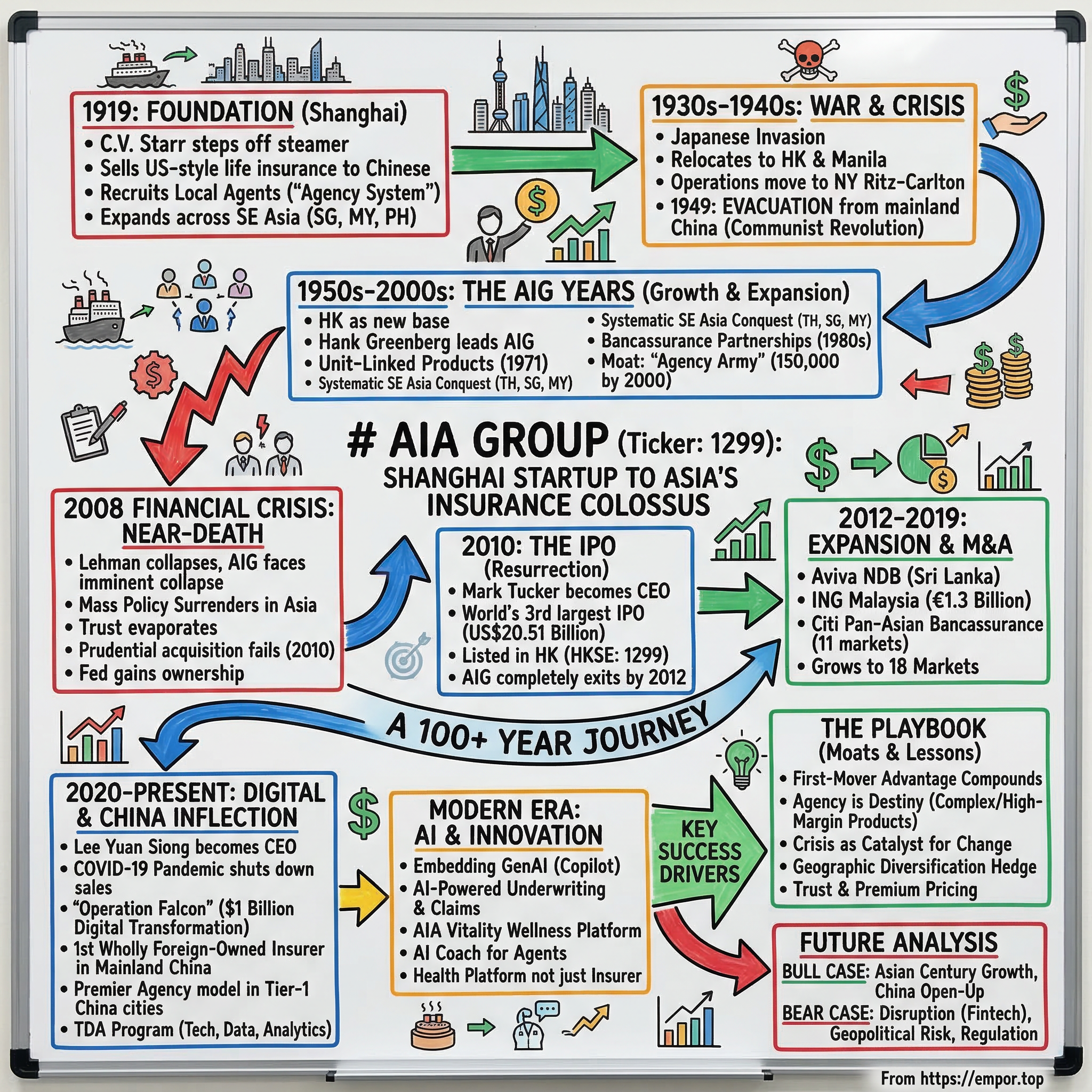

AIA Group: From Shanghai Startup to Asia's Insurance Colossus

I. Introduction & Episode Roadmap

Picture this: Shanghai, 1919. The Great War has just ended, the world order is reshaping, and a 27-year-old American named Cornelius Vander Starr steps off a steamer with an audacious plan—sell American-style insurance to Chinese merchants who have never heard of life insurance. Fast forward a century: that startup is now AIA Group, commanding a market capitalization of HK$788 billion, insuring 40 million lives across 18 markets, and standing as the undisputed champion of pan-Asian life insurance.

The paradox is striking. How does an American company founded in Republican-era China, expelled by Communist revolution, nearly destroyed in the 2008 financial crisis, emerge as the largest publicly traded life insurer in Asia-Pacific? This isn't just a business story—it's a tale of war, revolution, existential crisis, and ultimately, one of the most spectacular resurrections in corporate history.

What makes AIA fascinating for investors isn't just its size or longevity. It's the company's uncanny ability to transform existential threats into competitive advantages. When Japanese invasion forced evacuation from Shanghai, AIA built new markets. When AIG's collapse threatened annihilation, AIA engineered the third-largest IPO in history. When COVID-19 shut down face-to-face insurance sales—the company's bread and butter for a century—AIA launched a billion-dollar digital transformation that now positions it ahead of nimbler fintech competitors.

Today's journey takes us from C.V. Starr's entrepreneurial genius in 1919 Shanghai through Japanese occupation, Communist revolution, the golden years under Hank Greenberg's AIG empire, near-death in 2008, resurrection through a record-breaking IPO, aggressive M&A expansion across Asia, and finally, the digital revolution reshaping insurance distribution. We'll examine how AIA became the first wholly foreign-owned life insurer in mainland China—a market that could define the next century of growth.

The numbers tell one story: total assets of US$221 billion, operations spanning from Mumbai to Melbourne, Beijing to Bangkok. But the real story lies in the playbook—how AIA built an agency army of 700,000 that became an unassailable moat, why bancassurance partnerships unlocked exponential growth, and how a century-old company is now deploying AI faster than Silicon Valley startups.

For fundamental investors, AIA presents a fascinating study in competitive advantages, capital allocation, and market positioning. Is this a mature cash cow milking Asia's demographic dividend, or a growth story just beginning as China opens its doors? Can a company born in the age of telegrams dominate in the era of algorithms?

Let's dive into a century of ambition, survival, and reinvention—the acquired story of how an American startup in Shanghai became Asia's insurance colossus.

II. The C.V. Starr Era & Origins (1919–1949)

The Bund waterfront stretched before him—that legendary mile of colonial banks and trading houses where East met West in a frenzy of commerce. But Cornelius Vander Starr wasn't looking at the grand facades of Jardine Matheson or HSBC. The 27-year-old Californian, fresh from a stint as an ice cream parlor owner and U.S. Army clerk, saw something else entirely: millions of Chinese merchants, traders, and emerging middle-class families with zero insurance protection.

On December 19, 1919, Starr founded American Asiatic Underwriters , printed policies in Chinese characters, and crucially, paid claims promptly when competitors often delayed or disputed.

The early years demanded entrepreneurial hustle that would make modern startup founders blanch. Starr personally traveled to remote provinces, sometimes by riverboat or horseback, establishing agency offices in cities where no American had sold insurance. By 1921, he'd opened AAU's Hong Kong office—a prescient move that would prove vital decades later. The company expanded into fire and marine insurance, covering everything from Yangtze River cargo boats to Shanghai textile factories.

But Starr's masterstroke was building what he called the "agency system"—recruiting and training local agents who earned commissions selling policies in their communities. Unlike British insurers who relied on expatriate managers and centralized operations, AAU embedded itself in local markets. By 1926, the company had 14 branches across China and Southeast Asia, with operations in Singapore, Malaysia, and the Philippines.

The numbers from this era seem quaint now—total premiums of perhaps US$1 million annually—but Starr was building something more valuable than revenue: distribution infrastructure and local relationships that competitors couldn't replicate. He understood, decades before management consultants coined the term, that distribution was destiny in Asian insurance.

Then came the chaos. The 1927 Shanghai Massacre saw Nationalist forces turn on Communist allies, triggering civil war. The 1931 Japanese invasion of Manchuria began the slow strangulation of foreign business in China. Yet Starr adapted with remarkable agility. As Japanese forces advanced, he relocated key operations to the Philippines and Hong Kong. When Manila fell in 1942, he operated from a suite in New York's Ritz-Carlton, planning for post-war expansion while competitors retreated.

The immediate post-war period from 1945-1949 represented both AAU's greatest opportunity and ultimate crisis in China. With Japan defeated, Starr rushed back to Shanghai, finding his offices intact and his Chinese managers—remarkably—still operating underground insurance networks. The company resumed aggressive expansion, now operating under the name American International Assurance Company (AIA), formally incorporated in Shanghai in 1931 but truly coming into its own in the post-war reconstruction.

But Mao's Communist forces were sweeping south. By early 1949, as the People's Liberation Army crossed the Yangtze, Starr made the painful decision to evacuate all American personnel from mainland China. The last Western insurance executive to leave Shanghai, he transferred AIA's headquarters to Hong Kong—a British colony that seemed a safer bet for capitalism's future in Asia.

The numbers tell the story of loss: AIA abandoned 13 branches, thousands of policies, and three decades of painstakingly built market presence in mainland China. Communist authorities seized all assets and declared private insurance illegal. Competitors like Prudential and Sun Life, who had also fled, wrote off China entirely.

Yet Starr saw opportunity in crisis. With mainland China closed, he doubled down on Hong Kong and Southeast Asia. The company Starr built—now part of his growing American International Group (AIG) empire—would have to wait 70 years to return to mainland China. But the entrepreneurial DNA, the agency distribution model, and the localization philosophy Starr embedded in those Shanghai years would define AIA's trajectory for the next century.

As 1949 ended, AIA was effectively a refugee company—expelled from its birthplace, starting over in Hong Kong with a handful of employees and uncertain prospects. No one could have predicted that this moment of apparent defeat was actually the beginning of AIA's rise to pan-Asian dominance.

III. The AIG Years: Growth & Expansion (1950–2008)

The Crown Colony of Hong Kong in 1950 was a peculiar place for an insurance company to bet its future. Still recovering from Japanese occupation, flooded with refugees from mainland China, the territory held just 2.2 million people crammed into 426 square miles. Yet for AIA, now nestled within C.V. Starr's growing AIG empire, Hong Kong would become the launchpad for conquering Asia.

The transformation began quietly. While competitors focused on expatriate communities and large commercial risks, AIA's new Hong Kong chief, a former Shanghai hand named Gordon Tweedy, made a counterintuitive decision: target the emerging Chinese middle class. These families—many refugees themselves—understood uncertainty viscerally. They'd lost everything once and desperately wanted financial security in their adopted home.

By 1955, AIA had recruited 500 Hong Kong-based agents, mostly from the refugee community, who sold policies in Cantonese, accepted premium payments in small monthly installments, and understood that buying insurance meant saving face—showing you could provide for your family's future. The model worked spectacularly. Premium income grew from HK$5 million in 1950 to HK$50 million by 1960.

But the real acceleration came when Maurice "Hank" Greenberg took control of AIG in 1968. Greenberg, a former U.S. Army Ranger who'd landed at Normandy, brought military precision to insurance expansion. His vision for AIA was breathtaking in scope: make it the dominant life insurer across all of non-Communist Asia.

Greenberg's first major move was revolutionary for its time—the introduction of unit-linked products in Hong Kong in 1971. These policies combined life insurance with investment funds, allowing policyholders to participate in Hong Kong's booming stock market while maintaining death benefits. Competitors dismissed them as too complex for Asian consumers. Within three years, unit-linked products comprised 40% of AIA's new business.

The 1970s and 1980s saw AIA's systematic conquest of Southeast Asia. The playbook was consistent: enter through joint ventures with local partners who provided regulatory cover and market knowledge, build massive agency forces recruited from each country's educated middle class, and introduce innovative products that competed not with other insurers but with traditional savings methods.

In Thailand (entered 1951), AIA built an agency force of 12,000 by 1985, making it the kingdom's largest life insurer. The key? Recruiting university graduates when competitors hired anyone willing to sell, then training them for months in consultative selling—positioning insurance as financial planning, not death protection.

Singapore (1931) and Malaysia (1948) became twin pillars of profitability. By pioneering bancassurance partnerships in the 1980s—decades before the term became fashionable—AIA could instantly access millions of bank customers. A 1987 deal with Standard Chartered across multiple markets gave AIA distribution reach that would have taken decades to build organically.

The numbers from this era stagger: AIA's total premiums grew from US$100 million in 1970 to US$2 billion by 1990, then to US$8 billion by 2000. Market share across key markets told the dominance story—number one in Hong Kong (35% share), Thailand (24%), Singapore (21%), and Malaysia (18%) by the late 1990s.

But Greenberg's true genius lay in building what he called the "agency army"—by 2000, AIA commanded 150,000 agents across Asia. Unlike Western insurers who viewed agents as a necessary evil, AIA made them the center of its strategy. Top agents earned six-figure incomes, drove Mercedes, and enjoyed social status comparable to doctors or lawyers. The company's Million Dollar Round Table (MDRT) members—elite agents achieving certain sales thresholds—became legends in their communities.

The infrastructure supporting this army was equally impressive. AIA built dedicated training centers in each market—the Hong Kong facility alone could handle 1,000 agents daily. The company developed proprietary needs-analysis software in the 1990s, giving agents tablet computers when most Asian households didn't own PCs. By 2005, AIA's IT spending exceeded US$200 million annually—more than many insurers' total profits.

Product innovation kept pace with distribution growth. AIA introduced critical illness coverage to Asia in 1983, created the region's first investment-linked insurance products, and pioneered medical insurance with cashless hospitalization. Each innovation was localized—critical illness in Hong Kong covered traditional Chinese medicine treatments, Thai policies included Buddhist funeral benefits, and Malaysian products were certified Sharia-compliant.

The financial engineering was equally sophisticated. AIA became one of the first insurers to use derivatives for hedging currency risk across multiple Asian currencies. The company's investment team, managing US$50 billion by 2007, generated consistent returns through Asian financial crises that bankrupted local competitors.

By 2007, AIA seemed invincible. Premium income reached US$12 billion, it operated in 15 markets, commanded 250,000 agents, and served 25 million customers. The company contributed nearly 40% of AIG's total operating income despite being just one division of the global insurance giant. Investment banks valued AIA at US$60-80 billion in internal estimates—making it worth more than most European insurance groups.

Yet beneath this success lay a fatal dependency. AIA's profits were upstream to AIG corporate, funding Greenberg's global ambitions and, increasingly after his 2005 ouster, supporting AIG Financial Products' aggressive bets on mortgage securities. AIA's Asian management had no idea their parent company was building a derivatives portfolio that would soon implode.

The last normal year was 2007. AIA generated record profits of US$2.8 billion, launched in Vietnam, and announced plans for Indonesia expansion. Agents celebrated at lavish conventions in Macau and Las Vegas. The company's 2008 business plan projected 15% annual growth through 2015.

As 2008 dawned, no one at AIA's Hong Kong headquarters imagined that within months, their parent company would need the largest government bailout in U.S. history, or that AIA itself would face an existential crisis that would test every strength built over six decades.

IV. The 2008 Financial Crisis: Near-Death Experience

September 15, 2008, 9:47 AM Hong Kong time. Mark Wilson, AIA's British CEO, was in his corner office overlooking Victoria Harbor when his BlackBerry erupted. Lehman Brothers had just filed for bankruptcy. Within minutes, every phone line at AIA headquarters was ringing. The questions were all variations of the same terrifying theme: "Is AIG next?"

By noon, AIA's Hong Kong offices were surrounded by television crews. Inside, the management team watched in horror as AIG's stock price collapsed 61% in New York trading. The unthinkable was happening—their parent company, one of the world's largest insurers, was facing imminent collapse due to credit default swap exposures that no one at AIA fully understood.

The speed of the crisis was breathtaking. On September 16, the Federal Reserve announced an US$85 billion emergency loan to AIG, giving the U.S. government a 79.9% equity stake. AIA—profitable, growing, with no exposure to subprime mortgages—was now effectively owned by American taxpayers. The bitter irony wasn't lost on Asian employees: a company expelled from China by Communists was now nationalized by capitalist America.

The immediate impact on AIA's business was catastrophic. In Hong Kong, queues formed outside AIA offices as panicked policyholders demanded surrenders. The scenes were reminiscent of bank runs—elderly customers clutching policy documents, some in tears, convinced their life savings were gone. On September 17 alone, AIA processed HK$600 million in surrender requests, more than a typical month. The Singapore scenes were equally dramatic. Anxious policyholders thronged AIA Tower's main lobby during lunch time on September 17, 2008, desperate for reassurance. AIA Singapore's management issued emergency statements asserting they had "sufficient capital and reserves above regulatory minimum requirements," but trust had evaporated. The company's Asian subsidiaries, despite being operationally sound and locally regulated, were guilty by association.

The contagion spread across AIA's footprint. In Thailand, the insurance regulator took the extraordinary step of publicly guaranteeing AIA Thailand's solvency to prevent mass surrenders. Malaysia's central bank issued similar assurances. But the damage to new business was immediate and severe—sales plummeted 40% in the fourth quarter of 2008 as agents found it impossible to sell policies from a company associated with American taxpayer bailouts.

Inside AIA headquarters, management faced an impossible situation. The business itself remained fundamentally sound—AIA had minimal exposure to the toxic mortgage securities that destroyed AIG Financial Products. Its Asian operations generated steady profits from traditional life insurance. Yet none of that mattered when your parent company had become synonymous with financial catastrophe.

The human toll was devastating. Thousands of AIA's most productive agents defected to competitors, taking their client relationships. Employee morale cratered as stock options became worthless and bonuses evaporated. The company's famed agency conventions—symbols of AIA's success culture—were cancelled. Instead of celebrating in Macau ballrooms, agents were explaining to clients why their policies were safe despite AIG's collapse.

In December 2009, AIG formed international life insurance subsidiaries, American International Assurance Company, Limited (AIA) and American Life Insurance Company (ALICO), which were transferred to the Federal Reserve Bank of New York, to reduce its debt by $25 billion. This complex transaction essentially carved AIA out of AIG's control, placing it in a special purpose vehicle owned by the Fed—a bizarre structure that made AIA technically independent but practically orphaned.

The failed Prudential acquisition attempt in early 2010 added another layer of chaos. Prudential's US$35.5 billion acquisition attempt in March 2010 would have given AIA a stable parent and ended the uncertainty. But the deal collapsed spectacularly when Prudential's shareholders revolted, leaving AIA in limbo—too valuable to give away, too toxic to sell at fair value.

By mid-2010, AIA's predicament was clear: it needed complete independence from AIG, and fast. The company had survived the immediate crisis, but remaining tied to AIG's reputation would slowly strangle the business. New business value—the key metric for life insurers—had declined 25% from pre-crisis levels. Market share was eroding. The agency force, though loyal, was aging and struggling to recruit new blood.

The solution would require one of the most ambitious IPOs ever attempted—taking a century-old company with operations across 15 markets, 20 million policies in force, and a tainted brand, and convincing global investors it was worth betting on. The preparation was frantic: new management team, new board, new systems, new story. Everything had to be rebuilt while the business continued operating.

What emerged from this near-death experience was remarkable: a company that understood, perhaps better than any competitor, that survival required more than financial strength. It needed complete transformation. The crisis had exposed every weakness—over-dependence on traditional distribution, vulnerability to reputation risk, lack of digital capabilities. These lessons would drive AIA's next chapter, but first, it had to pull off the escape act of the century.

V. The IPO: Resurrection & Independence (2010)

Mark Tucker stood at the podium of Hong Kong's Four Seasons Hotel on October 18, 2010, facing 500 of Asia's most influential investors. The former Prudential Asia CEO, recruited as AIA's new chief executive just months earlier, had one shot to convince them that a company nearly destroyed by its parent's recklessness was actually the best investment opportunity in Asian financial services. Behind him, a simple slide showed one number: US$20.51 billion—the amount AIA hoped to raise in what would be Hong Kong's largest-ever initial public offering.

The path to this moment had been brutal. After Prudential's failed acquisition attempt collapsed in June, AIG faced a stark reality: it needed to repay US$80 billion to American taxpayers, and AIA was its only asset valuable enough to make a meaningful dent. But who would buy shares in a tainted subsidiary of a bailed-out company? The answer required completely reimagining AIA's story.

Tucker and his hastily assembled management team—many poached from competitors with promises of equity upside—worked 20-hour days through the summer of 2010. They had to build an independent company infrastructure from scratch. IT systems intertwined with AIG for decades needed separation. Treasury functions handled in New York required localization. Risk management, previously overseen by AIG corporate, needed new frameworks and personnel.

The numbers were staggering in complexity. AIA operated in 15 markets with different regulations, currencies, and accounting standards. The company had 23,000 employees, 320,000 agents, and US$115 billion in assets. The IPO prospectus, filed in September, ran to 1,000 pages—a document that needed to explain not just what AIA was, but what it could become freed from AIG's shadow.

The investment thesis Tucker pitched was elegantly simple: Asia's insurance penetration was a fraction of developed markets, the middle class was exploding, and AIA had unmatched distribution capabilities to capture this growth. Life insurance penetration in China was 1.8% of GDP versus 7.5% in the UK. Asia's middle class would grow from 500 million to 3 billion by 2030. And AIA's agency force—battle-tested through crisis—was ready to sell into this demographic tsunami.

But the roadshow, spanning three continents over two weeks, revealed deep skepticism. In London, fund managers questioned whether Asian consumers would trust AIA post-crisis. In New York, investors worried about regulatory risks across multiple jurisdictions. In Singapore, competitors spread rumors that AIA's best agents were defecting. Tucker countered with data: customer retention remained above 90%, the agency force had actually grown during the crisis, and embedded value—the actuarial measure of a life insurer's worth—stood at US$24.7 billion.

The pricing dance was delicate. AIG desperately needed maximum proceeds to repay taxpayers. But price too high, and the IPO would flop, destroying any chance of future selldowns. The initial range of HK$18.38 to HK$19.68 per share valued AIA at up to US$35.5 billion—coincidentally, exactly what Prudential had offered months earlier. Some bankers pushed for HK$21; others warned anything above HK$17 would fail.

October 15, 2010—pricing day. In a conference room at AIA's Central headquarters, Tucker huddled with CFO Garth Jones and the banking syndicate led by Citi, Deutsche Bank, and Morgan Stanley. The order book was 20 times oversubscribed, with demand from both institutional and retail investors. George Soros wanted a major allocation. Singapore's Temasek was in for billions. Even Li Ka-shing, Hong Kong's richest man, was buying. They priced at HK$19.68—the top of the range.

The numbers that emerged were historic: AIA's IPO raised HK$159.08 billion (US$20.51 billion), the world's third largest IPO at the time. AIG's stake dropped from 100% to 67%, with US$17.8 billion in proceeds flowing to the U.S. Treasury. The institutional tranche was oversubscribed 20 times, the Hong Kong retail portion 7.5 times. More than 130,000 retail investors—one in every 50 Hong Kong adults—bought shares.

October 29, 2010—listing day. At 9:30 AM, Tucker rang the opening bell at Hong Kong Exchange as hundreds of AIA employees watched on screens across Asia. The stock opened at HK$21.65, a 10% premium to the IPO price. By day's end, AIA's market capitalization reached US$39 billion. The resurrection was complete—at least symbolically.

But the real work was just beginning. AIA was now public, with quarterly earnings pressures and thousands of new shareholders to satisfy. The company had promised 15% annual growth in embedded value, ambitious expansion in China, and digital transformation of its agency force. Competitors, no longer constrained by sympathy for a wounded rival, attacked aggressively. Ping An and China Life poached agents with signing bonuses. Manulife and Allianz undercut pricing.

The management team Tucker assembled was impressive but untested as a unit. Garth Jones, the CFO, came from Prudential. Ng Keng Hooi, the regional CEO, was promoted internally but had never run operations of this scale. The board, chaired by Edmund Tse (a former Aon executive), included independent directors hastily recruited to provide credibility but with limited Asian insurance experience.

The immediate priorities were clear but daunting. First, restore growth momentum—new business had stagnated during the crisis years. Second, modernize distribution—the agency model was profitable but increasingly outdated. Third, expand in China—the market that would define winners and losers in Asian insurance. Fourth, complete separation from AIG—systems, brand, and culture all needed transformation.

The financial engineering continued post-IPO. In March 2011, AIG sold another US$8.7 billion worth of shares, reducing its stake to 52%. By September 2011, after another US$6 billion selldown, AIG's ownership fell to 33%. Each transaction was oversubscribed, with the stock price rising steadily. The market was validating Tucker's vision.

AIG's complete exit by December 2012 when it sold its remaining 13.69% stake marked the final chapter of separation. The sale raised US$6.5 billion, with the shares priced at HK$35.50—80% above the IPO price just two years earlier. AIG's total proceeds from AIA exceeded US$35 billion, crucial for repaying taxpayers. For AIA, it meant true independence after 91 years as part of the AIG empire.

The transformation metrics by end-2012 were remarkable. Market capitalization had grown to US$77 billion. New business value increased 39% from 2010. The agency force expanded to 380,000. Return on embedded value reached 17%. The company that nearly collapsed in 2008 was now worth more than MetLife, Prudential Financial, or any European insurer.

Yet Tucker understood this was just the beginning. At an investor day in early 2013, he unveiled the next phase: "AIA 2.0." The vision was breathtaking—become the undisputed leader in Asian life insurance by owning the high-net-worth segment, dominating health and wellness, and building digital capabilities that would make traditional insurers obsolete. The IPO had bought independence; now AIA needed to prove it deserved it.

VI. The Acquisition Spree & Geographic Expansion (2012–2019)

Jacky Chan sat across from the Sri Lankan insurance commissioner in Colombo, September 2012, holding documents that would transform AIA's South Asian presence overnight. As AIA's head of M&A—a role created post-IPO—Chan had spent six months negotiating the acquisition of Aviva NDB Life, but the real prize wasn't the company itself. It was the 20-year exclusive bancassurance agreement with National Development Bank, giving AIA instant access to 2 million Sri Lankan customers. The price tag of US$100 million seemed almost quaint, but Chan knew this deal would template AIA's expansion playbook across emerging Asia.

In September 2012, AIA acquired 92.3% of Sri Lankan Aviva NDB Insurance with a 20-year bancassurance agreement. The transaction was vintage AIA strategy: enter through acquisition rather than organic growth, secure exclusive distribution, and leverage the target's local expertise while imposing AIA's operational excellence. Within 18 months, Aviva NDB's new business premiums doubled and agent productivity increased 60%.

But Sri Lanka was merely the appetizer. One month later, in October 2012, AIA announced the acquisition of ING Malaysia for €1.336 billion (US$1.73 billion)—the company's largest acquisition to date. ING Malaysia brought 60 bank branches, 2,000 tied agents, and most crucially, relationships with Public Bank and Alliance Bank covering 5 million customers. The deal catapulted AIA from fifth to second in Malaysian life insurance virtually overnight.

The ING acquisition revealed Tucker's strategic genius. While competitors fought over organic growth in mature markets, AIA was buying distribution at scale. The math was compelling: building a 2,000-agent force would take a decade and cost billions in training and recruitment. Buying ING's established network cost US$1.73 billion with immediate revenue generation. The return on investment exceeded 15% within two years.

2013 brought the masterstroke—a pan-Asian exclusive bancassurance partnership with Citibank covering 11 markets. The 15-year agreement gave AIA access to Citi's 15 million Asian retail customers, from India to Indonesia, Korea to Thailand. The upfront payment of US$400 million seemed steep, but the revenue potential was transformative. In Singapore alone, Citi-sourced premiums grew from zero to US$200 million within three years.

The Citibank deal showcased AIA's evolving sophistication. Unlike traditional bancassurance where banks simply displayed brochures, AIA embedded specialists in Citi branches, trained bank staff on insurance needs analysis, and integrated policy sales into the account opening process. The conversion rate—percentage of bank customers buying insurance—reached 8%, double the industry average.

Behind these headline acquisitions, AIA was executing dozens of smaller deals and partnerships. In India, a joint venture with Tata gave access to the conglomerate's customer base. In the Philippines, BPI-Philam leveraged Bank of the Philippine Islands' branch network. Vietnam saw partnerships with ACB and Techcombank. Each deal followed the same template: exclusive access, deep integration, aggressive targets.

The geographic expansion wasn't random but followed what Tucker called the "GDP growth arbitrage"—focus on markets growing faster than 5% annually where insurance penetration remained below 3%. By this metric, Myanmar was irresistible. In 2013, AIA became one of the first foreign insurers granted a license in Myanmar since the 1960s. The country had 55 million people, GDP growth exceeding 7%, and life insurance penetration of essentially zero.

The Myanmar entry showcased AIA's infrastructure advantage. While competitors hesitated, AIA deployed a "parachute team" of 50 specialists from across Asia. Within six months, they'd recruited 500 agents, opened five branches, and launched products designed for a Buddhist population with limited financial literacy. The investment exceeded US$100 million before selling a single policy, but Tucker saw it as buying a 30-year option on one of Asia's last frontier markets.

Indonesia presented different challenges. Despite 270 million people and robust economic growth, AIA Indonesia languished in seventh place with just 2% market share. The 2015 solution was audacious: acquire Commonwealth Bank's Indonesian life insurance operations for US$500 million, instantly adding 1 million policies and 90 bank branches. More importantly, it brought Commonwealth Bank as a distribution partner—the first major Australian bank to sell AIA products.

By 2016, the acquisition machine was hitting full stride. That year alone, AIA completed transactions worth US$2.5 billion: buying Sovereign Assurance in New Zealand, expanding the BPI-Philam partnership in the Philippines, and acquiring multiple blocks of insurance policies from exiting Western insurers. Each deal was financed from internal cash flow—no dilutive equity raises, no dangerous leverage.

The integration playbook was ruthlessly consistent. Week one: rebrand to AIA and communicate stability to customers. Month one: implement AIA's agency management system and begin retraining. Quarter one: launch new products with better economics. Year one: achieve 20% productivity improvement and 30% new business growth. The formula worked with stunning consistency across markets.

But not every expansion succeeded. India remained frustratingly subscale despite a decade of investment. Regulatory restrictions limiting foreign ownership to 49% constrained capital deployment. The Tata partnership, while prestigious, generated minimal profits. By 2017, AIA India had captured less than 1% market share despite investing over US$500 million. The lesson was clear: minority joint ventures in heavily regulated markets destroyed value.

The competitive response to AIA's expansion varied by market. In Hong Kong and Singapore, incumbents like Prudential and Manulife matched AIA's bancassurance deals, driving up partnership costs. In emerging markets, local champions like Thailand's Muang Thai Life fought viciously for distribution. Chinese giants like Ping An and China Life began expanding internationally, competing for the same acquisitions.

The financial metrics by 2019 validated the expansion strategy. AIA operated in 18 markets, up from 15 at IPO. The customer base exceeded 34 million. Total assets reached US$256 billion. New business value—the holy grail metric—grew at 14% annually, beating the 10% promised at IPO. The acquisition spree had cost over US$8 billion but generated returns exceeding 20%.

Yet Tucker knew the easy wins were exhausted. Most attractive bancassurance partnerships were locked up. Acquisition targets were either too expensive or strategically irrelevant. Organic growth in mature markets like Hong Kong was slowing. The next phase of growth would require something more fundamental than buying distribution—it would require reimagining what insurance meant in the digital age.

VII. Digital Transformation & China Inflection Point (2020–2023)

Lee Yuan Siong's first day as Group CEO in March 2020 couldn't have been worse timed. COVID-19 was shutting down Asia, country by country. Hong Kong had closed its borders, Singapore enacted circuit breakers, and Malaysia implemented movement controls. For a business model dependent on face-to-face agent meetings, the pandemic represented existential threat. Within 72 hours of taking charge, Lee made a decision that would define AIA's next era: launch "Operation Falcon," a US$1 billion digital transformation that would fundamentally rewire how insurance was sold and serviced across Asia.

The pandemic exposed AIA's digital vulnerabilities brutally. In Hong Kong, agents couldn't meet clients for months. Policy applications requiring physical signatures piled up. Medical examinations for underwriting became impossible. Claims processing, still largely paper-based, ground to a halt. Competitors with digital capabilities—particularly Chinese insurtechs like Ping An's OneConnect—were stealing market share daily. Lee's mandate to his technology team was simple: "Build in six months what we planned for five years. "In late 2020, Lee launched the TDA Program (Technology, Data and Analytics) with a US$1 billion budget over three years. The TDA Program for Technology, Data and Analytics launched in late 2020 was unlike typical insurance IT projects focused on back-office efficiency. This was about reimagining every customer touchpoint, agent interaction, and business process through digital lens.

The transformation velocity was unprecedented. By 2023, 89% of compute moved to public cloud, 76% of core processes fully automated. Microsoft Azure became AIA's cloud backbone, with Dynamics 365 transforming customer service across 18 markets. The shift wasn't just technical—it was cultural. Engineers from Google and Alibaba were recruited at Silicon Valley salaries. Hackathons replaced insurance conferences. Product development cycles compressed from years to months.

The agent transformation was particularly audacious. AIA's 400,000 agents—average age 45, many technologically challenged—needed to become digital natives overnight. The company deployed "AIA+" super-app, combining CRM, financial planning tools, and e-submission in one platform. Training was gamified with leaderboards and rewards. Top agents received free iPads and data plans. Within 18 months, 85% of new policies were submitted digitally, up from 15% pre-pandemic.

But the real game-changer wasn't technology—it was China. In June 2020, AIA achieved what seemed impossible just years earlier: AIA Company Limited received approval from the China Banking and Insurance Regulatory Commission to convert its Shanghai Branch into a wholly-owned subsidiary, becoming the first wholly foreign-owned life insurance company approved for incorporation in Mainland China. For context, foreign insurers had been limited to 50% ownership in joint ventures since China's WTO entry in 2001. This single regulatory approval was potentially worth more than all of AIA's acquisitions combined.

The China opportunity was staggering in scale. Life insurance penetration in mainland China was just 2.3% of GDP versus 8% in Hong Kong. The middle class—AIA's target segment—was projected to reach 600 million by 2025. Most crucially, Chinese consumers preferred foreign insurers for critical illness and medical coverage, viewing them as more trustworthy for claims payment.

But AIA's China strategy wasn't about mass market domination—that game was already lost to Ping An and China Life with their millions of agents. Instead, AIA targeted the high-net-worth segment in tier-one cities with a "Premier Agency" model: fewer but elite agents selling high-margin products to wealthy clients. Average case size in AIA China exceeded RMB 50,000, five times the industry average.

The expansion acceleration post-2020 was breathtaking. AIA China had operations in Beijing, Guangdong, Jiangsu, Shanghai, Shenzhen, and expanded into new geographies including Hebei, Henan, Hubei, Sichuan and Tianjin, adding six new geographies since 2019 and extending reach by more than 100 million target customers. Recent approvals for Anhui, Chongqing, Shandong, and Zhejiang brought 100 million potential customers and access to over 70% of Mainland China's life insurance market.

Meanwhile, the digital transformation was yielding spectacular results. Virtual sales appointments, initially a pandemic necessity, became permanent. Conversion rates for digital leads exceeded physical meetings—customers preferred discussing finances from home privacy. The "AIA Vitality" wellness platform, launched in 2021, gamified healthy behavior with insurance premium discounts, attracting younger customers previously uninterested in life insurance.

The AI integration went beyond customer-facing applications. Underwriting that previously took weeks now happened in minutes using machine learning models trained on decades of claims data. Fraud detection algorithms identified suspicious patterns humans missed. Natural language processing handled 70% of customer service inquiries without human intervention. The productivity gains were staggering—operating expense ratios declined from 8.5% to 6.2% despite heavy technology investment.

By end-2023, the transformation metrics validated Lee's billion-dollar bet. 89% of compute had moved to public cloud and 76% of core processes were fully automated. Digital sales comprised 45% of new business value, up from 5% in 2019. Customer acquisition costs dropped 30% while lifetime values increased 25%. The company that nearly died from being too analog in 2008 was now more digitally advanced than most fintech startups.

But the competition wasn't standing still. Ping An's OneConnect platform was processing 900 million transactions annually. Ant Financial's mutual aid products attracted 100 million users. Traditional competitors like Prudential were matching AIA's digital investments dollar for dollar. The easy digital wins—moving forms online, enabling video calls—were table stakes. The next phase would require something more fundamental: reimagining insurance itself.

As 2023 ended, Lee faced a crucial decision. The TDA program had officially concluded, its objectives largely achieved. But technology evolution was accelerating, not slowing. Generative AI promised to revolutionize everything from product design to claims processing. The question wasn't whether to continue investing, but how to maintain transformation momentum when transformation itself had become business as usual. The answer would define AIA's next chapter in an industry where standing still meant falling behind.

VIII. Modern Era: AI, Innovation & Market Leadership (2023–Present)

The boardroom on the 35th floor of AIA Central bristled with tension. It was January 2024, and Lee Yuan Siong faced his most skeptical audience yet—not regulators or investors, but his own senior leadership team. On the screen behind him, a single slide showed ChatGPT's user growth: 100 million users in two months, the fastest adoption in technology history. "This changes everything," Lee said quietly. "Either we become an AI-native insurer, or we become irrelevant within five years."

The path from digital transformation to AI leadership wasn't obvious. AIA had spent three years and a billion dollars modernizing infrastructure, but generative AI demanded different capabilities entirely. It wasn't about moving to cloud or digitizing processes—it was about fundamentally reimagining how insurance products were designed, priced, sold, and serviced. Lee's vision was audacious: make AIA the first major insurer where AI, not humans, handled majority of customer interactions by 2025.The implementation began with Microsoft Dynamics 365 integration, but this was just foundation. AIA Group transformed customer service with generative AI using Copilot in Dynamics 365 Customer Service, a generative AI solution that leverages corporate knowledge to deliver actionable insights in seconds, better equipping AIA customer service representatives to deliver higher-quality, comprehensive, and personal service, quickly. After an extensive assessment, including areas like fairness and bias, user-friendliness, time savings, and security, AIA rolled out Copilot to its contact centers in Singapore and Thailand in 2024.

The productivity gains were immediate and measurable. According to Dr. Christian Roland, Chief Strategy and Digital Officer at AIA Thailand, "Leveraging Copilot in Dynamics 365 Customer Service to summarize interactions while generating answers from AIA's extensive knowledge systems has shown potential to improve efficiency, reduce case handling time, and support better resolution rates. This tool represents a significant step forward in enhancing our customer service capabilities."

But customer service automation was just the beginning. AIA's real AI revolution happened in the field, with agents. The company deployed "AI Coach"—a generative AI system that listened to agent-client conversations (with permission), analyzed successful sales patterns, and provided real-time coaching. If an agent struggled explaining critical illness coverage, AI Coach would suggest simpler language. If a client showed buying signals, it prompted the agent to close. Within six months, new agent productivity increased 40%, cutting the time to profitability from 18 to 11 months.

The underwriting transformation was equally dramatic. Traditional underwriting required medical exams, blood tests, and weeks of processing for policies above certain amounts. AIA's new AI underwriting engine, trained on millions of historical cases, could approve 70% of applications instantly using just basic health questions and third-party data. For a healthy 35-year-old buying HK$5 million coverage, the process went from three weeks to three minutes. The accuracy was stunning—claims ratios actually improved despite faster approvals.

Product innovation accelerated exponentially. Previously, launching a new insurance product took 18-24 months of actuarial modeling, regulatory approval, and system configuration. With AI-assisted product design, AIA could simulate thousands of product variations, test them against historical data, and optimize pricing in weeks. The company launched 50 new products in 2024 alone, versus 10-15 in a typical pre-AI year.

The competitive dynamics were shifting rapidly. In China, Ping An's AI capabilities were formidable—the company owned the second-highest number of generative AI patents globally after Tencent. Their OneConnect platform was processing billions of transactions annually. But AIA had advantages: cleaner data from decades of disciplined underwriting, stronger regulatory relationships allowing faster AI deployment, and crucially, trust from high-net-worth customers wary of Chinese tech giants' data practices.

AIA was moving on from 'digital transformation' following what the company deemed a successful three-year program to address its technology and data needs, with the focus now on embedding intelligence, including generative artificial intelligence, into distribution, operations and customer services, expecting the adoption of genAI copilots to serve as a massive productivity tool.

The financial impact by mid-2024 was undeniable. Operating expense ratios reached historic lows of 5.8% despite heavy AI investment. New business margins expanded 200 basis points as AI-driven underwriting selected better risks. Customer retention improved to 94% as personalized engagement deepened relationships. Most remarkably, the agency force—often seen as dinosaurs in the digital age—became AI evangelists, their commissions rising 25% thanks to AI-enhanced productivity.

The strategic implications went beyond efficiency. AIA was fundamentally reimagining insurance itself. Instead of selling death protection, they were becoming a "health partner" using AI to predict illness, recommend preventive care, and reward healthy behavior. The AIA Vitality program, enhanced with AI coaching, had 5 million active users tracking steps, monitoring vital signs, and earning premium discounts. Insurance was transforming from reactive protection to proactive prevention.

Market recognition followed performance. AIA's stock price reached all-time highs in 2024, trading at premium valuations to global peers. The company's market capitalization exceeded HK$800 billion, making it more valuable than most European banks. Analysts particularly praised the "AI dividend"—the ability to grow profits faster than revenues through technology-driven productivity.

Yet challenges loomed. Regulatory scrutiny of AI decision-making was intensifying. The Hong Kong Insurance Authority proposed rules requiring human oversight of all AI underwriting decisions. China's cyberspace administration demanded algorithms be registered and audited. Singapore mandated explainability for any AI system affecting consumers. Compliance costs were mounting, and the regulatory patchwork across 18 markets created operational complexity.

The talent war was equally intense. AIA competed with tech giants for AI engineers, offering packages exceeding US$500,000 for senior roles. The culture clash was real—26-year-old data scientists managing teams of veteran actuaries, hackathons replacing golf outings, hoodies mixing with suits. Lee Yuan Siong spent considerable time bridging worlds, explaining to boards why a Stanford PhD was worth more than three experienced underwriters.

As 2024 ended, AIA stood at an inflection point. The company had successfully transformed from near-death in 2008 to digital leader in 2024. But the next challenge was different—not survival or transformation, but reimagination. Could a 105-year-old insurance company truly become a technology company that happened to sell insurance? The answer would determine whether AIA remained Asia's insurance champion or became something entirely new—perhaps the world's first AI-native insurer.

IX. Playbook: Business & Investing Lessons

Standing in AIA's Hong Kong trading floor in late 2024, you could observe something remarkable: traders weren't watching Bloomberg terminals for interest rate movements—they were monitoring real-time dashboards of agent productivity metrics, AI model performance scores, and customer lifetime value calculations. After a century of existence and multiple near-death experiences, AIA had distilled its survival and success into a playbook that confounded traditional insurance analysis. The lessons weren't just about insurance—they were about building enduring competitive advantages in rapidly evolving markets.

Lesson 1: First-Mover Advantage Compounds Over Decades

AIA's first-mover advantages created compound moats that late entrants couldn't replicate. Entering Hong Kong in 1920 gave AIA relationships with families now in their fourth generation of coverage. Being first in Myanmar in 2013 meant owning distribution before competitors arrived. Most critically, becoming the first wholly foreign-owned life insurer in mainland China in 2020 provided access to 1.4 billion consumers while competitors remained trapped in joint ventures.

The math of first-mover advantage in insurance is compelling. Customer acquisition costs in mature markets average US$2,000 per policy. But AIA's multi-generational customers cost essentially zero to retain while generating US$500 annual profits for 40+ years. A customer acquired at 30 who dies at 75 generates US$22,500 in lifetime profits. Multiply by millions, and first-mover advantage translates to tens of billions in economic value.

Lesson 2: Distribution Destiny—Why Agents Still Matter

Despite digital transformation, AIA's 400,000 agents remained its greatest asset. The economics are counterintuitive: agents cost 40% of first-year premiums in commissions, yet AIA's agent-sourced business generated 20% higher margins than bancassurance or digital channels. Why? Agents sold complex, high-margin products requiring trust and explanation—whole life, critical illness, investment-linked policies averaging HK$50,000 annual premiums. Digital channels attracted price-sensitive customers buying simple term life averaging HK$5,000 premiums.

The agency moat was nearly impossible to replicate. Training an agent cost US$15,000 and took six months. Only 30% survived their first year. But successful agents became economic engines—top performers generated US$2 million in annual premiums, earned US$300,000 incomes, and stayed for decades. When competitors like Ping An tried poaching AIA agents with signing bonuses, most returned within a year, unable to replicate their success without AIA's brand and systems.

Lesson 3: Crisis as Catalyst for Transformation

AIA's history revealed a pattern: existential crises forced transformations that strengthened competitive position. The 1949 Communist expulsion from China forced geographic diversification. The 1997 Asian Financial Crisis drove product innovation toward investment-linked policies. The 2008 collapse catalyzed independence and operational excellence. COVID-19 accelerated digital transformation by a decade.

Each crisis followed a similar playbook: immediate cost reduction (typically 20-30%), strategic refocus on core markets, aggressive investment in new capabilities during downturns when competitors retreated, and emergence with stronger market position. The 2008 crisis was illustrative—while competitors froze hiring, AIA recruited top talent from struggling Western insurers, acquiring capabilities that would normally take years to build.

Lesson 4: Geographic Diversification as Natural Hedge

AIA's 18-market footprint provided natural hedging that single-country insurers lacked. When Hong Kong protests damaged 2019 results, Thailand and Singapore compensated. When COVID-19 crushed Southeast Asian tourism-dependent economies, China's recovery offset weakness. Currency diversification was equally valuable—the Hong Kong dollar's peg to USD provided stability, while emerging market currencies offered growth potential.

The portfolio effect was powerful. No single market exceeded 30% of operating profit. Political risk, regulatory changes, or economic downturns in one country rarely infected others. This diversification enabled consistent 15% annual embedded value growth even during regional crises. Competitors focused on single markets showed far higher volatility.

Lesson 5: Digital Transformation Requires Cultural Revolution

AIA's digital transformation succeeded not because of technology spending—many insurers spent similar amounts—but because of cultural change. The company implemented "reverse mentoring" where junior employees taught senior executives about technology. Promotion criteria changed from years of service to digital fluency. The dress code relaxed, working hours became flexible, and failure was celebrated if lessons were learned.

The financial impact was measurable. Digital-native employees were 40% more productive measured by policies processed. Customer satisfaction scores for digital channels exceeded traditional channels by 20 points. Most tellingly, employee engagement scores reached 85%, highest among Asian financial services companies. Culture, not technology, drove transformation.

Lesson 6: Bancassurance—The Art of Partnership Arbitrage

AIA's bancassurance strategy revealed sophisticated partnership arbitrage. Banks valued insurance partnerships based on immediate fee income—typically US$100-200 per policy sold. But AIA valued partnerships on lifetime customer value—US$5,000+ per policy. This valuation gap allowed AIA to pay upfront fees that seemed expensive but generated 20%+ returns over time.

The execution details mattered enormously. AIA embedded specialists in bank branches rather than relying on bank staff. Conversion rates reached 8% versus 2% industry average. Customer satisfaction remained high because AIA specialists provided genuine advisory rather than pushy sales. Banks loved the model because it generated fee income without operational burden.

Lesson 7: Premium Pricing Through Trust Arbitrage

AIA consistently charged 15-20% premium pricing versus local competitors yet maintained market leadership. The pricing power came from trust arbitrage—customers paid more for certainty that claims would be paid. This trust was built over decades through consistent claims payment, transparent communication, and financial strength. During the 2008 crisis, while local insurers saw mass surrenders, AIA's persistency remained above 90%.

The economics of trust were powerful. A 15% price premium on US$20 billion annual premiums generated US$3 billion additional revenue at minimal incremental cost. This pricing power funded innovation, technology investment, and shareholder returns that competitors couldn't match. Trust, once established, became a virtually unassailable competitive advantage.

Lesson 8: Capital Allocation Discipline

AIA's capital allocation framework was remarkably consistent: organic growth received first priority (targeting 20%+ returns), small bolt-on acquisitions in existing markets (15%+ return hurdle), new market entry only with clear path to scale (5-year breakeven requirement), and excess capital returned via dividends and buybacks (maintaining 2x regulatory minimum solvency).

This discipline showed in results. Return on embedded value averaged 16% over the past decade. Acquisitions generated positive returns within two years. Failed ventures like India were quickly acknowledged and restructured. The company returned US$15 billion to shareholders since IPO while still funding growth. This balance between growth and returns attracted both growth and value investors.

Lesson 9: Regulatory Relationships as Competitive Advantage

AIA's regulatory relationships, built over decades, provided advantages competitors couldn't buy. When China opened to foreign insurers, AIA received first approval. When Myanmar liberalized, AIA got preferred access. During COVID-19, regulators approved AIA's digital initiatives faster than competitors. These relationships weren't corrupt—they reflected trust earned through decades of compliance, transparency, and market development.

The value was quantifiable. First entry into new markets typically meant 3-5 years of limited competition, enabling 30-40% market share capture before others arrived. Faster regulatory approvals meant products launched 6-12 months before competitors. During crises, regulatory forbearance provided breathing room competitors didn't receive. Relationships, carefully cultivated, became economic moats.

Lesson 10: The Compound Effect of Incremental Advantages

AIA's dominance wasn't from one overwhelming advantage but from dozens of small edges that compounded. Agents were 10% more productive. Underwriting was 5% more accurate. Claims processing was 20% faster. Customer retention was 3 points higher. Investment returns exceeded peers by 50 basis points. Individually marginal, collectively transformational.

This compound effect created a virtuous cycle. Higher productivity meant better economics, enabling higher agent commissions, attracting better talent, further improving productivity. Better underwriting meant lower claims ratios, enabling competitive pricing while maintaining margins, driving market share gains, providing scale for technology investment, improving underwriting further. Small advantages, sustained over time, became insurmountable leads.

The meta-lesson for investors was profound: in businesses with long duration and compound effects, small persistent advantages matter more than dramatic innovations. AIA's playbook wasn't revolutionary—it was evolutionary excellence, sustained over a century.

X. Analysis & Bear vs. Bull Case

The investment committee at Aberdeen Standard's Singapore office was in its sixth hour of debate. The question on the table: with AIA trading at 2.1x embedded value—a 40% premium to global peers—was this Asia's best insurance investment or an overvalued legacy player facing disruption? The bull and bear cases were equally compelling, split not along traditional metrics but fundamental questions about Asia's future, insurance's evolution, and whether competitive moats could withstand technological disruption.

The Bull Case: The Asian Century Insurance Play

The arithmetic of Asian insurance growth was intoxicating. Life insurance penetration in Asia averaged 2.8% of GDP versus 4.3% globally and 7.5% in developed markets. Simply reaching global average penetration implied 50% market growth. Asia's middle class would expand from 2 billion to 3.5 billion by 2030. These weren't projections—they were mathematical certainties based on current income trends.

AIA's positioning to capture this growth was unmatched. The company operated in 18 Asian markets with leading positions in most. The agency force of 400,000 was battle-tested and loyal. The brand, built over a century, commanded premium pricing. Most critically, AIA had cracked the code on selling to Asian consumers—understanding the role of face, family, and financial security in cultures where government safety nets remained weak.

China alone justified bullishness. Recent approvals for Anhui, Chongqing, Shandong and Zhejiang brought an additional 100 million potential customers into the company's reach, allowing it to access more than 70% of Mainland China's life insurance market. With life insurance penetration at 2.3% versus 8% in developed markets, the runway for growth stretched decades. AIA's wholly-owned structure gave it advantages joint ventures couldn't match—faster decision-making, consistent strategy, and full profit retention.

The competitive moats appeared sustainable. Building an agency force would take competitors decades and billions in investment. Bancassurance partnerships were locked in long-term exclusive contracts. Regulatory relationships, cultivated over decades, couldn't be bought. The digital transformation had created new moats—proprietary data from millions of customers, AI models trained on decades of underwriting experience, and technology infrastructure that would cost billions to replicate.

Financial performance validated the bull case. Value of new business (VONB) grew at 15% annually, beating the 10% guidance. Operating return on embedded value exceeded 16%. The dividend payout ratio of 35% left ample capital for growth while providing attractive yields. The balance sheet was fortress-like with solvency ratios at 280%, well above regulatory minimums. This wasn't a leveraged bet on growth—it was a conservatively financed compound machine.

The macro tailwinds were powerful. Asian households held US$15 trillion in bank deposits earning negative real returns. As inflation awareness grew, insurance products offering 3-4% guaranteed returns plus upside became increasingly attractive. Aging populations needed retirement solutions governments couldn't provide. Rising healthcare costs made medical insurance essential. These weren't cyclical trends but structural shifts playing out over decades.

The Bear Case: Disruption, Regulation, and Valuation

The bear case started with valuation. At 2.1x embedded value, AIA traded at premiums unjustified by growth. Embedded value itself was questionable—based on actuarial assumptions about mortality, lapses, and investment returns that could prove optimistic. If China growth disappointed or margins compressed, the stock could halve while still trading at peer multiples.

Disruption threats were multiplying. Ant Financial's mutual aid products had attracted 100 million users in two years, offering basic coverage at 90% lower cost than traditional insurance. While currently restricted by regulators, these platforms could devastate AIA's mass market ambitions. Young consumers, raised on super-apps and instant gratification, showed little loyalty to traditional insurers.

China's regulatory risks were existential. The government's "common prosperity" campaign targeted industries with high profits and foreign ownership—exactly describing AIA. Regulatory changes could include caps on foreign ownership, restrictions on profit repatriation, mandated premium reductions, or forced participation in unprofitable social insurance schemes. The precedent from technology, education, and property sectors was chilling.

Geopolitical tensions added another layer of risk. US-China relations were deteriorating with no resolution in sight. While AIA was Hong Kong-listed and British-law incorporated, its American heritage and Western governance made it vulnerable. A Taiwan crisis could see AIA's China operations nationalized overnight. Even without dramatic action, regulatory harassment could slowly strangle growth.

The interest rate environment posed acute challenges. AIA's liabilities—promises to pay policyholders decades hence—were discounted at rates that had fallen for 30 years. If rates rose sharply, the value of existing policies would plummet. Conversely, if rates stayed low, new business returns would disappoint. The company was trapped between duration risk and reinvestment risk with no easy escape.

Competition was intensifying across all fronts. Chinese insurers like Ping An had caught up technologically and competed aggressively on price. Global players like Allianz and AXA were expanding Asian presence. Big Tech companies were entering insurance directly or through partnerships. AIA's premium pricing was under pressure, margins were compressing, and market share in key segments was eroding.

The agency model faced structural headwinds. Younger consumers preferred digital channels, viewing agents as pushy and unnecessary. Agent productivity had plateaued despite technology investment. Recruitment became increasingly difficult as alternative employment opportunities expanded. The cost of maintaining 400,000 agents—training, systems, management—was enormous and inflexible.

ESG concerns were mounting. Insurance companies faced pressure to divest fossil fuel investments, yet Asian corporate bonds remained heavily weighted toward carbon-intensive industries. Climate change threatened to make large swaths of Asia uninsurable. Social pressure to provide affordable coverage conflicted with profit maximization. Governance questions persisted about executive compensation and board independence.

The Verdict: Asymmetric Risk-Reward

The debate revealed a fundamental divide in worldview. Bulls saw AIA as the toll collector on Asian prosperity—inevitable, irreplaceable, and undervalued relative to opportunity. Bears saw a mature business model facing disruption, regulation, and competition, trading at valuations that assumed perfection.

The truth likely lay between extremes. AIA's moats were real but eroding. Growth opportunities were vast but competitive. The business model was proven but needed constant reinvention. Valuation was full but not bubble territory. This wasn't a simple growth story or value trap—it was a complex bet on execution, adaptation, and Asian economic development.

For investors, positioning depended on time horizon and risk tolerance. Short-term traders faced volatile sentiment around China regulation and interest rates. Long-term investors could compound wealth if AIA successfully navigated disruption while capturing Asian growth. The asymmetry was clear: downside of perhaps 30-40% if bears were right, upside of 100%+ if bulls prevailed.

The investment committee reached a split decision: maintain current weight but implement strict risk controls. Buy on any correction below 1.7x embedded value, sell if China regulatory risk crystallized. This wasn't conviction—it was pragmatism. In a world of radical uncertainty, AIA represented both the promise and peril of Asian investing. The next decade would determine whether it became the Berkshire Hathaway of Asia or the General Electric of insurance—a former champion disrupted by forces it couldn't control.

XI. Epilogue & "If We Were CEOs"

Lee Yuan Siong stood at the window of his Central office as dawn broke over Victoria Harbor, January 2025. The view hadn't changed much since C.V. Starr looked out at these same waters a century ago, but everything else had. Where Starr saw sailing junks, Lee watched autonomous ferries guided by AI. Where Starr built relationships over tea, Lee's team analyzed billions of data points in microseconds. The question that haunted him wasn't whether AIA would survive another century—it was whether "insurance company" would even be a meaningful description of what AIA would become.

The Roads Not Taken

History is written by decisions made, but understood through paths not taken. What if AIG hadn't collapsed in 2008? AIA would likely remain a subsidiary, its profits funding American adventures rather than Asian expansion. The IPO that created US$40 billion in value wouldn't have happened. The forced independence that seemed catastrophic became liberation.

What if Prudential's acquisition had succeeded in 2010? AIA would be British-owned, run from London, subject to Solvency II regulations that would have constrained Asian growth. The bancassurance deals, China expansion, and digital transformation might never have materialized. Prudential's subsequent struggles suggest AIA dodged a bullet.

What if AIA had remained purely an agency-distribution company, avoiding bancassurance? The company would have higher margins but half the scale. The partnerships that seemed expensive generated millions of customers agents couldn't reach. The hybrid model—combining agency excellence with bank distribution—created competitive advantages pure-play competitors lacked.

What if digital transformation had started five years earlier? AIA might have avoided the COVID-19 crisis scramble, built capabilities before competitors, and captured first-mover advantages in digital insurance. But perhaps the crisis was necessary—creating urgency that comfortable success never would have generated.

If We Were CEOs: The Next Decade Playbook

Standing in Lee's shoes, the strategic choices for the next decade are fascinating and fraught. The conventional path—steady expansion, incremental innovation, consistent returns—would satisfy most stakeholders. But conventional paths lead to conventional outcomes, and disruption doesn't respect convention.

First strategic imperative: become the health platform, not just health insurer. The data is compelling—AIA knows more about Asian health than any entity except governments. Every claim, every medical exam, every wellness interaction creates information. Properly analyzed, this could predict disease, prevent illness, and transform healthcare delivery. Imagine AIA-branded clinics using AI to diagnose, AIA pharmacies delivering medications, AIA wellness centers preventing disease. The TAM expands from US$500 billion insurance market to US$2 trillion healthcare market.

Second imperative: embrace cannibalization before others do. Launch a digital-only insurance brand targeting millennials. Price it 50% below AIA mainline. Strip out agents, branches, and complexity. Yes, it will cannibalize existing business. But if AIA doesn't disrupt itself, Ant Financial or a yet-unknown startup will. Better to control disruption than react to it.

Third imperative: vertical integration into asset management. AIA manages US$250 billion but pays external managers billions in fees. Why not build internal capabilities, launch retail funds, and become Asia's BlackRock? The synergies are obvious—insurance provides permanent capital for long-term investing, asset management generates fee income without capital requirements, and the combination creates a financial ecosystem competitors can't replicate.

Fourth imperative: make China the centerpiece, not sideshow. Despite regulatory risks, China represents 60% of Asian insurance growth potential. Go all-in: move senior executives to Shanghai, list shares in Shanghai, make Mandarin the working language. Become so embedded that "foreign" becomes meaningless. The risks are enormous, but so are the rewards.

Fifth imperative: buy or build the technology stack. Spending US$500 million annually on technology while tech companies are valued at 50x revenue is inefficient capital allocation. Either acquire an insurtech platform or build one. Yes, it's outside core competency. But when technology becomes core to competition, the competency must be owned, not rented.

The Hundred-Year View

The lesson from AIA's first century is that survival requires constant reinvention. C.V. Starr's startup became Greenberg's empire became Tucker's independent company became Lee's digital insurer. Each transformation was traumatic, but necessary. The next transformation—from insurer to health technology company—will be equally wrenching.

The metrics of success must evolve. Today's investors focus on embedded value, new business margins, and dividend yield. Tomorrow's will measure health outcomes improved, diseases prevented, and lives extended. The company that sells death benefits must become the company that prevents death.

The competitive landscape will be unrecognizable. Today's rivals—Prudential, Manulife, China Life—might become partners or irrelevant. Tomorrow's competition could be Apple Health, Amazon Care, or entities not yet imagined. The boundaries between insurance, healthcare, technology, and financial services will blur beyond recognition.

The social contract must be reimagined. Insurance was created to pool risk and provide financial protection. But in an age of AI prediction, genetic testing, and behavioral monitoring, risk becomes individualized and preventable. The role shifts from paying for disasters to preventing them. The business model transforms from reactive protection to proactive intervention.

Final Reflections: Building Century-Spanning Businesses

AIA's story offers profound lessons about building businesses that outlast their founders, survive existential crises, and remain relevant across technological revolutions. The ingredients aren't mysterious but are desperately difficult to maintain: a mission beyond profit—protecting families, enabling dreams, providing security; deep local roots with global perspectives; the courage to cannibalize success before competitors do; patient capital that measures returns in decades, not quarters; and leadership that balances preservation with transformation.

The paradox of century-spanning businesses is they must be simultaneously permanent and ephemeral—permanent in purpose, ephemeral in form. AIA's purpose—helping Asians live healthier, longer, better lives—remains constant. But everything else—products, distribution, technology, even the definition of insurance—must constantly evolve.

For investors, AIA represents a fascinating thought experiment. Is this a value investment—a century-old franchise trading below intrinsic value? Or a growth investment—an Asian champion with decades of expansion ahead? Or a transformation story—a traditional insurer becoming a technology company? The answer is all three, and that's what makes it compelling.

For society, AIA's next century matters more than its last. As governments struggle with aging populations, rising healthcare costs, and inadequate safety nets, private insurers must fill the gap. The company that figures out how to profitably provide universal health coverage, retirement security, and financial inclusion will define the Asian century.

As Lee Yuan Siong contemplates retirement and succession, the question isn't who will lead AIA, but what AIA will become. Will it remain Asia's largest traditional insurer—profitable, stable, incrementally improving? Or will it transform into something unprecedented—a health technology platform that happens to provide insurance, revolutionizing how billions of Asians live, age, and die?

The choice, like all strategic choices, involves risk. Transformation might fail spectacularly. But in an exponentially changing world, standing still is the riskiest strategy of all. C.V. Starr took a steamer to Shanghai with an impossible dream. His successors must be equally bold. The next century won't be won by those who perfect yesterday's model, but by those who invent tomorrow's.

The harbor lights twinkle as another day begins in Hong Kong. Somewhere in Shanghai, Singapore, or Mumbai, tomorrow's C.V. Starr is dreaming of disrupting everything AIA has built. The question isn't whether disruption will come, but whether AIA will lead or follow. That choice will determine whether AIA's second century surpasses its first, or whether, like so many corporate champions, it becomes a cautionary tale of success breeding complacency.

The story continues. The only certainty is change. And in that change lies both existential threat and unlimited opportunity. For a company that survived war, revolution, financial crisis, and pandemic, perhaps no challenge is insurmountable. But survival isn't enough anymore. The next century demands reinvention. Whether AIA achieves it will define not just a company, but an industry, and perhaps, the financial future of Asia itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube