Goldwind: The Direct Drive Dragon

I. Introduction & The "Tesla of Wind"

In the spring of 2024, when the Global Wind Energy Council published its annual rankings, something happened that would have been unthinkable a decade earlier. For the first time in the history of the modern wind industry, Chinese companies occupied the top four spots in global turbine installations. Vestas, the Danish pioneer that had essentially invented the commercial wind industry, had been pushed down the leaderboard. GE, the American industrial titan, had retreated. Siemens Gamesa, the German-Spanish engineering powerhouse, was nursing warranty losses that had bled billions from its parent company's balance sheet.

At or near the top of that list sat a company whose name most Western investors still could not pronounce confidently: Goldwind Science & Technology Co., Ltd., trading under the ticker 2208 on the Hong Kong Stock Exchange. The Chinese name, Jinfeng, literally translates to "Golden Wind." And the story of how this firm went from assembling imported Danish turbines in the Gobi Desert to shipping its machines to forty-seven countries is one of the most remarkable industrial ascents of the twenty-first century.

The thesis for this episode is straightforward but layered. Goldwind is not simply a Chinese manufacturer that won on cost. That narrative, while comforting to incumbent Western players, misses the actual story. The real story is about a technological bet that looked foolish in 2008, an acquisition that looked insignificant at the time, and a vertical integration strategy that looked like diversification drift until it suddenly looked like genius. It is a story about how a regional state-backed enterprise, born in the wind corridors of Xinjiang, transformed itself into the intellectual property owner for the gearless, permanent magnet direct drive turbine architecture that is now becoming the industry standard for offshore wind.

There are three themes that will thread through this narrative. The first is technological sovereignty, which is the Chinese industrial policy framework that says a country that buys its critical machinery from abroad is not truly a sovereign industrial power. The second is what might be called the reverse merger, which is the pattern of a smaller Chinese firm acquiring a Western boutique engineering shop and then scaling that Western IP to industrial volumes that the original owners could never have achieved. The third is the shift from selling turbines to selling electrons, which is perhaps the most important strategic pivot the company has made, and the one that most investors still do not fully appreciate.

Goldwind in 2026 is a fundamentally different company than the Goldwind of 2016. In 2016, it was a hardware manufacturer competing on blade length and nameplate capacity. Today, it is a platform company that spans turbine manufacturing, wind farm development and operation, battery energy storage systems, green methanol production, green hydrogen infrastructure, and even industrial water treatment. The stock market still prices it like a cyclical hardware company. Whether that valuation framework remains appropriate is the central question this episode tries to answer.

The journey begins, as so many Chinese industrial stories do, not in Beijing or Shanghai but in a desert outpost where the wind was so strong it could knock a man off his feet.

II. Xinjiang Roots: The Dabancheng Experiment

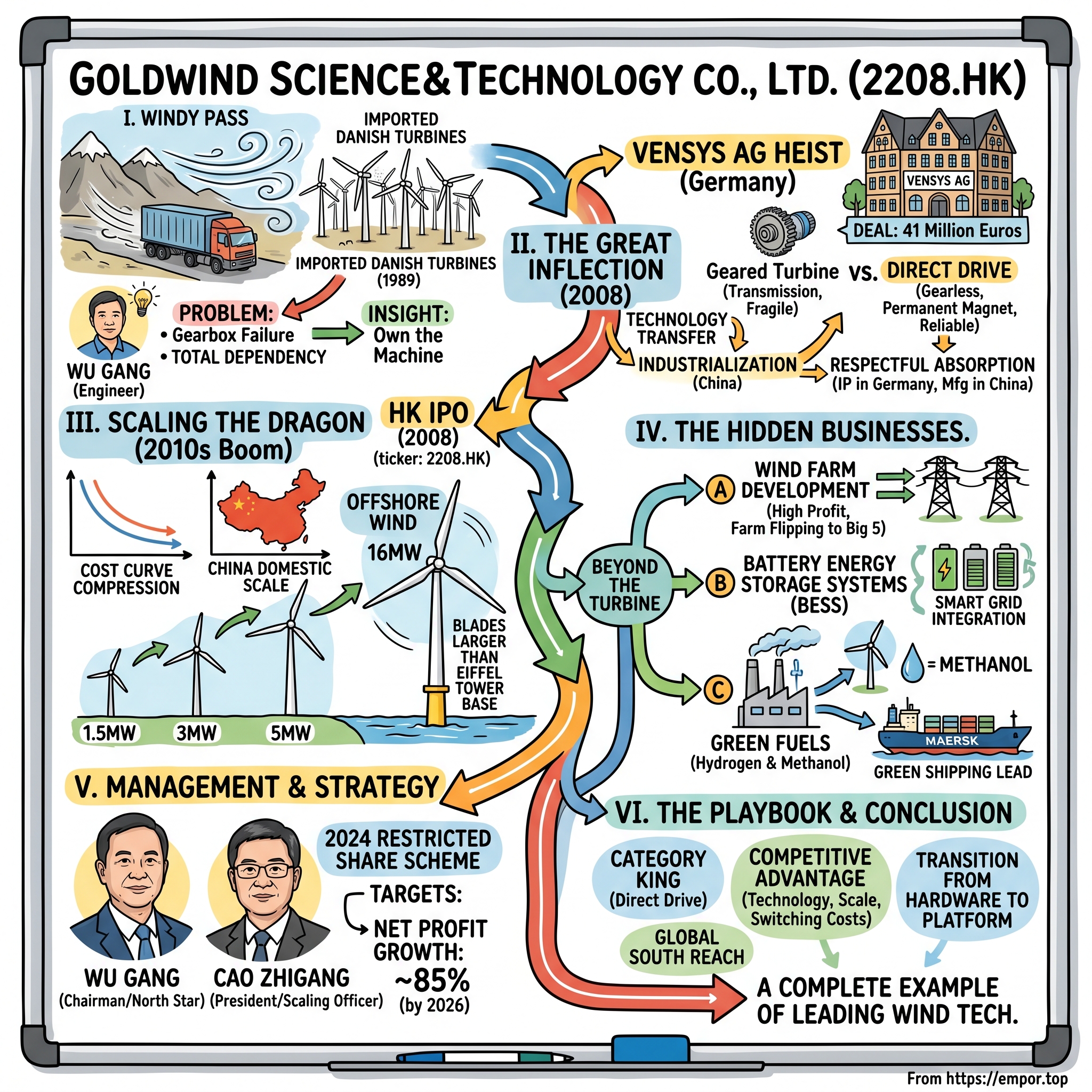

Dabancheng is a wind pass about forty miles southeast of Urumqi, where the Tianshan mountains funnel air currents through a narrow corridor at the edge of the Gobi Desert. In the 1980s, meteorologists already knew it was one of the windiest places on the Eurasian landmass. Truckers knew it too. Local folklore held that the wind at Dabancheng had, on more than one occasion, blown fully loaded cargo trucks off the highway. What nobody had figured out was how to turn all that free kinetic energy into electricity in any meaningful quantity.

Into this setting in the mid-1980s walked Wu Gang, a young engineer who had trained at the Xinjiang Institute of Engineering. Wu was not a flashy founder in the Silicon Valley mold. He was quiet, methodical, and obsessive about the mechanical details of things that spin. He had spent his early career working on state-funded wind research in a region that most of his urban Chinese counterparts considered a hardship posting. What Wu realized, walking those desert ridges, was both a blessing and a curse. China was almost certainly the windiest major country on Earth. China was also nearly incapable of building a utility-grade wind turbine.

The first Dabancheng wind farm, built in 1989, was assembled from thirteen Danish Bonus turbines imported through a World Bank loan. The machines were, by the standards of the day, genuinely impressive. They were also completely opaque to the engineers who were supposed to maintain them. When a gearbox failed, the only option was to wait for a Danish technician to fly in. When a blade needed replacement, the parts came from Europe, shipped across oceans and then trucked across continents. The power from those turbines was meaningful. But the dependency was total.

That dependency became the foundational insight of what would eventually become Goldwind. Wu Gang, who by the early 1990s had been put in charge of the Xinjiang Wind Energy Company, an enterprise of the local government, understood that operating imported hardware was not the same as building an industry. As long as China bought its turbines, it was a customer. To become a producer, the country had to own the blueprints, the molds, the metallurgy, and the control software. Wu wanted to own the machine.

In 1998, the company that would become Goldwind was formally incorporated, carrying with it the mixed-ownership DNA that would shape everything that followed. The largest shareholder was a state entity tied to the Xinjiang regional government. But unlike a classic state-owned enterprise, Wu and his engineering team had meaningful equity, meaningful operational autonomy, and a mandate to compete commercially. This hybrid structure, which Western observers often flatten into the misleading label of "Chinese SOE," was actually much closer to what Chinese industrial strategists came to call the mixed-ownership model. It combined patient state capital with the urgency of a private startup.

The early years were a grind. Goldwind's first domestically produced turbines, in the 600-kilowatt range, were reverse-engineered from licenses purchased from German firms like Jacobs and Repower. The quality was acceptable but not exceptional. The pricing was cheaper than Vestas or Gamesa, but the Chinese grid utilities were notoriously demanding buyers who had watched too many cheap local products fail in service. For much of the 2000s, Goldwind was one of perhaps a dozen Chinese wind turbine manufacturers, indistinguishable from the pack, surviving on state-directed orders and government subsidies tied to the nascent domestic renewables program.

Two things saved the company from commodity mediocrity. The first was Wu Gang's growing conviction that the dominant geared turbine architecture used by Vestas and the other Western leaders was actually a dead end. The second was an obscure German engineering boutique that most of the industry had barely heard of. These two threads, which would have seemed unrelated in 2005, were about to come together in a deal that would reshape the company.

III. The Great Inflection: The VENSYS Heist

To understand why the 2008 acquisition of VENSYS Energy AG matters, it is worth pausing to explain the difference between a geared wind turbine and a direct drive wind turbine. The analogy that makes this concrete for most people is the difference between an internal combustion car and an electric vehicle. A geared turbine works roughly like an internal combustion engine with a transmission. The blades spin slowly, perhaps fifteen rotations per minute. That slow rotation gets stepped up through a multi-stage gearbox to around fifteen hundred rotations per minute, which is what a conventional generator needs to produce grid-quality electricity. A direct drive turbine, by contrast, works like an electric vehicle. There is no gearbox. The blades connect directly to a very large, very slow-turning generator that uses powerful permanent magnets to produce electricity without needing to spin fast.

The geared approach had one massive advantage, which was that it let turbine makers use cheap, commodity off-the-shelf generators. It had one massive disadvantage, which was that the gearbox was the single most fragile component in the entire machine. Offshore, where repair costs are astronomical, a failed gearbox could destroy the economics of an entire project. The direct drive approach flipped these trade-offs. The generator was larger, heavier, and more expensive. But with no gearbox to fail, reliability over a twenty-five-year operating life was dramatically higher.

By the mid-2000s, almost the entire global wind industry had standardized on geared turbines. Vestas made them. GE made them. Gamesa made them. The Chinese licensees made them. There was one small European shop that was betting in the other direction. That shop was VENSYS Energy AG, a spinout from the Saarland University of Applied Sciences in Germany, founded by a professor named Friedrich Klinger. VENSYS had designed a permanent magnet direct drive platform that was, by any honest engineering assessment, roughly a decade ahead of anything else in the world. What VENSYS lacked was capital, manufacturing scale, and a market where its premium architecture could actually find customers. German wind developers in 2007 were generally risk-averse buyers who wanted proven platforms, not elegant outliers.

In 2008, as the Global Financial Crisis froze industrial dealmaking across Europe, Goldwind moved. The company acquired a roughly seventy percent controlling stake in VENSYS for approximately forty-one million euros. Let that number sit for a moment. Forty-one million euros. A few years later, Siemens would pay billions to combine with Gamesa. GE would spend roughly thirteen billion dollars on Alstom's power and grid assets. In the context of what the wind industry would soon pay for established turbine IP, Goldwind had bought the fundamental technology platform that would define the next two decades of global wind for something less than the price of a mid-sized commercial office building in central London.

The deal was not technically a steal, because VENSYS was not a forced seller and the valuation reflected what the firm was worth as a standalone engineering boutique. What made it a strategic heist was what Goldwind did afterward. The company took the VENSYS permanent magnet direct drive architecture, which had been designed for low-volume European production, and scaled it to Chinese industrial volumes. They industrialized the rare earth magnet supply chain domestically. They redesigned components for lower-cost Chinese manufacturing without sacrificing the core reliability advantage. They applied the architecture first to onshore turbines in the one-and-a-half to three megawatt range, then scaled it upward through five megawatts, eight megawatts, twelve megawatts, and ultimately to the sixteen megawatt class offshore machines that would define the 2020s.

What made this work, culturally, was something the deal architects at Goldwind called respectful absorption. The German engineers at VENSYS were not dispatched or diluted. They were kept in Saarland, given more resources than they had ever had, and handed a very simple mandate. Keep advancing the platform. The industrialization and cost engineering happened in China. The fundamental R&D stayed in Germany. This split, which sounds simple, is actually the operational model that has proven hardest for Western buyers of Chinese assets and Chinese buyers of Western assets to replicate. Goldwind pulled it off because Wu Gang genuinely believed that German precision engineering and Chinese manufacturing speed were complementary rather than competitive.

By 2012, just four years after the acquisition, Goldwind was shipping direct drive turbines at a scale that dwarfed what VENSYS had produced as an independent company by several orders of magnitude. The geared competitors, meanwhile, were starting to accumulate the reliability problems that had always lurked in their architecture. The shift was underway. The company that had started by importing Danish turbines now owned the dominant IP for the post-gearbox era.

IV. Scaling the Dragon: The 2010s Boom

The capital markets, slow as always to catch onto industrial inflections, finally noticed Goldwind in 2010 when the company listed its H shares on the Hong Kong Stock Exchange under the ticker 2208. The listing was not a typical Western IPO in the sense that the company had already been listed on the Shenzhen exchange since 2007. The Hong Kong listing was a secondary platform, designed specifically to raise international capital and to give global institutional investors a way to own the name. The proceeds, roughly seven billion Hong Kong dollars, were not flashy but they served a specific purpose. They funded the R&D and manufacturing capacity buildout required to take on Vestas and GE on global terms.

What followed was one of the most aggressive cost curve compressions in industrial history. Between roughly 2010 and 2020, the all-in cost of onshore wind electricity in China fell by roughly two-thirds. The levelized cost of energy for new Chinese wind projects crossed below the cost of coal-fired power sometime in the late 2010s, a milestone that had been considered unreachable by most Western analysts as recently as 2015. Goldwind was not the only driver of this compression. The entire Chinese wind supply chain, including blade makers like Sinomatech, gearbox makers, tower manufacturers, and cable suppliers, participated. But Goldwind, as the largest OEM, set the pace.

The mechanics of this cost compression are worth understanding because they explain why Western competitors have struggled to respond. Chinese turbine makers sold machines into a domestic market of unprecedented scale. In the peak years of the 2020s, China added more wind capacity in a single year than the entire European Union had installed cumulatively over the prior decade. That volume, amortized against fixed R&D and tooling costs, produced unit economics that Vestas could not match. It was not that Chinese labor was cheap, because by the late 2010s Chinese turbine assembly labor costs were comparable to many Eastern European sites. It was that Chinese fixed cost absorption was structurally superior.

The other strategic thread of the 2010s was the methodical push into offshore wind. Onshore wind is fundamentally a land-constrained business. Good onshore sites get developed, and eventually a country runs out of them. Offshore wind, in principle, has nearly unlimited resource potential. But offshore is also technically brutal. Saltwater corrodes everything. Installation vessels cost hundreds of thousands of dollars per day. Maintenance requires helicopters or jack-up boats. The economics only work with very large turbines that produce enough electricity per unit to justify the massive fixed installation costs.

Goldwind's response was to push its permanent magnet direct drive platform to ever-larger scales. In 2020, the company unveiled a ten-megawatt offshore platform. By 2022, the twelve-megawatt class was being installed in Fujian and Guangdong. In 2023, the company introduced its sixteen-megawatt offshore platform, with blades that swept a rotor diameter larger than the base of the Eiffel Tower. For context, a single sixteen-megawatt turbine running at reasonable capacity factors can power roughly twenty thousand Chinese households for a year. The reliability advantage of the direct drive architecture, which had always been theoretical in marketing decks, became commercially material in offshore applications where a gearbox failure at sea could cost millions to repair.

The cumulative effect of this decade was that Goldwind became, by installed capacity, the largest or second-largest wind OEM on Earth in almost every year after 2015, depending on the specific counting methodology. More importantly, the company began exporting. Pakistan. Chile. Vietnam. Argentina. South Africa. Thailand. Ukraine. By 2024, Goldwind machines were spinning in forty-seven countries on six continents. The Western narrative that Chinese manufacturers could only win at home on subsidies was becoming harder to sustain.

Two challenges, however, remained. The first was that the geopolitical posture of the United States and, to a lesser extent, the European Union, made direct penetration of those markets nearly impossible. Tariffs, security review processes, and domestic content requirements created barriers that had almost nothing to do with product competitiveness. The second was that the Chinese onshore market, the volume engine that had enabled the cost curve compression, was starting to mature. Growth rates were slowing. Competition among Chinese OEMs was brutal. Pricing wars were compressing margins toward uncomfortable levels.

This was the environment in which the next generation of management would have to navigate.

V. Management: The Founder and the Professional

Wu Gang is now past sixty-five, an age at which most Chinese industrial founders have formally stepped back from operational roles. He has not. As Chairman of Goldwind, he remains the strategic north star of the company, and his personal stake, reported in recent filings at roughly one and three-quarters percent of outstanding shares, represents something genuinely meaningful in the context of Chinese corporate governance. Most state-backed industrial chairmen in China hold trivial personal equity positions. Wu's holding, equivalent to roughly sixty-two million shares depending on the count and the disclosure date, means that when the stock goes up, he personally gets wealthier in a way that is visible and proportional. When it goes down, he personally gets poorer.

Wu's public style is understated. He does not give flashy interviews. He has been known to appear at industry conferences in a plain blue suit, deliver a fifteen-minute speech heavy with engineering metaphors, and then leave without the usual grip-and-grin reception. In internal company communications, which have occasionally leaked into the Chinese business press, he has been described as obsessed with what he calls the "long life" of the turbine, which is his shorthand for the reliability question that drove the VENSYS bet. He is also known for a habit of walking through factory floors unannounced, stopping workers to ask them to explain the specific part they are assembling.

The day-to-day operator of the company is Cao Zhigang, who holds the title of President. Cao's background is classical Chinese industrial management. He rose through the engineering and operations ranks, took on progressively larger operational responsibility, and now runs what amounts to a globally distributed manufacturing, development, and services enterprise. If Wu is the chief strategist and conscience of the company, Cao is the chief scaling officer. The division of labor has been remarkably stable, which in Chinese industrial firms of this size is itself a notable accomplishment given the political and factional dynamics that can fragment leadership teams.

The most revealing document about where management thinks the company is going is the 2024 Restricted Share Scheme, which the board approved and rolled out to roughly four hundred and sixty key employees. The structure of this plan is worth dwelling on because it is unusually aggressive. The participating employees received share grants at a discount of roughly sixty percent to the prevailing market price at the time of the grant. That discount is not a giveaway. It is conditional. The shares only vest if the company hits specific performance targets, including a net profit growth target of approximately eighty-five percent by 2026 over the baseline year.

An eighty-five percent net profit growth target over roughly two fiscal years is not a legacy-preservation incentive. This is what a founder and a board design when they genuinely believe the business has an underappreciated earnings runway and they want to align the next layer of leadership with extracting it. For investors reading the proxy, the interpretation is straightforward. The people closest to the operational reality of the business, including the engineering heads, the regional sales leaders, and the segment managers, are being paid to grow earnings dramatically, not to protect a steady-state cash flow.

It is also worth noting what this incentive structure is not. It is not a typical Chinese SOE compensation plan, which would usually emphasize revenue scale, market share, and political alignment over shareholder return metrics. The fact that Goldwind's plan is structured around net profit, rather than around revenue or installed capacity, reflects the ongoing evolution of the business from volume-chasing hardware into higher-margin energy services and development activities. The composition of the eighty-five percent target, according to the plan documentation disclosed in the company's Hong Kong filings, weights most heavily on group-level net profit rather than segment-specific metrics, which forces cross-functional cooperation.

The second-layer governance point worth noting is the auditor and accounting treatment. Goldwind's financial statements are audited by a Big Four firm under both PRC and Hong Kong standards, and the company has not had material restatements or going-concern qualifications in recent memory. The accounting judgments that matter most for the business are the warranty accruals on turbine sales, the cost capitalization decisions on R&D, and the revenue recognition timing on wind farm asset transfers. These are all areas where aggressive accounting has burned investors in this sector before, most famously at Siemens Gamesa, where warranty accruals proved catastrophically inadequate. Goldwind's disclosure quality in these areas has been, by the standards of Chinese industrial issuers, above average.

With management aligned and incentive targets set, the question becomes where the earnings growth is actually going to come from. For most observers, the answer seems obvious: more turbines. That answer is wrong, or at least dramatically incomplete.

VI. The Hidden Businesses: Beyond the Turbine

If you opened Goldwind's 2024 annual report and looked only at the revenue breakdown, you would conclude that this is a wind turbine company. The Wind Turbine Generator segment, which the company internally abbreviates as WTG, accounted for roughly seventy-nine percent of consolidated revenue. Every other segment, by that measure, looks secondary. This is exactly the wrong way to read the business. Revenue mix in a multi-segment industrial company with vastly different margin profiles tells you almost nothing about where the enterprise value is actually being created. Profit mix tells you far more, and the profit mix at Goldwind is a story that very few sell-side analysts have told well.

Consider the WTG segment on its own. Manufacturing wind turbines, after a decade of brutal cost compression in the Chinese market, is a low single-digit operating margin business in the best years and a loss-making business in the worst years. Chinese OEMs have at times quoted turbine prices below two thousand Chinese yuan per kilowatt of nameplate capacity, levels at which no Western manufacturer could plausibly compete and at which even the Chinese players struggle to make money. Goldwind does better than peers on this dimension because of the direct drive technology and the scale of its operations, but even for Goldwind, turbine manufacturing is not where the real profits live.

The real profits live, first and foremost, in wind farm development and operation. The mechanics of this segment are important to understand. Goldwind identifies a promising wind resource site, often in regions like Xinjiang, Inner Mongolia, Gansu, or Jilin. The company secures the land rights, the grid connection permits, and the power purchase agreements. It then builds the wind farm, using primarily its own turbines. Once the farm is operational and producing reliable cash flows, the asset can either be held on the balance sheet as a long-term operating investment or sold to a state utility buyer, typically one of the so-called Big Five power generators, at a price that reflects the de-risked operating asset value.

The margin profile on this activity is dramatically different from turbine sales. When Goldwind sells a wind farm to a state utility, the gross margin on that transaction typically runs above forty percent. The operating profitability, net of SG&A and development costs, is several multiples of what the WTG segment delivers. In the years when Goldwind has been particularly active in farm flipping, the segment has contributed a disproportionate share of total group net profit despite representing a minority of revenue. This is the hidden profit engine that the headline revenue split obscures.

But the company's strategic ambitions extend well beyond farm flipping. The second growth area, which has become materially visible in the 2023 and 2024 results, is battery energy storage systems. The logic is straightforward. Wind, by its nature, is intermittent. As wind penetration on the Chinese grid has risen past fifteen percent of generation in some regions, the challenge of matching intermittent supply to demand has gone from theoretical to acute. Battery storage, paired with wind, transforms the value proposition. Instead of selling electrons only when the wind blows, a wind-plus-storage system can sell electrons when the grid needs them. That ability to time-shift power production dramatically increases the average sale price.

Goldwind has been deploying utility-scale BESS both integrated with its own wind farms and as standalone grid assets. The segment is still relatively small as a share of revenue, but the growth rates have been dramatic, and the integration with existing wind assets provides a natural customer base that pure-play BESS competitors lack.

The third strategic frontier, which is genuinely speculative but potentially transformative, is green fuels. Specifically, green hydrogen and green methanol. The concept here is that electricity produced by wind farms, particularly surplus electricity during periods of low grid demand, can be used to electrolyze water into hydrogen. That hydrogen can then be combined with captured carbon dioxide to produce methanol, which is a liquid fuel with an existing global shipping and distribution infrastructure. Green methanol has emerged as the leading candidate to decarbonize international shipping, because major shipping lines like Maersk have committed to methanol-powered vessels for their long-haul fleets.

Goldwind has made several announcements about green methanol production projects, most notably in Inner Mongolia and the northwest. These projects are early, the economics are unproven at commercial scale, and the pathway to meaningful group-level earnings contribution is probably measured in years rather than quarters. But the strategic logic is compelling. Goldwind already owns the electrons. The incremental investment in electrolysis and methanol synthesis converts cheap surplus electricity into a liquid fuel that ships globally and sells into the decarbonization premium market.

There is also an industrial water treatment business, which often surprises investors encountering Goldwind for the first time. The historical rationale is that desert wind farm sites often need water treatment infrastructure, and the company developed internal capability that eventually spun out into a commercially addressable segment. The water business is not going to move the needle on group valuation, but it provides a steadier cash flow pattern that helps offset the notorious cyclicality of the wind equipment business. It is a small but meaningful example of how a decades-long industrial journey accumulates assets that would never have been planned from scratch.

When all of these segments are considered together, the thesis that Goldwind is transitioning from a hardware manufacturer into an integrated energy platform becomes concrete rather than aspirational. The transition is incomplete. The WTG segment still dominates revenue. But the direction of travel is unmistakable, and the 2024 restricted share plan ties management compensation to executing it.

VII. The Playbook: Business and Investing Lessons

Stepping back from the operational narrative, it is worth examining Goldwind through the lens of two frameworks that have become standard tools for industrial business analysis. The first is Hamilton Helmer's Seven Powers framework, which tries to identify the durable sources of above-market returns for a given business. The second is Michael Porter's Five Forces framework, which looks at the structural attractiveness of the industry itself.

Starting with Seven Powers, the most important power Goldwind possesses is what Helmer would call a Cornered Resource. The permanent magnet direct drive intellectual property inherited from VENSYS and extended through a decade and a half of internal R&D constitutes a genuinely differentiated technology position. The evidence that this is a real power, rather than a marketing story, is the performance of the Western competitors. Siemens Gamesa, which had its own direct drive platform, nonetheless accumulated severe quality problems in its onshore geared fleet that produced warranty losses running into the billions of euros during 2023 and 2024. Vestas, which maintained its geared architecture for longer, has been slower to transition to direct drive at the largest offshore scales. GE has effectively withdrawn from the merchant offshore market. Goldwind's direct drive lead is not absolute, because other Chinese OEMs have developed their own direct drive platforms, but in terms of installed fleet reliability data across a twenty-plus year history, Goldwind's position is genuinely differentiated.

The second power is Scale Economies. By dominating the Chinese domestic market, which is roughly half of all annual global wind installations in most recent years, Goldwind amortizes its fixed R&D and tooling costs across a unit volume that no Western competitor can match. This scale advantage is structurally durable as long as China continues to add wind capacity at the rates it has been doing. Scale economies are particularly pronounced at the edges of the product envelope, meaning the very large offshore turbines, where the R&D intensity per unit sold is highest.

The third power, which is more speculative but increasingly visible, is Switching Costs. Wind farms operate for twenty to twenty-five years. The digital operations and maintenance platforms, the spare parts supply chains, and the service contracts tie utility customers to a specific OEM for the life of the asset. Once a utility has standardized its O&M training, its software integration, and its spare parts inventory around a Goldwind fleet, switching to a competitor for the next farm carries real friction. The company's "Smart Wind" digital platform, which provides remote monitoring, predictive maintenance, and grid integration services, represents a deliberate attempt to deepen these switching costs.

Turning to Porter's Five Forces, the picture is more mixed. The threat of substitutes is significant. Solar photovoltaic technology has experienced cost compression even more dramatic than wind, and in many geographies utility-scale solar is now the lowest-cost new generation option on a pure levelized cost basis. The counter to this threat is that wind and solar are complementary rather than purely substitutable, because their generation profiles differ through the day and through the seasons. A grid with both resources and some storage is more stable than a grid with either alone. Goldwind's push into storage and its willingness to participate in hybrid wind-solar-storage projects reflects this strategic reality.

The bargaining power of buyers is high. The ultimate customers for Chinese wind turbines are a small number of state power utilities, including the so-called Big Five generators, plus provincial and municipal entities. These buyers have near-monopsony power in certain regional markets. The historical response to this buyer power has been brutal pricing competition among Chinese OEMs. Goldwind's structural response has been to become its own customer through the wind farm development business, which effectively captures the developer margin that would otherwise go to the utility buyer.

The bargaining power of suppliers is moderate and shifting. The most critical inputs for direct drive turbines are rare earth magnets, specifically neodymium-iron-boron magnets. China dominates the global rare earth supply chain, which benefits Chinese turbine makers but also creates geopolitical fragility when those supply chains become politically contested. Goldwind has taken steps to secure upstream supply, including strategic agreements with rare earth producers, but this remains a risk factor.

The threat of new entrants in the global turbine manufacturing business is low, because the capital intensity, the reliability data requirements, and the regulatory certification timelines create meaningful barriers. The threat of new entrants in the wind farm development business, by contrast, is higher, because any party with capital and local relationships can enter. This is part of why the developer margins, while currently attractive, may compress over time.

The competitive rivalry within the Chinese OEM landscape remains intense. Envision, Mingyang, Windey, Shanghai Electric, and CRRC all compete aggressively on both technology and price. Goldwind's historical installed base, direct drive IP, and international reach provide advantages, but the rivalry is real and it will continue to pressure margins.

Pulling these threads together, the investment playbook is relatively clear. The WTG hardware business is a scale business with moderate structural attractiveness. The real value creation, and the justification for thinking of Goldwind as something more than a cyclical manufacturer, comes from the wind farm development business, the services platform that extends throughout the asset life, and the optionality in storage and green fuels.

VIII. The Bull vs. Bear Case

No honest examination of Goldwind as an investment can avoid the geopolitical reality that frames the entire discussion. The bear case starts here, because it is where the hardest-to-hedge risks live. The United States, through tariffs and through the Inflation Reduction Act's domestic content provisions, has effectively closed its wind market to Chinese OEMs. The European Union, while more open in principle, has moved toward resilience-framed procurement policies that favor European manufacturers for strategic infrastructure. The result is that roughly half of the global wind market, by value, is structurally difficult for Goldwind to access. The addressable market is China plus the so-called Global South, which includes Latin America, Southeast Asia, parts of Africa, and the Middle East. This is a large and growing market, but it is not the global market.

The second leg of the bear case is domestic oversupply. With a dozen or more Chinese turbine OEMs competing for a slowing domestic installation base, pricing wars are a recurring feature of the industry. The historical pattern has been that Chinese industrial cycles produce periods of brutal margin compression followed by consolidation. Goldwind's scale and IP position should allow it to survive and eventually benefit from consolidation, but investors should not assume that consolidation will happen smoothly or quickly.

The third bear case element is execution risk on the green fuels pivot. Green methanol and green hydrogen are genuinely promising markets, but the technology is early, the commercial economics remain dependent on carbon pricing and regulatory frameworks that vary by jurisdiction, and the capex requirements are substantial. A firm that commits aggressive capital to green fuels before the technology matures risks the classic diworsification pattern, where a growth investment destroys rather than creates value. Management's track record here is too short to evaluate confidently.

The fourth bear case element, which is more of a second-layer diligence overlay, is the quality of receivables and the balance sheet exposure to the wind farm business. Selling wind farms to state utilities is a high-margin activity, but it is also an activity that can produce long receivable cycles and meaningful working capital pressure. Investors should watch the cash conversion cycle and the ratio of reported profit to operating cash flow. Industrial firms that grow reported earnings faster than cash have been a recurring source of disappointment in Chinese equities.

The bull case, in contrast, rests on the proposition that Goldwind is no longer the company the market is pricing. The hardware revenue dominates the top line, but the earnings composition, the strategic initiatives, and the management incentive plan all point toward a more diversified, higher-margin energy platform. If the farm development margins hold, if the services business compounds with the installed base, if the storage segment scales with the ongoing grid integration of renewables, and if even one of the green fuels initiatives reaches commercial economics, the business looks much more like a growing utility platform than a cyclical manufacturer.

The second leg of the bull case is international optionality. While the US and major EU markets are structurally difficult, the Global South is underpenetrated by renewables and is growing rapidly. Pakistan, Vietnam, Argentina, South Africa, Kazakhstan, and the Middle Eastern economies that are diversifying away from hydrocarbons all represent addressable markets where Chinese OEMs have cost and product advantages. Goldwind's presence in forty-seven countries is not evenly distributed, and the depth of that international business is an area where continued expansion could be meaningful.

The third bull case element is technology continuation. Direct drive is not the final word in wind turbine architecture. Superconducting generators, axial flux designs, and advanced magnetic materials are all areas of active research where Goldwind, through the VENSYS laboratory and its domestic R&D organizations, maintains visibility. The scale of the company's R&D budget, combined with the volume of operational data from the installed fleet, creates a compounding technology advantage that is hard to replicate.

For investors trying to track which case is winning, the handful of KPIs that actually matter can be narrowed meaningfully. The first KPI is the margin spread between the WTG segment and the wind farm development segment. If the company is successfully mixing toward higher-margin activities, this spread should translate into group-level margin expansion over time. The second KPI is external turbine orders by region, because international order growth is the cleanest signal that the company is reducing its dependence on the mature Chinese market. The third KPI is the net profit trajectory against the eighty-five percent growth target implicit in the 2024 restricted share scheme. That target is the company's own stated ambition, and tracking progress against it is the most direct way to evaluate whether management is executing.

Holders of concentrated positions and larger institutional investors have been notable in the H share register, and changes in those positions are typically disclosed on a delay through the Hong Kong exchange. Investors with the capacity to track these disclosures can use them as a second-layer signal on how sophisticated capital is positioning around the story. The historical ownership pattern has been a mix of mainland state-affiliated strategic holders, Hong Kong and Singapore asset managers with clean energy mandates, and a rotating cast of global long-only and event-driven funds.

The myth versus reality summary is worth stating directly. The consensus narrative is that Goldwind is a Chinese hardware manufacturer that wins on price and depends on domestic subsidies. The reality, based on the evidence, is that Goldwind is a technology-led, vertically integrated energy platform with a structurally advantaged IP position, a growing services and development business, and optionality in storage and green fuels. The two narratives lead to very different valuation multiples, and the gap between them is the opportunity, or the trap, depending on execution.

IX. Conclusion

The question of whether Goldwind qualifies as what the Acquired framework would call a Category King deserves to be treated seriously. A Category King is not simply a market leader. It is a firm that defines the category, sets the terms of competition, and captures a disproportionate share of the economic value the category creates. By that standard, Goldwind is clearly a Category King in direct drive wind turbines, and it is credibly a Category King in the broader Chinese wind market. The question of whether it is a Category King in global wind overall is complicated by the geopolitical segmentation of the industry. In the accessible two-thirds of the global market, it is dominant or near-dominant. In the politically closed markets of the US and parts of Europe, it is excluded.

What is indisputable is that Goldwind is the most complete example in the Chinese renewables industry of the transition from copying to leading. The company started by importing Danish turbines and licensing German designs. It now owns the dominant architecture for the next generation of wind technology and operates the largest direct drive fleet on Earth. The VENSYS acquisition, which in 2008 looked like a curiosity, turned out to be the hinge on which the entire subsequent history of the business turned. The industrial logic of asset-light engineering, acquired cheaply in Europe and then married to asset-heavy manufacturing scale in China, is a template that other Chinese industrial firms have attempted to replicate across sectors from robotics to semiconductors to biotechnology, with varying success.

The firm's journey is also a useful reminder of how long the arc of industrial competitive advantage actually is. The VENSYS deal closed in 2008. The meaningful commercial dominance of the direct drive architecture was not obvious until roughly 2018. The emergence of the wind farm development business as a material profit contributor took even longer. The green fuels and storage initiatives are still in their early commercial phase. Industrial transformations, unlike software platform shifts, unfold over decade-length time horizons, and patience is a prerequisite for understanding them.

For investors evaluating the name today, the analytical task is to assess how much of the future platform story is already discounted in the current valuation, and how much remains as optionality. That analytical task is genuinely hard because the company straddles multiple business models with different profitability profiles, growth rates, and risk factors. The hardware business trades like a cyclical. The development business trades like a financial sponsor. The services business trades like a utility. The green fuels business, if it succeeds, would eventually trade like a specialty chemicals or energy infrastructure firm. No single multiple does justice to the combination.

X. Epilogue

By the time this narrative was being written in early 2026, the real-world evidence on the eighty-five percent net profit growth target embedded in the restricted share scheme was starting to come in. The 2024 and 2025 results, reviewed against the 2023 baseline, reflected both the ongoing pricing pressure in the Chinese onshore turbine market and the growing contribution of the higher-margin segments. The sixteen-megawatt offshore platform, which had been in commercial demonstration through 2024, moved into volume production during 2025 with initial deliveries against major offshore tenders in Guangdong, Fujian, and two overseas projects. Early industry commentary suggested that if the offshore order pipeline held, the gross margin recovery in the WTG segment could be meaningful.

The Xinjiang legacy, which started the whole story, has not disappeared. Dabancheng, where Wu Gang walked those windy ridges nearly four decades ago, is now home to wind installations measured in gigawatts rather than kilowatts. The company still maintains significant operations in Urumqi and the surrounding region. A corporate anniversary event in 2023, reported in the Chinese business press, featured Wu personally revisiting the original 1989 Danish Bonus installation site, where some of those original turbines had been preserved as industrial heritage monuments. The symbolism of that moment, a Chinese founder standing next to the imported machines that had defined his country's early dependency and the domestic machines that now defined its leadership, captured something essential about the arc of the firm.

Whether the next decade produces another VENSYS-scale inflection, whether the green methanol bet pays off, whether the geopolitical environment opens any meaningful new markets, and whether the domestic Chinese industry consolidates in a way that rewards scale leaders, are all questions that the 2020s and 2030s will answer. What is already clear is that the firm that started in a desert with thirteen imported turbines became, within a single professional lifetime, the technological and operational leader of an industry that will power a non-trivial share of human civilization for the rest of this century. Few industrial stories of the early twenty-first century are as complete, or as instructive.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube