KB Financial Group: The Dual-Engine Giant of Korea and the Value-Up Revolution

I. Introduction & Episode Roadmap

Start with the central hook, because everything else flows from it. How does a company earn record profits, hold rock-solid capital, and still trade at a third of its book value? The short answer is that for most of its history, KB Financial—like the entire Korean banking sector—was rewarded by the system for the wrong things. It was rewarded for growing loans, for hoarding capital, for being large and safe and boring. It was not rewarded for returning cash to the people who owned it. The market, watching decades of capital pile up inside these institutions and never come back out, priced the shares accordingly.

The investment spine of this story is therefore the 코리아 디스카운트 Korea Discount—the persistent, structural gap between what Korean companies earn and what their equity is worth to shareholders.8 KB sits at the very center of that debate for a simple reason: it is arguably the best-run and most profitable banking franchise in the country, which makes it the cleanest test case for whether the discount is a fact of Korean nature or simply a fixable failure of capital allocation.

To get there, this article traces six arcs. First, the post-crisis genesis: how a state-orchestrated mega-merger in 2001 created the largest retail bank in Korean history. Second, the "Dual-Engine" transformation of the 2010s, when KB spent trillions of won buying its way into insurance and securities to escape the ceiling on pure banking. Third, the systemic distribution shock of the Hong Kong equity-linked securities crisis, which detonated in 2024 and exposed the dark side of KB's greatest asset—its enormous retail branch network. Fourth, the mechanics of the Value-Up program and the CET1 capital-return framework that has re-rated the stock. Fifth, the competitive war against both legacy rivals and a new generation of fintech-native banks. And finally, the playbook and the honest bull-versus-bear case for a long-term owner.

One more framing device is worth planting at the outset, because it recurs throughout the story: the difference between being big and being valuable. KB has never had trouble being big. It was engineered to be big; the whole point of the crisis-era consolidation was to build an institution too large to fail. Bigness gave it a genuine moat, but bigness also seduced it—into growing loans that consumed capital without earning it, into hoarding equity that the market refused to reward, and into pushing product through a branch network optimized for volume. The entire Value-Up era can be read as KB, under external pressure, finally being forced to ask a question it had avoided for two decades: not "how do we get bigger?" but "how do we get more valuable to the people who own us?" That is the through-line.

A note on posture before we begin. KB tells a compelling story about itself, and much of it is true. But this is not a shareholder letter. Where management claims it has changed, we ask what evidence supports the claim and what would prove it false. The interesting thing about KB in 2026 is that, for once, there is real evidence to weigh—and a live CEO succession contest that will test whether the reforms outlast the man who championed them.

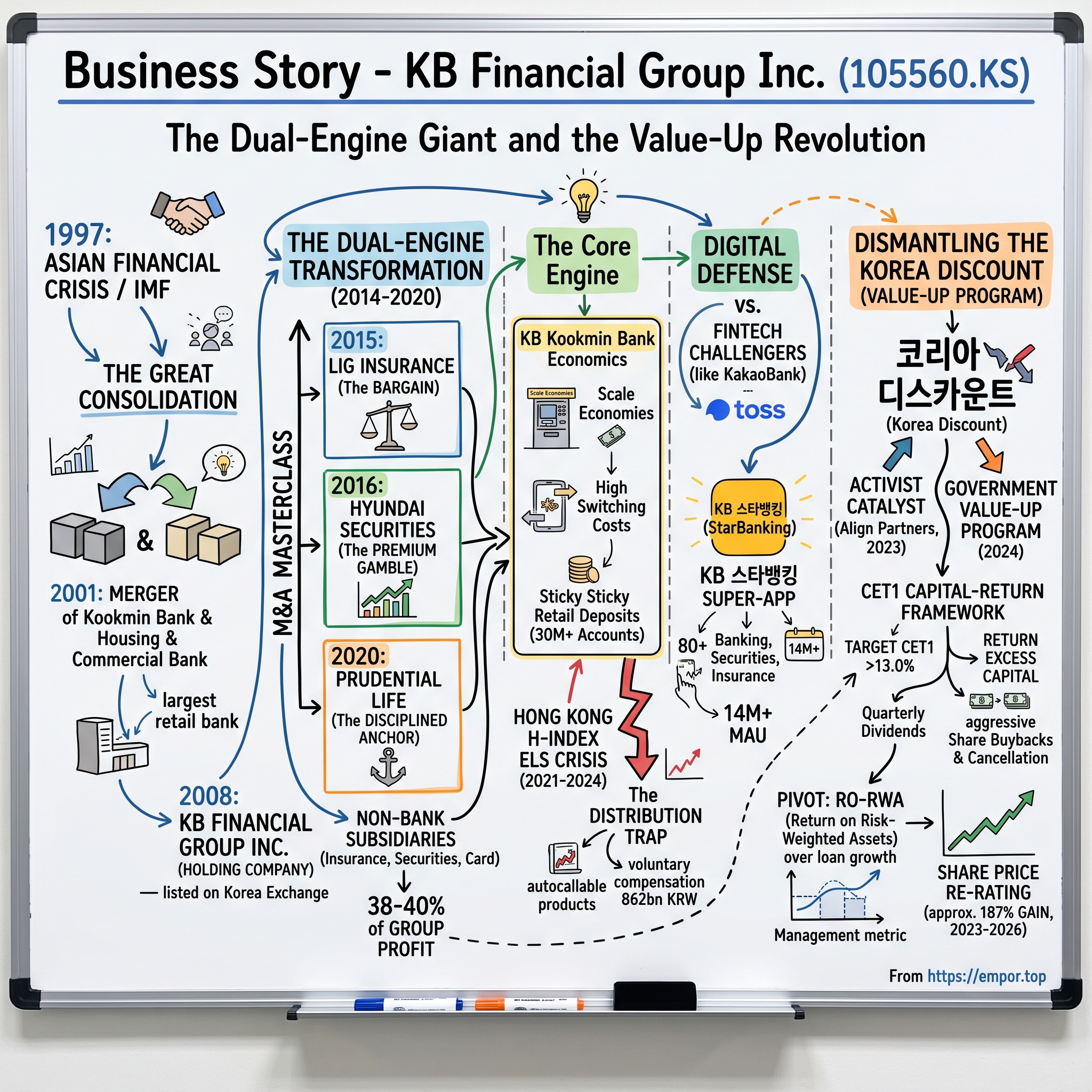

II. The Asian Financial Crisis & The Great Consolidation (1997–2008)

To understand why Korean banks were built to grow rather than to profit, you have to go back to the autumn of 1997, when the entire model nearly collapsed.

For three decades, South Korea had run one of the most spectacular development stories in economic history, and its banks were the plumbing. Their job was not to allocate capital efficiently or to reward shareholders; their job was to channel cheap credit into the 재벌 chaebol—the sprawling family conglomerates like Hyundai, Samsung, and Daewoo—at the direction of the state. Banks were instruments of industrial policy first and businesses second. Loan officers did not ask hard questions about return on capital, because that was not what the system was for.

Then the debt came due. In 1997, a regional currency contagion swept out of Southeast Asia and hit Korea's over-leveraged corporate sector like a wrecking ball. Chaebol that had borrowed at debt-to-equity ratios of four, five, and six to one began to default in a cascade. The banks that had funded them were suddenly staring at mountains of non-performing loans, and the country had to accept a humiliating $58 billion bailout from the International Monetary Fund. To this day, older Koreans refer to the episode not as the Asian Financial Crisis but simply as "the IMF"—shorthand for a period of forced restructuring, mass layoffs, and national trauma.

A merger of two monopolies

Out of that wreckage came consolidation, much of it engineered by a government determined to build banks large enough to survive the next shock. The centerpiece was the 2001 union of two state-entrenched institutions with almost mirror-image franchises. On one side stood 국민은행 Kookmin Bank, founded in 1963 as Citizens National Bank to serve retail savers and small businesses—the everyday deposit bank of the Korean household. On the other stood 주택은행 Housing & Commercial Bank, founded in 1967 and for decades the national monopoly on housing finance, the institution through which Koreans saved for and borrowed against their homes.1

The two signed their merger agreement in April 2001 and completed it that November, dissolving both entities to create a new Kookmin Bank that listed on both the Korean and New York exchanges.1 It was billed as a merger of equals, though Kookmin was clearly the larger partner. The combination was staggering in scope: it captured the retail deposit relationship of more than half the country's population and instantly became the biggest bank Korea had ever seen.

The scale came at a cost, and it is worth dwelling on because it reveals the DNA of the institution. Merging two former monopolies is not like merging two competitors; it is like fusing two bureaucracies that each believed they were the natural center of the universe. Branch networks overlapped street by street. Two proud corporate cultures, two entrenched labor unions, and two sets of managers who had spent their careers as rivals were suddenly forced under one roof. The integration was contentious, and the friction over redundant branches and headcount would echo for years. What the merger produced was not a lean machine but a giant—one whose competitive advantage was raw ubiquity rather than efficiency.

That distinction—ubiquity over efficiency—is not a historical footnote; it is the defining trait that explains both the best and the worst of KB across the next quarter-century. The sheer size of the deposit base and branch footprint became a genuine, durable moat, as later sections will show. But a sprawling, sales-oriented branch network staffed by tens of thousands of employees under constant pressure to justify their existence is also an organization perpetually tempted to push whatever product generates the most fee income this quarter. The same institutional DNA that made KB unbeatable in gathering deposits would, two decades later, make it the largest seller of a toxic structured product to its most vulnerable customers. Origins matter, and KB's origin as a bolted-together giant of overlapping monopolies is written into everything it has done since.

From bank to holding company

The second foundational move came in 2008. Korean banking regulation drew a tight box around what a bank could own and how it could deploy capital, and KB's leadership wanted out of that box. At an extraordinary shareholders' meeting in August 2008, Kookmin's owners approved a reorganization that placed the bank under a new parent, KB금융지주 KB Financial Group Inc., listed on the 한국거래소 Korea Exchange under the ticker 105560.2

The logic of a holding company is easy to state and hard to execute. A pure bank is capped—by regulation, by a mature domestic market, and by the political reality that a retail bank in Korea can never fully control its own interest rates without inviting "moral suasion" from the authorities. A financial holding company, by contrast, can own a bank, an insurer, a brokerage, a card company, and an asset manager, and can move capital among them. In principle, it can build a diversified earnings stream that no single regulator or interest-rate cycle can strangle. In 2008, that was still a PowerPoint aspiration. KB had the holding-company structure but not much to hold beyond the bank itself. Filling that structure with real non-banking businesses would become the defining project of the next decade—and the making of the men who would eventually run the group.

III. The Dual-Engine Transformation: Non-Bank M&A Masterclass (2014–2020)

By the mid-2010s, the strategic problem facing KB was no longer survival. It was stagnation. The domestic banking market was saturated, credit growth was capped by regulators wary of household debt, and net interest margins—the spread between what a bank earns on loans and pays on deposits—were structurally thin. A bank that could only lend was a bank that could only grow as fast as Korea's slowing economy would allow. Worse, KB had just endured a bruising governance scandal—a public feud between its previous chairman and its bank CEO that had paralyzed the group and embarrassed it in front of regulators. The company needed both a reset and a strategy.

The architect of the reset was chairman 윤종규 Yoon Jong-kyoo, and his backstory matters because it shaped everything that followed. Yoon was not a career banker groomed in the executive suite; he was an accountant, a man who had passed Korea's grueling certified public accountant exam and spent years reading balance sheets rather than glad-handing chaebol chairmen. He had even been forced out of KB once, earlier in his career, before returning to take the top job in 2014. An accountant's temperament—suspicious of round numbers, allergic to overpaying, obsessed with what a business actually earns rather than what it claims—is an unusual and, as it turned out, extremely useful trait in a man about to spend trillions of won on acquisitions. Yoon set about turning a bank into a group, and he did it with a spreadsheet in hand.

What followed was one of the more instructive M&A sequences in Asian finance—instructive precisely because it was a mix of a bargain, a gamble, and a discipline test, and because the executive who negotiated the first deal, 양종희 Yang Jong-hee, would ride that record all the way to the chairmanship. Together, Yoon and Yang formed the partnership that would define KB's second act: the accountant who set the discipline, and the strategist who executed the deals.

Case study one: LIG Insurance, the bargain

The first big move came in 2015 with the acquisition of LIG손해보험 LIG Insurance, then the country's fourth-largest non-life insurer. KB paid roughly ₩645 billion for an initial 19.47% controlling stake, later topping up its holding.3 The negotiation is the part worth remembering. Yang, then KB's chief strategist, is credited with driving a hard bargain by digging into the target's books and surfacing hidden losses buried in LIG's overseas branch operations, using them as leverage to extract a price concession before signing.

Why does that detail matter for an investor? Because it is the opposite of how most trophy acquisitions get done. The empire-building instinct—the one that destroys shareholder value across every market on earth—is to fall in love with a target, wave away the ugly bits in due diligence, and pay up to win. KB did the reverse: it treated diligence as a weapon and demanded the price move to reflect what it found. Rebranded as KB손해보험 KB Insurance, the business became a genuine second engine. In 2024 it earned ₩839.5 billion in net income, up nearly 18% year on year, making it one of the group's most valuable non-banking franchises.4 Measured against the sub-₩650 billion entry price a decade earlier, the deal looks less like an acquisition and more like a coupon that keeps paying.

Case study two: Hyundai Securities, the premium gamble

The 2016 acquisition of 현대증권 Hyundai Securities was the mirror image—a deal KB won by paying up. KB acquired a controlling stake of around 22.5% for roughly ₩1.25 trillion, a price that industry observers considered a substantial premium to where independent analysts pegged the stake's fair value. The reason was competitive: Korea Investment Holdings was also circling, and in a contested auction for a scarce asset, KB chose to overpay in the short term rather than lose the franchise entirely.

Did they overpay? On the day, almost certainly. Over time, the verdict is more favorable. Merged with KB's small existing brokerage, Hyundai Securities formed KB증권 KB Securities, which vaulted the group into the top tier of Korean investment banking and wealth management. The strategic payoff showed up vividly in the numbers years later: in 2024, KB Securities was the group's fastest-growing major subsidiary, with net income surging more than 50% to ₩585.7 billion as capital-markets activity recovered.4 The lesson is not that overpaying is fine—it is that the quality and strategic fit of an asset can, over a long enough horizon, redeem a rich entry price, provided the buyer actually integrates and grows it rather than letting it rot.

Case study three: Prudential Life, the disciplined anchor

The third deal arrived at the worst possible moment for confidence and the best possible moment for a buyer with cash. In the depths of the COVID-19 panic in 2020, KB agreed to acquire 100% of 푸르덴셜생명 Prudential Life Insurance of Korea from its U.S. parent for roughly ₩2.3 trillion, closing the transaction on the last day of August that year.[^4] The seller was a well-capitalized American insurer looking to exit; the buyer was a Korean group with the balance sheet to move while others froze.

Two things stand out. First, life insurance is a fundamentally different animal from non-life: it is a long-duration, capital-intensive business highly sensitive to interest rates, and paying a disciplined multiple for a well-reserved book matters enormously. Second, KB bought in a crisis, which is when the best prices are usually available and the fewest buyers are willing to act. Prudential was later folded together with KB's existing life operations to form KB라이프생명 KB Life Insurance in 2023, completing the group's transformation into a full-spectrum financial house.

What the sequence proves

Step back and the three deals tell a coherent story. By stringing together a bargain, a contested premium, and a counter-cyclical anchor, KB pushed its non-banking subsidiaries to something on the order of 38% to 40% of group profit—the highest non-bank contribution among Korea's big financial groups. In 2024, with the bank's share of group earnings falling to 60% from 67% a year earlier, the diversification was not a slogan; it was measurable in the profit mix.4 The "Dual-Engine" model gave KB a hedge that a pure bank simply does not have: when interest rates fall and lending slows, brokerage fees and insurance underwriting can pick up the slack.

A skeptic should register the counter-argument, because acquisitive diversification has a shadow name: diworsification, Peter Lynch's term for the value destroyed when companies buy their way into businesses they do not understand. Plenty of banks around the world have assembled financial supermarkets that promised synergies and delivered complexity, conglomerate discounts, and management distraction. What separates KB's version from the cautionary tales is, so far, the evidence in the numbers: the acquired businesses are individually profitable and growing, the group earns a respectable return on the capital tied up in them, and the diversification demonstrably cushioned the ELS shock rather than compounding it. That verdict is provisional—diworsification often reveals itself only in a downturn, when the acquired businesses turn out to share hidden risks with the core—but on the record to date, KB's dual engine looks like genuine diversification rather than empire-building dressed up as strategy.

But diversification is a double-edged strategy, and the same sprawling retail machine that made KB a distribution powerhouse was about to become the source of its worst self-inflicted wound. The bank that could sell anything to anyone was about to sell the wrong thing to exactly the wrong people.

IV. The Hong Kong H-Index ELS Crisis: The Distribution Trap (2021–2024)

Picture an elderly saver walking into a KB Kookmin Bank branch in 2021. She has spent her life accumulating a nest egg in term deposits, and the interest rate on those deposits is close to nothing. A helpful relationship manager offers an alternative: a structured product paying 5% or 6%, with reassuring language about how her principal is safe unless some far-off index falls by half. She trusts the bank—it is the largest and most respected in the country. She signs. Three years later, that decision has vaporized a large chunk of her savings, and the bank is holding an emergency press conference.

This is the anatomy of the 홍콩 H지수 주가연계증권 Hong Kong H-Index Equity-Linked Securities (ELS) crisis, and it is the most important governance story in KB's recent history.

The product, in plain language

An autocallable ELS is a bet dressed up as a savings product. The saver hands over cash and, in exchange, earns an above-market coupon so long as an underlying index—here the Hang Seng China Enterprises Index, a gauge of major Chinese companies listed in Hong Kong—stays above a "knock-in" barrier, typically 50% to 65% of its starting level. If the index holds, the product "auto-calls," returns principal plus the coupon, and everyone is happy. If the index breaches the barrier and stays there at maturity, the saver eats the losses, which can run to half the principal or more. The yield is not free money; it is the premium for having quietly sold a put option on Chinese equities. Most buyers had no idea that was the trade they were making.

Critically, KB Kookmin Bank sold products with a knock-in feature—the riskier variety—where several rival banks stuck to gentler "no-knock-in" structures.9 And it sold them at enormous scale. When the reckoning came, KB Kookmin was the single largest distributor in the country, with roughly ₩8 trillion of these products outstanding.9 These were sold in 2021, when the Chinese index was near its peak and the "no-loss" story felt plausible.

Why would the country's most trusted bank become the biggest seller of the riskiest version of a complex derivative to its most conservative customers? The answer is the dark logic of the distribution machine. In a zero-interest-rate world, retail savers were desperate for yield, and a branch network under pressure to generate fee income had every reason to offer it. The internal incentive structure did the rest. Branch employees were measured and rewarded, in large part, on how much product they moved. A relationship manager who sold more ELS scored better on their KPIs, earned a better evaluation, and advanced faster. Nobody in that chain was rewarded for telling a 72-year-old depositor that the safe-sounding 6% product was actually a leveraged bet on Chinese equities she did not understand. The system optimized for volume, and it got exactly the volume it optimized for—until the index broke.

The meltdown

Then Chinese equities collapsed. The Hang Seng China Enterprises Index fell by more than half from its early-2021 highs, and the knock-in barriers that had seemed so remote were breached en masse. Products written in 2021 began maturing in early 2024 directly into that crater, converting paper risk into realized losses for tens of thousands of ordinary savers.10 Korea's financial watchdog investigated and concluded that banks had misrepresented risky, China-linked notes to customers, including retirees who had no business being in the product at all.13

The bill

The financial and reputational toll was severe, and here KB's response is genuinely revealing of management. Rather than litigate for years against its own elderly customers—a legally defensible but reputationally catastrophic path—KB opted for proactive 자율배상, or voluntary compensation. KB Financial set aside roughly ₩862 billion in provisions to cover the redress, the largest reserve among the Korean banks caught in the scandal.12 Compensation offers to affected investors ranged from around 40% to 80% of losses depending on each customer's circumstances and the bank's sales conduct, and by 2025 the great majority of investors had been reimbursed.911 On top of the customer redress came the regulatory hangover: the Financial Supervisory Service pursued penalties against Kookmin Bank running into the hundreds of billions of won, and enforcement actions tied to the affair continued to surface into late 2025.14

You can see the damage directly in the results. KB Kookmin Bank's 2024 net profit actually slipped 0.3% to ₩3.25 trillion, and management attributed the weakness squarely to the large provision booked in the first quarter for the ELS crisis.4 The group as a whole still hit record profit that year—proof of the dual-engine cushion—but the bank, the crown jewel, took the hit.

The course correction, and the honest question

Under chairman Yang Jong-hee, who had inherited the crisis only weeks into his tenure, KB overhauled its wealth-management compliance: it curtailed the sale of high-risk derivative products through ordinary retail branches and began shifting employee incentives away from raw transaction volume, which was the rotten core of the problem. The KPIs had rewarded branch staff for pushing product, and staff pushed product.

There is a cold commercial logic to KB's generosity that is worth naming, because it complicates the flattering narrative. Paying out hundreds of billions of won in "voluntary" compensation is expensive, but the alternative—years of litigation against elderly customers, splashed across the evening news, while regulators and politicians pilloried the bank—would have been far more expensive in the currency that matters most to a deposit franchise: trust. KB's entire moat rests on being the institution Koreans reflexively trust with their savings. A protracted, ugly fight would have corroded that trust at the exact moment KB was asking those same customers to keep their money and use its super-app. Seen that way, the compensation was not pure altruism; it was a rational, and probably correct, investment in preserving the franchise. Good behavior and good business happened to align.

Here is where an independent lens matters most. Management now frames the episode as a one-off it has fixed, and the compensation was, by the standards of the industry, handled quickly and generously. But the honest analytical point is that the ELS crisis was not a freak accident; it was the predictable output of KB's core business model, in which an enormous, sales-driven branch network is under constant pressure to generate fee income from a captive base of trusting depositors. The same distribution machine that is KB's moat is also its most dangerous liability. Whether the compliance overhaul truly changes the incentives, or merely relabels them until the next yield-hungry product cycle, is a question no press release can answer—only time and the next bull market can. An activist stress-tester would put it sharply: KB has now demonstrated, twice in a generation counting earlier fund mis-selling episodes across the sector, that its branch conduct is a recurring liability, and it should be watched as a permanent feature of the investment case rather than a resolved incident. That tension between the branch network as asset and as hazard runs straight into the next section, because that network is the heart of the bank's economics.

V. The Core Engine: KB Kookmin Bank's Economics and Digital Defense

For all the talk of diversification, the truth is that KB is still, at its core, a deposit machine. Understanding why that machine is so valuable—and why a new generation of competitors has been trying to dismantle it—is essential to valuing the whole group.

The economics of a deposit franchise

KB Kookmin Bank remains the group's dominant profit center. In 2024 it generated ₩3.25 trillion of the group's ₩5.08 trillion in net income, and in 2025, freed of the ELS drag, it rebounded to ₩3.82 trillion on the back of ₩10.66 trillion in net interest income.46 Its balance sheet is one of the largest in the country, and its deposit base spans more than 30 million customer accounts—an extraordinary figure in a nation of roughly 51 million people.

The value of that deposit base is best explained through the lens of what strategists call scale economies, one of Hamilton Helmer's classic sources of durable advantage. A bank makes money on the spread between the yield it earns on assets and the cost of its funding. The cheapest funding on earth is a low-interest checking and savings deposit from a customer who keeps their money at the bank not for the rate but out of habit, convenience, and inertia. KB's vast pool of "sticky" core retail deposits gives it a structural cost-of-funding advantage over regional banks, and especially over non-bank lenders who have to borrow in wholesale markets at far higher rates. When your raw material—money—costs less than your competitor's, you can either earn a fatter margin or win business by lending more cheaply. That is the quiet engine underneath every headline profit number.

Layered on top are high switching costs, the second pillar of the moat. A Korean household's relationship with KB is rarely just a savings account. It is often the mortgage—leveraging the housing-finance DNA inherited from the old Housing & Commercial Bank—plus the payroll account through which a salary arrives every month, plus automatic bill payments, plus the credit card. Unwinding all of that to chase a marginally better rate elsewhere is a genuine hassle, and hassle is the friction that keeps customers in place. The moat is not glamorous. It is ubiquity plus inertia. But it is real, and it has compounded for decades.

The digital onslaught

That moat came under direct assault in the late 2010s from an entirely new kind of competitor. 카카오뱅크 KakaoBank, spun out of the country's dominant messaging platform, and 토스뱅크 Toss Bank, born from a fintech payments app, launched internet-only banks with no branches, no legacy cost structure, and a slick mobile experience that made the incumbents' apps look like relics. Their pitch was simple: open an account in minutes from your phone, get better rates because we have no branches to pay for, and never speak to a banker again. They went straight for the profitable middle of the market—mid-interest personal credit and everyday transactions—and their growth was ferocious. By 2025, Toss and KakaoBank had each amassed monthly active user bases in the tens of millions, with KakaoBank alone surpassing 20 million monthly users and openly targeting 30 million.16

For a bank whose entire advantage rested on being the default place Koreans kept their money, this was existential. If a generation of young customers formed their primary financial relationship inside a chat app instead of a KB branch, the sticky deposit franchise would erode from the bottom up.

The counter-offensive: build, don't buy

KB's response is a case study in how an incumbent can fight platform disruption. Rather than launch a separate digital brand—the tempting but usually value-destructive move that splits focus and cannibalizes the core—KB poured its resources into a single super-app, KB스타뱅킹 KB StarBanking, designed to bundle the entire group into one phone screen. The bet was that KB's breadth was a weapon the monoline fintechs could not match: banking, securities trading, IPO subscriptions, insurance, and card services, plus mobile ID, QR payments, even domestic flight boarding passes and train tickets, all stitched into one portal spanning more than 80 services across the group's subsidiaries.15

The single KPI that captures whether this is working is monthly active users. StarBanking crossed 14 million MAU by 2026, the highest among Korea's traditional financial groups.15 That figure is the clearest evidence that KB has not simply surrendered the digital front. It has not out-innovated the fintechs on user experience—few incumbents anywhere have—but it has done something arguably more important for a bank: it has kept its customers inside its own ecosystem, and with them, the low-cost deposits that fund everything.

It is worth being clear-eyed about what StarBanking is and is not. It is not, on the evidence, a fintech-killer. The internet-only banks are still growing faster off a nimbler base, and by raw app usage Toss and KakaoBank command larger audiences, the former with more than 24 million users and the latter above 18 million as of 2025.16 What StarBanking does is defensive: it raises the switching cost of leaving KB by making the app the single place a customer manages a salary account, a mortgage, a credit card, a brokerage account, and a stack of everyday conveniences. A customer who trades stocks, subscribes to IPOs, and buys travel insurance inside StarBanking is a customer who is unlikely to move their primary deposit to a chat-app bank, no matter how slick its interface. The strategic insight is that the fintechs won the battle for the best mobile experience, but the war that actually matters for a bank is the war for the primary relationship—and there, breadth beats polish. The war is not won, but KB has proven it can hold the line, and holding the line is enough when your underlying franchise is this profitable. The real question for investors shifted from "can KB survive digitization?" to "now that it survives, what will it do with all the capital it generates?"—which is exactly the battle the activists forced into the open.

VI. Dismantling the Korea Discount: Align Partners & the Value-Up Program

Return now to that email from the first trading day of 2023, because this is the section where the paradox of the opening finally gets resolved—or at least seriously challenged.

Anatomy of a discount

The 코리아 디스카운트 is one of the most studied puzzles in global equity markets. Korean companies, and Korean banks especially, have long traded at valuations far below their global peers. On the eve of the activist campaign, Korean banks changed hands at roughly 0.3 times book value, against something closer to 1.0 times for U.S. and European banks and about 0.6 times for Japanese lenders.8 A price-to-book ratio below one is the market's way of saying it does not trust management to earn a decent return on the equity it holds—or, worse, that it expects that equity to be trapped, deployed into low-return growth or hoarded indefinitely rather than returned to owners.

The root cause was not weak profits. Korean banks were highly profitable. The root cause was capital allocation. For decades, the sector chased brute asset growth, expanding loan books even when the market was valuing those earnings at a mere two-to-five times, while paying out only a small slice of profits to shareholders—Korean banks returned roughly a quarter of earnings on average, versus nearly two-thirds for global peers.8 Capital went in and never came out. To a shareholder, retained capital that earns a mediocre return and is never distributed is worth far less than a won paid out today, and the 0.3x multiple was the market pricing exactly that fear.

The activist catalyst

Into this walked 얼라인파트너스 Align Partners Capital Management, led by 이창환 Lee Chang-hwan, a former private-equity investor who had grasped that the discount was not destiny but a solvable problem of governance. In January 2023, Align sent public letters to seven listed financial groups, including KB, laying out a precise set of demands: stop expanding low-margin loans purely for size, adopt a transparent capital-allocation framework, and commit to a medium-term shareholder return ratio of at least 50% of earnings.8 The genius of the campaign was its universality—by targeting the whole sector at once, Align turned capital return into an industry standard rather than a company-specific fight, and made it awkward for any single bank to be the laggard.

Preemptive stewardship, or forced conversion?

KB's response separated it from the pack. Rather than dig in for a hostile proxy war, KB positioned itself as the most cooperative and proactive reformer in the sector. Management appears to have done the arithmetic that Align was counting on them to do: if the reason the stock trades at 0.3x book is inadequate capital return, then credibly committing to return capital should re-rate the equity toward book value—a gain that would dwarf the cost of the dividends and buybacks themselves. Reform was not charity; it was the single highest-return investment available to a KB shareholder, and management held a lot of KB shares' worth of reputational capital riding on it.

An independent read should note the ambiguity here. KB deserves credit for moving early and decisively. But it is also true that the company reformed under intense simultaneous pressure from an activist, from the broader market, and—crucially—from the Korean government itself, which in 2024 launched a national 기업 밸류업 프로그램 Corporate Value-up Program explicitly designed to close the discount. The government's program borrowed openly from Japan, where the Tokyo Stock Exchange had begun publicly pressuring companies trading below book value to explain themselves and fix it—a campaign widely credited with helping re-rate Japanese equities. Korean policymakers, watching their own market languish while Tokyo's soared, wanted the same medicine: tax incentives for companies that raised payouts, disclosure guidelines for "corporate value enhancement" plans, and a general political climate in which returning capital to shareholders became a patriotic act rather than a concession to foreign hedge funds. KB, which built a dedicated Value-Up disclosure hub and made its framework a centerpiece of its investor communications, became the program's most visible corporate success story.[^10]

Whether KB's conversion was conviction or convenience matters, because convenient reforms can be un-reformed when the pressure lifts. It is worth being precise about the political fragility here: the Value-Up program is government policy, and government policy changes with governments. A future administration less enamored of shareholder returns—or more inclined to lean on banks to fund social priorities—could cool the whole campaign. The evidence for genuine commitment, then, has to come from the mechanics KB has actually hard-wired into its own capital policy, so look at the mechanics.

The CET1 framework

In October 2024, KB formalized what became the benchmark Value-Up plan in Korea, and it is worth understanding precisely because its transparency is the whole point.[^8]7 The architecture rests on a single number: the Common Equity Tier 1 ratio, or CET1, which measures a bank's highest-quality capital against its risk-weighted assets. It is the regulator's core gauge of resilience, and it is also, cleverly, KB's chosen trigger for capital return.

The rule is simple to state. KB set a target CET1 ratio of 13.0% and a minimum return on equity of 10%.[^8] Any capital the group generates above the 13% CET1 threshold in a given year is, by policy, returned to shareholders the following year through a combination of stable quarterly dividends and aggressive share buybacks followed by cancellation. Because the trigger is a published, auditable capital ratio rather than a vague promise, shareholders can calculate roughly what is coming before management announces it. The plan also committed to lifting average annual earnings-per-share growth toward 10% and to retiring more than 10 million shares a year—buybacks that cancel stock rather than park it, permanently shrinking the share count.[^8]

It is worth pausing on why buybacks-and-cancellation, specifically, matter so much to this story, because Korean companies historically preferred to hoard cash or, at best, pay modest dividends. When a company buys back its own shares and then cancels them—permanently retiring them rather than holding them as treasury stock that can be re-issued later—it shrinks the number of slices the corporate pie is cut into. Each remaining shareholder's slice grows without them doing anything. For a bank trading below book value, this is close to a free lunch: buying back a share worth one won of book value for, say, 0.6 won of market price is instantly accretive to the book value of every share that remains. The reason this was rare in Korea is cultural and structural—controlling families and management often preferred to keep capital inside the company, where it fed their prestige and their empire-building. KB's commitment to cancel more than 10 million shares a year is therefore a direct repudiation of that old instinct, and it is the single most tangible proof that the reform is real.

Underneath sits the deeper strategic shift: the pivot from loan growth to Return on Risk-Weighted Assets (RoRWA) as the primary management metric. In the old world, a division head was a hero for growing the loan book. In the new world, growth that consumes capital without earning an adequate return is punished, because every won of risk-weighted assets is capital that could otherwise have been returned to shareholders. Think of risk-weighted assets as the regulatory "cost" a bank pays, in required capital, to hold a given loan; a low-margin loan to a giant conglomerate might consume nearly as much capital as a high-margin one to a small business while earning a fraction of the return. RoRWA forces managers to see that trade-off. Executives are now incentivized to shrink low-margin, capital-hungry lending and concentrate capital in high-return segments. That is a genuine reorientation of the business, not a cosmetic one—and it is exactly the behavioral change that decades of "grow the loan book at any cost" had made almost unthinkable inside a Korean bank.

The market's verdict

Did it work? At the end of 2024, KB's CET1 ratio stood at 13.51%, comfortably above the 13% trigger, releasing well over a trillion won of excess capital for return.[^25] For the 2024 financial year, KB delivered roughly ₩1.2 trillion in dividends plus ₩820 billion of buybacks and cancellations, and in early 2025 announced a further large buyback program.[^8][^25] And the stock responded exactly as the theory predicted. By mid-2026, KB shares had climbed to around ₩156,600—a gain of nearly 187% over the roughly two and a half years since Yang took office in late 2023.20 The bank that once traded at a third of book value had re-rated dramatically, leading the Korean financial sector.

The re-rating is real, and it is the strongest evidence that the Korea Discount was always more about behavior than about some immutable national characteristic. But a skeptic would add a caveat: a policy that returns capital is easy to sustain when profits are at record highs and the economy is stable. The framework's true test will come in a downturn, when the CET1 ratio falls toward the trigger and management must choose between defending the buyback and defending the balance sheet. The person who will make that choice deserves a closer look.

VII. Executive Spotlight: Yang Jong-hee's Leadership & Capital Allocation

When Yang Jong-hee took the chairmanship of KB Financial Group on November 21, 2023, he inherited a crisis before he had unpacked his office.19 The Hong Kong ELS products were about to start maturing into their losses, the activist campaign was in full swing, and the government's Value-Up push was gathering steam. It was, in other words, exactly the kind of moment that reveals whether a leader is a capital allocator or a caretaker.

The insider who was really a strategist

Yang is notable as KB's first pure internal successor—a career KB man rather than a government-parachuted appointee, which in the Korean context is itself a signal of institutional maturity. For most of KB's history, and Korean banking's history generally, the top jobs were subject to intense external influence; regulators, politicians, and the ever-present shadow of the state shaped who got to run the country's biggest banks. A clean internal succession, decided by the board on the strength of a track record rather than by political connection, is exactly the kind of governance improvement that foreign investors had long demanded and rarely received.

But the more important fact about his background is where he made his name: as the group's chief strategist, architecting the very non-banking acquisitions that built the dual engine. He was the man in the room extracting the price concession on LIG Insurance, the deal that became the template for his whole approach—diligence as leverage, discipline over prestige. When a chairman's formative achievement is a well-priced acquisition rather than a trophy purchase, it tells you something about how he is likely to allocate capital. It is a meaningful contrast with the archetype of the Korean conglomerate boss who measures success by the size of the empire; Yang's résumé rewards him for buying well and integrating well, not for buying big.

Skin in the game

Yang's alignment with outside shareholders is more than rhetorical, though it should be assessed honestly rather than taken at face value. He holds a modest 5,914 shares in the group, and during the depths of the ELS crisis in 2024 he bought KB stock in the open market to signal 책임경영—"responsible management"—putting his own capital alongside the public shareholders he had just asked to trust the recovery.1718 His compensation is structured to reward long-term value creation rather than short-term size, with a significant portion of incentive pay deferred over multiple years and linked to relative total shareholder return against peers and to return on equity. This is exactly the incentive design an activist would demand, and it aligns the chairman's payout with the same re-rating thesis that drives the Value-Up plan.

A stress-tester would note that 5,914 shares, while a genuine personal commitment, is not a controlling or even a large economic stake; Yang is a professional manager, not an owner-operator, and KB has no founding family whose fortune rises and falls with the stock. That is the norm for Korean financial holding companies, and it is precisely why external governance pressure—activists, the National Pension Service as a major shareholder, and the government's Value-Up framework—matters so much. The discipline is imposed as much as it is chosen.

The credibility test

The best evidence for Yang's credibility is behavioral: he met the Value-Up CET1 targets and delivered record group profits even while absorbing the enormous ELS compensation drag in his first full year. He did not use the crisis as an excuse to quietly abandon the capital-return promise, which is what a weaker manager would have done. He set targets, explained the misses on the ELS front rather than burying them, and hit the shareholder-return commitments anyway. That is guidance discipline under genuine adversity, and it is rare.

The live test of that credibility is unfolding right now. Yang's initial term expires in late 2026, and KB's board has run a formal succession process, narrowing a field of twelve down to a shortlist of six candidates in mid-2026—a group that includes Yang himself, seeking a second term, alongside internal division heads, the president of Kookmin Bank, and an external former bank president.1920 A final candidate is due to be confirmed in September 2026 and installed at an extraordinary shareholders' meeting in November.19 Market observers see Yang as the front-runner, and the nearly 187% share-price gain during his tenure is a powerful argument for continuity.20 But the very existence of a competitive, publicly scrutinized succession—rather than a quiet coronation—is itself a marker of improved governance, and a reminder that the Value-Up reforms will eventually have to prove they can survive a change of leadership. That question—durability under pressure—is the natural bridge to the risks that could break the whole thesis.

VIII. Risk Radar: Real Estate PF, NIM Compression, and Demographics

Every re-rating story invites a hard question: what could send it into reverse? For KB, three structural risks stand out, and none of them is hypothetical.

Risk one: real estate project finance

The most immediate credit risk sits in 부동산 프로젝트파이낸싱 Real Estate Project Finance, the mechanism through which most Korean property development is funded. In a typical PF structure, developers borrow heavily against a project that does not yet exist, betting that pre-sales and completion will repay the debt. It works beautifully when money is cheap and property prices rise. When global and domestic interest rates surged, that machine seized up: high-leverage projects stalled, and a wave of builder restructurings began in late 2023, threatening lenders across the system.

KB's exposure is asymmetric in a way investors should understand. The core bank underwrote PF conservatively and is relatively insulated. The exposure is concentrated in the non-bank subsidiaries—KB Real Estate Trust, KB Savings Bank, and KB Capital—which reach further down the credit and risk curve for yield. Those units have had to book ongoing, painful credit provisions that drag on exactly the non-banking profitability that the dual-engine strategy was built to celebrate. It is a reminder that diversification into higher-yielding businesses also means diversification into higher-risk ones, and that the group's earnings quality is only as good as the underwriting in its riskiest corners.

The second-order diligence point for a careful investor is provisioning adequacy. When a development project stalls, the loss does not appear all at once; it accretes as the collateral is slowly revalued, as restructurings drag on, and as the "extend-and-pretend" instinct delays recognition. The danger sign to watch is not the provisions a bank takes, but the ones it defers—the gap between the losses embedded in a stalled real-estate market and the losses actually run through the income statement. KB's disclosure on this front is reasonable by sector standards, but the honest position is that no outside investor can fully verify the marks on illiquid, half-finished property developments. This is precisely the kind of hidden qualitative risk concentration that can turn a "record profit" year into a disappointing one if the cycle worsens and the deferred losses finally crystallize.

Risk two: NIM compression

The second risk is cyclical but painful: net interest margin compression. A bank's NIM is the spread between what it earns on assets and what it pays for funding. In a rising-rate environment, that spread tends to widen, which is a large part of why Korean banks posted record profits through the recent cycle. But as central banks pass the peak and begin cutting rates, the yields on a bank's loan book reprice downward faster than its deposit costs can follow, squeezing the margin. Analysts have pressed KB management hard on precisely this point—how it intends to defend NIM as rates fall—and the honest answer is that no bank can fully escape the cycle. The dual engine helps, because fee-based securities and insurance income are less rate-sensitive than lending, but the core bank's profitability will face genuine downward pressure if Korean rates decline meaningfully. A portion of KB's recent record earnings is a gift of the rate cycle, and gifts of the rate cycle get taken back.

Risk three: the demographic cliff

The third risk is the slowest-moving and the most profound. South Korea has the lowest birth rate in the world, and its population has begun to shrink and age faster than almost any society in history. For a bank whose entire franchise is built on domestic deposits, mortgages, and consumer credit, this is a structural headwind of the deepest kind. Fewer young households means fewer new mortgages, slower deposit formation, and a shrinking pool of borrowers over the coming decades. A domestic-centric engine cannot outrun a shrinking domestic market forever.

The logical answer is overseas growth, and here KB's record is honestly mixed. Its ventures into Southeast Asian retail banking have not delivered the credible second geographic engine the group needs, and building or buying meaningful scale abroad in banking is notoriously difficult. This is arguably the single most important unsolved problem in the entire KB story: the current profitability is excellent, the capital-return machine is working, but the long-run terminal growth of the core market is negative, and the offshore alternative remains unproven. An investor can be entirely convinced by the Value-Up thesis for the next five years and still worry about the next twenty-five. Those competing time horizons are exactly what the bull and bear cases have to reconcile.

IX. Playbook: Key Strategic & Investment Lessons

Before weighing the verdict, it is worth extracting the transferable lessons from KB's arc, because they generalize well beyond one Korean bank.

The first lesson is the resilience of the dual-engine model. A pure-play commercial bank is a leveraged bet on the interest-rate cycle and the whims of its regulator. By deliberately building or buying top-tier non-banking businesses—insurance and securities in KB's case—a financial group creates a natural hedge: when falling rates and capped lending squeeze the bank, brokerage fees and insurance underwriting can carry more of the load. KB's ability to post record group profit in 2024 even as the core bank absorbed the ELS provision is the clearest proof of the model's value. The caveat, learned the hard way, is that non-banking businesses import their own risks—PF exposure, market sensitivity—so diversification reduces volatility only if each engine is underwritten with discipline.

The second lesson is that M&A discipline is mostly about the willingness to walk away and to demand a lower price. The LIG Insurance deal, in which thorough diligence surfaced hidden liabilities that were then used to extract a price concession, is the archetype. The empire-builders who destroy shareholder value are the ones who fall in love with a target and pay whatever it takes to win. The capital allocators who create value treat diligence as leverage and are prepared to lose the deal rather than overpay for it. KB has done both over its history—overpaying for Hyundai Securities, disciplining LIG and Prudential—and the contrast is itself the lesson.

The third lesson is the power of preempting activists rather than fighting them. Across global markets, the companies that wage total war against activist investors tend to burn management credibility, distract from operations, and destroy value in the process. KB did the opposite: it absorbed the substance of the Align Partners campaign—the capital-return framework, the payout discipline, the CET1 trigger—institutionalized it as its own Value-Up plan, and in doing so converted a potential adversary into a validator of its equity story. The re-rating that followed rewarded shareholders and management alike. The subtle point is that this only works when the activist is right on the merits; KB's reforms succeeded because capital return genuinely was the highest-return use of its capital, not because appeasement is always wise.

Taken together, these lessons describe a company that has mostly learned to allocate capital like an owner rather than a bureaucrat—buying businesses on discipline, retiring stock instead of hoarding it, and reorienting incentives around return rather than size. That is a rare arc for any large bank, and rarer still for one born of a state-orchestrated merger in a market long defined by the opposite instincts. The open question, which the final section confronts directly, is whether these are durable institutional habits or a favorable-conditions performance that could unwind when the profit cycle, the interest-rate cycle, and the political cycle all turn at once.

X. Bull vs. Bear Case: The Long-Term Investor's Verdict

Assemble the evidence, and the two sides of the KB debate come into sharp focus. This is not a recommendation; it is a framework for what an owner should watch.

The bull case: the Value-Up compounder

The bull case begins with the proposition that KB is the gold standard of the Korean Value-Up movement. The 13% CET1 capital-return formula is transparent, programmatic, and precisely the kind of rules-based framework that foreign institutional capital rewards, because it removes discretion and lets shareholders forecast their own returns. The re-rating from roughly 0.3x book toward a more normal multiple is the market ratifying that logic, and if the discipline holds, the combination of steady earnings, a shrinking share count from buyback-and-cancel, and a rising payout can compound attractively.

Underneath the capital story sits a genuinely defensible franchise. Through the lens of Helmer's 7 Powers, KB commands scale economies in its low-cost deposit base and high switching costs in its embedded relationships with 30 million-plus customers—advantages a branchless fintech can dent but cannot easily replicate at KB's cost of funding. Through Porter's five forces, the picture is favorable on several axes: the threat of new entrants into full-service banking is muted by regulation and capital requirements; the bargaining power of individual depositors is low; and the dual-engine model diversifies away some of the rivalry pressure that afflicts pure lenders. The digital counter-offensive, evidenced by StarBanking's 14 million monthly users, shows KB can neutralize fintech disruption enough to retain the deposit base that funds everything.15

The macro backdrop has also been kind. Korea's four largest financial groups collectively posted record profits again in the most recent year, with fee income surging across the sector—evidence that the entire industry, not just KB, is in a sweet spot of high rates and recovering capital markets.[^24] A bull would argue that KB, as the largest and best-diversified of the four, is the highest-quality way to own that trend, and that its leadership position in Value-Up disclosure gives it first claim on the foreign institutional flows chasing the re-rating. The competitive comparison within the peer group is instructive: KB carries the highest non-bank profit share and the strongest super-app engagement among the traditional groups, which is precisely the combination—diversified earnings plus digital retention—that the market is willing to pay a higher multiple for.

The bear case: structural stagnation

The bear case is equally coherent and rests on forces KB cannot control. The most powerful is demographic: a shrinking, aging population caps the long-run growth of every domestic banking product, and KB's overseas expansion has not yet proven it can supply a credible second geographic engine. A company can execute flawlessly and still be swimming against a receding tide.

The second bear pillar is the heavy hand of the Korean state, and this is where Porter's framework turns against KB. The most important "force" acting on a Korean bank is not a competitor or a supplier; it is the regulator and the government, which repeatedly step in during crises to make banks absorb social costs. The ELS voluntary compensation is the textbook example: a nominally "voluntary" ₩862 billion payout that was, in practice, strongly encouraged by a regulator wielding fines and public pressure.1214 Add the periodic pressure to support distressed real-estate PF projects and the recurring "moral suasion" on lending rates, and you have a structural cap on return on equity. The government can, and does, decide that the banks will help pay for the nation's problems. That is a permanent tax on KB's upside that no capital-return formula can fully offset.

The third pillar is the counter-cyclical fragility of the Value-Up promise itself. The capital-return machine has been tested only in good times. Its real trial will come when NIM compresses in a rate-cutting cycle, when PF provisions bite harder, and when the CET1 ratio drifts toward its 13% trigger—forcing a genuine choice between the buyback and the balance sheet. And the ELS episode is a standing reminder that KB's greatest asset, its sales-driven distribution network, is also a recurring source of conduct risk that can vaporize profit and trust in a single product cycle.

What to actually watch

For a long-term owner, the noise reduces to a small number of signals. The first and most important KPI is the CET1 ratio relative to the 13% target, because it is the master valve controlling every won of capital return; watch whether it holds above the trigger through a full profit and rate cycle, not just in record years. The second is the non-bank profit contribution—the roughly 37-40% share that measures whether the dual engine is genuinely diversifying earnings or merely importing new risks like PF losses.6 The third, quieter signal is StarBanking's monthly active users against the relentless growth of KakaoBank and Toss, the clearest gauge of whether KB is holding its deposit franchise against the fintech tide.1516

The final variable is human. A live succession contest will determine, before the end of 2026, whether the architect of the Value-Up era stays to see it through or hands the framework to someone new.19 The deepest question for KB is not whether the current strategy is working—the record profits, the re-rating, and the capital returns say plainly that it is. It is whether a set of reforms adopted under simultaneous pressure from activists, regulators, and the government will prove to be a permanent change in how a Korean financial giant treats its owners, or a fair-weather policy that bends when the weather turns. The next downturn, and the next chairman, will supply the answer.

References

-

2001 — KB Financial Group History: Merger of Kookmin Bank and Housing & Commercial Bank — KB Financial Group ↩↩

-

Kookmin Bank — Company History and 2008 Holding Company Formation — Encyclopedia.com ↩

-

How KB Financial Built its Non-Banking Empire: LIG Insurance and Hyundai Securities — Invest Chosun, 2020-04-13 ↩

-

KB Financial logs industry's first W5tr annual earnings — The Korea Herald, 2025-02-05 ↩↩↩↩↩

-

KB Financial beats estimates with record W5.84tr profit — The Korea Herald, 2026-02-05 ↩

-

KB Financial FY2025 slides reveal 15.1% profit growth and strategic pivot to AI investments — Investing.com, 2026-02-05 ↩↩

-

Sustainable Value-Up Plan Disclosure (Form 6-K) — SEC EDGAR, 2024-10-24 ↩

-

Activist fund Align aims to dispel Korean stocks' undervaluation — The Korea Times, 2023-02-15 ↩↩↩↩

-

Korean banks at risk of W3tr in losses in HK-tied ELS sales — The Korea Herald, 2024 ↩↩↩

-

Catastrophic losses pile up from HK-tied ELS — The Korea Herald, 2024 ↩

-

Korean banks agree to redress investors hit by HSCEI-linked autocall losses — Structured Retail Products, 2024 ↩

-

Korea's top finance firms put aside W1.7tr for Hong Kong-tied ELS compensation — The Korea Herald, 2024 ↩↩

-

South Korean bankers misrepresented risky China-linked notes to retirees, financial watchdog says — South China Morning Post, 2024 ↩

-

Kookmin Bank faces additional fines over overseas property funds after HK-linked ELS scandal — The Korea Times, 2025-12-08 ↩↩

-

How Far Can Financial Apps Go? — Maximizing the Lock-In Effect with Super Apps — The Asia Business Daily, 2026-06-30 ↩↩↩↩

-

KakaoBank Targets 30 Million Users via AI, Global Push — Seoul Economic Daily, 2026-05-03 ↩↩↩

-

Bank, financial group heads rush to buy company stocks — The Korea Times, 2025-01 ↩

-

Chairman Yang Jong-hee Purchases Shares to Signal Responsible Management — BusinessPost Korea, 2024-03-25 ↩

-

KB Financial Narrows CEO Shortlist to Six, Including Chairman Yang — Seoul Economic Daily, 2026-07-03 ↩↩↩↩

-

KB Financial shortlists 6 candidates for chair post — The Korea Herald, 2026-07 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube