Classys: The Hidden Giant of K-Beauty Tech

I. Introduction & The "K-Beauty" Thesis

Everyone knows K-Pop. BTS has conquered stadiums from Seoul to São Paulo, their choreography studied by teenagers on every continent, their merchandise driving billions in revenue. Everyone knows K-Content. Squid Game made Netflix executives weep with joy as 142 million households tuned in during its first month, spawning a global obsession with Korean storytelling. But here is the real sleeper hit of the Korean Wave, the one that has not yet penetrated Western investor consciousness: K-Aesthetics.

Walk down the streets of Gangnam, Seoul's gleaming district of designer boutiques and towering medical buildings, and you will encounter something remarkable. Every few blocks, another dermatology clinic. Another plastic surgery center. Another aesthetic medicine practice promising to turn back time without surgery. Neon signs advertise the latest treatments in Korean, Chinese, Japanese, and English, catering to an international clientele that flies in specifically for procedures. This is not a neighborhood phenomenon. This is an industry.

South Korea has more plastic surgeons per capita than any country on earth. Its citizens spend more on beauty procedures than those of almost any other nation. The country has transformed aesthetic medicine from a luxury indulgence to a mainstream wellness category, with procedures marketed as casually as gym memberships or spa treatments. And its medical device companies have quietly built global empires while Western investors looked elsewhere, dismissed these upstarts as copycats or niche players.

In this ecosystem, a quiet revolution took place. While American and European device makers charged premium prices for machines that delivered impressive results but left patients wincing in pain, a dermatologist-turned-entrepreneur named Jung Sung-jae asked a fundamentally different question. What if the device did not need to be perfect? What if it just needed to be good enough, fast enough, and accessible enough to transform an occasional luxury into an everyday procedure?

That question birthed Classys, a company that started as a copycat device maker in a cramped office and evolved into what private equity giant Bain Capital came to see as the potential "LVMH of Aesthetics." The numbers tell part of the story, and they are extraordinary. A market capitalization hovering around three trillion Korean won, roughly three billion US dollars. Operating margins exceeding fifty percent, the kind of profitability typically reserved for software companies, not hardware manufacturers who must source components, assemble devices, and manage physical supply chains. A razor-and-blade business model so elegant that it generates recurring revenue streams that would make SaaS executives green with envy.

But numbers alone do not capture what makes Classys remarkable. This is a company whose flagship product became so ubiquitous in Korea that patients walk into clinics asking for a "Shurink" the same way Americans ask to "Google" something or "Uber" somewhere. Brand genericization, that rare phenomenon where a trademark becomes synonymous with an entire category, happened organically through word of mouth, influencer recommendations, and the relentless pursuit of accessibility. It is a company that attracted Bain Capital to pay a substantial premium for control in 2022, seeing in it not merely a Korean device maker but a global platform waiting to be unleashed. And it is a company now in the midst of an aggressive M&A spree, acquiring competitors and distributors as it transforms from an R&D-focused innovator into a consolidated aesthetics empire.

The journey from a dermatologist's side project to a private equity darling spans nearly two decades. It encompasses the democratization of cosmetic procedures, the power of brand-building in medical devices, the delicate transition from founder-led to professionally managed, and the question every investor should ask: can a Korean company truly become the dominant global player in the multi-billion-dollar non-invasive aesthetics market? The global HIFU aesthetics market alone is projected to grow from approximately 1.7 billion dollars in 2025 to over 4.1 billion dollars by 2033, representing a compound annual growth rate exceeding eleven percent. Classys commands roughly seventeen percent of that global market and an astounding fifty-five percent of its home Korean market.

Let us trace that journey from the beginning, from a Gangnam clinic where a dermatologist noticed something his American colleagues had missed.

The stakes are high. The global aesthetic device market generates tens of billions in annual revenue and is growing at double-digit rates. An aging global population, the rise of social media that puts appearance under constant scrutiny, and increasing acceptance of cosmetic procedures among younger demographics all contribute to secular tailwinds. But the industry remains fragmented, with no single player commanding dominant global share the way market leaders do in pharmaceuticals or medical devices for other specialties. The opportunity for consolidation is real. The question is whether Classys can seize it.

Understanding Classys requires understanding the intersection of several trends: the globalization of beauty standards, the professionalization of aesthetic medicine, the rise of Asia as a center of medical innovation, and the increasing willingness of private equity to invest in healthcare businesses with attractive unit economics. Each trend creates opportunity and risk. Together, they define the landscape in which Classys must execute its ambitions.

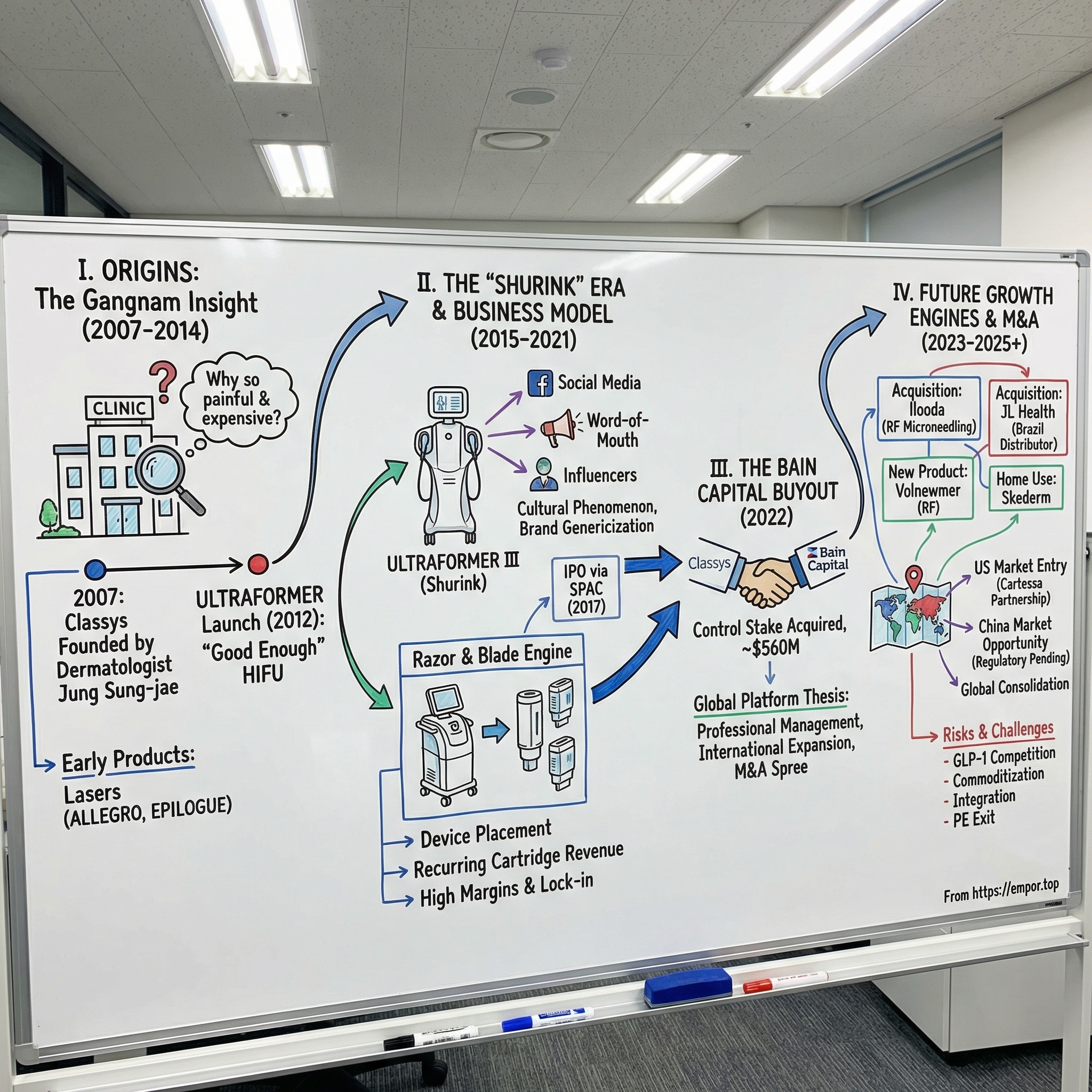

II. Origins: The Democratization of Lifting (2007-2014)

In the early 2000s, Jung Sung-jae was living a comfortable life as a dermatologist in Gangnam, the affluent district that would later become synonymous with Korean beauty culture through viral songs and international media coverage. Born in October 1967, Jung had followed a conventional path for a Korean medical professional. He earned his medical degree from Hanyang University, one of Korea's respected institutions, then specialized in dermatology. By 2002, he had established himself as the director of Soft Touch Dermatology Clinic in Seoul, treating patients who wanted to turn back time without going under the knife.

The clinic's location in Gangnam was no accident. By the turn of the millennium, Gangnam had already become a destination for cosmetic procedures, drawing patients from across Korea and increasingly from neighboring countries like China and Japan. The district's dermatology clinics competed fiercely for a demanding clientele, patients who had seen the latest treatments advertised on television dramas and expected nothing less for themselves.

Gangnam's concentration of aesthetic medicine practices created a unique ecosystem for innovation. With hundreds of clinics within walking distance of each other, physicians could easily compare notes on new technologies. If one clinic achieved impressive results with a new device, word spread quickly. Patients, similarly, could comparison-shop among clinics, creating competitive pressure to adopt the latest and most effective treatments. This hothouse environment accelerated the diffusion of innovations and raised the bar for quality continuously.

But something nagged at Jung as he worked. The dominant technology for non-surgical face lifting was a device called Ultherapy, developed by the American company Ulthera. Ultherapy represented genuine innovation. It used High-Intensity Focused Ultrasound, or HIFU, to focus sound waves at precise points beneath the skin, heating tissue to temperatures around 65 degrees Celsius. To understand how this works, think of a magnifying glass focusing sunlight to create a hot spot. HIFU does the same thing with ultrasound energy, creating tiny points of thermal damage at specific depths beneath the skin surface. This thermal energy triggered the body's natural collagen production, gradually lifting and tightening sagging skin over the following weeks and months. No scalpels. No general anesthesia. No extended recovery. Patients could have a treatment during lunch and return to work in the afternoon.

The problem was the execution. Ultherapy sessions were excruciatingly painful. Despite applying topical anesthetics, patients often required sedation or significant numbing agents to tolerate the procedure. Some described it as feeling like rubber bands snapping against the face while someone simultaneously poked them with hot needles. A single treatment cost three thousand dollars or more. The device itself was prohibitively expensive for most clinics, requiring a substantial capital investment that only premium practices could justify. And the procedure took so long, sometimes ninety minutes or more, that dermatologists could only squeeze in a handful of patients per day.

The high pain threshold created a patient experience problem that affected repeat treatment rates. Patients who endured one Ultherapy session often hesitated to return for follow-up treatments, even when results were good. This reluctance limited the lifetime value of each customer relationship and constrained the growth of the overall market. A less painful alternative could not only capture share from Ultherapy but also convert patients who had sworn off the category entirely.

Ultherapy was effective, but it was also exclusive. It served wealthy patients willing to endure significant discomfort. It did not serve the masses. And in Gangnam, where middle-class Koreans increasingly sought the same treatments as the wealthy, that exclusivity represented a market failure waiting to be exploited.

The gap between what was technologically possible and what was practically accessible haunted Jung. He saw patients in his clinic who needed lifting but could not afford Ultherapy. He saw patients who started Ultherapy treatments but did not return because the pain was too severe. He saw an incumbent company that seemed more interested in maintaining premium positioning than expanding the market. The classic innovator's dilemma was playing out in real time, and Jung recognized the opportunity.

Jung saw this gap with the eyes of both a physician and an entrepreneur. He watched patients leave his clinic because they could not afford Ultherapy or could not tolerate its pain profile. He watched competitors charge premium prices while turning away volume. His insight was deceptively simple: what if a device could deliver ninety percent of Ultherapy's results for twenty percent of the price with fifty percent less pain? In the world of technology strategy, this approach has a name. Clayton Christensen, the Harvard Business School professor who coined the term, called it disruptive innovation. The establishment dismisses the newcomer as "not good enough" while the newcomer captures the entire bottom of the market and steadily works its way up.

On January 10, 2007, while continuing to run his dermatology practice, Jung founded Classys. The name itself was aspirational, evoking class and sophistication, the kind of brand identity that would resonate with Korean consumers who valued premium positioning even in accessible products. The reality was more modest. Working alongside his clinic responsibilities, Jung assembled a small team to develop energy-based devices for aesthetic medicine. The early years were spent learning, reverse-engineering existing technologies, understanding the physics of therapeutic ultrasound and light-based treatments.

The dual role of practicing physician and medical device entrepreneur gave Jung a unique advantage. He could test concepts directly on patients, gather real-time feedback, and understand clinical needs in ways that pure device company executives could not. This physician-founder archetype is common in successful medical device companies, from the orthopedic surgeons who founded Zimmer to the cardiac specialists who built Medtronic's pacemaker business. Jung fit the mold: technically capable, clinically credentialed, and entrepreneurially ambitious.

The first products, launched in 2009, were competent but unremarkable: a 1450nm diode laser for acne treatment called ALLEGRO and an 808nm diode laser for hair removal called EPILOGUE. These devices entered a crowded market where dozens of Korean and Chinese manufacturers were producing similar equipment. They proved Classys could manufacture functional medical devices, but they did not differentiate the company or suggest the breakthrough that would come.

The real breakthrough came in February 2012 when Korea's Ministry of Food and Drug Safety approved the ULTRAFORMER, Classys's first HIFU device. This was not just another laser. This was a direct assault on Ultherapy's market position. The ULTRAFORMER could perform the same basic function, focusing ultrasound energy to stimulate collagen production, but it did so with a fundamentally different philosophy. Where Ultherapy prioritized clinical precision and supported that precision with premium pricing and elaborate training programs, Classys prioritized accessibility. The devices were cheaper to purchase. The treatments were faster to perform. The pain, while still present, was more manageable because the energy delivery was optimized for comfort over maximum intensity.

The regulatory approval represented validation that Classys could meet the quality and safety standards required for medical devices. Korea's MFDS is a rigorous regulator, and approval signaled that the ULTRAFORMER was not merely a knockoff but a legitimate medical device that could be safely used on patients. This regulatory milestone opened doors to international markets that required evidence of home-country approval as a prerequisite for their own review processes.

What Jung understood, and what American medical device executives sometimes missed, was that the Korean market valued different tradeoffs. Korean patients were more price-sensitive and more willing to undergo frequent, milder treatments rather than occasional intensive ones. Korean clinics operated on tighter margins and needed higher patient throughput to remain profitable. A device that was perhaps eighty percent as effective but could treat three times as many patients at one-third the price per session was not a compromise. It was a better product for its target market.

Interestingly, Jung was not content with building just one company. In 2004, three years before founding Classys, he had co-founded the skincare brand Dr. Jart+ with entrepreneur Lee Jin-wook. The name was a clever portmanteau: "Doctor joins art," signaling a fusion of medical expertise with aesthetic sensibility. Dr. Jart+ would go on to become a globally recognized K-beauty brand, famous for its BB creams and sheet masks, eventually attracting acquisition interest from Estée Lauder, which acquired a stake in 2015 and later full ownership. This dual entrepreneurial track revealed something important about Jung's thinking. He understood that the K-beauty wave was coming, and he positioned himself to catch it from multiple angles, both consumer products and medical devices.

By August 2014, Classys had refined its HIFU technology into the ULTRAFORMER III, which received Korean regulatory approval. The third generation represented genuine advancement. It featured what Classys called MMFU Technology, standing for Micro and Macro Focused Ultrasound, allowing practitioners to target different tissue depths with different treatment heads. By December, the device had earned CE marking for European markets, opening distribution possibilities beyond Asia. The company was ready for the next phase.

But what happened next exceeded even Jung's ambitious projections. The ULTRAFORMER III, marketed in Korea under the brand name "Shurink," was about to become a cultural phenomenon that would redefine how Koreans talked about facial rejuvenation.

The timing proved fortuitous. The mid-2010s saw the acceleration of Korean Wave cultural exports, with K-Pop groups achieving unprecedented international success and Korean dramas streaming globally on Netflix and other platforms. The world was becoming increasingly interested in Korean culture, Korean style, and Korean beauty secrets. Classys was about to ride that wave in ways that no Western medical device company could replicate.

III. The "Shurink" Era & The Razor-Blade Engine (2015-2021)

The name was genius in its simplicity. "Shurink" derived from "shrink," the English word perfectly describing what the device did to sagging skin. In Korean, it was catchy, easy to remember, and crucially, it did not sound like medical jargon. When Korean women began discussing their beauty routines at cafes and on social media, they did not say they were getting "High-Intensity Focused Ultrasound treatments" or even "ULTRAFORMER III procedures." They said they were getting "a Shurink."

This linguistic transformation was not accidental. It reflected a broader strategy that Classys executed with remarkable precision during the mid-2010s. The company understood something that Western medical device manufacturers often missed: in aesthetic medicine, brand recognition matters as much as clinical efficacy. Perhaps more. Patients do not analyze clinical studies or compare energy output specifications. They ask their friends what works. They watch what influencers recommend. They trust names they have heard repeated again and again.

The power of a memorable brand name should not be underestimated in healthcare. Botox became synonymous with wrinkle reduction even though it competes against other neurotoxins like Dysport and Xeomin. Lasik became the generic term for laser eye surgery regardless of the specific technology used. Brands that achieve this categorical status enjoy marketing advantages that competitors struggle to overcome. Shurink's emergence as a categorical brand in Korea represented a strategic asset that would prove difficult for rivals to replicate.

The Gangnam clinics provided the perfect laboratory for this brand-building experiment. By 2015, the district had become a global destination for cosmetic procedures, drawing medical tourists from across Asia and beyond. Japanese women flew in for weekend treatment getaways. Chinese tourists combined shopping trips with dermatology appointments. Southeast Asian patients sought treatments unavailable or unaffordable in their home countries. The clinics competed fiercely for this cosmopolitan clientele, and they needed devices that could deliver visible results quickly enough to justify an international trip.

The medical tourism angle deserves elaboration because it would prove central to Classys's international expansion. Patients who visited Gangnam for treatments returned home as ambassadors for Korean aesthetic medicine. They shared their experiences on social media, recommended treatments to friends, and created demand for Korean devices in their home markets. This organic word-of-mouth marketing proved more powerful than any advertising campaign could achieve.

The phenomenon created a virtuous cycle. As more patients sought "Shurink" treatments, more clinics worldwide wanted to offer them, which expanded the installed base, which generated more word-of-mouth, which attracted more patients. This flywheel effect is difficult for competitors to replicate because it depends on accumulated brand equity and patient experiences that cannot be created overnight.

The ULTRAFORMER III fit this need perfectly. Its treatment speed allowed clinics to see dramatically more patients per day compared to Ultherapy. Where an Ultherapy session might consume ninety minutes or more of chair time, a Shurink treatment could be completed in thirty minutes, sometimes less. One industry estimate suggested a tenfold increase in patient volume was theoretically possible, though actual improvements varied by practice. This throughput advantage transformed clinic economics.

The math was compelling. If a clinic invested in an Ultherapy machine at significant capital cost, it could perhaps perform three to four treatments daily, each generating several thousand dollars. With Shurink, the same clinic might perform thirty to forty treatments at lower individual prices, but with far higher aggregate revenue and better capacity utilization. And because the price point was lower, it attracted patients who would never have considered Ultherapy. Young professionals seeking preventive maintenance. Students preparing for job interviews where appearance mattered. Middle-class mothers who wanted to look refreshed without spending a month's salary. The market was not zero-sum. Classys was expanding the entire pie.

This market expansion strategy echoes what happened in other industries when "good enough" alternatives emerged. When Southwest Airlines offered no-frills flights at lower prices, it did not simply steal passengers from legacy carriers. It created entirely new categories of travelers who would not have flown at all at premium prices. When Japanese automakers introduced reliable, affordable vehicles in the 1970s and 1980s, they did not just take market share from Detroit. They brought car ownership to segments of the population that had relied on used vehicles or public transit. Classys was doing the same thing for facial rejuvenation: democratizing access to treatments that had previously been reserved for the affluent.

The social dynamics of Korean beauty culture amplified this effect. In Korea, discussing cosmetic procedures carries less stigma than in many Western cultures. Women openly share their beauty routines, including professional treatments, with friends and on social media. This transparency meant that each satisfied Shurink patient became a potential referral source, recommending the treatment to friends and family members who might never have considered it otherwise.

But the truly elegant aspect of the business model remained hidden from casual observers. Like Gillette with razors or HP with printers or Keurig with coffee machines, Classys had constructed a razor-and-blade engine that generated exceptional economics from an installed base.

Here is how it works. The device itself, the "razor," was priced accessibly relative to competitors to maximize clinic penetration. Classys wanted its machines in every dermatology office, every med spa, every aesthetic practice that treated facial concerns. Getting the hardware placed was step one.

The real profit came from the "blades": disposable cartridges containing the ultrasound transducers that delivered the treatment. Unlike laser devices, which use solid-state emitters that can operate essentially indefinitely with minimal consumables, HIFU machines require these cartridges. The ultrasound transducers wear out over time, losing efficacy after a certain number of "shots" or energy pulses. Each cartridge had a limited number of shots, typically several hundred, and once depleted, the clinic needed to purchase more from Classys.

This created a recurring revenue stream that grew more valuable as the installed base expanded. Every new machine placement represented years of future cartridge purchases. By the early 2020s, consumables had grown to represent more than fifty-five percent of company revenue, with gross margins reportedly exceeding eighty-five percent. Think about that for a moment. More than half of Classys's revenue came from products with margins approaching those of software licenses, but these were physical goods that customers had to keep buying to use equipment they had already purchased.

Consider what this means for competitive dynamics. Once a clinic purchases a Classys device for fifty thousand dollars or more, it is effectively locked into purchasing Classys cartridges for the five to seven year useful life of that machine. The clinic has already trained its staff on the device, invested time in learning its protocols and optimal settings. It has marketed Shurink treatments to its patients, building recognition around that specific brand. It has built workflows around the technology, scheduling slots and pricing services accordingly. Switching to a competitor would mean writing off that capital investment, retraining staff, rebuilding marketing around a new brand, and explaining to loyal patients why they should try something different. The switching costs are enormous.

The financial implications of this lock-in are profound. Each new device placement represents not just a one-time sale but a multi-year revenue stream from cartridges. Analysts who value Classys purely on device revenue miss the point. The proper framework values the installed base as an annuity, generating predictable high-margin revenue for years after the initial sale. This annuity characteristic explains why Classys's valuation multiples exceed those of competitors with similar revenue but less favorable revenue mix.

The consumables model also creates barriers to competitive displacement. Even if a competitor develops a superior HIFU device, clinics with existing Classys machines have strong incentives to continue using them until end-of-life rather than write off the capital investment. This installed base protection provides Classys with several years of visibility into its revenue trajectory, a luxury that pure equipment companies do not enjoy.

In October 2017, Classys announced its intention to go public through a merger with KTB Special Purpose Acquisition 2 Co, a SPAC listed on the KOSDAQ exchange. The merger ratio was set at one KTB SPAC share for every 54.97 shares of Classys, reflecting the relative valuations. The merger became effective in late November, and trading began on December 28, 2017, under the stock code 214150.

The SPAC route was unconventional for a company of Classys's profile. Most successful Korean medical device companies would pursue traditional IPO processes with underwriters and roadshows. But the SPAC structure offered advantages: faster execution, more certain pricing, and the ability for existing shareholders to monetize a portion of their holdings without the unpredictability of a public offering. Jung Sung-jae and his family retained controlling stakes while gaining access to public market liquidity.

The choice of a SPAC merger rather than a traditional IPO reflected pragmatic calculation. Traditional IPOs in Korea require extensive disclosure, lengthy regulatory review, and acceptance of whatever price the market determines on offering day. SPAC mergers provide more negotiating flexibility and faster timeline. For a company that did not urgently need capital but wanted public market access and founder liquidity, the SPAC route made sense.

The merger also provided Classys with a platform for future capital raising if needed. Public company status enabled access to equity markets for potential acquisitions and gave the company currency in the form of publicly traded shares. These options would prove valuable years later when Bain Capital came calling.

The public market initially responded with skepticism. Was this really just another Korean device company? Could margins this high be sustainable when the underlying technology was not proprietary? Would Chinese competitors, already flooding Asian markets with lower-cost alternatives, eventually commoditize the technology to zero? Would Ultherapy fight back with pricing adjustments or new product launches? These questions would persist for years, even as the company's financial performance provided increasingly emphatic answers.

By fiscal year 2020, revenue had reached 76.5 billion Korean won. The company had proven its model worked, but growth was about to accelerate. In October 2021, Classys launched the next generation device: the ULTRAFORMER MPT, marketed as "Shurink Universe." The "MPT" stood for Micro-Pulsed Technology, a meaningful refinement in energy delivery.

To understand why this mattered, consider the physics. Traditional HIFU creates a line of discrete thermal points beneath the skin, typically seventeen coagulation points per treatment line. Each point triggers collagen remodeling, but the untreated tissue between points can limit overall efficacy. The MPT technology created 417 micro-coagulation points per line, a fundamentally denser pattern of thermal injury that stimulated more comprehensive collagen production. Classys claimed three times more powerful tissue effects with enhanced procedural speed. The innovation pipeline was not slowing down.

Financial results during this period were remarkable. Revenue grew from 76.5 billion won in 2020 to 180 billion won by 2023, a compound annual growth rate exceeding thirty percent. Operating margins remained consistently between forty-eight and fifty-three percent, defying expectations that competition would compress profitability. The company had installed over eighteen thousand units globally since the 2014 Ultraformer III launch, representing an annuity stream of cartridge purchases.

What investors may have underestimated was the cultural flywheel effect. As Shurink became synonymous with HIFU in Korea, it generated continuous free marketing. Beauty influencers on Instagram and YouTube documented their treatments, showing before-and-after photos to millions of followers. Medical tourism agencies promoted Shurink specifically to foreign visitors, using the brand name rather than the generic category. Korean celebrities casually mentioned their procedures in interviews and variety show appearances, normalizing regular maintenance treatments. Foreign visits to South Korean beauty clinics reached an all-time high in 2024, spiking over ninety percent year-over-year to 1.17 million visitors. Many of those visitors came specifically seeking the Shurink experience they had heard about online.

Classys had achieved something rare in medical devices: genuine consumer brand recognition. In an industry where products are typically purchased by physicians and unknown to patients, Classys had built a brand that patients asked for by name. This flipped the typical power dynamic. Clinics could not simply switch to a cheaper alternative because their patients expected Shurink. The brand had become both a competitive moat and a source of pricing power.

The financial performance reflected this success. By fiscal year 2024, revenue had reached approximately 243 billion Korean won, nearly 180 million dollars, with year-over-year growth of thirty-five percent. Net profit margins exceeded forty percent, a figure almost unheard of in medical device manufacturing. The gross profit margin of nearly seventy-nine percent reflected the power of the consumables-heavy business model. These were not the financials of a typical hardware company. They were closer to what one might expect from a luxury brand or a software business.

Earnings per share grew at a compound annual rate exceeding twenty-five percent from 2020 to 2024, climbing from approximately 590 won to over 1,500 won. The stock price appreciated accordingly, rewarding early investors who recognized the business model's power before the market fully understood it. By late 2024, trailing twelve-month revenue had grown to over 318 billion won as international expansion accelerated.

But to truly unlock global potential, the company would need more than innovative products and a strong domestic brand. It would need capital for international expansion, professional management experienced in multinational operations, and a strategic playbook for cracking markets far more challenging than Gangnam. Enter Bain Capital.

IV. The Bain Capital Buyout: The Game Changer (2022)

The transaction that would reshape Classys's future closed in early 2022. Bain Capital, the Boston-based private equity giant with nearly 175 billion dollars in assets under management, acquired a 60.84% controlling stake in Classys for approximately 670 billion Korean won, roughly 560 million US dollars at prevailing exchange rates.

To understand the significance of this deal, consider Bain Capital's history and approach. Founded in 1984 by partners from Bain & Company, the consulting firm, Bain Capital pioneered the modern private equity playbook: acquire controlling stakes in companies with strong fundamentals but unrealized potential, install professional management, accelerate growth through operational improvements and strategic acquisitions, and exit at a premium valuation. The firm had backed some of the most successful private equity investments in history, including Staples, Dunkin' Brands, and Canada Goose. It had also been involved in more controversial transactions that became talking points in American political debates. Love it or hate it, Bain represented the pinnacle of private equity sophistication.

The price Bain paid deserves scrutiny. At 17,000 Korean won per share, Bain was paying slightly above the market price of approximately 15,950 won at closing. But this was significantly below the all-time high of 27,200 won reached just months earlier in August 2021. The Korean stock market had corrected during late 2021 as global risk appetite declined, and Classys shares had fallen with the broader market despite strong operating performance. Bain was arguably buying at a cyclical discount.

On the other hand, Bain was paying a substantial absolute price for a Korean medical device company, particularly one that generated most of its revenue domestically at the time. International sales represented only about forty percent of revenue. The company had minimal presence in the United States, the world's largest aesthetic medicine market. China remained largely unaddressed due to regulatory requirements. Bain was paying platform valuation for a company that had yet to prove it could scale internationally.

The sellers were Jung Sung-jae himself, his wife Lee Yeon-joo, and their two children. The family would retain a minority stake, but control would pass to the American private equity firm. For Jung, who had built Classys from scratch over fifteen years while simultaneously running a dermatology practice, this represented both validation and transition. He had created something valuable enough to attract one of the world's premier investors. At approximately 560 million dollars for the controlling stake, the implied enterprise value suggested Jung's creation was worth approaching a billion dollars. Now he would step back and let others take the company to the next level.

The personal dynamics of founder exits are rarely discussed in financial analysis but matter enormously. Jung was fifty-five years old at the time of the sale. He had already achieved financial independence through Dr. Jart+ and other investments. He did not need to keep running Classys. But watching someone else reshape your creation is psychologically difficult for many founders. Some stay involved through advisory roles or board seats. Others cut ties completely. Jung chose something in between, maintaining a minority friendly shareholder position while ceding operational control.

Why was Bain interested in the first place? The thesis, as communicated through various reports and interviews, was ambitious. Bain was not buying a Korean device maker. It was buying a global platform. The firm saw Classys as a potential consolidator of the fragmented aesthetics device industry, analogous to how LVMH rolled up luxury brands from Louis Vuitton to Sephora to Tiffany, or how Danaher consolidated life sciences and diagnostics companies through relentless acquisition and operational improvement.

Several factors made this thesis credible. First, the razor-and-blade model provided predictable, high-margin recurring revenue that could support leverage and finance acquisitions. Banks love lending against subscription-like revenue streams. The visibility of cartridge revenue allowed Bain to model returns with more confidence than would be possible for a pure device company with lumpy one-time sales.

Second, the brand strength in Korea demonstrated that Classys could build consumer recognition in ways that pure clinical device companies could not. The Shurink phenomenon proved that medical device marketing could transcend physician channels and reach patients directly. This suggested potential for similar brand-building in other markets where K-beauty influence was growing.

Third, the company had barely scratched the surface of international markets, with massive geographic white space remaining. At the time of acquisition, exports represented only about forty percent of revenue. The United States, the world's largest aesthetic medicine market, was essentially untapped. China, with its enormous population and rising middle class, represented an even larger opportunity if regulatory barriers could be overcome.

Fourth, the broader K-beauty phenomenon provided cultural tailwinds that competitors from other countries could not easily replicate. Korean aesthetic expertise had become aspirational worldwide. K-Pop stars and Korean actresses were global style icons whose flawless skin became a marketing asset for Korean beauty brands. This cultural premium represented a form of country-of-origin advantage that American or European competitors simply could not claim.

Notably, this was Bain Capital's third acquisition of a Korean beauty company, suggesting a considered strategy rather than an opportunistic single bet. The firm had developed conviction that Korean companies possessed unique advantages in aesthetics and beauty, advantages rooted in domestic consumer sophistication, intense competition that drove innovation, and cultural exports that created global demand. This was not Bain buying a random medical device company. This was Bain executing a regional thesis.

The Korea-as-platform concept extended beyond aesthetics. Korean companies in gaming, entertainment, food, and consumer electronics had demonstrated the ability to build global franchises leveraging domestic innovation and cultural influence. BTS became the world's biggest band. Parasite won the Academy Award for Best Picture. Korean fried chicken chains expanded globally. The pattern was clear: Korean companies that achieved domestic dominance in culturally-sensitive categories could leverage that success internationally in ways that companies from other countries struggled to replicate.

The market initially struggled to process the transaction. Some viewed the founder exit as concerning, wondering whether Jung's departure would sap the company's innovative spirit. Medical device companies often depend on founder-physicians who understand clinical needs viscerally. Could a professional management team maintain that connection? Others questioned whether a private equity firm, typically focused on three to seven year holding periods, was the right steward for a business that required sustained R&D investment and long-term brand building. Still others simply did not understand why Bain would pay such a premium for what appeared to be a niche player in a competitive industry.

But Bain had a playbook, one that would become clearer as the months unfolded. Step one was installing professional management with international experience, executives who knew how to build global sales organizations and navigate complex regulatory environments. Step two was accelerating geographic expansion, particularly in the lucrative but challenging US and Chinese markets where the real growth opportunity lay. Step three was deploying capital for strategic acquisitions that would fill product gaps and capture distribution, transforming Classys from a single-product company into a diversified platform.

The playbook was textbook private equity, but executed with unusual ambition for a company of this size. Most PE acquisitions in this range would focus on cost-cutting and financial engineering. Bain's approach emphasized top-line growth and strategic expansion, suggesting confidence that the underlying business could support significant scale-up.

Within the first year of Bain's ownership, the results were becoming visible. International revenue, which had represented around forty percent of the total, began climbing rapidly toward seventy percent. The company established stronger presences in Brazil, Australia, Thailand, and Taiwan. And the M&A engine, dormant during the founder era when Jung focused on organic innovation, roared to life.

For Jung Sung-jae, the sale proved financially rewarding beyond the initial proceeds. By 2024, he appeared on Forbes' list of the fifty richest Koreans, ranked at number forty-three with a net worth of approximately 760 million dollars. His minority stake in Classys, which had appreciated significantly under Bain's ownership, combined with his earlier success with Dr. Jart+ and other investments, had made him one of the wealthiest entrepreneurs to emerge from the K-beauty wave. But his creation was now in different hands, being reshaped for purposes he could not fully control.

The transition from founder to financial sponsor ownership represents one of the most significant inflection points in any company's history. Some companies thrive under PE ownership, gaining access to capital and expertise that founders cannot provide. Others falter, as the focus on exit timelines and financial engineering undermines the patient culture-building that created value in the first place. Classys's future would depend heavily on which path it followed.

V. The New Guard: Management & Incentives

When Bain Capital takes control of a company, the first order of business is typically management. Private equity firms succeed or fail based on their ability to install operators who can execute aggressive growth plans while maintaining operational discipline. Finding the right CEO is arguably the most important decision a PE owner makes. In Classys's case, that meant finding someone who understood both healthcare and international expansion, someone who could transform a founder-led Korean SME into a polished global enterprise capable of competing against multinational giants.

They found Seung-Han Baek.

Baek's background was strikingly different from Jung Sung-jae's. Where Jung was a dermatologist who stumbled into entrepreneurship through clinical observation and patient interaction, Baek was a career healthcare executive groomed in multinational corporations. He had earned his undergraduate degree from the College of Health Sciences at Yonsei University, one of Korea's most prestigious institutions known for producing healthcare industry leaders. He then added an MBA from the Helsinki School of Economics in Finland, a choice that signaled international ambitions and comfort operating across cultures. This dual Korean-European educational pedigree was precisely what a company seeking global expansion needed.

His career trajectory reinforced this impression of systematic preparation for global leadership. Baek had worked at Bayer Korea, the German pharmaceutical giant known for rigorous operations and global coordination. He had joined Abbott Korea, the American healthcare conglomerate with diverse businesses spanning pharmaceuticals, diagnostics, nutrition, and medical devices. He had run a healthcare business division at SK Telecom, giving him exposure to the intersection of technology and medicine, the convergence of digital health and traditional care that was reshaping the industry.

The diversity of Baek's background represented both strength and risk. On one hand, he brought exposure to multiple management styles and business models. On the other hand, he lacked the deep industry specialization that might come from spending an entire career in aesthetic medicine. This generalist-versus-specialist tradeoff is common in PE-backed companies where owners prioritize management capability over domain expertise.

Most relevantly, Baek had served as CEO of Beckman Coulter Korea and as a board director of Danaher Korea. The Danaher connection was particularly telling. Danaher Corporation is famous in industrial circles for the "Danaher Business System," a management philosophy borrowed from Toyota's lean manufacturing principles and applied ruthlessly across acquired companies. DBS, as insiders call it, emphasizes continuous improvement, standardized processes, problem-solving methodologies, and relentless measurement. Danaher has built an empire worth over 200 billion dollars by acquiring promising industrial and life sciences businesses, then applying DBS to extract margin expansion and growth acceleration that previous owners could not achieve.

Anyone who had served on Danaher Korea's board had witnessed this playbook firsthand. They had seen how professional management could transform acquired companies. They had learned the vocabulary and frameworks that Danaher deployed globally. When Bain hired Baek, they were hiring someone who already spoke the language of operational excellence that private equity prizes.

Baek also brought credibility within Korea's medical device industry, having served as Chairman of the In Vitro Diagnostics Committee at the Korea Medical Devices Industry Association. This meant he understood the regulatory environment intimately, had relationships with key government officials who controlled approvals and market access, and could navigate the sometimes Byzantine certification processes that foreign companies found so frustrating. These relationships would prove valuable as Classys sought to expand while maintaining its regulatory standing at home.

The mandate Bain gave Baek was clear, ambitious, and non-negotiable. First, professionalize the supply chain. A company transitioning from founder-led to professionally managed needed standardized processes, documented procedures, and scalable systems. The informal ways of working that sufficed when Jung could personally oversee operations would not scale to a global organization. Second, crack the US and Chinese markets. Korea and Southeast Asia had been proven; now it was time to tackle the world's two largest economies, markets that represented the majority of global aesthetic medicine spending but where Classys had minimal presence. Third, deploy capital through strategic acquisitions that would expand the product portfolio and capture distribution channels.

The incentive structure supporting this mandate followed typical private equity conventions, though specific terms were not publicly disclosed. Management teams in Bain portfolio companies typically receive significant equity stakes tied to exit multiples. The mechanics work roughly like this: if Bain entered at 670 billion won and exited at two trillion won, management would share in the value creation through carried interest, direct equity participation, and performance bonuses tied to achieving milestones. The more value created, the more management earned. This aligned Baek's personal financial interests directly with delivering the kind of aggressive growth and margin improvement that private equity demands.

The contrast with the founder era was stark, reflecting fundamentally different organizational cultures. Under Jung, Classys had operated with a family business mentality. Decisions were made based on long-term vision rather than quarterly performance metrics. Dividends flowed to the founder family as a form of ongoing compensation for entrepreneurial risk. R&D received investment even when short-term returns were uncertain, because Jung believed in building capabilities for the future. The culture was Korean to its core: hierarchical, relationship-driven, focused on domestic market excellence, and patient about international expansion.

Under Baek, the culture began shifting toward what one might call "global PE standard." English became more common in internal communications, necessary for coordinating with international offices and reporting to Bain. Presentations to the board emphasized international revenue percentages and acquisition pipelines rather than product development stories. The organizational structure flattened to enable faster decision-making, removing hierarchical bottlenecks that slowed execution. Performance metrics became more quantitative, tied to specific targets with clear accountability for individual executives.

This cultural transformation was necessary but not without friction. Some long-tenured employees, veterans of the scrappy startup days, struggled with the new pace and expectations. They had joined Classys because of Jung's vision and leadership style. The R&D function, so central to Classys's original innovation story, had to adapt to a more structured product development process with stage gates and portfolio reviews. The company was becoming more professional but perhaps less entrepreneurial, more disciplined but potentially less creative.

For investors, the management transition raised a fundamental question about sustainability. Could operating margins exceeding fifty percent survive the transition from founder efficiency to professional management overhead? Jung had run a lean operation with minimal bureaucracy. Professional management brought capabilities but also costs: executive compensation, expanded administrative functions, consultant engagements, compliance infrastructure. Would these investments pay for themselves through accelerated growth, or would they simply compress the exceptional margins that made Classys attractive?

Could the innovation culture that produced Shurink and Ultraformer MPT continue under a Danaher-trained executive focused on operational discipline and process standardization? Some companies lose their innovative edge when founders depart. Others discover that professional management can actually accelerate innovation by providing resources and removing bottlenecks. Time would tell which path Classys would follow.

Baek's early moves suggested he understood the balance required. He invested in international sales infrastructure without gutting domestic operations. He pursued acquisitions that built capabilities rather than simply adding revenue. He maintained R&D investment levels while imposing more structured product development processes. Whether this balance would prove sustainable across a full private equity holding period remained to be seen.

The organizational changes under Baek extended beyond strategy to daily operations. Reporting structures were redesigned to provide clearer accountability. Planning cycles were formalized with quarterly business reviews and annual strategic planning sessions. Key performance indicators were defined and tracked systematically. The informal, relationship-based management style that characterizes many Korean family businesses gave way to process-driven professional management.

These changes were necessary but not without cost. Some institutional knowledge resided in long-tenured employees who found the new environment uncomfortable. Relationships with distributors and customers that had been personally managed by founders now needed to be systematized into customer relationship management systems and formal contracts. The transition period created friction that inevitably distracted from day-to-day execution.

For investors evaluating management quality, the Baek appointment represented a deliberate choice. Bain could have chosen a more aggressive growth executive focused purely on top-line expansion. Instead, they selected someone with operational experience who could build sustainable infrastructure. This suggested a long-term perspective rather than a quick-flip mentality, consistent with Bain's broader strategy for Classys.

VI. Capital Deployment: The M&A Spree (2023-2025)

Private equity firms do not acquire companies simply to operate them better. They acquire companies to transform them, typically through a combination of operational improvement, financial engineering, and strategic acquisitions. By 2023, Classys had checked the first box with the management transition and operational professionalization. Now Bain turned to the M&A playbook, deploying capital to reshape Classys's competitive position.

The logic was straightforward, rooted in basic competitive dynamics. Classys dominated the HIFU category in Korea and had established footholds in several international markets. But aesthetic dermatology encompasses many technologies beyond HIFU: radiofrequency for skin tightening, lasers for resurfacing and hair removal, microneedling for collagen stimulation, light-based devices for pigmentation and acne, and various combinations of these modalities. A typical dermatologist's office needs devices across multiple categories. If Classys only sold HIFU machines, it captured only a portion of each clinic's capital budget and mindshare.

Consider the economics from a clinic's perspective. A busy aesthetic dermatology practice might spend one to two million dollars on devices over its lifetime. If Classys only offers HIFU, it might capture fifty thousand dollars of that spending. But if Classys offers HIFU, RF, lasers, and microneedling, it could capture several hundred thousand dollars from the same customer. The lifetime value of each customer relationship multiplies with the breadth of the product portfolio.

The solution was to "fill the bag," industry jargon for expanding a product portfolio to serve more customer needs. Acquire companies with complementary technologies, then cross-sell the combined portfolio to the same customer base. A Classys sales representative who previously walked into a clinic with one product could now present three or four. The clinic's capital allocation decisions became simpler: they could standardize on a single vendor relationship. The switching costs increased as clinics invested in training across multiple product lines. The relationship deepened beyond a transactional purchase into a strategic partnership.

The first major acquisition target was Ilooda, a Korean competitor specializing in microneedle radiofrequency and laser technologies. Ilooda had carved out its own niche with the "Secret" series, devices that combined radiofrequency energy with microneedling to stimulate collagen production through a different mechanism than HIFU. The company had built particular strength in the United States and Europe, markets where Classys remained relatively weak.

In September 2023, Classys acquired an initial eighteen percent stake from Ilooda's largest shareholder, Kim Yong-han, for 40.5 billion won. This stake provided a toehold, board observation rights, and time to assess the full integration opportunity through due diligence that went beyond what an external buyer could conduct.

By June 2024, Classys was ready to move. The company announced its intention to acquire the remaining 82.4% of Ilooda for 130 billion won, bringing total consideration for the company to approximately 170 billion won. The merger would be effected through a share exchange at a ratio of 0.14 Classys shares for each Ilooda share, reflecting relative valuations and allowing Ilooda shareholders to participate in the combined company's future. Shareholders approved the deal in August, and the transaction closed on October 2, 2024.

The share exchange structure was notable because it aligned Ilooda shareholders with the long-term success of the combined entity. Rather than taking cash and exiting, former Ilooda owners became Classys shareholders with incentives to support successful integration. This alignment can smooth the organizational challenges that often plague acquisitions where seller and buyer have divergent interests post-close.

The strategic rationale was compelling. Ilooda's flagship Secret series, a radiofrequency microneedling device that had sold over five thousand units globally, addressed skin texture and scarring concerns that HIFU did not target. While Classys had dominated in Korea and Asia, Ilooda had built stronger distribution networks and physician relationships in the United States and Europe. The combined company could now offer HIFU through Shurink, monopolar RF through Volnewmer, and RF microneedling through Secret, while leveraging complementary geographic footprints to accelerate growth in underserved markets.

Some analysts questioned the valuation. At the time of the deal, the broader aesthetics device sector was trading at depressed multiples following a pullback from 2021 highs. InMode, the Israeli competitor that had been the sector darling commanding valuations exceeding twenty-six times EBITDA at its peak, had seen its multiple compress to single digits amid concerns about GLP-1 competition and market saturation. Yet the Ilooda deal appeared to value the company closer to peak 2021 multiples. Was Classys overpaying?

The answer depends on perspective. From a strict comparable company analysis using current trading multiples, the price appeared aggressive. But strategic acquisitions should not be valued solely on comparable company analysis. The question is different: how much would it cost Classys to develop its own RF microneedling platform from scratch, build its own US distribution network, hire and train sales representatives, develop relationships with key opinion leaders, and earn physician trust in a category where it had no track record? That organic path would take five years or more and likely cost well over 170 billion won when accounting for time value, execution risk, and competitive erosion during the development period. Viewed through this build-versus-buy lens, the premium looked more justified.

The second major acquisition came in October 2025, when Classys announced the purchase of a 77.5% stake in JL Health Participacoes S.A. for 18.27 billion won, approximately thirteen million dollars. JL Health might seem small relative to the Ilooda deal, but its strategic significance was substantial.

JL Health owned Medsystems, described as the largest distributor of aesthetic medical devices in Brazil, serving over fifteen thousand hospitals and aesthetic clinics across the country. Brazil matters enormously for the aesthetics industry. With the world's fourth-largest market for aesthetic devices, valued at approximately 800 million dollars annually, Brazil represents a major growth opportunity. Brazilians have long embraced cosmetic enhancement, both surgical and non-surgical. The country's middle class has expanded, creating demand for accessible aesthetic procedures. And crucially, Brazil was already Classys's second-largest market, contributing significantly to the company's international revenue growth.

This acquisition represented a fundamental shift in go-to-market strategy. Previously, Classys had sold through independent distributors in most international markets. The distributors purchased equipment at wholesale prices, handled local marketing and sales, managed customer relationships, and provided service and support. This model allowed rapid geographic expansion without building local infrastructure, but it came with significant drawbacks. Distributors captured a portion of the margin, often twenty to thirty percent of the final customer price. They controlled the customer relationship, limiting Classys's visibility into market dynamics and customer needs. They could potentially switch to competing products if terms became unfavorable.

By acquiring its Brazilian distributor, Classys was "going vertical," capturing the full margin stack from manufacturing through end-customer sale. This provides several advantages beyond the obvious margin improvement. Better market intelligence flows from direct customer contact. Faster feedback loops enable more responsive product development. Direct relationships create opportunities to cross-sell the expanded product portfolio. And eliminating intermediary margin leakage improves unit economics.

The Brazil vertical integration playbook could be replicated in other markets. If successful, expect Classys to acquire distributors in Japan, Thailand, Taiwan, and eventually larger markets like China and the United States. Each acquisition would deepen the company's competitive moat while improving unit economics. The risk, of course, is execution complexity. Operating direct distribution in multiple countries requires local talent, regulatory expertise, logistics infrastructure, and management attention that an export-focused manufacturer may lack.

Together, the Ilooda merger and JL Health acquisition signaled that Bain's strategy was unfolding according to plan. Classys was transforming from a single-product company into a platform, and from an exporter dependent on partners into an integrated global organization. Whether this transformation would ultimately create or destroy value remained to be seen.

The total capital deployed across these acquisitions exceeded 200 billion won, a significant commitment that reflected Bain's conviction in the platform thesis. The integration challenges were real but manageable. Both acquired entities operated in adjacent markets with complementary rather than overlapping customer bases. The synergy math, while aggressive, was not unreasonable. If executed well, the combined company would emerge as a far more formidable competitor than any of its individual components.

The acquisitive strategy also sent a signal to the market about Bain's intentions. This was not a PE firm seeking quick financial engineering and a rapid exit. This was a firm building a platform for long-term value creation, willing to reinvest profits into transformative acquisitions rather than extracting dividends. Whether the public markets would reward this patience remained to be seen, but the strategic direction was unmistakably clear.

VII. The "Hidden" Growth Engines

Beyond the headline-grabbing M&A activity, several growth initiatives deserve attention from investors seeking to understand Classys's trajectory over the coming years. These are the options embedded in the business that do not yet contribute meaningfully to financial results but could drive substantial value if executed successfully.

The first is Volnewmer, known in the US market under the brand name EVERESSE. This is Classys's answer to Thermage, the radiofrequency skin tightening device developed by Solta Medical. Thermage pioneered the category and dominated it for years, becoming a brand name that patients requested by name, similar to what Shurink achieved in HIFU. Solta claimed over five million procedures performed globally and one thousand cumulative devices installed in Korea alone by early 2025.

But like Ultherapy in HIFU, Thermage carries significant baggage. The treatments are painful, requiring comfort protocols that slow procedures and reduce clinic throughput. The consumables are expensive, with treatment tips costing several hundred dollars each and limiting accessibility for price-sensitive patients. The device itself commands premium pricing that many clinics cannot justify. Thermage represented the best of late 1990s and early 2000s technology, but it had not kept pace with more recent innovations in energy delivery and patient comfort.

Volnewmer applies the same "Shurink strategy" to radiofrequency that proved so successful in HIFU. Using 6.78 MHz monopolar RF technology, it delivers skin toning and tightening with what Classys claims is superior patient comfort and procedural speed. The energy delivery system is optimized for the modern Korean market's preferences: faster treatments, less discomfort, more accessible pricing, and comparable clinical outcomes. If Classys can replicate its Korean market dominance in RF the way it did in HIFU, the revenue implications would be substantial. The global RF skin tightening market represents billions in annual spending.

The US market entry is particularly notable. In late 2024, Classys announced a partnership with Cartessa Aesthetics, an established US distributor of aesthetic devices with existing relationships with dermatologists and plastic surgeons across the country. Cartessa would serve as the exclusive US distributor for EVERESSE, leveraging its sales force and market access while Classys focused on product excellence. The partnership launched publicly at a Cartessa user meeting in Florida in September 2024. Importantly, all Cartessa products carry FDA clearance, meaning EVERESSE has cleared the regulatory hurdle that blocks many foreign devices from the American market.

The partnership model reflects pragmatic recognition of market realities. The US aesthetic device market is notoriously difficult for foreign entrants. Physicians are skeptical of unfamiliar brands. Regulatory requirements are onerous. Reimbursement dynamics differ from Asian markets where most treatments are cash-pay. Distribution is fragmented with thousands of independent dermatology practices, med spas, and plastic surgery offices. Competing against entrenched incumbents with established relationships and extensive service networks requires boots on the ground that take years to build.

The Cartessa partnership represents a middle ground between direct market entry and pure export through distributors. Cartessa handles customer relationships, sales, and service, while Classys provides the product and captures wholesale margins. If the partnership succeeds, Classys gains market intelligence and brand recognition that could eventually support more direct involvement. If it fails, the company has limited its downside by avoiding large fixed investments in US infrastructure.

The US market opportunity, while challenging, is substantial. American consumers spend more per capita on aesthetic procedures than any other population. The market for non-invasive facial rejuvenation alone represents billions in annual spending. Even modest market share gains could meaningfully contribute to Classys's revenue and profit growth.

The second hidden growth engine is home-use devices, marketed under the Skederm brand. The professional aesthetic device market is enormous, but it captures only patients willing to visit clinics, schedule appointments, and pay for professional treatments. A vast population of consumers wants skin improvement but will not take these steps. They prefer at-home solutions that fit their routines, devices they can use while watching television or before bed.

Skederm represents Classys's attempt to capture this adjacent market. The brand sells high-frequency and radiofrequency devices designed for consumer use, along with complementary cosmetics and skincare products. These are not medical devices requiring physician supervision but consumer electronics positioned as beauty tools. While current contribution to revenue is modest, the strategic optionality is significant.

The home device market is both an opportunity and a minefield. On one hand, it represents a massive addressable market of consumers who want professional-quality results without clinic visits. On the other hand, consumer electronics face different competitive dynamics than medical devices. Brand matters enormously. Marketing budgets must be substantial. Distribution through retail channels requires capabilities that a B2B company may lack. And the regulatory environment for consumer devices, while less onerous than medical devices, still requires careful navigation.

If Classys can establish credibility in the home device market, it creates multiple value drivers. First, a pipeline of consumers who experience efficacy from home devices may eventually "graduate" to in-clinic treatments, seeking more powerful professional versions of what they use at home. Second, recurring revenue streams from device replenishment and cosmetic repurchase could provide predictable baseline income. Third, consumer brand building creates opportunities for category expansion beyond devices into skincare, supplements, and other beauty products. The K-beauty playbook that Jung originally executed with Dr. Jart+ could potentially be replicated under Classys ownership.

The third growth engine is geographic expansion, particularly in China. The Chinese aesthetic medicine market is massive and growing rapidly, driven by rising disposable incomes, social media influence that promotes appearance consciousness, and cultural acceptance of cosmetic procedures that has expanded dramatically among younger generations. Chinese consumers represent a significant portion of medical tourism to Korean clinics, suggesting existing demand for Korean aesthetic expertise.

However, market entry requires NMPA approval, China's equivalent of FDA clearance, which can take years and requires significant investment in local clinical trials, regulatory relationships, and distribution infrastructure. The regulatory environment has also become increasingly complex as Chinese authorities seek to promote domestic manufacturers and maintain control over foreign healthcare companies.

Classys has been preparing for China entry for several years. While specific NMPA approval status has not been publicly confirmed, the company's international revenue trajectory suggests significant progress. If and when China opens fully, it would represent a step-change in Classys's addressable market, potentially doubling or tripling the available opportunity. The combination of device sales to Chinese clinics and continuing medical tourism to Korean facilities by Chinese patients could create a virtuous cycle of brand building and revenue growth.

The China opportunity comes with significant risks beyond regulatory approval. Geopolitical tensions between South Korea and China have periodically disrupted business relationships in sensitive sectors. Local competition from Chinese device manufacturers is intensifying. Intellectual property protection remains challenging. And the regulatory environment can shift unpredictably based on government policy priorities. These risks must be weighed against the substantial opportunity that the Chinese market represents.

Medical tourism from China to Korea for aesthetic procedures has created a foundation of brand awareness that could accelerate market entry if regulatory barriers fall. Chinese patients who received Shurink treatments in Gangnam return home familiar with the brand and potentially willing to seek it out domestically. This existing demand could jumpstart sales once devices become available through local channels.

Each of these growth engines carries execution risk. Volnewmer must prove it can replicate Shurink's success in a different technology category where competitive dynamics and customer preferences differ. Skederm must compete against established consumer beauty brands with massive marketing budgets and shelf-space advantages in retail channels. China entry depends on regulatory approvals that remain uncertain and government policies that can shift unpredictably. But collectively, these initiatives suggest a company that has not exhausted its growth options, even as core markets mature.

The optionality embedded in these growth engines is significant from an investor perspective. Even if only one or two succeed, the impact on company value could be substantial. Volnewmer alone, if it achieves even a fraction of Shurink's success in RF, could add meaningful revenue streams. China, if it opens, could double the addressable market. The home device business, if it gains traction, could provide a recurring consumer revenue stream that diversifies away from dependence on clinic purchases.

This portfolio of options distinguishes Classys from many competitors who remain dependent on single product lines or single geographies. It also helps explain the premium valuation that the market has assigned to Classys shares despite the competitive pressures in the core HIFU business.

VIII. Analysis: Powers & Forces

For investors trying to assess Classys's long-term competitive position, frameworks developed by Hamilton Helmer and Michael Porter provide useful analytical scaffolding. These are not just academic exercises. They help identify where sustainable competitive advantage actually resides and where competitive pressure may erode returns.

Helmer's "7 Powers" framework identifies sources of sustainable competitive advantage that allow companies to earn excess returns over extended periods. Three powers appear particularly relevant to Classys.

Switching costs represent perhaps the company's strongest moat. Once a dermatologist purchases a fifty thousand dollar Classys device, trains staff on its operation, develops treatment protocols optimized for its capabilities, and begins marketing Shurink treatments to patients, the cost of switching to a competitor becomes prohibitive. The doctor would need to write off the capital investment or sell the used equipment at a loss. Staff would require retraining on new devices with different interfaces and treatment parameters. Marketing materials would need updating. And most critically, the clinic would need to explain to loyal patients why they should try something different when they have been satisfied with Shurink results.

These switching costs lock in customers for the five to seven year useful life of the equipment and ensure ongoing cartridge purchases throughout that period. As the installed base grows, so does the annuity stream of consumable revenue. This is not a power that competitors can easily overcome. A new entrant offering a marginally better or cheaper HIFU device must provide enough improvement to justify the switching costs, a high bar when the existing product works well.

Brand power is substantial in Korea but less established globally. In Korea, "Shurink" has achieved the holy grail of brand recognition: becoming a generic term for the entire category. Patients ask for Shurink by name, forcing clinics to stock Classys equipment regardless of what competitors might offer at lower prices. When patients specify the brand, physicians lose negotiating leverage with suppliers. This brand power is beginning to extend into international markets through medical tourism and social media influence, as patients who visited Korean clinics share their experiences globally. But brand building takes time. In Western markets where most consumers have never heard of Classys, the company must compete on other dimensions.

Scale economies exist but are moderate. Classys benefits from distribution leverage in Korea and Brazil, where established sales forces and service networks create efficiencies that new entrants cannot easily match. The company also benefits from manufacturing scale that allows competitive pricing on devices and attractive margins on consumables. However, the aesthetics device industry does not exhibit the extreme scale effects seen in semiconductors, where marginal costs approach zero and market leaders can price competitors out of existence. A well-funded competitor with reasonable scale can compete effectively on manufacturing costs.

Process power, another of Helmer's seven powers, may be developing. The company's experience in managing the transition from device sale to consumables revenue, its expertise in training physicians across multiple geographies, and its ability to navigate regulatory approvals in diverse markets represent accumulated knowledge that competitors cannot easily replicate. This institutional capability takes years to develop and represents a subtle but meaningful advantage.

Network effects, by contrast, are largely absent. Unlike platforms where each additional user increases value for all users, aesthetic devices do not become more valuable as more clinics adopt them. There is no network benefit to being the hundredth clinic to purchase Shurink rather than the first. This absence of network effects limits the "winner-take-all" dynamics that characterize some technology businesses and suggests that multiple competitors can coexist profitably.

Porter's Five Forces analysis reveals a mixed competitive picture, highlighting where Classys is strong and where vulnerabilities exist.

The threat of new entrants is genuinely high. HIFU technology is not proprietary to Classys. The underlying physics of focused ultrasound for tissue ablation has been understood for decades and is covered by expired patents. Dozens of competitors, particularly in Korea and China, manufacture similar devices. Companies like Jeisys Medical, Ultracel, and Liftera compete directly in the HIFU category with products that achieve similar clinical outcomes at similar price points. What prevents commoditization is not technology but rather brand and distribution. A Chinese startup can build a HIFU device that works as well as Ultraformer, but it cannot overnight create the "Shurink" brand recognition or the distribution relationships and installed base that Classys has cultivated over fifteen years.

Supplier power is low. Classys sources standard electronic and mechanical components, ultrasound transducers, displays, housings, and other parts that are available from multiple vendors in competitive markets. No single supplier has leverage to extract excessive margins or constrain production. This is a business-friendly position that allows Classys to maintain its own margins without passing concessions to component suppliers.

Buyer power is moderate and worth watching. Individual clinics have limited negotiating leverage against Classys. A single dermatology practice purchasing one device cannot demand significant discounts. But large clinic networks, hospital systems, and major distributors can demand volume discounts that compress margins. As Classys increasingly sells through fewer, larger distribution partners, buyer power may increase. The Brazil acquisition, by cutting out a distributor, actually reduced this risk in that market.

The evolution of the customer base matters for assessing buyer power trends. If the industry consolidates toward larger clinic chains and fewer independent practitioners, buyer power will increase. Conversely, if the market remains fragmented with many small buyers, Classys retains pricing leverage. Monitoring the concentration of the customer base provides forward-looking insight into margin sustainability.

Threat of substitutes is the wild card that generates the most investor debate. The most discussed substitute threat comes from GLP-1 weight loss drugs like Ozempic, Wegovy, and their successors. These medications, originally developed for diabetes management, have proven remarkably effective at reducing body fat with minimal effort from patients. Some market observers speculate that pharmaceutical fat loss could reduce demand for body contouring devices, lipsuction alternatives, and fat-reduction technologies.