Hugel: The Botox War & The Billion-Dollar K-Beauty Export

I. Introduction & The "Play"

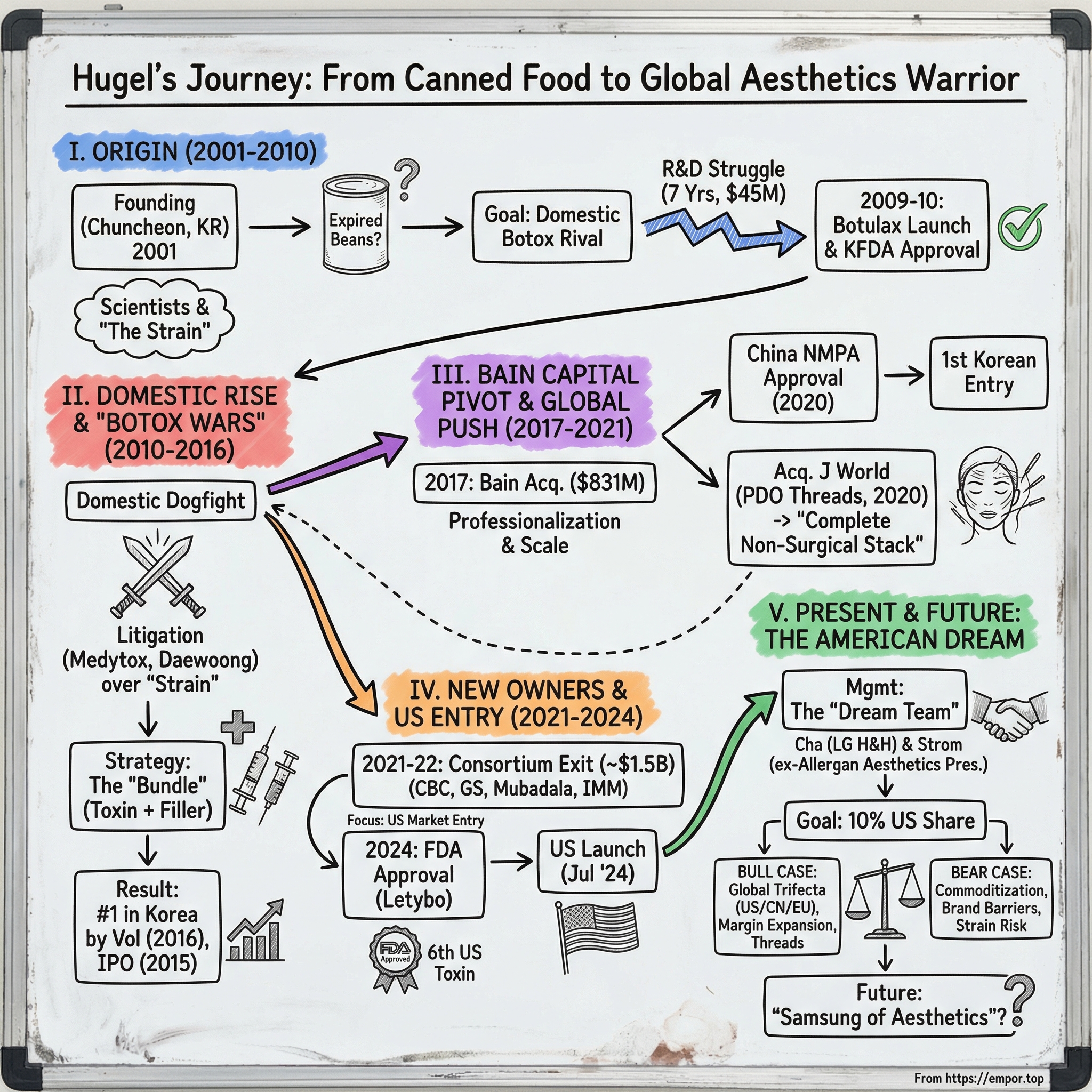

In the summer of 2024, something remarkable happened in the highly regulated world of American aesthetics. A Korean company that most Americans had never heard of received FDA approval to sell botulinum toxin—the same neurotoxin that powers the $4.5 billion Botox franchise—directly into the belly of the beast, competing head-to-head with Allergan on its home turf.

The company was Hugel. And if you're wondering how a firm born in the sleepy provincial city of Chuncheon, best known for its spicy chicken dishes and Olympic ski resorts, managed to crack the most coveted regulatory approval in aesthetics—well, that's exactly the story we're going to tell.

But first, some context on why this matters. South Korea performs more cosmetic procedures per capita than any country on Earth. It's not even close. The aesthetics industry there is what the semiconductor industry is to Taiwan, or what automotive manufacturing is to Germany—a source of deep expertise, relentless competition, and increasingly, global export ambition. Korean clinics pioneered the high-volume, low-cost model for injectables that has since spread worldwide. And at the center of this industry sits Hugel, which rose from scrappy challenger to become the dominant player in the world's most competitive botox market.

The asset itself is elegant in its simplicity. Hugel makes three things: botulinum toxin (sold as Botulax domestically and Letybo globally), hyaluronic acid dermal fillers (The Chaeum), and through its 2020 acquisition of J World, PDO lifting threads. Think of it as the complete non-surgical facelift toolkit. If Botox freezes wrinkles, fillers add volume, and threads physically lift sagging skin—Hugel now owns all three layers of the stack.

The company's journey reads like a Korean drama complete with espionage allegations, corporate warfare, and a parade of private equity owners. There's the founding myth involving expired canned food and bacterial strains. There's the brutal "Botox Wars" where rival companies accused each other of stealing trade secrets in courtrooms from Seoul to Washington. There's Bain Capital's $831 million bet that turned a local champion into a global platform. And there's the star-studded executive team now assembled to storm the American market—including the former president of Allergan Aesthetics itself.

The investment thesis is straightforward: Hugel is one of the only companies on Earth with regulatory approval to sell botulinum toxin in the United States, China, and Europe. That trifecta is extraordinarily difficult to achieve, requiring hundreds of millions of dollars in clinical trials and years of regulatory patience. The barriers to entry are so high that only six botulinum toxin products have ever received FDA approval—and Hugel's Letybo is the newest addition to that exclusive club.

What we'll explore today is whether Hugel can translate its Korean dominance into global leadership. Can a company that perfected the art of low-cost, high-volume aesthetics compete against the marketing might of Allergan and the scientific prestige of Merz? Can the new management team, led by an executive who literally used to run the Botox business, capture meaningful share in a market where brand loyalty runs deep and physicians are notoriously slow to switch? And lurking beneath all of this—the strain question. Where did Hugel's bacteria actually come from? A question that has fueled lawsuits, regulatory investigations, and whispered accusations for over a decade.

Let's begin where all good origin stories do: with scientists who were frustrated enough to start a company.

II. History: Doctors, Debt, and "The Strain" (2001–2010)

In the early 2000s, South Korea's aesthetic medicine industry had a problem. Allergan's Botox, imported from the United States, commanded premium prices that only affluent patients could afford. For doctors like Moon Kyung-hyeop, who saw demand for botulinum toxin treatments exploding but watched most of that economic value flow overseas, the situation seemed absurd. Korea had world-class pharmaceutical manufacturing capabilities. It had the scientific talent. Why couldn't it make its own toxin?

Moon and his co-founders established Hugel in November 2001, not as businessmen chasing a market opportunity, but as scientists and physicians who believed they could solve a technical problem. Their mission was simple in concept and fiendishly difficult in execution: develop a domestically-produced botulinum toxin that could match or exceed the quality of Botox while dramatically undercutting its price.

The challenge they faced goes to the heart of what makes botulinum toxin such a peculiar business. This is not a drug you can synthesize in a laboratory from chemical precursors. Botulinum toxin is a biological product, manufactured by living bacteria. To make it, you need access to a specific strain of Clostridium botulinum—the organism responsible for the deadly disease botulism—and the expertise to cultivate it, extract its toxin, and purify it to pharmaceutical-grade standards. Every company in this industry guards its strain like a state secret, because the strain determines everything: potency, consistency, yield, and ultimately, margins.

This is where the story enters murky territory. The industry's dark secret is that obtaining a Clostridium botulinum strain is both trivially easy and extraordinarily difficult. The bacteria exists throughout the natural environment—in soil, in water, in decaying organic matter. Technically, anyone with basic microbiology skills could isolate a strain from an environmental sample. But finding a strain with the right characteristics for pharmaceutical production? That requires luck, skill, and typically years of screening and optimization.

Hugel's official founding story involves an expired can of beans. The company claims its scientists discovered their proprietary strain in spoiled canned food—a not-implausible origin, since botulism outbreaks have historically been associated with improperly canned goods. Critics, most vocally the rival company Medytox, have alleged something more sinister: that the strain was stolen from competitors or academic laboratories. These accusations would later fuel years of litigation and regulatory investigation, with the matter only fully resolved by a U.S. International Trade Commission ruling in Hugel's favor in October 2024.

Whatever the true origin, Hugel spent seven years and $45 million in R&D before achieving its breakthrough. Seven years of cultivating bacteria, optimizing fermentation conditions, and developing purification processes. Seven years of burning cash with zero revenue. Seven years of watching Medytox, which had beaten them to market, establish itself as the domestic incumbent.

The technical challenge cannot be overstated. Botulinum toxin is the most potent biological substance known to science—a single gram could theoretically kill a million people if properly distributed. Manufacturing it requires navigating biosafety protocols, achieving consistent potency across batches, and purifying the final product to remove proteins that could trigger immune responses in patients. The margin between a therapeutic dose and a toxic dose is razor-thin, and the regulatory bar reflects that danger.

Hugel's scientists focused obsessively on purity. The company's manufacturing process eventually achieved claimed purity levels exceeding 99%, a figure that would become central to its marketing pitch. High purity meant fewer side effects, more predictable dosing, and the ability to compete on quality, not just price.

In 2009, Hugel's persistence paid off. The company launched Botulax, becoming only the second Korean company to bring a botulinum toxin to market. The following year, they secured full KFDA (now MFDS) approval, officially entering a market still dominated by imported Botox and the incumbent Medytox.

The timing could hardly have been better. South Korea was entering what would become a golden age of medical tourism, with patients from across Asia flocking to Seoul for cosmetic procedures. The aesthetic medicine market was growing at double-digit rates, driven by cultural acceptance of cosmetic enhancement and an increasingly sophisticated clinic infrastructure. Hugel had spent nearly a decade preparing for this moment. Now came the hard part: actually winning.

III. The Domestic Dogfight & The Rise to #1 (2010–2016)

When Hugel's Botulax hit the Korean market in 2009, the company faced a competitive landscape that would have discouraged less determined founders. Medytox held the dominant position among domestic producers, having achieved first-mover advantage with its Meditoxin product. And towering above everyone was Allergan's Botox, which commanded premium pricing and the clinical credibility that came from decades of global use.

Hugel's initial strategy was aggressive pricing—entering the market at roughly two-thirds the prevailing cost of Botox procedures. But the founders understood that competing on price alone would be a race to the bottom. They needed to compete on quality and, crucially, on the business model itself.

This is where Hugel's "bundle strategy" emerged, a tactical innovation that would transform how Korean aesthetic clinics operated. Rather than selling toxin as a standalone product, Hugel pushed to sell Botulax alongside The Chaeum, its hyaluronic acid filler line. The pitch to clinic owners was compelling: why manage relationships with multiple suppliers when Hugel could provide your complete injectable portfolio? The bundle approach increased wallet share, created switching costs, and allowed Hugel to offer volume discounts that individual product sales couldn't match.

Think of it as the McDonald's Happy Meal of aesthetic medicine. The customer comes in wanting a burger (toxin for wrinkle relaxation), and leaves with fries and a drink (fillers for volume restoration). The economics work for everyone: the clinic simplifies its supply chain, the patient often adds additional treatments, and Hugel captures more revenue per customer relationship.

By 2012, just three years after launch, Botulax had captured 18% of Korea's neurotoxin market. The trajectory was unmistakable. Hugel was growing faster than the market, and faster than its competitors.

During this period, the Korean botulinum toxin industry descended into what became known as the "Botox Wars"—a period of litigation, accusation, and regulatory maneuvering that made Silicon Valley patent disputes look genteel by comparison. The core issue, as always, was the strain. Medytox alleged that both Daewoong (another Korean competitor) and Hugel had somehow obtained their bacterial strains through improper means. Daewoong claimed its strain came from a barn in Gyeonggi Province. Hugel maintained the canned food story. Medytox believed neither account.

The companies refused to make their strain genetic sequences public, citing trade secret protections. The disputes played out in Korean courts, regulatory proceedings, and eventually in front of the U.S. International Trade Commission. What's remarkable about Hugel's positioning during this period is how effectively the company stayed above the fray. While Medytox and Daewoong engaged in direct legal combat, Hugel kept its head down, focused on execution, and continued taking market share.

By 2015, Hugel had built such momentum that the company pursued an IPO on the KOSDAQ exchange. The listing, completed on December 24, 2015, valued Hugel at levels that reflected investor enthusiasm for the aesthetics sector and confidence in the company's trajectory. Shares initially traded as low as 55,500 KRW in the days following the IPO, but within eight months had soared to nearly 440,000 KRW—an eight-fold increase that signaled the market's recognition of Hugel's growth potential.

The numbers told the story of a company hitting its stride. By 2016, Hugel had overtaken its domestic competitors to become the market leader by volume. The company had achieved what seemed impossible just a decade earlier: displacing both foreign giants and entrenched domestic players to dominate the world's most competitive botulinum toxin market.

How did they do it? Three factors converged. First, product quality—Hugel's emphasis on purity and consistency gave physicians confidence in clinical outcomes. Second, commercial execution—the bundling strategy and aggressive clinic partnerships created a distribution network that competitors struggled to match. Third, timing—Korea's medical tourism boom meant the market was growing fast enough to absorb a new entrant without triggering destructive price wars.

But domestic dominance, while impressive, was always going to be a ceiling. Korea, for all its appetite for aesthetics, is a market of 51 million people. The real prize lay elsewhere: the 1.4 billion consumers in China, the high-margin American market, and the emerging middle classes across Southeast Asia and beyond. Hugel's founders had built something valuable. The question now was whether they could scale it globally—or whether they needed help to do so.

IV. The Bain Capital Pivot (2017–2021)

In April 2017, Bain Capital announced a deal that would fundamentally reshape Hugel's trajectory: the private equity giant would acquire a controlling stake in the Korean company for approximately $831 million. The transaction involved 354.7 billion won for newly issued shares, an additional 100 billion won in convertible bonds, and the purchase of a 24.36% stake held by existing shareholder Dongyang HC. When the dust settled, Bain would control roughly 45% of Hugel and hold full management rights.

At the time, skeptics questioned whether Bain had overpaid. The multiple implied a substantial premium for what was still, fundamentally, a Korean company with limited international presence. But Bain wasn't buying Hugel's current business—they were buying a platform they believed could go global.

The private equity playbook that followed was textbook, but executed with precision. First came professionalization. Hugel's founder-driven management structure gave way to experienced corporate executives. The company brought in professional managers and began building the organizational infrastructure required for global expansion: international regulatory affairs capabilities, global commercial operations, and the compliance systems that multinational markets demand.

Second came operational efficiency. Bain orchestrated the consolidation of Hugel's subsidiary structure, merging previously separate entities like Hugel Pharma and Hugel Meditec into a streamlined organization. The logic was simple: fewer legal entities meant lower overhead, cleaner decision-making, and better margin visibility.

Third—and most importantly—came the global push. Under Bain's ownership, Hugel pursued regulatory approvals with the urgency of a company that understood its competitive window. The China opportunity represented the most immediate prize. China's botulinum toxin market was growing explosively, driven by the same forces that had transformed Korea a generation earlier: rising affluence, cultural acceptance of aesthetic enhancement, and improving clinic infrastructure.

In October 2020, Hugel achieved a milestone that validated the entire Bain thesis: Letybo received approval from China's National Medical Products Administration. Hugel became the first Korean company—and only the fourth globally—to secure regulatory clearance to sell botulinum toxin in China. The approval came through a distribution partnership with Sihuan Pharmaceutical, giving Hugel access to one of the world's fastest-growing aesthetic markets without the capital intensity of building its own commercial infrastructure from scratch.

Simultaneously, Hugel was pursuing the more arduous path to US FDA approval. Between 2015 and 2019, the company conducted Phase III clinical trials—known as the BLESS I, II, and III studies—across 31 sites in the United States and Europe, involving 1,271 patients. The trials targeted the glabellar lines indication, the vertical furrows between the eyebrows that represent the bread-and-butter application for botulinum toxin.

The FDA process would prove longer and more complex than initially hoped. A Complete Response Letter in March 2022 required additional data submission. But the foundation was being laid for what would eventually become the company's most significant market expansion.

What Bain accomplished during this period cannot be reduced to financial engineering. They transformed Hugel from a Korean company with international ambitions into a genuinely global company headquartered in Korea. They installed the management systems, regulatory capabilities, and commercial infrastructure that would make subsequent expansion possible. And they did so while maintaining the operational excellence that had made Hugel successful domestically—the company continued growing market share in Korea even as it pursued international approvals.

The Bain era also saw Hugel's first major acquisition, a deal that would diversify the company's product portfolio and position it uniquely in the global aesthetics market.

V. The "Hidden" Business: J World & Threads (2020)

In November 2020, Hugel announced the acquisition of an 80% stake in J World, a relatively unknown Korean manufacturer of something called PDO lifting threads. The deal received minimal attention at the time—most analysts were focused on Hugel's botox business and the pending China and US approvals. But with hindsight, the J World acquisition may prove to be one of the most strategically important moves in Hugel's history.

To understand why, you need to understand what PDO threads actually do—and why they represent the third leg of a non-surgical facelift stool.

Polydioxanone, or PDO, is a biodegradable material long used in surgical sutures. Someone, likely in Korea where aesthetic innovation happens at breakneck speed, realized that these same sutures could be inserted under the skin of the face to physically lift sagging tissue. Unlike botulinum toxin, which relaxes muscles to smooth expression lines, or fillers, which add volume to replace lost fat and collagen, threads create mechanical tension that pulls tissue upward. The effect mimics what a surgical facelift achieves, without the incisions, general anesthesia, or extended recovery time.

The thread lifting market was growing explosively, particularly in Asia. Procedures that once required surgery could now be performed in a thirty-minute clinic visit. Patients could return to work the same day. The threads themselves gradually dissolve over six to twelve months, during which time the body's healing response deposits new collagen along the thread tracks, providing some lasting benefit even after the material disappears.

J World had developed expertise in manufacturing these PDO threads to pharmaceutical standards—a capability that only a handful of companies worldwide possessed. The company had already obtained CE certification for European sales and was exporting to Japan and Indonesia. By acquiring J World, Hugel accomplished something no competitor had achieved: ownership of the complete non-surgical facial rejuvenation portfolio.

Consider what this means for Hugel's commercial relationships. A clinic owner purchasing Botulax for wrinkle relaxation might also need fillers for volume restoration and threads for mechanical lifting. Each product category has different use cases, but they're often used on the same patient, sometimes in the same treatment session. Hugel can now offer a one-stop solution, simplifying procurement for clinics while maximizing revenue per customer relationship.

The economic characteristics of the thread business are also attractive. Manufacturing threads requires precision but not the biological containment infrastructure that botulinum toxin production demands. Regulatory pathways, while still rigorous, are generally faster and cheaper than those for biologics. Gross margins are healthy, and the market is growing at double-digit rates in most geographies.

Perhaps most importantly, threads represent expansion into a category where Allergan—Hugel's primary global competitor—has limited presence. While AbbVie's Allergan Aesthetics division dominates in toxin and fillers, its thread offering is minimal. The J World acquisition gave Hugel a differentiated product line where it could compete without going head-to-head against the industry giant.

The strategic vision was crystallizing: Hugel wouldn't just be a botox company. It would be the complete medical aesthetics platform, offering physicians everything they needed to treat the aging face without surgery. That positioning would become increasingly important as the company prepared for its next chapter—one that would involve new owners with even more ambitious global plans.

VI. The Exit & The New Owners (2021–2022)

By mid-2021, Bain Capital had held Hugel for four years—a typical holding period for private equity. The company had achieved most of what Bain had set out to accomplish: domestic market leadership was consolidated, China approval was secured, the European footprint was expanding, and the US FDA application was progressing. It was time to exit.

On August 24, 2021, Bain announced the sale of its 46.9% stake—approximately 6.16 million shares—to an unusual consortium of buyers. The group included CBC Group, Singapore's largest healthcare-dedicated investment firm; GS Holdings Corp., one of Korea's major conglomerates with interests spanning energy, retail, and construction; Mubadala Investment Company, the Abu Dhabi sovereign wealth fund; and IMM Investment Corp., a leading Korean investment firm.

The price tag: approximately 1.7 trillion won, or roughly $1.5 billion. For Bain, which had invested approximately $831 million four years earlier, the sale represented a return of roughly 1.8x their invested capital. Solid, if not spectacular—a successful large-cap exit in a sector where Bain had developed deep expertise.

More interesting than Bain's return, however, was the consortium's composition. Each buyer brought something different to the table. CBC Group offered healthcare sector expertise and connections throughout Asia. GS Holdings provided Korean corporate credibility and potential synergies with its diverse business portfolio. Mubadala brought sovereign wealth patient capital and Middle Eastern market access. IMM contributed local investment expertise and Korean regulatory relationships.

The implied valuation—approximately 39x trailing price-to-earnings at the time—looked expensive by conventional metrics. But the consortium wasn't paying for current earnings. They were paying for the China distribution agreement, which was just beginning to ramp, and for the US FDA pipeline, which promised access to the world's most lucrative aesthetic market. They were betting that Hugel's best years were ahead of it.

The deal, however, nearly collapsed before closing.

The drama centered on regulatory concerns that emerged during the due diligence process. Questions arose about indirect export practices and compliance with Ministry of Food & Drug Safety regulations. The Medytox litigation, which had been simmering for years, flared up again when the rival company filed a new complaint with the US International Trade Commission in March 2022, concurrently with the deal's expected closing. Medytox sought an import ban on Hugel products, alleging the same strain theft claims that had been circulating for over a decade.

The consortium had to assess a suddenly complicated risk profile. If the ITC ruled against Hugel, the entire US market opportunity—arguably the primary driver of the acquisition premium—could evaporate. Deal terms were adjusted. Closing dates slipped from the originally anticipated timeline. Lawyers on both sides worked to structure protections against various adverse outcomes.

Ultimately, the consortium's conviction held. The transaction closed on April 29-30, 2022, transferring control of Hugel to its new ownership group. The buyers were betting that Hugel would prevail in its regulatory and legal battles, and that the underlying business fundamentals—strong domestic position, growing international sales, pending US approval—would deliver returns worthy of the premium they had paid.

What followed would prove their thesis correct—though not without additional challenges along the way.

VII. Current Management & The American Dream (2024–Present)

The consortium that acquired Hugel in 2022 understood something fundamental: conquering the American market would require American expertise. Korean manufacturing excellence and Asian market dominance could only take the company so far. To compete against Allergan in its home territory, Hugel needed executives who understood American healthcare, American physicians, and American patients.

In March 2023, the company appointed Suk-yong Cha as Executive Chairman and Chairman of the Board. Cha's credentials were impeccable: he had served as CEO of LG H&H, the Korean cosmetics and household products giant, for eighteen years, during which he achieved an almost unprecedented record of seventeen consecutive years of increasing sales and operating profit. He brought credibility, operational discipline, and experience managing global consumer brands.

But the real signal of Hugel's US ambitions came in October 2025, when the company announced that Carrie Strom would join as Global CEO and President.

Strom's background reads like a strategic asset tailor-made for Hugel's needs. From May 2020 through 2025, she served as Senior Vice President at AbbVie and President of Global Allergan Aesthetics—meaning she was the person responsible for the worldwide Botox Cosmetic, Juvederm, Kybella, CoolSculpting, SkinMedica, and Latisse franchises. Before that, she was Senior Vice President of US Medical Aesthetics at Allergan, the role directly responsible for American Botox sales.

Strom had spent over a decade at Allergan, starting in 2011 when Botox was already well-established and helping drive the brand's continued growth. Prior to Allergan, she spent more than ten years at Pfizer, where she led marketing for Lipitor—one of the best-selling pharmaceutical products in history. Her academic background includes a BA in Communications from the University of Colorado Boulder, and her professional network spans the aesthetic medicine industry.

When Hugel hired Strom, they weren't just bringing in expertise—they were hiring institutional knowledge of exactly how Allergan operates, what physicians value, and where competitive vulnerabilities might exist. The message to the market was unmistakable: Hugel was serious about the US, and they had recruited one of the industry's most accomplished commercial leaders to prove it.

The path to this moment had required navigating significant obstacles. Hugel's FDA application received its first Complete Response Letter in March 2022, requiring additional data. After resubmission in October 2022, a second Complete Response Letter arrived in April 2023, this time related to manufacturing facility issues identified during FDA inspection. The company invested in facility improvements, addressed the agency's concerns, and continued pushing forward.

On February 29, 2024, persistence finally paid off. The FDA approved Letybo (letibotulinumtoxinA-wlbg) for the treatment of moderate-to-severe glabellar lines in adults. Hugel's product became only the sixth botulinum toxin to receive FDA approval—joining Botox, Dysport, Xeomin, Jeuveau, and Daxxify in the exclusive club of US-approved neuromodulators.

Commercial launch followed quickly. In July 2024, Hugel announced a US distribution partnership with BENEV Company, Inc., and Letybo reached American clinics by the end of that month. The company articulated an ambitious goal: capture 10% of the US market within three years.

That target deserves scrutiny. The US aesthetic botulinum toxin market generates billions in annual revenue, with Allergan's Botox Cosmetic commanding roughly three-quarters of the market. Achieving 10% share would mean displacing hundreds of millions of dollars of incumbent sales—no small feat in a market where physician habits are sticky and patient brand awareness runs high.

To incentivize the management team to deliver, Hugel's board approved aggressive stock option programs in 2025. The company is effectively betting its equity value on US growth, aligning management compensation with shareholder interests in the most direct way possible.

The dual CEO structure that emerged—with Daniel Chang leading Korea and Asian operations while Strom drives global expansion—reflects the balance Hugel must strike. Korea remains the cash cow, generating the profits that fund international expansion. But the company's future valuation depends almost entirely on its ability to penetrate markets where Korean brand recognition means nothing and execution must speak for itself.

VIII. Power Analysis: Moats, Forces, and Competitive Position

To understand Hugel's strategic position, it helps to examine the company through multiple analytical lenses. Let's start with Michael Porter's Five Forces framework before turning to Hamilton Helmer's 7 Powers.

Competitive Rivalry: Intense and Personal

The botulinum toxin industry is a knife fight disguised as a pharmaceutical business. Allergan, with its Botox franchise generating over $4.5 billion in annual revenue and roughly 78% global market share, dominates from the top. Ipsen's Dysport and Merz's Xeomin compete for the remainder alongside newer entrants like Evolus's Daxxify and Daewoong's Jeuveau. In Korea specifically, Hugel faces Medytox, Daewoong, and a growing roster of smaller competitors—more than ten companies now participate in the Korean neuromodulator market.

The rivalry extends beyond normal competitive dynamics. The Medytox litigation that has pursued Hugel across multiple jurisdictions represents the kind of sustained corporate warfare rare in most industries. Though Hugel prevailed in the October 2024 ITC ruling, the history of strain disputes suggests legal risk may never fully disappear in this sector.

Barriers to Entry: Formidable

This is where Hugel's position becomes compelling. Achieving FDA approval for a botulinum toxin requires five to seven years of clinical development and hundreds of millions of dollars in investment. Only six products have ever cleared this bar. The regulatory moat is nearly insurmountable for new entrants, protecting incumbent margins even as competition intensifies within the existing player set.

Manufacturing barriers are equally significant. Producing pharmaceutical-grade botulinum toxin requires specialized biosafety infrastructure, deep process expertise, and consistent quality systems that take years to develop. The margin between success and failure in biological manufacturing is razor-thin; batch consistency determines commercial viability.

Supplier Power: Moderate

Hugel controls its own bacterial strains and manufacturing processes, limiting upstream dependencies. Raw material inputs for biological production are generally commoditized. The J World acquisition further reduced supplier exposure by bringing thread manufacturing in-house.

Buyer Power: Growing

This represents Hugel's greatest structural challenge. In Korea, botulinum toxin has effectively become commoditized, with treatment prices as low as $100-300 per session and per-unit costs of $5-7. Clinics operating on thin margins exert significant pricing pressure, and switching between suppliers requires minimal effort for adequately trained injectors.

The US market offers temporary respite: per-unit prices of $12-20 or more, and per-session costs of $350-900, provide substantially higher margins. But the Korean precedent suggests what could happen globally as competition intensifies.

Threat of Substitutes: Limited Near-Term, Uncertain Long-Term

For now, botulinum toxin has no close substitute for temporary muscle relaxation. Alternative wrinkle treatments—topical retinoids, laser resurfacing, radiofrequency devices—address different aspects of facial aging and typically complement rather than replace injectable neuromodulators. Surgical facelifts serve different patient populations with different risk tolerance.

The longer-term question is whether new modalities could disrupt the toxin paradigm. Gene therapies, novel peptides, or entirely new approaches to muscle relaxation represent theoretical threats, though none appear commercially imminent.

Now consider Hamilton Helmer's 7 Powers framework:

Process Power emerges as Hugel's most defensible advantage. Manufacturing botulinum toxin is extraordinarily difficult—biological variation, purification challenges, and quality control requirements create substantial know-how barriers. Hugel's claimed 99%+ purity levels represent accumulated process knowledge that competitors cannot easily replicate. This "secret sauce" in manufacturing translates directly to margin advantages and product reliability.

Scale Economies flow from Hugel's Korean dominance. The company operates in the world's highest per-capita market for aesthetic procedures, providing volume that drives unit costs below levels achievable by smaller players. This domestic scale advantage enables competitive pricing in export markets without sacrificing profitability.

Cornered Resources include Hugel's specific bacterial strains and, increasingly, its regulatory licenses. The FDA approval represents a resource that required years and hundreds of millions of dollars to obtain—and that cannot be acquired through any alternative means. Similarly, the China NMPA approval and European authorization constitute regulatory assets that competitors must duplicate independently at similar cost and time investment.

Network Effects are limited in this industry—toxin usage by one physician doesn't directly increase value for others. However, clinical experience and injection technique training create soft network effects: physicians trained on Botulax in Korea may prefer continuing with Letybo when practicing elsewhere or treating international patients.

Switching Costs exist but are modest. While physicians develop muscle memory with specific products and dosing protocols, conversion between brands is technically straightforward. This limits Hugel's ability to extract premium pricing from existing customers but also means competitor entrenchment is equally vulnerable.

Brand remains Allergan's most powerful asset. Botox has achieved near-universal name recognition—patients ask for "Botox" generically, regardless of actual product used. Hugel must overcome this brand deficit through clinical results, pricing advantages, and physician education.

IX. Bear vs. Bull & Conclusion

The Bear Case

The most concerning long-term threat to Hugel isn't competition—it's commoditization. In Korea, where the aesthetic market is most mature, botulinum toxin has become almost fungible. Per-unit prices of $5-7 and procedure costs of $100-300 reflect a market where brands matter less than availability and convenience. If global prices converge toward Korean levels, the high-margin American opportunity that underpins Hugel's current valuation could prove ephemeral.

The arithmetic is sobering. Today, a vial sold in the US generates five to ten times the margin of the same vial sold in Korea. That differential reflects American pricing power, brand premiums, and a market still dominated by physician loyalty to established products. But every new FDA approval—and there are now six competing toxins—erodes that pricing power incrementally. As more options become available, payors push harder on reimbursement, clinics comparison shop more aggressively, and consumers grow more price-conscious.

There's also the strain risk that never quite disappears. While Hugel prevailed in the October 2024 ITC ruling, the pattern of litigation in this industry suggests legal challenges may resurface. The origin of bacterial strains remains contested across multiple companies, and the precedent of Medytox's successful enforcement action against Daewoong—which resulted in a 21-month import ban before eventual reversal—demonstrates real commercial consequences can flow from these disputes.

Finally, there's the execution risk inherent in any US market entry. Allergan has spent decades building physician relationships, training injectors, sponsoring conferences, and establishing clinical education programs. Botox's brand recognition extends beyond physicians to patients themselves—it's one of the rare pharmaceutical products that consumers actively request by name. Overcoming that incumbent advantage requires sustained investment, flawless execution, and patience that shareholders may not provide.

The Bull Case

Start with the demand environment. The "Lipstick Effect"—the observation that affordable luxury purchases often increase during economic downturns as consumers trade down from larger indulgences—applies with particular force to aesthetics. Historical data suggests that Botox procedures prove remarkably resilient through recession cycles. People may defer a new car or vacation, but they continue maintaining their appearance. This demand durability provides baseline protection even in adverse economic scenarios.

Then consider Hugel's unique geographic positioning. The company holds regulatory approval to sell botulinum toxin in the United States, China, and Europe—a trifecta that only a handful of competitors can claim. China alone represents a market growing at double-digit rates, with penetration levels far below Korean precedents. The joint venture with Sihuan Pharmaceutical provides distribution without capital intensity. Every year that Chinese consumers grow more familiar with aesthetic procedures represents potential revenue growth for Hugel.

The margin expansion story is compelling. If Hugel achieves even modest US market share, the financial impact is transformative. Consider: a single vial sold in America at $12-20 per unit generates margins comparable to several vials sold domestically. The company's 2025 financial results—record sales of 425.1 billion KRW, up 14% year-over-year, with operating profit of 201.6 billion KRW, up 21%—demonstrate operational leverage that could accelerate dramatically with US revenue contribution.

The management team assembled for US expansion brings unusual credibility. Carrie Strom literally ran the Botox business; she understands what drives physician adoption, where competitive vulnerabilities exist, and how to position against her former employer. Executive Chairman Suk-yong Cha brings proven operational excellence from his LG H&H tenure. The combination of American commercial expertise with Korean manufacturing discipline could prove formidable.

Finally, the thread business acquired through J World provides growth optionality often overlooked in Hugel analyses. PDO lifting threads represent a product category growing faster than traditional injectables in many markets, with lower regulatory barriers and limited competition from Allergan. As Hugel's international distribution expands, threads provide incremental revenue opportunity without requiring additional regulatory investment.

Key Performance Indicators

For investors tracking Hugel's execution, three metrics warrant close attention:

US Revenue Growth Rate: The company's stated goal of 10% US market share within three years translates to specific revenue milestones. Quarterly US sales figures will indicate whether Letybo is gaining traction or struggling against incumbent resistance. The trajectory matters more than any single quarter—sustained sequential growth would validate the investment thesis, while stagnation would raise questions about ultimate addressable opportunity.

China Revenue Contribution: The Sihuan partnership began revenue recognition in late 2020. Year-over-year growth in Chinese sales indicates both market expansion and Hugel's ability to capture share. China represents the swing variable that could drive long-term valuation; deteriorating growth there would signal significant risk to the bull case.

Geographic Revenue Mix: As international sales grow relative to Korean domestic revenue, margin characteristics should shift. Monitoring the quarterly progression of export versus domestic contribution provides insight into Hugel's transformation from Korean champion to global player.

Final Thought

Is Hugel the "Samsung of Aesthetics"—a Korean company that mastered manufacturing excellence domestically before conquering global markets through quality, scale, and relentless execution?

The parallel is tempting but imperfect. Samsung succeeded in categories where technology leadership and manufacturing prowess could overcome brand deficits. Semiconductors and displays are fundamentally commodities where buyers optimize for specification and price. Aesthetics is different. Physicians prescribing botulinum toxin rely on clinical experience, training history, and trust relationships that develop over years. Patients asking for Botox by name won't easily switch to alternatives they've never heard of.

Yet Hugel's strategic position contains elements Samsung would recognize: world-class manufacturing capability, cost structure advantages from domestic scale, and regulatory assets that took years and hundreds of millions of dollars to accumulate. The company has assembled a management team that combines Korean operational discipline with American commercial expertise. It has secured approvals in the world's three largest aesthetic markets. And it has positioned itself as the only player offering the complete non-surgical facelift stack—toxin, filler, and threads in one portfolio.

Whether that positioning translates to global leadership remains to be determined. What's certain is that the company born from expired canned food and scientific stubbornness in sleepy Chuncheon has accomplished something remarkable: it has earned the right to compete for the global aesthetics crown. The next few years will reveal whether Hugel can seize that opportunity—or whether the Botox empire proves more durable than the challengers from Korea hoped.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube