Nan Ya Plastics: The King of PVC's Secret Semiconductor Lifeboat

I. Introduction: The Polyvinyl Trojan Horse

Walk into almost any hardware store in Taipei, Kaohsiung, or Taichung and you will find the company hiding in plain sight. The grey PVC pipe stacked in the corner, the vinyl flooring rolled against the wall, the plastic wrap at the checkout counter, the polyester in a cheap raincoat — a startling share of it traces back to a single corporate parent that most Taiwanese consumers file mentally under "old economy." For three generations, 南亞塑膠工業股份有限公司 Nan Ya Plastics Corporation has been the workhorse of everyday Taiwanese materials, the maker of unglamorous stuff you use without ever noticing the brand.

Now travel to the other end of the economy — to the clean rooms of advanced packaging houses, to the assembly lines building AI servers around NVIDIA accelerators, to the procurement desks of the world's largest cloud companies. Ask the engineers there what keeps them up at night, and a surprising number will name the same company. Not for pipes. For the razor-thin sheets of copper-clad laminate and the ultra-fine glass fiber that sit underneath the most expensive silicon on Earth. To that audience, Nan Ya is not a plumbing supplier. It is a gatekeeper.

This is the central paradox of the company trading under ticker 1303.TW on the 台灣證券交易所 Taiwan Stock Exchange. It is simultaneously one of the most old-fashioned industrial businesses in Asia and one of the most quietly essential suppliers to the AI hardware boom. In 2025 it generated roughly NT$260 billion in revenue — on the order of US$8 billion — making it one of the cornerstone members of the sprawling 台塑關係企業 Formosa Plastics Group.1 And through a controlling stake of just under 67% in IC-substrate maker 南亞電路板股份有限公司 Nanya PCB, it reaches directly into the beating heart of advanced semiconductor packaging.2

Here is the dramatic tension that makes Nan Ya worth two hours of your attention. The businesses that built this company — commodity petrochemicals like ethylene glycol and bisphenol-A, plus bulk polyester fiber — are trapped in a structural depression. Not a normal down-cycle, but something closer to a permanent regime change, driven by a wall of state-subsidized capacity coming out of mainland China. Those legacy segments are bleeding. And yet the company is not merely surviving. It is executing a pivot, three decades in the making, toward a high-value Electronic Materials segment that management has said it wants to lift past 60% of revenue by the end of 2026, up from just over half.3

The company itself frames this as a triumphant transformation. Our job here is not to take that framing at face value. It is to ask the harder questions. Is the electronics business genuinely a durable moat, or a cyclical bounce dressed up as a secular story? Is the pivot fast enough to outrun the collapse in chemicals? And what does it mean that this "technology company" still carries a DRAM stake that has vaporized capital for years? Those are the questions a skeptical long-term investor should be asking, and they are the ones we will test.

Our roadmap follows the arc of the company itself. First, the genesis — the post-war rise of the Wang brothers and the founding of a plastics empire out of near-bankruptcy. Then the vertical-integration playbook that carried a resin processor, improbably, into fiberglass and copper foil. Then the petrochemical pincer, as Chinese self-sufficiency gutted commodity margins and Beijing dismantled the tariff preferences that once made cross-strait chemical exports viable. Then the AI lifeboat itself — the laminates, the specialty glass, and the substrates that now anchor the growth story. And finally the capital-allocation puzzle: the cross-shareholdings, the family foundations, and the awkward economics of a parent company perpetually rescuing its siblings.

The through-line is a question about the nature of moats. Nan Ya's defenders argue it has built something rivals cannot copy — a fully integrated materials stack, from raw glass and epoxy chemistry all the way to finished laminate. Its critics argue it is a lumbering conglomerate whose few good assets are trapped inside a low-return structure. Both can be partly true. Let's find out how much.

It helps, before we start, to appreciate the sheer physical scale of what we are describing, because the numbers can lull you into thinking of Nan Ya as a mid-cap. It is not. On any given day it is running plastics-processing lines, polyester spinning, bulk-chemical reactors, glass-fiber furnaces, copper-foil electroplating baths, and copper-clad-laminate presses across dozens of plants in Taiwan, mainland China, and the United States, employing on the order of tens of thousands of people. Its revenue puts it comfortably among the largest industrial companies in Taiwan, and it is one of a small handful of listed anchors — alongside Formosa Plastics Corporation, Formosa Chemicals & Fibre, and Formosa Petrochemical — that together constitute the group that Wang Yung-ching built into a pillar of the island's economy. When a company of this heft turns from petrochemicals toward electronics, it is not a startup pivot. It is an aircraft carrier changing heading, and the interesting question is whether it can turn fast enough before the seas it was built for close in around it.

II. The Genesis: The Wang Brothers & The Cost-Control DNA

The origin story begins not with plastics but with rice. In the 1930s, in the hardscrabble tea-farming hills of Japanese-colonial Taiwan, a teenager named 王永慶 Wang Yung-ching left school around the age of fifteen and, with a small borrowed sum, opened a rice shop in the town of Chiayi. The legend — and in Taiwan it is very much a legend — is that Wang out-hustled his competitors through obsessive attention to detail no one else bothered with. He would sift the grit and stones out of his rice by hand when rivals sold it dirty. He kept notebooks on each household: how many people lived there, how much rice they ate, roughly when they would run out. Then he would show up at the door with a fresh sack before the customer even knew they needed one, and he would carry it into the kitchen and pour it into the jar himself, oldest rice on top so nothing spoiled.

Strip away the folklore and what remains is the DNA of everything that followed. Wang did not win on a better product — rice is rice. He won on system, on service, and on a fanatical, penny-by-penny grip on cost and waste. That instinct, formed over a rice barrel during a colonial depression, would later be scaled into one of Asia's largest industrial groups. Alongside him for much of the journey was his younger brother 王永在 Wang Yung-tsai, the operator and builder to Wang Yung-ching's strategist — the pair became inseparable as a management partnership, and the family's dual-brother structure would echo through Formosa's governance for decades.

The rice shop did not last; wartime rationing and the disruptions of the 1940s wiped out much of what Wang had built, and he spent the interwar and post-war years bouncing through other trades — timber, brick, and small commerce — accumulating capital and, more importantly, the operational scar tissue of someone who had already been to the edge of ruin once. By the time the plastics opportunity arrived, Wang was in his late thirties, no longer a naïve merchant but a hardened operator who understood in his bones that survival in commodity businesses is won on cost discipline, not on cleverness. This matters because it explains the psychology of the empire that followed: Formosa and Nan Ya were never run like companies chasing the next exciting thing. They were run like companies that had once nearly starved and never intended to again. That defensive, cost-first mentality is the single most important cultural fact about the group, and it explains both its extraordinary resilience and its congenital slowness to abandon a losing business.

The pivot into chemicals came in 1954, and it came with a push. In the reconstruction years, U.S. aid money was looking for Taiwanese entrepreneurs willing to build basic industry. Backed by an American-supported development loan, Wang founded 台灣塑膠工業股份有限公司 Formosa Plastics Corporation and bet on polyvinyl chloride — PVC, the workhorse plastic of pipes, cables, and flooring. It was, by most accounts, a decision made on the advice of others as much as personal conviction, and it nearly ended in disaster. When the first plant opened, it produced a few tons of PVC resin a day and could sell almost none of it. Taiwan in the mid-1950s had essentially no downstream plastics-processing industry. There was nobody to buy the raw powder.

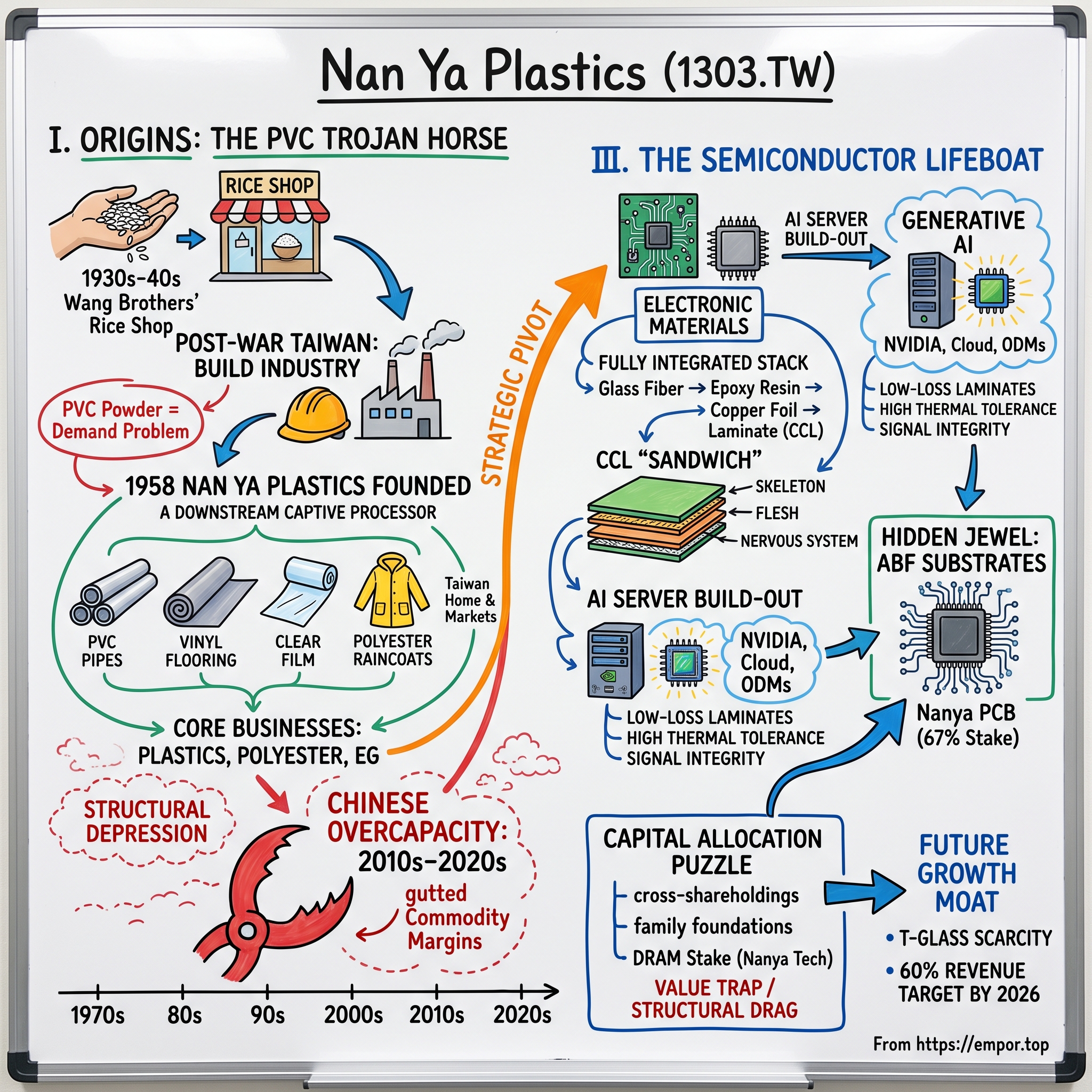

Most first-time industrialists would have folded. Wang did the opposite — he doubled down, and in doing so stumbled onto the strategic move that would define the entire group. If no one would buy his resin, he would build the customer himself. In 1958 he established Nan Ya Plastics as a captive downstream processor whose founding mandate was blunt: absorb Formosa's excess PVC resin and physically convert it into things people could actually use — pipes, sheeting, artificial leather, film, raincoats.4 Nan Ya was, quite literally, created to solve a demand problem for its own parent. It was demand-creation by vertical integration before anyone in Taipei used those words.

This is the first thing to understand about Nan Ya, because it never really changed. The company was not born to invent premium products at high margins. It was born to take a commodity input off its sibling's hands, run it through heavy processing at relentless cost efficiency, and sell the output in volume. Value came from the system, not the molecule.

Over the following decade that system compounded. Formosa integrated upstream toward the chemistry; Nan Ya pushed downstream toward the customer and outward into new outlets for the group's growing stream of chemical intermediates. The most consequential expansion came in the 1970s, when Nan Ya moved aggressively into polyester — fibers, yarns, and films — riding the global textile boom. It became one of the largest polyester producers on the planet, and for years polyester and plastics processing were the twin engines of the business. The logic was, again, integration: polyester consumed ethylene glycol and other intermediates the group could supply, closing another loop.

The polyester bet is worth pausing on, because it is the template for everything Nan Ya later did in electronics, just in a lower-tech key. The move worked for the same integrated reason PVC did: the group could feed the new business with intermediates it already made, capturing margin at multiple stages instead of buying inputs from strangers. Polyester also plugged Nan Ya into a genuinely global growth wave — the explosion of synthetic textiles that reshaped the world's clothing industry from the 1970s onward — and for a couple of decades it delivered exactly the kind of high-volume, cost-driven scale the company was built to exploit. The catch, invisible at the time, was that polyester is a commodity, and commodities eventually attract exactly the kind of low-cost mega-scale competition that would one day arrive from mainland China. The same pattern — win big on integrated commodity scale, then watch a state-backed competitor flood the market decades later — would repeat with almost eerie precision in bulk chemicals. Nan Ya's history rhymes with itself.

By this era the Formosa culture had hardened into something distinctive and, to outsiders, slightly intimidating. Wang Yung-ching preached a management philosophy Taiwanese business students still study, often rendered as 異常管理 — "abnormal management," the practice of drilling relentlessly into every deviation from expected cost until you find its root cause. Every kilogram of raw material, every labor-hour, every machine cycle was benchmarked, tracked, and interrogated. The point was not cost-cutting as an occasional campaign; it was cost-control as a permanent nervous system running through the whole organization. Wang built a large in-house team of industrial engineers whose entire job was to find fractions of a cent, and he institutionalized it through a central management office that policed cost performance across every group company. The famous artifacts of this culture — Wang's insistence on precise data, his early-morning meetings, his personal interrogation of managers over tiny variances — became case studies in Taiwanese business schools. Whatever else you think of Formosa, no one has ever accused it of not knowing its costs to the last decimal.

For investors, this founding chapter carries a lesson that outlasts the founders. Nan Ya's competitive edge, from day one, was never product innovation. It was system-level vertical integration, absolute cost leadership, and the willingness to manufacture its own demand when markets failed to provide it. Hold that thought, because in the 1980s that exact instinct — build the whole chain yourself, control every cost layer — would carry a plastics processor into a business that had nothing to do with plastics, and everything to do with the future.

III. The Great Pivot: Designing the Electronics Lifeboat

Picture the mood in Taiwanese industry in the early-to-mid 1980s. The government was orchestrating a national turn toward high technology; the Hsinchu Science Park was filling up, and a state-backed foundry called TSMC would soon be spun out of a research institute to change the world. In that atmosphere, a plastics and petrochemicals patriarch in his late sixties looked at his own empire and saw a vulnerability that the good years were hiding: commodity chemicals are viciously cyclical, exposed to every swing in oil prices and global demand, and structurally incapable of ever escaping that gravity. Wang Yung-ching's conclusion was that Nan Ya could not stay what it was forever. It had to find a business with a steeper, longer growth curve — or it would slowly become a relic.

The context here is essential, because Nan Ya was not moving in isolation — it was riding a national tide. Taiwan in the 1980s was in the middle of a deliberate, state-choreographed transformation from a low-cost manufacturing economy into a technology powerhouse. Government research institutes were spinning out semiconductor ventures; the Hsinchu Science Park was becoming a magnet for returning engineers trained in the United States; and an entire ecosystem of component suppliers, assemblers, and board makers was coalescing around the emerging electronics cluster. For a group as large and as plugged-in as Formosa, the direction of travel was unmistakable. The question was not whether Taiwan would build a technology industry, but whether Nan Ya would supply it or watch from the sidelines as a pure old-economy relic. Wang chose to supply it — and to supply it at the layer he understood best, materials, rather than trying to leapfrog into chip design where he had no edge.

The obvious question was: why would a maker of pipes and polyester think it could win in electronic components? The answer, and it is the whole key to the story, is that Wang did not see electronics as foreign territory. He looked at what a printed circuit board actually is, physically, and saw two things Nan Ya was already world-class at. First, chemistry — the boards are held together by epoxy resins, and Nan Ya's chemical streams could feed exactly that. Second, precision heavy manufacturing — the boards are built by laminating layers under heat and pressure, which is not conceptually far from what Nan Ya already did at industrial scale. Where outsiders saw a leap into semiconductors, Wang saw an adjacency he could attack with the cost-control machine he had spent thirty years building.

So Nan Ya made a bet that looked, at the time, slightly crazy: rather than buy laminates on the open market or assemble components from other people's parts, it would build the entire upstream stack of the copper-clad laminate itself. To understand why that mattered, you need to understand what a copper-clad laminate — CCL — is, because it sits at the physical foundation of nearly every electronic device.

Think of a CCL as a high-tech sandwich. In the middle is a woven cloth of glass fiber, which gives the board its rigidity and dimensional stability — the skeleton. That cloth is soaked in epoxy resin, which hardens into the insulating body and glues everything together — the flesh. And on the outside are ultra-thin sheets of copper foil, which get etched into the circuit traces that carry electrical signals — the nervous system. Stack and press these together and you get the rigid green board that every chip eventually sits on. It is mundane and utterly indispensable.

Most CCL makers buy their glass cloth, their resin, and their copper foil from specialist suppliers and simply do the final pressing. Nan Ya decided to make all of it. It built out glass-fiber yarn and woven glass fabric, mastering the delicate art of drawing high-purity glass into filaments — including through joint ventures with Western partners such as the U.S. glass and coatings company PPG Industries to acquire the process know-how. It synthesized its own epoxy resins, drawing directly on the chemical streams flowing from the group's refineries. It manufactured copper foil through high-precision electroplating. And then it pressed the finished laminate. By the end of the build-out Nan Ya was, uniquely, present at every single layer of the sandwich — from raw sand-and-chemical inputs to the finished board material.

Why bother? On the surface this looks like the opposite of good strategy. Management orthodoxy says to focus, to own the highest-value link in the chain and outsource the rest. Nan Ya did the reverse, and the reason traces straight back to the rice shop. To a cost-obsessed operator, every link in a supply chain is a place where somebody else earns a margin at your expense and where quality can slip out of your control. If you can run each of those links yourself, at Formosa-grade cost discipline, you strip out the middlemen's markups and you guarantee that your glass, your resin, and your foil are made to your own specification. In a good market, that means you capture margin at four stages instead of one. In a bad market — and this is the subtle, decisive advantage — it means you can keep pressing and selling laminate at prices that would bankrupt a rival who has to buy every input at market. Integration, done by a cost fanatic, is not diversification. It is a weapon calibrated for downturns.

Alongside the materials build-out came a spin-off strategy that fanned the group into the highest-value corners of the semiconductor supply chain. In 1995 Nan Ya helped create 南亞科技 Nanya Technology to enter the DRAM memory-chip business — the most brutally cyclical, capital-devouring corner of all of semiconductors, a decision whose costs would echo for decades. Nanya Technology's history is itself a cautionary tale in dependence: lacking its own leading-edge memory process, it leaned on a succession of foreign technology partners, forming a joint venture with Germany's Infineon to build the memory maker Inotera in 2003, and later striking a technology-and-joint-venture arrangement with America's Micron in 2008.4 DRAM is a business where you either own the bleeding edge of process technology or you rent it, and renting it — as Nanya effectively did — leaves you perpetually one step behind on cost per bit, which in a commodity is close to fatal. In 1997 the group carved out 南亞電路板股份有限公司 Nanya PCB to specialize in high-layer-count circuit boards and, crucially, IC substrates — the intricate mini-boards that connect a bare silicon chip to the outside world.4 And in a separate joint venture with Japan's SUMCO, the group entered silicon-wafer manufacturing through 台勝科 Formosa Sumco Technology, one of its more quietly successful bets.

The pattern across these spin-offs is instructive. The group used the same playbook it always used — build the whole chain, control the inputs, apply relentless cost discipline — but the results diverged wildly depending on the underlying economics of the end market. Where the product was a genuinely differentiated material that benefited from integration (laminate, substrates, specialty glass), the strategy compounded into real advantage. Where the product was a pure commodity governed by whoever owned the newest process node (DRAM), integration could not save it, and the capital poured in mostly evaporated across successive memory downturns. Same discipline, same culture, opposite outcomes — a reminder that even a superb operating system cannot rescue a business whose fundamental economics are stacked against it.

There is a temptation to narrate all of this as visionary genius, and some of it was. But the honest read is more mixed. The materials integration — glass, resin, foil, laminate — turned out to be a genuinely durable structural advantage, one that pure-play laminators could never fully replicate because they will always be buying inputs Nan Ya makes in-house. The DRAM bet, by contrast, was a decades-long lesson in how capital-intensive commodity semiconductors can destroy shareholder value even inside a disciplined group. Same integration instinct, wildly different outcomes. That divergence — a brilliant materials stack shackled to a value-destroying memory stake — is a tension we will return to, because it sits at the center of the modern investment debate.

What Wang got unambiguously right was the timing and the direction. He deployed patient capital into fiberglass, epoxy, and copper foil in the 1980s, when none of it looked strategic and all of it looked like a plastics company wandering off its map. Decades later, when AI turned advanced laminates and substrates into some of the most sought-after materials on Earth, that "side bet" would become the thing keeping the whole corporation afloat. But before the lifeboat could matter, the ship had to start taking on water — and in the 2010s, it did.

IV. The Petrochemical Trap: The China Overcapacity Crisis

For roughly two decades, the reliable, boring, cash-gushing core of Nan Ya was chemistry sold into China. The picture was almost idyllic from a Taiwanese boardroom. The group's giant 麥寮六輕 Mailiao Sixth Naphtha Cracker complex in Yunlin County — an integrated petrochemical city on reclaimed land, with its own cracker turning out millions of tons of ethylene a year — supplied cheap, steady feedstock.5 Nan Ya converted that feedstock into commodity chemicals, above all ethylene glycol (EG), the building block of polyester, and bisphenol-A (BPA), the building block of polycarbonates and epoxy resins. And across the strait, China's endlessly hungry factory sector bought all of it. For years, the arithmetic worked: cheap integrated feedstock in Taiwan, insatiable demand in China, healthy spreads in between.

The Mailiao complex itself deserves a word, because it is one of the great feats of stubborn Taiwanese industrial will. Wang Yung-ching spent much of the 1970s and 1980s fighting to build an integrated naphtha cracker — the upstream facility that would free the group from buying feedstock at others' prices — and was thwarted for years by regulatory resistance and local opposition. He famously threatened, at various points, to build the plant abroad. The group finally secured a site on reclaimed land off the coast of impoverished Yunlin County in the early 1990s, and over the following decade erected an entire petrochemical city there, complete with its own harbor and power generation, culminating in a cracker capable of producing on the order of nearly three million tons of ethylene a year.5 For the group, Mailiao was liberation: it meant Formosa controlled its feedstock costs from crude all the way to finished plastic, the ultimate expression of the integration religion. For a while, it was a money machine.

You can see the good years in the numbers. As recently as 2022, Nan Ya posted revenue of around NT$355 billion and net income of roughly NT$32 billion — a genuinely fat year, with earnings per share above NT$4.1 That was the top of the mountain. What happened next was not a normal cyclical dip. It was the floor giving way.

The cause was a deliberate act of Chinese industrial policy. Starting in the mid-2010s and accelerating through the turn of the decade, Beijing designated petrochemical self-sufficiency a national priority. State-owned enterprises and enormous private refiners — names like Hengli and Rongsheng — built integrated petrochemical complexes at a scale the industry had never seen, swallowing crude at one end and extruding polyester-grade chemicals at the other. China set out, quite explicitly, to stop importing the very products Taiwan had spent two decades exporting to it.

To grasp why this is so dangerous for an incumbent, you have to understand the peculiar economics of commodity chemicals. These are enormous fixed-cost plants; once built, they want to run flat-out, because the marginal cost of the next ton is low and idling the plant is ruinous. So when a wave of new capacity arrives, nobody wants to be the one to cut production — everyone keeps running, the market floods, and prices fall until they approach the cash cost of the least efficient producer. If your rival's plant is newer, bigger, more integrated, and partly financed on terms a state bank would extend but a commercial lender would not, then the price that clears the market can sit below your cash cost for years. This is not a cycle that mean-reverts on its own. It reverts only when enough capacity permanently closes, and state-backed capacity is exactly the kind that does not close on schedule.

The consequence for a company like Nan Ya was brutal and, worse, structural. China went from being Taiwan's biggest customer to its most formidable competitor, seemingly overnight in industrial-time. The new mega-plants did not just meet Chinese domestic demand; they overshot it, and the surplus washed out into export markets. The global market for EG and BPA was suddenly flooded with cheap Chinese product, and price spreads — the gap between what the chemicals sold for and what they cost to make — collapsed, in many quarters falling below the cash cost of production.7 You can watch it hit the income statement: from that ~NT$32 billion peak in 2022, Nan Ya's net income cratered to around NT$6.3 billion in 2023 and roughly NT$3.3 billion in 2024, even though revenue barely moved on a headline basis — a textbook margin collapse rather than a demand collapse.1 The volume was still there. The profit in it was gone. To put a finer point on it: the company sold roughly the same amount of stuff in 2024 as in 2022, but earned less than a tenth as much profit doing it. That is the signature of a business whose pricing power has been stripped away by a competitor it cannot out-cost.

Here the company's own culture became part of the problem, and it is worth being direct about it. Formosa and Nan Ya were built on a paternalistic ethos — deep loyalty to a long-tenured workforce, a reluctance to inflict the kind of ruthless, sudden plant closures that a purely financial owner would order without blinking. For several quarters, Nan Ya kept money-losing EG and BPA lines running, absorbing losses in the hope of a cyclical recovery that, this time, was not a cycle at all. A skeptical investor would call this exactly what it was: a delayed, over-hoped response to a structural shift, the kind of paternalistic inertia that protects employees and community in the short run while eroding returns. Management would frame it as prudence and social responsibility. Both readings contain truth, and the tension between them is a recurring theme in how this company allocates capital.

Then came the geopolitical body blow. The 兩岸經濟合作架構協議 Economic Cooperation Framework Agreement (ECFA), the 2010 cross-strait pact that had granted preferential, low-tariff access for a list of Taiwanese goods into China, began to unwind. Beijing moved to strip tariff preferences from tranches of Taiwanese petrochemical products, a step widely read as economic pressure carrying an unmistakable political message.6 For Nan Ya's commodity chemicals, the effect was to layer punitive tariffs on top of already-collapsed spreads. Exporting EG and BPA from Taiwan into China went from marginally profitable to plainly uneconomic. The door that had been the whole business model was being quietly bolted shut.

The ECFA unwinding deserves to be understood as more than a tariff footnote, because it captures a broader vulnerability. When it was signed in 2010, ECFA was celebrated on both sides of the strait as a landmark normalization of cross-strait commerce, and its "early harvest" list of tariff-free goods handed Taiwanese petrochemical exporters a real, durable edge into the mainland market. That edge was always, in retrospect, a political gift — and political gifts can be revoked. As cross-strait relations chilled through the 2020s, Beijing began treating those preferences as leverage, suspending tariff concessions on tranches of Taiwanese products, with petrochemicals prominently in the crosshairs.6 The lesson for an investor is uncomfortable but important: a meaningful slice of Nan Ya's historical chemical profitability rested on a preference that existed at the pleasure of a government now hostile to it. A moat granted by policy is a moat that policy can drain. Nan Ya learned that the hard way, and it is a large part of why management now speaks of the chemical business in the language of managed decline rather than recovery.

Faced with that, the overdue restructuring finally began. Nan Ya curtailed production and shuttered multiple EG and BPA lines in Taiwan, taking the pain it had deferred and beginning the slow, expensive work of shrinking a legacy chemical division that no longer had a viable core market.7 The commodity-chemical story, in other words, is not one of a temporary downturn to be waited out. It is one of permanent impairment — a business model overtaken by a rival state's industrial strategy. That reframing matters enormously, because it changes what the electronics segment has to be. It is not a nice supplement to a healthy core. It is the replacement for a core that is not coming back. Which raises the stakes on the lifeboat considerably — so let's climb aboard and see how seaworthy it actually is.

V. The AI Revolution & The Modern Electronic Shield

Every so often a slow-burning corporate bet gets validated by a demand shock so large it rewrites the company's identity. For Nan Ya, that shock was generative AI. The same low-loss laminates and specialty glass fibers that Wang Yung-ching's engineers began developing in the 1980s turned out, four decades later, to be precisely the materials the AI-server buildout could not get enough of. The 1980s side bet became the 2020s main event.

The rebalancing is visible in the mix. Management has described the Electronic Materials segment climbing from a little over 40% of revenue in 2024 toward a majority of the business, and it has set a public goal of pushing that share past 60% by the end of 2026 — with new pillars in medical materials, semiconductor materials, and power solutions layered on top.3 For a company whose identity was built on plastics and polyester, crossing the line where electronics becomes more than half of everything is not a rounding change. It is a redefinition of what Nan Ya is.

To see why AI is so demanding of these humble-sounding materials, you have to understand what an AI server does to a circuit board. A rack of accelerators — the NVIDIA H100 and B200 generations, with the next-generation Rubin architecture on the horizon — is essentially a machine for moving colossal amounts of data between chips at staggering speeds while running blisteringly hot. Two physical problems dominate. First, signal integrity: when data pulses race through copper traces at very high frequencies, the surrounding insulating material saps and distorts the signal, and the faster you go, the more it hurts. Second, heat: these parts run hot enough that the board material itself must stay dimensionally stable under thermal stress. Ordinary board material simply cannot cope. You need laminates engineered for ultra-low signal loss and high thermal tolerance — and that is a materials-science problem, exactly the kind Nan Ya spends its life on.

There is a second, less obvious reason materials matter so much in AI: these systems are not single chips but sprawling assemblies. A modern AI accelerator package places a large logic die next to towering stacks of high-bandwidth memory — HBM — all mounted together on an advanced substrate, and then that package sits on a large baseboard connecting it to other accelerators, networking, and power. Every one of those interfaces is a place where signal can degrade and heat can build. The materials are, in a real sense, the connective tissue of the whole machine. When people talk about "the AI supply chain," they usually mean the chips; but the chips are useless without the mundane-sounding laminates and substrates that let them talk to each other at speed. That is the layer Nan Ya occupies, and it is a layer that scales directly with the number of accelerators the world builds.

The industry grades these high-speed laminates on a loss ladder that engineers refer to with shorthand like M6, M7, M8, and beyond, each rung representing progressively lower signal loss and tighter performance for faster designs. Think of it as a ladder of ever-quieter materials: the higher the rung, the less the board "muffles" the signal, and the more advanced the AI hardware it can support. Nan Ya has been climbing that ladder, transitioning production lines to qualify at the higher-loss grades demanded by AI baseboards while sampling still-more-advanced generations with major server ODMs. That last detail matters more than the grade names: in this business, being technically capable is worthless until a specific customer qualifies your material into a specific design. Qualification is the whole game — a months-long, expensive process of testing a material inside a real product for signal integrity, reliability, and manufacturability. A vendor can have a technically excellent laminate on the shelf and earn nothing from it until a server maker and its manufacturing partner have signed off. This is why the language management uses on its earnings calls — "sampling," "qualifying," "ramping" — is worth listening to closely: it is the leading indicator of whether the technology translates into revenue, and it is where a fast-follower like Nan Ya can quietly lose the highest-value slots to a faster rival without any single dramatic announcement.

Underneath the laminate sits an even more specialized ingredient where Nan Ya may hold its most defensible position: the glass itself. Standard glass fabric introduces too much dielectric loss for the fastest signals, so high-speed servers demand ultra-fine, low-dielectric glass — often called "T-glass" or low-DK glass. It is genuinely hard to make; drawing glass this fine and this pure, consistently, at scale, is a craft few companies have mastered. Nan Ya's low-dielectric glass fabric has passed third-party certification, and the company has signaled that its T-glass supply is tight — meaning demand is running ahead of what it can produce — with plans to expand capacity substantially over the coming years.2 A tight-supply position in a scarce, hard-to-make input is, potentially, one of the best places to sit in the whole AI materials chain. The word to keep is "potentially" — scarcity today is a real advantage, but it is also exactly the signal that pulls competitors and customers to build or qualify alternatives.

Then there is the hidden jewel. Nan Ya's controlling stake of just under 67% in Nanya PCB gives the parent direct exposure to one of the hardest, highest-value products in electronics: ABF substrates.2 An ABF substrate — named for the Ajinomoto Build-up Film insulating material at its core — is the exquisitely fine platform onto which a giant GPU or CPU die is mounted, fanning out thousands of microscopic connections and increasingly hosting stacks of high-bandwidth memory alongside the logic die in advanced 2.5D and 3D packages. To appreciate why an ABF substrate is so hard, picture the problem it solves. A modern GPU die may need to connect to the outside world through many thousands of tiny contacts, far more densely packed than a circuit board could ever route directly. The substrate is the translator between the near-invisible scale of the silicon and the coarser scale of the board — a multi-layer platform, built up film-by-film, that fans those thousands of connections outward without letting any of them cross or fail. As AI packages grow larger and stack more memory beside the logic die, the substrates must grow larger, thicker in layer count, and flatter to nanometer tolerances, all while not warping under heat. Yield — the fraction of substrates that come out usable — is punishing, and a company that can hold yield at high layer counts has something genuinely scarce. Only a handful of companies worldwide can make high-layer-count ABF substrates at the required quality, which is why they periodically become a genuine bottleneck for the entire AI supply chain. On recent commentary, Nanya PCB has been a clear beneficiary, with demand for its BT and ABF substrates strong and pricing rising — and, tellingly, tight T-glass supply feeding through into firmer substrate prices, a neat illustration of how Nan Ya's own scarcity in one layer ripples into value in the next.2

The near-term operating data give some texture to how quickly this segment is turning. Commentary around late 2025 pointed to electronic-materials operating margins improving sharply quarter-on-quarter — from low single digits toward the mid single digits as AI demand tightened — while polyester clawed back to breakeven and the chemical division's losses narrowed.2 Those are the fingerprints of a genuine inflection: the good segment accelerating while the bad segments stop getting worse. But note the modesty of the absolute numbers. A mid-single-digit operating margin in electronic materials is a respectable commodity-plus margin, not the fat, differentiated margin of a technology leader with pricing power. That gap — between "improving nicely" and "structurally high-margin" — is precisely the gap between the cost-integration story and the true-moat story, and it is where the analytical action is.

But an honest look at the competitive landscape punctures any temptation to crown Nan Ya the king of AI materials, because it is not. In high-speed CCL, the acknowledged leader is 台光電子材料 Elite Material (台光電, EMC), which has held the lion's share of NVIDIA's AI baseboard business on the strength of superior R&D agility and first-mover qualification at the most advanced specs. Fierce competitors like 聯茂電子 Taiwan Union Technology (聯茂, TUC) and 台燿科技 ITEQ (台燿) fight for the same high-speed server slots. Against that field, Nan Ya is not the fastest innovator. What it brings instead is a different weapon: cost structure and supply security. Because it synthesizes its own epoxy resins and weaves its own glass, it can, in principle, underprice pure-play laminators through a downturn and guarantee supply when inputs get scarce. There is also a subtler strategic angle here: several of Nan Ya's laminate competitors have to buy their specialty glass from — among others — Nan Ya. Being a key input supplier to your own rivals is an unusual and underappreciated position; it means that even when Nan Ya loses a laminate socket to a competitor, it may still capture value one layer down as the glass supplier. Integration turns some competitive losses into partial wins, which is exactly the kind of structural hedge a downturn-hardened operator prizes.

So what should an investor actually take from the AI chapter? Two things, held in tension. The bullish read is real: Nan Ya has genuine, qualified positions in low-loss laminate, a scarce and defensible position in specialty glass, and a controlling interest in one of the few credible ABF-substrate makers — a legitimate, integrated seat at the AI table. The sober read is equally real: it is a fast-follower, not the technology leader, in the highest-margin laminate slots; its edge is cost and integration rather than being first to the newest spec; and much of the current strength rides on a demand wave and tight-supply conditions that are, by nature, cyclical. The segment is unquestionably the growth engine and the lifeboat. Whether it is a durable moat or a well-timed cyclical surge is the exact question the bull and bear cases turn on — and both, revealingly, run straight through the same corporate structure. Which brings us to how this company is actually run.

VI. Capital Allocation, Management, & Governance Playbook

To understand how Nan Ya allocates capital, you first have to understand that it does not really behave like a standalone company. It behaves like a load-bearing pillar inside a temple — the Formosa group — and some of its most important decisions are made in service of the structure, not the individual stock. That single fact explains most of what a Western investor would otherwise find baffling about it.

Start with management. When Wang Yung-ching died in 2008 and Wang Yung-tsai in 2014, the group faced the classic founder-succession question, and it answered in a distinctly Formosa way: not by anointing a single heir, but by shifting toward a professionalized, multi-member executive council drawn from career insiders, with family influence exercised through foundations and board seats rather than day-to-day command. The current chairman of Nan Ya, 吳嘉昭 Wu Chia-chau, is a lifelong Formosa man, and in 2025 his stature was underscored when he took on the presidency of the group's top executive board — effectively becoming one of the most powerful figures across the entire conglomerate.8 Alongside him, president 鄒明仁 Tzou Ming-jen runs the operating business as another deeply steeped company veteran.8 This is not a management team hired to disrupt the culture. It is a management team selected to embody it: conservative, cost-obsessed, incremental, and loyal.

There is a governance question worth sitting with here, because it shapes everything downstream. A multi-member executive council staffed by loyal lifers is superb at operational continuity and cost discipline — nobody is going to blow up the Formosa cost system on a whim. But it is, by construction, not a structure built for bold, contrarian, fast strategic reinvention. Consensus-driven councils of veterans tend to do more of what the organization already knows how to do. That is a feature when the task is running enormous plants at world-beating efficiency. It is a potential bug when the task is out-innovating a nimble, founder-led competitor in a fast-moving technology like advanced laminates. An investor weighing Nan Ya's chances in the AI materials race has to weigh not just its assets but its metabolism — and this is a deliberately slow metabolism.

That culture shows up most clearly in how Nan Ya deploys capital. It almost never buys growth. You will not find a history of expensive, control-premium acquisitions of third parties — the kind of deal-making that fills the pages of American conglomerate stories. Instead, Nan Ya builds. It deploys capital through large internal greenfield projects — expanding electronic-materials capacity at its plants in Taiwan and across mainland sites like Kunshan and Huizhou — where it can design the unit economics from scratch and impose the group's cost-control systems on every layer.3 The philosophy is coherent and, on its own terms, disciplined: don't pay someone else's markup for an asset you could build and run more cheaply yourself. The obvious cost is speed and reach — organic build-out is slow, and it cannot buy you a capability, like leading-edge R&D agility, that you don't already have. When your competitive gap is innovation speed, a build-don't-buy doctrine does not obviously close it. It is also worth flagging the geographic complexion of this capital: a meaningful chunk of the electronics expansion sits on the mainland, at Kunshan and Huizhou, which is efficient for serving Chinese customers and cost-competitive on labor — but which also plants a material share of the company's growth engine squarely inside the jurisdiction that is simultaneously its fiercest chemical competitor and the counterparty in the region's central geopolitical standoff. That is optionality and exposure in the same breath.

Then there is the part of the capital story that a skeptical investor cannot ignore: the cross-shareholdings, and specifically DRAM. Nan Ya Plastics holds a stake of roughly 29% in 南亞科 Nanya Technology, the memory-chip maker the group spun up in the 1990s.9 DRAM is one of the most capital-hungry, viciously cyclical businesses in the world — a place where fortunes are made and unmade on the timing of node transitions, and where staying in the game requires writing enormous checks precisely when the cycle is punishing you. Over the years, Nan Ya Plastics has been drawn into supporting Nanya Technology through the cycle, and for a long stretch that stake behaved less like an asset and more like a recurring call on the parent's capital. For shareholders who own Nan Ya Plastics for its materials business, the DRAM affiliate has been a structural drag on return on equity and a persistent complication in any clean valuation of the company.

That said, the DRAM stake is not permanently one-directional, and intellectual honesty requires acknowledging the other side. Memory is cyclical in both directions, and when the cycle turns up — as it periodically does when supply tightens, for instance amid shortages of older memory generations still needed for a long tail of devices — the very affiliate that has drained capital can swing to contributing meaningful equity income.2 The point is not that DRAM is always bad; it is that DRAM is volatile and outside Nan Ya's control, injecting a large, unpredictable swing factor into consolidated results that has little to do with the materials business a long-term investor is actually trying to own. For valuation purposes, the cleaner mental model is to treat the parent's operating materials-and-chemicals business separately from the marked-to-cycle value of its listed affiliate stakes, rather than blending them into a single earnings number that lurches with the memory cycle.

This is where the activist-style stress test writes itself, and it is worth articulating in full because it is the sharpest critique of the company. A hard-nosed investor would look at Nan Ya and see value trapped by structure. Why, they would ask, does a company with a world-class integrated materials business and a controlling stake in a scarce ABF-substrate maker trade at a conglomerate discount? Because those jewels are commingled with a depressed commodity-chemical division and a cyclical DRAM holding, all wrapped in a web of cross-shareholdings that no outside investor can unwind. Unlock it, the argument goes: spin off Nanya PCB to let the market price the AI jewel on its own; sell down the DRAM stake and return the capital. On paper, the sum of the parts looks worth more than the whole.

It is worth assessing management credibility on its own terms here, through behavior rather than rhetoric, because the pivot story lives or dies on execution. On the positive side of the ledger, the narrative has been strikingly consistent: for several years running, management has told the same story across calls and shareholder meetings — chemicals are structurally challenged, electronics is the future, the goal is to lift the electronic-materials share past 60% — and it has backed that story with concrete, verifiable actions: shuttering chemical lines, certifying low-dielectric glass, expanding substrate and glass capacity.3 That consistency, and the willingness to state plainly that the chemical business faces a prolonged glut rather than a passing dip, is a mark of candor that not every cyclical-industry management shows. On the cautious side, the 60% target is a mix-shift goal that can be "achieved" partly by the denominator shrinking — if chemicals collapse far enough, electronics becomes a majority of revenue without electronics itself doing anything heroic. A skeptic should therefore watch the absolute growth and margin of the electronics business, not just its rising share, and should note that management's guidance has historically been conservative in the group tradition — a tendency that cuts both ways, protecting against overpromising but also occasionally obscuring how much of the improvement is genuine progress versus arithmetic.

And here is the reality check that makes this company genuinely different from a Western break-up target: it is close to structurally impossible to force. The Formosa entities own large slices of one another; family foundations sit atop the pyramid; board seats interlock across the group. There is no realistic path for an outside activist to accumulate enough leverage, or enough friendly votes, to compel a restructuring against the group's wishes. That is a double-edged fact for a minority shareholder. On one hand, it means the value-unlock catalyst that a Western activist would push for is probably not coming — the discount may simply persist. On the other, it means the parent's balance sheet fortitude and long time horizon are equally durable; this is not a company that will be blown up, levered up, or financially engineered by outsiders. You are buying into a structure that trades some capital efficiency for near-unbreakable stability. Whether that is a bug or a feature depends entirely on what you want from the investment. Which is the perfect place to lay the bull and bear cases side by side.

VII. The Investment Case: Hamilton Helmer's Powers & Risk Radar

Let's war-game this properly, using a couple of the frameworks sophisticated investors actually reach for, and then stress-testing them rather than reciting them.

Start with Hamilton Helmer's 7 Powers, applied to the electronic-materials business — because that, not the legacy chemicals, is where any durable advantage has to live. The strongest candidate is Scale Economies fused with what we might call vertical scope. Nan Ya is arguably the only player that spans the full CCL stack — from raw fiberglass and epoxy synthesis through copper foil to finished laminate — under one roof. That integration is a real cost advantage, and critically, it is counter-cyclical: when the market turns down and pure-play laminators get squeezed between input costs and falling prices, Nan Ya can lean on internally-produced inputs to keep underpricing them. That is a genuine Power, and it is the most defensible thing about the company.

A second candidate is Switching Costs, and this one is real but often overstated, so be precise about where it lives. Once a specific high-speed laminate or substrate is qualified into a server platform by a brand like Dell or HPE and its manufacturing ODM, swapping the material vendor means months of expensive re-testing and signal-integrity re-verification. That friction genuinely protects an incumbent — but note where it cuts. It protects whoever wins the qualification. If Elite Material, not Nan Ya, is designed into the flagship NVIDIA baseboard, then switching costs are working against Nan Ya, locking it out of that slot. Switching costs are a moat only for the vendor already inside the wall. For a fast-follower, they are as often an obstacle as an asset.

The third framing the company's defenders invoke is Counter-Positioning — the idea that commodity-chemical rivals simply cannot replicate Nan Ya's decades-deep integration into downstream electronics. There is something to this: you cannot conjure thirty years of glass-drawing, resin chemistry, and PCB-fab relationships overnight. But be careful not to overclaim it. Counter-positioning in Helmer's strict sense means an incumbent can't copy you without damaging its existing business. Nan Ya's real barrier is more prosaic and still powerful: time, accumulated process know-how, and capital. Rivals can't easily copy it — but the players who already can compete, the Elite Materials and ITEQs of the world, are formidable and, in the highest-value slots, ahead on the thing that matters most.

Run it through Porter's Five Forces and the picture sharpens further. Supplier power: low and, for Nan Ya, largely neutralized — it is its own supplier for the key inputs, which is the whole point. Buyer power: high and rising — the customers are enormous, sophisticated ODMs and cloud giants who dual-source relentlessly and squeeze on price. Threat of substitutes: modest in the near term for the specific physics of low-loss laminate. Rivalry: intense, with Elite Material, TUC, ITEQ and others all sprinting up the same materials ladder. New entrants: limited at the high end by exactly the capital-and-know-how barrier described above. The net read is a business with real structural defenses on the supply and entry side, but genuine pressure on the demand side — which is why cost leadership, not pricing power, is Nan Ya's most reliable edge.

Now the bull case, stated at its strongest. First, the demand driver is structural, not a fad: the global buildout of AI data centers and high-performance computing represents a multi-year, arguably multi-decade, wave of demand for exactly the low-loss laminates, specialty glass, and ABF substrates Nan Ya makes. Second, product premiumization improves the whole company: as loss-making commodity chemical units are phased out and high-value electronics grows, the consolidated margin and quality of earnings should structurally improve, transforming the business mix toward specialty materials. Third, financial fortitude: backed by the immense asset base of the Formosa group, Nan Ya has the balance-sheet strength to survive prolonged downturns and to fund long, patient capacity build-outs that a weaker competitor could not. This is a company built to endure, and endurance in a cyclical industry is itself a Power of sorts.

The bear case is equally coherent, and it deserves equal airtime. First, the chemical glut may simply persist or worsen: if Chinese overcapacity in EG, BPA, and polyester keeps spreads below cash cost for years, those legacy segments can bleed cash faster than the electronics segment generates it, and the "lifeboat" spends its buoyancy just keeping the ship level rather than moving it forward. Second, R&D obsolescence: Nan Ya is a fast-follower, and the highest-margin AI slots go to whoever qualifies the newest spec first. If it falls behind on the transition to the next laminate generations or to ultra-thin substrates, it risks being permanently relegated to the lower-value rungs while rivals harvest the premium. Third, geopolitics cuts both ways and is unusually acute here: the same ECFA rollback that gutted the chemical export model could deepen, and a serious escalation in the Taiwan Strait would threaten a manufacturing footprint split between Taiwan and mainland sites like Kunshan and Huizhou — a company physically straddling the exact fault line of the region's biggest geopolitical risk.

It is worth confronting the consensus narrative directly — the myth-versus-reality of the "AI materials play." The myth, in its most breathless form, holds that Nan Ya is a hidden AI beneficiary whose electronics business will re-rate it into a high-margin technology company. The reality is more textured. Yes, Nan Ya has real, qualified AI exposure through laminates, glass, and its Nanya PCB substrate stake — that part is not hype. But it is a fast-follower earning commodity-plus margins in most of its electronic-materials lines, not a design-in leader commanding premium prices; its single most exciting exposure (ABF substrates) sits inside a separately listed subsidiary rather than in the parent's own operations; and its consolidated results are still dominated by the drag of legacy chemicals and the noise of a DRAM affiliate. The stock is "an AI play" only in the diluted sense that a well-run tollbooth on a busy road is a transportation company. There is genuine value in the tollbooth. Just don't confuse it with the traffic.

The honest synthesis is that Nan Ya is neither the doomed old-economy dinosaur the bears caricature nor the triumphant AI-materials champion the company's own narrative implies. It is a genuinely integrated, cost-advantaged materials player with a real and defensible position in parts of the AI supply chain, currently carrying a structurally impaired chemical business and a value-trapping DRAM stake, run by a conservative culture inside an unbreakable group structure. The stock is a bet on whether the electronics transition compounds faster than the chemical core decays — and on whether integration-and-cost can hold its ground against faster innovators.

If you strip all of that down to what you would actually watch quarter after quarter, three KPIs carry most of the signal. The first is the electronic-materials share of revenue and its segment operating margin — the single cleanest gauge of whether the pivot is real and profitable, not just growing. The second is Nanya PCB's ABF/BT substrate demand and pricing, the highest-value exposure the company has to the AI cycle. The third is the commodity-chemical spread environment — EG and BPA margins — because that is what determines whether the legacy division is a manageable drag or an active drain. Track those three and you are tracking the entire thesis. Everything else is detail.

VIII. Epilogue & Enduring Strategic Lessons

Step back from the quarterly noise and Nan Ya offers a set of lessons that outlast any single cycle — lessons that are, in the end, about the deep architecture of how industrial companies survive disruption.

The first is the Trojan Horse lesson. The most durable defense against structural disruption is to have built the next business inside the old one before the old one starts to rot. Nan Ya did not decide to become an AI-materials supplier in 2023 when it needed one; it planted the seeds in the 1980s, when doing so looked eccentric and unnecessary. The lifeboat has to be built while the ship is still cruising, not after it hits the rocks — because by the time you need it, you no longer have the years, the capital, or the calm required to build it. That timing, more than any single product, is the strategic heart of this story.

The second is the double-edged sword of vertical integration. When demand is booming and you own every layer of the value chain, integration is a compounding Power — you capture margin at each stage and can undercut anyone who has to buy what you make yourself. But the same integration becomes an anchor when an upstream commodity layer — a petrochemical cracker, a bulk-chemical line — is swamped by global oversupply, because now you own the losses too. Nan Ya embodies both faces of the same strategy at the same time: the integration that makes its laminates cost-competitive is the very integration that chains it to money-losing chemical plants. Integration is not free insurance. It is leverage, and leverage cuts in both directions.

The third is the long game, and it is really a lesson about time horizons and what "moat" actually means. Formosa's patient, multi-decade deployment of capital into fiberglass, epoxy, and copper foil — investments that produced no glory for years — is what laid the foundation for whatever advantage Nan Ya holds in the AI era today. True moats are not dug in a quarter, or even a decade. They are dug over the working life of a founder and inherited by managers who mostly did not build them. That is inspiring and sobering in equal measure: inspiring because it shows what patient industrial capital can create, sobering because the same patience is inseparable from the conservatism and structural rigidity that today traps value inside a conglomerate discount.

Which leaves the investor exactly where a good story should: without a verdict handed to them, but with the right questions sharpened. Nan Ya is a company whose past brilliance and present limitations spring from the same source — an integrated, cost-obsessed, patient, immovable industrial culture. Whether that culture can pivot fast enough, into high enough value, to outrun the collapse of the world it was built for is not a question that management's confidence can settle. It is a question that only the next several years of that electronic-materials share, those substrate prices, and those chemical spreads will answer. The King of PVC has built itself a semiconductor lifeboat. The open question is not whether the lifeboat exists — it plainly does — but whether it is big enough, and fast enough, for everyone still aboard.

References

-

Nan Ya Plastics Corporation — annual income statement history (FY2022–FY2025 revenue and net income) ↩↩↩

-

Taiwan's Nan Ya Plastics sees benefits from moving into AI supply chains — Taiwan News, 2025-11-24 ↩↩↩↩↩↩

-

Nan Ya Plastics targets three new business pillars to lift electronic materials to 60% by 2026 — Digitimes, 2026-05-29 ↩↩↩↩

-

Formosa Plastics Group — Corporate History & Structure — FPG ↩↩↩

-

Nan Ya Plastics — Company Overview and Investment (Mailiao Sixth Naphtha Cracker integration) — NPC ↩↩

-

The End of ECFA Tariff Preferences: Impact on Taiwan's Industrial Giants — Taipei Times, 2025-12-05 ↩↩

-

China Petrochemical Overcapacity Pressures East Asian Exporters — Reuters, 2025-11-20 ↩↩

-

FPG's Executive Board Appoints Chia Chau Wu as President — Formosa Plastics Group, 2025 ↩↩

-

Nan Ya Plastics Year 2025 Operations & Performance report (Nanya Technology ~29% holding; segment performance) — NPC, 2026-03 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube