Pentamaster: The Architects of the Silicon Shift

I. Introduction: The "Invisible" Giant of Penang

Drive north along Malaysia's coastal expressway, cross the Penang Bridge as the South China Sea glints below, and you arrive in Bayan Lepas—a stretch of humid, low-rise industrial parks that looks, at first glance, unremarkable. A few warehouses. A few fences. A lot of palm trees. And then, tucked between them, the kind of buildings that don't advertise what happens inside: sheds stamped with logos of Intel, AMD, Broadcom, Bosch, Osram, Lumentum, ams. This is the so-called "Silicon Valley of the East," and it has been quietly stitching together the guts of the global electronics industry for more than fifty years.

Inside one of those buildings, behind a modest reception desk, sits a company whose name almost no retail investor outside Southeast Asia could recognize. Pentamaster International Limited—ticker 1665 on the Hong Kong Stock Exchange—is not a chipmaker. It does not design processors or fabricate wafers. It builds the machines that test the chips, the robots that assemble the modules, and the automated cells that bolt those modules into everything from electric vehicle inverters to insulin pens.

And yet, if you pull the covers off the modern EV drivetrain, or peer inside a cataract surgery device, or trace the supply chain of a smartphone's 3D-sensing module, there is a reasonable probability that a Pentamaster system touched that component on its way to you. The company operates in the most unglamorous slice of the semiconductor value chain—back-end test and factory automation—but that slice is precisely where the industry's new center of gravity is migrating as cars become computers and medical devices become consumables.

The thesis for this episode is simple but, as always at Acquired, worth interrogating carefully: Pentamaster is not really a "picks and shovels" business in the generic sense. It is something more specific and more durable. It is a custom-tool maker, an embedded co-engineering partner, for the industries going through the hardest transitions of this decade: internal combustion to electric, silicon to silicon carbide, manual medical assembly to fully automated single-use device lines. The business model is therefore less about cyclical semiconductor capex and more about being permanently bolted into the production roadmaps of the world's most demanding OEMs.

That thesis only works if two things are true. First, that the switching costs are as catastrophic as the company's retention rates suggest. Second, that a family-controlled Penang engineering house can keep out-innovating the Teradynes and Advantests of the world in the niches that matter. The story of how a firm founded in 1991 by a former MNC engineer came to sit in the cockpit of the EV and MedTech revolutions is what this episode is about. And like all good Acquired stories, it starts not in a boardroom but in a free trade zone.

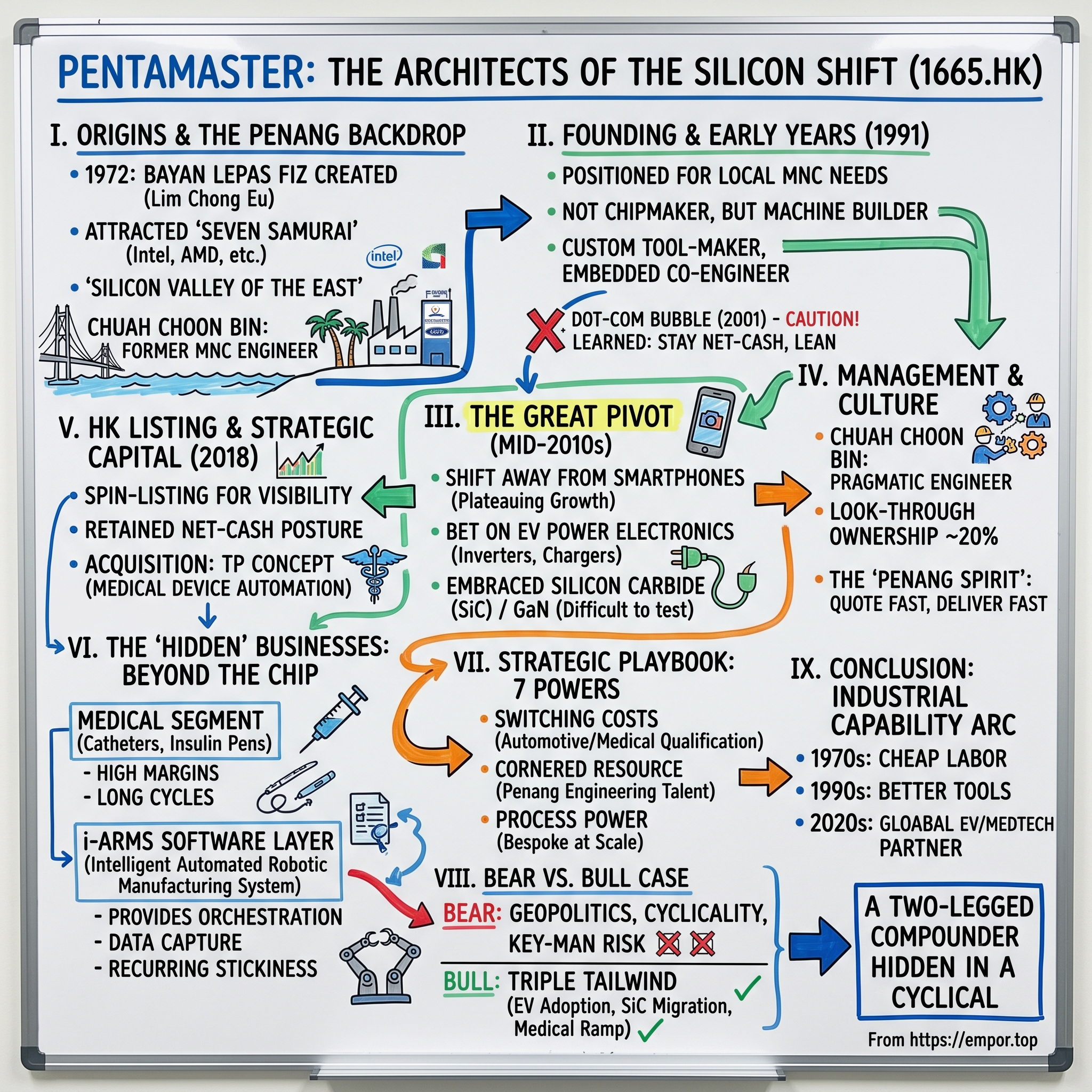

II. Origins & The Penang Backdrop

To understand Pentamaster, you have to understand Penang. And to understand Penang, you have to rewind to 1972, a year most Western histories of semiconductors skip. The American industry was just getting on its feet—Intel was three years old, AMD two, National Semiconductor still the dominant force—and every one of those companies was running into the same wall: labor. Assembling and testing chips was brutally manual work, and California wages were strangling the economics. Penang's Chief Minister at the time, Lim Chong Eu, saw the opening. He created the Bayan Lepas Free Industrial Zone, waived duties, built roads and power, and sold the island to the Americans as a place where skilled, English-speaking technicians could be hired at a fraction of Silicon Valley costs.

They came. Intel arrived in 1972, followed in quick succession by AMD, National Semiconductor, Hewlett-Packard, Hitachi, Bosch, Osram, and Clarion. Locals still call them the "Seven Samurai," and over the next two decades they built up an ecosystem that looked nothing like the cliché of low-cost Asian assembly. Penang's technicians didn't stay technicians. They became process engineers, then line managers, then plant directors. By the 1990s, the entire management chain of Intel Malaysia, from shift supervisor to managing director, was local. Engineers trained at Intel and AMD were absorbing not just the how of semiconductor manufacturing but the why—the specifications, the tolerances, the culture of zero-defect, the back-and-forth of co-development with equipment vendors.

Chuah Choon Bin was one of those engineers. He spent his early career inside that MNC ecosystem, watching the economics from the inside. The pattern he saw was consistent. Whenever a Penang plant needed a custom test handler or a bespoke automation rig, it had to import that equipment from Japan, Germany, or the US, typically at eye-watering prices and with lead times measured in quarters. The local content of a multi-billion-dollar Penang semiconductor industry, in terms of actual tools, was near zero. That struck him as an opening. You did not need to out-invent Texas Instruments; you simply needed to stand in the hallway and take orders from the plant next door, faster and cheaper than the incumbents.

In 1991, he founded Pentamaster. The name itself is unremarkable—a stitched-together word signalling mastery across multiple disciplines—but the positioning was deliberate. Rather than chase the prestige customers, the firm started with whatever the MNCs in Bayan Lepas needed: handlers, feeders, inspection rigs, pick-and-place stations. The business was what you would today call "capability-expansion services." If a customer wanted something that didn't exist, Pentamaster would design it, build it, install it, and keep tweaking it until it worked. There was nothing glamorous or venture-capital about the early decade. It was cash-in, cash-out engineering, funded by customer deposits and retained earnings, paid for in ringgit that did not go very far.

The dot-com bubble nearly killed the firm. Pentamaster had built up optoelectronics exposure in the late 1990s—testers for laser diodes, handlers for fiber-optic components—and when the telecom capex cycle collapsed in 2001, orders evaporated almost overnight. Management did not raise equity. They did not pivot to a different market. They simply cut, absorbed, and waited. What the episode taught them, and what still informs balance sheet policy today, is that this is a business where feast and famine can arrive within a single quarter, and where the only way to survive is to stay net-cash, lean, and humble.

The 2008 crisis tested the same muscle. Pentamaster survived again, largely by leaning into the smartphone wave just as Apple's iPhone and the broader Android ecosystem were beginning to demand enormous volumes of miniature optical and sensor components. By the early 2010s, what had started as a job-shop for Bayan Lepas had turned into a recognized specialist in automated test equipment for consumer electronics, particularly anything involving a small lens, a laser, or a proximity sensor. That's where the smartphone chapter starts—and, eventually, where the company's most consequential pivot would begin.

III. The Great Pivot: From Smartphones to EVs

The numbers looked great, and that was precisely why Chuah Choon Bin became nervous. Somewhere around 2014 and 2015, Pentamaster's consumer-electronics business was growing faster than anything else in the company. Automated test handlers for smartphone camera modules, testers for 3D-sensing laser diodes, vision-inspection rigs for proximity sensors—these were feeding straight into what was then the single most voracious supply chain in industrial history. Every refresh cycle of the iPhone and its Android competitors pulled another wave of capex through the company's order book. Management could have simply rolled forward that playbook and ridden the consumer wave for another decade.

They chose not to. What the leadership team saw, a full two or three years before it became a consensus view on Wall Street, was a smartphone plateau. Unit volumes were decelerating. Refresh cycles were lengthening. The optical innovation that had pulled so much ATE spend into Penang—dual cameras, then triple, then time-of-flight sensors—was becoming incremental rather than step-change. And, critically, the margin structure of serving a handful of enormous consumer OEMs was deteriorating as they began pitting equipment vendors against one another in brutal RFQ wars.

At roughly the same time, Tesla's Model S was beginning to scale, and every traditional automotive OEM was waking up, with varying degrees of panic, to the fact that a car was about to become an electric appliance with a very complicated battery. That meant inverters. That meant onboard chargers. That meant DC-to-DC converters. Power electronics, the subsystems that had previously been a sleepy corner of a semiconductor industry obsessed with logic and memory, were about to eat the automotive bill of materials. And those components had one inconvenient property: you couldn't sell them to a car company without testing every single one, at high voltage and high current, under conditions that no smartphone tester was built to handle.

Pentamaster's bet was to redirect the most talented engineering resources in the firm away from camera modules and into high-voltage power electronics test. Internally, this was a painful call. The consumer teams were the ones winning awards. The automotive opportunity was smaller, slower-moving, and meant re-tooling competencies for customers—German and Japanese Tier 1s, mostly—that were notoriously conservative about qualifying new equipment vendors. There was no guaranteed payoff. What there was, instead, was a multi-decade migration pattern: once you qualified into an automotive platform, you stayed in for the life of the platform, and EV platforms were being architected with fifteen-year horizons.

Embedded in that automotive bet was a second, more technical bet: silicon carbide. For most of the history of power electronics, the underlying semiconductor had been plain silicon—cheap, well-understood, and good enough for inverter duty in the 600-volt range. Electric vehicles were pushing toward 800-volt architectures, where the physics of silicon starts to get ugly: switching losses balloon, heat management becomes miserable, and efficiency drags down range. Silicon carbide, a wide-bandgap material long used in niche military and aerospace applications, had the opposite profile: it switched faster, ran hotter, and lost less energy. The catch was that it was much harder to test. Defect rates were higher, voltages were higher, and the handlers had to manage thermal conditions that melt consumer-grade sockets.

That difficulty was Pentamaster's opportunity. The incumbents in automated test equipment—Teradyne out of Boston, Advantest out of Tokyo—were monstrously competent at logic and memory but had never built their businesses around the finicky world of discrete power devices. The Penang firm saw that the test problem for SiC and, later, gallium nitride, was not a scale problem; it was a customization problem. Every customer wanted a slightly different socket, a slightly different thermal profile, a slightly different throughput target. That played directly to what Pentamaster had been doing since 1991: bespoke engineering, delivered at speed, against a customer specification that often wasn't finalized until the project was already underway.

What emerged from all this was the so-called "co-engineering" model. Rather than sell a standard product off a brochure, Pentamaster embedded engineers with the customer, often sitting inside the customer's facility for weeks at a time, iterating on hardware and software together. For a power-electronics customer trying to ramp a new SiC inverter module, the alternative to this model was spending eighteen months and tens of millions of dollars working with a larger vendor whose roadmap might not align. For Pentamaster, the model meant orders that were smaller in any single quarter but vastly stickier, and margins that held up because the work was genuinely custom rather than commoditized. By the late 2010s, that approach had pulled the firm from a consumer-electronics specialist into the co-pilot seat of the EV power-electronics build-out. The logical next step was to make the story legible to capital markets—and that meant leaving Bursa Malaysia behind.

IV. The HK Listing & Strategic Capital Deployment

The parent company, Pentamaster Corporation Berhad, had been listed on Bursa Malaysia since 2003. That listing had done what listings are supposed to do: given founding shareholders liquidity, funded modest expansion, kept the firm in the spotlight of a local investor base. What it had not done was deliver a valuation that remotely matched the underlying economics of the business. By the mid-2010s, Pentamaster's ATE and Factory Automation Solutions units were growing at rates and margins that would have commanded double-digit EBITDA multiples on any American or Taiwanese exchange. On Bursa, they traded at a stubborn mid-single-digit multiple, because Bursa simply did not have a deep investor base for specialized capital-equipment stories.

The fix was a structure that is common in family-controlled Asian conglomerates but remains poorly understood by many Western investors: a spin-listing. In 2018, the group carved out the ATE and FAS businesses into Pentamaster International Limited, incorporated in the Cayman Islands, and listed the vehicle on the Hong Kong Stock Exchange. Pentamaster Corporation Berhad retained a controlling stake of roughly 54 to 55 percent; the float was placed with Hong Kong and international institutional investors. The parent remained listed in Kuala Lumpur. Investors could now choose their poison: the holdco at a conglomerate discount, or the opco at a valuation that reflected its actual growth trajectory.

The strategic logic of the Hong Kong listing was about more than multiple arbitrage. It was about visibility to the customer base. Increasingly, Pentamaster's buyers were global: a German Tier 1 automotive supplier, an American MedTech giant, a Korean power-device maker, a Chinese EV OEM. Those buyers' procurement teams were far more comfortable signing multi-year framework agreements with a company whose financials were pored over by regional sell-side analysts in Hong Kong than with a name obscurely listed on a Southeast Asian exchange. The listing was, in part, an enterprise-grade credibility signal.

The more interesting story, however, is what the company did with its capital once it was listed. Pentamaster did not embark on an acquisition spree. It did not buy a Teradyne-adjacent Taiwanese peer, or roll up a collection of regional automation houses. It made one consequential deal, in 2019: the acquisition of TP Concept Engineering, a Malaysian automation-equipment firm specializing in the manufacturing and assembly of medical devices. The purchase price was around 10 times earnings, materially below the 15 to 20 times that comparable public capital-equipment peers were commanding. That wasn't because TP Concept was troubled; it was because it was small, privately held, and operating in a niche where the trade comps were thin.

What the acquisition bought Pentamaster was not primarily revenue. It bought a qualified seat at the table of the medical-device industry—a market that looks superficially adjacent to semiconductors but is in fact regulated, slower-moving, and built on validation cycles that can take years. TP Concept had already qualified tooling for customers in IV sets, catheter assembly, and lancet manufacturing. Rebuilding that qualification from scratch, inside Pentamaster's existing FAS business, would have taken half a decade and a far larger investment than the purchase price. What the deal really represented, in Acquired terms, was the classic "build versus buy" playbook executed with unusual discipline: buy the qualification, plug in the engineering bench, let the combined entity compound.

The remainder of the capital strategy has been equally disciplined, almost to a fault. Management has run the balance sheet in what it calls a "net cash" posture, meaning the company has essentially never carried interest-bearing debt in excess of its cash and short-term deposits. For investors used to modern capital-allocation sermons about the virtues of leverage, this looks inefficient. For a business that is, underneath, exposed to lumpy capital-equipment order cycles and customer-specific project risk, it is survival insurance. When Covid hit in early 2020, and when semiconductor capex swung violently in 2023, Pentamaster did not have to raise equity at distressed prices or renegotiate with lenders. That optionality is invisible on a normal multiples screen, but it is exactly the kind of balance sheet optionality that compounds over decades. The philosophy, investors learn when they sit across the table from management, is not theoretical. It was written into the firm's instincts by the dot-com collapse and reinforced by 2008. It is less a capital-allocation strategy than a generational memory.

V. Management Deep Dive: The Chuah Choon Bin Era

Meet the boss, and you do not meet the archetype. Chuah Choon Bin is not the Steve Jobs of Penang. He does not give keynote speeches in black turtlenecks. He rarely sits for long-form interviews, and when he does, his style is unfailingly technical. Ask him about a new test socket for 1,200-volt SiC modules and you will get fifteen minutes on thermal impedance; ask him about personal vision and you will get a shrug and a redirection back to the test socket. That temperament, to the extent that it can be read at all, is what has stamped the company since 1991: extreme engineering pragmatism, an allergy to puffery, a relentless bias toward the next order.

The biographical arc is the classic Penang engineer's story. Chuah came up through the MNC ecosystem that landed in Bayan Lepas in the 1970s and 1980s, working on semiconductor production lines before he was thirty. What distinguished him from his peers, most of whom stayed inside Intel or Hewlett-Packard and eventually rose to become plant directors, was a conviction that the interesting economics lay not in running the factory but in selling it the tools. Founding Pentamaster in 1991 was less an act of entrepreneurial daring and more an act of arbitrage on skills and access: he knew the customers, he knew what they needed, and he knew none of the existing vendors were close enough or fast enough.

That grounding matters for understanding incentive alignment. Chuah's economic exposure to Pentamaster International is indirect, held primarily through his controlling interest in the parent company, Pentamaster Corporation Berhad, which in turn holds roughly 54 to 55 percent of Pentamaster International. The effective look-through ownership for the Chuah family is in the ballpark of 20 percent of the Hong Kong-listed entity—substantial enough that the family's personal wealth moves with the share price, but not so concentrated that governance concerns become acute. Board composition and audit oversight broadly reflect Hong Kong listing standards, with independent directors on the audit and remuneration committees. Related-party transactions between the opco and the parent are disclosed and, so far, uncontroversial; investors should nonetheless keep the dual-listed structure in their peripheral vision as a perennial watch item.

What is harder to capture in a filing, but is arguably the most important attribute of the management system, is the way Pentamaster handles engineering talent. Penang has a talent problem, though not of the usual sort. The problem is not scarcity; it is poaching. Intel, AMD, Broadcom, Micron, Infineon, and Bosch are all hiring engineers out of the same pool, and an MNC salary plus a dollar-denominated paycheck is a formidable proposition. Pentamaster's response has been a long-running employee share-grant scheme that vests over multi-year horizons, combined with R&D-linked performance bonuses and a cultural insistence that engineers are given unusually wide latitude to own projects from quote through installation. Several of the firm's most senior technical leaders have been with the company for two decades or more—a tenure profile that is unusual anywhere, and almost unheard of in Bayan Lepas.

The phrase you hear repeatedly from inside the firm, often delivered with a half-smile, is "Penang Spirit." What it means, in practice, is a specific operating tempo: quote fast, engineer fast, deliver fast, and let the specs evolve in parallel with the build. Western competitors tend to work in a rigidly sequential fashion—freeze the spec, build the tool, ship it, validate it. Pentamaster's teams are more willing to ship something that is 80 percent defined and iterate the last 20 percent on the customer's line. For conservative, safety-critical customers, that sounds like a nightmare. In practice, the firm has built a reputation for pulling it off, and the customers who've experienced it once rarely go back to the alternative.

The concern that analysts raise most often—and that Chuah himself has addressed, gently, in investor meetings—is key-man risk. The founder is now in his sixties. Day-to-day leadership has been increasingly shared with a deep bench of managing directors who oversee the ATE, FAS, and medical verticals, and with a CFO team that has grown significantly since the Hong Kong listing. The cultural DNA, however, remains heavily bound up with the founder's personal presence. Succession is not an immediate question, but it is a ten-year question, and it is a question that any long-horizon investor should be tracking with the same seriousness they would track the power-electronics pipeline. That pipeline, incidentally, is where the next story lives: the businesses that have grown up inside Pentamaster while the market was distracted by the EV headline.

VI. The "Hidden" Businesses: Beyond the Chip

Take a tour of Pentamaster's factories in Penang and you will notice something counterintuitive. The halls are not dominated by EV inverter testers. Those exist, of course, and they are enormous. But increasingly, the floor space is occupied by long, snake-like lines of articulated robots, precision conveyors, sterile-cell enclosures, and optical inspection stations—lines that do not test semiconductors at all. They make medical devices. Catheters. Insulin pens. IV sets. Safety syringes. Ostomy bags. Single-use devices in the literal sense: used once, thrown away, replaced by the next one coming off a line that, increasingly, Pentamaster built.

The medical segment is the part of the story that most EV-obsessed investors undervalue, and understanding why the company has pushed into it so aggressively tells you a lot about management's thinking. Medical devices, particularly single-use consumables, share two attributes that are almost irresistible to a capital-equipment firm: the end product has near-infinite demand elasticity (hospitals consume billions of units annually), and the manufacturing process demands extreme automation because labor cost, contamination risk, and regulatory compliance all push in the same direction. If you're making catheters, you cannot afford for a human being to touch the product. Automation is not a nice-to-have. It is the product.

The incumbents in that space have historically been specialty automation firms in Germany, Switzerland, and the US—Mikron, Stoeger, some divisions of ATS. Pentamaster's entry through TP Concept, and the subsequent re-platforming of that capability inside its broader FAS infrastructure, has created a credible Asia-based alternative that is increasingly winning work from multinational MedTech customers looking to diversify their equipment supply chains away from Europe. The pandemic accelerated that trend. So did the subsequent push by major MedTech OEMs to localize production in Malaysia itself, where Penang and Johor have become clusters for glove, syringe, and catheter manufacturing.

What makes this more than a simple diversification story is the economics. The medical automation business carries gross margins that are, in most reporting periods, comfortably at or above the ATE segment, with the added advantage of longer project cycles and more predictable cash flow profiles. MedTech customers do not rush. Once qualified, they do not swap vendors. And they are increasingly willing to pay for custom solutions because their own pricing power, regulated and reimbursement-driven, allows them to absorb upstream equipment costs far more comfortably than a consumer-electronics customer ever could.

Underneath both the automotive and medical businesses, and this is the part that rarely makes it into sell-side reports, Pentamaster has been quietly building a proprietary software layer. Internally, it's called i-ARMS—the Intelligent Automated Robotic Manufacturing System. The simplest way to describe it is as the factory-floor equivalent of an operating system. It handles the orchestration of robotic cells, the data capture from sensors and machine-vision cameras, the predictive-maintenance logic that tells an operator a bearing is about to fail, and the analytics dashboards that MedTech and automotive customers increasingly demand for regulatory traceability. A single-use medical device must be traceable to the individual production batch; an automotive power module must be traceable to the individual test result. i-ARMS is what makes that traceability seamless.

The strategic importance of i-ARMS is that it transforms what would otherwise be a hardware transaction into a long-term operational relationship. When a customer buys a Pentamaster line today, they are also subscribing, implicitly, to the software that runs it. Upgrades, modules, new analytics packages, integration with the customer's enterprise systems—these generate recurring work that does not show up as software-as-a-service revenue in the accounts, but does show up as stickiness, aftermarket parts and services revenue, and, most importantly, as the first firm on the list when the customer is designing its next production line.

If you look at the segment disclosures, the picture that emerges is of a business whose revenue mix has shifted dramatically over the past decade. Automotive and broader semiconductor test remains the largest segment, typically accounting for somewhere in the range of 45 to 50 percent of revenue in any given year, with the specific number moving around with EV capex cycles. Medical has grown from a single-digit share of revenue pre-TP Concept to a double-digit share today, with growth rates that have compounded at a noticeably faster pace than the legacy segments. Consumer electronics, once the dominant source of top-line, has been deliberately throttled back and now sits in the mid-teens, reflecting the strategic choice management made a decade ago. The result is a company that, while still sensitive to semiconductor capex, is structurally less exposed to any single end market than it was in 2016. That diversification is not an accident; it is the whole strategic point. The question for investors, then, is how defensible this mix really is—which is where frameworks become useful.

VII. The Playbook: 7 Powers & Porter's 5 Forces

Every Acquired episode reaches the moment when the frameworks come out, and for good reason: strategy language makes otherwise-elusive durability arguments legible. Pentamaster is a good test case because at least three of Hamilton Helmer's Seven Powers are visibly in play, and several more are plausibly in play.

Start with the one that is most obviously operative: switching costs. When a European automotive Tier 1 qualifies a Pentamaster test cell for its next-generation SiC inverter, that qualification is not a quick signoff. It involves months of correlation studies, failure-mode analyses, ISO/TS 16949 or IATF 16949 paperwork, and the creation of a documented "equipment master" that the customer's own quality team signs into the production release. Once that signature is in place, the cell becomes part of the production system for the life of the vehicle platform, which for an EV architecture can run ten to fifteen years. Ripping out that cell and replacing it with a competing vendor's equipment means redoing the entire qualification from scratch, at a cost that usually dwarfs the original equipment purchase. Medical customers are, if anything, even stickier: any change to the qualified production process triggers regulatory re-filings that can take a year or more. Switching costs, in other words, are not just present; they are compounding with every new platform Pentamaster lands.

The second power, less obvious but arguably just as important, is a cornered resource—specifically, the concentrated pool of specialized mechatronic engineering talent in Penang. The island has spent fifty years producing engineers who can straddle mechanical design, electrical integration, vision systems, and automation software. That combination is unusual anywhere and is especially rare in jurisdictions that have strong single-discipline engineering cultures but weaker cross-disciplinary fluency. Pentamaster has spent three decades building relationships with the local universities, training partnerships with technical institutes, and an internal engineering ladder that retains senior talent through equity and project ownership. New entrants cannot replicate this overnight; even better-capitalized competitors in Taiwan, Korea, or China have struggled to stand up equivalent benches because the skills are culturally embedded in Penang in ways that do not translate simply through hiring.

The third power, process power, is where it gets interesting. The firm's ability to run bespoke engineering projects at scale, without descending into the usual custom-development chaos, is a learned capability accumulated over hundreds of projects. The i-ARMS software layer, the modular hardware architectures that allow a new test cell to reuse 60 to 70 percent of a prior design, the project-management tempo that compresses timelines—these are organizational capabilities that do not sit in any one engineer's head and that competitors would have to build, painfully, over years. Process power is the hardest power to evidence, but it is the one that most consistently separates good capital-equipment firms from mediocre ones.

Now the other side of the ledger: Porter's Five Forces. The threat of new entrants is low. ATE is not a business where a well-funded startup can write a few clever algorithms and take share; it is a business where the cost of defect escapes to customer facilities is measured in production shutdowns, and where qualification cycles make even very clever newcomers invisible for years. The threat of substitutes is also low for any workload that genuinely requires physical test and handling; chips and medical devices cannot be inspected by software alone.

Buyer power is the most nuanced force. Pentamaster's customer base is concentrated among a small number of global OEMs, particularly on the automotive side, and those customers have enormous purchasing leverage in principle. In practice, the mission-critical nature of test—you cannot ship a drive module whose SiC MOSFETs haven't been screened, period—mitigates that leverage at the margin. The customer can squeeze on price, and they do, but they cannot credibly threaten to walk away. Supplier power is modest; Pentamaster sources critical subsystems from a diversified base of Japanese and European precision-component suppliers. Rivalry is the force that investors should watch most actively: in any single test niche, the firm competes with Teradyne, Advantest, Cohu, Chroma, and Japan's Techwing, and the pricing environment in commoditized segments is real. The firm's strategy has been to compete on customization in the niches where incumbents cannot or will not operate, and to avoid head-to-head battles on standard products.

One useful lens for stress-testing this strategic position is to benchmark the company against its closest peers in the so-called Penang Trio: Pentamaster, ViTrox, and Greatech. ViTrox plays more heavily in machine vision inspection, Greatech in factory automation for adjacent industries such as solar. All three trade at valuations that carry what you might call a Malaysian discount—price-to-earnings multiples typically below what a similarly profitable capital-equipment firm would command on a US or Taiwanese exchange. That discount is partly a function of lower index inclusion, partly a function of smaller float, and partly a function of investor unfamiliarity with specialist Southeast Asian names. Whether the discount persists is a separate question from whether the underlying economics justify a re-rating over time.

The KPIs that matter most for tracking Pentamaster's execution narrow down, in the end, to two that capture almost everything else. The first is the share of revenue coming from the combined automotive and medical segments; the higher that share, the more the business has successfully migrated from cyclical consumer exposure into longer-cycle, higher-margin verticals. The second is gross margin stability across end-market mix shifts; if margins hold up as the mix tilts toward medical and EV, the switching-cost and process-power arguments above are being confirmed by the income statement. A third, which is softer but worth watching, is the disclosed backlog or order book where it is provided, because it captures forward visibility in a business where revenue recognition can lag bookings by several quarters. With the playbook sketched, the last strategic question is the familiar one: bull, bear, and what kind of business we are actually looking at.

VIII. Bear vs. Bull Case

The bear case begins, inevitably, with geopolitics. Pentamaster sits at the junction of two supply chains—automotive semiconductors and advanced capital equipment—that are increasingly fault lines in the US-China technology contest. The company counts Chinese EV power-device makers among its customers, and it also supplies European and American Tier 1s whose procurement policies are being shaped in real time by export-control regimes that change on a weekly basis. The risk is not that the firm ends up sanctioned; it is that the operating cost of compliance rises, that certain high-margin Chinese accounts become effectively off-limits for politically sensitive tooling, and that the cross-strait volatility broadly compresses demand from end customers caught in the middle. None of this is hypothetical; it has been a live friction in capital-equipment supply chains since 2023.

The second bear argument is cyclicality dressed up as structural growth. The EV thesis, as consensus now has it, is a multi-decade build-out. The order book for any given quarter, however, is not; it is hostage to specific OEM platform decisions, inventory corrections, and the occasional brutal destocking cycle of the kind that swept through 2023 and dented utilization rates at power-device makers from Wolfspeed to Infineon. When the customers slow, Pentamaster slows. That does not invalidate the long-term story, but it does mean that revenue in any one year may bear only loose resemblance to revenue in the next, and that gross margin can wobble with mix shifts between front-loaded project work and aftermarket parts.

Third is the key-man question discussed earlier. A founder-led firm whose founder is in his sixties, whose culture is deeply shaped by his personal presence, and whose largest shareholder is a family vehicle, has a succession risk that cannot be entirely engineered away. Professional management bench-building has accelerated since the Hong Kong listing, but investors who underwrite a ten-year holding period must underwrite, implicitly, a transition scenario that has not yet been tested.

The fourth bear consideration is more subtle: margin pressure from customers who have become too large, too important, and too sophisticated. When a single automotive Tier 1 begins to represent a double-digit share of any capital-equipment vendor's revenue, that customer's procurement team will eventually discover its leverage. The mission-critical nature of test partly insulates the firm against this, but the insulation is not absolute, and the pricing discipline of buyers has been tightening as EV capex budgets face scrutiny. Related to this, any large customer-specific qualification effort carries project execution risk; a single botched platform launch can produce one-off losses that are material to a quarter or even a year.

Now the bull case. The cleanest framing of it is the "triple tailwind." The first tailwind is EV adoption itself. The world is very likely to sell tens of millions more electric vehicles in 2030 than it does in 2026, and every one of those vehicles requires tested power electronics, onboard chargers, and battery management modules. The capital-equipment intensity of that transition is significantly higher than the equivalent internal-combustion build-out because the underlying components are more defect-sensitive and operate at higher voltages. Pentamaster is qualified into the production lines of multiple major Tier 1s for exactly this work.

The second tailwind is the migration from conventional silicon to wide-bandgap materials—silicon carbide and, to a lesser extent, gallium nitride—across EV traction inverters, fast-charging infrastructure, and industrial motor drives. Each of these applications has its own test challenges, and each is a market that is only beginning to scale. The installed base of SiC production capacity globally is still a fraction of what forecasters expect by the end of the decade. Every new SiC fab or module line creates a new set of qualified vendor slots, and Pentamaster's head start in this niche is not trivial.

The third tailwind is the medical automation ramp, which is driven by a different set of forces entirely—aging populations, regulatory push toward single-use devices for infection control, the localization of MedTech manufacturing in Southeast Asia—and which has almost no correlation with the semiconductor capex cycle. The diversification between these two pillars is structurally valuable. In a quarter when automotive slows, medical can hold the line. Over a cycle, they should smooth one another out.

Set those three tailwinds against a valuation that continues to reflect the "Malaysian discount," and against a balance sheet that carries net cash and therefore the option to deploy into another strategic acquisition opportunistically, and the setup is attractive on its face. The more sophisticated bull argument adds one further element: the enterprise value is, arguably, undercounting the software and data layer that i-ARMS represents. If you believe that factory-floor software is going to become a recurring-revenue business for industrial-automation firms over the next decade—and the precedent of Siemens, Rockwell, and Dassault suggests it might—then Pentamaster has a head start inside its installed base that no accounting convention currently values.

The Acquired question at the end of all this is the one that defines the investment identity: is Pentamaster a compounder or a cyclical? The honest answer, and the more interesting one, is both. In the short term, quarterly results will swing with capex cycles, and anyone who thinks otherwise has not been paying attention to the industry's history. In the long term, the combination of switching costs, process power, and a steadily diversifying end-market mix points toward a business whose earnings power should trend upward over a multi-cycle horizon. The compounder is hiding inside the cyclical, and the question for investors is whether management continues to execute well enough to let the former win out over the latter.

IX. Conclusion & Final Reflections

Pull back, and the Pentamaster story turns out to be less about semiconductors and more about the long arc of industrial capability. In the 1970s, Penang was a place where American MNCs went because labor was cheap. In the 1990s, it was a place where the locals started building better tools than their foreign bosses realized they needed. In the 2010s, it became a place where the tools themselves got good enough to compete on the world stage. And in the 2020s, it has become, in specific niches, a place where the global EV and MedTech industries simply cannot get what they need from anywhere else.

The myth versus reality cut on this company is therefore worth stating plainly. The myth, widely held by investors who glance at the ticker and move on, is that 1665.HK is a small Malaysian semiconductor test company levered to the smartphone cycle and sensitive to any broader tech-capex wobble. The reality is that the consumer-electronics share of revenue is already in the mid-teens and shrinking, that the automotive book is structurally tied to decade-long EV platform lifecycles rather than annual refresh cycles, and that the medical segment is quietly building into a second pillar whose cyclicality is almost entirely decoupled from the first. The myth flattens the firm into a cyclical; the reality is something closer to a two-legged compounder with a volatile quarterly overlay.

The lesson, if you zoom all the way out, is about how a company from a developing nation can climb the value chain. Penang's trajectory is not the story of cheap labor permanently locked into low-margin assembly. It is the story of an ecosystem that absorbed transferable know-how from fifty years of multinational presence, digested it, and eventually started to export it. Pentamaster is one of the clearest embodiments of that arc. The firm did not start out with access to advanced research, venture capital, or global brand recognition. It started out with proximity to demanding customers, discipline about customer pain, and an unfashionable patience about building the balance sheet. Those are repeatable ingredients in other emerging markets, if anyone is willing to wait the thirty years it takes.

What the case ultimately illustrates is the playbook of the modern industrial firm, divorced from geography. Deep customer embeddedness. A bias toward customization over standardization in markets where customization is actually valued. A balance sheet managed like it might need to absorb a civilizational shock, because someday it might. A willingness to make painful portfolio bets—killing consumer exposure at its peak, funding automotive before the capex arrived—that look obvious in hindsight but were genuinely contrarian at the time. And a cultural stance toward engineering talent that treats the engineers themselves as the compounding asset, rather than as interchangeable inputs.

For investors, the two or three things worth continuing to watch are, in order, the evolving mix between automotive-semiconductor, medical, and consumer revenues; the gross margin profile as that mix shifts; and the progression of i-ARMS from embedded enabler into something that might, eventually, look like a services and software business in its own right. Those three lenses will tell you, over the next few years, whether the compounder is winning out over the cyclical.

And then, of course, there is the larger bet, the one that sits behind all of the specific analysis: that the transitions this decade is built around—the end of internal combustion, the rise of SiC and GaN, the automation of medical manufacturing—will continue to demand custom tools that can only be built by firms with deep domain knowledge and extreme engineering agility. If that bet is right, then the architects of the silicon shift are not the chipmakers. They are the ones building the machines that make the chipmakers possible. Pentamaster has been quietly betting that it belongs on that list, and the evidence is that the world's most demanding customers agree.

X. Top References & Further Reading

- Pentamaster International Limited, Annual Reports 2018–2024, available via the Hong Kong Exchange HKEXnews portal, for tracking the shift in segment revenue from consumer to automotive and medical.

- Pentamaster Corporation Berhad, Annual Reports and investor presentations via Bursa Malaysia, for parent-company context on group strategy and related-party disclosures.

- Malaysia Investment Development Authority (MIDA) historical publications on the evolution of the Bayan Lepas Free Industrial Zone and the fifty-year arc of the Malaysian semiconductor ecosystem.

- Penang Institute research notes on the "Seven Samurai" era and the long-term human-capital effects of multinational presence in Penang.

- Comparative public filings for ViTrox Corporation Berhad and Greatech Technology Berhad, for peer benchmarking within the "Penang Trio."

- Global semiconductor industry capex datasets from SEMI and VLSI Research, for framing the backdrop of ATE demand cycles.

- Research coverage from Hong Kong–based brokerages initiated following the 2018 listing, for segment-level modeling and margin trajectories.

- Industry primers on silicon carbide and gallium nitride power devices published by Yole Group, for technical context on the wide-bandgap transition.

- Hamilton Helmer, "7 Powers: The Foundations of Business Strategy" (Deep Strategy, 2016), for the strategic framework applied in Section VII.

- Michael Porter, "Competitive Strategy" (Free Press, 1980), for the Five Forces lens applied alongside.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube