WuXi XDC: The Architecture of the Magic Bullet

I. Introduction: The "Magic Bullet" Gold Rush

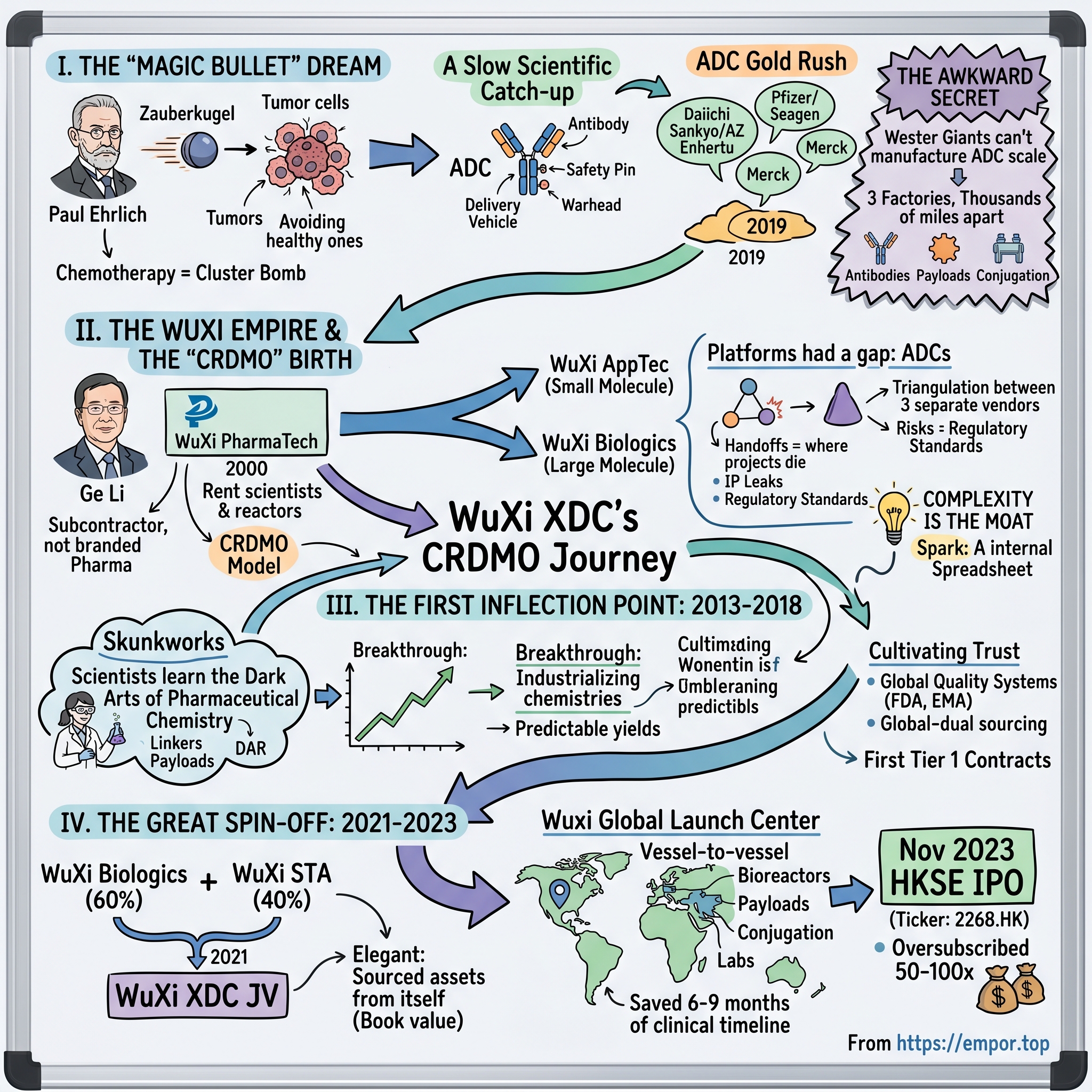

Picture a laboratory in Frankfurt at the dawn of the twentieth century. Paul Ehrlich, a bearded chemist who had already won a Nobel Prize, was pacing between his chemical reagents, obsessing over a question that would haunt oncology for the next hundred years. What if a drug could travel through the bloodstream like a guided projectile, find only the diseased cell, and ignore every healthy one it passed? He called this hypothetical weapon a Zauberkugel, a "Magic Bullet." For a century after he coined the term, the phrase remained a metaphor. Chemotherapy, the dominant cancer treatment of the twentieth century, was the exact opposite of a magic bullet. It was closer to a cluster bomb—poisoning the entire body in the hope that the tumor would die faster than the patient.

Then, slowly, the science caught up with the dream. Researchers figured out how to chemically bolt a cell-killing toxin onto a monoclonal antibody, a protein that knows how to recognize a tumor's surface protein. The antibody became the delivery vehicle. The toxin became the warhead. The chemical leash between them, called a "linker," became the safety pin. This three-part molecule earned a drab industrial acronym: the ADC, or antibody-drug conjugate.

And then, around 2019, the category exploded. Daiichi Sankyo and AstraZeneca's Enhertu posted clinical results so strong in HER2-low breast cancer that a 2022 oncology conference audience literally stood up to applaud. Pfizer paid $43 billion for Seagen in 2023. Merck poured billions into Kelun-Biotech partnerships. The pharmaceutical industry, which had been whispering about ADCs for a decade, suddenly had every major CEO repeating the same line on earnings calls: we need an ADC franchise.

But here is the awkward secret of the modern ADC gold rush. Almost none of these Western giants actually know how to manufacture an ADC at commercial scale. Making one requires three factories that normally live thousands of miles apart—one that grows antibodies in living cells, one that synthesizes toxic small-molecule payloads in reactors behind blast walls, and one that carefully bolts the two together without scrambling the protein or diluting the poison. It is wet chemistry, living biology, and nuclear-grade containment all under one roof.

Which is where our company enters the story. WuXi XDC Cayman Inc., trading under 2268.HK on the Hong Kong Stock Exchange, is not making the bullets. WuXi XDC is the high-precision armory where nearly every general of the pharmaceutical world has outsourced the construction of their magic bullets. As of its most recent disclosures, the company captured roughly 9.8% of the global ADC outsourced manufacturing market and had grown from a small internal team to a multi-billion-dollar public company in under a decade. Its November 2023 IPO on the HKSE was oversubscribed dozens of times in what was arguably the worst biotech funding winter in fifteen years.

The thesis for this episode is simple. Drug companies bet on specific molecules. WuXi XDC bet on the complexity of making those molecules. That is a very different, and in many ways more durable, business. Let us unpack how they built it.

II. The Genesis: The WuXi Empire & The "CRDMO" Birth

To understand WuXi XDC, you have to first understand the strange and underappreciated empire that produced it. In 2000, a chemist named Ge Li returned to Wuxi, a mid-sized industrial city between Shanghai and Nanjing, and founded WuXi PharmaTech. His bet was deceptively simple. Western pharma spent enormous sums on bench chemists and process engineers. China had more chemistry PhDs than any country on earth and paid them a fraction of the American rate. Ge Li did not try to build a Chinese Pfizer. He built the subcontractor to Pfizer.

That decision was heretical at the time. Every ambitious Chinese healthcare founder in the early 2000s wanted to build a branded pharma empire. Ge Li went the other way. He built what became known as the CRDMO model—contract research, development, and manufacturing organization. The company would never own its own drugs. It would simply rent its scientists, reactors, and bioreactors to anyone with a molecule worth advancing.

The result was extraordinary. WuXi AppTec, the small-molecule arm, and WuXi Biologics, the large-molecule arm that spun out separately in 2017, became the plumbing of global drug discovery. By the late 2010s, if you worked in oncology at any top-twenty pharma company, you had a WuXi project. Most people outside the industry had never heard of the company. Inside it, they were the quiet kingmakers.

But the platform had a gap, and it was a gap that would soon matter enormously. In the early 2010s, if a pharmaceutical company wanted to build an antibody-drug conjugate, it had to awkwardly triangulate between three separate vendors. Someone needed to make the antibody. Somewhere else, someone needed to synthesize the toxic payload under high-containment conditions—these are molecules so potent that a few micrograms can kill a cell, and you do not want them floating around a normal pharmaceutical plant. Finally, a third party had to design and attach the linker, the chemical bridge that decides when and where the payload releases.

Three vendors meant three contracts, three quality audits, three shipping chains, and, critically, three chances for something to go wrong. The handoffs were where projects died. An antibody that was pristine when it left Boston arrived slightly degraded in New Jersey. A payload synthesized in Switzerland failed stability tests after shipping. Timelines slipped by quarters, and in drug development, a lost quarter can translate into a lost year of patent-protected revenue on the back end.

The spark at WuXi was not a eureka moment. It was, more prosaically, a spreadsheet. Internal project managers at WuXi Biologics and WuXi STA (the small-molecule sibling) kept seeing the same clients trying to orchestrate ADC programs across both companies and a handful of external vendors. The friction was visible, measurable, and—if you believed the trend lines on ADC clinical trials—about to multiply tenfold.

Complexity, the WuXi team began to realize, was not the problem. Complexity was the moat. If you could internalize all three disciplines—biologics, small molecule, and conjugation—under one quality system and one project manager, you would not just win business. You would lock it in. The question was whether to bolt this offering onto the existing companies, or whether to build something new.

III. The First Inflection Point: 2013–2018

In 2013, deep inside WuXi Biologics's Wuxi campus, a small team of maybe a dozen scientists was given an unusual mandate. They were told to stop working on antibodies, at least directly, and instead figure out how to glue antibodies to toxic warheads without destroying either one. This was not a company. It was not even a business unit. It was closer to an internal skunkworks, funded almost as an R&D line item, with no clear revenue expectation for several years.

The science they were learning was, to borrow a phrase, the dark arts of pharmaceutical chemistry. Antibodies are large, fragile, three-dimensional proteins with dozens of reactive sites. A toxin is a small, greasy molecule that badly wants to fall apart or fall off. A linker has to be stable enough to survive the bloodstream for days but cleavable enough to release the payload once inside a tumor cell's acidic compartments. Get any of the three wrong and the drug either kills healthy tissue or does nothing at all.

There is a manufacturing concept called DAR, or drug-to-antibody ratio. An ADC with too little payload will not kill the tumor. Too much, and the antibody gets so loaded with greasy warheads that it clumps, aggregates, and the patient's immune system rejects it. Early ADC manufacturers routinely lost a third or more of their material to aggregation. Yields in the forties and fifties percent were considered acceptable. In any normal manufacturing industry, those numbers would be grounds for firing a plant manager. In ADC-land, they were standard.

The WuXi team's breakthrough, hammered out between 2014 and 2017, was less about inventing a new chemistry than about industrializing existing chemistries to the point where yields became predictable. Process analytics. In-line monitoring. Reactor designs borrowed from WuXi STA's experience with highly potent small molecules. By 2018, internal yield figures had improved enough that WuXi could quote a fixed price and a fixed timeline to a global client, which was close to a revolutionary statement in that sector.

But technical capability is only half the equation. The other half is trust. In 2015 and 2016, a Chinese contract manufacturer walking into a boardroom at a Tier 1 global pharma and asking to handle the most sensitive intellectual property in the oncology pipeline was, frankly, an unusual request. Western clients had two fears. First, would their IP leak? Second, would a Chinese FDA inspection meet US FDA standards?

WuXi's answer to both was cultural, not technical. They hired heavily from Western pharma. They built quality systems that were audited not just by the Chinese NMPA but by the US FDA and the European EMA directly. They pitched a model they called "global-dual sourcing"—a client could manufacture simultaneously in both China and, later, the United States through WuXi's Philadelphia site. If geopolitics got ugly, no single client program would be stranded on one side of an ocean.

The first Tier 1 contracts landed between 2016 and 2018. None were publicly disclosed, which is standard in the CRDMO world. What mattered was that once those contracts were in place, they unlocked a reference effect. The second client signed faster than the first. The fifth signed faster than the second. By the end of 2018, the ADC skunkworks inside WuXi Biologics was no longer a skunkworks. It was a fast-growing business line with a backlog and a waiting list.

That combination of technical moat and client momentum is the thing that sets the stage for what happens next: the decision to spin it out, merge the relevant assets from two parent companies, and put a ticker on the result.

IV. The Great Spin-Off: 2021–2023

Corporate structure is normally the most boring topic in finance. In WuXi XDC's case, it is actually the most important one, because the way the company was assembled explains why it makes so much money relative to its nominal capital base.

The story picks up in June 2021. WuXi Biologics, the Hong Kong-listed biologics arm, and WuXi STA (later rebranded as part of WuXi AppTec's small-molecule CDMO), the small-molecule arm, executed a joint venture. WuXi Biologics contributed 60%. The STA side contributed 40%. Into this JV went all of the ADC-relevant conjugation assets, the payload and linker synthesis capability, the analytical infrastructure, and—critically—the existing client book.

Now, here is the piece that is easy to miss. In 2021, the global ADC CDMO market was white-hot. Lonza had just spent billions expanding capacity. Catalent was acquiring conjugate capabilities at valuations of fifteen to twenty times revenue. If WuXi had chosen to acquire its way into the space, it would have paid through the nose for assets and carried a mountain of goodwill onto its balance sheet for the next decade.

Instead, WuXi did something far more elegant. It sourced the assets from itself. The joint venture transferred capabilities from WuXi Biologics and WuXi STA at roughly book value. There was no premium to a third party, no auction, no banker's fee calibrated to a frothy comparable transaction. The JV walked out of 2021 with Tier 1 ADC capabilities and a balance sheet that looked almost suspiciously clean.

The second piece of the structural bet was geographic. Rather than distribute its ADC operations across multiple cities, WuXi XDC concentrated the core of its global capacity in Wuxi itself, in what management internally referred to as a "Global Launch Center." Antibodies grew in bioreactors on one floor. Highly potent payloads were synthesized in containment suites on another. Conjugation reactors sat in between. Analytical labs sat across the courtyard.

The industry shorthand for this design was "vessel-to-vessel." A client's antibody never left the campus between production and conjugation. There were no customs inspections between steps, no cold-chain shipping, no chain-of-custody paperwork multiplying across borders. For a typical ADC development program, that integrated campus shaved roughly six to nine months off the clinical timeline. In oncology, where commercial drugs often clear a billion dollars of annual revenue at peak, nine months of earlier patent-clock start is worth a very large number.

The capital markets took about twenty-four months to absorb what WuXi had built. On November 17, 2023, WuXi XDC listed on the Hong Kong Stock Exchange. The context matters. The biotech winter of 2022 and 2023 had been brutal. The XBI biotech index had been cut in half from its 2021 peak. IPOs had become rare, and Hong Kong IPOs had become rarer. Many observers assumed the WuXi XDC deal would be delayed, downsized, or pulled.

Instead, the institutional book closed oversubscribed roughly 50 times over. The retail tranche was oversubscribed more than 100 times. The stock opened above its IPO price and kept going. What investors saw, in an otherwise desolate biotech landscape, was a business that combined three features almost never seen together: high growth, genuine profitability, and a visible multi-year backlog.

The listing did more than raise capital. It effectively separated WuXi XDC's narrative from the broader WuXi group, which was already fielding difficult questions from Washington about the Biosecure Act. Having an independently listed entity with its own governance, its own disclosures, and its own investor base gave clients, especially Western clients, something they could point to internally as a clean counterparty. That narrative hygiene would matter a great deal within twelve months.

V. The Management: The Executioners

Drug industry profiles often default to a familiar template. There is a charismatic scientist-founder. There is a pivotal patent. There is a garage, or at least a university laboratory. WuXi XDC does not fit that template, and the mismatch is itself the story.

Dr. Jimmy Li, the chief executive, is not a charismatic founder-innovator. He is something rarer and, for a CDMO, far more valuable. He is an industrializer. His career arc ran through the WuXi Biologics apparatus, where he oversaw process development and manufacturing operations during the period when WuXi was figuring out how to turn laboratory-scale antibody chemistry into reliable, FDA-inspectable commercial output. He is an engineer by temperament, a manager by practice, and a project manager by religion.

Walk into a WuXi XDC review meeting, by the account of former clients who have described the experience in public presentations, and the first thing you see is not a whiteboard covered in molecular structures. It is a Gantt chart. Deadlines, handoffs, batch release dates, regulatory filing windows, and client decision points are tracked in a granularity that Western pharma project managers describe, with some envy, as "obsessive." The phrase internally used for this is "WuXi Speed." It is not marketing. It is a cultural artifact, and it is arguably the single most important competitive asset the company owns.

Think about what WuXi Speed actually means in a client's cost model. Every month of delay in early clinical development burns between several hundred thousand and a few million dollars in direct trial costs. It also eats into the effective commercial patent life at the back end. A CDMO that can reliably compress a timeline by a quarter is not saving the client a quarter's worth of fees. It is saving them potentially tens of millions in peak-year revenue. That is why clients tolerate premium pricing, and it is why WuXi XDC's gross margins run meaningfully above those of many Western CDMO peers.

The incentive structure reinforces the culture. WuXi XDC operates with an RSU-based management compensation scheme that vests over multiple years and is tied to both operational metrics and the parent group's reputation. That last phrase matters. The Li family of WuXi entities—WuXi AppTec, WuXi Biologics, WuXi XDC—share a brand, share clients, and share, to a meaningful degree, personnel. A reputational failure at one ricochets through all three. Management compensation is structured to make sure no executive has an incentive to extract short-term gain at the expense of the broader ecosystem.

There is also an under-appreciated governance nuance. WuXi Biologics, as the majority shareholder, retains a strong steward role over WuXi XDC. That relationship has pros and cons. On the pro side, it ensures that capital allocation decisions are informed by the deep operational knowledge of the parent. On the con side, it means minority shareholders have to trust that the parent will not extract value at their expense—through, for example, priced related-party transactions or the allocation of joint clients. To the credit of the management team, disclosures around related-party dealings have remained detailed, and pricing of inter-group services is benchmarked to arm's-length equivalents with some rigor.

Jimmy Li's own public appearances reinforce the execution-first brand. At industry conferences, he speaks in metrics, not in vision statements. He describes capacity expansions, hiring plans, and backlog dynamics. He does not forecast which molecule will win in 2030. That restraint is, in a sector full of scientific promise theater, almost refreshing. It is also, commercially, precisely what big pharma clients want from their manufacturing partner. The partner's job is to deliver, not to dream.

With the culture and leadership established, the next question becomes: what exactly is the shape of the business that these executioners are running?

VI. The Hidden Business: Beyond ADCs

The "X" in WuXi XDC is the most commercially interesting letter on the company's masthead, and almost no one outside the industry notices it. XDC stands not for antibody-drug conjugates specifically, but for bioconjugates more broadly. The X is a wildcard. Whatever gets bolted onto an antibody-like targeting molecule—a toxin, a nucleic acid, an immune stimulator, a radioactive isotope—WuXi has positioned to make it.

That deliberate ambiguity is the company's longest option on the future. And within it, the fastest-growing sub-category right now is not the classic antibody-drug conjugate. It is the radionuclide drug conjugate, or RDC.

A quick layperson's translation is useful here. An RDC takes the same targeting concept—an antibody or a peptide that knows how to home in on a tumor-specific marker—but instead of a chemotherapy toxin, it carries a radioactive atom. When the targeting molecule lands on the cancer cell, the radioactive atom emits short-range radiation that shreds the cancer's DNA. Because the range is short, healthy tissue a few millimeters away is largely spared. It is, essentially, microscopic brachytherapy delivered by a protein postman.

RDCs had their blockbuster moment when Novartis's Pluvicto began posting strong clinical and commercial data in prostate cancer. Suddenly, half the major oncology developers wanted an RDC program. And, exactly as had happened with ADCs a decade earlier, those developers discovered that making an RDC at scale required chemistry, biology, and, in this case, radiation safety engineering—three disciplines that almost no one had under one roof.

WuXi XDC's RDC segment has grown from near zero to a meaningful revenue contributor in under three years. The company has publicly disclosed that RDC-related revenue is growing faster than its core ADC business, off a small base. That small base is precisely the point. Investors rarely get to buy into a platform where a second S-curve has already begun to compound before the first has matured.

It is worth pausing to walk through the segment architecture, because it reveals how the company's economics actually work. At the top of the funnel sits Discovery, which is pre-clinical work, small-dollar contracts, and a huge number of projects. Margins here are thin, but the strategic value is enormous because Discovery is where WuXi gets written into a project at its earliest possible moment. Once a client has used WuXi's linkers and processes in discovery, moving to a different CDMO later means recapitulating years of process knowledge.

The middle of the funnel is Development, which covers CMC—chemistry, manufacturing, and controls—work. This is where process development, scale-up, and regulatory filings live. Margins are better. More importantly, the intellectual property of how the drug is made becomes embedded in WuXi's filings. Transferring that IP elsewhere is technically possible and practically excruciating.

The bottom of the funnel is Commercial Manufacturing. This is where a drug that has cleared its clinical trials gets made at scale for paying patients. Margins here are the highest. Revenue per project is an order of magnitude larger. And switching costs are near-prohibitive, which is a point we will return to in the Powers framework discussion.

The most important internal metric to watch, for a company of this shape, is the flow of projects up the funnel. WuXi's disclosed pipeline, as of its most recent annual results presentation, showed a meaningful increase in the number of projects in Phase II and Phase III clinical trials relative to purely pre-clinical stage work. That migration up the funnel is the revenue cliff moving upward. It is the leading indicator of the next several years of commercial revenue, regardless of what the macro biotech environment does next quarter.

With the business segmented, we can look under the hood at why this structure is so durable.

VII. The 7 Powers & Porter's 5 Forces

Hamilton Helmer's 7 Powers framework is, in the author's biased view, the most useful strategic framework built in the last twenty years. It asks a simple question: why does this business, specifically, earn persistent abnormal returns? Applied to WuXi XDC, three of the seven powers stand out with unusual clarity.

The first, and arguably the most important, is Switching Costs. Once a drug has been approved by the FDA using a specific manufacturing process at a specific site, changing that process or that site requires a Prior Approval Supplement, or PAS. A PAS is not a paperwork exercise. It is a multi-year, multi-million-dollar regulatory project that requires comparability studies, stability data, and, often, bridging clinical trials. From the client's perspective, moving an approved ADC from WuXi's conjugation suite to a competitor's conjugation suite is roughly equivalent to re-running part of the clinical trial. No CFO wants to sign that purchase order.

This is the single most important moat in the entire CDMO industry, and it is stronger in ADCs than almost anywhere else in pharma because ADC manufacturing is more process-sensitive than, say, small-molecule tablet manufacturing. Every site has its own quirks. Every reactor has its own thermal profile. Every column has its own resin. A client who has spent three years de-risking WuXi's specific process is effectively locked in for the commercial life of the drug.

The second power is Cornered Resource, and here the cornered resource is human. The number of scientists and engineers globally who deeply understand linker-payload conjugation at commercial scale is, genuinely, in the low thousands. Not tens of thousands. Low thousands. They are concentrated in a handful of geographies. WuXi's Wuxi and Suzhou campuses employ a disproportionate share of them, and the talent pool is self-reinforcing: the best ADC scientists want to work where the most projects are, and the most projects are where the best scientists work. Competing CDMOs, including well-capitalized Western ones, have discovered that simply announcing a new ADC facility does not conjure a workforce capable of running it.

The third power is Scale Economies. An ADC manufacturing facility is ruinously expensive to build. High-containment suites, with their air handling, waste treatment, and personnel protection systems, cost a multiple of what a conventional biologics facility costs per square meter. A single client running a single drug program cannot amortize that cost efficiently. But a CDMO running one hundred programs concurrently can. The fixed cost gets spread thin. Overhead per project drops. The CDMO's per-program cost structure becomes one that no in-house client could rationally replicate, which is itself a strong argument against the "insourcing" bear thesis we will tackle in the next section.

Porter's Five Forces round out the picture. Start with the Bargaining Power of Buyers. AstraZeneca, Pfizer, Merck, and the other mega-pharma clients are, individually, more valuable than most CDMOs. In a normal industrial relationship, they would have enormous negotiating leverage. In ADC manufacturing, though, capacity is scarce. The number of high-quality ADC manufacturing slots available globally in any given year is measurably smaller than the number of projects competing for them. The scarcity flips the pricing power back to the CDMO—specifically to the CDMOs with proven regulatory track records and available slots, which is a short list with WuXi XDC near the top.

The Threat of Substitutes is the most nuanced force. One reasonable bear case is that alternative oncology modalities—CAR-T cell therapies, bispecific antibodies, naked antibodies, or cancer vaccines—could diminish the need for ADCs. The counter-argument is that ADCs are not substituting for other modalities so much as expanding the addressable frontier of oncology. A patient may receive a CAR-T for their hematologic malignancy and an ADC for their solid tumor, not one or the other. The clinical data over the last three years has tended to support expansion rather than substitution.

The Threat of New Entrants is moderate. Announcing an ADC facility is easy. Commissioning one that passes FDA inspection and consistently produces commercial-grade batches is a years-long, hundreds-of-millions-of-dollars undertaking. Some new entrants will succeed; most will not. Rivalry among existing players, mainly Lonza, Catalent (now part of Novo Holdings), and smaller specialty shops, is real but constrained by the same capacity shortage that gives the sector its pricing power. Finally, the Bargaining Power of Suppliers is low; inputs are commoditized, and WuXi's scale of purchasing further tilts the relationship in its favor.

What this means in plain language is that WuXi XDC sits inside an unusually favorable competitive geometry. The moats are not hypothetical. They are written into FDA inspection schedules and comparability protocols.

VIII. The Playbook: Lessons for Investors & Builders

Step back from the financials for a moment and look at the pattern. There is a reason this business looks the way it looks, and it is worth extracting the lessons because they generalize far beyond one Hong Kong-listed CDMO.

The first lesson is what could be called the "Vanguard Strategy," borrowing loosely from index investing's famous pitch. In a gold rush, you can either try to pick the winning miner or you can sell the picks, shovels, and denim jeans. The history of biotech is littered with investors who correctly identified that ADCs would be important and then lost money betting on specific ADC developers whose candidates failed in the clinic. Clinical trials are binary. Manufacturing is a distribution. If you believe the overall category of ADCs will grow, the CDMO captures a share of the entire distribution without needing to pick the winning molecule. This is, structurally, the same trade that made TSMC one of the most valuable companies in technology.

The second lesson is efficiency over ego. There is a near-irresistible temptation for a successful CDMO to eventually develop its own drugs. The margins on a marketed drug are vastly higher than the margins on a manufacturing contract. But the moment a CDMO develops its own drug, it becomes a competitor to its clients. Trust collapses. The moat that took a decade to build drains in a quarter. WuXi group's discipline around never developing its own branded drugs, even as tempting adjacent opportunities appeared, is one of the most quietly important strategic decisions in the company's history. It is a refusal to chase the short-term, higher-margin business in order to protect the long-term compounding of the core business.

The third lesson is about geopolitical resilience. The Biosecure Act, a piece of US legislation aimed at restricting federal contracts with certain Chinese biotech companies, hung over the entire WuXi ecosystem starting in 2024. The bill's path through Congress was uneven. It passed committee, stalled, was reintroduced, and has continued to bounce between legislative vehicles. But regardless of whether it ever becomes law, the overhang itself changed client behavior. Some US clients began asking for dual-source manufacturing, with at least one manufacturing site outside of mainland China, as a condition of new contracts.

WuXi XDC's response, rather than defensive lobbying, was operational. The company announced and began building out capacity in Singapore, with additional expansion slots in Europe, including Ireland. The Singapore site, in particular, is strategically interesting because it places WuXi XDC's operations in a jurisdiction with strong IP protection, robust regulatory infrastructure, and geographic proximity to both the Chinese operational nerve center and the growing Asian pharma client base. The capital commitment to these sites is not small, and in the short term it weighs on free cash flow. In the long term, it is arguably the most important single investment the company has made since its IPO.

That hedge does not eliminate the political risk. No amount of Singapore real estate makes a US client comfortable if US legislation specifically names the parent entity. But it changes the conversation from "can you operate outside China?" to "which of your operations do you want your program placed in?" And that is a far more commercially useful question to be asked.

The fourth, less-discussed lesson is about the compounding power of a reference-first sales motion. CDMOs do not win business through advertising. They win business through references. A program that goes well becomes three future programs, either from the same client or from its scientists when they move to other companies. WuXi XDC's client list is not public, but the order of magnitude is disclosed. The company has disclosed that a meaningful majority of the top global pharmaceutical companies are clients. That concentration of references creates a flywheel effect that is extremely difficult for a new entrant to disrupt, because the new entrant has no reference list.

Taken together, these four lessons sketch a playbook that applies well beyond pharma. Find the complexity no one else wants to manage. Refuse to compete with your customers. Hedge your jurisdictional risk operationally, not rhetorically. And let references do the selling.

IX. The Bear vs. Bull Case

No episode worth its runtime would end without a fair presentation of both sides. The honest bear case on WuXi XDC is not about valuation. It is structural.

Start with geopolitical decoupling. The Biosecure Act's ultimate form is unclear, but the broader direction of US-China biotech decoupling is not. Even if WuXi XDC is never specifically named, a chilling effect on US federal contracts, US academic collaborations, and US-funded clinical trials could slow client adoption at the margin. A meaningful share of WuXi's revenue comes from North American clients. Any policy that specifically penalizes those clients for routing work through Chinese CDMOs is a direct headwind, regardless of the Singapore hedge.

The second bear thesis is insourcing. Big Pharma, flush with cash, could decide that ADC manufacturing is too strategic to outsource and begin building its own facilities. Merck, AstraZeneca, and Johnson & Johnson have each made noises in this direction. The counterargument is that the per-project economics of an in-house ADC plant are brutal unless you have a very large ADC portfolio, and even then, the flexibility of CDMO capacity is hard to replicate. But the threat is real, and it deserves to be monitored, particularly at mega-pharma clients whose ADC pipelines are getting deep enough to justify the capital expenditure.

The third bear thesis is technological obsolescence. Linker chemistry is not static. New payload classes—topoisomerase inhibitors, immune modulators, degrader-based payloads—are advancing. A sufficiently disruptive linker or payload platform could theoretically render existing conjugation infrastructure less useful. WuXi's internal R&D investment is meant to stay ahead of this curve, but no incumbent manufacturer is immune from a platform shift. It is worth noting that in chemistry, unlike in software, platform shifts happen over years, not quarters, which gives incumbents time to retool. But time is not infinite.

A fourth, less macro concern is client concentration. Although WuXi XDC's client base spans a large share of the global pharmaceutical majors, any large CDMO will have a handful of clients whose projects dominate revenue in any given year. Disclosure of customer concentration should remain a watch item, particularly for revenue concentration that exceeds 10% from a single customer. Not disclosed at high granularity in public filings, so investors should keep an eye on it.

Now the bull case. The most important single bull argument is what might be called the "ADC-ification" of oncology. ADCs are, across multiple tumor types, starting to replace traditional chemotherapy as the standard of care. Enhertu's expansion in breast cancer is the flagship example. Similar replacement dynamics are emerging in urothelial cancer, lung cancer, and others. If you project the ADC market even conservatively from its 2025 base to 2030, you get growth rates that are extraordinary in a pharma context. WuXi XDC's market share does not need to expand for the business to grow rapidly; the underlying market's growth alone is sufficient.

The second bull argument is the RDC acceleration discussed earlier. The RDC category is where ADCs were around 2018: clinically validated, commercially tiny, and about to compound at triple-digit rates for several years. WuXi XDC is one of the few players globally with the chemistry, regulatory, and containment infrastructure to handle RDCs at scale, and it is compounding off a base measured in tens of millions of dollars today.

The third, more quantitative, bull argument is the backlog. WuXi XDC has disclosed a backlog that has grown into the hundreds of millions of dollars. A backlog of that size, for a company with the revenue base this one has, represents a meaningful multiple of forward-year revenue already locked in under signed contracts. In a world where most small-cap biotech companies cannot tell you what next quarter looks like, a multi-year visible revenue base is an unusual asset.

Combining the bear and bull cases in a Porter-adjacent framework, the final picture is this: WuXi XDC operates inside a competitive structure with unusually strong Hamilton Helmer powers (switching costs, cornered resource, scale economies), faces manageable but real Porter forces (buyer scarcity favoring the CDMO, substitution threat limited), and carries genuine geopolitical overhang that the company has addressed operationally but cannot fully eliminate.

If one had to identify the one-to-three key performance indicators for long-term fundamental investors to track, the shortlist would be: first, the backlog, because it is the single best leading indicator of forward revenue; second, the mix of projects by clinical stage, because projects migrating from pre-clinical to Phase III is the funnel moving toward commercial manufacturing; and third, the geographic mix of capacity and revenue, because that is the single cleanest barometer of how the company is navigating the geopolitical overhang. These three numbers, more than any others, will tell an investor whether the thesis is tracking or fraying.

X. Epilogue: The Future of Bioconjugation

There is a useful mental model for what WuXi XDC is, and it is worth stating plainly. WuXi XDC is the TSMC of bioconjugation. That analogy is not marketing hyperbole. It is structural. Like TSMC, WuXi XDC took a capability that the industry's leading designers had originally done in-house, externalized it with superior execution, and in doing so became the indispensable utility underneath a broad class of products. Like TSMC, WuXi XDC's customers are also its competitors, in the sense that many pharmaceutical companies at least notionally could do their own manufacturing. Like TSMC, most of them have concluded, one by one, that the CDMO does it better, faster, and more cheaply than they could justify doing it themselves.

The next chapter, already visible in outline, is geographic diversification. Singapore is not just a political hedge; it is a launchpad for serving Asian pharma, which is a rapidly maturing client base. Ireland and broader European capacity positions the company for European clinical and commercial supply. The 2030 vision, implicit in management's disclosed capex plans, is to run a genuinely multi-continental manufacturing network that offers any client, anywhere, the ability to source their bioconjugate drug from a jurisdiction of their choice.

The other chapter, less visible but possibly more important, is category expansion within bioconjugation. ADCs and RDCs are today's large categories. Tomorrow's categories likely include antibody-oligonucleotide conjugates, antibody-immune-stimulator conjugates, and combinations of modalities that have not yet been named. The central insight—that a targeting molecule plus a cargo equals a powerful drug—is likely to generate new permutations for at least another decade. The "X" in XDC was always a bet on that permutation space.

Paul Ehrlich died in 1915. He never saw his Magic Bullet. He would probably have been amused, or perhaps horrified, to discover that the realization of his dream required not a single brilliant chemist but an entire industrial apparatus spread across Wuxi, Suzhou, Shanghai, and now Singapore. But the dream itself—a drug that kills the tumor without touching the healthy cell—has, a century late, begun to come true. And the factory building the bullets has a ticker.

XI. Top 5 Recommended Links for the Show Notes

- The 2023 HKSE Prospectus for WuXi XDC Cayman Inc. — the closest thing to a "Bible" of the ADC outsourced supply chain, with industry sizing, segmentation, and competitive benchmarking that is not readily available anywhere else in public form.

- Nature Reviews Drug Discovery, "The next generation of antibody-drug conjugates" — the canonical scientific overview of where linker and payload chemistry is heading.

- WuXi XDC Annual Results Presentation — segment-level disclosure on RDCs, global disease coverage, and the project-stage funnel.

- The Biosecure Act Legislative Tracker — essential for calibrating the geopolitical overhang and its evolution through successive Congressional sessions.

- Jimmy Li's keynote presentations at the World ADC Conference — the closest available public articulation of the technical and operational vision from the executive directing it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube