J&T Global Express: The Blitzscale of Global Logistics

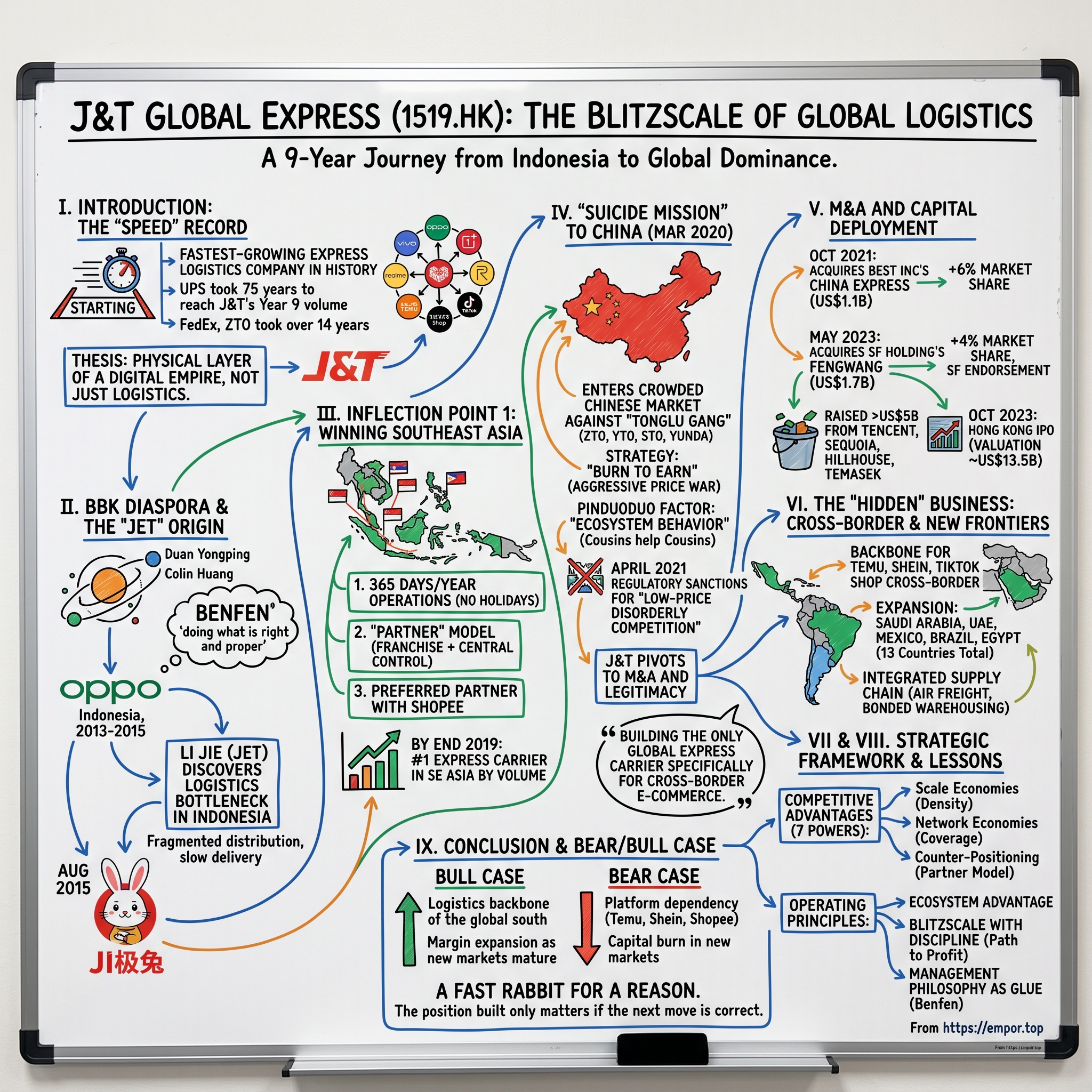

I. Introduction: The "Speed" Record

Picture a warehouse on the outskirts of Jakarta in late 2015. The corrugated steel roof groans under tropical heat. A handful of men in unbranded polos stand around a long folding table, sorting bubble-mailers by hand into piles labeled with marker pen: Surabaya, Medan, Bandung. There is no conveyor belt. There is no scanner. There is no software. There is, in fact, barely a company. What there is, is a 38-year-old Chinese expat named Li Jie, who has just left a comfortable executive role at one of the most successful smartphone companies on earth, and who has decided that he is going to build the FedEx of Southeast Asia. Starting today.

If you had walked into that warehouse and told the people inside that within nine years their company would be moving more than 24 billion parcels a year across thirteen countries, that they would have crushed three publicly listed Chinese express incumbents in a price war, that they would have acquired the China express division of one NYSE-listed company and the lower-tier brand of the world's most respected logistics carrier, that they would have IPO'd in Hong Kong at a valuation north of US$13 billion, and that they would be quietly powering the cross-border delivery operations of Temu, Shein, and TikTok Shop, you would have been escorted politely to the door.

And yet that is exactly what happened. J&T Global Express, ticker 1519.HK, is the fastest-growing express logistics company in the recorded history of the industry. Not the fastest-growing in Asia. Not the fastest-growing in this decade. The fastest-growing, full stop. UPS took 75 years to reach the package volumes that J&T cleared by year nine. FedEx, founded in 1971, did not break a billion packages annually until well into the 1990s. ZTO, the Chinese express darling that listed on the NYSE in 2016, took roughly 14 years to scale to where J&T arrived in nine.

The thesis of this episode is that J&T is not really a logistics company in the traditional sense. It is the logistics arm of an ecosystem, and that ecosystem traces back to a small electronics conglomerate in Dongguan, China called BBK. BBK is the parent or spiritual ancestor of OPPO, vivo, OnePlus, Realme, and, through founder Duan Yongping's investment and mentorship, Pinduoduo. J&T's founder Li Jie ran OPPO Indonesia. The capital, the playbook, the management talent, and the customer demand all flow from the same source. To understand J&T, you have to understand that you are not looking at a courier. You are looking at the physical layer of a digital empire.

Over the next 160 minutes of reading, the journey runs from a hand-sorting warehouse in Jakarta to the bloodiest price war in the history of Chinese parcel delivery, then onward to the deserts of Saudi Arabia and the favelas of São Paulo. The narrative arc is one of audacity, of capital deployed with a ferocity that made even seasoned venture investors uneasy, and of an organizational culture that, depending on whom you ask, is either the most disciplined operating model in modern Chinese business or the most cult-like. Probably both.

The story begins, as so many of the great consumer technology stories of the last twenty years do, with a man named Duan Yongping and a philosophy called Benfen.

II. The BBK Diaspora & The "Jet" Origin

To understand Li Jie, one has to first understand the orbit he came from. In the early 2000s, Duan Yongping, the legendary Chinese entrepreneur who had previously built the Subor educational electronics empire and then BBK Electronics, made a series of decisions that would echo across the global consumer technology industry for the next two decades. He spun out two of his most promising lieutenants and gave them their own brands: Chen Mingyong got OPPO, and Shen Wei got vivo. He moved to California, took up golf, became friends with Warren Buffett, and started writing essays about a concept he called Benfen, a Chinese word that loosely translates as "doing what is right and proper, sticking to your essential nature." It is the opposite of opportunism. It is the discipline of asking, before any decision, what is the correct thing to do, not the clever thing.

Duan also famously paid US$620,000 in 2006 to have lunch with Buffett, and brought along a young man named Colin Huang. Huang would go on to found Pinduoduo. The BBK ecosystem, then, is not just a smartphone company. It is a network of operators who share a worldview, a capital base, and, crucially, a willingness to reinvest in each other.

Li Jie, known internally and externally by his English name "Jet," entered this orbit as a junior manager at BBK in the early 2000s. Born in Hunan province in 1977, he was, by the accounts of those who worked with him, intense, soft-spoken, and obsessive about operational detail. He rose through the OPPO ranks during the company's domestic Chinese growth phase, and then in 2013 was given what was widely considered an exile assignment: open up the Indonesian market for OPPO smartphones.

Indonesia in 2013 was a graveyard for foreign mobile brands. Distribution was fragmented. Retail was informal. Consumers had no credit. And the existing logistics infrastructure, dominated by the state-owned Pos Indonesia and a handful of private regional players, treated Saturdays and Sundays as days of rest. If a phone shipped on Friday afternoon, it would arrive on Tuesday at the earliest. For a consumer electronics product launching with weekend marketing campaigns, that timing was lethal.

Li Jie did what BBK operators do: he flooded the country with offline retail. Within two years, OPPO had become the second-largest smartphone brand in Indonesia, behind only Samsung. But in the process, Li Jie discovered something that would reshape his career. The bottleneck was not marketing. It was not product. It was the fact that you simply could not move a box from Jakarta to a tier-three city in Sulawesi reliably. The logistics layer was broken, and no amount of clever marketing could compensate for a customer who waited eight days for a phone.

This was the "Aha!" moment. Sometime in mid-2015, Li Jie made a decision that, at the time, looked completely irrational. He resigned from OPPO Indonesia, walked away from one of the most lucrative country-manager jobs in Asian consumer electronics, and announced that he was going to start a parcel delivery company. The reaction inside the BBK ecosystem was, by most accounts, bewilderment followed by quiet support. Duan Yongping, who almost never invests publicly, was reportedly an early backer. So were a number of OPPO and vivo distributors who had grown wealthy alongside Li Jie and trusted his judgment.

J&T, originally branded "Jet" after Li Jie's English name and later expanded to stand for "Ji极兔" or "Extreme Rabbit" in Chinese, opened for business in August 2015. The company's founding logo featured a cartoon rabbit, a deliberate signal of speed and harmlessness in a market where the largest carriers all chose intimidating eagles, lions, and arrows.

The management team that Li Jie assembled was, almost without exception, drawn from the OPPO Indonesia organization. The regional heads, the IT lead, the finance chief, the marketing team — they were all former OPPO. This was not nepotism. It was a deliberate choice to import an operating system. OPPO's distribution model in emerging markets was based on a philosophy of treating regional managers as quasi-owners. They received substantial profit shares, they were given enormous autonomy to make local decisions, and they were measured ruthlessly on a small set of operational KPIs. Li Jie ported this model wholesale into J&T, calling it the "Partner" model. It was franchise-like in economics but command-and-control in operating standards. As of the most recent disclosures in J&T's 2024 annual report, Li Jie controlled approximately 11.54% of the economic interest in the company but, through a weighted voting rights structure granted at IPO, held roughly 76% of the voting power. He runs J&T the way a founder-CEO runs a venture-stage startup, even at a US$13 billion market cap.

This origin story matters because it explains every subsequent decision the company has made. J&T was not built by logistics professionals. It was built by consumer electronics distributors who happened to need parcels moved. That distinction is the entire game.

The first test of whether the model would work was about to come, and it would come in the form of the largest e-commerce wave Southeast Asia had ever seen.

III. Inflection Point 1: Winning Southeast Asia

In late 2015, e-commerce in Southeast Asia was a rumor. Lazada, founded by Rocket Internet in 2012, was burning cash trying to teach Indonesians, Vietnamese, Filipinos, and Thais to buy things online. Shopee, the C2C marketplace launched by Sea Ltd in mid-2015, was less than six months old. Tokopedia was a domestic Indonesian player. Total e-commerce gross merchandise value across the entire region was perhaps US$5 billion, less than what Alibaba processed in a single Singles Day.

But the trajectory was unmistakable. Smartphone penetration was crossing 50% in Indonesia. Mobile data prices were collapsing. And the unbanked population, which traditional analysts considered a barrier, turned out to be a feature rather than a bug, because cash-on-delivery created a deeply entrenched need for someone to physically show up at the door, take the cash, and hand over the package. That someone was the delivery driver. And in 2015, almost no carrier in Southeast Asia was set up to do this efficiently.

Li Jie's first strategic move was the kind of decision that looks obvious in retrospect and was considered insane at the time. He announced that J&T would operate 365 days a year. No weekends off. No public holidays off. No Lebaran shutdown, no Chinese New Year hiatus, no Christmas pause. Every single day, every parcel that came in went out. To a competitor running a traditional state-owned post office mentality, this was unthinkable. To a former OPPO distributor who knew that a smartphone sitting in a warehouse over a long weekend was a smartphone that did not generate a sale, it was the only logical answer.

The second move was the Partner model in practice. Rather than building company-owned depots in every city, J&T recruited local entrepreneurs to operate sortation centers and delivery fleets under franchise agreements. The franchisees put up the capital. J&T provided the brand, the IT system, the operating playbook, and, crucially, the volume from major e-commerce platforms. This was identical to how OPPO had built its retail distribution: local owners, central system, shared upside. Within 18 months, J&T had presence in all 34 provinces of Indonesia.

The third move, and perhaps the most important, was the relationship with Shopee. The exact terms of the original Shopee-J&T arrangement have never been publicly disclosed, but industry observers and former employees have consistently described it as a deeply preferred-partner relationship. When Shopee exploded in scale across Indonesia, Vietnam, the Philippines, Thailand, and Malaysia in 2017 and 2018, J&T was the carrier of choice, often handling the majority of Shopee's parcel volume in any given country. Lazada, despite its head start and Alibaba ownership, found itself unable to dislodge J&T from this position because, by 2019, the network density advantage was already insurmountable.

There is a useful mental model for what was happening here. Logistics networks have a property that economists call "path dependence with increasing returns." The first carrier to achieve dense national coverage in a given geography enjoys a per-parcel cost that competitors cannot match, because each new package marginal costs almost nothing to add to a route that is already running. Once J&T had built the densest network in the Indonesian archipelago, with its 17,000 inhabited islands and notoriously difficult road infrastructure, the unit economics tilted permanently in its favor. By 2019, J&T was processing more than two million parcels per day in Indonesia alone, making it the largest express carrier in the country, ahead of every incumbent.

The same pattern repeated, with regional variation, across Vietnam, the Philippines, Thailand, Malaysia, Cambodia, and Singapore. By the end of 2019, J&T was the number one express carrier in Southeast Asia by volume, a region that had not even existed as a coherent e-commerce market five years earlier. The company had, in a single business cycle, captured the position that UPS and FedEx had taken decades to build in their home markets.

But Li Jie was not satisfied. He had watched his old colleagues at OPPO and his old mentor's protégés at Pinduoduo build businesses an order of magnitude larger than what was possible in Southeast Asia. He had also watched the Chinese express market, the largest parcel market in the world, settle into a comfortable oligopoly of four publicly listed carriers known collectively as the Tonglu Gang. He looked at that market and decided, in the early months of 2020, that he was going to enter it. With a pandemic raging. From a standing start. Against incumbents with twenty-year head starts and combined annual volumes of more than 70 billion parcels.

What happened next is, depending on your perspective, either the most audacious go-to-market in the history of Chinese logistics or the most reckless. Both interpretations are correct.

IV. Inflection Point 2: The "Suicide Mission" to China

In March 2020, as the world locked down for the first wave of COVID-19, J&T quietly opened its first Chinese sortation center in Dongguan, Guangdong province. The location was not coincidental. Dongguan is the manufacturing heartland of the Pearl River Delta, the place where OPPO and vivo make their phones, and the place where Pinduoduo's army of factory-direct merchants is concentrated. It is also where Duan Yongping made his original fortune. J&T was coming home, in a sense, to the soil from which its founders had sprung.

The Chinese express market in early 2020 was a four-sided knife fight. ZTO, the largest carrier with roughly 20% market share, had IPO'd on the NYSE in 2016 and was the consolidator and price leader. YTO, STO, and Yunda rounded out the so-called Tonglu Gang, named for the small county in Zhejiang province from which all four had originated. Together they accounted for more than 70% of national volume. SF Express, the premium "FedEx of China" run by founder Wang Wei, occupied the high-end time-definite segment. Best Inc, a company funded by Alibaba and listed on the NYSE, was the perpetual fifth wheel, losing money but holding on. Average revenue per parcel had been falling for years, from roughly 12 RMB in 2010 to under 3 RMB by 2019, and operating margins for even the best-run incumbents had compressed to mid-single digits.

Into this market, Li Jie brought the same playbook that had worked in Indonesia, with one crucial twist. He went on offense with price.

The opening salvo, in mid-2020, was a per-parcel rate that, depending on the route, ranged from 1.0 to 1.4 RMB. To put that in context, the marginal cost of moving a single small parcel through a Chinese express network at scale was estimated by industry analysts at the time to be somewhere between 1.4 and 1.8 RMB. J&T was selling below cost, on every package, deliberately, with no end date announced. The strategy had a name inside the company: "Burn to Earn." The thesis was straightforward. Build network density at any cost in the first 18 months. Once volume reached a certain threshold, unit economics would inflect. The capital to fund the burn would come from a combination of Tencent (which had led a US$1.8 billion round in early 2021), Sequoia, Hillhouse, Boyu, and Temasek, plus a constant injection from the Indonesian profitable operations.

The Tonglu Gang's response was, predictably, to match. ZTO, YTO, STO, and Yunda all cut prices. By the spring of 2021, average revenue per parcel in China had dropped below 2.5 RMB, the lowest level in industry history, and almost every listed carrier reported a sequential collapse in margins. ZTO's gross margin compressed from the high 20s to the mid-teens. The smaller players were bleeding. Best Inc, already weak, was approaching insolvency.

Then came the Pinduoduo factor, which is the part of the J&T story that tends to get whispered about rather than written about. Pinduoduo, the social commerce phenomenon that had grown from zero to more than 700 million annual active buyers in less than five years, was generating an enormous and growing volume of low-value, high-frequency parcels: the cheap apparel, household goods, and groceries that powered its team-purchase model. This volume was, for any carrier that could capture it, the perfect baseload — the kind of predictable, dense, recurring flow that allowed a network to optimize routes and amortize fixed costs.

Pinduoduo, founded by Colin Huang, the same Colin Huang who had been mentored by Duan Yongping and had attended that famous Buffett lunch, directed a substantial portion of its parcel volume to J&T from the moment J&T entered China. The exact percentage has never been disclosed, but at one point analysts estimated that Pinduoduo accounted for more than 60% of J&T's Chinese volume. This was not a sweetheart deal in any documented sense. It was, in the BBK tradition, ecosystem behavior. Cousins help cousins.

The arrangement drew regulatory attention. In April 2021, the State Post Bureau of Zhejiang province, the regulatory body responsible for the Tonglu Gang's home turf, issued a formal sanction against J&T for "low-price disorderly competition." Several J&T sortation centers in Yiwu were temporarily shut down. The State Post Bureau followed up nationally with new rules that effectively banned predatory pricing in the express sector. The era of below-cost shipping had to end.

This is where Li Jie's instincts proved sharp. Rather than fight the regulators, J&T adapted immediately. Prices were raised in line with industry norms. The "Burn to Earn" rhetoric quietly disappeared. And the company pivoted toward what would become the next phase of its strategy: M&A. By the time the regulatory hammer fell, J&T was already processing more than 20 million parcels per day in China, had built more than 100 sortation centers, and had achieved roughly 8% national market share, putting it in striking distance of the smallest of the Tonglu Gang. It was, by any measure, the fastest cold-start in the history of any major express market on earth.

But organic growth was no longer the right tool. To break into the top tier in China, J&T needed not more density but more legitimacy. It needed acquisitions. And there were, conveniently, two motivated sellers waiting in the wings.

V. M&A and Capital Deployment: Buying the Seat

In October 2021, six months after the regulatory crackdown, J&T announced the acquisition of Best Inc's domestic China express business for approximately US$1.1 billion in cash. Best Inc, which had IPO'd on the NYSE at US$10 per share in 2017, had seen its stock collapse to below US$1. Its express division had lost money for years and had ceded share to the Tonglu Gang and to J&T's onslaught. For Best, the sale was a lifeline. For J&T, it was the acquisition of approximately 6% additional Chinese market share, plus more than 90 sortation centers, more than 24,000 service outlets, and a regulatory license that had taken Best a decade to assemble.

Did J&T overpay? On a multiple of historical earnings, the deal was infinitely expensive, because Best's express business was generating losses. On a multiple of revenue, it was roughly 0.4 to 0.5 times trailing twelve months. And on the metric that actually mattered to Li Jie — cost per incremental percentage point of market share — the deal was a bargain. Building the equivalent infrastructure organically would have taken three to four more years and consumed perhaps US$2 billion in additional losses. Buying it shaved years off the timeline.

There is a useful framework here, originally articulated by Marc Andreessen in a different context, called the "speed premium." In markets characterized by network effects and winner-take-most dynamics, the value of being early at scale is measured not by what you spend but by what your competitors are prevented from spending. By acquiring Best's express business, J&T did not just gain density. It removed a fifth-place competitor from the market, denying that asset to anyone else who might have wanted to use it as a beachhead. The integration would be painful — and it was, with reported employee attrition and some service quality issues through 2022 — but the strategic logic was unimpeachable.

Eighteen months later, in May 2023, J&T announced an even bolder deal. It acquired Fengwang, the lower-tier express brand owned by SF Holding, for approximately RMB 11.83 billion, or roughly US$1.7 billion. Fengwang was SF's attempt to compete in the economy parcel segment that the Tonglu Gang and J&T dominated, and it had failed to gain traction. SF Holding, run by the legendary founder Wang Wei, decided that rather than continue to bleed cash trying to compete head-on with J&T, it would sell the asset and turn J&T from a competitor into a partner.

This deal was strategically more important than the Best acquisition, and not because of the price. It was important because it represented an explicit endorsement of J&T by the most respected logistics operator in China. SF Express does not partner lightly. Wang Wei has spent two decades building SF into the gold standard of Chinese express, with industry-leading service quality, dedicated air freight, and a premium brand position. By selling Fengwang to J&T, SF was effectively saying: we will not compete in the economy segment; we will let J&T own it; and we will integrate our networks at the seams. The Fengwang deal added another roughly 4% of Chinese market share and brought J&T's national share to roughly 11%, putting it firmly in the top three.

The capital to fund all of this came from a combination of equity raises and, eventually, the public markets. Across multiple rounds from 2017 through 2022, J&T raised more than US$5 billion from a roster of investors that read like a who's-who of Asian growth equity: Tencent, Sequoia China (now HongShan), Hillhouse, Boyu Capital, Temasek, ATM Capital, D1 Capital, and the SoftBank Vision Fund. The 2021 round alone, led by Boyu and Tencent, valued J&T at approximately US$20 billion, making it one of the largest unicorns in Asia at the time.

The IPO came on October 27, 2023, on the Hong Kong Stock Exchange. J&T priced at HK$12.00 per share, raising approximately US$502 million in primary proceeds at a market capitalization of roughly US$13.5 billion. The valuation was below the peak private market mark, reflecting the broader compression in Chinese tech valuations and the post-2022 reality that growth was no longer free. The stock traded essentially flat on its first day, a signal that public market investors were neither euphoric nor skeptical, but were waiting to see whether the China business could turn the corner from cash burn to cash generation.

By the company's most recent disclosed financials, that turn has begun. For the full year 2024, J&T reported revenue of approximately US$10.3 billion, up roughly 16% year-over-year, parcel volume of approximately 24.6 billion, and adjusted EBITDA of approximately US$840 million. The Southeast Asia segment continued to be the profit engine, with adjusted EBITDA margins in the high teens. The China segment turned adjusted EBITDA positive on a full-year basis for the first time in 2024, a milestone Li Jie had been promising investors since the 2023 IPO. The new markets segment, encompassing Latin America, the Middle East, North Africa, and the company's expanding cross-border operations, was still in investment mode and dragging on consolidated profitability — but, as the next section will explain, it is also the segment that may matter most for the next decade.

The acquisitions were, in the end, not really about China. They were about earning the right to be taken seriously globally.

VI. The "Hidden" Business: Cross-Border & New Frontiers

If the China story is the one investors talk about, the cross-border and new markets story is the one they should be paying attention to. Because it is here that J&T is quietly building what may become its most defensible long-term franchise.

Consider the rise of Temu. Pinduoduo's international arm launched in September 2022 with a singular value proposition: ship cheap goods from Chinese factories directly to American, European, and Asian consumers, at prices that Amazon and Walmart could not match. Within 18 months, Temu had become one of the most downloaded apps in the world, processing tens of millions of parcels per month from China to global destinations. Each of those parcels needs to be picked up at a Chinese factory, consolidated, flown or shipped abroad, customs-cleared, and last-mile delivered to a consumer's doorstep. Each step of that chain is a logistics problem. And J&T, by virtue of its BBK lineage and its preexisting last-mile networks in dozens of destination countries, was the natural backbone.

Shein, the fast-fashion phenomenon that has become one of the largest apparel companies in the world by gross merchandise value, follows a similar pattern. So does TikTok Shop, the ByteDance-owned commerce platform that has been growing aggressively across Southeast Asia, the United States, the United Kingdom, and parts of Latin America. All three of these platforms — Temu, Shein, and TikTok Shop — share a common need: the ability to move enormous volumes of low-value parcels from Chinese origin to a fragmented set of global destinations, reliably, cheaply, and with end-to-end tracking. None of the legacy global integrators (DHL, FedEx, UPS) is structurally well-positioned for this flow, because their cost structures are built around higher-value, higher-margin shipments. J&T, with its origins in low-value Indonesian e-commerce parcels and its hardened experience in the Chinese price war, is built for exactly this segment.

The geographic expansion that has accompanied this cross-border push is breathtaking. In September 2022, J&T launched in Saudi Arabia and the United Arab Emirates. In October 2022, it entered Mexico, Brazil, and Egypt. By 2024, it was operational in thirteen countries spanning Southeast Asia, China, Latin America, and the Middle East and North Africa. The new markets segment, which encompasses everything outside Southeast Asia and China, generated revenue of approximately US$483 million in 2024, up more than 50% year-over-year, and processed approximately 0.7 billion parcels in the year. It remains a small fraction of total volume, but it is growing at roughly three times the rate of the mature China business.

The strategic logic for the Middle East entry in particular bears closer examination. Saudi Arabia has, over the past five years, undergone a massive e-commerce transformation driven by Vision 2030, Crown Prince Mohammed bin Salman's economic diversification program, and by the rapid expansion of platforms like Noon, Amazon.sa, and Shein. The kingdom's logistics infrastructure, however, remained underdeveloped, and the existing carriers were either state-affiliated and slow or international integrators that were too expensive for mass e-commerce. J&T saw an opportunity that looked exactly like Indonesia 2015: a massive consumer market, a nascent e-commerce sector, weak incumbent logistics, and a wave of new platforms desperate for a partner. The playbook deployed in Riyadh was, by all accounts, identical to the one deployed in Jakarta nine years earlier. Local franchisees, central IT, 365-day operations, and aggressive bundled pricing for major platform partners.

The integrated supply chain layer is the other thing worth paying attention to. J&T has begun building out air freight capacity, charter relationships, bonded warehousing, and customs brokerage services, all aimed at competing with DHL and UPS on the global cross-border e-commerce lane rather than the traditional B2B air freight lane. This is a different market, one that the legacy integrators have historically deprioritized in favor of higher-margin business, and it is growing at perhaps 20-25% annually as cross-border e-commerce continues to compound.

There is a real question about how much of this new markets growth will ultimately translate into durable profit. Latin America in particular has been a graveyard for foreign logistics ambitions, with currency volatility, complex labor regulations, and entrenched local players like Mercado Envíos (Mercado Libre's logistics arm) presenting serious obstacles. Brazil's tax regime alone has defeated more than one global expansion plan. Investors should expect the new markets segment to remain in heavy investment mode for several more years, with operating losses that drag on consolidated margins.

But the optionality is enormous. If J&T succeeds in building dense networks in even three of its new markets, it will have created the only globally integrated express carrier built specifically for cross-border e-commerce. That is not a market that exists today in any coherent form. It is a market J&T is creating.

VII. Framework Analysis: 7 Powers & 5 Forces

Stepping back from the narrative, it is worth asking: which of the durable competitive advantages identified in Hamilton Helmer's 7 Powers framework actually apply to J&T, and which are illusions of recency?

Scale Economies is the most obvious power, and it is real. Express logistics is a business in which fixed costs — sortation centers, IT systems, last-mile fleet — are large relative to variable costs, and in which routes that are already running can absorb additional parcels at near-zero marginal cost. The carrier with the highest density per route enjoys structurally lower unit costs than competitors, and that advantage compounds. J&T has demonstrated the extreme version of this dynamic in Indonesia, where it has been the cost leader for several years, and in China, where the unit economics inflected once daily volume crossed the 30 million parcel threshold around 2022. The risk to scale economies, in any market, is that competitors close the density gap fast enough to deny J&T the cost advantage. In China, this risk is real because the Tonglu Gang carriers are not going anywhere. In Southeast Asia and the Middle East, it is less acute.

Network Economies is the second power, and it is somewhat different from scale. Network economies refers to the phenomenon in which the value of the service to each user increases as more users join. In express logistics, this manifests as coverage: a carrier that serves every postal code in a country is more valuable to a national e-commerce merchant than one that serves only major cities. J&T has built true national coverage in Indonesia, Vietnam, the Philippines, Malaysia, Thailand, and increasingly in China. This is a real moat, because the cost of the next coverage point in a remote area is paid for by the existing network's profitability. New entrants have to build coverage from scratch, with no revenue base to fund it.

Counter-Positioning is perhaps the most interesting power to analyze. J&T's Partner model — franchise economics with central command — is something the incumbents in many of its markets cannot easily replicate, because they are either state-owned (which makes franchising politically difficult) or asset-heavy (which makes the capital efficiency of franchising look like a margin sacrifice on the income statement). In Indonesia, this counter-position let J&T move faster than Pos Indonesia and the regional incumbents. In the Middle East, it is letting J&T move faster than the state-affiliated postal services. In China, however, counter-positioning is less of a moat, because the Tonglu Gang carriers all use franchise models too. There, the advantage is more about scale and ecosystem.

Switching Costs is a power that does not really apply to J&T. E-commerce platforms multi-source their carrier capacity, and switching one carrier for another at the parcel level is essentially frictionless. This is why the Bargaining Power of Buyers, in Porter's framework, is the single most important threat to J&T's long-term margins. Three customers — Shopee, Lazada, and Pinduoduo (including Temu) — likely account for more than half of J&T's volume across its entire business. If any one of them decides to in-source logistics, build a competing relationship, or simply demand price concessions, J&T's margins will compress. This is not a hypothetical risk. Shopee built out its own last-mile arm, SPX Express, partly to reduce dependence on third-party carriers including J&T. Pinduoduo has invested in alternative logistics relationships. Alibaba's Cainiao network is a perpetual threat in China.

The other Porter forces are mostly favorable. Threat of New Entrants is low at scale, because the capital required to build a national network is in the billions of dollars and the time to density is multi-year. Threat of Substitutes is low for physical goods, though crowdsourced delivery models like Lalamove are nibbling at certain segments. Bargaining Power of Suppliers — meaning labor, fuel, and real estate — is moderate and rising in some markets, particularly China, where labor costs have been escalating. Industry Rivalry is the highest in China and lowest in the new markets, where J&T has first-mover advantages.

The honest synthesis is that J&T has real and durable competitive advantages in Southeast Asia and increasingly in the new markets, and a contested but improving competitive position in China. The single biggest long-term risk is platform dependency, and the company's diversification efforts — expanding the customer base, entering new geographies, building integrated supply chain services — are best understood as deliberate moves to reduce that dependency.

VIII. The Playbook: Lessons for the Modern Operator

Strip away the geographic detail and the timeline, and J&T's story can be reduced to a small number of operating principles that have generalizability beyond logistics.

The Ecosystem Advantage. J&T did not build a business in a vacuum. It built one alongside its cousin companies in the BBK ecosystem. OPPO provided the founding talent and the operating philosophy. Pinduoduo and Temu provided the parcel volume that allowed the network to scale. The shared capital pool — investors who knew Duan Yongping, who knew Colin Huang, who knew Li Jie — provided the funding to absorb years of losses. This is a different model from the Silicon Valley playbook of building a standalone startup that grows independent of its peers. It is closer to the Korean chaebol or Japanese keiretsu model, but operating across companies that are formally independent. For investors, the lesson is that ecosystem-embedded businesses can grow faster than their standalone unit economics would suggest, because they are subsidized by the success of related companies. The risk is that they can also collapse faster if the ecosystem turns.

The Blitzscale Playbook with Discipline. Reid Hoffman's blitzscaling thesis — prioritize speed over efficiency to capture market share before competitors can react — is well known. J&T executed it more aggressively than almost any company outside of Uber and DiDi. But unlike Uber, which spent more than a decade unable to demonstrate consolidated profitability, J&T has shown a willingness to pivot toward unit economics once market share is captured. The China business turned adjusted EBITDA positive within four years of entry, faster than almost any growth-at-all-costs playbook in modern memory. The lesson is that blitzscale works when there is a clear path to network density that produces structural cost advantage, and it works less well when the underlying business does not have that property. Logistics, fortunately, does.

Operational Excellence at the Hub. J&T's "Direct-to-Hub" model — in which parcels move from origin city directly to destination city's primary sortation hub, bypassing intermediate sortation steps — reduces transit time and damage rates compared to the traditional multi-hub model used by some incumbents. This is a small operational choice with large compounding implications, because faster transit and lower damage rates translate into higher customer satisfaction, which translates into platform partners directing more volume, which translates into more density, which translates into lower costs. The flywheel is real, and it is built on operational details that are easy to underestimate from the outside.

Management Philosophy as Cultural Glue. Benfen — doing what is right and proper, sticking to your essential nature — sounds like a philosophical abstraction, but in practice it manifests as a small number of operating disciplines: tell the truth even when it is uncomfortable, stick to the long-term plan even when short-term metrics suffer, treat partners as quasi-owners and expect them to behave accordingly. This culture has, by most accounts, traveled remarkably well from Dongguan to Jakarta to Riyadh. The reason is that it is not really a Chinese culture or a Southeast Asian culture or a Middle Eastern culture. It is an operating culture, and operating cultures, when they are clear and well-enforced, can be ported across geographies in a way that consumer-facing brand cultures usually cannot. This is one of the reasons J&T has been able to expand into so many markets so quickly: the central operating model is consistent, even as the local execution is adapted.

Capital Discipline Within Aggressive Spending. This is the most subtle lesson. J&T spent enormous amounts of capital. But it spent it on a small number of clearly defined bets: dense networks in specific geographies, two strategic acquisitions in China, and a measured rollout into new markets. It did not, despite having access to nearly unlimited venture funding through 2021, diversify into adjacent businesses, build proprietary technology platforms, or pursue vanity acquisitions. The discipline was in saying no to dozens of plausible adjacencies in order to say yes to the few that compounded. Operators in any high-growth context can learn from this.

The myth-versus-reality test is worth applying here. The myth of J&T is that it is simply a price-cutting upstart that bought market share with venture capital. The reality is that the price-cutting was a tool, not a strategy, and the strategy has always been about network density and ecosystem alignment. When the regulatory environment forced prices up, J&T did not collapse; it adapted, because the underlying network economics were sound. That distinction matters for anyone trying to underwrite the next ten years.

IX. Conclusion & Bear/Bull Case

Where does J&T go from here?

The bull case is straightforward and ambitious. J&T is on track to become the dominant logistics infrastructure for the next two billion e-commerce consumers in emerging markets — the consumers in Indonesia, Vietnam, the Philippines, Mexico, Brazil, Saudi Arabia, the UAE, Egypt, and dozens of countries that will move online over the next decade. None of the legacy global integrators (DHL, FedEx, UPS) is structurally well-positioned to serve this market, because their cost structures are built for higher-value B2B and premium B2C shipments. Amazon Logistics is geographically constrained to a handful of Amazon's core markets. Cainiao is structurally tied to Alibaba and faces growing skepticism from non-Alibaba platforms. SF Express is premium and not playing in the value segment outside China. The competitive set, in the long-term emerging market e-commerce backbone, may be narrower than it appears today, and J&T may have the field largely to itself in many of its target geographies. If that vision plays out, the company's revenue base could compound at high teens to low twenties for another five to seven years, with margin expansion as the new markets segment matures.

The bear case is equally coherent. The capital burn in new markets will continue to drag on consolidated profitability for longer than the bulls expect. China, despite the recent EBITDA inflection, remains a market with structural overcapacity and a regulatory environment that limits price competition as a moat. The platform dependency on Pinduoduo, Temu, Shein, Shopee, and TikTok Shop is concentrated and not getting more diversified, and any one of those platforms faces its own existential risks (Temu's regulatory exposure in the United States and Europe is material; TikTok Shop's geopolitical position is fragile; Pinduoduo's domestic Chinese growth is decelerating). In a downside scenario, J&T's valuation deflates as growth slows and the new markets segment fails to scale to profitability.

The honest read is that both cases have merit, and that the actual outcome will depend on three factors that are largely outside Li Jie's control: the trajectory of cross-border e-commerce regulation in major Western markets, the pace of consumer adoption in the Middle East and Latin America, and the willingness of the BBK ecosystem to continue providing baseload volume to its logistics cousin. None of these is easy to forecast.

For investors building a watch list, the small number of KPIs that actually matter for J&T are these. First, parcel volume growth by segment, broken out into Southeast Asia, China, and new markets — this is the leading indicator of network scale and the variable from which all unit economics derive. Second, adjusted EBITDA margin in the China segment — this is the test of whether the post-acquisition integration thesis is working, and whether the company has earned the right to be considered a structural winner in the world's largest parcel market. Third, revenue from non-top-three customers — this is the proxy for how successfully J&T is reducing platform dependency, and it will determine whether the long-term margin profile of the business looks more like a software company or more like a commodity carrier.

There are second-layer items worth watching that do not fit neatly into the KPI set. The regulatory environment for cross-border e-commerce in the United States, particularly the future of the de minimis exemption that has powered the Temu and Shein flows, is a material overhang. The labor cost trajectory in China continues to grind upward and will eventually pressure the franchisee economics that power the Partner model. The auditor relationship and any disclosure changes in segment reporting are worth monitoring, particularly given the company's relatively short track record as a public reporter. And the personal succession question — what happens to J&T if Li Jie, who controls the votes and embodies the culture, is no longer at the helm — is one that does not have a clear answer in the current disclosures.

What is undeniable, in the final accounting, is the audacity of the project. A man who left a comfortable smartphone job in Jakarta in 2015 has built, in less than a decade, one of the five largest express logistics companies in the world. He has done it by treating logistics not as a truck-and-driver business but as a software-and-scale game. He has done it by leveraging an ecosystem of cousin companies in a way that no Western entrepreneur has fully replicated. He has done it by pricing aggressively when it served his purpose and adapting fast when regulators pushed back. And he has done it while building a company culture that, despite operating in thirteen countries with hundreds of thousands of employees and franchisees, still feels more like a startup than a multinational.

The next decade will tell us whether J&T becomes the logistics backbone of the global south or whether it becomes a cautionary tale about the limits of blitzscale in capital-intensive industries. The early evidence, the financial trajectory, and the underlying ecosystem dynamics all suggest the former is more likely than the latter. But in logistics, as in chess, the position you have built only matters if you can play the next move correctly. Li Jie has so far played them all.

The rabbit, it turns out, is fast for a reason.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube