مصرف الراجحي Al Rajhi Bank: The Sidewalk Shariah Juggernaut

I. Introduction & Episode Roadmap

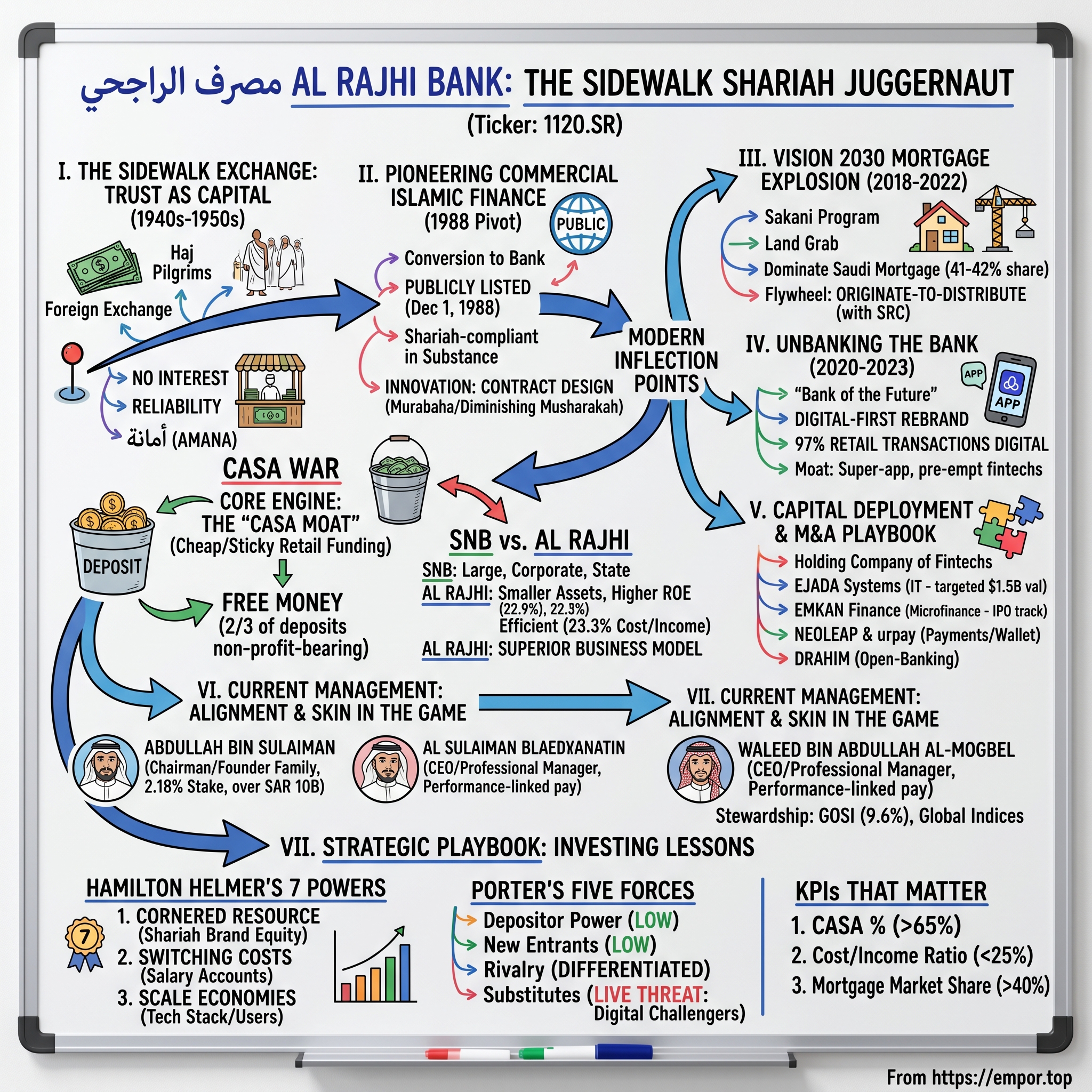

Picture a stretch of packed dirt in 1940s Riyadh, before the oil money, before the skyscrapers, before there was anything resembling a central bank in the Kingdom of Saudi Arabia. A pilgrim arrives for the Haj — الحج — carrying a pocketful of Indian rupees, Egyptian pounds, Ottoman-era coins, whatever currency his journey demanded. He needs riyals, and he needs someone he can trust not to clip the coins or rig the rate. On the side of the road, four brothers have laid out their wares: foreign banknotes and coins, organized on a cloth, in the open air. No vault. No marble lobby. No license from any authority, because no authority yet exists. Just four men named Al Rajhi and the only collateral that matters in a society like this one — their word.

Now fast-forward roughly eighty years. That sidewalk money-changing stall has become مصرف الراجحي Al Rajhi Bank, trading on تداول Tadawul under the ticker 1120.SR, sitting on a balance sheet of more than SAR 1.05 trillion — about $280 billion — and wearing the crown as the largest Islamic bank on Earth by assets.1 How does a currency stall on a dirt road become a trillion-riyal financial institution without ever — not once, not for a single transaction — charging or paying interest? That is the story of this episode.

And here's the part that should make any global bank investor sit up. Al Rajhi does not earn its keep the way most banks do. In the first quarter of 2026, the bank reported a return on equity of 22.9% and a cost-to-income ratio of 23.3%.23 Sit with those two numbers for a moment. The median large global bank fights tooth and nail to clear a 10% ROE, and most Western retail banks would throw a party if they could push their cost-to-income ratio below 50%. Al Rajhi is roughly twice as profitable on equity and roughly twice as efficient as the typical big bank. It spends less than a quarter of every riyal of income just to keep the lights on. In banking, that is not a rounding difference. That is a different sport.

The lazy assumption would be that this is some sleepy, sand-and-stone mortgage lender coasting on a captive religious market. The reality is almost the opposite. Al Rajhi is, functionally, a technology company that happens to hold a banking license. Roughly 97% of its retail transactions run through digital rails, and about nine of every ten new accounts are opened with no branch visit and no paper.4 The bank has spent the last several years quietly building and buying fintech businesses inside its own walls — a payments processor, a microfinance lender, an IT software powerhouse, an open-banking robo-advisor — and is now preparing to spin several of them out at multibillion-dollar valuations.

So here is the roadmap. We start on that dirt sidewalk and trace how trust — amana, أمانة — became the original form of capital. We walk through the 1988 transformation from exchange house to publicly listed bank, and the financial engineering the brothers had to invent to build a commercial bank with no interest. Then we hit the modern inflection points that define the company investors are buying today: the Vision 2030 mortgage explosion, the digital "unbanking" of the bank, and an aggressive capital-deployment and M&A machine. We'll war-game the rivalry with البنك الأهلي السعودي Saudi National Bank, dissect the team running the place today, and close by running Al Rajhi through Hamilton Helmer's 7 Powers and Porter's Five Forces. Three themes will recur, so name them now: the CASA moat (Shariah compliance as a source of near-free retail money), the Sakani boom (re-engineering the Saudi housing market), and unbanking the bank (building a digital ecosystem that out-fintechs the fintechs). Let's begin where it began — on the sidewalk.

II. The Sidewalk Exchange: Trust as the Original Capital

To understand Al Rajhi, you have to understand the economy it was born into, because that economy barely resembles a financial system at all. In the 1940s and 1950s, the Kingdom of Saudi Arabia had no meaningful banking infrastructure for ordinary citizens, no deposit insurance, no monetary authority worth the name until the Saudi Arabian Monetary Agency was founded in 1952. What it had instead was the single largest recurring movement of people and money in the Muslim world: the annual pilgrimage to Mecca. Every year, hundreds of thousands of pilgrims arrived from dozens of countries, each one needing to convert foreign money into something usable locally. That flow of pilgrims was, in effect, a foreign-exchange market wandering through the desert on foot.

Into that gap stepped four brothers — Saleh, Sulaiman, Abdullah, and Mohammed Al Rajhi — sons of a modest family from the town of Al Bukayriyah in the Qassim region.5 The origin story is almost comically humble, and the family has never tried to dress it up: the brothers began as small-scale money changers, at points so poor that the youngest reportedly worked as a porter and a kafeel (a kind of guarantor-cum-laborer) before the business found its feet.6 What they were selling on that sidewalk wasn't really currency. Currency is a commodity; anyone with a cash box can sell it. What they were selling was reliability — the assurance that the exchange rate was fair, that the count was honest, and that money handed over in Riyadh could be reliably delivered or redeemed elsewhere. In a cash society with no courts to speak of for commercial disputes and no regulators to call, that reliability was the product.

By 1957 the brothers had formalized the operation, and over the following two decades they built something genuinely remarkable for the era: a sprawling physical network of cash-transfer and exchange centers spread across the Kingdom, eventually consolidated in 1978 under the umbrella of شركة الراجحي للصرافة والتجارة Al Rajhi Trading and Exchange Corporation.5 Think about what that network actually was. Long before "remittances" became a fintech buzzword, the Al Rajhis had built a domestic and cross-border money-movement rail by hand — physical offices where a worker in one city could hand over cash and have a relative collect it in another. They were running a manual, analog version of what we'd now call a payments network, and they were doing it at national scale.

Now, the decision that defined everything. From the very beginning, the brothers refused to deal in riba — ربا, the interest that Islamic jurisprudence forbids. This was not a marketing position or a late-stage rebrand; it was a religious conviction baked into the enterprise from day one. And in a society as devout as mid-century Saudi Arabia, that conviction was worth more than any product feature. The conventional banks that existed in the Kingdom were foreign or interest-based, and a large segment of the population regarded depositing money with them as spiritually compromised. The Al Rajhi name, by contrast, carried an almost unimpeachable reputation for Shariah purity. The brothers had built a monopoly not on a product but on a feeling — the confidence of a religiously observant population that their money was being handled in a way that wouldn't cost them in the next life.

Here's why this matters for the trillion-riyal bank that exists today, and why we don't need to linger longer in the mid-century. That manual network of remittance and exchange centers became the physical skeleton of a modern retail-deposit machine. The branches were already there. The customer relationships were already there. The brand's association with trust and religious propriety was already there. When the business eventually became a bank, it didn't have to acquire customers the way a startup does — it inherited a nation's worth of them, pre-sold on the single most important attribute a Saudi depositor cares about. The brothers had spent thirty years accumulating the one asset that cannot be bought, copied, or out-spent: generational trust. The only question left was how to turn an exchange house into a bank without betraying the very principle that made it valuable. That question came to a head in the late 1980s.

III. The 1988 Pivot: Pioneering Commercial Islamic Finance

By the mid-1980s, the Al Rajhi exchange business had a problem that most businesses would kill for: it had grown too big and too important to remain an unregulated money changer. It was holding what amounted to deposits from a huge swath of the population, moving enormous sums, and operating at a scale that made the monetary authorities understandably nervous. An exchange house of that size, sitting outside the formal banking system, was a systemic question waiting to be answered. The resolution came from the top. In June 1987, Royal Decree No. M/59, together with a resolution of the Council of Ministers, authorized the conversion of the Al Rajhi exchange operation into a formal, licensed joint-stock bank.5

This was not a trivial bureaucratic reshuffle, and to appreciate the drama you have to understand the theological tightrope involved. Saudi Arabia's religious establishment had long been wary of banks precisely because banks, by definition, run on interest. For the Al Rajhi business — whose entire brand equity rested on not being a riba institution — to become a "bank" risked the gravest possible reputational injury: the accusation that the family had sold its principles for a banking license. The conversion was, in the words of one contemporary analysis, a kind of financial redemption that arrived only after genuine religious controversy.7 The resolution was elegant: Al Rajhi would become a bank in legal form, but it would remain entirely Shariah-compliant in substance, never charging or paying conventional interest. It would be a commercial bank built on Islamic contracts.

The capstone was the public listing. On December 1, 1988, Al Rajhi Banking and Investment Corporation listed its shares on the Saudi exchange, the institution that would later become تداول Tadawul.8 For the Saudi public, this was not just another IPO — it was the chance to own a piece of the one financial institution that carried the family's stamp of religious legitimacy. Public appetite to own a Shariah-compliant, joint-stock bank was fervent, reflecting how rare and how culturally resonant the proposition was. The newly minted bank inherited the exchange network, the deposit relationships, and above all the brand, and converted them into the foundation of a publicly traded enterprise.

But going public solved only the corporate-structure problem. It did nothing to solve the harder, more interesting puzzle: how do you actually run a commercial bank if you can't lend money at interest? A conventional bank's entire engine is the spread between what it pays depositors and what it charges borrowers. Strip out interest and, on paper, you've removed the motor. This is where Al Rajhi's real innovation lived — not in the marble of a new headquarters, but in contract design. The bank became one of the great pioneers of practical, commercial-scale Islamic finance, taking concepts that had existed mostly in jurisprudential texts and turning them into mass-market banking products.

Two structures matter most, and they're worth explaining in plain terms because they power the modern bank. The first is murabaha — مرابحة, or cost-plus financing. Instead of lending you SAR 100,000 to buy a car and charging interest, the bank itself buys the car for SAR 100,000 and then sells it to you for, say, SAR 115,000, payable in installments. There's no interest; there's a disclosed markup on a real asset the bank genuinely owned, however briefly. Economically it rhymes with a loan, but legally and theologically it is a trade, and that distinction is the whole ballgame. The second structure is diminishing musharakah — مشاركة, or co-ownership that shrinks over time. Here the bank and the customer jointly buy an asset — most importantly, a house. The customer gradually buys out the bank's share while paying rent on the portion the bank still owns, until the customer owns it outright. No interest, just a partnership that winds down. Hold that second concept in your mind, because diminishing musharakah is the exact mechanism that would, three decades later, let Al Rajhi run the table on the entire Saudi mortgage market. The playbook invented in 1988 was about to meet the biggest housing push in the Kingdom's history.

IV. Modern Inflection Point I: The Vision 2030 Mortgage Explosion (2018–2022)

In April 2016, a thirty-year-old crown prince stood in front of the Saudi public and the world and unveiled a document that would reorder the Kingdom's economy: رؤية 2030 Vision 2030. HRH Crown Prince Mohammed bin Salman's grand strategy to wean Saudi Arabia off oil was sweeping and ambitious, but buried within its hundreds of targets was one line that would prove transformational for Al Rajhi specifically: the goal of raising the rate of Saudi homeownership from 47% to 70%. On its face, that's a social-policy aspiration. In practice, it was a starting gun for the single largest mortgage-origination opportunity in the history of the Kingdom — and Al Rajhi was standing closest to the line.

The mechanism the government built to hit that target was the سكني Sakani program, run through the Ministry of Housing. Sakani's job was to make homeownership achievable for ordinary Saudi citizens by subsidizing and supporting home financing at massive scale — providing land, units, and crucially, subsidized financing for hundreds of thousands of households.9 For a Saudi family, the deal was suddenly compelling: the government would underwrite a big chunk of the cost of getting into a home. All that family needed was a bank to write the actual mortgage. And which bank did a religiously observant Saudi household — newly able to afford a home — trust to structure that mortgage in a Shariah-compliant way? You already know the answer.

What happened next was a land grab, and the word is not too strong. Al Rajhi pointed its single greatest asset — an enormous base of retail deposits gathered from across the Kingdom — directly at the mortgage opportunity, and used the diminishing-musharakah structure to write home financing at a pace nobody could match. The bank's home-finance book exploded over the 2018–2022 window, and Al Rajhi captured something on the order of 41% to 42% of all residential mortgages in the entire country, making it the dominant force in the most concentrated mortgage market in the world — a market where just three banks together hold north of 60% share.10 To put that in perspective: in most large economies, the biggest single mortgage lender might hold low-double-digit market share. Al Rajhi alone was writing roughly four of every ten home loans in a nation of tens of millions. That is not market leadership; that is market gravity.

But running a mortgage machine at that velocity creates a very specific engineering problem, and this is where the strategy gets sophisticated. Mortgages are long-dated assets — twenty, twenty-five, thirty years — while the deposits funding them are short-term and can walk out the door tomorrow. Write enough of them and you tie up enormous amounts of capital and balance-sheet capacity in illiquid, decades-long commitments. Eventually the machine seizes up: you simply run out of room to write the next loan. Al Rajhi needed a way to keep originating without drowning in its own success.

The answer was an "originate-to-distribute" arrangement with the Saudi Real Estate Refinance Company — SRC, the mortgage-liquidity vehicle owned by the Public Investment Fund and modeled loosely on America's Fannie Mae. In a landmark deal, SRC agreed to purchase mortgage portfolios from Al Rajhi totaling SAR 10 billion — later extended to roughly SAR 10.8 billion — effectively buying seasoned home loans off Al Rajhi's books.1112 Why does that matter? Because every riyal of mortgage that SRC takes off the balance sheet is a riyal of capital and capacity that Al Rajhi can recycle into writing new loans. The bank originates, hands off a chunk of the long-dated risk to a government-backed refinancer, frees up its balance sheet, and goes back to originating. It's a flywheel: write loans, sell some down, write more loans, all while keeping the lucrative customer relationship. Al Rajhi had figured out how to dominate the mortgage market and stay liquid — capturing the upside of Vision 2030's housing push without choking on the very assets it was creating. The mortgage engine was roaring. But management could see a second front opening up, one that had nothing to do with bricks and everything to do with screens.

V. Modern Inflection Point II: "Unbanking" the Bank (2020–2023)

Here is a question that should worry the executive team of any incumbent bank in the 2020s: what happens when an entire generation of your customers decides they never want to walk into one of your branches again? For most of banking history, the branch was the bank. The branch was where trust was performed — the vault, the teller, the manager who knew your name. Al Rajhi had built the largest branch and exchange network in the Kingdom over half a century. And around 2020, the bank made a counterintuitive bet: that its single greatest physical asset was becoming a liability, and that the future belonged to whoever could deliver the bank through a glass rectangle in a customer's hand.

The strategic framing was called "Bank of the Future," and in 2021 it manifested as a sweeping digital-first rebrand — a new visual identity, yes, but more importantly a reorganization of the bank's entire operating philosophy around digital channels. The thesis was blunt: modern Saudi consumers, one of the youngest and most smartphone-saturated populations on the planet, did not want to visit branches, fill out forms, or wait in queues. They wanted to do everything from their phones, instantly. So Al Rajhi set out to build not just a better banking app, but a financial super-app — a single digital surface where a customer could bank, pay, borrow, invest, and manage their entire financial life.

The execution numbers are genuinely staggering, and they're the heart of why the "tech company with a banking license" framing isn't hype. The Al Rajhi app grew into one of the most-used applications in the country, with a base of active users running into the tens of millions — extraordinary penetration in a population the size of Saudi Arabia's. Roughly 97% of the bank's retail transactions now execute digitally, meaning the branch has been almost entirely disintermediated from day-to-day banking.4 Even more telling: around 90% of new customer accounts are opened with zero physical documents and zero branch visits — fully remote, fully digital onboarding.4 A new customer can go from "downloaded the app" to "fully verified account holder" without ever touching paper or speaking to a human. For a bank whose brand was built on physical, face-to-face trust, that is a remarkable act of self-reinvention.

Now, the analytically interesting part — why this was defensive, not just convenient. Across the world in this era, traditional banks were being picked apart by fintech challengers: nimble, app-native startups that peeled off the profitable, easy-to-digitize pieces of banking — payments, lending, foreign exchange, savings — and left incumbents with the expensive, regulated, low-margin remainder. The fintech playbook works because legacy banks are slow, their apps are bad, and their cost structures are bloated. Al Rajhi looked at that threat and effectively pre-empted it. By building a digital experience that was as good as or better than what a standalone fintech could offer — and embedding it inside an institution that already had the trust, the deposits, the license, and the customer base — the bank converted potential disruptors into features inside its own ecosystem. Why would a Saudi customer download a separate payments app or a separate savings app when their Al Rajhi super-app already does it, backed by the most trusted name in the Kingdom?

This is the "unbanking the bank" idea in full. Al Rajhi didn't wait to be disrupted; it disrupted itself, on its own terms, with its own balance sheet behind it. The digital leapfrog didn't just modernize the customer experience — it built a moat. Each new capability folded into the super-app raised the cost, for any external fintech, of prying a customer away. And it set up the most aggressive phase of the whole story: rather than merely defending against fintechs, Al Rajhi decided it would build and buy them, run them as subsidiaries, and then crystallize their value in the public markets. The bank was about to become a fintech holding company.

VI. Modern Inflection Point III: The Capital Deployment & M&A Playbook

Every great compounder eventually faces the same luxury problem: it generates so much cash that the question shifts from "how do we survive?" to "what do we do with all of this?" By the early 2020s, Al Rajhi's core engine was throwing off enormous profits, and management made a decision that separates the merely profitable banks from the genuinely strategic ones. Rather than simply pay it all out or pile it into more mortgages, Al Rajhi went on a build-and-buy campaign across the fintech and IT stack — internalizing capabilities that most banks rent from vendors, and structuring each one as a standalone subsidiary it could eventually monetize. The core question for investors is the obvious one: did they overpay during this aggressive expansion? The evidence so far suggests the opposite.

Ejada Systems — buying the software factory. Start with the most contrarian move. In 2022, Al Rajhi acquired 100% of إيجادة Ejada Systems, one of the region's significant IT and software-services firms, to bring its technology development in-house rather than depend on external integrators.13 On the surface, a bank buying an IT services company looks like classic empire-building — the kind of "diworsification" that destroys value. But look at what the asset has done. By the close of 2024, Ejada posted a 22% year-over-year jump in revenue and built its new-contract backlog to roughly SAR 2.16 billion, a 41% annual increase that blew past its own targets.14 Why does that matter for valuation? Because comparable Saudi IT powerhouses — the likes of Solutions by stc — trade in the public market at rich multiples of 25 to 30 times earnings, the kind of premium reserved for high-growth technology, not low-growth banking. Al Rajhi is now preparing to list Ejada on Tadawul. The company secured regulatory clearance from the Capital Market Authority to float a large minority stake, and reporting has pegged the targeted valuation at around $1.5 billion, with global banks including Goldman Sachs tapped to arrange the deal.1516 If a software business Al Rajhi bought to serve itself can be floated at a billion-and-a-half-dollar tech multiple, the bank didn't overpay — it bought an accretive asset at a banking-sector discount and is about to re-rate it at a technology-sector premium. That's the M&A equivalent of buying retail and selling wholesale, in reverse.

Emkan Finance — incubating a lender inside the lender. The second move was internal rather than acquired. In 2018, Al Rajhi founded إمكان للتمويل Emkan Finance, a digital microfinance and SME lender, and capitalized it heavily — a capital base on the order of SAR 2 billion.17 The temptation is to file this under "small experimental side project." That would be a mistake. Emkan is a serious financial business in its own right: in 2024 it generated net profit of about SAR 887 million — roughly $236 million.18 That is a quarter-billion dollars of annual profit from a subsidiary that didn't exist a decade ago. Emkan's model — small-ticket consumer loans, credit cards, and SME financing delivered digitally — reaches a segment the mortgage-and-deposits core doesn't fully serve, and it does so at attractive margins. Al Rajhi has now appointed Morgan Stanley, alongside Al Rajhi Capital, to lead an IPO of Emkan, joining a wave of Saudi fintechs racing to list and aiming to crystallize the embedded value for shareholders.18

Neoleap and urpay — owning the payment rails. Payments are the connective tissue of any modern financial ecosystem, and Al Rajhi chose to own that tissue rather than rent it. Launched internally in 2021, نيوليب Neoleap became the bank's payments-fintech arm, spanning merchant acquiring, payment gateways, and the consumer-facing urpay digital wallet. The scale it has reached in just a few years is the tell: by the end of 2024, Neoleap commanded roughly a 25% share of managed point-of-sale terminals in the Kingdom and about a 17% share of the payment-gateway market, processing well over 146 million transactions, with urpay positioned as one of the region's fastest-growing pay-tech offerings.19 Owning the payment layer does two things at once — it captures fee economics that would otherwise leak to outside processors, and it keeps customers transacting inside the Al Rajhi ecosystem rather than on someone else's rails.

Drahim — the seed-to-scale open-banking play. The final piece is the smallest in dollars but arguably the most forward-looking. In June 2024, Al Rajhi acquired a 65% stake in دراهم Drahim — a Saudi open-banking and personal-finance fintech, notable as the first Saudi startup to pass through Y Combinator — for a cash consideration of SAR 83.4 million, roughly $22.2 million.2021 It was billed as the first acquisition of a local open-banking fintech by a major Saudi bank, and the strategic logic is elegant: Drahim's technology embeds budgeting, automated savings, and robo-advisory directly into the core app, deepening engagement and giving Al Rajhi a homegrown foothold in open banking just as that framework reshapes the Saudi financial landscape. Drahim's registered user base grew more than 250% in the year of the deal.21

Step back and the pattern is unmistakable. Al Rajhi isn't just a bank that uses technology; it's becoming a holding company of financial-technology businesses — software, microfinance, payments, open banking — each built or bought cheaply, scaled inside the protective shell of the bank's brand and balance sheet, and then teed up for the public markets at multiples the bank itself doesn't command. But all of this — the fintech empire, the mortgage dominance, the digital super-app — rests on one unglamorous foundation that we've been circling the entire episode. It's time to talk about where the money actually comes from.

VII. The Core Engine: The "CASA War" and the SNB Rivalry

Strip away the apps and the IPOs and the gigaproject headlines, and a bank is fundamentally a spread business: it gathers money cheaply and deploys it profitably, and the gap between the two is the whole game. Al Rajhi's supremacy comes down to the cheaply half of that sentence, and it traces directly back to that dirt sidewalk and the refusal to deal in riba. Here is the punchline of the entire business, the thing that makes the 22.9% ROE possible: a huge share of Al Rajhi's funding costs essentially nothing.

The technical term is CASA — current and savings accounts, the everyday checking-style money that customers park at the bank for convenience rather than yield. More than two-thirds of Al Rajhi's deposit base of roughly SAR 679 billion sits in non-profit-bearing accounts — money on which the bank pays its depositors precisely nothing.2 And this is where Shariah compliance flips from constraint to superpower. Because devout retail depositors are not chasing a profit rate in the first place — they value Shariah-compliant custody and app convenience far above yield — Al Rajhi can hold an enormous pile of deposits at a cost of funds that rounds to zero. A conventional bank competing on interest has to keep raising the rate it pays to hold onto deposits. Al Rajhi's customers stay for trust and convenience, not for a quarter-point of extra return. Its money is sticky and free.

Now watch what that does when the macro environment turns. Between 2022 and 2025, central banks worldwide — and SAMA, the Saudi central bank, with them — pushed benchmark rates sharply higher. For a normal bank, rising rates are a double-edged sword: you can charge more on loans, but you also have to pay more on deposits, and the two largely offset. For Al Rajhi, with the bulk of its funding paying nothing regardless of where rates go, higher rates flowed much more cleanly into the income line. Its net interest margin — the spread between what it earns on financing and what it pays for funding — expanded dramatically relative to international peers who were busy handing their gains back to depositors. The zero-cost deposit base isn't just an efficiency story; it's a structural advantage that widens exactly when rates rise. That, more than anything, is why the bank's profitability has looked almost too good to be true in recent years.

This brings us to the rivalry that defines the top of the Saudi banking league table: Al Rajhi versus البنك الأهلي السعودي Saudi National Bank, or SNB. The two banks are studies in contrast. SNB — itself the product of the 2021 merger that created the Kingdom's "national champion" — is the corporate and institutional heavyweight, the balance sheet behind the massive Vision 2030 gigaprojects, the lender of choice for the state and big business. By total assets it remains the largest bank in the Kingdom, in the vicinity of SAR 1.2 trillion against Al Rajhi's roughly SAR 1.05 trillion.1 On the scoreboard of size, SNB wins.

But size and quality are not the same thing, and on quality the gap runs the other way — emphatically. Al Rajhi has now overtaken SNB on the metric that maps most directly to its retail-funding moat: total customer deposits, where Al Rajhi's roughly SAR 679 billion edged ahead of SNB's base.2 More striking is the efficiency and return comparison. Al Rajhi's 22.9% ROE and 23.3% cost-to-income ratio tower over SNB, whose return on equity sat around 12–14% with a cost-to-income ratio in the high-20s percent in early 2026.22 Read those side by side and the lesson is stark: SNB is the bigger ship, but Al Rajhi is the better business. The reason is exactly the CASA engine — SNB, with its heavier corporate and institutional funding mix, simply cannot match a deposit base where two-thirds of the money is free. The retail-focused, low-cost, Shariah-anchored deposit machine is structurally a superior model for generating returns on capital, and the numbers prove it quarter after quarter. The question for an investor, then, becomes: who is steering this machine, and are their incentives pointed the same direction as mine?

VIII. Current Management: Alignment & Skin in the Game

We're going to skip past the long parade of historical executives, because the only team that matters for an investment decision today is the one running the bank right now. And the structure at the top of Al Rajhi tells a deliberate story about how the institution bridges its family-founded past and its professionally managed present.

At the top of the board sits the chairman, عبدالله بن سليمان الراجحي Abdullah bin Sulaiman Al-Rajhi — a member of the founding family and, crucially, a man who actually ran the bank. Before moving to the chairmanship in 2014, he served as chief executive and managing director for over three and a half decades, making him the living bridge between the old exchange-house culture and the modern, governance-driven corporate institution.23 This is not a ceremonial figurehead parachuted in for the family name; this is someone who spent a career building the machine he now oversees. And his interests are welded to the share price. Al-Rajhi holds a direct stake reported at roughly 2.18% of the bank — on the order of 130 million-plus shares, a position worth well over SAR 10 billion, or north of $2.7 billion.24 When the chairman's personal fortune rises and falls in lockstep with the smallest minority shareholder's, the alignment problem that plagues so many large institutions largely takes care of itself. He doesn't need an incentive plan to care about the stock; a meaningful chunk of his net worth is the stock.

The day-to-day architect is the managing director and CEO, وليد بن عبدالله المقبل Waleed bin Abdullah Al-Mogbel — and his résumé is the mirror image of the chairman's. Where Abdullah Al-Rajhi represents family and legacy, Al-Mogbel represents the professional-manager era. He joined the bank in 2007, rose through the most demanding seats in the building as chief financial officer and then deputy CEO, and took the top job at the start of 2020 — which is to say, he was handed the controls right as the "Bank of the Future" transformation and the fintech build-out kicked into high gear.25 He is, in a very real sense, the master architect of the modern Al Rajhi: the digital super-app, the subsidiary IPO pipeline, the efficiency obsession that keeps the cost-to-income ratio near the global frontier all bear his fingerprints. A career CFO running a bank tends to produce exactly what Al Rajhi exhibits — relentless cost discipline and capital-allocation rigor.

Now, a fair second-layer diligence flag on incentives. Al-Mogbel's direct shareholding is listed at essentially 0.00%, which to an outside investor can look like a misalignment red flag. In the Gulf context, though, this is typical for non-family professional executives, and it doesn't mean his pay is divorced from performance. His compensation is heavily weighted toward the bank's results through an active employee share scheme and a performance-linked long-term incentive plan, the standard modern toolkit for tying an executive's reward to total shareholder return rather than a flat salary. The structure to watch — as always with LTIPs — is whether the performance hurdles are genuinely demanding, but the direction of travel is clearly toward pay-for-performance.

Around this leadership sits a base of institutional stewardship that reinforces the strategy rather than fighting it. The single largest institutional holder is the المؤسسة العامة للتأمينات الاجتماعية General Organization for Social Insurance — GOSI, the Kingdom's social-insurance fund — with a stake of roughly 9.6%, a quasi-sovereign anchor whose presence signals state confidence in the franchise.26 Alongside it sit the global index and active giants — the likes of BlackRock and Vanguard holding low-single-digit percentages each — whose ownership reflects Al Rajhi's heavy weight in emerging-market and Saudi indices and a broad institutional endorsement of the digital, retail-led strategy. The cap table, in short, pairs aligned insiders, a sovereign anchor, and global institutions — a configuration that tends to keep a management team honest and long-term oriented. With the people and incentives mapped, we can finally run the whole business through the strategic frameworks and stress-test the bull and bear cases.

IX. Strategic Playbook: Powers, Forces, & Investing Lessons

Let's put Al Rajhi on the operating table and dissect it with the two frameworks every serious business analyst reaches for: Hamilton Helmer's 7 Powers and Michael Porter's Five Forces. The goal isn't to collect buzzwords — it's to figure out which of Al Rajhi's advantages are durable and which could erode.

Hamilton Helmer's 7 Powers. Three of the seven powers map onto Al Rajhi with unusual clarity. The first and most distinctive is Cornered Resource — Shariah-compliant brand equity. The "Al Rajhi" name in Saudi Arabia is not a brand in the ordinary marketing sense; it's a generational stamp of religious legitimacy that no competitor can manufacture, because it was earned over eighty years starting on that sidewalk and cannot be bought, replicated, or out-advertised. When a devout Saudi family chooses where to bank, Al Rajhi starts the race already at the finish line. That is a cornered resource in the truest sense — a unique asset that confers a persistent cost-of-acquisition advantage. The second power is Switching Costs, embodied most concretely in the salary-transfer account. When a Saudi citizen routes their monthly salary directly into an Al Rajhi account — and millions do — the friction of unwinding that arrangement, re-pointing direct debits, moving the mortgage, and re-onboarding elsewhere is enormous relative to any benefit. The customer is locked in not by a contract but by inertia and integration, the stickiest lock of all. The third power is Scale Economies: Al Rajhi spreads the fixed cost of its technology stack — Ejada's software development, Neoleap's payment infrastructure, the super-app's engineering — across a base of more than 20 million customers, driving the per-transaction cost down to a level smaller competitors simply cannot reach. The 23.3% cost-to-income ratio is scale economics made visible. (One could argue Counter-Positioning too — a conventional bank literally cannot copy the zero-interest deposit model without abandoning its own economics — but the three above are the load-bearing ones.)

Porter's Five Forces. The framework that explains why the profits persist. Start with the Bargaining Power of Buyers, meaning depositors — and here it's extraordinarily low. Retail depositors who value Shariah compliance and app convenience over yield have almost no leverage to demand a better rate, because rate was never why they came. That's precisely what lets the bank hold two-thirds of its funding at zero cost. The Threat of New Entrants is similarly low: a would-be competitor faces strict licensing from SAMA — ساما, the Saudi Central Bank — daunting capital requirements, and the near-impossible task of replicating eight decades of accumulated trust. Rivalry, as we saw, exists chiefly with SNB and the other large banks, but it's a rivalry of differentiated models rather than a price war, which keeps margins intact. The Threat of Substitutes is the most interesting force to watch — and it's where the bear case lives — because digital-only challengers like STC Bank and D360 represent a new substitute for the everyday-banking relationship. The Bargaining Power of Suppliers (in banking, largely depositors and capital markets) is muted by the same dynamics that crush buyer power. Four of the five forces point firmly in Al Rajhi's favor; only the substitute threat is genuinely live.

The myth versus reality check. The consensus narrative on Al Rajhi is "sleepy, faith-based mortgage bank riding a religious moat." The reality, as this episode has argued, is closer to "the most efficient digital retail bank in its region, using a religious moat to fund a fintech holding company at near-zero cost." The moat is real, but it is not passive — management has spent the moat's surplus building digital infrastructure rather than resting on it. That's the distinction the consensus misses.

The bull case. The optimist sees several engines still in early innings. Al Rajhi is pushing aggressively and successfully into corporate and SME lending, taking share from SNB on its home turf rather than staying boxed into retail. The tech-asset monetization story — the Ejada and Emkan IPOs — could surface billions in value that the market currently buries inside a bank multiple, and re-rate the whole sum-of-the-parts. And the core retail-deposit dominance, the CASA moat, shows no sign of cracking. A bank compounding equity at north of 20% while sitting on free funding and optionality on multiple fintech spin-offs is a rare animal.

The bear case. The skeptic has three legitimate worries, and they deserve airtime rather than dismissal. First, margin compression: the same zero-cost deposit base that turbocharges profits when rates rise works in reverse when SAMA cuts. If rates fall rapidly, Al Rajhi's net interest margin — having expanded so dramatically on the way up — gives some of that windfall back, and the recent guidance debates around margin direction are a live reminder that this is the dominant swing factor. Second, digital competition: the substitute threat from STC Bank, D360, and other digital-only entrants is exactly the kind of force that erodes everyday-banking relationships at the margin, even if it can't easily dislodge the salary account. Third, real estate sensitivity: a bank writing four in ten of the Kingdom's mortgages is, by definition, heavily exposed to Saudi housing. A property slowdown — whether from oil-driven fiscal pressure, oversupply, or cooling subsidies — would slow the mortgage flywheel that drove so much of the recent growth, and concentrate credit risk in a single asset class.

The KPIs that actually matter. Forget the dozens of metrics in the earnings deck. For this specific business, three numbers tell you almost everything about whether the thesis is intact. One: the CASA, or non-profit-bearing deposit, percentage — the lifeblood of the cheap-funding moat; watch for it to hold above roughly 65%, and treat any sustained slippage as the single most important warning sign. Two: the cost-to-income ratio — the proof of the scale-and-digital efficiency story; as long as it stays below about 25%, the operating model is working as designed. Three: retail mortgage market share — the gauge of dominance in the core growth engine; holding above 40% means the Vision 2030 land grab is being defended. Track those three and you're tracking the real Al Rajhi, no spreadsheet gymnastics required. (As a fourth, watch the progress of the Ejada and Emkan listings — not as an ongoing operating metric, but as discrete catalysts that could re-rate the stock when value is crystallized.)

X. Epilogue & Outro

From four brothers displaying foreign coins on a dirt sidewalk in 1940s Riyadh to a digital institution processing billions of transactions in the cloud and floating fintech subsidiaries at tech-sector valuations — Al Rajhi is one of the most remarkable stories of trust-scaling in the whole of global corporate history. The throughline never changes. The asset the brothers accumulated on that sidewalk was never really currency; it was amana, the confidence of a people that their money was being handled honestly and in accordance with their faith. Everything since — the 1988 conversion, the diminishing-musharakah mortgage engine, the Vision 2030 land grab, the Bank of the Future super-app, the Ejada and Emkan and Neoleap and Drahim build-out — is that original trust, compounded, re-invested, and operationalized at national scale.

The ultimate lesson for an investor is one that travels far beyond Saudi banking. Al Rajhi did not win by importing a Western financial model and running it slightly better. It won by understanding its own cultural context so deeply that it turned the one thing a foreign competitor could never replicate — generational religious trust — into a permanent, compounding financial moat, and then layered modern technology on top to widen it. The deposit base costs nothing because the customers came for faith and convenience, not yield. The mortgage book dominates because the family name carries Shariah legitimacy no marble lobby can buy. The fintech subsidiaries scale cheaply because they grow inside a brand that a nation already trusts. Strip out the cultural insight and none of the financial superlatives are possible. That is the deepest moat of all — and the hardest one for any competitor, foreign or domestic, to ever cross.

References

-

Al Rajhi Bank Q1 2026 slides: double-digit growth, guidance raised — Investing.com, 2026-04-22 ↩↩

-

Alrajhi Bank Reports 14% Growth in Net Income, Reaching 6,752 Million Riyals in Q1 2026 — Al Rajhi Bank, 2026-04-22 ↩↩↩

-

Al Rajhi Bank posts 26% profit growth, driven by diversification and lending shift — The Asian Banker, 2026 ↩↩↩

-

Saudi bank's IPO brings financial redemption after religious controversy — The Conversation ↩

-

Al Rajhi Bank (1120) Company Profile — Saudi Exchange (Tadawul) ↩

-

Mortgage Market in Saudi Arabia: Overview and Trends — Arab MLS ↩

-

PIF-owned SRC buys $799m mortgage portfolio from Al Rajhi Bank — Arab News ↩

-

alrajhi bank and Saudi Real Estate Refinance Company (SRC) Sign SAR 10 Billion Real Estate Refinance Portfolios Agreements — Al Rajhi Bank, 2025 ↩

-

SRC buys 2 mortgage portfolios worth SAR 10B from Al Rajhi Bank — Argaam ↩

-

Al Rajhi Bank in 2024 | ejada systems (revenue growth and backlog) — Al Rajhi Bank ↩

-

Al Rajhi Bank's Ejada Systems mulls IPO in Saudi market — Argaam ↩

-

Saudi Tech Firm Ejada Taps Goldman for IPO at $1.5 Billion Value — Bloomberg Law ↩

-

Fintechs Look to Join Saudi Listing Boom Amid Growing Demand — Bloomberg, 2025-07-04 ↩↩

-

Embracing Innovation and Legislation: alrajhi bank's Strategic Acquisition of Drahim App — Al Rajhi Bank, 2024 ↩

-

Mr. Abdullah bin Sulaiman Al Rajhi — Al Rajhi Bank Board of Directors ↩

-

Abdullah Al-Rajhi: Positions, Relations and Network — MarketScreener ↩

-

Mr. Waleed Abdullah Al-Mogbel — Al Rajhi Bank Executive Management ↩

-

Al Rajhi Banking and Investment Corporation: Shareholders and Shareholding Structure — MarketScreener ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube