Industrial & Commercial Bank of China: The $5.7 Trillion Dragon

I. Introduction & Episode Thesis

Picture this: It's October 27, 2006, and the trading floors in Hong Kong and Shanghai are electric. Traders are witnessing history—not just another IPO, but the simultaneous debut of a bank that shouldn't exist according to every Western economics textbook. The Industrial & Commercial Bank of China, a state-owned enterprise born from communist central planning, is about to raise $21.9 billion in the world's largest public offering. Goldman Sachs, having poured $2.6 billion into this bet just months earlier, watches as their largest investment ever transforms into pure gold.

But here's the paradox that would make Milton Friedman spin in his grave: How does a bank owned by a communist government, operating under party directives, and carrying the baggage of decades of policy lending become the world's most valuable financial institution? By 2024, ICBC commands $5.7 trillion in assets—more than JPMorgan Chase and Bank of America combined. Its 720 million retail customers exceed the entire population of Europe. Its profits dwarf those of banks that invented modern capitalism.

The central question isn't whether ICBC succeeded—the numbers scream that answer. It's how a bank can simultaneously serve Communist Party objectives and generate shareholder returns that make Wall Street salivate. This is the story of an institution that breaks every rule of Western finance yet dominates global banking. It's about patient capital triumphing over quarterly earnings obsessions, state backing becoming a competitive weapon rather than a handicap, and digital transformation happening at a scale that makes Silicon Valley look quaint.

We'll trace ICBC's journey from a spinoff of China's monobank system in 1984 to its current throne atop global finance. We'll explore the NPL crisis that nearly destroyed it, the restructuring that saved it, and the IPO that transformed it. We'll examine how it weathered the 2008 financial crisis while Western banks collapsed, its aggressive global expansion through the Belt and Road Initiative, and its ongoing battle with fintech giants like Ant Group.

This isn't just a banking story—it's about the rise of state capitalism, the reshaping of global finance, and a glimpse into a future where the rules of money and power are being rewritten from Beijing, not New York. As we dive into ICBC's labyrinthine history, remember this: every assumption you have about how banks should work is about to be challenged.

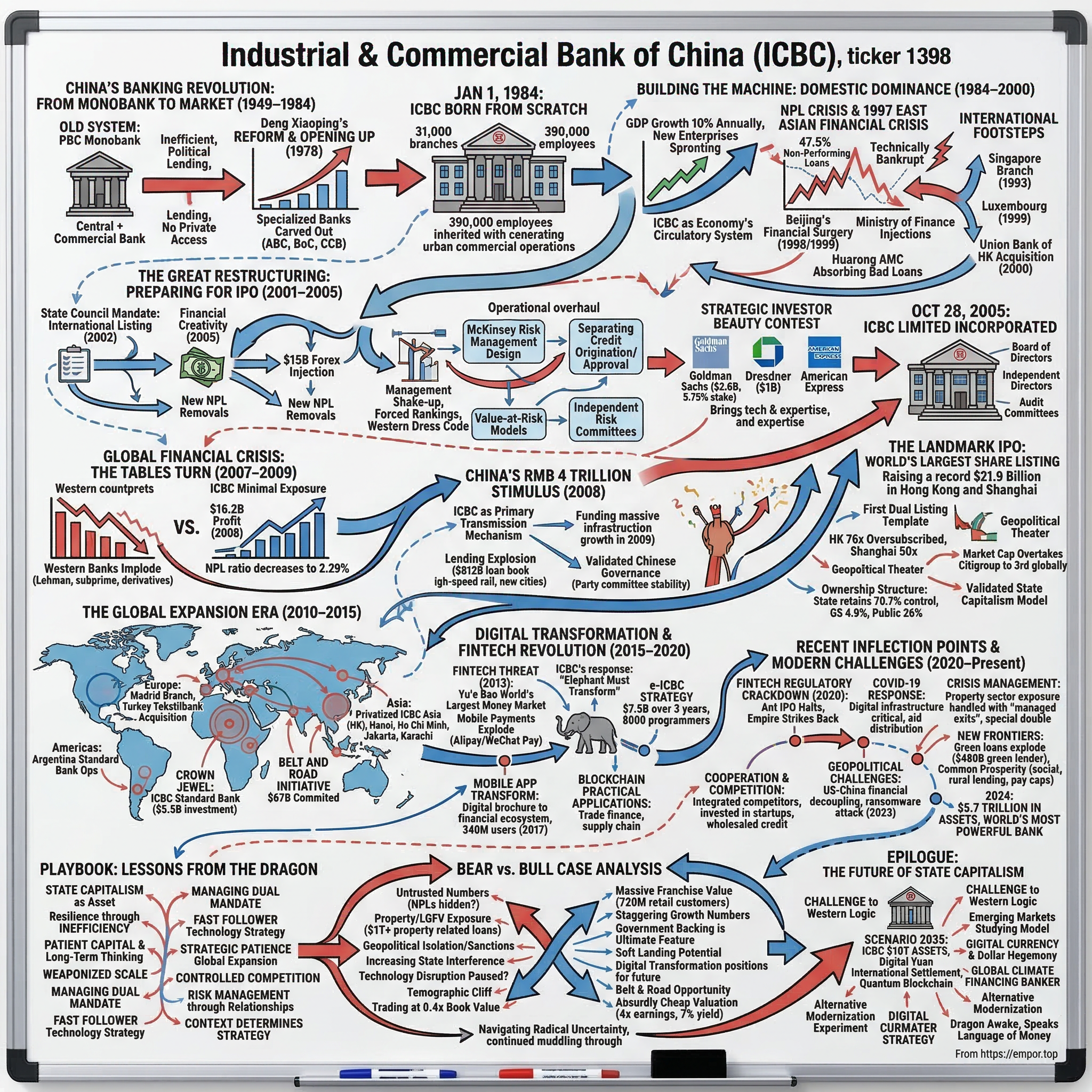

II. China's Banking Revolution: From Monobank to Market (1949–1984)

The year is 1978. Mao Zedong has been dead for two years, and in the halls of Zhongnanhai—China's equivalent of the White House—a diminutive man with a perpetual cigarette is engineering the most radical economic transformation in human history. Deng Xiaoping, barely five feet tall but towering in political acumen, understands something his predecessors didn't: China needs banks that actually function like banks.

For three decades under Mao, China operated what economists call a "monobank" system—a financial monstrosity where the People's Bank of China (PBC) served as central bank, commercial bank, and government treasury rolled into one. Imagine the Federal Reserve also being JPMorgan, Wells Fargo, and the U.S. Treasury. That was China's financial system: a single institution allocating capital based on political directives, not economic logic. Interest rates? Market forces? Return on investment? These concepts existed only in banned economics textbooks.

The monobank wasn't just inefficient—it was suffocating China's economy. State-owned enterprises received unlimited credit regardless of performance, while productive private businesses couldn't access a yuan. By 1978, China's per capita GDP languished at $156, lower than most African nations. Deng's famous declaration—"It doesn't matter if a cat is black or white, as long as it catches mice"—signaled the end of ideological purity in economics.

The transformation began in December 1978 at the Third Plenum of the 11th Central Committee, where Deng unveiled his "Reform and Opening Up" policy. But reforming banking posed unique challenges. How do you dismantle a financial system without triggering economic collapse? How do you create commercial banks in a country where profit was a dirty word just years earlier?

Deng's solution was quintessentially Chinese: gradual, experimental, and pragmatic. Rather than shock therapy à la Russia's later reforms, China would "cross the river by feeling the stones." The first stone was separating central banking from commercial banking. In 1979, the State Council began carving specialized banks out of the PBC's bloated carcass. The Agricultural Bank of China emerged first, resurrected from its pre-Cultural Revolution incarnation to serve rural areas. The Bank of China followed, handling foreign exchange and international transactions. The China Construction Bank came next, financing infrastructure projects.

But China's industrial and commercial sectors—the factories, steel mills, department stores, and trading companies that formed the economy's backbone—still lacked a dedicated financial institution. These enterprises, ranging from massive state-owned manufacturers to small municipal shops, operated in financial limbo, dependent on irregular allocations from various government departments.

The State Council's September 1983 decision would change everything. Document No. 146, issued with little fanfare, mandated the creation of the Industrial and Commercial Bank of China. Unlike its three predecessors, ICBC would be built from scratch, inheriting the PBC's commercial banking operations in urban areas—31,000 branches, 390,000 employees, and a loan book that read like a Communist Party membership roll.

On January 1, 1984, ICBC officially opened its doors. The last of the "Big Four" state banks was also the largest from day one, controlling 35% of China's total banking assets. Its first president, Chen Muhua, faced an impossible mandate: transform a political lending machine into a commercial bank while maintaining social stability. She had to serve both Marx and the market.

The early years revealed the challenge's magnitude. ICBC's loan officers, trained to follow party directives, suddenly had to evaluate creditworthiness. Branch managers accustomed to unlimited government backing now faced concepts like "bad debt" and "provisioning." The bank's initial charter reflected this schizophrenia—it would "support the state's economic policies" while "operating according to economic principles."

Yet within this confusion lay opportunity. China's economy was exploding—GDP growth averaged 10% annually through the 1980s. Township and village enterprises sprouted like mushrooms after rain. Private businesses, officially sanctioned in 1981, multiplied exponentially. All needed banking services, and ICBC was the only game in town for most.

By 1990, ICBC had become China's circulatory system, moving money from savers to builders, from the state to enterprises, from the old economy to the new. Its deposits reached 430 billion yuan, its loans topped 380 billion yuan. But success bred complacency, and complacency bred crisis. The bad loans accumulating on ICBC's books—loans made for political rather than economic reasons—would soon threaten not just the bank but China's entire economic miracle.

As China entered the 1990s, ICBC stood at a crossroads. It could remain a tool of state policy, allocating capital based on political connections and five-year plans. Or it could evolve into a genuine commercial bank, making decisions based on risk and return. The choice would determine not just ICBC's fate but the trajectory of Chinese capitalism itself.

III. Building the Machine: Domestic Dominance (1984–2000)

The Mandarin Oriental hotel in Singapore, 1993. ICBC's delegation, led by a young executive named Jiang Jianqing, sits across from skeptical Singaporean regulators. They're pitching something unprecedented: a Chinese state bank wants to open its first overseas branch in the Lion City. The regulators' questions cut deep: "How can we trust your accounting?" "What happens when Beijing calls with orders?" "Are you a bank or a government department?"

Jiang, who would later become ICBC's transformational chairman, understood their skepticism. Back home, ICBC operated in a parallel universe where normal banking rules didn't apply. State-owned enterprises received loans not based on creditworthiness but on guanxi—connections—and government priorities. A steel mill hemorrhaging money? If it employed 50,000 workers, ICBC would keep lending. A profitable private manufacturer? Sorry, wrong ownership structure.

This schizophrenia defined ICBC's adolescence. By day, it proclaimed itself a commercial bank. By night, it funneled credit to politically favored projects. The numbers told the story: by 1995, state-owned enterprises consumed 70% of ICBC's loan book despite generating less than 40% of industrial output. The bank had become China's economic life support system, keeping zombie companies alive to preserve social stability.

The Singapore branch finally opened in November 1993—ICBC's first tentative step beyond China's borders. But even as it expanded internationally, domestic realities grew grimmer. The East Asian Financial Crisis of 1997 exposed the rot beneath Asia's economic miracle. Thailand's banks collapsed. Korea's chaebols crumbled. Indonesia's rupiah evaporated. China watched its neighbors burn and realized its banks were sitting on similar kindling.

Premier Zhu Rongji, a tough-talking former mayor of Shanghai, ordered China's first comprehensive audit of the banking system in 1998. The results were catastrophic: non-performing loans at the Big Four banks exceeded 40% of total loans. At ICBC specifically, NPLs reached 47.5%—nearly half its loan book was effectively worthless. By Western standards, ICBC was not just insolvent but spectacularly bankrupt.

Yet bankruptcy meant something different in China. The government couldn't let ICBC fail without triggering economic apocalypse. Instead, Beijing engineered one of history's largest financial rescues, though "rescue" hardly captures the Byzantine complexity of what followed. In 1999, the Ministry of Finance injected 270 billion yuan into the Big Four banks. But this was just the appetizer.

The main course came with the creation of asset management companies (AMCs)—special purpose vehicles designed to absorb bad loans. Huarong AMC was created specifically for ICBC, taking 408 billion yuan of NPLs off its books at face value. It was accounting alchemy: bad loans disappeared from ICBC's balance sheet and reappeared on Huarong's, where they could be worked out over decades without poisoning the banking system.

While Beijing performed financial surgery at home, ICBC pushed deeper into international markets. The Luxembourg branch opened in 1999, giving ICBC a foothold in European Union banking. Then came the acquisition that signaled serious ambition: Union Bank of Hong Kong in 2000, purchased for HK$10.3 billion. This wasn't just buying assets—it was buying respectability, expertise, and a gateway to international capital markets.

The Union Bank deal revealed ICBC's evolving sophistication. Due diligence took eighteen months. International auditors scrutinized every loan. The integration plan covered everything from IT systems to coffee machines. ICBC even retained Union Bank's senior management, acknowledging it had much to learn about modern banking.

Jiang Jianqing, promoted to president in 2000, embodied this new mentality. Unlike his predecessors—career bureaucrats who viewed banking as administration—Jiang was a banker's banker. He spoke fluent English, understood derivatives, and could debate Basel capital requirements with any Wall Street executive. Under his leadership, ICBC began its most radical transformation yet.

The numbers from this period reveal an institution in violent transition. Total assets grew from 2.7 trillion yuan in 1995 to 5.3 trillion yuan by 2000. But growth alone meant nothing if the underlying assets were garbage. The real achievement was operational: ICBC installed its first centralized IT system, introduced credit scoring models, and began training loan officers in actual credit analysis rather than political evaluation.

China's 2001 entry into the World Trade Organization loomed like a ticking clock. WTO rules mandated that China open its banking sector to foreign competition by 2006. Citibank, HSBC, and Standard Chartered were already circling, eager to feast on China's vast deposit base. ICBC had five years to transform from a state-controlled policy bank into something resembling a modern financial institution.

The challenge seemed insurmountable. How do you restructure a bank with 390,000 employees, many hired for political rather than professional reasons? How do you price risk in an economy where the government ultimately backstops everything? How do you satisfy shareholders while serving the Communist Party?

As 2000 ended, ICBC stood at the precipice of its greatest transformation. The old model—unlimited government support in exchange for policy lending—was dying. The new model remained undefined. But one thing was clear: the comfortable monopoly ICBC had enjoyed since 1984 would soon face competition from banks that actually knew how to bank. The countdown to confrontation had begun.

IV. The Great Restructuring: Preparing for IPO (2001–2005)

Goldman Sachs's headquarters, 85 Broad Street, New York. January 2005. Henry Paulson, Goldman's CEO and future U.S. Treasury Secretary, stares at a proposal that would either cement his legacy or destroy it. His team wants to invest $2.6 billion—Goldman's largest investment ever—in a Chinese state-owned bank with a communist party committee embedded in its management structure. The investment committee's reaction: "Have you lost your minds?"

But Paulson saw what others missed. China's banking reform wasn't just financial engineering—it was the largest transfer of wealth from government to market in human history. And ICBC, the crown jewel of Chinese banking, was about to undergo a metamorphosis that would make Kafka jealous.

The transformation began in 2002 when President Jiang Jianqing received his marching orders from the State Council: prepare ICBC for international listing by 2006. The deadline coincided with WTO-mandated banking liberalization—not a coincidence but strategic timing. China would meet foreign competition not with protectionism but with world-class institutions.

The first challenge was mathematical: how to transform a balance sheet that looked like a crime scene into something investors might actually buy. The 1999 bailout had removed 408 billion yuan of bad loans, but like a hydra, new NPLs kept sprouting. By 2003, ICBC's NPL ratio still exceeded 25%. The solution required financial creativity that would make Wall Street's structured products look simple.

In April 2005, the State Council approved a radical restructuring plan. First, the Ministry of Finance would inject $15 billion from China's foreign exchange reserves—not yuan but hard dollars, signaling international ambition. Second, Huarong AMC would purchase another 246 billion yuan of doubtful loans, this time at a discount that reflected actual recovery values. Third, and most controversially, ICBC would write off 247 billion yuan of accumulated losses against its capital.

The numbers were staggering but the politics were harder. Every bad loan represented someone's relationship, someone's career, someone's cousin's factory. Jiang Jianqing personally reviewed thousands of loans, making enemies with each rejection. Branch managers accustomed to lending based on lunch conversations suddenly faced credit committees demanding cash flow projections and collateral valuations.

The cultural transformation went deeper than accounting. ICBC hired McKinsey to redesign its risk management system—a $50 million contract that represented China's largest consulting engagement. McKinsey's consultants, many fresh from restructuring American banks, encountered a parallel universe. Loan documents were often single pages. Credit analysis meant checking if the borrower was state-owned. Risk management meant hoping the government would bail everyone out.

The consultants' recommendations were revolutionary by Chinese standards: segregate credit origination from approval, implement value-at-risk models, create independent risk committees. ICBC's old guard resisted. "You don't understand China," they told the twenty-something MBAs. "Banking here is about relationships, not ratios."

But Jiang backed the reforms with ruthless determination. He replaced 30% of senior management, promoting younger executives who understood modern banking. He introduced forced rankings—the bottom 5% of employees faced termination, unheard of in state enterprises where employment was lifetime. He even changed the dress code, banning the Mao suits that senior bankers still wore, mandating Western business attire.

The strategic investor beauty contest began in 2004. Every major global bank wanted in—this was the ticket to China's financial future. But Beijing had conditions: investors must bring technology and expertise, not just capital. They must commit for the long term. And crucially, they couldn't threaten state control.

Goldman Sachs understood the game better than most. Paulson had cultivated Chinese relationships for decades, visiting Beijing seventy times as CEO. Goldman's proposal went beyond capital: they would second executives to ICBC, transfer risk management systems, and provide global markets access. The $2.6 billion investment would buy just 5.75% of ICBC, valuing the bank at $45 billion—a generous price for an institution that technically remained insolvent by Western standards.

The Goldman deal, announced in January 2006, triggered a feeding frenzy. Dresdner Bank quickly invested $1 billion. American Express added $200 million, seeking access to China's credit card market. These weren't passive investments but strategic partnerships. Goldman's risk management chief spent six months in Beijing training ICBC staff. Dresdner transferred its entire Asian retail banking technology platform. AmEx shared customer analytics that ICBC's managers had never imagined possible.

October 28, 2005, marked the official transformation: Industrial and Commercial Bank of China Limited was incorporated as a joint-stock company. The old ICBC—a government department masquerading as a bank—ceased to exist. The new ICBC had a board of directors, independent directors (including Goldman nominees), and audit committees that actually audited.

The prospectus preparation revealed the transformation's extent. ICBC's financials, previously state secrets, were now audited by PricewaterhouseCoopers using International Financial Reporting Standards. The bank's operations, once opaque even to insiders, were documented in 600 pages of disclosure. Every related-party transaction, every government directive, every Communist Party decision that affected banking operations had to be explained to potential investors.

The numbers by late 2005 told a remarkable story. NPL ratios had dropped to 4.7%. Tier 1 capital reached 9.8%. Return on assets hit 0.6%—not spectacular by Western standards but miraculous for a bank that was technically bankrupt five years earlier. Cost-to-income ratios fell from 60% to 42%. ICBC had become efficient, profitable, and allegedly clean.

But skeptics remained. How could NPLs drop so dramatically so quickly? Were the new loans genuinely commercial or just better-disguised policy lending? Could foreign investors really influence a bank where the Communist Party committee still met weekly? These questions would only be answered by the ultimate test: letting the market decide ICBC's value.

V. The Landmark IPO: World's Largest Offering (2006)

4:47 AM, October 27, 2006. Jiang Jianqing stands in ICBC's Beijing headquarters, connected by video link to trading floors in Hong Kong and Shanghai. In three minutes, his bank will attempt something unprecedented: simultaneous listing on two exchanges, raising more money than any IPO in history. The prayer he mutters isn't to Marx or Mao but to the market gods: "Please, let the price hold."

The roadshow had been brutal. Twenty-three cities in twenty-five days. Jiang and his team faced every conceivable question from skeptical fund managers. In London, investors questioned ICBC's government ownership. In Boston, they probed NPL ratios. In Singapore, they wondered about corporate governance. In Dubai, they asked about Islamic banking capabilities. Each meeting was a trial, each question a test of whether Chinese state capitalism could speak the language of global finance.

The pricing negotiations revealed the stakes. ICBC wanted to price at the top of the range—HK$3.07 per share in Hong Kong, RMB 3.12 in Shanghai. This would value the bank at $140 billion, making it the world's fifth-largest by market capitalization on day one. Goldman Sachs, conflicted between its role as cornerstone investor and global coordinator, pushed for aggressive pricing. China Construction Bank's successful IPO a year earlier had proven investor appetite for Chinese banking stories.

The allocation process became geopolitical theater. The Hong Kong tranche was 76 times oversubscribed—HK$420 billion chasing HK$5.5 billion of shares. The Shanghai A-share offering was 50 times oversubscribed, with Chinese retail investors lining up at branches before dawn to submit applications. But the real drama was institutional allocation. Every major fund wanted a piece, but ICBC and its underwriters played favorites, rewarding long-term investors while punishing hedge funds suspected of planning quick flips.

The opening trades shattered expectations. In Hong Kong, ICBC opened at HK$3.52, up 15% from the offer price. Volume in the first minute exceeded most stocks' full-day trading. In Shanghai, the A-shares rocketed 5%—the maximum allowed on listing day. By noon, ICBC's market capitalization had reached $156 billion, overtaking Citigroup as the world's third-most-valuable bank after Bank of America and JPMorgan Chase.

The numbers were historic: US$21.9 billion raised, obliterating NTT DoCoMo's 1998 record of $18.4 billion. The Hong Kong portion raised US$16 billion, the Shanghai portion US$5.9 billion. Including the greenshoe options exercised immediately, ICBC had created the world's largest IPO, a record that would stand until Alibaba's 2014 listing.

But the real story wasn't the size—it was the structure. This was the first major simultaneous A+H share listing, creating a template that dozens of Chinese companies would follow. The dual listing solved multiple problems: it satisfied Beijing's desire to develop domestic capital markets while accessing international liquidity. It allowed Chinese retail investors to own their national champion while giving foreign institutions exposure to China's growth.

The post-IPO ownership structure revealed the delicate balance ICBC had achieved. The Chinese government retained 70.7% control through the Ministry of Finance (35.3%) and Central Huijin (35.4%), ensuring state dominance. Goldman Sachs held 4.9%, just below the 5% threshold that would trigger additional regulatory scrutiny. Other strategic investors—Dresdner, AmEx—held smaller stakes. The public float was 26%, enough for liquidity but not enough to threaten control.

The first day's trading patterns exposed the different investor bases. In Hong Kong, institutional investors dominated, with measured accumulation and profit-taking. In Shanghai, retail investors drove volatile swings, treating ICBC like a lottery ticket rather than a bank stock. The price divergence between H-shares and A-shares—the latter trading at a 20% premium—would become a permanent feature, reflecting capital controls and different investor sophistication.

International reactions ranged from admiration to alarm. The Financial Times called it "the coming of age of Chinese capitalism." The Wall Street Journal warned of "irrational exuberance with Chinese characteristics." The Economist, ever skeptical, questioned whether investors understood what they were buying: "Is ICBC a commercial bank or a policy tool? Can it be both? For how long?"

Inside ICBC, the IPO's success created its own challenges. Suddenly, every decision faced market scrutiny. Quarterly earnings calls meant explaining loan growth to analysts who could move the stock price with a single downgrade. The government's policy directives now had to be balanced against shareholder interests. The Communist Party committee still met weekly, but now their decisions could trigger SEC investigations if they affected U.S. depositary receipt holders.

Jiang Jianqing's post-IPO strategy was clear: use the capital and credibility to accelerate international expansion. Within weeks of listing, ICBC announced new branches in Moscow, Dubai, and London. The bank hired veteran Western bankers, paying packages that scandalized Chinese media but barely registered in global markets. It launched new products—wealth management, investment banking, insurance—that moved beyond traditional lending.

The IPO proceeds—$15 billion in fresh capital—transformed ICBC's capabilities. Tier 1 capital ratio jumped to 11.3%, among the highest of major global banks. This war chest would prove providential. Within two years, the subprime crisis would devastate Western banks while ICBC's fortress balance sheet would allow it to expand while competitors retreated.

As 2006 ended, ICBC's stock had risen 43% from its IPO price in Hong Kong, creating $60 billion in market value. Early investors like Goldman Sachs were sitting on paper gains exceeding $1 billion. But the real winner was the Chinese government, which had transformed a technically insolvent policy bank into a $200 billion market capitalization powerhouse while maintaining absolute control.

The IPO's success validated China's state capitalist model, at least temporarily. You could have your cake and eat it too—maintain government control while accessing international capital. You could serve political objectives while generating shareholder returns. You could be both communist and capitalist, both Chinese and global. The contradictions that Western economists said would destroy Chinese banking had instead become competitive advantages. But the real test was coming: a global financial crisis that would challenge every assumption about how banks should work.

VI. Global Financial Crisis: The Tables Turn (2007–2009)

September 15, 2008, 1:14 AM Beijing time. ICBC Chairman Jiang Jianqing is woken by a phone call from Hong Kong. Lehman Brothers has just filed for bankruptcy. His chief risk officer's next words are crucial: "Our exposure is minimal—$182 million in bonds, fully hedged." Jiang's response: "Check again. Then check our exposures to everyone else. This is going to spread."

While Jiang worked the phones, Dick Fuld was clearing out his corner office at Lehman, and Hank Paulson was preparing to face Congress. The contrast was stark: Western banks were imploding from their addiction to subprime mortgages and derivatives they didn't understand, while ICBC had barely touched the toxic waste that poisoned global finance.

This wasn't luck—it was strategic conservatism born from inexperience. In 2007, when Merrill Lynch was packaging CDO-squareds, ICBC's investment banking division was still learning how to structure basic corporate bonds. When Citigroup was leveraging 33-to-1, ICBC maintained a stodgy 15-to-1 ratio. Chinese bankers joked they were too backward to be sophisticated, too naive to be greedy.

ICBC had actually tried to join the party. In 2007, the bank explored purchasing mortgage-backed securities, sending teams to New York to learn structured finance. The reports they sent back were telling: "We don't understand how these products generate returns beyond their credit risk," one analyst wrote. "The Americans say we're too conservative. Perhaps conservative means careful."

The numbers from 2008 tell an extraordinary story. While Citigroup lost $27.7 billion, Bank of America lost $4.4 billion, and Royal Bank of Scotland lost £24.1 billion, ICBC posted a profit of RMB 111 billion ($16.2 billion)—up 35% from 2007. Its NPL ratio actually decreased to 2.29%. Return on equity held steady at 20%. The bank that Western analysts had mocked as a communist dinosaur was suddenly the industry's profit leader.

But ICBC's real advantage wasn't avoiding toxic assets—it was China's response to the crisis. In November 2008, Beijing announced a RMB 4 trillion ($586 billion) stimulus package, equivalent to 13% of GDP. The speed was breathtaking: while the U.S. Congress debated TARP for weeks, China's State Council approved its stimulus in a single weekend. ICBC would be the primary transmission mechanism, turning government directives into credit creation.

The lending explosion that followed defied comprehension. ICBC's loan book grew by RMB 812 billion in 2009 alone—more than most European banks' entire portfolios. The bank was approving infrastructure projects that Western banks would spend years analyzing in mere weeks. A high-speed rail line from Beijing to Shanghai? Approved. A new city for 500,000 people in Inner Mongolia? Funded. Solar panel factories with no confirmed buyers? Here's your credit line.

Western observers were horrified. This wasn't banking—it was monetary defibrillation. The Financial Times warned of "credit-fueled disaster." The Economist predicted "China's coming financial crisis." But they missed the point: in a state-controlled system, bad loans are just government expenditures in disguise. If the loans soured, Beijing would recapitalize the banks. If they succeeded, China would have world-class infrastructure while America debated shovel-ready projects.

The irony was delicious. Free-market America was nationalizing banks—the government took majority stakes in Citigroup and AIG. Communist China was listing banks on stock exchanges and attracting foreign capital. Hank Paulson, who as Goldman's CEO had championed ICBC's IPO, now found himself implementing socialist policies as Treasury Secretary while his former Chinese clients practiced capitalism.

ICBC's international position strengthened as Western banks retreated. In 2008, while Barclays was absorbing Lehman's corpse and Bank of America was choking on Merrill Lynch, ICBC quietly expanded across Asia. It established branches in Jakarta, Karachi, and Bangkok—markets abandoned by capital-starved Western competitors. The bank's pitch was simple: "We have capital, we have patience, and we're not going anywhere."

The cultural impact was profound. A generation of Chinese bankers who had grown up worshipping Wall Street watched their idols collapse. The Harvard MBAs that ICBC had recruited were suddenly less impressive than the home-grown cadres who understood relationship banking. The risk models imported from New York were less reliable than the common sense of branch managers who knew their customers personally.

By 2009's end, the transformation was complete. ICBC's market capitalization reached $246 billion, making it the world's most valuable bank. Total assets exceeded $1.4 trillion. The bank that couldn't get meetings with second-tier Wall Street firms five years earlier was now their largest trading counterparty in Asian markets.

The crisis also validated ICBC's governance model, perverse as that sounds. The Communist Party committee that Western investors feared had actually provided stability. While Western banks cycled through CEOs—Citigroup had three in three years—ICBC's leadership remained constant. The same party discipline that enabled policy lending also prevented rogue trading. No ICBC trader could lose $6 billion like UBS's Kweku Adoboli because no individual had that much autonomy.

But the seeds of future problems were being sown. The lending explosion of 2009 would eventually create its own NPL crisis. The infrastructure projects funded at warp speed would generate overcapacity. The relationship-based lending that seemed prudent during crisis would look corrupt during recovery. ICBC's balance sheet was growing faster than its risk management capabilities.

Still, as 2009 ended, ICBC stood triumphant. It had survived—no, thrived—during history's worst financial crisis. It had proven that Chinese state capitalism could compete with and even surpass Western financial institutions. Most importantly, it had accumulated the capital and confidence for its next act: true global expansion. The student had become the master, and the master was about to go shopping.

VII. The Global Expansion Era (2010–2015)

The Standard Bank boardroom in Johannesburg, March 2007. ICBC's delegation faces the African banking giant's directors across a table that once hosted negotiations between De Beers and Anglo American. The Chinese team's proposal is audacious: ICBC wants to buy 20% of Africa's largest bank for $5.5 billion. Standard Bank's century-old tradition meets China's newfound ambition in a deal that will reshape global finance's geography.

The Standard Bank investment wasn't random—it was strategic chess. While Western banks saw Africa as a charity case requiring development aid, ICBC saw the world's last frontier market. By 2010, Chinese trade with Africa had reached $127 billion. Chinese construction companies were building roads from Cairo to Cape Town. Every project needed financing, and ICBC wanted to be the banker of choice for China's African century.

The partnership bore fruit quickly. By 2011, ICBC and Standard Bank had co-financed $2 billion in African infrastructure projects. They funded the Morupule power plant in Botswana, copper mines in Zambia, and telecommunications networks in Nigeria. Standard Bank provided local knowledge and regulatory relationships; ICBC brought Chinese contractors and seemingly unlimited capital.

But ICBC's global ambitions extended far beyond Africa. In December 2010, the bank privatized ICBC (Asia), its Hong Kong subsidiary, transforming it from a sleepy outpost into an aggressive regional hub. The timing was perfect: European banks were retreating from Asia to meet Basel III capital requirements, creating a vacuum ICBC eagerly filled.

The expansion strategy was methodical: follow Chinese companies abroad, then attract local clients. When Chinese manufacturers established factories in Vietnam, ICBC opened branches in Hanoi and Ho Chi Minh City. When Chinese miners descended on Peru, ICBC set up shop in Lima. The bank was creating a parallel financial system for China's global expansion.

2011 brought breakthrough entries into Europe and South Asia. The Madrid branch opening seemed routine until you realized its purpose: financing Chinese companies acquiring distressed Spanish assets. During Spain's banking crisis, Chinese investors bought everything from olive oil producers to football clubs, all financed by ICBC. The Karachi and Islamabad branches served the China-Pakistan Economic Corridor, a $62 billion infrastructure program that would transform Pakistan's economy.

The November 2012 acquisition of Standard Bank's Argentine operations for $600 million showcased ICBC's opportunism. Standard Bank was retreating from Latin America after decades of losses. ICBC saw opportunity where others saw chaos. Argentina's soybean exports to China were exploding. Chinese companies were investing in lithium mines and shale gas. ICBC would become their financial bridge, earning fees from trade finance and foreign exchange that Western banks considered too risky.

The crown jewel came in 2014: creating ICBC Standard Bank in London through a complex merger of Standard Bank's London operations with ICBC's nascent investment banking platform. This wasn't just another acquisition—it was ICBC's entry ticket to global markets' inner sanctum. Suddenly, ICBC could trade commodities in London, structure derivatives in New York, and arrange syndicated loans anywhere.

The London operation revealed ICBC's evolved sophistication. The dealing room, staffed by veterans poached from Goldman Sachs and JPMorgan, traded everything from copper futures to credit default swaps. The corporate finance team, led by ex-Morgan Stanley bankers, was arranging multi-billion dollar acquisitions. This wasn't your father's Chinese bank—it was a global financial institution that happened to be Chinese.

Turkey came next. The 2015 acquisition of Tekstilbank for $316 million seemed small, but Turkey was the buckle in China's Belt and Road Initiative. Chinese companies were building Turkey's third Bosphorus bridge, its high-speed rail network, and its nuclear power plants. ICBC would finance these projects while capturing trade flows between China and Europe.

The numbers by 2015 were staggering. ICBC operated 412 overseas branches in 42 countries. International assets reached $350 billion. Cross-border lending exceeded $180 billion. The bank that had nervously opened its first overseas branch in Singapore just 22 years earlier now spanned six continents.

But expansion created unexpected challenges. Managing credit risk in Nigeria was different from Ningbo. Regulatory compliance in London required armies of lawyers. Cultural integration proved painful—Chinese managers' authoritarian style clashed with local banking cultures. ICBC's Argentine subsidiary faced a fraud scandal when local employees exploited weak controls. The Turkish operation struggled with lira volatility.

The Belt and Road Initiative, officially launched in 2013, turbocharged ICBC's international growth. The bank became Beijing's financial spearhead, funding ports in Greece, railways in Kenya, and power plants in Pakistan. By 2015, ICBC had committed $67 billion to Belt and Road projects. Critics called it debt-trap diplomacy. ICBC called it development finance. The truth was somewhere in between.

The competitive dynamics were fascinating. In markets like Indonesia and Brazil, ICBC competed directly with Citibank and HSBC for multinational corporate clients. In frontier markets like Myanmar and Ethiopia, ICBC was often the only international bank willing to take risk. The bank's pitch was compelling: we understand emerging markets because we are one. We don't lecture about governance while refusing to lend. We're partners, not professors.

Yet ICBC's international expansion faced a fundamental tension. The same government backing that enabled aggressive expansion also created suspicion. When ICBC bid for agricultural land in Australia, politicians blocked it on national security grounds. When it tried to acquire a U.S. bank, regulators stonewalled. The Communist Party committee that provided strategic direction in Beijing became a liability in Washington.

As 2015 ended, ICBC stood at another inflection point. It had successfully globalized, but at what cost? The international operations generated just 8% of profits despite consuming 20% of capital. The Belt and Road loans were accumulating but not yet generating returns. Most critically, ICBC faced a new challenge that no amount of international expansion could solve: digital disruption from within China itself.

VIII. Digital Transformation & FinTech Revolution (2015–2020)

Jack Ma's apartment in Hangzhou, 2013. The Alibaba founder is explaining his vision for Ant Financial to a skeptical audience of bankers. "ICBC is not our competition," he says with characteristic bravado. "ICBC is an elephant. We are the ants. But you know what? Ants can move mountains, one grain at a time." Within five years, those ants would force ICBC into the most radical transformation in its history.

The threat wasn't immediately obvious. In 2013, when Alibaba launched Yu'e Bao, a money market fund embedded in its payment app, ICBC executives dismissed it as a novelty. Who would trust their savings to an e-commerce company? By 2015, Yu'e Bao had attracted 260 million users and $165 billion in assets, making it the world's largest money market fund. Those deposits came from somewhere—and that somewhere was increasingly ICBC's branches.

The statistics were alarming. Between 2015 and 2017, foot traffic at ICBC branches declined 38%. Mobile payment transactions through Alipay and WeChat Pay exploded from $1 trillion to $15 trillion. Young Chinese consumers were living entirely digital financial lives—paying with QR codes, investing through apps, borrowing from algorithms. ICBC's 16,000 branches and 440,000 employees suddenly looked less like assets and more like anchors.

Chairman Yi Huiman, who succeeded Jiang Jianqing in 2016, understood the existential threat. Yi wasn't a traditional banker but a technology enthusiast who spent weekends studying artificial intelligence papers. His diagnosis was blunt: "We're not competing against other banks. We're competing against technology companies with banking licenses. If we don't transform, we'll become the Kodak of banking."

The e-ICBC strategy launched in 2015 was ambitious to the point of absurdity. ICBC would digitize every product, automate every process, and analyze every customer interaction. The investment was massive: $7.5 billion over three years, more than most fintech startups' entire valuations. ICBC hired 8,000 programmers, data scientists, and user experience designers. It partnered with Tencent, despite WeChat Pay being a direct competitor, to modernize its technology stack.

The mobile app transformation told the story. ICBC's 2014 app was essentially a digital brochure—users could check balances and little else. The 2017 version was a financial ecosystem. Users could trade stocks, buy insurance, book flights, pay utilities, and even order coffee. The app used artificial intelligence to predict customer needs, offering loans before customers realized they needed them.

The numbers were impressive. By end-2017, ICBC's mobile banking users reached 340 million—more than the entire U.S. population. Digital transactions exceeded counter transactions for the first time. The Easy Loan platform, using machine learning for instant credit decisions, had disbursed $450 billion to 4.5 million small businesses. Processing time dropped from weeks to minutes. Default rates actually decreased because algorithms proved better at assessing credit risk than human loan officers.

But ICBC's real innovation was blockchain—not the cryptocurrency speculation plaguing Western banks, but practical applications for trade finance and supply chain management. In 2017, ICBC completed the world's first blockchain-based international factoring transaction. By 2019, its blockchain platform was processing $50 billion in trade finance annually, reducing documentation time from days to hours.

The partnership strategy was counterintuitive but brilliant. Rather than fighting the tech giants, ICBC embraced them. It integrated Alipay and WeChat Pay into its own systems, earning transaction fees from competitors' success. It provided banking services to Ant Financial's lending platform, essentially wholesaling credit to its retail competitor. It even invested in fintech startups that might disrupt its business, preferring to own the disruption rather than be victimized by it.

The robo-advisor launch in 2017 exemplified ICBC's evolved thinking. Traditional wealth management required minimum investments of 1 million yuan and served just 2% of customers. The robo-advisor had no minimum and used algorithms to create personalized portfolios. Within two years, it attracted 15 million users and $75 billion in assets. The cannibalization of traditional wealth management was intentional—better to disrupt yourself than be disrupted.

The COVID-19 pandemic accelerated everything. When China locked down in January 2020, ICBC's digital infrastructure became critical national infrastructure. The bank processed government relief payments to 400 million citizens through its mobile app. Its AI-powered lending platform approved 2 million small business rescue loans in six weeks. Contact-free banking went from nice-to-have to necessity overnight.

Yet digital transformation created new vulnerabilities. The November 2023 LockBit ransomware attack on ICBC Financial Services, the bank's U.S. subsidiary, disrupted Treasury markets and exposed cybersecurity weaknesses. The incident was contained, but it highlighted an uncomfortable truth: digitization meant new attack vectors that no amount of Communist Party discipline could prevent.

The competitive landscape by 2020 was unrecognizable from 2015. ICBC's main rivals were no longer Bank of China or China Construction Bank but Ant Group and Tencent. The metrics of success had changed too. Market capitalization mattered less than monthly active users. Branch networks mattered less than API connections. Relationship managers mattered less than recommendation algorithms.

The transformation's financial impact was mixed. Operating costs declined—the cost-to-income ratio dropped from 42% to 31% as automation replaced employees. But technology investments pressured margins. Return on equity fell from 20% to 14% as ICBC sacrificed profitability for digital market share. The stock price languished, with investors uncertain whether ICBC was a bank becoming a tech company or a tech company burdened by banking regulations.

As 2020 ended, ICBC had successfully digitized but at tremendous cost. It had avoided disruption by disrupting itself. It had embraced competitors rather than fighting them. But fundamental questions remained: Could a state-owned bank really compete with nimble tech companies? Could algorithms replace relationships in Chinese business culture? Most importantly, how would Beijing balance financial innovation with social stability?

The answer would come sooner than expected. In November 2020, regulators dramatically halted Ant Group's $37 billion IPO, signaling a crackdown on fintech that would reshape China's financial landscape once again. ICBC, the incumbent that had adapted to survive, suddenly found the rules changing in its favor.

IX. Recent Inflection Points & Modern Challenges (2020–Present)

November 3, 2020, Shanghai. Jack Ma stands at the Bund Finance Summit, delivering what will become the most expensive speech in history. "Chinese banks have a pawnshop mentality," he declares. "They only lend to those who don't need money." Within 48 hours, Ant Group's $37 billion IPO is suspended. Within months, China's entire fintech sector faces regulatory annihilation. For ICBC, the empire strikes back.

The regulatory crackdown that began with Ant's failed IPO wasn't just about one company or one speech. It represented Beijing's recognition that financial innovation had spiraled beyond control. Peer-to-peer lending platforms had collapsed, wiping out millions of investors' savings. Tech companies were leveraging deposits 50-to-1, making Lehman Brothers look conservative. Consumer lending apps were charging interest rates that would make loan sharks blush.

ICBC, once threatened by fintech disruption, suddenly found itself on the right side of history. The same bureaucratic caution that made it slow to innovate now looked like prudence. The same government ownership that scared off investors now provided stability. The regulatory hammer that fell on Ant Group barely dented ICBC because it had never strayed far from Beijing's comfort zone.

The COVID-19 response had already demonstrated ICBC's systemic importance. While Western banks struggled with payment protection programs, ICBC seamlessly distributed government aid. Its technology platform, built to compete with fintechs, proved robust enough to handle 900 million digital transactions daily during lockdown. The bank that critics called a dinosaur had become China's financial circulatory system.

But ICBC faced its own crisis: property sector exposure. By 2021, real estate and related industries comprised 29% of ICBC's loan book—nearly $1 trillion. When Evergrande defaulted on $300 billion in liabilities, every Chinese bank held its breath. ICBC's direct exposure was manageable—$3.6 billion—but the indirect exposure through suppliers, contractors, and homebuyers was unknowable.

Chairman Chen Siqing, appointed in 2019, managed the property crisis with surgical precision. Rather than mass foreclosures that would trigger social unrest, ICBC orchestrated "managed exits." Distressed developers received bridge loans to complete projects, protecting homebuyers. Viable projects got refinanced at lower rates. Hopeless cases were liquidated quietly. It was extend-and-pretend with Chinese characteristics, but it worked.

The numbers from this period reflect controlled chaos. NPL ratios increased from 1.42% in 2020 to 1.48% in 2023—a rounding error by historical standards. But special mention loans—the category just above NPLs—doubled to 3.2%. ICBC was managing a slow-motion crisis through financial engineering and government support that Western banks could only dream of.

The geopolitical environment added another layer of complexity. U.S.-China financial decoupling accelerated after Russia's invasion of Ukraine. ICBC found itself walking a tightrope—maintaining Western investor confidence while serving Chinese national interests. When sanctions hit Russian banks, ICBC had to choose between profitable Russian business and access to dollar clearing. It chose dollars, but created yuan-denominated workarounds that satisfied neither Washington nor Moscow.

The November 2023 ransomware attack on ICBC Financial Services exposed unexpected vulnerabilities. Hackers encrypted systems that clear U.S. Treasury trades, forcing ICBC to process transactions manually. For several hours, the world's largest bank was reduced to passing USB drives between computers. The attack was contained, but it revealed how digitization had created new risks that traditional risk management hadn't anticipated.

ESG emerged as another challenge-turned-opportunity. International investors increasingly demanded environmental accountability. ICBC's loan book included coal power plants, steel mills, and other carbon monsters. But China's 2060 carbon neutrality pledge gave ICBC cover to pivot. Green loans exploded from $150 billion in 2020 to $480 billion by 2023. The bank financing coal plants was suddenly the largest green lender globally—a contradiction only possible in China.

The Common Prosperity campaign, launched in 2021, required another recalibration. ICBC had to demonstrate service to society, not just shareholders. Rural lending quotas increased. Fees for basic services were eliminated. Executive compensation was capped at $500,000—pocket change by Wall Street standards. The bank that had spent two decades becoming commercial was being re-politicized, but subtly.

Competition evolved in unexpected directions. State-owned peers like Bank of China and China Construction Bank were no longer rivals but allies against common threats. The real competition came from digital banks like WeBank and MYbank, backed by Tencent and Ant respectively. These banks had no branches, no legacy systems, and no political obligations. They could offer loans in seconds while ICBC still required days.

ICBC's response was typically Chinese: if you can't beat them, co-opt them. The bank became the largest shareholder in several fintech companies. It provided wholesale funding to digital banks that competed for its retail customers. It even launched its own digital bank subsidiary, offering products the parent bank couldn't. It was competition and cooperation simultaneously—what Chinese call "coopetition."

By 2024, ICBC had adapted to its new reality. Total assets reached $5.7 trillion. Profit exceeded $50 billion annually. The bank served 720 million retail customers and 10.7 million corporate clients. It operated in 49 countries. By every quantitative measure, it was the world's most successful bank.

But success in Chinese banking means something different than on Wall Street. It means serving government objectives while generating profits. It means innovating within boundaries. It means competing globally while remaining fundamentally Chinese. ICBC had mastered these contradictions, but new challenges kept emerging.

The future held more questions than answers. Could ICBC maintain growth as China's economy slowed? Could it navigate increasing U.S.-China tensions? Could it balance commercial objectives with Common Prosperity demands? Could it defend against cyber threats while maintaining digital leadership? The bank that had survived every crisis from NPLs to COVID faced its most complex environment yet.

X. Playbook: Lessons from the Dragon

What can Western capitalism learn from a Communist bank that conquered global finance? The lessons are counterintuitive, uncomfortable, and occasionally heretical to free-market orthodoxy. But ICBC's playbook—refined over four decades of transformation—offers insights that transcend ideology.

State Capitalism vs. Free Market: When Government Backing is an Asset

The conventional wisdom says government ownership breeds inefficiency. ICBC proves the opposite can be true. During the 2008 crisis, implicit government backing became explicit strength. While Citigroup and Bank of America required embarrassing bailouts, ICBC's state ownership was its business model. Depositors never doubted their money's safety. Borrowers knew the bank wouldn't fail. Investors understood the downside was limited.

The lesson isn't that state ownership is superior—it's that ownership structure must match market context. In mature, stable markets with strong institutions, private ownership optimizes efficiency. In developing markets with weak institutions, state backing provides stability that enables growth. ICBC thrived because its ownership matched China's development stage.

The Paradox of Inefficiency Breeding Stability

ICBC's inefficiencies—the overstaffing, the bureaucracy, the political lending—actually created resilience. A bank with 440,000 employees can absorb shocks that would cripple lean competitors. Relationship-based lending that seems primitive actually provides information that algorithms miss. Political loans that appear irrational serve social stability that enables economic growth.

This isn't an argument for inefficiency—it's recognition that efficiency isn't everything. Lehman Brothers was incredibly efficient until it wasn't. ICBC's redundancies and inefficiencies were insurance premiums against catastrophic failure. In complex systems, resilience matters more than optimization.

Patient Capital and Long-Term Thinking in Volatile Markets

ICBC's investment horizon spans decades, not quarters. The bank spent ten years building presence in Africa before seeing meaningful returns. It invested billions in technology that wouldn't pay off for years. It accepted lower returns during crisis to maintain relationships that would prove valuable during recovery.

This patience comes from alignment between ownership, management, and strategy. When your majority shareholder thinks in Five-Year Plans and century-long rejuvenations, quarterly earnings become less important. Western banks, enslaved to quarterly earnings calls and activist investors, can't match this strategic patience.

Using Scale as a Competitive Weapon

ICBC weaponized scale in ways Western banks never imagined. Its 16,000 branches became distribution points for everything from insurance to airline tickets. Its 720 million customers created network effects that no competitor could replicate. Its $5.7 trillion balance sheet enabled lending that smaller banks couldn't match.

But scale without strategy is just obesity. ICBC succeeded because it used scale strategically—entering markets where size mattered, crushing competitors through pricing power, absorbing losses that would bankrupt smaller players. The lesson: in banking, being biggest isn't everything, but it's something.

Managing the Dual Mandate: Profit vs. Policy

Every bank serves multiple stakeholders, but ICBC's dual mandate—serving both shareholders and the Communist Party—seems impossibly contradictory. Yet ICBC found synthesis: policy lending that generates economic growth creates future commercial opportunities. Infrastructure loans that seem political today become profitable when the infrastructure generates commerce tomorrow.

The key was transparency about the dual mandate. Investors knew they were buying a state-influenced bank. They accepted lower returns for lower volatility. They understood that government objectives sometimes trumped profit maximization. This clarity prevented the disappointment that comes from mismatched expectations.

Technology Adoption: Fast Follower vs. Innovator Strategy

ICBC rarely invented anything. Its mobile app copied Alipay's features. Its robo-advisor mimicked Western models. Its blockchain platform adapted existing protocols. But ICBC implemented at scale what others invented in labs. It took proven concepts and deployed them to hundreds of millions of users.

This fast-follower strategy avoided the costs and risks of innovation while capturing most benefits. Let fintech startups experiment and fail. Let Western banks debug new technologies. Then adopt what works, implement at massive scale, and use government relationships to create regulatory moats. It's not glamorous, but it works.

Global Expansion Through Strategic Patience

ICBC's international expansion followed Chinese diaspora and businesses, then broadened to local markets. It didn't try to compete with JPMorgan in New York or Barclays in London. Instead, it dominated corridors others ignored—China to Africa, Pakistan to the Middle East, Latin America to Asia.

The bank accepted lower returns internationally because presence mattered more than profit. Being the only international bank in Laos or Myanmar created options for when those markets matured. Following Chinese companies abroad created captive clients. Patience turned marginal markets into profitable franchises.

The Power of Controlled Competition

ICBC competed fiercely with Chinese peers but cooperated against foreign threats. It partnered with tech giants while competing for customers. It funded fintech disruptors while defending its core business. This wasn't confusion—it was sophisticated strategy that recognized competition and cooperation aren't mutually exclusive.

Risk Management Through Relationships

ICBC's risk management seems primitive—loan officers who know borrowers personally, credit decisions based on relationships, collateral that's more social than physical. But in markets where legal systems are weak and information asymmetric, relationships provide information that credit scores miss. A loan officer who attended university with a borrower knows things no algorithm can capture.

The Ultimate Lesson: Context Determines Strategy

ICBC succeeded not despite Chinese characteristics but because of them. State ownership worked because China's government was competent and stable. Relationship banking worked because Chinese business culture values relationships. Policy lending worked because China's economy was growing fast enough to bail out mistakes.

The playbook isn't universally applicable—it's context-dependent. A U.S. bank copying ICBC's strategy would fail spectacularly. But understanding why ICBC's approach works in its context provides insights applicable everywhere: match strategy to environment, use your advantages even if they're unfashionable, and remember that what's irrational in one context might be optimal in another.

XI. Bear vs. Bull Case Analysis

The investment case for ICBC splits analysts into two camps with diametrically opposed views. Bears see a communist relic heading for inevitable crisis. Bulls see the world's most powerful bank at a generational discount. Both cite the same facts to reach opposite conclusions—a sure sign we're dealing with something genuinely complex.

The Bear Case: A House of Cards in a Hurricane

The bear thesis starts with the numbers nobody trusts. ICBC claims NPL ratios of 1.48%, but bears argue the real number could be 10x higher. Chinese banks have infinite ways to hide bad loans—rolling them over, restructuring terms, moving them off-balance-sheet, or simply lying. The property sector alone, with $1 trillion in exposure, could trigger cascading defaults that overwhelm any government backstop.

The math is terrifying. Chinese property prices must permanently plateau to avoid crisis—they can't rise (bubble), can't fall (collapse), must just freeze. What's the probability of threading that needle? Meanwhile, local government financing vehicles owe $13 trillion, much of it unpayable. ICBC's exposure is "only" $400 billion, but that's before second-order effects when municipalities can't pay suppliers who can't repay loans.

Then there's geopolitical isolation. Every scenario where U.S.-China relations deteriorate hurts ICBC disproportionately. Secondary sanctions could cut access to dollar funding. Technology restrictions could cripple IT systems. Capital controls could trap foreign investors. The Huawei playbook—destroyed by U.S. sanctions despite technological leadership—haunts every Chinese bank executive's nightmares.

State interference keeps intensifying. Common Prosperity means accepting lower returns to serve social goals. Rural lending quotas mean financing unprofitable projects. Executive pay caps mean talent flight to private sector. The bank that spent 20 years becoming commercial is being re-politicized at exactly the wrong moment.

Technology disruption hasn't disappeared—it's just paused. Digital banks will eventually crack ICBC's profitable niches. Cryptocurrency will undermine cross-border payment revenues. Embedded finance will eliminate the need for traditional banking. ICBC's 440,000 employees and 16,000 branches are legacy costs that nimble competitors don't carry.

The demographic cliff amplifies everything. China's population peaked in 2022. The workforce shrinks by 5 million annually. Household formation—the driver of mortgage demand—is collapsing. ICBC's growth model assumes more customers, more loans, more deposits. What happens when everything reverses?

Bears see ICBC trading at 0.4x book value as the market pricing in catastrophe. The dividend yield of 7% isn't generous—it's desperate. Foreign ownership has dropped to historic lows. Even Chinese investors are skeptical, with A-shares trading at their smallest premium to H-shares ever. When your own citizens won't pay up for your stock, something's wrong.

The Bull Case: The Dragon at a Discount

Bulls start with the franchise value. ICBC has 720 million retail customers—more than any institution in history. Each customer represents multiple revenue streams: deposits, loans, payments, investments, insurance. Even at China's slowing growth rates, GDP per capita will double by 2035. ICBC captures value from every yuan of that growth.

The numbers are staggering even at conservative assumptions. If ICBC maintains just 15% market share of Chinese banking (down from current 18%), and Chinese banking assets grow just 5% annually (half the historical rate), ICBC's assets reach $10 trillion by 2030. At a 0.8% return on assets (below historical averages), that's $80 billion in profit. The current market cap of $250 billion prices none of this growth.

Government backing isn't a bug—it's the ultimate feature. ICBC can't fail because China can't let it fail. The government has $3 trillion in foreign reserves, owns 80% of land, controls the printing press, and faces no electoral constraints. Western analysts applying Lehman-style bankruptcy scenarios to ICBC misunderstand Chinese political economy. The Communist Party's legitimacy depends on financial stability. They'll print, restructure, or nationalize whatever necessary to prevent crisis.

The property exposure fear is overblown. Yes, ICBC has $1 trillion in property-related loans. But Chinese households have 30-50% down payments, unlike America's subprime zero-down insanity. The government controls supply through land auctions and demand through purchase restrictions. They can engineer a soft landing through policies impossible in free markets. Even if property loans generate 10% losses—a catastrophic scenario—that's $100 billion against $400 billion in equity and unlimited government support.

Digital transformation positions ICBC perfectly for China's future. The bank already has 340 million mobile users, more than any Western bank. Its technology spending exceeds most fintech valuations. The regulatory crackdown on Ant and Tencent leveled the playing field. ICBC gets the benefits of digitization without the winner-take-all dynamics that threatened its existence.

The international opportunity remains massive. Belt and Road Initiative involves $1 trillion in infrastructure investment. ICBC finances 30% of BRI projects, earning fees and interest from ventures Western banks won't touch. As Chinese companies globalize, ICBC follows. The bank already operates in 49 countries. Each new market is an option on future growth.

The valuation discount is absurd by any metric. ICBC trades at 4x earnings while JPMorgan trades at 12x. It trades at 0.4x book while Bank of America trades at 1.3x. The dividend yield of 7% is triple the S&P 500 average. Even assuming zero growth and permanent discounts, you're buying dollar bills for 40 cents.

Bulls see the current pessimism as opportunity. Foreign ownership at historic lows means potential rerating when sentiment improves. The Common Prosperity alignment, while pressuring near-term returns, ensures political support long-term. The technology investments, while expensive today, position ICBC for decades of digital dividends.

The Synthesis: Navigating Radical Uncertainty

The truth, as always, lies between extremes. ICBC faces real challenges—property exposure, geopolitical tensions, technological disruption. But it possesses unique advantages—government backing, market dominance, patient capital. The binary outcomes bears and bulls envision—total collapse or massive rerating—are both unlikely.

The most probable path is continued muddling through. China will manage its property slowdown through financial repression and gradual adjustment. ICBC will absorb losses through earnings rather than capital. Growth will slow but remain positive. Returns will disappoint but not disappear. The stock will trade at permanent discounts but generate decent total returns through dividends.

For investors, ICBC represents a complex bet on China's economic model. Bears betting on collapse have been wrong for decades. Bulls expecting Western-style valuations will likely stay disappointed. But for those who accept Chinese characteristics—the state influence, the dual mandates, the permanent complexity—ICBC offers exposure to the world's most dynamic economy at a remarkable discount.

The investment decision ultimately depends on your view of China itself. If you believe China's model is unsustainable, avoid ICBC regardless of valuation. If you believe China will continue growing despite challenges, ICBC is the cheapest way to participate. There's no middle ground—you're either comfortable with Chinese characteristics or you're not.

XII. Epilogue: The Future of State Capitalism

Shanghai, 2035. A holographic projection of ICBC's chairman addresses the annual shareholders meeting. The bank just reported its 51st consecutive year of profit growth. Assets have reached $10 trillion. The digital yuan processes 80% of international trade settlements. ICBC's quantum-encrypted blockchain clears more transactions than SWIFT. The West's predictions of collapse, repeated annually since 2010, have proven spectacularly wrong. Again.

This scenario isn't fantasy—it's extrapolation. ICBC has defied Western economic logic for four decades. Every time experts predicted its demise—the NPL crisis of 1999, the global financial crisis of 2008, the property slowdown of 2023—the bank emerged stronger. The question isn't whether ICBC will survive but what its survival means for global capitalism.

The China model that ICBC embodies challenges every assumption about how financial systems should work. Markets don't always know best—sometimes bureaucrats make better capital allocators. Competition doesn't always improve outcomes—sometimes cooperation generates superior results. Private ownership doesn't always maximize value—sometimes state control creates more wealth. These heresies are becoming harder to dismiss as Chinese banks dominate global rankings.

Emerging markets are watching and learning. Indonesia's state banks are copying ICBC's playbook. India's State Bank is studying ICBC's digital transformation. Brazil's development banks are adopting ICBC's patient capital approach. The Washington Consensus that preached privatization and deregulation is being replaced by a Beijing Consensus that emphasizes state capacity and strategic control.

The implications extend beyond banking. If ICBC can successfully combine state ownership with market discipline, what else is possible? Can governments run technology companies? Can central planning work with artificial intelligence? Can authoritarian capitalism outperform democratic capitalism? ICBC's success makes these questions urgent rather than theoretical.

The digital currency revolution amplifies ICBC's importance. The digital yuan isn't just another cryptocurrency—it's a challenge to dollar hegemony. Every transaction that settles in digital yuan rather than dollars weakens American financial power. ICBC, as the primary interface between the digital yuan and global commerce, becomes the architect of a new financial order.

Climate finance offers another avenue for ICBC's influence. The bank's $480 billion green loan portfolio already exceeds most countries' entire banking systems. As China exports renewable energy technology and finances its deployment, ICBC becomes the banker for the global energy transition. The institution that funded coal plants for decades could ironically become the savior of the planet's climate.

Yet ICBC's future isn't predetermined. The bank faces existential challenges that no amount of government support can eliminate. Demographic decline means fewer customers and lower growth. Technological disruption means traditional banking may become obsolete. Geopolitical fragmentation means global ambitions may remain unrealized. The strengths that brought ICBC to dominance may become weaknesses in a changed world.

The most likely future is neither triumph nor collapse but transformation. ICBC will evolve into something unrecognizable—part bank, part technology platform, part government agency, part global utility. It will operate in digital realms that don't yet exist, serving customers not yet born, financing industries not yet invented. The only certainty is that it will remain fundamentally Chinese, shaped by and shaping the Middle Kingdom's trajectory.

For the global financial system, ICBC represents both promise and peril. Promise because it demonstrates alternative paths to development, proves that different models can succeed, and provides capital to underserved markets. Peril because it concentrates power in unaccountable institutions, enables authoritarian governance, and challenges the liberal international order.

The ultimate question isn't about ICBC but about us. How should democratic societies respond to state capitalism's success? Should we copy Chinese methods or double down on market principles? Can we compete with patient capital using quarterly earnings? How do we balance efficiency with resilience, innovation with stability, freedom with order?

ICBC forces these uncomfortable questions because its success can't be dismissed as temporary or accidental. Four decades of outperformance isn't luck—it's evidence that our economic models are incomplete. The bank that shouldn't exist according to our textbooks has become the world's largest. The institution that violates our principles has generated enormous wealth. The system we said couldn't work has worked spectacularly.

As we observe ICBC's next chapter, we're not just watching a bank—we're witnessing an experiment in alternative modernization. Every loan ICBC makes, every innovation it adopts, every crisis it survives provides data about whether state capitalism can sustainably create prosperity. The results so far suggest yes, but the experiment is far from over.

The story of ICBC is ultimately the story of China's rise, told through debits and credits rather than diplomacy and conflict. It's about a civilization reclaiming its historical position through financial engineering rather than military conquest. It's about proving that there are multiple paths to prosperity, not just the one prescribed in Chicago or Cambridge.

Whether ICBC maintains its dominance or eventually succumbs to its contradictions, it has already changed global finance forever. It proved that banks can be both commercial and political. It demonstrated that state ownership can coexist with public markets. It showed that Chinese characteristics aren't bugs to be fixed but features to be understood.

The dragon has awakened, and it speaks the language of money. Those who ignore its lessons do so at their peril. Those who understand its logic gain insight into the emerging world order. And those who invest alongside it—despite the risks, complexities, and contradictions—participate in the greatest economic transformation in human history.

ICBC's journey from communist policy bank to global financial titan isn't just a business story—it's a preview of the 21st century's defining contest between different visions of capitalism. The winner remains undetermined, but one thing is certain: the rules of money and power are being rewritten, and ICBC holds the pen.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube