SITC: The Intra-Asia Network Effect

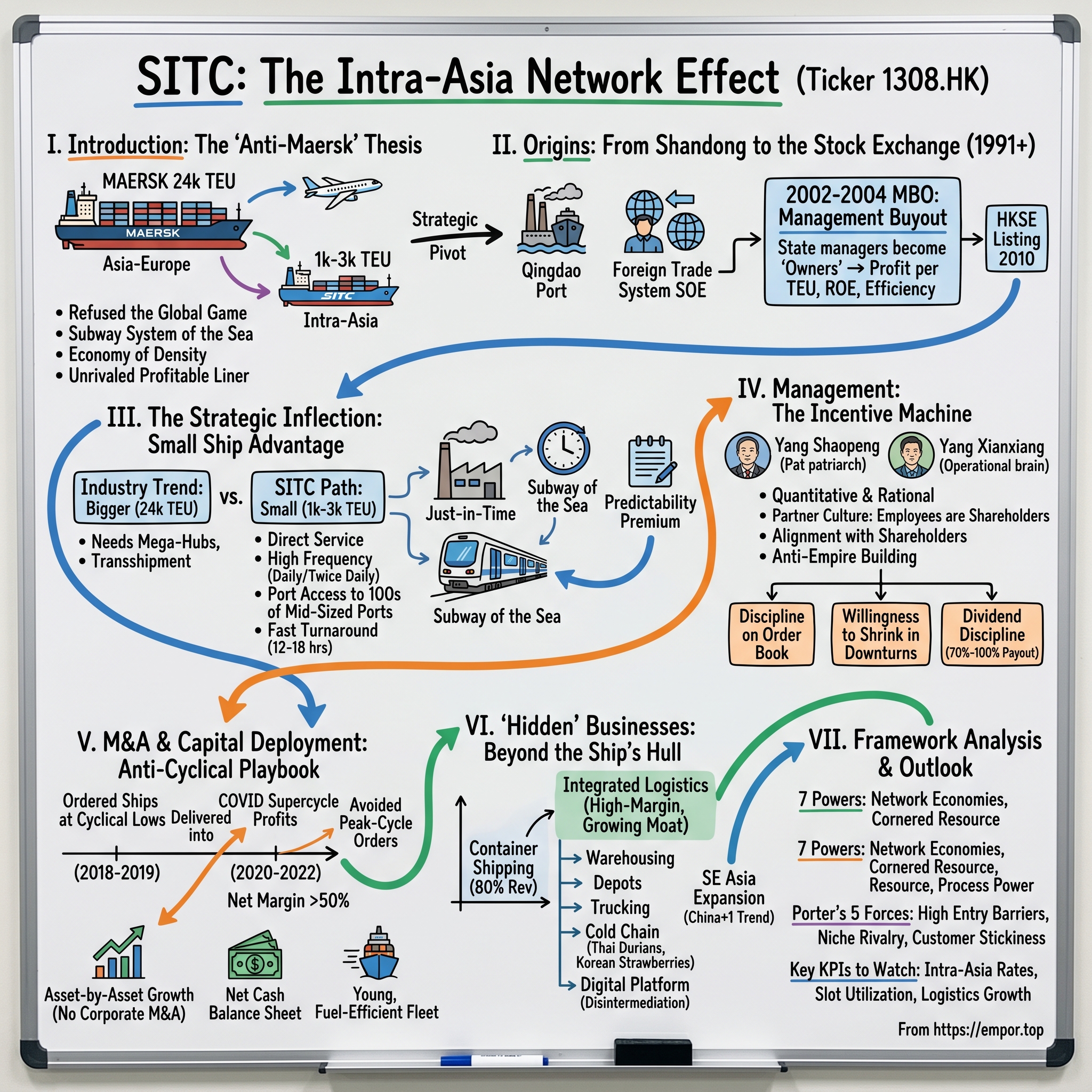

I. Introduction & The "Anti-Maersk" Thesis

Picture the Port of Rotterdam on a gray November morning. Stacked like a cityscape of Lego bricks, a 24,000 TEU behemoth—longer than four football fields—inches toward its berth. Tugboats nuzzle its flank. Gantry cranes, each the height of a twenty-story building, unfold above it in choreographed anticipation. This is the cathedral of modern globalization: Maersk, MSC, CMA CGM, COSCO, Hapag-Lloyd—five carriers who between them move roughly half the world's seaborne trade. They fight for every dollar of freight along the great trunk routes: Asia-Europe, trans-Pacific, trans-Atlantic. Their fortunes swing with the whims of Walmart's Christmas stocking plan, a Houthi missile in the Red Sea, or the price of a barrel of Brent crude.

Now zoom out and fly east. Skip past Suez, past the Gulf, past Singapore. Land in Qingdao, a coastal Chinese city better known for its beer than its ships. Here, in an office tower that would be unremarkable in Hong Kong, sits the headquarters of a company most global investors cannot name. SITC International Holdings. Ticker 1308 on the Hong Kong Exchange. A fleet of roughly 108 vessels, almost all of them small. None of its ships could even fit into the berths that big-liner executives obsess over. And yet, through cycle after cycle, SITC has posted returns that would make a luxury goods conglomerate envious. During the COVID supercycle, its net margins cracked 50%. Its return on equity, in multiple years, has landed north of 40%—in an industry whose long-term average hovers near zero.

The thesis of this episode is simple, but it cuts against every instinct a shipping analyst has been trained to follow. SITC is not really a shipping company. It is a high-density regional logistics network that happens to own ships. Where Maersk built an ocean highway, SITC built a subway system. Where the big carriers chase economies of scale, SITC harvests economies of density. And where the Western majors treat their fleets as commodity capacity, SITC's managers treat every TEU slot like a hotel room at a boutique resort—overbooked, priced dynamically, and rarely discounted.

Over the next three hours, we are going to trace how that happened. We will go back to the company's state-owned roots in 1991 Qingdao, through the management buyout that changed everything, into the counter-intuitive bet on small vessels while the rest of the world went mega-max, and into the playbook of a CEO, Yang Xianxiang, whose annual letters read more like Charlie Munger's than a shipping executive's. We will walk through the COVID-era masterstroke that made SITC one of the most cash-rich companies in Hong Kong. We will dig into the hidden land-side business that is slowly, quietly, building a second moat. And we will ask the hardest question of all: in a world where everyone now wants a piece of intra-Asia, can the "Subway of the Sea" keep running on time?

This is the story of a company that became the biggest fish by choosing a smaller pond—and then, once inside it, refused to let anyone else in.

II. The Origins: From Shandong to the Stock Exchange

Qingdao in 1991 smelled of salt air and possibility. Deng Xiaoping's Southern Tour was still a year away, but the city had already been designated one of China's coastal open cities, and its harbor—the same harbor that had hosted German gunboats and Japanese occupiers in the previous century—was being retooled for a new kind of trade. Into this cocktail of reform, uncertainty, and state-driven ambition, a modest enterprise was founded under the umbrella of the Shandong Province Foreign Trade system: a little shipping agent and freight handler that would, over the next decade and a half, quietly morph into SITC.

The company's earliest years were the kind of story that does not appear in slick investor decks. It was a state-owned enterprise, competing for cargo alongside other provincially administered shipping arms across the Chinese coast. Every major decision routed upward—through party committees, provincial commerce departments, and the usual thicket of approvals. Promotions had as much to do with seniority as performance. The fleet, such as it was, consisted of chartered tonnage and a few small owned vessels that plied routes between China and Japan, and China and Korea. This was not Cosco, not China Shipping. This was a niche regional player, and it knew it.

Two things, however, made the Shandong cradle unusual. First, Qingdao sits at the geographic heart of intra-Asian trade. It is roughly equidistant between the Yangtze River Delta, the Bohai Rim, Japan, and the Korean Peninsula. Ships bound for Osaka, Busan, and Shanghai could all leave from the same pier. Second, the cadres running SITC had lived their professional lives inside the Japan-Korea-China trade lane. They knew Komatsu's spare parts schedule. They knew which Korean chaebol needed aluminum coils on which day. They were not in awe of Long Beach or Rotterdam—they were obsessed with Yokohama and Incheon. That specialization, initially a limitation, would become a superpower.

Then came the turn of the century, and with it the transformational event: the management buyout. Between 2002 and 2004, in a process that was quietly facilitated by the state's broader reform of small and medium SOEs, the management team led by Yang Shaopeng—Yang Xianxiang's father and the company's strategic architect—acquired a controlling stake in the company. The details were, like most Chinese MBOs of the era, modest in size and enormous in consequence. Overnight, the men and women running the company stopped being salaried officials and became owners. The distance between the boardroom and the bottom line collapsed. Decisions that used to take a month were now made in an afternoon.

The cultural pivot that followed is the single most important fact in SITC's modern history. The state-owned instinct had been to maximize tonnage, maximize crew count, and maximize the flag-carrying presence of Chinese shipping on the world seas. The new owners flipped it. What mattered now was profit per TEU. What mattered was return on capital. If a vessel was not earning its keep, it would be sold or returned to its charterer, no matter how prestigious it looked in the fleet register. This language—ROE, profit per slot, capital efficiency—was rare in the Chinese shipping industry of 2005. At SITC, it became scripture.

By the time the company listed on the Hong Kong Stock Exchange in October 2010, the pivot was complete. SITC raised roughly HK$1.89 billion in an IPO that, by the standards of Chinese shipping IPOs, was undersubscribed in Hong Kong but oversubscribed globally. Most analysts who covered it filed the company under "small intra-Asia liner, nothing to see here." They filed it wrong. What they were looking at was a company that had already, years earlier, placed its strategic bet. The bet was this: the future of global trade was not a single great ribbon between East and West, but a dense, thickening mesh within East Asia itself. Call it "China plus one" before it had a name. Call it the regionalization of supply chains. SITC had been positioning for it since before the words existed.

As we move into the post-IPO years, the question the market kept asking—why on earth would you buy shares in a regional liner when you could own the big boys?—was about to get a very expensive answer.

III. The Strategic Inflection: The "Small Ship" Advantage

For anyone who lived through the 2010s in container shipping, one word dominated: bigger. The Emma Maersk, launched in 2006, carried 15,000 TEU and was hailed as a marvel. Within a decade, the industry had moved to 18,000 TEU, then 21,000, then 24,000. CMA CGM, MSC, and Maersk raced each other to the next tier, convinced that scale was the only moat that mattered. The logic was airtight on paper: a 20,000 TEU ship burns barely twice the fuel of a 10,000 TEU ship, so unit costs fall. The bigger the ship, the lower the cost per box. Therefore, if you are not building bigger, you are dying.

Except SITC heard all of this and did the opposite.

Walk down any Chinese shipyard between 2012 and 2022 and you would find SITC's orders lined up in a row, each one looking almost embarrassingly modest. The largest new ships the company has ever operated top out around 2,700 TEU. Most sit between 1,000 and 2,000 TEU. In an industry where the glamour ships now carry 24,000, SITC's fleet looks like a collection of speedboats next to aircraft carriers. And in that contrast lies one of the great strategic insights in modern transportation.

The big-ship strategy only works if you can fill the ship. A 24,000 TEU vessel sailing half-empty is a financial catastrophe. To fill it, you have to aggregate cargo from dozens of smaller ports into one or two mega-hubs, then transship. Every transshipment adds cost, time, and damage risk. The big-ship model, in other words, is a point-to-point long-haul system that only works on trunk lanes between mega-ports. It is Heathrow-to-JFK on a 747.

Intra-Asia is not that. Intra-Asia is hundreds of mid-sized ports, thousands of smaller shippers, and a fanatically just-in-time manufacturing base that hates transshipment. A Japanese automotive parts supplier sending aluminum castings to a Korean Tier-1 does not want its cargo loaded onto a feeder, shipped to Shanghai, transshipped to a mega-vessel, taken back to Busan, and then trucked inland. It wants a direct, reliable, high-frequency connection. A subway, not a freight train.

That is precisely what SITC built. By deploying small, nimble vessels, the company created a routing architecture that functions almost exactly like a metro system. Think of Shanghai-to-Osaka not as a single weekly voyage but as a daily or twice-daily service, with ships running back and forth on a near-bus-schedule basis. A factory manager in Suzhou can promise a Japanese customer a consistent 48-hour lead time because SITC has made that lead time a published timetable, not a negotiation. The value to the customer is not low cost per box—the mega-liners could theoretically offer that on paper—it is predictability. And predictability, in a just-in-time factory, is worth a premium of 10%, 20%, sometimes more.

The second advantage of small ships is port access. A 24,000 TEU ship needs a deepwater berth with specialized cranes and a draft of 16 meters or more. There are only a handful of ports in Asia—Shanghai Yangshan, Busan, Kaohsiung, Singapore, Yokohama—that can even accommodate one. A 1,500 TEU vessel can call almost anywhere. Haiphong, Qinzhou, Incheon Inner Harbor, Nagoya, Semarang, Hai An. This means SITC can offer direct service between combinations that the mega-carriers simply cannot serve without transshipment. On many of these secondary lanes, SITC is effectively the only high-frequency carrier. That is not competition. That is a natural monopoly on a niche corridor, repeated dozens of times across the map.

The third advantage is what operators call "turn." A small ship in a nearby port can be discharged and reloaded in 12 to 18 hours. A mega-vessel can take two to three days. In the space of a week, an SITC vessel might complete a full Shanghai-Osaka-Shanghai round trip, generating revenue on both legs. The asset works harder. This compounds the margin advantage: higher utilization, higher frequency, higher customer value, all on a vessel that cost far less to build.

There is, finally, a defensive dimension to the small-ship strategy. When freight rates collapse—as they did in 2015, 2016, and again in 2023—mega-vessels become stranded cost. Their owners have no choice but to keep sailing, because the fixed cost of a $150 million vessel demands revenue, even unprofitable revenue. Small vessels are far more flexible. Charter them out. Redeploy them. Scrap the oldest ones. SITC, which owns the majority of its fleet but charters to cover the peaks, can flex capacity up and down with a nimbleness the big liners envy.

Put all of this together and you arrive at a quiet, almost heretical conclusion: in intra-Asia trade, smaller is not just viable, it is better. The "Mega-Max" consensus, which swallowed so much capital between 2010 and 2020, left the most profitable slice of global container shipping strangely under-contested. While the giants fought over trunk-lane market share with rates that occasionally went below operating cost, SITC was quietly printing money in a market nobody wanted to compete in.

That sets up the obvious question. If the strategy was this powerful, why didn't everyone copy it? To answer that, we have to meet the people who built it.

IV. Current Management: The Incentive Machine

There is a particular kind of annual report, rare in the shipping industry, that reads less like a corporate filing and more like a conversation with a thoughtful business owner. The tone is dry. The humor is occasional and Chinese-inflected. The numbers are not dressed up. Losses are named; mistakes are acknowledged; predictions that failed to come true are revisited. If you have read enough Berkshire Hathaway letters, you know the rhythm. If you have read enough shipping reports, you find yourself reading SITC's with mild astonishment.

The tone starts at the top. Yang Shaopeng, the founding chairman, remains the patriarch of the company. But the operational mind—the one most investors have come to know through earnings calls, site visits, and the occasional measured appearance at industry forums—is Yang Xianxiang. He serves as the company's executive director and, in practice, the commercial and strategic brain of SITC. He is a second-generation operator, but unlike many second-generation heirs in Asia, he did not arrive to polish a trophy. He arrived to run a machine.

Yang Xianxiang's style has been described by industry colleagues as "unusually quantitative for a shipping man." He speaks in charter-rate spreads, in vessel day-cost deltas, in the inch-by-inch economics of a 1,700 TEU container lane. He is famously allergic to empire-building. There is a story—probably apocryphal, though it is repeated by multiple bankers who have pitched the company—that when a senior banker suggested SITC should take advantage of its COVID-era cash pile to make a major liner acquisition, the answer was a polite Chinese phrase that translates roughly to: "Why would we pay a premium for somebody else's mistakes?"

The second figure worth knowing is Xue Mingyuan, who has served in senior executive capacities overseeing the operational and commercial functions. The combination—Yang on strategy and capital allocation, Xue and a deep bench on execution—produced what investors have come to call the "SITC partner culture." Senior employees are not simply paid. They are shareholders, through a chain of investment vehicles that funnel economic interest down into the operational ranks. The result is a management team whose compensation rises and falls more or less in lock-step with dividends received. It is hard to overstate how different this is from the typical global shipping firm, where executive pay is determined by committee, benchmarked to peers, and almost always disconnected from free cash flow per share.

The ownership structure tells the same story. Through a holding vehicle that is typically described in filings as SITC Investment, founder-related interests hold a meaningful plurality of the company's economic stake. When you layer in the equity held by the broader management team, the inside ownership is substantial enough to ensure that, for the people running this business, what is good for the shareholder is very simply what is good for them. There is no principal-agent problem to manage, because the agents are the principals. It is a boring truth that most investors under-appreciate until the cycle turns—and then it becomes the only thing that matters.

What does this alignment actually produce? Three behaviors, all of them visible in the financial record.

The first is discipline on the order book. SITC has spent almost the entire cycle refusing to order ships when the market tells it to. The company's biggest newbuild commitments were placed during the depths of 2018 and 2019, when shipyard prices were at cyclical lows and most competitors were canceling orders. When global liners were tripping over themselves to order ultra-large vessels at peak prices in 2021, SITC was remarkably quiet. The cold math of ordering a small vessel that will be delivered two years later into an uncertain market is forbidding, and Yang's team has proven remarkably willing to walk away from temptations that look like obvious money at the time.

The second is the willingness to shrink. In the brutal freight-rate downturn that hit intra-Asia in late 2022 and 2023, many competitors kept sailing and kept chartering because they had to defend market share. SITC let its fleet size contract as charters rolled off and uneconomic lanes were suspended. In the company's commentary, the logic was simple: if the rate does not cover the cost, the ship does not sail. That sounds obvious, but almost nobody in the industry actually does it, because market share is religion.

The third behavior is dividend discipline. Over the past decade, SITC has consistently paid out between 70% and 100% of net earnings as dividends to shareholders. In the extraordinary years of 2021 and 2022, when freight rates exploded and SITC's profits went vertical, the company distributed nearly all of it. There was no vanity mega-order. There was no diversification into unrelated businesses. There was a dividend check, as large as the business could responsibly pay. The message to shareholders was: we cannot invest this money at anything close to your required rate of return, so we will send it back to you.

This is where the comparison with peers becomes uncomfortable. The world has watched ZIM, Israel's container liner, swing from blockbuster payouts during COVID to a dividend cut and massive losses afterward. It has watched HMM sit on tens of billions of dollars of cash and then face persistent government pressure over what to do with it. It has watched many storied lines squander their COVID windfalls on speculative vessel orders that are now delivering into a weaker market. SITC, by contrast, essentially returned the windfall, kept its powder dry, and kept its fleet young and efficient. When the next downturn came, shareholders had been paid. The business was still lean.

Yang Xianxiang's favorite line, relayed by multiple investors who have met with him, is a version of: we do not know where rates will be next year. We only know what our costs are, and we only pay for ships that work at today's rates. It is a startlingly simple rule, and it explains a great deal of what makes this company different.

The next logical question—what do you actually do with all that cash, if you are refusing to overpay for ships?—is the question that leads us into one of the most interesting capital allocation stories in recent shipping history.

V. M&A and Capital Deployment: The Anti-Cyclical Playbook

In early 2018, when SITC quietly placed an order for a series of 1,700 TEU newbuildings at a Chinese yard, the freight-rate environment was miserable. Intra-Asia rates had been battered for two years. BDI and SCFI indices were low. The consensus view was that a long, grinding period of overcapacity lay ahead. Analysts generally advised operators to hold off on newbuildings, pay down debt, and wait. A handful of Chinese brokerage reports, in fact, specifically flagged SITC's ordering activity as counter-cyclical and potentially risky.

It was counter-cyclical. It was not risky. It was one of the single most profitable capital allocation decisions any container liner made in the past decade.

By the time those ships began delivering in 2020 and 2021, the world had changed. COVID had blown up the supply chain. Port congestion turned 18-knot voyages into 14-knot slogs. Containers were stranded in the wrong places. Rates on the trans-Pacific famously exploded, but the intra-Asia rates, while less dramatic, also surged to multi-year highs. Every operator scrambled to add capacity. Chartering a vessel on the spot market became eye-wateringly expensive—benchmark short-term charters for feeder tonnage peaked at over $100,000 per day during parts of 2021 and 2022, up from $8,000 to $15,000 in normal times.

In that market, an SITC vessel ordered at 2018 prices and financed conservatively was effectively earning something close to a free margin spread. Its all-in daily cost, including depreciation, financing, and operating expenses, might land near $12,000 to $18,000 per day, depending on size. Its market-based revenue equivalent, at spot-charter rates, was a multiple of that. The profit difference—call it roughly $60,000 to $80,000 per vessel per day during the peak months—scaled across a fleet of around a hundred vessels and several hundred sailing days, and you begin to understand how SITC generated the multi-billion-dollar free cash flow it posted in 2021 and 2022.

The deeper story, though, is not just that SITC was lucky to have ordered at the bottom. It is that the company systematically avoided the mistakes its competitors made at the top. During 2021 and 2022, as freight rates screamed higher, global carriers went on a vessel-ordering spree. Capacity commitments placed during that window have been delivering into 2023, 2024, and now into 2025 and 2026—exactly as trade volumes have normalized and rates have cooled. For many operators, those orders now look like classic top-of-cycle overextension. SITC, watching the same market, ordered comparatively little. The company leaned instead on the depth of its existing fleet, the durability of its contracts, and the reinvestment into its land-side businesses.

The company's approach to M&A is equally distinctive, because it is essentially to not do M&A as it is conventionally practiced. SITC has never made a major corporate acquisition. It has not bought a rival liner. It has not tried to leapfrog into a new trade lane by acquiring a local champion. Instead, when it deploys capital for growth, it buys assets: specific vessels, specific warehouses, specific depots, specific pieces of logistics infrastructure in a specific port. This is sometimes called "brownfield bolt-on" strategy in infrastructure circles. It is a way of buying growth without paying for goodwill, overhead, or integration risk. The unit of acquisition is a wrench, not a company.

Consider the math that drives this. A corporate acquisition almost always involves paying a premium to book value, often to EBITDA, and inheriting a culture you have to either preserve or destroy. An asset acquisition costs what the asset is worth on that day, integrates instantly into existing operations, and can be scaled as demand dictates. For a company whose competitive advantage is cost discipline and operational homogeneity, asset-by-asset growth preserves the DNA. Corporate M&A would dilute it.

Within the asset-level category, SITC has been quietly building two portfolios. The first is the fleet itself: small, young, fuel-efficient vessels, increasingly dual-fuel or methanol-ready in the recent orders placed from 2023 onward in anticipation of tighter emissions rules. The second is the land-side logistics portfolio: depots in secondary Chinese ports, container freight stations in Vietnamese industrial parks, warehouses near the northern Thai border, handling facilities in Malaysia. None of these would make headlines. Together, they are stitching together the land side of the subway network.

All of this capital deployment, remarkably, has been financed out of operating cash flow and internal reserves. SITC has run at low leverage throughout the cycle. Its balance sheet after the COVID boom became something genuinely unusual in shipping: net cash, not net debt, even after paying out extraordinary dividends. That cash pile is itself a strategic weapon. When the next downturn comes—and in shipping, there is always a next downturn—SITC has the ammunition to buy distressed tonnage from weaker competitors at cycle-trough prices. This is exactly what the company has done in previous down-cycles, and there is every reason to expect the pattern to repeat.

The benchmarking exercise here is brutal. Over the last decade, SITC's cumulative shareholder returns, inclusive of dividends, have crushed almost every container liner in the world. HMM, despite its massive COVID windfall, has struggled to translate earnings into per-share wealth. ZIM made its shareholders spectacularly rich for two years and then gave much of it back. Maersk's decade-long transformation into integrated logistics has generated solid but not spectacular returns. SITC, quietly, without drama, paid out dividend after dividend, grew its intrinsic value, and never once needed to apologize for a bad order.

The question that logically follows is whether SITC is really a shipping company at all—or something else wearing shipping's clothes. The answer sits in the segments that do not get the headlines.

VI. The "Hidden" Businesses: Beyond the Ship's Hull

If you strip down SITC's segment disclosures and read them carefully, you will notice something curious. The container shipping and logistics segment accounts for roughly 80% of revenue. That is the headline. But underneath it sits a thicket of integrated services—warehousing, container depots, trucking, last-mile distribution, cold chain handling, digital platform services—that together represent a structurally higher-margin, less cyclical, and faster-growing set of businesses. Collectively these are often bundled into what the company calls "integrated logistics" or, informally, the land-side business. They are the hidden moat.

The story of how they came to be is a classic case of a company solving its own customers' problems, one at a time, until it realized it had accidentally built a second business. In the early 2010s, an SITC customer—say, a small Japanese industrial parts shipper—would often complain about the same friction: "Your ship arrives at Shanghai Yangshan fine, but then my cargo sits at the yard, waits for a truck, waits for customs, waits for the warehouse, and by the time it reaches my Chinese factory buyer, my reliability advantage is gone." SITC's response, over a period of years, was to start filling those gaps itself. If trucks were slow, SITC contracted dedicated trucking. If warehouses were mismanaged, SITC built its own. If customs was bureaucratic, SITC hired licensed agents. Slowly, the company became a door-to-door provider for a growing segment of its shippers.

By the mid-2020s, this land-side business had become one of the most interesting hidden assets in Asian logistics. The economics are different from shipping. Warehouse occupancy is driven by long-term contracts, not spot rates. Depot revenue is tied to container throughput, which grows smoothly with trade volume rather than swinging with charter markets. Trucking has meaningful barriers to entry in certain Chinese logistics parks, where bonded-zone licenses are scarce. Put together, these non-shipping segments have grown at a compound annual rate materially above that of the container shipping segment. Over time, their contribution to group profit has been growing, and their contribution to defensiveness—cash flow visibility, counter-cyclical stability—has been growing even faster.

Inside the land-side portfolio, one initiative is worth pausing on. Cold chain logistics in Asia is, by any reasonable measure, a structurally under-served market. The volume of perishable goods moving across Asian borders has grown dramatically as consumer diets upgrade: Thai durians into China, Vietnamese dragonfruit into Korea, Chilean cherries transshipped through Southeast Asian hubs, Japanese seafood into mainland markets, Korean strawberries into high-end Chinese retail. All of this cargo demands reefer containers (refrigerated boxes with temperature controls) and uninterrupted cold-chain handling from origin farm to destination shelf.

SITC has been steadily building out its cold chain capability. Smart reefers that remotely report temperature and location. Dedicated cold-storage warehouses near key cross-border nodes. Integrated customs and phytosanitary handling for specific product categories. The margins on this business are materially better than dry cargo shipping. A standard reefer slot on an SITC vessel is priced at a significant premium to a dry container, and the premium is stickier—because the customer cares far more about reliability than price. A ruined pallet of durians is a very expensive reminder that cheapest is not always best. SITC has quietly made itself one of the more trusted intra-Asia cold chain operators, and in a region where food trade will only keep growing, that is a durable position.

The digital layer sits on top of all of this. SITC's digital platform, which the company has variously branded around "Land-Sea" connectivity, is designed to let small and medium shippers interact directly with its operational backbone. A Vietnamese apparel exporter who used to go through a traditional freight forwarder—paying the forwarder's markup, tolerating the forwarder's opacity—can now book directly on a platform, track the container in real time, and manage the land-side handling through the same interface. The parallel in passenger travel is the move from travel agents to online booking. The move is not complete; large shippers still tend to work through forwarders or their own logistics departments. But for the long tail of SMEs, a carrier-operated digital platform is a meaningful disintermediation.

Crucially, the digital platform is more than a sales channel. It is a data advantage. SITC is building a live, proprietary view of container flows across dozens of Asian ports. That data feeds everything from vessel deployment decisions to empty-container repositioning to cold-chain capacity planning. Shipping companies that do not own their customer relationships are essentially blind. SITC, increasingly, is not.

The final piece of the non-core story is geographic expansion. The "China plus one" trend—the slow, structural migration of certain manufacturing activities from coastal China into Vietnam, Indonesia, Malaysia, and the Philippines—has been one of the defining trade stories of the 2020s. SITC, with its dense network of small-vessel routes, has been positioned for it longer than almost any other carrier. As Vietnamese electronics factories ramp up, as Indonesian textile parks expand, as Malaysian component makers take share, SITC's intra-Asia routes are where those exports travel. The company has been adding calls, opening offices, and investing in local handling capabilities in each of these markets. In a world where Southeast Asia is the fastest-growing export block, being the default intra-Asia carrier is a near-ideal place to stand.

Taken together, the hidden businesses change the investment case for SITC in a subtle but important way. If you think of the company as a pure liner, it looks like a well-run but cyclical shipping firm whose earnings will inevitably swing. If you think of it as an intra-Asia logistics platform that uses shipping as its backbone, the growth algorithm is different. Shipping provides the core cash flow. Land-side logistics provides the compounding. Cold chain and digital provide the margin uplift. The combined entity is less cyclical, more scalable, and structurally more valuable than any single piece.

The next natural question is how an outside investor is supposed to judge the moat. For that, we turn to frameworks.

VII. Framework Analysis: 7 Powers & Porter's 5 Forces

Whenever an investor encounters a business with persistently superior returns, the discipline is to ask: why hasn't competition eroded this? In shipping, which is famously commodified, that question becomes particularly important. Hamilton Helmer's 7 Powers framework and Michael Porter's 5 Forces give us two complementary lenses.

Start with Helmer. The most powerful of the seven powers operating at SITC is, clearly, Network Economies. A liner network's value scales nonlinearly with the number of ports served, the frequency of calls, and the density of the schedule. A Japanese OEM that needs to ship to twelve Chinese cities and six Southeast Asian countries cares enormously about whether a single carrier can serve all those routes reliably. Every time SITC adds a new direct lane, the marginal value of its existing network rises. This is why small competitors find it so hard to catch up: even if they match frequency on a single lane, they cannot match the network utility of SITC's 80-plus route structure. The network effect here is weaker than, say, Visa's, because customers can and do multi-home, but it is real, and it has been compounding for two decades.

Second, Cornered Resource. Preferred berthing slots at congested Asian ports are a scarce, non-replicable asset. When SITC signed its first long-term berthing agreements in ports like Shanghai, Ningbo, Osaka, Busan, Kobe, Yokohama, and Keelung in the 1990s and 2000s, it did so at a time when port authorities wanted reliable partners and were willing to give preferential treatment. Those slots, renewed repeatedly, are now nearly impossible to replicate. A new entrant trying to run the same frequency on the same lanes would find that the only available slots are the off-peak ones—and in shipping, timing is everything. Control of prime slots is a moat nobody outside the industry fully appreciates.

Third, Process Power. There is something SITC employees call, half-jokingly, "the SITC way" of vessel turnaround. It refers to the company's near-legendary efficiency in getting a ship in and out of port. The exact practices—preloading documentation before arrival, standardized crew drills, optimized stowage plans, integrated terminal relationships—are not individually proprietary. Taken together, they form a reliably faster turnaround than peers. This compounds into more sailings per year, higher revenue per vessel, and better on-time performance. Process power is often the most under-rated moat in operational businesses because it is invisible to outsiders. Here, it is crucial.

The remaining four powers—Scale Economies, Counter-Positioning, Switching Costs, and Branding—are also present but weaker. Scale economies exist at the regional network level (not the individual vessel level, because SITC chose small ships). Counter-positioning is visible in the fact that the big global liners structurally cannot replicate SITC's model without cannibalizing their trunk-route strategy. Switching costs are modest but real, especially in reefer and time-sensitive cargoes. Branding exists within the industry, less so outside it.

Now Porter. The question Porter's 5 Forces framework forces you to ask is: where does the margin actually come from?

Barriers to entry in intra-Asia shipping are far higher than they appear on the surface. Yes, anyone can buy a ship. But replicating SITC's network requires simultaneous access to scarce port slots, decades-old customer relationships, licensed land-side operators, and an intra-country logistics web. A greenfield competitor with $2 billion of capital would struggle to be taken seriously on core lanes for a decade. This is a structural disadvantage for would-be entrants, and it has held up remarkably well.

Competitive rivalry is where SITC looks most differentiated. The big global liners—COSCO, Maersk, Evergreen, CMA CGM—all run intra-Asia operations, and in nominal capacity terms they are larger than SITC. But those operations are structured as feeder networks for their trunk-route businesses, which means they are optimized around transshipment and hub-and-spoke, not around direct service. SITC competes head-on only where its direct-service model and the mega-carriers' feeder service model overlap, which is a surprisingly small slice. On many niche corridors—Shanghai-to-secondary-Japan-port, Shanghai-to-Thailand-inland, Korea-to-Indonesian-outer-port—SITC has effectively no direct competition.

Threat of substitutes is limited but worth naming. Rail, air, and overland trucking all compete with short-sea shipping for certain goods. Overland rail (the Belt and Road rail corridors between China and Southeast Asia) can substitute for some near-border cargo, though capacity constraints and reliability issues continue to limit that substitution. Air competes only for very high-value, time-sensitive cargo, where the volume is small. For the vast middle of intra-Asia manufactured goods and components, short-sea shipping is structurally dominant.

Bargaining power of customers is split. Very large shippers (multi-nationals with massive annual contracts) have meaningful leverage and routinely extract volume-based pricing concessions. But the long tail of small and medium shippers—who collectively represent a growing share of SITC's volume—have far less leverage, especially on niche lanes where SITC is effectively the only viable direct provider.

Bargaining power of suppliers is worth watching. Shipyards, particularly Chinese and Korean yards, control the supply of new vessels. Port authorities control berths. Fuel suppliers control bunker costs. Each of these has the power to squeeze liner margins in certain conditions. SITC has managed this by maintaining long-standing yard relationships (especially with Chinese yards for its core fleet), locking in fuel contracts where practical, and diversifying its port relationships so that no single authority has too much leverage.

The synthesis of all of this is straightforward. SITC operates in an industry that is, in aggregate, a famously bad business—capital-intensive, cyclical, commoditized, low-return. But within that industry, SITC has identified a structural niche where the normal rules do not apply. Within that niche, it has built a moat stack—network economies, cornered resources, process power—that has let it earn unusually high, unusually persistent returns on capital. The question for the future is whether the niche is durable. That is exactly where the bull and bear cases diverge.

Before we get there, though, there are lessons in this story that generalize.

VIII. The Playbook: Lessons for Investors & Founders

Every great business case has a set of transferable lessons, and SITC's story contains several of the clearest in modern Asian corporate history. They are worth spelling out because they contradict some of the most popular wisdom in business strategy today.

The first lesson is niche over scale. The dominant narrative of the last twenty years of global capitalism has been that scale always wins. The bigger the platform, the bigger the advantage. The bigger the data asset, the more unassailable the position. The bigger the ship, the lower the cost per box. That story is not wrong, but it is incomplete. For every category where scale dominated, there has been another where scale created brittleness, and where a well-chosen niche compounded to a better outcome. SITC chose to be the biggest player in the fragmented, high-density intra-Asia market rather than the number-eight player in the global mega-trunk market. The result was superior returns for two decades. In industries with complex local variation and high switching friction, being the biggest fish in a well-chosen pond often beats being a minnow in the ocean.

The second lesson is asset-right, not asset-light. The post-2010 startup world fell in love with asset-light models, often for good reasons. Capital efficiency is a virtue. But it is a mistake to confuse asset-lightness with capital efficiency. Some assets are bottlenecks. The right question is not "do I own assets?" but "do I own the assets that other people need?" SITC owns the ships, the port slots, the depots, the warehouses in the right places. It does not try to own the entire supply chain. It owns the scarce, defensible pieces and leaves the rest to partners. That is asset-right, and it is materially different from being either asset-heavy or asset-light. In a world where too many businesses have over-outsourced their way into becoming commodity resellers, SITC's model is a reminder that owning the right assets is a moat.

The third lesson is the power of alignment. Management teams that think like owners behave differently from management teams that think like employees. The difference shows up in the boring, repeated decisions: whether to order ships at a market peak, whether to chase market share during a downturn, whether to pay the dividend or hoard the cash. SITC's founding family and senior executives, collectively holding a meaningful equity stake, have behaved with remarkable consistency. They have not diversified into unrelated industries to justify their bonuses. They have not gotten into bidding wars to save their pride. They have not, most importantly, sacrificed per-share returns for enterprise growth. Alignment is not a magic solution to all governance problems, but it is the single most powerful lever available in Asian family-founded companies, and SITC is one of its cleanest examples.

The fourth lesson is customer centricity in a commodity industry. Shipping is, in theory, a pure commodity. A TEU is a TEU. But SITC has shown that if you build the schedule around the factory's needs rather than the ship's capacity, you can create pricing power even in a commodity. A Japanese auto parts supplier does not choose SITC because SITC is the cheapest. It chooses SITC because SITC's schedule aligns with the factory's production rhythm. That alignment—frequent sailings, predictable transit times, flexible volume adjustments—creates a relationship that is far stickier than price. The broader lesson is that in any commodity industry, the real premium is for reliability and integration, not for the lowest quoted price.

The fifth lesson, perhaps the most subtle, is anti-cyclical discipline. The shipping industry has been ruined for generations by one recurring behavior: ordering ships at the top of the cycle because the cash is there. It happened in the 1970s. It happened in the 2000s. It happened again in 2021. SITC has managed to do the opposite—ordering when yards are hungry and prices are depressed, refusing to order when everyone else is. This is not because the management team has a magic crystal ball. It is because their incentives reward long-term per-share returns rather than short-term growth. They have institutionalized a rule: never pay for capacity at peak prices. It sounds obvious. Almost no one does it.

The meta-lesson, across all five, is that great businesses are often built on principled, patient contrarianism. They are built by people willing to be wrong in the short term to be right in the long term. And in an industry as cyclical, capital-intensive, and ego-driven as shipping, that kind of discipline is a competitive weapon the incumbent players cannot easily copy, because copying it would require them to change who they are.

With the framework clear, the honest next step is to stress-test it. What could go wrong?

IX. Bear vs. Bull Case

The bear case on SITC begins with a truth every shipping investor eventually learns: no moat in this industry is permanent. Oceans change. Trade lanes shift. Port relationships erode. And the minute a model becomes famous enough to appear in case studies, the clock starts ticking on its imitators.

Start with competitive imitation. The small-vessel, high-frequency intra-Asia playbook is no longer a secret. Global liners have started to pay more attention to their intra-Asia feeder operations. Regional players—Wan Hai, Sinokor, Heung-A, TS Lines, Interasia—have gradually expanded. Chinese state-owned carriers have ambitions to grow their feeder networks. The "ship glut" scenario—where too many operators chase the same intra-Asia TEU—is a real risk. If intra-Asia capacity grows faster than intra-Asia demand, even SITC's superior cost and schedule cannot fully protect margins. This played out in a milder form in 2023, when intra-Asia rates cooled materially after the COVID peak and competitors that had added capacity suffered. SITC was insulated, but not immune.

Second is geopolitical friction. SITC's fleet spends an enormous number of days per year navigating the East and South China Seas. Tensions around Taiwan, the Korean Peninsula, and the South China Sea are persistent and have escalated at various points. A serious regional conflict—most obviously around Taiwan—would disrupt the very lanes that form SITC's highest-margin corridors. Unlike a global liner that can redeploy tonnage to trans-Pacific or Asia-Europe routes, SITC is structurally concentrated in the region that is geopolitically hottest. This is a true tail risk, not a likely scenario, but it is the kind of risk that can impair intrinsic value overnight.

Third is key person risk. The intellectual and cultural center of gravity of SITC is a small group of senior executives, with Yang Xianxiang central among them. Their instincts, their discipline, their willingness to say no to bad deals—those qualities are not easily institutionalized. A succession event, voluntary or otherwise, would be a genuine test. The company has developed a deep managerial bench and has visible partner-culture practices, but the identity of SITC as a disciplined capital allocator is still, to a meaningful extent, the shadow of its current leadership.

Fourth is regulatory and environmental risk. International Maritime Organization rules around carbon emissions—the IMO's progressive tightening of CII (Carbon Intensity Indicator) and EEXI (Energy Efficiency Existing Ship Index) thresholds, along with the EU's inclusion of maritime shipping in its Emissions Trading System since 2024—are raising the operating cost of older, less efficient tonnage. SITC's modern fleet has a meaningful advantage here, but the regulatory environment is still unsettled. The cost of methanol, LNG, or ammonia fueling at scale is unclear. Bunker cost volatility could hurt margins. The next fifteen years of shipping regulation will look nothing like the last fifteen.

Finally, there is the commoditization risk on the land side. The non-shipping businesses are a genuinely attractive growth vector, but Asian logistics is one of the most competitive industries on earth. Local players with superior last-mile expertise, digital-native freight-forwarding startups, and well-capitalized 3PLs all compete for the same wallet. SITC's advantage here is its integration with its shipping backbone. That integration is real, but it is not invincible.

The bull case pushes back on every one of these concerns.

On permanent regionalization, the structural drivers of intra-Asia trade growth look extremely durable. The ASEAN-China supply chain network is deepening. Indian component exports to ASEAN are rising. Korean and Japanese manufacturing continues to reorganize around multi-country networks. The gradual deglobalization of Western trade with China—if anything—intensifies the importance of intra-Asia flows, because regional self-reliance depends on regional shipping. SITC is positioned exactly where the secular trend is strongest.

On capital armory, SITC's balance sheet is one of the most resilient in the industry. Net cash, high dividend cover, low CapEx discipline, and a young fleet together form a fortress that most peers cannot match. In the next downturn—whenever it arrives—SITC will be one of the few operators able to buy distressed tonnage cheaply, take share, and emerge stronger. This pattern has played out three times in the company's history, and the bull case is that it will play out again.

On green shipping, the emerging carbon-cost regime is arguably a tailwind for SITC rather than a headwind. The company has been ordering dual-fuel-capable vessels and methanol-ready hulls. Older, less efficient tonnage from competitors will face rising carbon surcharges. A carrier with a modern, efficient, young fleet has a durable unit-cost advantage against operators clinging to aging ships. The parallel is with airlines in the 2010s: carriers with modern fleets had structurally better economics than carriers hauling around a legacy wide-body inventory.

On the land-side growth ramp, the non-shipping businesses are still in relatively early innings. Cold chain is a secular winner. Digital freight platforms in Asia are underpenetrated versus their Western peers. Southeast Asian warehousing is one of the most attractive logistics asset classes globally. SITC has quietly built beachheads in all three. If even a portion of the expected growth materializes, the land-side businesses can evolve from being supporting cast to being a primary profit driver, smoothing cyclicality and adding a premium multiple to the consolidated valuation.

On governance, the partner culture and alignment structure are well-established and largely institutionalized. Yang Xianxiang and the senior team continue to run the company with the same discipline investors have come to expect. The board and the broader management team have grown organically over the years rather than being assembled top-down.

If you push through all of this and ask what investors should watch, the answer is surprisingly narrow. There are, across the full complexity of the business, two or at most three KPIs that matter most for tracking SITC's ongoing trajectory.

The first is intra-Asia freight rate indices, specifically the Shanghai-to-Japan, Shanghai-to-Korea, and Shanghai-to-Southeast-Asia lane rates as reported in the Shanghai Shipping Exchange's SCFIS sub-indices and, where available, specialized intra-Asia rate trackers. These directly drive the core shipping segment's top line and, by extension, margin. Even a few percentage points of rate movement show up dramatically in operating profit given SITC's stable cost base.

The second is fleet utilization, or more specifically, slot utilization on core lanes. SITC has historically run at exceptionally high utilization—often mid-90% or higher on core intra-Asia routes—which is a direct measure of whether the network-density advantage is holding. If utilization begins to slip materially, it would be an early signal that either competition is intensifying or demand is softening faster than SITC can flex supply.

The third, less universally tracked but increasingly important, is the integrated logistics (land-side) segment's revenue growth and operating margin. This segment is the most important non-shipping lever in the investment case. Its trajectory—growing faster than the core, holding or expanding margins—validates the thesis that SITC is evolving into a true logistics platform. If that segment stalls, so does the highest-multiple piece of the story.

Everything else—fuel price sensitivity, individual port congestion metrics, currency moves, specific customer wins—matters, but it matters less than these three anchors. Investors tracking SITC well are tracking intra-Asia rates, slot utilization, and the land-side growth rate.

X. Epilogue & Final Reflections

Go back to Qingdao. The year is now 2026. Walk along the same waterfront where, decades earlier, a small state-owned shipping office was rearranging its desks for a new reform era. The harbor is busier. The skyline is denser. The ships nosing in and out are bigger, but the ones that carry SITC's red-and-white funnels are not the biggest. They are, by design, the right size.

The story of SITC is in many ways a story about choosing not to grow into what you could have grown into. The company had every opportunity, during the 2010s, to chase trunk-route glory. It had every opportunity, during the COVID boom, to do what HMM did with a massive cash pile and become a "diversified shipping conglomerate." It had every opportunity, when banks were lining up to lend, to lever up and order mega-ships at peak prices. It said no to every one of those temptations. The no was the strategy. The no was what created the miracle.

A Chinese shipping executive once said, in a quiet aside at an industry conference, that what made SITC extraordinary was not any single decision but the accumulation of boring discipline over twenty years. The company had refused to overpay for assets. It had refused to chase market share. It had refused to confuse enterprise growth with per-share value creation. Most importantly, the people running it had refused, again and again, to behave like employees of a public company and had instead behaved like long-term owners. The result, compounded across two decades, was a business that earned multiples of its industry peers' returns on capital while paying out most of it to shareholders.

The "Subway of the Sea" metaphor is useful precisely because it captures what is hardest to imitate. A subway's value is not in any single train. It is in the density of the network, the reliability of the schedule, the familiarity that a commuter builds over years, and the political-economic relationships that make it impossible for a competitor to simply lay new rails. Container shipping is not rail, but intra-Asia short-sea shipping has, in SITC's hands, taken on something of the same character. The company's ships are trains. Its port slots are stations. Its land-side warehouses are the extension of the transit card to the last mile. And its loyal base of industrial shippers is the equivalent of a commuter who has stopped checking the schedule because the schedule is always there.

There will be cycles ahead. There will be rates that crash and rates that surge. There will be disruptive events—pandemics, wars, canal closures, carbon shocks—that nobody has yet modeled. And through all of it, the question for SITC will be the same one Yang Xianxiang has effectively been answering for two decades: are we still earning our cost of capital on every slot, every warehouse, every fresh order? If the answer is yes, the dividend continues. If it is no, the fleet contracts. No ego, no growth-for-growth's-sake, no apology.

In an industry famously plagued by ego, vanity orders, and ruinous capital cycles, that kind of discipline is itself the moat. The ships are ordinary. The ports are ordinary. The routes are ordinary. The discipline is not.

That is the SITC story. A boring, beautiful machine, built in a quiet corner of Asia, running a timetable the rest of the industry is still trying to understand.

XI. Top 5 "Long Form" References & Reading

-

SITC Annual Reports (2010–2025) — The Management Discussion & Analysis sections, particularly those authored during the 2018 newbuild cycle and the 2020-2022 COVID windfall, offer some of the most candid capital-allocation commentary in Asian shipping. Read them alongside the dividend declarations to see how discipline translates into distributable cash.

-

DynaLiners Weekly and Alphaliner Monthly Monitors — For benchmarking intra-Asia deployed capacity, market share shifts, and competitor fleet movements. These are the gold standard for independent data on Asian container shipping and remain indispensable for anyone tracking the regional trade flows SITC dominates.

-

"The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger" by Marc Levinson — Essential macro context for the containerization revolution. Levinson's account of how a simple steel box transformed global trade is the foundation for understanding why intra-Asia, as a late-stage containerization beneficiary, has become one of the most dynamic trade corridors on earth.

-

SITC's Strategic Vision Communications (2020–2025) — The company's investor presentations, particularly those detailing cold chain infrastructure build-out, digital platform strategy, and Southeast Asian expansion, provide critical color on the non-shipping businesses that are quietly reshaping the equity story.

-

Academic and Industry Case Studies on Chinese SOE Management Buyouts (2002–2005) — For understanding the unique governance transition that turned a provincial state-owned shipping agent into an incentive-aligned private enterprise. The MBO template that transformed SITC is one of the cleanest case studies in modern Chinese corporate governance and explains much of what makes the company's behavior so unusual within its industry.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube