day operations and manages the global client relationships. The division of labor plays to each leader's strengths.

The management team's incentive structure is worth examining for what it reveals about the company's strategic priorities. CEO Chen's total compensation was reported at approximately 9.4 million yuan—substantial by Chinese standards but modest compared to what the CEO of a similarly-sized Western biotech company would earn. More importantly, a significant portion of management compensation is tied to performance-based restricted share units, and the key performance indicator underlying those RSUs is not revenue or profit. It is the number of integrated projects. This is a telling choice. The number of projects is the leading indicator for the "Follow the Molecule" flywheel—each project represents a molecule that has entered the WuXi ecosystem and is progressing through the stages of development and manufacturing. By tying compensation to project count, the company ensures that management's attention is focused on feeding the flywheel, not on short-term earnings optimization.

The broader executive team reflects the company's dual identity as both a Chinese manufacturer and a global pharmaceutical services provider. Jijie Gu, the Chief Scientific Officer, oversees global biologics research. Xuejun Gu, the Chief Technology Officer, manages the development side. CFO Ming Tu handles the financial architecture. And notably, the head of Global Business Development and Alliance Management is Angus Turner—a Western executive whose presence in the senior leadership signals WuXi's commitment to bridging the cultural and operational gap between Eastern manufacturing and Western pharmaceutical clients.

The talent pool beneath the executive suite is, in many ways, WuXi's most underappreciated asset. The company employs over twelve thousand five hundred people, a substantial majority of whom are scientists and engineers. China produces more STEM graduates than any other country on earth, and WuXi has positioned itself as one of the most desirable employers for biologists and bioengineers in China. The scale of this talent base—thousands of trained scientists who understand biologics development and manufacturing—is something that simply does not exist at any single company in the West. It is what enables WuXi to simultaneously manage over six hundred active projects, each with its own unique requirements, timelines, and challenges.

The question of management quality is always subjective, but there is one objective indicator that speaks volumes: client retention. In the CDMO business, the ultimate vote of confidence is when a client returns with a second project, then a third, then a fourth. WuXi's reported retention rates and its growing share of revenue from repeat clients suggest that the people running the company are delivering on their promises. In a business built on trust—where a single manufacturing failure can destroy a drug's chances of regulatory approval—that track record is arguably the most valuable asset on the balance sheet.

VI. "Hidden" Businesses: XDC, Vaccines, and Microbial

The market narrative around WuXi Biologics tends to focus on monoclonal antibodies—the bread-and-butter biologic drugs that have dominated the industry for two decades. But underneath the surface of the core business, WuXi has been quietly building several subsidiary businesses that may prove to be even more strategically important than the parent operation. The most significant of these is WuXi XDC.

Antibody-Drug Conjugates—ADCs—are one of the hottest areas in pharmaceutical development. The concept is elegant in its simplicity and brutal in its application. Take a monoclonal antibody, which is essentially a guided missile that can find and bind to a specific target on a cancer cell. Now attach a potent chemotherapy payload to that antibody using a chemical linker. The antibody finds the cancer cell, binds to it, gets absorbed into the cell, and then releases the chemotherapy drug directly inside the tumor. It is, in the language of oncologists, a "chemo-bomb"—a way to deliver devastating doses of cell-killing drugs precisely where they are needed, while sparing the rest of the body from the ravaging side effects of traditional chemotherapy.

The manufacturing challenge with ADCs is that they combine the complexity of biologics (producing the antibody) with the complexity of chemistry (producing the payload and the linker) and then add a third layer of complexity: the conjugation process that attaches the payload to the antibody with precise stoichiometry. Very few companies in the world can do all three. WuXi XDC, which was spun off as a separately listed entity on the Hong Kong Stock Exchange in late 2023 (trading as 2268.HK), is one of them.

The growth numbers for the XDC business have been extraordinary—consistently exceeding fifty percent year-over-year in recent periods, far outpacing the growth rate of the core biologics business. This is not a niche business. The global ADC market has been projected to grow from single-digit billions to tens of billions of dollars over the coming decade, driven by a wave of clinical approvals and an expanding pipeline of ADC candidates. WuXi XDC's market capitalization, at roughly HKD 68 billion as of recent trading, reflects the market's recognition that this is not just a subsidiary—it is potentially a franchise in its own right.

The strategic logic of the XDC business within the WuXi ecosystem is powerful. A client who comes to WuXi Biologics to develop an antibody can seamlessly move to WuXi XDC to develop an ADC based on that same antibody. The institutional knowledge transfers. The regulatory relationships carry over. The "Follow the Molecule" flywheel spins faster because the molecule has more places to go within the WuXi network.

The second hidden business is WuXi Vaccines, a joint venture with the Merck-backed Hilleman Laboratories that focuses on vaccine CDMO services. Vaccine manufacturing is, in many respects, an even higher-moat business than antibody manufacturing. The regulatory requirements for vaccines are among the most stringent in pharmaceuticals—you are, after all, injecting these products into healthy people, including children. The manufacturing processes are bespoke for each vaccine, often involving exotic production systems like insect cells or viral vectors that require specialized expertise. Once a vaccine manufacturer has been qualified and included in regulatory filings with agencies like the FDA, the WHO, or the EMA, the switching costs are effectively permanent. No company in its right mind would voluntarily re-validate a vaccine manufacturing process at a new facility when the existing one is working.

The third expansion vector is less glamorous but no less important: microbial fermentation. While the core business focuses on mammalian cell culture (growing drug proteins in Chinese hamster ovary cells, the workhorse of the industry), microbial systems—using bacteria or yeast as production organisms—are increasingly important for certain types of biologics, including some biosimilars and novel protein therapeutics. By adding microbial capabilities to its platform, WuXi further broadens the range of molecules it can "follow" through the development lifecycle.

The common thread running through all of these business extensions is the evolution of WuXi's self-description from "CDMO" to "CRDMO"—Contract Research, Development, and Manufacturing Organization. The addition of that "R" is not merely cosmetic. It represents a fundamental shift in the company's position in the value chain. WuXi is no longer just the factory that prints the drug. It is increasingly involved in the discovery and design of the drug itself—optimizing antibody sequences, engineering cell lines, designing conjugation strategies. This upstream involvement deepens the client relationship, increases the switching costs, and captures a higher share of the total value created in the drug development process.

For investors, these hidden businesses represent optionality that may not be fully reflected in the current valuation. The core biologics CDMO business is well-understood by the market. But the ADC business, the vaccine business, and the expanding research capabilities represent additional growth vectors that could, individually, become businesses of substantial scale. The XDC spinoff provided a partial window into this value, but the vaccine and microbial businesses remain embedded within the consolidated financials, their contribution visible only to those who look closely enough to find it.

VII. The Power Analysis: 7 Powers and Porter's 5 Forces

To understand why WuXi Biologics' competitive position is so durable—or to understand the risks to that durability—it helps to apply the rigorous frameworks that serious investors use to evaluate business quality.

Start with Hamilton Helmer's 7 Powers, the framework for identifying the sources of persistent differential returns. WuXi Biologics exhibits at least three of the seven powers in force, and possibly a fourth.

The primary power is Switching Costs, and it is worth dwelling on because it is the single most important driver of WuXi's business quality. When a biologic drug is developed and approved by the FDA, the manufacturing process is effectively "locked in" as part of the regulatory filing. The process is not just a recipe—it is a precisely documented, validated, and inspected set of procedures tied to a specific facility, specific equipment, and specific personnel training programs. Moving that process to a different facility is not like switching from one contract manufacturer to another in the widget business. It requires a formal regulatory submission, new facility inspections, process validation studies, and often new clinical comparability studies to demonstrate that the drug produced at the new facility is identical to the drug produced at the old one. This process can take two to three years and cost tens of millions of dollars. For a drug generating hundreds of millions in annual revenue, the opportunity cost of disruption during the transfer is even larger than the direct costs. The result is that once a drug is approved in a WuXi facility, the client is effectively locked in for the commercial life of that product—which, for a successful biologic, can be ten to twenty years.

The second power is Scale Economies. WuXi's global network of more than fifteen manufacturing sites gives it capabilities that smaller CDMOs simply cannot match. It can shift production between sites to accommodate demand fluctuations. It can offer clients manufacturing in multiple geographies to satisfy local regulatory preferences. Its purchasing power for raw materials—cell culture media, single-use consumables, chromatography resins—gives it cost advantages that grow with scale. And the fixed costs of its research and development platform are spread across six hundred-plus projects, giving each incremental project a lower effective R&D cost than a smaller competitor managing fifty projects.

The third power is what Helmer calls a Cornered Resource—an asset that competitors cannot readily replicate. For WuXi, this is its army of over twelve thousand scientists and engineers in China. The talent pool exists because of a unique combination of factors: China's enormous STEM education pipeline, WuXi's reputation as a premier employer for biologists in the country, and the cost differential that allows WuXi to employ five scientists for the cost of one in Boston or Basel. No Western CDMO can replicate this talent base at this scale and this cost. Samsung Biologics in South Korea has scale but is concentrated in a single geography. Lonza has global reach but at far higher labor costs. The WuXi scientist army is a resource that exists at the intersection of geography, education infrastructure, and decades of institutional investment in training—and it cannot be recreated overnight.

A possible fourth power is Process Power—the accumulated know-how embedded in WuXi's operations that allows it to deliver faster and more reliably than competitors. The "WuXi Speed" advantage is not just about single-use bioreactors. It reflects thousands of small process optimizations, institutional learning from six hundred-plus projects, and a culture of execution that has been built over more than a decade. This kind of embedded operational knowledge is difficult for competitors to observe, let alone copy.

Now turn to Porter's Five Forces for a view of the industry structure.

The Bargaining Power of Buyers is bifurcated. Large pharmaceutical companies like Pfizer, Roche, or AstraZeneca have significant bargaining power—they represent large contracts, they have (or could build) internal manufacturing capabilities, and they can credibly threaten to take their business elsewhere. But these big pharma companies represent only a portion of WuXi's client base. The much larger number of clients are small and mid-sized biotech companies—the hundreds of venture-backed firms that have a promising drug candidate but no manufacturing capability of their own. For these companies, bargaining power is low. They need capacity, they need speed, and they have neither the capital nor the expertise to build their own factories. WuXi is often the only realistic option for getting a drug manufactured at the quality and speed required for regulatory approval.

The Threat of New Entrants is moderate but constrained by high barriers. Building a biologics manufacturing facility requires hundreds of millions of dollars in capital, several years of construction time, and a workforce with highly specialized skills. Regulatory approval for a new facility adds additional time and uncertainty. The established players—WuXi, Samsung Biologics, Lonza, Boehringer Ingelheim—benefit from the track records and regulatory relationships that new entrants lack. However, government-backed initiatives to build domestic CDMO capacity in the US and Europe could gradually create new competitors, particularly if supported by policy incentives driven by supply chain security concerns.

The Threat of Substitutes is low and arguably declining. Biologics represent the future of medicine. The pharmaceutical industry's pipeline is increasingly dominated by large-molecule drugs—antibodies, ADCs, cell therapies, gene therapies. Small molecule drugs are not going away, but the growth and innovation are overwhelmingly in biologics. There is no substitute for a manufacturing partner that can produce these complex molecules. The question is not whether the world needs biologics CDMOs; it is which CDMOs will capture the demand.

The Rivalry Among Existing Competitors is intense but segmented. At the top tier, WuXi competes with Samsung Biologics (the Korean giant with massive stainless steel capacity), Lonza (the Swiss incumbent with deep expertise in mammalian and microbial systems), and Boehringer Ingelheim (the German pharmaceutical company with a significant CDMO arm). Chinese competitors like Asymchem and Pharmaron are present but generally more focused on small molecules or specific niches. The competitive dynamics are less about price wars and more about capacity availability, speed, quality track record, and geographic coverage. WuXi's differentiation—the combination of speed, scale, integrated services, and cost—positions it favorably, but no CDMO has the market to itself.

The Bargaining Power of Suppliers is worth noting as a potential risk. WuXi is dependent on suppliers of critical raw materials—most notably, the single-use bioreactor bags and assemblies that are central to its manufacturing strategy. During the COVID-19 pandemic, supply chain disruptions in single-use consumables caused significant challenges across the industry. While WuXi has worked to diversify its supply base and even develop some in-house capabilities, the concentration of single-use technology suppliers (dominated by companies like Cytiva and Sartorius) represents a structural vulnerability.

Taken together, the power analysis paints a picture of a company with durable competitive advantages, strong switching costs, and significant scale benefits—but one that is not immune to disruption, particularly from geopolitical forces that could alter the industry's competitive landscape in ways that pure business analysis cannot fully anticipate.

VIII. Inflection Point 2: The COVID Surge and The Geopolitical Pivot

The COVID-19 pandemic was, for WuXi Biologics, both the greatest validation of its business model and the catalyst for its most serious strategic challenge.

When the pandemic struck in early 2020, the global pharmaceutical industry faced an unprecedented manufacturing challenge: produce billions of doses of vaccines and therapeutic antibodies in a timeframe that would normally be measured in years, not months. The established vaccine manufacturers—Serum Institute of India, Sanofi, GSK—had capacity, but not nearly enough. The mRNA vaccines from Pfizer-BioNTech and Moderna were revolutionary but required entirely new manufacturing processes. And the viral vector vaccines, like AstraZeneca's, needed biologics manufacturing capacity of exactly the type that WuXi specialized in.

WuXi Biologics stepped into the breach. The company supported the manufacturing of AstraZeneca's COVID-19 vaccine and provided CDMO services for numerous other COVID-related programs. The pandemic "stress-tested" WuXi's global manufacturing network in a way that no peacetime scenario could have, and the company passed the test. Revenue nearly doubled from 5.6 billion yuan in 2020 to 10.3 billion yuan in 2021, driven by a surge in both COVID-related work and the broader acceleration of biologic drug development that the pandemic catalyzed. Gross margins expanded to nearly 47 percent—the highest in the company's history—as capacity utilization soared.

But the pandemic also set in motion a chain of geopolitical events that would pose the most serious threat to WuXi's business model. The experience of depending on a Chinese company for critical pharmaceutical manufacturing infrastructure—at a time when US-China relations were deteriorating rapidly—raised alarm bells in Washington, London, and Brussels. The strategic vulnerability was obvious: if geopolitical tensions escalated to the point of trade restrictions or sanctions, the West's access to a significant portion of its biologic drug manufacturing capacity could be disrupted.

The most concrete manifestation of this concern was the proposed Biosecure Act in the United States. The legislation, which gained bipartisan support in Congress, sought to restrict US government-funded entities from contracting with certain Chinese biotechnology companies, with WuXi entities explicitly named as potential targets. The bill sent shockwaves through the biotech industry—not because of its immediate impact, which was limited, but because of what it signaled about the direction of US policy. If the Biosecure Act passed in its proposed form, US government-funded research institutions, the Department of Defense, and potentially any company receiving federal grants or contracts would be prohibited from using WuXi's services.

The market reaction was severe. WuXi Biologics' share price, which had peaked at around HKD 148 in mid-2021 during the COVID-era euphoria, entered a prolonged decline that took it below HKD 20 by early 2024—a drawdown of more than 85 percent from peak to trough. The sell-off reflected not just the Biosecure Act risk but also a broader de-rating of Chinese biotechnology companies, the normalization of COVID-related revenues, and concerns about overcapacity in the CDMO industry as pandemic-era demand faded.

WuXi's response to the geopolitical challenge has been to accelerate what it calls its "Global-Local" strategy—building manufacturing capacity outside of China at a pace that demonstrates to clients and regulators that the company can serve Western markets from Western facilities. The investments in Worcester, Massachusetts, in Dundalk, Ireland, and in Singapore are all part of this strategy. The message to clients is clear: you can have WuXi's speed, quality, and cost advantages without the geopolitical risk of depending solely on Chinese facilities. Your drug can be manufactured in the US by a US-based WuXi subsidiary, using American workers, under the supervision of the FDA.

Whether this strategy will be sufficient to neutralize the geopolitical risk is one of the most consequential questions facing the company. The Biosecure Act, as of early 2026, had not been enacted into law in its original form, but the legislative threat remained and the broader trajectory of US-China decoupling continued to create uncertainty for Chinese companies operating in strategically sensitive industries. For WuXi, the challenge is that the "TSMC of Biotech" analogy cuts both ways: just as TSMC's dominance of chip manufacturing created concerns about Taiwan dependency that are reshaping the semiconductor industry, WuXi's dominance of biologics manufacturing is creating concerns about China dependency that could reshape the pharmaceutical industry.

The post-COVID financial trajectory tells the story of a company navigating this transition. Revenue growth decelerated from the torrid pace of the pandemic years—from 83 percent growth in 2021 to 48 percent in 2022, then to roughly 12 percent in 2023 and 10 percent in 2024. Net income, which had peaked at 4.4 billion yuan in 2022, settled at approximately 3.4 billion yuan in both 2023 and 2024. The market has been recalibrating its expectations from "hyper-growth" to "steady compounder"—a transition that is common for companies that have passed through their most explosive growth phase but one that is complicated by the overlay of geopolitical uncertainty.

The share price, trading around HKD 34 as of March 2026, represents a market capitalization of roughly HKD 141 billion—about one-sixth of the peak valuation reached during the pandemic. At this level, the enterprise value to EBITDA multiple is approximately ten times, a significant discount to the multiples that the company and its peers have historically commanded. The market is effectively pricing in a meaningful probability of adverse geopolitical outcomes—or, alternatively, it is offering long-term investors a compelling entry point into a business whose fundamental competitive advantages remain intact.

IX. Playbook: Lessons for Founders and Investors

The WuXi Biologics story, stripped to its essentials, offers three strategic lessons that extend far beyond the biotech industry.

The first lesson is what might be called the Infrastructure Play: do not dig for gold; sell the shovels—and then own the mine. The pharmaceutical industry is littered with the wreckage of companies that bet everything on a single drug candidate. For every Humira or Keytruda, there are hundreds of drugs that failed in clinical trials, destroying billions of dollars of investor capital along the way. WuXi Biologics found a way to participate in the pharmaceutical value chain without taking on the binary risk of drug development. By positioning itself as the manufacturing infrastructure that all drug developers need, WuXi earns revenue regardless of which specific drugs succeed or fail. Its revenue is diversified across six hundred-plus projects, and any individual project failure has minimal impact on the overall business. This is the "toll booth" model at its purest: every car on the highway pays, no matter where it is going.

The insight for founders is that in any industry undergoing rapid growth, there is usually an infrastructure layer that is undersupplied and underappreciated. In the early days of the internet, it was server hosting and cloud computing—which is how Amazon Web Services became Amazon's most profitable business. In the electric vehicle revolution, it is battery manufacturing—which is why companies like CATL have become indispensable. In biotech, it is manufacturing capacity. The founders who identify these infrastructure opportunities and build platforms to serve them can create businesses that are more durable, more predictable, and ultimately more valuable than the companies they serve.

The second lesson is that Speed Can Be a Moat. In the biotech industry, the economics of speed are staggering. A blockbuster biologic drug can generate a billion dollars or more in annual revenue. Every month of delay in getting that drug to market represents roughly eighty to one hundred million dollars in foregone revenue. Against that backdrop, a CDMO that can shave six to twelve months off the timeline from process development to commercial manufacturing is not just a vendor—it is a strategic partner whose speed advantage justifies a significant price premium.

WuXi turned speed into a systematic capability through its bet on single-use bioreactors, its integrated "Follow the Molecule" model, and its willingness to invest in capacity ahead of demand. The lesson is broadly applicable: in any industry with high time-value—software, construction, logistics—a company that can reliably deliver faster than competitors can turn that speed into a durable competitive advantage, provided it is backed by genuine operational capability rather than cutting corners on quality.

The third lesson is about Platform Economics: how to use a high-margin service business to fund a high-moat manufacturing business. WuXi Biologics' early revenues came from relatively high-margin research and development services—process development, cell line engineering, analytical testing. These services were capital-light and generated cash that could be reinvested into the capital-heavy manufacturing infrastructure. As the manufacturing business grew, it generated its own cash flows, which in turn funded further expansion. The result was a virtuous cycle where the service business funded the factory business, the factory business deepened client relationships, and deeper relationships generated more service revenue.

This "services-to-infrastructure" evolution is a playbook that has been applied successfully in numerous industries. It requires patience—the manufacturing business takes years to build and even longer to optimize—but it creates a competitive position that is far more defensible than either the service business or the manufacturing business would be on its own. The combination of high-margin upstream services and high-moat downstream manufacturing is the structural foundation of WuXi's business quality.

For investors, the meta-lesson from WuXi is about the power of embedded optionality. When you invest in a company with six hundred active projects spanning the full lifecycle of drug development, you are not making a bet on any single drug. You are making a bet on the productivity of the pharmaceutical industry as a whole. Each project in the pipeline represents a potential commercial manufacturing contract—a stream of predictable, high-margin revenue that could last for a decade or more. The question is not whether biologic drugs will continue to be developed and manufactured—they will. The question is whether WuXi will remain the preferred manufacturing partner, and whether geopolitical forces will disrupt the business model before the embedded optionality is fully realized.

X. Bear vs. Bull Case and Key Metrics

Every great investment thesis has a worthy adversary. WuXi Biologics is no exception.

The Bear Case rests on three pillars. First, geopolitical decoupling. If the United States and its allies decide that dependence on Chinese biologics manufacturing is a strategic vulnerability—in the same way that dependence on Taiwanese semiconductors is viewed as a vulnerability—the result could be a systematic effort to repatriate manufacturing capacity to the West. The Biosecure Act is the leading edge of this movement, but the broader trend extends beyond any single piece of legislation. A world in which US and European biotechs are incentivized or required to use domestic CDMOs would fundamentally alter WuXi's addressable market. The company's investments in overseas facilities would partially offset this, but the cost structure of operating in Massachusetts or Ireland is fundamentally different from operating in Wuxi, and the margin and competitive advantages would be significantly diminished.

Second, overcapacity. The pandemic triggered a massive wave of investment in biologics manufacturing capacity—not just by WuXi, but by Samsung Biologics, Lonza, and numerous smaller players. If demand growth does not keep pace with capacity additions, the result will be pricing pressure that compresses margins across the industry. WuXi's revenue growth deceleration from 83 percent in 2021 to 10 percent in 2024 may reflect not just the normalization of COVID-related demand but also the early stages of a capacity cycle that could pressure utilization rates and pricing power for years.

Third, concentration risk. WuXi's business is ultimately dependent on the health of the global pharmaceutical R&D ecosystem. A sustained downturn in biotech funding—driven by higher interest rates, tighter venture capital markets, or a series of high-profile clinical trial failures—could reduce the flow of new projects into WuXi's pipeline. The "Follow the Molecule" flywheel works best when new molecules are constantly entering the system. If the pipeline dries up, the flywheel slows.

The Bull Case is equally compelling. The biological "backlog" is real and growing. WuXi Biologics has over six hundred active integrated projects, representing a multi-year revenue pipeline that is largely insulated from short-term fluctuations in new business activity. The backlog is not just a number—it reflects hundreds of molecules progressing through clinical trials, each of which represents a potential commercial manufacturing contract worth millions of dollars per year. Even in a scenario where new project wins decelerate, the existing backlog provides substantial revenue visibility.

The structural demand tailwind is powerful. Biologics represent the future of pharmaceutical development. The pipeline of monoclonal antibodies, ADCs, bispecific antibodies, and other novel modalities is larger than it has ever been. The biosimilar wave—generic versions of off-patent biologic drugs—is just beginning, and it will require massive manufacturing capacity that most biosimilar companies do not have internally. The global biologics market is projected to continue growing at high single-digit to low double-digit rates for the foreseeable future, and WuXi is positioned to capture a disproportionate share of that growth.

The valuation today may already reflect the bear case. At roughly ten times trailing EBITDA, WuXi Biologics trades at a significant discount to its historical multiples and to the multiples of Western peers like Lonza, which typically commands fifteen to twenty times EBITDA. If the geopolitical risks prove manageable—if the "Global-Local" strategy succeeds in reassuring Western clients—the re-rating potential is substantial. And the optionality from the XDC, vaccine, and microbial businesses is arguably being given away for free at the current valuation.

The competitive landscape supports WuXi's position. Among its HKSE-listed peers, WuXi XDC (2268.HK) trades at a HKD 68 billion market cap—roughly half of the parent company—suggesting the market assigns significant standalone value to the ADC franchise. Pharmaron (3759.HK), a smaller CRO/CDMO peer, trades at HKD 51 billion. Asymchem (6821.HK), more focused on small molecules, sits at HKD 27 billion. None of these competitors matches WuXi's scale, breadth of services, or global manufacturing footprint in biologics. Samsung Biologics in Korea is the closest true competitor, but it operates with a different model—large stainless steel facilities rather than the flexible single-use approach—and lacks the integrated discovery-to-manufacturing platform that defines WuXi's value proposition.

The KPIs That Matter

For investors tracking WuXi Biologics' ongoing performance, two metrics stand above all others.

The first is Total Integrated Projects, broken down by phase (pre-clinical, Phase I, Phase II, Phase III, and commercial). This is the North Star metric for the business. It is the leading indicator of future revenue, the measure of flywheel velocity, and the metric to which management compensation is tied. A growing total project count—particularly growth in the later phases—signals that molecules are progressing through the system and converting from low-revenue development projects into high-revenue commercial manufacturing contracts. A declining project count, or a failure of projects to advance from early to late stages, would be the earliest warning sign of deteriorating competitive position.

The second is Revenue from Non-China Facilities as a Percentage of Total Revenue. This metric captures the progress of the "Global-Local" strategy—the single most important strategic initiative for the company in the current geopolitical environment. As WuXi brings its facilities in Ireland, the US, and Singapore to full operational capacity, the share of revenue generated outside China should steadily increase. A rising non-China revenue share would signal that the company is successfully de-risking its business from geopolitical concentration. A stagnating or declining share would suggest that the overseas expansion is failing to gain traction, leaving the business more vulnerable to decoupling risks.

The WuXi Biologics story is, at its core, a story about the tension between two powerful forces. On one side, the inexorable logic of specialization and scale—the same logic that made TSMC the center of the semiconductor world, that made Foxconn the center of electronics manufacturing, and that made WuXi the center of biologics manufacturing. On the other side, the equally powerful force of geopolitical fragmentation—the recognition by governments that strategic dependence on any single country for critical infrastructure carries unacceptable risks. How this tension resolves will determine not just the future of WuXi Biologics, but the future of how the world manufactures the medicines that keep its people alive. It is a company that sits, quite literally, at the intersection of science, commerce, and geopolitics—and the outcome matters far beyond the pages of any financial report.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube