DPC Dash: The Tech-Enabled Delivery Phenomenon Rebuilding Domino's in China

I. Introduction & Episode Roadmap

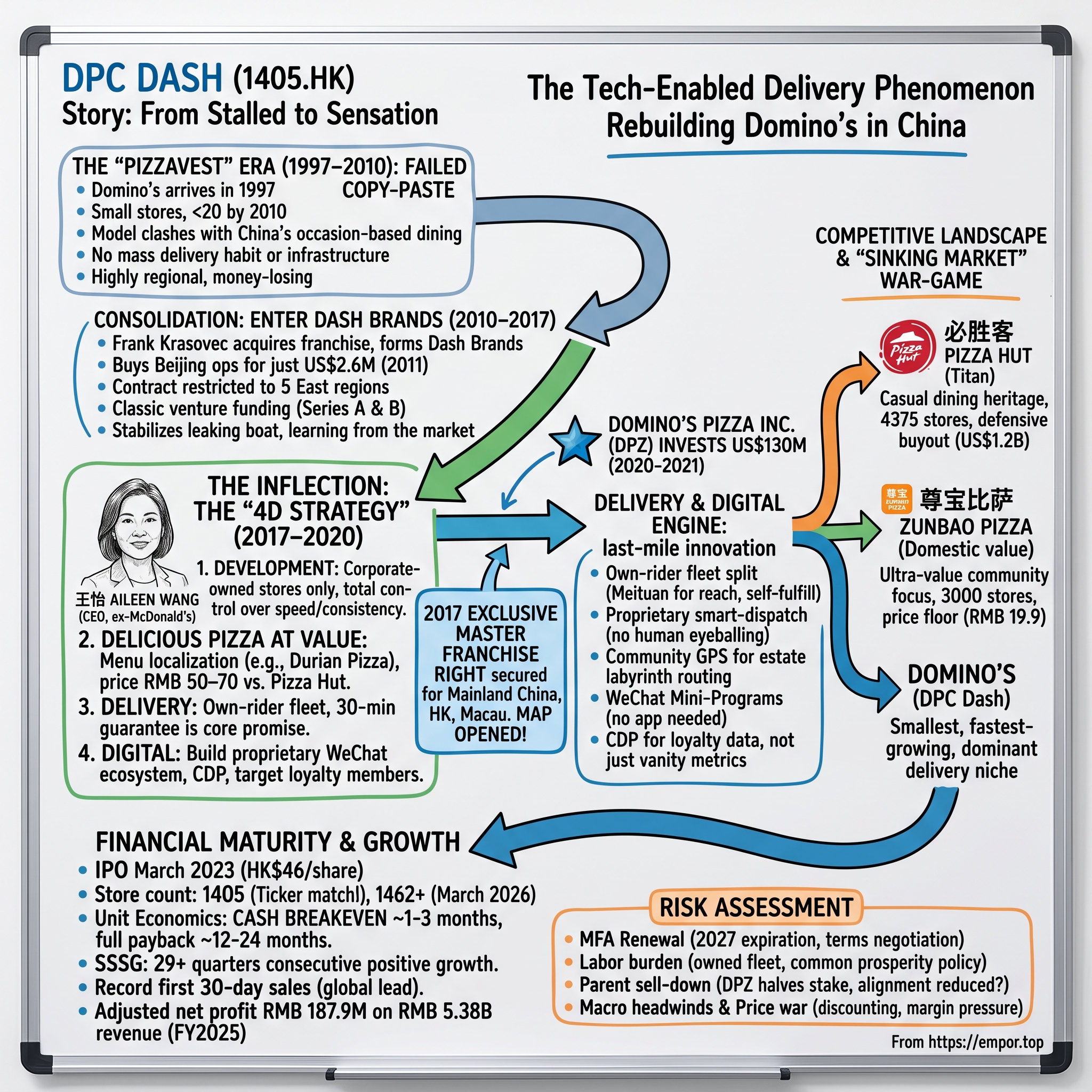

Picture a Domino's storefront tucked into the ground floor of a Shanghai office tower in 2015. It is small, fluorescent-lit, and mostly empty. A couple of expatriates wander in for a familiar taste of home. The pizza is fine. The brand is invisible. For nearly two decades, this was the entire story of Domino's in the world's largest consumer market — a Western fast-food name that arrived in 1997, planted a few flags, and then essentially stalled. While 必胜客 Pizza Hut built hundreds of polished, table-service restaurants across China and turned pizza into an aspirational night out, Domino's languished with fewer than two dozen stores and a reputation, where it had one at all, as the also-ran.

Now fast-forward. In January 2026, the company that operates Domino's in China cut the ribbon on its 1,405th store — a number it celebrated precisely because it matched its own Hong Kong stock ticker, 1405.HK.[^1] By March 2026 the count had climbed past 1,462 outlets,[^2] and the business had just posted its 29th-plus consecutive quarter of positive same-store sales growth — a streak that, in a global restaurant industry where two or three good years is considered a hot hand, borders on the absurd.[^3] DPC Dash stores routinely seize the top spots in the entire 22,000-store global Domino's system for first-30-day sales. The sluggish regional also-ran had become, by several measures, the fastest-growing pizza chain on the planet.

The subject of this episode is 达势股份有限公司 DPC Dash Ltd (HKEX: 1405.HK), the exclusive master franchisee of the Domino's Pizza brand across Mainland China, Hong Kong, and Macau. And the central paradox is this: DPC Dash won by leaning into exactly the thing that supposedly doomed Domino's in China for twenty years. Western quick-service restaurants were "supposed" to succeed in China by going premium and experiential — big rooms, full menus, dine-in occasions. Domino's, built globally on cramped delivery-first storefronts and a 30-minute promise, looked structurally mismatched to that thesis. The reality of the last decade is that the thesis itself was wrong, or at least it expired. As China's delivery ecosystem exploded and a younger, mobile-native consumer emerged, the very "weakness" of the Domino's model — speed, convenience, low overhead, delivery to your door — became the wedge.

This is a story about what changes when a tired playbook meets the right market at the right moment, and the right operator to exploit it. So here is the roadmap.

We will start with the "Pizzavest" Era (1997–2010), the copy-paste failure that proved a mature Western operating manual doesn't survive contact with an emerging market. Then the Dash Brands consolidation (2010–2017), where a Texan entrepreneur bought the wreckage cheap and spent seven years grinding. Then the genuine inflection: the 2017 pivot under 王怡 Aileen Wang and her "4D Strategy," the moment the company stopped being a restaurant chain and started behaving like a logistics-and-data company that happens to sell pizza. We will go deep on the delivery and digital engine — the own-rider fleet, the smart-dispatch algorithms, the WeChat loyalty machine — because that is where the real moat, if there is one, actually lives. We will war-game the competitive landscape against Pizza Hut and 尊宝比萨 Zunbao Pizza. We will work through financial maturity and the 2023 IPO, the unit economics, and the margin debates. And finally we will run the whole thing through an activist stress test and the strategy frameworks — Hamilton Helmer's 7 Powers and Porter's Five Forces — to separate the durable advantages from the management narrative.

Because the question that matters for a long-term investor is not "did DPC Dash grow fast?" It plainly did. The question is whether the engine that produced that growth is defensible, repeatable in smaller cities, and resilient to a Chinese consumer who is suddenly, aggressively trading down. Let's find out.

II. The "Pizzavest" Era: High Friction, Low Growth (1997–2010)

In 1997, the same year Hong Kong returned to Chinese sovereignty and the Asian financial crisis began rippling across the region, a Domino's Pizza sign went up in mainland China for the first time. The vehicle was Pizzavest China Ltd, a Taiwanese-owned master franchisee that held the rights to bring the brand into the country.1 The ambition, in theory, was obvious: China's cities were urbanizing fast, a middle class was forming, and Western fast food was the shiny new thing. KFC had arrived in 1987 and was already a phenomenon. McDonald's followed in 1990. Pizza Hut was busy turning itself into a sit-down institution. Surely there was room for the planet's largest pizza-delivery brand.

There was not — at least not yet, and not in the form Domino's brought. To understand why the next thirteen years were a slow-motion stall, you have to understand how profoundly the global Domino's model clashed with the China of that era.

Domino's worldwide was, and is, an engineering company disguised as a pizza chain. Its entire economic logic rests on a tight, low-overhead, delivery-centric format: small footprints in cheap real estate, a kitchen optimized for throughput, riders out the door in minutes, and a brand promise built around speed — most famously the 30-minute delivery guarantee. It is takeout and delivery first, dine-in barely an afterthought. That model is gorgeous when two conditions hold: customers want food delivered quickly to their homes, and the infrastructure exists to do it — addressable streets, reliable phones, a culture of ordering in.

China in the late 1990s and 2000s had almost none of that for a Western brand. Home delivery of restaurant food was not yet a mass habit; the smartphone-and-app delivery revolution was a decade away. More fundamentally, the cultural meaning of a Western restaurant was inverted. Eating at KFC or Pizza Hut was not a grab-a-quick-bite act of convenience — it was an occasion, a slightly aspirational outing, a clean and modern room where you sat down, lingered, maybe celebrated a child's birthday. Pizza Hut understood this perfectly and ran with it, positioning itself as a polished casual-dining destination with large layouts, table service, and a sprawling high-margin menu of pasta, steak, appetizers, and desserts. Pizza, in the Chinese imagination of that period, was something you went out for and sat down to enjoy.

Domino's showed up selling the opposite: a small box, handed to a delivery rider, eaten on your couch. The format was solving a problem most Chinese consumers didn't yet feel they had. The product itself — a relatively plain American pizza — competed poorly on the dine-in dimension where the category's energy actually was, and the delivery dimension where Domino's was strong barely existed as a market.

The result was a grind. Under Pizzavest, Domino's opened fewer than twenty stores across roughly thirteen years — a glacial pace for a market this size.1 The footprint was highly regionalized, concentrated in pockets of Beijing and Shanghai where expatriates and a thin slice of cosmopolitan locals provided just enough demand to keep the lights on. Brand recall outside those circles was negligible. And the stores were not making money. This was not a beachhead being patiently expanded; it was a business treading water.

The strategic lesson here is one Acquired listeners will recognize from a dozen other cross-border stories, and it is worth stating plainly because it sets up everything that follows: a mature operating playbook, however brilliant in its home market, is not portable by default. Domino's global manual assumed delivery demand, delivery infrastructure, and a consumer who valued speed over experience. Drop that manual into a market where none of those conditions held, run it without deep structural localization, and you get exactly what Pizzavest got — a slow, unprofitable burn. The model wasn't wrong. It was early, and it was un-localized. Someone would eventually have to either wait for China to come to the model or rebuild the model for China. For now, the franchise just needed an owner willing to absorb the losses long enough to find out which. That owner was about to arrive — and he came not from the restaurant world, but from Texas.

III. Consolidation and Reorganization: Enter Dash Brands (2010–2017)

In December 2010, a consortium led by an American entrepreneur named Frank Paul Krasovec acquired the Domino's China master franchise, and the entity that would eventually become DPC Dash — Dash Brands Ltd — was born.1 Krasovec was not a pizza man by trade. He was a businessman and investor with a portfolio of interests, backing the deal through a family-trust structure, Good Taste Limited, linked to his Ocean Investments vehicle.1 What he saw in a money-losing, sub-twenty-store franchise that had gone nowhere for over a decade was not the present — it was an option on China's future quick-service boom, available for almost nothing.

And "almost nothing" is close to literal. Shortly after taking the master rights, Dash Brands moved to consolidate the operating heart of the business: in 2011 it spent roughly US$2.6 million to purchase Beijing Pizzavest Fast Food Co., Ltd. — the Beijing Domino's operating company — from the Jinghua Hotel Group.1 Step back and weigh that number. Two-point-six million dollars to control the Beijing operations of a global brand in what everyone already understood would become one of the most important consumer cities on earth. As an entry price, it was asymmetric to the point of being a lottery ticket: tiny downside in absolute dollars, enormous theoretical upside if the China QSR market did what the bulls expected.

But cheap is cheap for a reason, and the asymmetry cut both ways. The Beijing stores Dash Brands inherited were deeply unprofitable, carrying years of operational baggage. Fixing them meant real capital and real time. And the master franchise agreement itself came with a hard ceiling on ambition: it covered only five geographic regions — Beijing, Tianjin, Shanghai, Jiangsu, and Zhejiang.1 In other words, the company that would one day brand itself the exclusive franchisee for all of Greater China was, in 2011, contractually boxed into a cluster of eastern provinces and two municipalities. You could not have built a national champion on those rights even if you'd wanted to. The geography of the contract capped the size of the dream.

So the early-2010s chapter is best understood not as expansion but as stabilization — keeping a leaky boat afloat while raising enough capital to slowly patch it. Dash Brands ran a classic venture-style financing cadence to fund the grind: a US$2.9 million Series A in 2008 and a US$14.0 million Series B in 2011.1 These are small numbers by the standards of what would come later, and that smallness tells you something honest about the period: nobody was throwing hyper-growth money at this business, because it had not yet earned it. The company opened roughly twenty stores a year — respectable, steady, unremarkable — and crept toward the 100-store mark by early 2017.1

Here is the analytical point that matters for an investor reading the later fairy tale backward. The 2010–2017 stretch produced almost none of the explosive growth DPC Dash is now known for, and it would be easy to dismiss it as dead years. That misreads it. What this period actually accomplished was unglamorous but essential: it put the franchise into the hands of a committed, long-horizon owner; it consolidated fragmented operations under one roof; it kept the brand alive and learning through a market that wasn't ready for it; and — crucially — it built the relationship and the credibility with the global parent that would later be needed to renegotiate the territorial rights. None of that shows up in a same-store-sales chart. All of it was a precondition for what came next.

Because the thing the slow years could not fix were the two structural constraints baked into the franchise: the geographically restricted contract, and the absence of an operator who could rebuild the model for the China that was finally emerging — a China where, by the mid-2010s, smartphones were ubiquitous, 美团 Meituan and 饿了么 Ele.me were turning food delivery into a daily reflex, and a generation of young urban consumers had stopped treating Western fast food as a special occasion. The market was at last arriving at the doorstep of the Domino's model. What the company needed was someone who could see that, and the leverage to act on it. In May 2017, both arrived at once.

IV. The Inflection: The "4D Strategy" & National Expansion (2017–2020)

When 王怡 Aileen Wang walked into Dash Brands as CEO in May 2017, she inherited a hundred-store regional pizza company that had spent seven years climbing a wall.[^5] She did not come from inside it, and that was the point. Wang's pedigree was operational and large-scale: she had served as Vice President of Franchising at McDonald's China, one of the most demanding restaurant-operations schools on earth, where the entire job is making thousands of outlets run with machine-like consistency.[^5] She arrived with a McDonald's-grade obsession for systems, speed, and unit economics — and a conviction that Domino's problem in China had never been the model, only the execution and the moment.

Wang moved quickly to remake the company's metabolism. She replaced much of the legacy management team and set about converting the culture from a sleepy regional restaurant chain into something closer to a technology-driven logistics operation — fast, data-instrumented, expansion-hungry.[^5] But culture change is hollow without the right to actually grow, and the single most important thing Wang did in her first months had nothing to do with pizza recipes. It was a contract.

In June 2017, Wang and Krasovec sat across from Domino's Pizza International and renegotiated the master franchise agreement.1 The old deal, recall, locked the company into five eastern regions. The new one blew the ceiling off: DPC Dash secured the exclusive franchise rights for the entirety of Mainland China, Hong Kong, and Macau.1 In a single stroke, a regional operator became the national — indeed Greater-China — steward of the Domino's brand. This was the legal precondition for everything the company is today. You cannot "go broader and go deeper" across a country when your contract stops at a provincial border. Now the map was open.

With the territory unlocked, Wang installed the strategic blueprint that has defined the company ever since — the "4D Strategy." It is worth walking through each D, because together they explain both the growth and the risks.

Development was the commitment to scale through corporate-owned stores, with no sub-franchising. This is a more capital-intensive path than the asset-light franchising model Domino's uses in much of the world, and it deserves scrutiny rather than applause: owning every store means the company eats all the build-out CAPEX and all the operating risk itself. But it also means DPC Dash captures one hundred percent of store-level operating margin instead of skimming a franchise royalty, and — arguably more important in a brand-sensitive market — it retains total control over consistency, service, and the customer experience. For a company whose entire promise is speed and reliability, refusing to let third-party franchisees dilute the operation was a deliberate trade of capital efficiency for control.

Delicious Pizza at Value was the menu localization, and this is where DPC Dash earned its folklore. The company built pies engineered for the Chinese palate — Teriyaki Beef, Peking Duck, and above all the now-legendary 苏丹王黄金果肉榴莲比萨 Durian Pizza, a gooey, pungent, love-it-or-flee-it creation that became a genuine social-media phenomenon and a brand signature.[^5] Just as important as the toppings was the pricing: average tickets were kept in the roughly RMB 50–70 band, deliberately undercutting Pizza Hut's more premium RMB 70–100 positioning.[^5] The strategic message was clear — Domino's would not try to out-fancy Pizza Hut; it would be the faster, cheaper, more convenient option that still felt like a treat.

Delivery was the re-engineering of the last mile around the strict 30-minute guarantee — the operational core we will dig into in the next section. And Digital was the deliberate migration of customers off third-party platforms and into DPC Dash's own digital ecosystem, chiefly via WeChat. Taken together, the four Ds describe a company trying to own its growth, its product, its logistics, and its customer relationship — to internalize as much of the value chain as a restaurant reasonably can.

Did it work? The market's most credible validator thought so. Between roughly 2020 and 2021, Domino's Pizza Inc. (DPZ) — the global parent — made a rare and telling move: it put US$130 million of its own equity into DPC Dash across three rounds.1 Step back and consider how unusual this is. A global franchisor's whole financial design is to be capital-light, collecting royalties without owning operating risk in local markets. For DPZ to write a nine-figure direct equity check into one of its master franchisees was an explicit statement that something exceptional was happening on the ground in China — strong enough same-store-sales momentum to override the parent's instinct to stay asset-light. It validated the model globally and, just as practically, it handed DPC Dash the balance-sheet firepower to fund hyper-growth without immediately tapping public markets.

The honest caveat, which we will return to, is that a parent's enthusiasm at the moment of acceleration tells you about the past, not the future — and DPZ's later behavior with that same stake would raise a very different question. But in 2020, the signal was unambiguous: the pivot was working, the engine was lit, and the thing actually powering it was sitting in the third D. It is time to open the hood on delivery.

V. The Delivery & Digital Engine: Re-engineering the Last Mile

Here is where the pizza company stops being a pizza company. If you want to understand why DPC Dash compounds the way it does — and where its real, if contestable, moat lives — you have to look not at the ovens but at the riders, the algorithms, and the little green WeChat windows where the orders are born.

Start with how much delivery actually matters. In mature Tier-1 cities like Beijing and Shanghai, delivery accounts for the dominant share of the economics — on the order of 76.2% of revenue.2 This is not a restaurant with a delivery side hustle. It is a delivery business with a kitchen attached. And once you accept that framing, the company's most counterintuitive decision starts to make sense.

In China, the obvious, cheap, "everyone does it" way to deliver food is to plug into the crowdsourced gig fleets of the big platforms — let 美团 Meituan and 饿了么 Ele.me dispatch their oceans of riders to ferry your pizza. DPC Dash refused. The company runs its own dedicated rider fleet, with riders stationed at specific stores, employed within the system rather than summoned from a gig pool.2 To hit a 30-minute guarantee — with the company reporting that the large majority of orders land within roughly 24 to 30 minutes — you cannot rely on a freelance rider who might be carrying a bubble-tea order and two hotpots in the same run and who has no particular loyalty to your brand promise.2 Speed and consistency at that tolerance require control, and control means owning the fleet.

But notice the clever hybrid in how DPC Dash relates to the aggregators. It still lists on Meituan and Ele.me — because that is where the traffic is, and refusing to appear there would be like refusing to be findable on the internet. What it does not do is let those platforms fulfill the delivery. The customer may discover and order through an aggregator, but a Domino's own-rider carries the box.2 This split — use the platforms for reach, keep the last mile in-house — does two things at once. It shields the brand from the punishing commission rates that aggregator fulfillment extracts from most restaurants, and it preserves total control over the single most emotionally charged moment of the transaction: the knock on the door. The flip side, which we will weigh later, is that an owned fleet converts a variable, outsourced cost into a large fixed labor commitment — a genuine vulnerability if China's labor regulations tighten.

Now the brains. A delivery fleet is only as good as the system that tells it what to do. DPC Dash licenses Domino's global point-of-sale platform, PULSE, from the parent, but localized it and built a proprietary data-driven smart-dispatch layer on top.2 The plain-English version: when an order comes in, an algorithm — not a human dispatcher eyeballing a whiteboard — decides which rider takes it, when, and on what route, balancing oven timing, rider location, and traffic so that pies leave hot and arrive on time. Layered onto that is what the company calls Community GPS routing, a piece of engineering aimed squarely at a peculiarly Chinese problem: the country's high-density residential estates are mazes. A single address can mean a sprawling compound with a dozen towers, confusing internal roads, and gates a scooter can't pass. Standard map navigation gets a rider to the front gate and abandons them; Community GPS is designed to guide them the last few hundred meters through the labyrinth to the right building and door.2 It is an unglamorous, deeply local optimization — exactly the kind of thing that is invisible to customers, brutal to replicate at scale, and decisive in whether you hit thirty minutes or forty.

Then the demand engine. DPC Dash pulled ordering directly into 微信小程序 WeChat Mini-Programs — the embedded mini-apps inside China's dominant super-app — so that ordering a pizza is a frictionless tap inside the app where Chinese consumers already live, with no separate download required.[^7] Behind it sits a Customer Data Platform that, by early 2026, had grown to 38.8 million active loyalty members.[^3] That membership base is the real point. It is not a vanity metric; it is a proprietary, first-party data asset. Every order teaches the system who buys what, when, and how often — which feeds targeted promotions, drives repeat purchase, and reduces dependence on buying traffic from third parties at full price. In a market where most restaurants are renting their customer relationships from Meituan, DPC Dash spent years building its own.

So step back and assemble the machine. Owned riders provide speed and control. Smart dispatch and Community GPS provide efficiency and on-time reliability at scale. The WeChat ecosystem and loyalty data provide demand, repeat purchase, and cheaper customer acquisition. Each piece reinforces the others — and crucially, each piece gets better as store density rises, because more stores in a city means shorter routes, faster delivery, more orders, and more data. That flywheel is the strongest candidate for a genuine, durable advantage in this whole story. Whether it constitutes a real moat or merely a hard-to-copy operational lead is a question best answered by looking at who is trying to copy it — which brings us to the battlefield.

VI. The Competitive Landscape: Pizza Hut vs. Domino's vs. Zunbao

Imagine the Chinese pizza market as a three-sided chessboard, each player attacking from a different corner with a fundamentally different weapon. By 2024 that board had grown to roughly RMB 48 billion (about US$6.6 billion) in annual value, with online delivery already representing over 58% of all industry transactions — a structural fact that tilts the whole game toward whoever does delivery best.[^8] Let's meet the three players, because their differences are the entire strategic story.

In the dominant corner sits 必胜客 Pizza Hut, operated by 百胜中国 Yum China — the incumbent titan. As of the first quarter of 2026 it commanded roughly 4,375 stores and something like 30% market share, dwarfing everyone.[^9] Pizza Hut is the brand that taught China what pizza was, and it did so through the dine-in, sit-down, casual-dining format we discussed earlier. That heritage is now both its strength and its trap: an enormous footprint and brand familiarity, but a cost structure built around large restaurants and table service in a market that is sprinting toward cheap, fast delivery. Pizza Hut has been pivoting hard in response — and the most dramatic evidence came in November 2025, when Yum China spent US$1.2 billion to buy out full ownership of the Pizza Hut China master franchise, eliminating the roughly 2.8% royalty it had been paying to its former parent and consolidating control to defend its turf.3 It is a defensive, expensive move, and analysts have openly debated whether Yum China overpaid given how soft Chinese consumption had become.3 Alongside the buyout, Pizza Hut leaned aggressively into a value format — "Pizza Hut WOW" — explicitly engineered to fight the price-down trend with lower price points.3 The titan, in other words, is being dragged downmarket to meet the moment.

In the value corner sits 尊宝比萨 Zunbao Pizza — "Champion Pizza" — the domestic insurgent. With over 3,000 stores and roughly 6% share, Zunbao plays a game neither Western brand wants to play: ultra-value, community-focused, hyper-cheap.[^11] Its average ticket runs a startling RMB 30–40, and it has built its brand on relentless value campaigns — the headline being its "19.9 RMB solo dining" pushes, pizza for the price of a coffee.[^11] Zunbao is the price floor of the market, a homegrown operator with no royalty to a foreign parent and a model tuned for the most cost-sensitive corners of China. It is the reason "trading down" is not an abstract macro risk for DPC Dash but a competitor with three thousand storefronts.

And in the speed corner sits Domino's (DPC Dash) itself — at roughly 1,462 stores as of March 2026 and an estimated 5–7% market share, the smallest of the three by footprint but the fastest-growing, dominating the high-efficiency delivery niche we just dissected.[^2][^9] Its weapon is neither Pizza Hut's brand heritage nor Zunbao's rock-bottom price, but the delivery-and-digital machine: thirty minutes, hot, every time, ordered from your couch.

Now here is the strategically interesting part — where the three players are heading. The old battlefield was Tier-1 cities, where DPC Dash built its density and its reputation. The new battlefield is the sinking market: "New Tier-1," Tier-2, and Tier-3 cities, the vast urban middle of China where pizza penetration is low and competition is less entrenched. For DPC Dash this lower-tier expansion has become the growth engine, contributing close to 60% of new revenue growth, and it comes with an attractive financial feature — store-level payback periods tend to be shorter in these cities because real estate and operating costs are lower while a novelty-hungry consumer drives strong early sales.[^5]

But — and this is the war-game tension an investor must hold — the sinking market is also exactly where Zunbao is strongest and where Pizza Hut WOW is aiming its value guns. DPC Dash is carrying a relatively premium, RMB 50–70 delivery proposition into territory where the local champion sells pizza for RMB 19.9 and the incumbent titan is slashing prices to defend share. The company's bet is that speed, brand, and digital experience justify the price gap even to a Tier-3 consumer. That bet is unproven at scale and runs directly against the deflationary current sweeping Chinese consumption. Whether the delivery flywheel travels intact into smaller cities — or whether it dilutes against cheaper local rivals and a thinner wallet — is the single most important open question in the competitive picture. To judge it, we need to look hard at the actual economics. So let's open the financials.

VII. Financial Maturity & The 2023 IPO

On March 28, 2023, DPC Dash rang the bell on the Main Board of the Hong Kong Stock Exchange under ticker 1405.HK, pricing its shares at HK$46.00 and raising roughly HK$590 million in net proceeds.4 After a quarter-century in China — thirteen sleepy years under Pizzavest, seven grinding years of consolidation, and six transformative years under the 4D Strategy — the Domino's China business was finally a public company. The IPO was not a blockbuster fundraise by Hong Kong standards; it was a modest, almost workmanlike listing. But it crystallized the transformation and, more practically, it gave the company a public currency and the disclosure obligations that let outsiders finally inspect the engine. So let's inspect it.

The heart of DPC Dash's investment case is its unit economics, and they are genuinely striking. A standard new store costs around RMB 1.5 million to build.[^5] What you get back for that capital is what makes the model hum. Stores reach cash breakeven at the store level within roughly one to three months of opening, and the full CAPEX payback period in new cities runs about 12 to 24 months.[^5] Translate that out of finance-speak: a new Domino's store in China tends to start covering its own running costs almost immediately and to return the entire cost of building it within one to two years. For a physical-footprint retail business — where the usual story is years of patient payback — that is fast. It is the financial signature of strong, front-loaded demand meeting a low-cost build.

How strong is that opening-day demand? Strong enough to embarrass the rest of the global system. DPC Dash stores have consistently occupied the top 50 spots worldwide for "first 30-day sales" across Domino's entire 22,000-store global network.[^5] Sit with that. Out of more than twenty thousand stores spanning every market Domino's operates in, the highest-grossing store openings on the planet keep coming from China. That is not a marketing line; it is the clearest single piece of evidence that DPC Dash's combination of pent-up demand, dense urban siting, and digital pre-marketing produces opening volumes that genuinely lead the world. The bullish reading writes itself. The bearish counterweight, which we will hold onto, is that record opening sales tell you about novelty and launch hype, not about whether a store still thrives in year three — and a chain growing this fast is always heavily weighted toward young, honeymoon-phase stores.

The path to actual profitability took longer than the growth, as it usually does for a company plowing cash into expansion. DPC Dash crossed into positive adjusted net profit for the first time in the first half of 2024, posting RMB 50.9 million.[^5] From there it scaled: for full-year 2025 the company reported adjusted net profit of RMB 187.9 million on revenue of RMB 5.38 billion, the latter up 24.8% year over year.[^3] So the story by 2025 was a business that had not only sustained its blistering top-line growth but had finally converted it into a meaningful and growing bottom line — the moment a growth company starts to look like a real one.

And yet the FY2025 results announcement, delivered on March 25, 2026, was not a victory lap, because of one number that gave analysts pause. Store-level operating margin contracted from 14.5% in 2024 to 13.7% in 2025.[^3] On its face an 0.8-point dip is small. But for a company whose entire equity story rests on the pristine economics of the individual store, any margin erosion during a period of rapid growth demands an explanation, because it raises the central fear: that the wonderful unit economics of the Tier-1 era will not survive the march into smaller cities.

Management's explanation, offered around the results, attributed the compression to three forces working at once: the costs of rapid lower-tier expansion (newer, lower-tier stores running at lower maturity and absorbing build-out drag), increased investment in rider safety, and promotional discounting in a deflationary consumer environment.[^3] Each of those is plausible and even reassuring in isolation — expansion drag fades as stores mature, safety investment is responsible, discounting is a response to the price war we just described. But notice that all three point in the same uncomfortable direction: the further DPC Dash pushes into the lower-tier, lower-price future it has staked its growth on, the more pressure sits on the very margins that justify the whole enterprise. The company is, in effect, spending some of its premium unit economics to buy lower-tier scale. Whether that trade compounds into durable share or slowly grinds the model down to a commodity is the question the income statement cannot yet answer — and it puts an unusual amount of weight on whether you trust the people making the call. So let's meet them.

VIII. Current Management, Incentives, and Credibility

A company is, in the end, a bet on the people allocating its capital and steering its strategy — and at DPC Dash that bet is concentrated heavily on one person. The management team is led by CEO 王怡 Aileen Wang, with Helen Wu (Ting Wu) as CFO and Jun Zhong as COO.[^5] But make no mistake: this is Wang's company in everything but name. She is the architect of the 4D Strategy, the executive who negotiated the territorial rights, and the cultural force that turned a regional laggard into a delivery machine. The credibility of the whole enterprise is, to an unusual degree, the credibility of one operator.

So how should an investor judge that credibility? Not by the press releases, but by behavior over time — and on the most important axis, execution against stated ambition, the record is strong. Under Wang, DPC Dash has strung together more than 29 consecutive quarters of positive same-store sales growth, a streak that survived the brutal stress test of China's zero-COVID lockdowns.[^3] That episode is actually the most revealing data point in the whole credibility question, because lockdowns were a near-extinction event for dine-in restaurants — and DPC Dash's delivery-first model, the very thing that had handicapped it for two decades, turned the catastrophe into a tailwind. When sitting in a restaurant was illegal, getting a hot pizza delivered to your locked-down apartment was close to ideal. Management did not merely survive the pandemic; the architecture they had built happened to be the right one for it. And they delivered on the expansion targets, reaching past 1,462 stores by early 2026.[^2] Setting aggressive goals and hitting them, repeatedly, across a once-in-a-generation disruption, is the strongest possible evidence that the narrative is backed by execution rather than spin.

Now, alignment. Does Wang win when shareholders win? Partly. She holds a roughly 1% direct ownership stake — worth somewhere around US$10 million depending on the stock's considerable volatility — through her holding vehicle Molybdenite Holding Limited.5 That is real skin in the game, enough that her personal wealth moves with the share price. But it is a modest stake for a founder-operator of her centrality, and the bulk of her economic alignment comes through compensation rather than legacy ownership. Her total annual compensation runs CN¥15.31 million, and the structure is aggressively performance-weighted: roughly 71% is tied to performance-related bonuses and equity grants rather than fixed salary.5 In principle this is exactly what you want — pay that flexes with results, not a guaranteed check. In practice, heavy equity weighting only aligns interests if the grants are sized and priced reasonably. And that is precisely where the most current controversy sits.

In May 2026, the Board proposed a substantial new equity package for Wang: 1,650,000 share options and 1,655,000 share awards (RSUs), alongside a refresh of the scheme limit to 10% of total share capital, with the whole proposal set for a shareholder vote at an extraordinary general meeting on July 10, 2026.6 A skeptical investor should hold two thoughts at once here. On one hand, richly rewarding the executive who manufactured a world-leading growth story is defensible, even necessary to retain her. On the other hand, a grant of this magnitude, paired with a refreshed 10% scheme ceiling, is exactly the kind of move that triggers legitimate activist concern over shareholder dilution — the quiet transfer of value from existing owners to management through the issuance of new shares. The size of the package and the timing of the EGM are now a live governance question, and how minority shareholders vote on July 10 will be a real-time referendum on whether the board is rewarding performance or overreaching.

This is the appropriate posture toward DPC Dash's management: deep respect for a demonstrated execution record, paired with clear-eyed attention to the governance and incentive structures being built on top of it. The execution is proven; the capital-allocation discipline, especially around its own equity, is still being tested. And the dilution debate is only one of several swords hanging over the story. To see the rest, we need to put on the activist's hat fully and stress the whole thing.

IX. Activist / Skeptical-Investor Stress Test & Risks

Every great growth story attracts a chorus of believers. The job of this section is to play the other side — to ask, as a hard-nosed long/short investor or activist would, what could break DPC Dash, and which risks are structural rather than cosmetic. There are four worth taking seriously.

The MFA renewal: a sword of Damocles dated June 1, 2027. Everything DPC Dash is — its brand, its system, its very right to exist — flows from the master franchise agreement with Domino's Pizza International, and that agreement expires in 2027.1 The consensus, and the company's clear expectation, is that it will be renewed for two additional ten-year terms; given the parent's past US$130 million equity vote of confidence and the obvious success of the relationship, renewal is highly likely.1 But "highly likely" is not "certain," and more to the point, the terms of renewal matter enormously. The current economics — a royalty of around 3% of sales plus roughly US$10,000 per new store opening, on top of POS licensing costs — are favorable.1 Any unfavorable adjustment to those terms at renewal would compress future margins directly, and the leverage in that negotiation sits substantially with the parent. The risk is not that DPC Dash loses the brand; it is that it pays meaningfully more to keep it, right at the moment its store-level margins are already under pressure. A skeptic notes that the company is entering this negotiation from a position of having proven exactly how valuable the China rights are — which is wonderful for the brand and potentially expensive for the franchisee.

The own-rider labor burden and the 共同富裕 common prosperity overhang. Earlier we praised the owned delivery fleet as a moat. The activist sees the same fact as a fixed-cost liability. Store staff and rider compensation together account for 27.7% of total revenue — a heavy, largely fixed labor load.2 Pizza Hut and local players like Zunbao that lean on gig-economy riders have effectively externalized this cost onto third-party platforms, keeping it variable and off their own books. DPC Dash deliberately internalized it. In a stable regulatory environment that trade buys control and consistency. But China's policy climate around labor protections has been tightening under the banner of 共同富裕 common prosperity, and here is the asymmetric danger: any regulatory mandate requiring full social security, housing-fund contributions, or strict insurance coverage for part-time delivery riders would land squarely on DPC Dash's own payroll, instantly compressing store-level margins — while a gig-reliant competitor might absorb the same rule more diffusely through its platforms. The very decision that gives DPC Dash its operational edge also concentrates its exposure to Chinese labor regulation. That is a real, structural, hard-to-hedge risk, not a hypothetical.

The DPZ sell-down: what does the parent know? Recall the global parent's enthusiastic US$130 million equity investment around 2020–2021. Now consider what it did later. In late 2024, Domino's Pizza Inc. sold down its stake from roughly 14% to 6.2% via block trades to institutional investors.7 This is the kind of insider behavior that should make any investor sit up, because there are two competing interpretations and they point in opposite directions. The benign reading: DPZ is simply an early venture-style backer crystallizing an excellent return on a successful investment, recycling capital, and the block-trade-to-institutions structure (rather than a panicked open-market dump) signals an orderly exit, not a fire sale. The bearish reading: the party with the deepest insight into the franchise — the global parent that sees DPC Dash's books and prospects more intimately than any outside shareholder — chose to roughly halve its exposure at this particular juncture, just ahead of the 2027 MFA renewal it sits on the other side of. The truth is probably closer to the benign reading, but an honest skeptic does not get to simply assume that. A parent reducing its strategic stake from 14% to 6.2% is, at minimum, a reduction in alignment and a data point that deserves to sit uncomfortably in the bull case rather than be explained away.

Macro headwinds and the price war. Finally, the deflationary environment that is now the backdrop to everything. Chinese consumers are trading down across categories, and the pizza market has tipped into an aggressive price war — Zunbao at RMB 19.9, Pizza Hut WOW slashing its way downmarket. DPC Dash's entire premium-to-Zunbao, value-to-Pizza-Hut positioning depends on protecting an average ticket in the RMB 50–70 zone. Can it hold that line while the floor of the market keeps dropping? The FY2025 margin compression we examined was, in part, the early cost of not fully holding it — the discounting management cited. The bear's thesis is simple and uncomfortable: in a sustained consumption downturn, "fast and premium-ish" gets squeezed between "cheap" and "established," and the wonderful unit economics slowly converge toward the commodity. Nothing in the 2025 numbers refutes that thesis; they are merely consistent with management's more benign explanation of it. Which interpretation prevails is, again, unproven.

Hold all four risks together — renewal terms, labor concentration, parent sell-down, and the price war — and the picture is not of a fragile company, but of a strong one whose key advantages each carry an embedded, specific vulnerability. That is exactly the kind of nuanced reality the strategy frameworks are built to dissect. So let's run DPC Dash through them.

X. The Playbook: Strategic Frameworks & Investing Lessons

We have told the story; now let's pressure-test the advantages with the two frameworks Acquired listeners know best — Hamilton Helmer's 7 Powers and Porter's Five Forces — and then isolate the handful of metrics that actually matter going forward. The goal is not to crown DPC Dash with a moat; it is to ask which of its powers are durable and which are merely a head start.

Hamilton's 7 Powers Analysis

Process Power — the smart last mile. This is DPC Dash's most credible source of durable advantage. The proprietary smart-routing algorithms, store-based dispatch, Community GPS navigation, and dedicated fleet together produce a roughly 24-minute average delivery at 1,400-plus-store scale.2 Process Power, in Helmer's framework, is an advantage embedded in a company's organization and operations that is slow and difficult for rivals to replicate even when they can see it — and that fits here. A competitor cannot buy this; it would have to build the fleet, the algorithms, the local routing data, and the operational muscle memory across thousands of riders and hundreds of stores, over years. That is genuinely hard to copy. The caveat is that Process Power is a lead, not a law of nature — a well-capitalized rival (and Yum China is very well capitalized) could in principle close it over time.

Scale Economies — the central kitchens. DPC Dash consolidates fresh, never-frozen dough production across four large central kitchens — Shanghai, Sanhe, Dongguan, and Wuhan.[^5] High store density in target cities then lets the company spread logistics, lower per-unit food costs (COGS), and amortize marketing across more outlets. This is textbook scale economics: bigger lowers unit cost. But it is also the most contestable of DPC Dash's powers, because at roughly 1,462 stores it is dwarfed by Pizza Hut's 4,375 — meaning on pure scale, DPC Dash is the sub-scale player, not the dominant one. Its scale advantages are real within its delivery-density niche, but it does not enjoy industry-wide scale supremacy.

Cornered Resource — the master franchise rights. The exclusive right to operate the Domino's brand across Mainland China, Hong Kong, and Macau is a genuine Cornered Resource: a uniquely valuable asset that competitors simply cannot obtain, because there is only one, and DPC Dash holds it.1 This is as clean an example of the power as you'll find — but it comes with the asterisk we have already nailed down: it is contractual and it expires in 2027. A Cornered Resource you have to re-lease from a powerful counterparty is a weaker thing than one you own outright.

Network Effects. Here we should be precise rather than generous, because "network effects" is the most over-claimed power in business writing. DPC Dash's flywheel — more stores → shorter, faster delivery → more active users → more orders on WeChat → more data → better routing and supply optimization → support for still more stores — is real and powerful, but it is closer to a scale-and-data flywheel than a classic network effect, where each user directly makes the product more valuable to other users.2 The distinction matters for durability: a density flywheel can be matched by a competitor who achieves comparable density in the same city, whereas a true network effect locks users in. DPC Dash's loop is a formidable reinforcing mechanism, but an investor should not mistake it for the unbreakable kind.

Porter's 5 Forces Analysis

Rivalry among existing competitors — Very High. The three-way war between Pizza Hut, Zunbao, and DPC Dash is intensifying, sharpened by consumer price-sensitivity and the defensive margin tactics — buyouts, value formats, RMB 19.9 promotions — we have already war-gamed. This is the force pressing hardest on the company right now.

Threat of new entrants — Low. This is DPC Dash's friend. Building a nationally integrated QSR supply chain with central fresh-dough kitchens and a proprietary owned-rider delivery network requires enormous upfront CAPEX, regulatory clearance, and technology infrastructure. The very things that made Domino's entry slow and painful are now the moat against the next would-be entrant. The barrier that hurt DPC Dash on the way in protects it now that it's inside.

Bargaining power of buyers — High. Consumers face essentially zero switching costs. If price or quality slips, a customer reorders from Pizza Hut, Zunbao, or any of a thousand other options with a couple of taps. This force is structurally unfavorable and is precisely why the loyalty program and digital experience matter — they are attempts to manufacture switching cost where none naturally exists.

Bargaining power of suppliers — Low. The core inputs — flour, cheese, meats — are heavily commoditized, and DPC Dash's centralized purchasing gives it the upper hand over suppliers. Favorable, and not seriously contested.

Threat of substitutes — High. This is the force investors most underrate. China's food-delivery ecosystem is staggeringly rich; pizza competes not just with other pizza but with noodle chains, chicken joints, hotpot, bubble tea — thousands of fast, cheap, delivered alternatives. Pizza is a choice among an enormous menu of equally convenient options, and that ceiling on category loyalty is permanent.

Net of the frameworks: DPC Dash's most durable edge is Process Power in delivery, anchored by a Cornered Resource that expires and amplified by a scale-and-data flywheel — operating inside an industry where rivalry and substitution are fierce but entry is genuinely hard. That is a real competitive position. It is not an impregnable one.

Key KPIs to Track on an Ongoing Basis

For an investor following this story quarter to quarter, three metrics matter more than all the rest. First, same-store sales growth (SSSG) — the ultimate gauge of brand health and whether the density flywheel is still spinning; the moment the 29-quarter streak breaks is the moment the core thesis needs re-examination. Second, store-level operating profit margin — the single number that tells you whether lower-tier expansion and rising labor costs are eroding the unit economics; watch whether it holds the historical 13.5%–14.5% band or keeps sliding. Third, active loyalty members and WeChat Mini-Program engagement — the health of the 38.8-million-member data asset and its purchase frequency, which is the leading indicator of demand durability and customer-acquisition efficiency. Track those three and you are tracking the actual machine, not the marketing.

XI. Epilogue, Surprises & Lessons for Founders

Step back from the spreadsheets and the frameworks, and the most surprising thing about the DPC Dash story is how thoroughly it inverts its own premise. A brand that arrived in China as a cheap Western derivative — wrong format, wrong moment, wrong cultural fit — did not win by becoming more premium or more Chinese-restaurant-like. It won by waiting for the market to swing toward its native strengths and then ruthlessly exploiting the high-efficiency delivery niche that everyone else had treated as an afterthought. The durian pizza gets the headlines and the social-media virality, but durian was never the strategy. The strategy was the rider, the algorithm, and the WeChat window.

That distinction is the first and most important lesson for founders and investors watching from afar: localize the channel, not just the product. It is easy and cheap to put a local topping on a foreign product and call it localization. DPC Dash's actual achievement was re-engineering the delivery and digital channel itself — building an owned fleet, a smart-dispatch system, Community GPS routing, and a WeChat-native ordering and loyalty ecosystem — to match how Chinese consumers actually live and order. Pizzavest spent thirteen years localizing nothing structural and went nowhere. Aileen Wang's team localized the channel and went everywhere. Product localization is table stakes; channel localization is the moat.

The second lesson is the one embedded in the owned-rider decision: if speed and quality are your brand promise, do not outsource the part of the business that delivers on it. The cheap, obvious path was to hand the last mile to Meituan and Ele.me. DPC Dash refused, accepted a heavier fixed-cost structure, and in exchange got control over the single moment that defines the brand. That choice is the source of both its Process Power and its labor-cost vulnerability — which is exactly the point. The decisions that create a company's deepest advantages and its sharpest risks are often the very same decisions. There is no version of DPC Dash that has the delivery moat without the labor exposure; they are two faces of one strategic bet.

As for the road ahead, management has set an ambitious destination: roughly 3,000 stores by 2029, a target that would roughly double the current footprint and position the company to challenge Pizza Hut's overall dominance in China rather than merely lead a niche.[^5] An investor should hold that number the way we have held every other management claim in this story — as a stated ambition backed by a real execution record, not as a fact. The path to 3,000 runs straight through the lower-tier cities where the margins are thinner, the consumer is poorer, Zunbao is entrenched, and the price war is hottest. It runs through the 2027 MFA renewal and whatever it costs. It runs through China's evolving labor regime. The same engine that produced the most remarkable growth story in global pizza will now be tested in exactly the conditions least flattering to it.

That is what makes DPC Dash worth watching rather than worth dismissing or worshipping. It has proven, beyond reasonable doubt, that the model works in the China it grew up in. What it has not yet proven is that the model survives intact into the harder, cheaper, more competitive China it is now expanding into. The next three years will answer the only question that matters: whether the fastest-growing pizza chain in the world built a durable machine, or simply caught a wave at exactly the right moment with exactly the right operator. The streak says machine. The macro says wait and see. Both can be true at once — and for now, both are.

References

-

DPC Dash Ltd. Full IPO Prospectus (2023-03-16) — HKEXnews ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

DPC Dash Ltd. 2025 Annual Results Announcement (2026-03-25) — HKEXnews ↩↩↩↩↩↩↩↩↩

-

Yum China Announces Buyout of Pizza Hut China Master Franchise for $1.2 Billion — Reuters, 2025-11-14 ↩↩↩

-

DPC Dash Board Proposes Share Option and RSU Grants to CEO Aileen Wang — Investing.com, 2026-05-28 ↩

-

Domino's Pizza Inc. Sells Down Stake in DPC Dash via Block Trade — Bloomberg, 2024-10-18 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube