Nayuki: The "Starbucks of Tea" and the New-Style Revolution

I. Introduction: The $10 Billion Cup of Tea

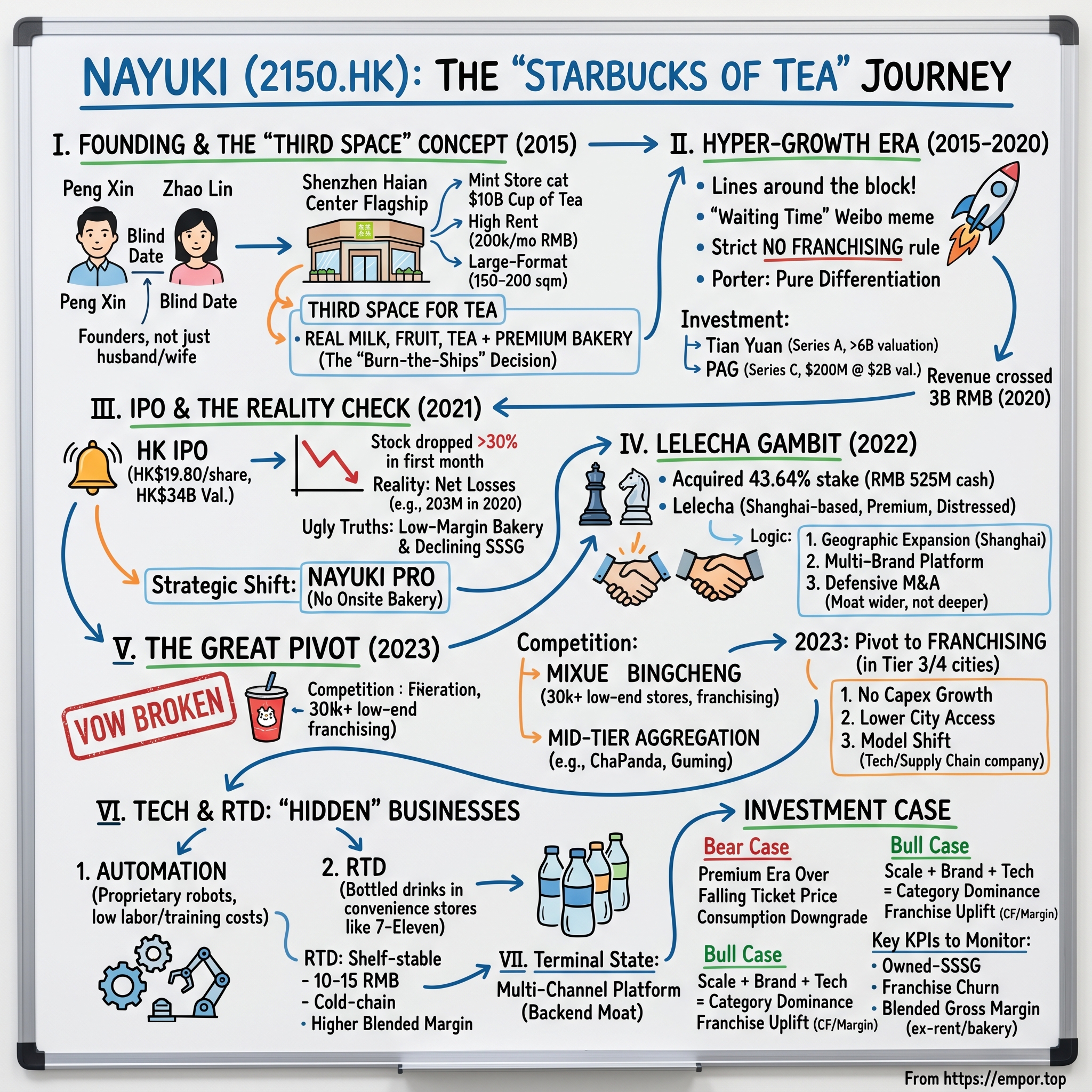

Picture Shenzhen in the summer of 2015. Not the Shenzhen of Huawei or Tencent—though both are quietly minting fortunes a few blocks away—but the Shenzhen of Haian Center, a gleaming luxury mall where the rents approach Hong Kong levels and the retail slots are reserved for Dior, Hermès, and Apple. Into that unlikely real estate walks a 37-year-old woman named Peng Xin, carrying blueprints for a tea shop.

Not a chá-guǎn in the classical sense—no rosewood tables, no scholarly calligraphy, no decorous pouring of pu-erh. Peng wants something stranger. She wants a 200-square-meter flagship with an onsite bakery, a marble-countered bar, soft-lit seating for eighty, and a menu that pairs fresh-brewed jasmine green tea with a strawberry-cheese layer cake. The landlord thinks she has lost her mind. So does almost every retail consultant in Guangdong. Tea shops in China in 2015 meant one of two things: the dusty traditional teahouse frequented by retirees, or the 10-square-meter CoCo kiosk peddling powdered milk tea for 8 yuan. Peng is proposing neither. She is proposing, in her words, "a third space for tea"—and she is proposing to pay 200,000 RMB a month in rent to prove it.

Rewind six months. The story, as Peng later told Chinese business press, begins not with a pitch deck but with a blind date. A friend had introduced her to Zhao Lin, a 45-year-old veteran of the F&B industry who had spent years operating restaurants and bakeries across Guangdong. Peng wasn't looking for a husband. She was looking for a co-founder. Over tea—naturally—she laid out her concept: high-end, fresh fruit, real milk, real tea leaves, premium bakery, flagship locations. Zhao listened. He pushed back on the margins. He asked about the supply chain. He said yes. Six months later, they married. Two years later, their company was a unicorn. Six years later, it listed on the Hong Kong Stock Exchange as the first "new-style tea" stock in history.

That company is Nayuki Holdings Limited, ticker 2150.HK. And the story of Nayuki is not really a story about beverages. It is a story about the invention of a category—"new-style tea"—that redefined what Chinese Gen Z consumers drink, how much they pay for it, and where they drink it. It is a story about a founder couple who bet the company three times: once on large-format flagship stores when everyone said kiosks were the future, once on an IPO at the absolute peak of the bubble, and once on a franchising pivot that violated their own founding vow. And it is a story about a brutal, ongoing war—between Nayuki, HeyTea, Mixue Bingcheng, ChaPanda, Guming, Luckin, and Starbucks—for the most fragmented, most lucrative, and most volatile consumer category in modern China.

Over the next three hours, we'll trace the arc from that blind date in 2015 to the sprawling enterprise of 2026: a business that encompasses over 1,800 stores, an automated tea-making robotics program, an RTD (ready-to-drink) bottled beverage line distributed through every 7-Eleven in China, a 43.64% stake in a rival called Lelecha, and a franchise network that stretches into cities most Western analysts couldn't locate on a map. We'll cover the hyper-growth years, the IPO, the post-IPO hangover, the "PRO" concept that killed the bakery, the Lelecha gambit, the 2023 pivot to franchising, and the price war that is reshaping the entire industry as we speak. We'll look at the bear case, the bull case, and what long-term fundamental investors should actually watch. And we'll ask a question that seems simple but is surprisingly hard: in a country where tea is five thousand years old, how does a brand less than eleven years old end up worth more than most traditional tea houses combined?

II. The Founding Context: China's "Third Space"

To understand why Nayuki matters, you have to understand what Chinese tea culture looked like in 2014. It looked, frankly, bifurcated.

On one end of the spectrum was the "Old World." This was the China of classical tea ceremonies—gongfu cha pouring, Yixing clay pots, loose-leaf oolong from Wuyishan, and a clientele that skewed heavily over fifty. The Old World was beautiful and reverent and utterly unappealing to anyone born after 1990. It was also expensive in the wrong way: you didn't pay for a drink, you paid for an afternoon of slow ritual, and the average young professional didn't have that kind of time. The Old World teahouse in 2014 was, economically, what the traditional coffeehouse had been in America circa 1980—a dying format preserved in amber.

On the other end of the spectrum was the "Street Style." This was the China of CoCo, Happy Lemon, and 85°C, which had built their empires on the Taiwanese bubble tea template: a small kiosk, a small menu, powdered creamers, flavored syrups, non-dairy whitener, and tea brewed from tea bags of variable quality. A large cup of "milk tea" cost between 6 and 12 RMB, which is to say, between one and two US dollars. It was cheap, portable, and deeply beloved by high school and college students, but it was also widely understood to be unhealthy. In 2012, a series of Chinese state media investigations revealed that many street-style milk teas contained zero actual milk, zero actual tea, and enough sugar and plant-based creamer to alarm a nutritionist.

Between these two poles was a gaping, multi-billion-dollar chasm. This was the chasm Peng Xin proposed to fill.

Her thesis, delivered in her earliest pitch decks and later repeated in dozens of interviews, went something like this: China had five thousand years of tea culture but almost no modern tea brands. The country had become, through Starbucks' twenty-year education campaign, a sophisticated coffee market—by 2014, Starbucks operated over 1,400 stores in China and had trained an entire generation of urban professionals to understand that a beverage could cost 35 RMB and come with an ambient space to sit in. If Starbucks had built a "third space" for coffee—between home and office—then surely someone could build a third space for tea. The Chinese consumer, Peng believed, was ready to pay Starbucks prices for a beverage that tasted better, looked better on Instagram (or WeChat Moments, more accurately), and connected to a culture that was actually Chinese rather than imported.

The insight was not original to Peng. HeyTea, founded by the enigmatic 1990s-born entrepreneur Nie Yunchen in the small town of Jiangmen, Guangdong, had been selling "cheese-topped tea" since 2012 and was building a cult following. ChaPanda was pursuing a similar but lower-priced thread. What distinguished Peng's vision was the insistence on two specific ingredients that almost nobody else was using: fresh, seasonal fruit, and freshly baked pastry under the same roof.

The fruit idea came from Peng's own habits—she was, by her own account, a picky eater who drank tea but hated powdered sweeteners. She had tried pairing brewed tea with fresh strawberries at home and become convinced this was the future. The bakery idea came from Zhao. Having spent years in the food business, Zhao understood that an onsite bakery did two things at once: it created an irresistible smell that pulled customers through the door, and it created a second revenue stream that subsidized the premium real estate. A store that sold only tea couldn't justify Floor 1 of a luxury mall. A store that sold tea and fresh-baked strawberry cheese cakes could.

The couple's dynamic, in these early months, established a template that would persist for the next decade. Peng was the product visionary: she obsessed over flavor profiles, store aesthetics, packaging, and the emotional texture of the brand. Zhao was the operator: he managed supply chains, negotiated leases, ran the P&L, and played bad cop with landlords. In Chinese business press, they would be described as "the husband runs the company, the wife runs the brand"—an oversimplification, but a useful one. Nayuki is in many ways a case study in founder complementarity, and the partnership is backed by 60%+ combined equity ownership, which we'll return to later.

The name "Nayuki" (奈雪的茶, "Nai Xue's Tea") was Peng's invention. She picked a Japanese-inflected name because it sounded youthful and aspirational, and because she wanted the brand to feel different from the earthy, national-heritage naming conventions of older Chinese tea brands. It was, at the time, a controversial choice—why not a Chinese name?—but it signaled exactly what the brand wanted to signal: this was not your grandfather's teahouse.

In December 2015, armed with around 8 million RMB of personal savings and friends-and-family money, the couple opened their first three Nayuki stores simultaneously in Shenzhen. Each was between 150 and 200 square meters. Each had a full bakery. Each was in prime shopping-mall real estate. It was, by any reasonable assessment, an insane way to enter a market. It was also, as it turned out, the only way that could have worked.

III. The Hyper-Growth Era (2015–2020)

The three Shenzhen flagships opened in late November and early December 2015, and within a week, the lines were around the block.

The image that defined Nayuki's first year was a simple one: twenty-somethings in puffer jackets, clutching iPhones, queueing in the winter air of a Shenzhen mall concourse to buy a 28-RMB cup of "Supreme Strawberry Magic Tea"—fresh strawberries, green tea base, light cream cheese foam, cut strawberries layered into the cup. It was expensive, it was photogenic, and it was completely unlike anything the Chinese tea market had produced before. Within months, "Nayuki waiting time" had become a Weibo meme. In one Shenzhen Haian store, reported waiting times routinely exceeded two hours.

Zhao and Peng made a critical decision in early 2016 that would define everything that followed: they refused to open kiosks. Every franchisee who came knocking was turned away. Every mall operator who offered a smaller, cheaper slot was declined. The model would be large-format flagship stores only, each with a bakery, each designed as an instagrammable "third space." Peng later called it "the burn-the-ships decision"—they made it impossible to retreat into a cheaper format.

The logic was both cultural and economic. Culturally, Peng wanted every Nayuki store to reinforce the premium brand. A kiosk on the third floor of a B-tier mall would dilute the equity she was building in the Haian flagship. Economically, the bakery model required scale—you couldn't run a bakery at a kiosk—and the economics of the bakery were what made the tea category work. The bakery, despite its modest sales mix, was the thing that let Nayuki pay rents that matched Starbucks and Apple.

This was a genuinely strange strategic choice, and it's worth sitting with for a moment. In every other tea chain in China, the strategy was to miniaturize the store, automate the drink, and maximize store count. Nayuki did the opposite. It maximized the size of each store and the complexity of each transaction. In Porter's language, it was a pure differentiation play in a category where everyone else was pursuing cost leadership.

By 2017, Nayuki had opened its 50th store. In October of that year, the company raised its Series A from Tianyuan Capital at a reported valuation of over 6 billion RMB—making it, almost overnight, one of the most valuable F&B startups in Chinese history. The check size was modest by tech standards (tens of millions of RMB) but the valuation was eye-popping: it implied the market was paying growth-equity multiples for a business that, at its core, brewed tea and baked bread.

Investors weren't crazy. What they were betting on was category creation. New-style tea—the emerging label for the fresh-fruit, fresh-milk, fresh-leaf segment—was growing at 30-40% per year, and Nayuki was one of the two brands (alongside HeyTea) that defined the premium tier. If new-style tea was to become the next Starbucks-scale category in China—and most Chinese consumer analysts believed it would—then Nayuki was already among the top two or three brands positioned to capture it.

The real capital flood came in mid-2020, when PAG, one of Asia's largest private equity firms, led a $200 million Series C at a reported valuation of approximately $2 billion. By that point, Nayuki had over 400 stores across 50+ Chinese cities, and revenue had crossed 3 billion RMB. Crucially, PAG's check signaled something specific: sophisticated growth capital was willing to underwrite the asset-heavy model. Most Chinese consumer companies at that valuation were asset-light franchising plays. Nayuki was building out owned flagship real estate in the most expensive shopping malls in the country. It was Starbucks' playbook, fifteen years behind.

The competition during this period was ferocious. HeyTea, Nayuki's perpetual shadow, was growing just as fast, had arguably stronger product innovation (its "cheese tea" foam was genuinely inventive), and had attracted investment from Tencent. In Chinese tech and consumer discourse, the Nayuki-vs-HeyTea rivalry became a cultural meme on par with Pepsi-vs-Coke. Peng and Zhao obsessed over it. Every store Nayuki opened, HeyTea opened one nearby. Every new fruit Nayuki debuted, HeyTea copied within weeks. The two companies were effectively running a joint educational campaign for Chinese consumers, each funding the other's customer acquisition even as they competed for the same Floor 1 lease.

By the end of 2020, Nayuki operated 491 stores in 60+ cities. The brand had genuine prestige. Queues were still frequent. Weibo and RED (Xiaohongshu) were overflowing with content. The couple was about to take their company public.

What they, and their bankers, could not have fully appreciated was that they were arriving at the Hong Kong Stock Exchange at exactly the moment the Chinese consumer equity party was about to end.

IV. The IPO and the Reality Check

June 30, 2021, was a warm Wednesday in Hong Kong. At 9 a.m., Peng Xin stood on the bourse floor with Zhao Lin, ringing the ceremonial bell as Nayuki began trading under the ticker 2150.HK. The IPO was oversubscribed more than 400 times in the retail tranche. The company raised approximately HK$5.1 billion (around US$656 million) at an offer price of HK$19.80 per share, valuing Nayuki at roughly HK$34 billion—around US$4.4 billion.

Headlines across Asia called it the "First New-Style Tea Stock." The Financial Times' Lex column noted that Nayuki was trading at over 15x sales, a multiple more consistent with software than with food service. Peng and Zhao, paper-wealthy, did the round of Hong Kong CNBC interviews and smiled for cameras.

Then, in the first thirty minutes of trading, the stock dropped 13.5%. By the end of day one, it closed at HK$17.12, below the offer price. By the end of the first month, it was down 30%. By the end of 2022, it would trade below HK$5.

What happened?

The short answer is that two things went wrong simultaneously, one cyclical and one structural. Cyclically, the IPO landed just as the Chinese regulatory crackdown on internet and consumer companies was entering its most aggressive phase. The Didi IPO debacle a few days later triggered a multi-month reassessment of all US-listed Chinese tech, which spilled into Hong Kong. Global fund managers de-risked. Local Chinese retail investors, burned by Meituan and KE Holdings, pulled back.

Structurally, the reality check was harsher. The prospectus, which is a genuine masterclass in Chinese consumer disclosure, revealed that Nayuki had been operating at net loss every year of its existence. In 2020, the company reported a loss of roughly 203 million RMB on 3.06 billion RMB of revenue. Worse, same-store sales had been declining—the 2020 number showed a 25.3% drop in average daily store sales versus 2018, partly due to COVID but partly due to the cannibalization of new stores opening in the same markets. The gross margin story was fine, but the operating leverage story wasn't there.

And then there was the asset-heavy model. Each new Nayuki flagship cost approximately 1.8 million RMB to build out. Each required a manager, a baker, multiple tea-makers, and a full service team. Each was in Floor 1 of a luxury mall, which meant rents of 35,000-80,000 RMB per month. The model worked when a store was doing 70,000-100,000 RMB in daily sales. It broke when daily sales drifted to 40,000-50,000 RMB. And as the company opened more stores in more cities, the average daily sales per store was drifting, not climbing.

The segment breakdown told the story:

The core tea segment—fresh fruit teas, milk teas, and boutique single-ingredient teas—was the margin engine. A 28 RMB cup of Strawberry Magic Tea had genuinely attractive unit economics: raw material cost around 30-35% of retail, labor well-managed, gross margins in the 50s. This was a beautiful business.

The bakery segment was a different story. The prospectus revealed that bakery products—which Peng and Zhao had loved and defended against every consultant—carried meaningfully lower gross margins than tea. Fresh-baked goods had high waste rates (anything not sold by closing time was thrown out), required specialized labor (a trained baker is a full-time, full-salary hire), and needed equipment (ovens, proofing cabinets, refrigeration) that consumed store real estate that could otherwise be used for more seating or tea-making stations. The bakery was the differentiator—but it was also, financially, a drag.

By late 2021, Nayuki's management team began making noises about a concept called "Nayuki PRO." The PRO stores would be smaller (80-100 square meters instead of 180-200), cheaper to build out (around 1 million RMB per store versus 1.8 million), and, crucially, would remove the onsite bakery. Bakery items would still be sold, but they'd be shipped from centralized commissaries rather than baked on premises.

The PRO format was the company's first public admission that the original thesis had partially broken. The bakery, so central to the brand's early identity, had become an economic burden as the chain scaled. In Acquired terms, this was a classic "ugly truths in the prospectus" moment—the IPO forced the company to confront economics that private capital had been willing to overlook.

By the end of 2022, over a third of Nayuki's network was operating in the PRO format, and management was guiding to 70%+ PRO by 2024. The original standard-format flagships—the temples Peng had built—were being quietly rebranded, downsized, or in some cases closed. The strategic direction was clear: the company needed to cut capex per store, accelerate store-count growth, and find a way to get the asset base light enough to actually earn a return on capital.

And then, in October 2022, Nayuki did something nobody in the market saw coming.

V. M&A and the "Lelecha" Gambit

On October 9, 2022, Nayuki Holdings announced it had acquired a 43.64% stake in Shanghai-based Lelecha—specifically, in the operator Lelecha Holdings Limited—for approximately RMB 525 million in cash. The deal made Nayuki Lelecha's single largest shareholder, though it stopped short of control.

If you haven't followed the Chinese new-style tea market closely, Lelecha probably doesn't ring a bell. In fact, that was much of the point.

Lelecha was founded in Shanghai in 2016 by a younger entrepreneur named Wang Xiaolong. The brand was positioned as a premium, design-forward tea chain with a strong presence in Shanghai and Jiangsu-Zhejiang—exactly the Yangtze Delta market where Nayuki, a Guangdong-born company, had historically been weaker. At its peak, Lelecha had raised multiple rounds of VC funding and hit a reported valuation of 4 billion RMB in early 2021, just ahead of the new-style tea bubble top. By 2022, that valuation had collapsed. The company was burning cash, struggling to scale, and its backers were looking for an exit.

Nayuki's 525 million RMB check valued Lelecha at approximately 1.2 billion RMB—a 70% discount to the peak. On the surface, this was a classic distressed acquisition. But the strategic logic was richer than pure bargain-hunting.

First, geographic expansion. Lelecha's strongest city was Shanghai, where Nayuki had real presence but where HeyTea had historically been dominant. A 43.64% stake in the leading indigenous Shanghai premium chain gave Nayuki an instant foothold in the most lucrative consumer city in China without the cost of building from scratch.

Second, brand portfolio. Zhao Lin told Chinese business press at the time that he saw Lelecha as a "complementary brand" rather than a directly overlapping one. Lelecha had a slightly different positioning—younger, more design-trendy, a touch more art-studio—and could coexist with Nayuki rather than cannibalize it. This was the first hint that Nayuki's ambition was not just to be a tea chain but to become a multi-brand tea platform.

Third—and this is the piece Chinese consumer analysts noticed most—it was defensive M&A. The real risk to Nayuki in late 2022 was not that Lelecha would beat them. Lelecha on its own was weak. The risk was that HeyTea, or a consolidator like ChaPanda, would acquire Lelecha at a fire-sale price, bolt it onto their supply chain, and use it to blitz Shanghai. By taking the 43.64% stake, Nayuki put a poison pill in place: any future strategic transaction involving Lelecha would now require Nayuki's cooperation.

Did Nayuki overpay? This is a nuanced question. At 1.2 billion RMB for a company with rough parity to maybe 8-10% of Nayuki's own revenue, and at a moment of maximum distress in the sector, the absolute price was defensible. But the strategic cost was real: 525 million RMB was a significant chunk of the IPO proceeds, and it went into a minority stake in a struggling competitor rather than into new Nayuki stores, automation, or RTD expansion. Some analysts argued that the capital would have been better deployed in direct organic investment, given that Nayuki's own same-store sales were still under pressure.

The capital-allocation philosophy at play here is worth naming. Zhao Lin, in a rare CFO-style interview around the time, described Nayuki's approach as "building a moat wider than it is deep." Translated out of Chinese executive-speak, that meant: we would rather occupy more territory (more brands, more segments, more cities) than drive margins at the top of a single brand. This is a familiar posture in Chinese consumer M&A—think of how Alibaba or Meituan treat adjacent categories—and it runs directly counter to the kind of focused, high-ROIC capital allocation that Western long-term investors usually prefer.

Whether the Lelecha stake ultimately earned its cost of capital is, as of 2026, still an open question. Lelecha under joint oversight has stabilized, slowed its cash burn, and expanded selectively. It has not, however, become a breakout brand in its own right. In fundamental-investing terms, the transaction is better understood as an insurance premium against competitor consolidation than as a growth investment.

What the Lelecha deal really did was set up a pattern that would soon repeat: Nayuki was willing to abandon orthodoxy in pursuit of scale and market share. That willingness would be tested in the most dramatic way possible less than a year later.

VI. Inflection Point 2: The 2023 Great Pivot

In the early summer of 2023, the Chinese new-style tea market was a battlefield. The headline story was not Nayuki. It was Mixue Bingcheng.

Mixue, the self-described "snow king" of low-end tea, was a Henan-based chain that had been growing for years at the bottom end of the market—6 RMB lemon teas, 8 RMB milk teas, 500+ city coverage, and, crucially, pure franchising. By mid-2023, Mixue had blown past 30,000 stores globally. It was, by store count, almost ten times the size of Starbucks China. And it was growing faster.

Meanwhile, a second wave of mid-tier players—ChaPanda (Cha Bai Dao), Guming (Good Me), and Shanghai Auntie—were consolidating the 10-15 RMB price band with aggressive franchising models, hitting 5,000-7,000 stores each and taking meaningful share from both Mixue (on the upside) and Nayuki/HeyTea (on the downside).

The pincer was obvious. Mixue owned the value tier. The mid-tier chains owned the mass market. Nayuki, stranded at the premium top, was watching its addressable market shrink from below. Same-store sales were weak. The company's original 30+ RMB average ticket was drifting down toward 25 RMB as management rolled out lower-price SKUs to defend traffic.

Peng Xin and Zhao Lin had, from the founding, publicly vowed never to franchise. "A Nayuki cup must be a Nayuki cup," Peng had said in multiple interviews. The concern was classic premium-brand concern: franchisees would cut corners on fruit quality, ingredient freshness, and service, diluting the brand they had spent eight years building. Every time Chinese business press had asked about franchising, the answer had been a polite but firm no.

On July 20, 2023, they broke the vow.

Nayuki announced it would open its first franchisees in Tier 3 and Tier 4 cities. The initial franchise fee was set at 70,000 RMB, with total investment per store (including buildout, deposit, equipment, and initial inventory) in the 980,000 RMB range. Candidates had to demonstrate F&B experience, a minimum net worth, and an ability to operate at least two stores in their home region. Nayuki would control the supply chain (all raw materials sourced through central logistics), the digital systems, and the store design.

It was, as Zhao later acknowledged in interviews, a decision "three years later than it should have been." The team's resistance to franchising had been sincere—but the market had changed, and the competitive gap was growing too quickly to close with owned stores alone.

Why did this fundamentally change the trajectory? Three reasons.

First, the math. An owned Nayuki PRO store required roughly 1 million RMB of company capex. A franchised store required zero company capex. If Nayuki wanted to go from 1,200 stores to 3,000 stores—necessary to compete with ChaPanda and Guming on network density—doing it owned would have required 1.8+ billion RMB in additional capex, roughly the entire IPO proceeds. Doing it franchised let the company grow the network using someone else's balance sheet.

Second, the market access. Nayuki's brand prestige was real but lopsided. Survey data from Chinese consumer research firms showed that in Tier 1 and Tier 2 cities, Nayuki was among the most-recognized tea brands. In Tier 3 and Tier 4 cities—where a meaningful share of the population lived and where consumption was growing fastest—the brand was known (Chinese internet culture is extremely networked) but physically unavailable. Franchising was the only mechanism that could convert brand awareness into actual stores in these cities, because owned flagship economics didn't work outside of large metropolises.

Third, the strategic transition. What Peng and Zhao were really doing was shifting Nayuki from an Apple-style model ("we design, build, and operate everything") to a McDonald's-style model ("we provide the brand, the supply chain, the systems—franchisees provide the capital and local operations"). This was a profound business-model change. McDonald's, famously, is a real estate and franchising company dressed up as a restaurant chain. Nayuki was signaling that it wanted to become a brand, supply-chain, and technology company dressed up as a tea chain.

The impact showed up in the numbers within a year. By the end of 2024, Nayuki had opened over 300 franchised stores in 100+ cities, and the franchised cohort was weighted heavily toward Tier 3 and Tier 4. Average franchised-store revenue was lower than owned stores—the lower city tiers simply don't support the same ticket sizes—but franchised unit economics for the parent company were far better, because Nayuki earned a supply-chain margin on every cup sold without carrying the store-level capex.

The pivot was not without costs. Chinese consumer media reported multiple early franchising disputes, including at least one viral case where a franchisee in Fujian alleged that the company had oversold the economics. Internal quality-control had to be retooled rapidly—the company's proprietary store-management software became genuinely mission-critical, because it was the only way to monitor 1,800+ stores spread across hundreds of cities without a massive fieldforce.

By 2026, the owned-vs-franchised mix had shifted meaningfully, and the company's trajectory had clearly changed direction. The IPO-era Nayuki had been a premium Tier-1 flagship chain. The post-pivot Nayuki was something different: a tiered brand, operating owned flagships in the top cities and franchised PRO stores in the rest of the country, held together by a central supply chain and proprietary technology.

The move probably saved the company. It also forced a hard question: what would Nayuki mean as a brand if its stores ranged from a 200-square-meter flagship in Shenzhen Haian to a 60-square-meter franchise in a Tier 4 city in Anhui? That question is not yet fully answered.

VII. Management, Ownership, and Incentives

Stepping back from the strategy, one of the most distinctive features of Nayuki as a public company is how tightly it is still controlled by its founders.

Zhao Lin serves as Chairman. Peng Xin serves as General Manager. The division of labor remains much as it was at the blind date: Zhao handles capital, supply chain, and governance; Peng handles product, brand, and store experience. They are unusually open about their partnership in Chinese media, and they appear together at most investor events.

As of the most recent public filings, Zhao and Peng together—through their jointly controlled holding vehicle, Linxin Holdings Group—hold over 60% of the outstanding shares. This is, by the standards of Hong Kong-listed companies, an extremely high founder concentration. It matters for three reasons.

First, alignment. The couple's net worth is dominated by Nayuki equity. Every decision they make—pivoting to franchising, cutting prices, acquiring Lelecha, investing in automation—flows through their own pocketbook first. This is the kind of structural alignment that long-term fundamental investors usually prize. When management's economic interest and shareholders' interest are the same instrument, incentive misalignment drops sharply.

Second, speed. The 2023 franchising pivot is a decision that most professionally managed F&B companies would have debated for years. The Nayuki board approved it within weeks of management's recommendation. Founder control, when the founders are thoughtful, produces fast decision-making—especially useful in markets that move as quickly as the Chinese tea sector.

Third, governance risk. The flip side of founder control is a reduced check on the founders. If Peng and Zhao make a bad decision, there is no functional minority that can stop them. Chinese Hong Kong-listed companies with dominant founders have had mixed track records on governance, and while Nayuki has not had any notable governance controversies to date, the structural risk is real. Board independence, related-party transaction disclosure, and executive compensation are all areas where minority shareholders have to take some on trust.

On incentives, the company has rolled out share-option schemes in 2022 and 2023 that extend equity participation beyond the founding couple. The schemes target two groups: senior corporate management (CFO, Head of Supply Chain, Head of Technology) and, more interestingly, store managers. The store-manager grants are particularly notable during the franchising transition, because they create a direct economic tie between store-level outcomes and equity ownership—useful for keeping top operators on-side as the company's model becomes less owned and more franchised.

The culture at the corporate level is described by former employees, in generally favorable terms, as "product-obsessed and data-obsessed." Peng is known inside the company as a relentless taster—product launches can be delayed for weeks if she decides a flavor isn't right. Zhao is the classic operator—focused on supply-chain cost, lease terms, and unit economics. The management style is neither Silicon Valley nor old-line Chinese SOE; it is something more like a modern Asian consumer company, heavily digital, with a sharp-edged founder team at the top.

One particularly telling detail: Nayuki built its own proprietary store-management software from the very early days, and the company operates a significant internal tech team. In an F&B sector where most Chinese chains use off-the-shelf systems from vendors like Kaiyunchubang or Meituan, Nayuki's decision to develop its own stack signals how seriously the founders take data and operations as competitive advantages. That decision, which seemed indulgent when the company had 50 stores, looks prescient when you're coordinating 1,800.

The founder structure also shapes how capital is returned. Nayuki has declared modest dividends in profitable years but has not been aggressive on buybacks or on return of capital. With 60%+ of the shares in founder hands, any large buyback would disproportionately benefit the founders, and the company has been cautious about those optics. For long-term investors, the reinvestment-over-return-of-capital stance is worth watching: as the business matures and capex needs decline with franchising, the pressure for dividend or buyback policy to evolve will increase.

The short version: Nayuki is a founder-led company in the strongest sense. Investors who buy 2150.HK are, in effect, entering a partnership with Zhao Lin and Peng Xin—one that has produced excellent product and brand outcomes but requires trust in the couple's strategic judgment for the indefinite future.

VIII. The "Hidden" Businesses: Tech and RTD

Most discussion of Nayuki centers on the stores. But two segments buried in the filings reveal what the company is quietly becoming, and they are arguably more interesting than the store count.

The first is automation. Starting around 2019, Nayuki began investing in what the company calls its "automated tea-making machine"—a proprietary piece of kitchen equipment that automates the most labor-intensive and skill-dependent parts of the drink-making process. In a traditional new-style tea store, a trained barista needs around three months to become fully proficient: they have to learn fruit prep, tea brewing times, cheese-foam whipping, cup layering, and quality control across dozens of drinks. High turnover in the category—annual employee turnover at Chinese F&B chains typically runs 60-80%—means chains are perpetually training.

Nayuki's machine changes that math. According to company filings and trade-press coverage, the proprietary equipment automates tea brewing, fruit dosing, milk and cheese-foam application, and sugar calibration. The result, the company claims, is that training time for a new store employee drops from roughly three months to roughly one week. If that's broadly accurate—and independent Chinese trade press has largely confirmed it—the labor-cost implications at scale are substantial. Less training time means lower turnover costs, smaller per-store labor footprints, and more consistent product quality across 1,800+ stores.

More importantly for the long-term investor, the automation capability is a platform. Once a company has robotics good enough to make its own drinks, it can extend that capability in several directions: licensing the machines to other chains, using them to open smaller-footprint stores, or building "tea robots" into convenience-store partnerships. Nayuki has been quiet about commercial extensions, but the filings note ongoing R&D investment and multiple generations of the machine.

Calling Nayuki a "robotics company" is an overstatement. Calling it a "tea operations company with a robotics capability" is probably about right. But as the industry moves toward franchising-at-scale, the value of standardized, low-training-time equipment rises sharply. The automation R&D, viewed through that lens, is a direct enabler of the franchising pivot discussed in the previous section.

The second hidden business is RTD—Ready-To-Drink bottled beverages.

Starting around 2019 and accelerating after the IPO, Nayuki began selling bottled versions of its signature drinks through convenience-store channels: 7-Eleven, FamilyMart, Lawson, and the major domestic chains. These are not freshly made drinks—they're shelf-stable or chilled bottled teas, typically sold at 10-15 RMB per bottle, distributed through the same cold-chain networks that serve Coca-Cola and Uni-President.

RTD is a very different business from store-based tea. It has almost no labor cost. It requires no premium real estate. It scales through distribution agreements rather than store openings. Gross margins on established bottled-beverage SKUs typically run 40-60% for brand owners who don't manufacture their own bottles (Nayuki is a brand-and-recipe owner, with production contracted to third parties). The Chinese RTD tea market is enormous—Uni-President, Master Kong, Nongfu Spring, and a handful of other brands generate billions of RMB in revenue annually—and the growth of the segment has been robust as health-conscious consumers migrate away from sugar-heavy colas.

For Nayuki, RTD matters for two reasons. First, it's a margin-accretive revenue stream that doesn't compete with the stores—a customer buying a bottled Nayuki at 7-Eleven is often doing so at a time when visiting a store isn't convenient, not as a substitute. Second, it extends the brand's daily presence in consumers' lives. A Nayuki flagship, no matter how beautiful, is something you visit once a week at most. A Nayuki bottle in your fridge is something you reach for daily. In brand equity terms, RTD is a moat-deepener.

The challenge for RTD is shelf competition. Chinese convenience-store shelves are fiercely contested, and placement is pay-to-play. Nayuki, as a newer RTD entrant, has had to invest heavily in slotting fees and marketing support to secure premium shelf positions. The segment has been growing, but it has not yet reached the scale where it materially shifts the company's overall P&L. What it has done is establish Nayuki as a credible multi-channel beverage brand rather than a store-only operator, and that matters for how the business is valued over a long horizon.

Taken together, the automation and RTD businesses give a window into how Nayuki sees its own future. The store business is the front-end. The real moat—if there is one—is the backend combination of supply chain, technology, and brand, extended across owned stores, franchised stores, and bottled beverages.

IX. The Playbook: 7 Powers and Porter's 5 Forces

Now let's do the strategic work properly—the kind of structured analysis that Acquired does in its "playbook" segments. We'll apply Hamilton Helmer's 7 Powers first, then Porter's 5 Forces, and then draw the conclusions out.

Brand. Nayuki's primary power is brand, in the specific sense Helmer defines: a persistent and durable price premium unsupported by functional superiority alone. A 28 RMB Nayuki Strawberry Magic Tea is not objectively twice as good as a 14 RMB equivalent from ChaPanda. But Chinese Gen Z consumers have been willing to pay the premium, because "Nayuki" signals something—quality, aspiration, sophistication—that the cheaper brands don't. Whether the premium is 20% or 40% depends on the drink and the market, but it is real, and it has persisted through significant competitive pressure. Brand is the only one of the 7 Powers that reliably survives a price war, and we'll come back to this in the bear/bull analysis.

Scale Economies. Nayuki is approaching the scale at which its purchasing power starts to matter. With 1,800+ stores and strong RTD presence, the company is now a large enough buyer of premium fresh fruit—strawberries, grapes, peaches—that its supply contracts genuinely move markets. In winter, when fresh strawberries are scarce and expensive, Nayuki's contracts with specific suppliers in Yunnan, Shandong, and (for off-season) imports from Mexico give it pricing and availability that smaller chains can't match. This is Helmer's "cornered resource" in a soft form—not a patent, but a logistics edge that compounds with scale.

Counter-Positioning. The most interesting of the 7 Powers as applied to Nayuki is counter-positioning against the traditional beverage incumbents, especially Starbucks China. When Nayuki and HeyTea started, Starbucks paid no attention—tea was beneath them. By 2020, Starbucks China had introduced fruit-forward tea drinks, cold brews, and a "Starbucks Reserve" concept clearly designed to counter the premium new-style tea threat. Starbucks is now forced to compete in a segment that Nayuki helped create, but it cannot do so wholeheartedly without cannibalizing its coffee business. This is textbook counter-positioning: the incumbent cannot copy the disruptor's model without breaking its own.

Switching Costs, Network Economies, and Process Power—the remaining four of the 7 Powers—are largely absent. Consumers have no switching costs in tea (the category is famously promiscuous), there is no network effect, and while Nayuki's SOPs and automation confer some process advantage, this is nowhere near the level of, say, a Toyota Production System.

Now Porter's 5 Forces on the Chinese new-style tea industry as a whole.

Bargaining Power of Buyers: High. Chinese Gen Z consumers are cross-shopping across five to ten different tea brands. App-based ordering makes price comparison instantaneous. Loyalty programs matter at the margin but do not lock anyone in. The customer always has alternatives, and the customer knows it.

Bargaining Power of Suppliers: Moderate. Fresh fruit and dairy suppliers have some leverage in peak seasons and for premium ingredients, but the industry has enough aggregation (cross-chain buying, large agricultural co-ops, frozen alternatives) that no single supplier can dominate. The real supplier power is in commercial real estate—landlords at Floor 1 of top malls genuinely can dictate terms. This is why the franchising pivot, which transfers real-estate risk to franchisees, is so important.

Threat of New Entrants: Moderate, declining. In 2015, the category was wide open and a good concept with capital could enter freely. In 2026, the space is crowded, brand-heavy, and requires meaningful capital to achieve competitive scale. New entrants face difficulty, unless they come from adjacent categories (a coffee chain adding tea, an F&B conglomerate launching a new sub-brand). The biggest risk of new entry is actually re-entry by large beverage incumbents with huge brand budgets.

Threat of Substitutes: High. This is the single most important of the five forces for Nayuki's long-term story, and it deserves a full paragraph. Coffee is the silent killer. Luckin Coffee, which operates a technology-forward, app-first, low-price coffee model, had crossed 20,000 stores in China by late 2024 and was priced aggressively at 10-15 RMB for a latte. Manner Coffee, premium-positioned, was at 1,000+ stores. Starbucks continued to expand. Chinese Gen Z consumers genuinely substitute between tea and coffee on a daily basis—the same 25 RMB budget gets spent on Luckin on Monday, Nayuki on Tuesday, HeyTea on Wednesday. The rise of coffee in China, which was not on anyone's Nayuki investment memo in 2018, has become the most important competitive pressure on the category by 2026.

Intensity of Rivalry: Extreme. "Red Ocean" is the phrase Chinese business press uses, and it is apt. The category contains at least ten chains with 2,000+ stores each, all competing in overlapping price bands, with significant VC and strategic capital fueling expansion. Consolidation will eventually come—it always does in Chinese consumer markets, as Mixue's IPO signaled—but we are not yet through the worst of the rivalry phase.

The practical implication of this analysis for long-term investors is straightforward: brand is the only durable power Nayuki possesses, and brand alone is not enough in a category with high buyer power, high substitute threat, and extreme rivalry. Management has to compound brand with scale, cost position, and technology to produce sustainable returns. The 2023 franchising pivot, the Lelecha stake, the automation R&D, and the RTD expansion can all be read as attempts to build those additional supports.

X. Analysis: The Bear vs. Bull Case

Every good company has both a bear case and a bull case that a reasonable investor can hold. Nayuki has two particularly well-developed versions of each.

The Bear Case: The Premium Era Is Over.

The bear case starts with a simple observation: Nayuki's average ticket has fallen meaningfully from its 2019 peak. The "30 RMB tea" that defined the brand's founding thesis has given way to a more bifurcated menu where popular drinks sit at 15-22 RMB. Management framed this as "broadening the price range" but the honest version is that Gen Z consumers, after a decade of cross-shopping, are no longer willing to pay 30 RMB routinely when 14 RMB alternatives taste broadly similar.

If this trend continues, the bear says, Nayuki's brand premium erodes into a "slightly better than average" position rather than a premium one. The company becomes one of several large mid-tier chains, differentiated on logo and store aesthetics but not on price power. The franchising pivot, which is necessary for scale, also accelerates the commoditization—franchised stores in Tier 3 cities operate at prices that look nothing like the Shenzhen flagship, and over time the brand's center-of-gravity moves downward. In the worst case, Nayuki becomes the BMW of tea: premium historically, aspirational in emerging markets, but structurally unable to command Starbucks-like margins because the underlying product is too easy to substitute.

Add to this the macro challenges: Chinese consumer sentiment has been weak through 2024 and 2025, discretionary spending among young consumers has been under pressure, and the broader economic environment has favored value over premium across most categories. If "consumption downgrade" becomes the dominant pattern, a premium-born brand has more to lose than a Mixue Bingcheng does.

The valuation lens for the bears: the stock, which listed at HK$19.80 and cratered below HK$5, has been volatile. Earnings visibility is imperfect, and the transition period of moving from owned-heavy to franchise-heavy makes near-term comparisons noisy.

The Bull Case: Scale Plus Brand Plus Technology Equals Category Dominance.

The bull case starts with the observation that Nayuki is one of only two or three brands in all of Chinese new-style tea with genuine national prestige. HeyTea is the other clear one. Everyone else is regional, or value-positioned, or in a niche. Prestige brands in large consumer categories, once earned, are hard to build and usually survive shocks.

The bull says: the franchising pivot has unlocked a massive Tier 3 and Tier 4 market that Nayuki couldn't access before. The automation technology solves the labor and training problem that plagues every scaled F&B operation. The RTD business gives the company a second, higher-margin revenue stream. The supply-chain infrastructure, built for 1,800+ stores, becomes a competitive moat because new entrants can't replicate it quickly.

If Nayuki can maintain its premium brand positioning in Tier 1 and Tier 2 cities—through the owned flagship network, careful franchise quality control, and ongoing product innovation—while expanding aggressively in lower tiers through franchising, the company captures the full economic pyramid of Chinese tea consumption. In this scenario, Nayuki becomes something like what Starbucks is in the US: the default brand for urban consumers across multiple price points, with broad-based distribution that a pure premium player can't match.

On the numbers, bulls point to the structural economics of franchising: a franchised store generates high-margin supply-chain and royalty revenue for Nayuki with essentially zero ongoing capex from the parent company. As the franchised cohort grows past 1,000 stores, the P&L starts looking meaningfully different—higher blended margins, lower capex intensity, better free cash flow. Add in the RTD segment, and the terminal state of the business is more attractive than the IPO-era store-based model ever was.

Competitive Comparison.

Against HeyTea, Nayuki has a similar premium brand position but has been slightly slower and less aggressive on innovation. HeyTea tends to have more viral product launches; Nayuki tends to have a steadier, more restrained brand voice. The two are broadly matched on scale.

Against Mixue Bingcheng, Nayuki is competing in a different segment entirely. Mixue is the value king, and its 40,000+ store network (as of 2026) and recent listing represent the dominant force in the value tier. Nayuki cannot compete with Mixue on price and should not try.

Against ChaPanda, Guming, and Shanghai Auntie, Nayuki's edge is pure brand. These mid-tier chains have larger store networks and similar store economics but lack the top-tier prestige. Nayuki's strategic question is whether its brand premium justifies a smaller network or whether it needs to get its network close to mid-tier scale to matter.

Against Starbucks and Luckin (substitutes more than direct competitors), Nayuki sits in an interesting middle. It is more Chinese, more product-forward, and better on tea than either, but it cannot match Starbucks on space (Starbucks' "third space" in coffee is still the gold standard) or Luckin on price-per-cup efficiency.

The Investing Lesson.

The Acquired-style one-liner for Nayuki is this: operational excellence is a prerequisite, but brand is the only moat that survives a price war. Nayuki's management understands this. The question for long-term fundamental investors is whether the brand, extended across an increasingly franchised and tiered network, can sustain the premium that underwrites the business. That is a judgment call, not a calculation, and it is the single most important variable to track.

Key KPIs to Monitor.

For the long-term investor following Nayuki, three KPIs stand out as the most useful signals:

Same-store sales growth (SSSG) in the owned-store portfolio. This is the purest read on brand health. Because owned stores are concentrated in Tier 1 and Tier 2 cities where the brand premium is tested most aggressively, owned-SSSG is the canary in the coal mine for any erosion of brand power.

Net franchise store additions and franchise churn. Franchising at scale requires a healthy pipeline of new operators and, crucially, low churn of existing ones. A rising franchise store count paired with low franchise exits is a sign of a healthy system. Rising churn is a warning.

Blended gross margin, ex-bakery and owned-store rent. As the mix shifts toward franchising and RTD, the headline gross margin moves in ways that don't cleanly reflect operational performance. The underlying ingredient and supply-chain margin, stripped of one-off model effects, is the real signal on the unit economics of the category.

Peripheral flags to keep an eye on, lightly: related-party transactions and executive compensation disclosure (given the founder-concentrated ownership), any changes in auditor or material accounting judgments around the Lelecha investment, expansion or restatement of the automation and RTD segment disclosures, and any 13F-style disclosures from Chinese PE or strategic investors moving into or out of the equity. None of these are presently flashing red, but given Nayuki's structure and stage, they are worth a glance each quarter.

XI. Epilogue

There's a scene described in a Chinese magazine profile from 2022 that sticks with you. Peng Xin is doing a store walkthrough at a Nayuki flagship in Shanghai. She tastes a new peach tea, pauses, and tells the store manager the ice-to-tea ratio is off by about five percent. The store manager, who has been in the job for two years, adjusts the recipe on the spot. Peng moves to the bakery side, picks up a strawberry-cheese cake, bites into it, and says the strawberries are a day too old. The manager nods. Zhao, who has been standing nearby, pulls up a tablet, looks at the supply-chain data, and confirms that the current delivery is from a backup supplier because the primary one had a logistics delay. Within twenty minutes, the primary supplier's operations manager is on a call getting a pointed conversation.

That scene, to the extent it is accurate, captures why Nayuki has been able to do what it has done. It is a company run by people who care about the product in a detailed, almost obsessive way. The blind date in 2015 brought together a product visionary and an operator, and the partnership has produced, over eleven years, one of the most valuable and most recognizable new consumer brands in China.

Today, Nayuki is not just a tea chain. It is a brand, a supply chain, a technology stack, a robotics program, an RTD business, a franchise system, and a minority stake in a secondary brand—all held together by a founder couple with 60%+ of the equity and a willingness to pivot when the evidence demands it. The company has survived the IPO hangover, the Lelecha bet, the franchising pivot, and the price war, and it is still standing in a category where many peers have not.

What happens next depends on factors that are both knowable and unknowable. Knowable: the rate of franchise expansion, the progress of automation, the RTD shelf presence, the same-store sales trajectory. Unknowable: whether Chinese Gen Z consumers in 2030 will still pay a premium for a branded tea, whether coffee continues its relentless encroachment, whether a new disruptor emerges with a format nobody has imagined yet.

A decade ago, Peng Xin walked into a mall in Shenzhen with a set of blueprints most people thought were crazy. Eleven years later, her blueprints have been copied, contested, scaled, and reimagined across a country of 1.4 billion people. The tea in the cup has not changed that much. Almost everything else has.

XII. Outro and Further Reading

Recommended Links: The Nayuki Holdings 2021 Prospectus (a genuinely outstanding read on the Chinese F&B market, the category's origins, and the asset-heavy-to-asset-light transition), the company's 2023 Interim Announcement introducing the franchising program, industry reports on the "Great Tea War" from iResearch and Frost & Sullivan, and Zhao Lin's early interviews with Chinese business press describing the Shenzhen tech-and-consumer scene circa 2015.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube