The Eye in the Sky: The Satrec Initiative Story

I. Introduction: The "New Space" Dark Horse

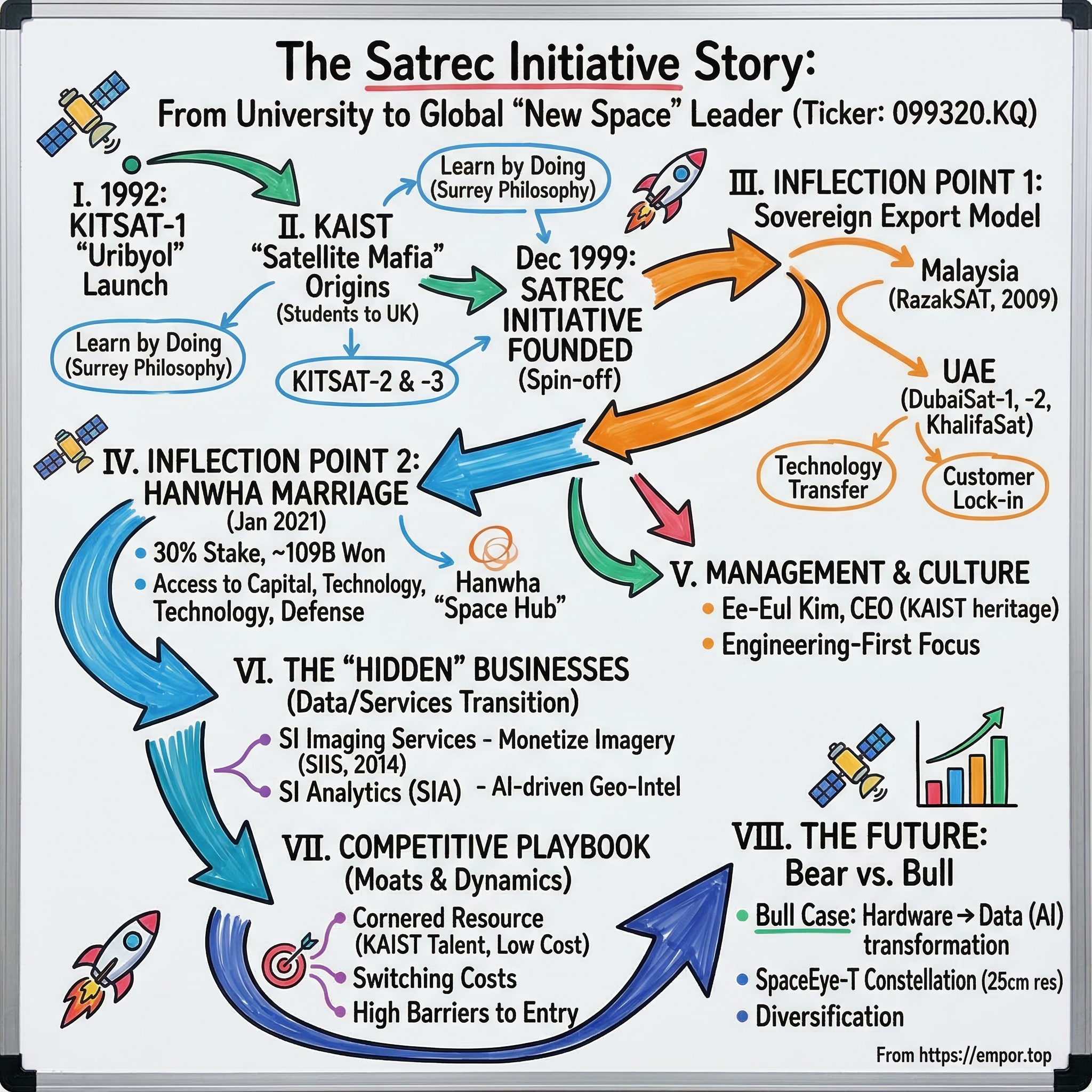

In the summer of 1992, a cluster of graduate students at the Korea Advanced Institute of Science and Technology huddled around a radio receiver in Daejeon, South Korea, waiting for a signal from 680 kilometers above their heads. Moments earlier, an Ariane-4 rocket had lifted off from French Guiana carrying a 48-kilogram microsatellite called KITSAT-1, or "Uribyol"—meaning "Our Star." When the signal came through, South Korea became the twenty-second nation on Earth to operate its own satellite. The students erupted. The satellite they had built with their own hands, in a university lab, was alive in orbit.

Fast forward to March 2025. A SpaceX Falcon 9 rocket launched from Vandenberg Space Force Base in California, carrying a satellite called SpaceEye-T into a sun-synchronous orbit roughly 510 kilometers above Earth. Within three hours, it beamed down its first image—a stunningly crisp photograph of the Canary Islands at 25 centimeters of native resolution. That number is worth pausing on. At 25 centimeters, you can distinguish individual beach umbrellas, read lane markings on highways, and count cars in a parking lot. SpaceEye-T instantly became the highest-resolution commercial optical Earth observation satellite in the world. The company behind it? Satrec Initiative—a small Korean firm that most Western investors have never heard of, trading quietly on the KOSDAQ under ticker 099320.

The arc between those two moments—from a student-built microsatellite to the planet's sharpest commercial eye in the sky—is one of the most remarkable and underappreciated stories in the global space industry. It is a story about how a handful of engineers trained at a British university returned to Korea and built a sovereign satellite export business from scratch. It is a story about how "New Space" existed in Daejeon long before the term was coined in Silicon Valley. And it is a story about how Hanwha, one of South Korea's largest conglomerates, spotted the opportunity that global investors missed—acquiring a crown jewel of space technology for a fraction of what the frothy Western SPAC market was paying for companies with far less heritage.

But the most important chapter of the Satrec Initiative story may be the one being written right now: the transition from a cyclical hardware manufacturer into an AI-driven geospatial intelligence company. If the hardware business is the body, the emerging data and analytics businesses—SI Imaging Services and SI Analytics—are the brain. And the brain, as investors in every technology cycle eventually learn, is where the real value accrues.

To understand where Satrec Initiative is going, we need to start where it began: with a group of students, a one-way ticket to England, and a mission to bring space technology home to Korea.

II. The KAIST "Satellite Mafia" and the Lean Startup Origins

In 1989, South Korea had no satellites, no launch vehicles, and no meaningful space infrastructure. The country's space program, such as it was, consisted of aspiration and not much else. The Cold War was winding down, and nations across Asia were beginning to recognize that space capability—particularly Earth observation—was not a luxury but a strategic necessity. The question was how to get there. The Americans had NASA, with a budget measured in tens of billions. The Europeans had ESA. The Russians had Roscosmos and decades of Soviet-era heritage. South Korea had none of that. What it did have was a university.

KAIST, South Korea's premier science and technology institute, established the Satellite Technology Research Center—SaTReC—in August 1989, under the direction of Dr. Soon-dal Choi. Choi, who would later be recognized as the father of Korea's first satellite, had a deceptively simple plan. He would send a small team of KAIST graduate students to the University of Surrey in Guildford, England, to learn how to build satellites from the ground up. Surrey, under the leadership of Prof. Martin Sweeting, had pioneered a radical concept: building capable, functional satellites for under a million dollars using commercial off-the-shelf components. While the traditional aerospace giants—Lockheed, Boeing, Hughes—were constructing bus-sized spacecraft costing hundreds of millions, Surrey was proving that a team of clever engineers could accomplish useful missions with satellites the size of a washing machine at a hundredth of the cost.

Between six and ten KAIST students made the journey to Guildford in the late 1980s. Among them was Sungdong Park, a KAIST electrical engineering graduate from the class of 1986, who would later become one of Satrec Initiative's co-founders. The students did not simply observe. They got their hands dirty, working alongside Surrey engineers on every aspect of satellite design, integration, and testing. Think of it as an apprenticeship—the Korean students were learning a craft, not studying a textbook. By the time they returned to Daejeon with the knowledge to build KITSAT-1, they had absorbed something far more valuable than technical specifications. They had internalized a philosophy: that space technology did not require enormous budgets, just exceptional engineering talent and an obsessive focus on simplicity.

KITSAT-1's successful launch in August 1992 was a watershed moment for South Korea, but the SaTReC team was already looking ahead. KITSAT-2 followed in September 1993, with a greater share of design and assembly performed domestically. Then came KITSAT-3 in May 1999—a 110-kilogram satellite designed and built almost entirely in Korea, carrying a multispectral Earth observation camera with significantly improved resolution. With each successive satellite, the Korean team had shifted the center of gravity from Surrey to Daejeon. By the time KITSAT-3 reached orbit, the KAIST engineers did not need Surrey anymore. They had become the teachers.

But here is where the story takes its critical turn. KAIST was an academic institution. It could train engineers and publish papers, but it could not sign commercial contracts, bid on international tenders, or build a sustainable business. The graduates who had built three satellites from scratch—who represented perhaps the most concentrated pool of small satellite expertise in Asia—faced a choice. They could stay in academia, continue doing government-funded research, and watch their skills atrophy. Or they could do something audacious: spin off into a private company and sell satellites to the world.

In December 1999, they chose the audacious path. Satrec Initiative Co., Ltd. was founded in Daejeon by a core team of SaTReC alumni, including Sungdong Park, who had served as project manager for both KITSAT-2 and KITSAT-3. The name itself was a tribute to their origins—"Satrec" derived directly from SaTReC. The company's proposition was essentially this: we will do for other countries what Surrey did for us. We will build you a high-performance, low-cost Earth observation satellite, train your engineers, set up your ground stations, and give you a sovereign space capability—all for a price that makes the Western aerospace primes look like highway robbery.

They were, in every meaningful sense, a "New Space" company before the term existed. Small team. Lean operations. A focus on driving down cost and timeline without sacrificing performance. The only difference between Satrec Initiative in 1999 and the Silicon Valley "New Space" startups that would emerge a decade later was that Satrec was not backed by venture capital or billionaire founders. It was backed by talent—a cornered resource of engineering expertise that no amount of money could replicate overnight.

The lean startup origins would shape everything that followed. But the real inflection point came when Satrec realized that selling satellites was not just about hardware. It was about selling entire space programs.

III. Inflection Point 1: The Sovereign Export Model

Picture a conference room in Kuala Lumpur in the early 2000s. On one side of the table, officials from Malaysia's Astronautic Technology Sdn Bhd—the country's space technology company—are laying out their ambition. Malaysia wants an Earth observation satellite. Not just to buy imagery from someone else's satellite, but to own one. To operate it. To train Malaysian engineers who can build the next one. To have a sovereign capability that does not depend on the goodwill of a foreign government or the pricing whims of a commercial imagery provider. On the other side of the table, a small Korean company most of the room has never heard of is making a pitch that sounds almost too good to be true.

Satrec Initiative understood something that the Western aerospace primes did not fully appreciate, or perhaps did not care to pursue. For emerging nations seeking space capability, the satellite itself was only part of the value proposition—and perhaps not even the most important part. What these nations truly wanted was a space program. They wanted the ground stations, the mission control software, the training programs for their own engineers, and the institutional knowledge to eventually build satellites domestically. The satellite was the product. The space program was the platform.

This insight became the foundation of what might be called the "Sovereign Export Model." When Satrec won the contract for what would become RazakSAT—Malaysia's first Earth observation satellite—the deal was structured not as a simple hardware purchase but as a comprehensive technology partnership. Satrec would design and build the satellite on its SI-200 bus platform, a compact and capable spacecraft weighing roughly 180 kilograms. But critically, Malaysian engineers from ATSB would be embedded in the development process, working alongside the Korean team at every stage. Satrec was not just selling a satellite; it was seeding a satellite engineering culture in Malaysia.

RazakSAT launched on July 14, 2009, aboard a SpaceX Falcon 1 rocket from Omelek Island in the Kwajalein Atoll—notably one of the earliest commercial flights for SpaceX's debut orbital vehicle. The satellite carried an electro-optical camera capable of 2.5-meter panchromatic resolution, designed for a three-year operational life. The launch itself was a milestone for two companies simultaneously: for SpaceX, it was validation of a commercial launch model still in its infancy; for Satrec, it was proof that a Korean company could deliver a turnkey satellite system to an international customer.

But it was the UAE contracts that truly demonstrated the power and scalability of the Sovereign Export Model. In May 2006, the Emirates Institution for Advanced Science and Technology awarded Satrec Initiative the contract for DubaiSat-1. Once again, the deal included a Technology Transfer Program, with roughly ten UAE engineers traveling to Daejeon to work directly on the satellite's design, assembly, integration, and testing. DubaiSat-1 launched on July 29, 2009, from the Baikonur Cosmodrome in Kazakhstan aboard a Dnepr rocket—a converted Soviet-era ICBM repurposed as a space launch vehicle. The satellite, built on the same SI-200 platform as RazakSAT, delivered 2.5-meter panchromatic and 5-meter multispectral imagery.

The genius of the model became apparent with what happened next. DubaiSat-2 followed in 2013, with sixteen UAE engineers participating in development—a significant increase from the ten who had worked on DubaiSat-1. The Emirati team was not just observing anymore; they were designing, testing, and manufacturing. By the time the program evolved into KhalifaSat—often referred to as DubaiSat-3—the balance of work had shifted further toward the UAE side. The satellite was initially designed in Korea, then production was transferred midway to EIAST's own facilities in the UAE. Satrec had, in effect, replicated the Surrey-to-KAIST technology transfer model with the Emiratis, and each successive contract deepened the relationship and expanded the scope.

This created something extraordinarily valuable from a business strategy perspective: switching costs. Once a nation had built its ground infrastructure on Satrec's software stack, trained its engineers in Satrec's design philosophy, and invested years in a collaborative development program, the cost of switching to an Israeli, American, or European provider was not just financial—it was institutional. The entire knowledge base of the country's satellite engineering workforce was built on Satrec's architecture. Moving to a competitor would mean starting over. In Hamilton Helmer's framework, this is one of the most durable forms of competitive advantage.

The sovereign export model also generated something that one-off government research grants never could: recurring revenue and deepening relationships. Malaysia came back. The UAE came back—repeatedly. Each contract was larger, more sophisticated, and more profitable than the last. Satrec had transformed itself from a university spin-off into a global exporter of sovereign space capability, and it had done so without the backing of a major defense prime or a government agency with a trillion-won budget.

By the late 2000s, the small Korean company from Daejeon had delivered operational satellites to multiple nations and established itself as one of the only companies in the world—alongside Surrey's SSTL—that could offer the complete package of satellite manufacturing, ground systems, and institutional capacity building at a price point that emerging nations could afford. The question was no longer whether Satrec could compete globally. The question was how big it could get—and what kind of partner it would need to get there.

IV. Inflection Point 2: The Hanwha Marriage and Capital Deployment

In January 2021, the global space industry was in the grip of a very particular kind of mania. SPACs—Special Purpose Acquisition Companies—had become the vehicle of choice for space startups looking to access public capital markets without the scrutiny of a traditional IPO. Planet Labs, the San Francisco-based Earth observation company, was in the process of going public at a valuation of roughly $2.8 billion on revenue of approximately $113 million. Spire Global, a weather and maritime data company, was headed for the public markets at around $1.2 billion on revenue of roughly $28 million. BlackSky, an intelligence company with a small constellation, was valued at approximately $1.1 billion on revenue of about $18 million. Rocket Lab, which at least had the distinction of being a proven launch provider, was valued at north of $4 billion on revenues of roughly $35 million. The common thread was that these were speculative bets—forward-looking valuations based on projected revenues that, in many cases, were years away from materializing.

Against this backdrop, Hanwha Aerospace quietly announced on January 13, 2021, that it would acquire a 30 percent stake in Satrec Initiative for 109 billion won—approximately $100 million. The deal was structured in two tranches: 59 billion won for a 20 percent stake via a third-party share placement priced at 32,426 won per share—a 22 percent discount to the prior closing price of 41,200 won—and an additional 50 billion won in convertible bonds that would bring the total ownership to 30 percent upon conversion. The implied full-company valuation was roughly 330 to 363 billion won, or approximately $290 to $320 million.

Let that sink in. At a moment when Western investors were paying $2.8 billion for a company with decent revenue but unproven unit economics, and over $1 billion for companies generating less than $30 million in annual sales, Hanwha was acquiring a controlling interest in a profitable company with three decades of flight heritage, more than thirty successful satellite missions, and the engineering talent pool to build the world's highest-resolution commercial optical satellite—for roughly $100 million. The deal valued Satrec at a fraction of the multiples being lavished on its Western peers. Hanwha was buying Tier 1 technology at a middle-market price.

The strategic logic was compelling from both sides. For Hanwha, Satrec filled a critical gap in what the conglomerate envisioned as a vertically integrated space value chain. Hanwha Aerospace was already positioning to take over production of South Korea's Nuri rocket—the KSLV-II launch vehicle—from the government space agency KARI. Hanwha Systems was investing $300 million in OneWeb, the LEO broadband constellation, and had acquired Phasor Solutions, a UK-based antenna technology company. What Hanwha lacked was the satellite manufacturing capability itself—the ability to design, build, and operate the spacecraft that would ride on its rockets and feed data into its networks. Satrec provided exactly that.

For Satrec, the benefits were equally transformative. The company had spent two decades operating on the financial razor's edge that characterizes most small aerospace firms. Satellite contracts are large but lumpy—a multi-year development program generates significant revenue during the build phase, but there can be long droughts between contracts. The Hanwha investment provided not just capital—roughly 110 billion won in cash that would sit on the balance sheet—but access to Hanwha's radar and infrared technologies, its defense procurement relationships, and, perhaps most importantly, the credibility that comes with being backed by one of South Korea's largest industrial groups. Satrec could now pursue larger, more complex programs that would have been beyond its reach as an independent small-cap company.

Two months after the acquisition announcement, Hanwha formalized its ambitions by launching the "Space Hub" task force on March 7, 2021, led by Kim Dong-kwan, the heir and now vice chairman of Hanwha Group. The Space Hub consolidated all space-relevant resources across Hanwha's affiliates—rocket propulsion, satellite manufacturing, communications, ground terminals—under a single strategic umbrella. Kim Dong-kwan himself joined Satrec's board as an unpaid director, a signal that the conglomerate was not treating this as a passive financial investment but as a strategic cornerstone. The vision was nothing less than building a "Korean SpaceX"—a vertically integrated space company capable of launching rockets, building satellites, and selling the data they collect.

The timing proved prescient. Within eighteen months of the SPAC frenzy, many of those richly valued Western space companies had seen their stock prices collapse by 60 to 90 percent as the market revalued speculative growth stories in a rising interest rate environment. Planet Labs, Spire, BlackSky—all traded well below their SPAC-era valuations by 2023. Hanwha, meanwhile, had locked in its stake in a proven, profitable enterprise at a conservative valuation. By early 2026, Satrec's market capitalization had grown to approximately 2 trillion won—roughly $1.5 billion—representing a nearly sixfold increase from the implied valuation at the time of the Hanwha deal. The SPAC-era space companies, by and large, were still trying to claw their way back to their debut valuations.

The Hanwha marriage did not just change Satrec's balance sheet. It changed its strategic trajectory. With access to capital, defense relationships, and complementary technology, Satrec could now think in terms of constellations rather than individual satellites, in terms of recurring data services rather than one-off hardware contracts. The era of building one satellite at a time was over. The constellation era had begun.

V. Management: The New Guard and Incentive Structures

When Ee-Eul Kim took the helm as CEO of Satrec Initiative in January 2019, he inherited a company at a crossroads. The engineering culture was world-class—decades of accumulated expertise in designing and building high-performance Earth observation satellites, rooted in the KAIST SaTReC tradition. But the commercial trajectory was troubling. International revenue, which had historically accounted for roughly two-thirds of total sales thanks to the sovereign export contracts with Malaysia, the UAE, and others, was beginning a steep decline. By the time Kim's tenure matured, foreign revenue would collapse to below 10 percent of total sales—a dramatic reversal that raised uncomfortable questions about the company's ability to sustain its export-first identity.

Kim brought a particular set of credentials to the role. A KAIST alumnus himself, he had served as a Senior Research Engineer at the very SaTReC lab that had birthed the company. He was, in the parlance of the space industry, a "heritage guy"—someone who understood the technology from the component level up, who had lived through the transition from academic microsatellites to commercial Earth observation platforms, and who commanded the respect of the engineering workforce that remained Satrec's most irreplaceable asset. Forbes Korea recognized him in October 2023 as "a pioneer in the Korean space industry," and by some rankings he stood as the second-highest value creator among space company CEOs globally, with approximately $195 million in shareholder value created during his tenure.

Yet the CEO's challenge was not primarily technical. It was organizational. The Hanwha acquisition in 2021 transformed Satrec from a founder-led, independently operated company into a subsidiary of one of South Korea's largest conglomerates—one with ambitions spanning rockets, communications satellites, defense electronics, and lunar exploration. Managing this transition—preserving the high-trust, engineering-first culture that made Satrec's technology possible while integrating into Hanwha's corporate structure and leveraging its resources—required a particular kind of leadership. Too much corporate integration would suffocate the innovative culture that had produced satellites like SpaceEye-T. Too little would waste the strategic synergies that justified the acquisition in the first place.

The solution, at least structurally, was to maintain Satrec's operational independence while embedding it within Hanwha's strategic framework. Satrec continues to operate as a distinct entity on the KOSDAQ, with its own management team, its own engineering processes, and its own product development roadmap. But it now has access to Hanwha's radar and infrared technologies—capabilities that are essential for building the next generation of dual-use satellites that serve both commercial and defense customers. The arrangement is not unlike how Alphabet manages its various subsidiaries: strategic alignment at the top, operational autonomy in the middle, shared resources where it makes sense.

The incentive structures tell an important part of the story. The Hanwha deal was structured in a way that protected Satrec's engineering talent—the core asset—by ensuring that stock options and equity participation remained meaningful for key personnel. At a company where 60 percent of employees hold master's or doctoral degrees at the time of IPO, talent retention is not a nice-to-have; it is existential. You cannot hire satellite systems engineers off the street. The knowledge required to design a 25-centimeter-resolution optical payload, integrate it into a spacecraft bus, and ensure it survives the vibration, thermal, and radiation environment of low Earth orbit is the product of years—often decades—of specialized experience. If the senior engineers walk, the company's competitive advantage walks with them.

Kim's management style reflects this reality. Decisions are made with an engineering-first orientation—the question is not "what does the market want?" but "what is technically possible, and how do we get there?" This approach delivered SpaceEye-T, which pushed commercial optical resolution to its current frontier. But it also contributed to the international sales drought. While the company was focused on developing next-generation technology, the commercial pipeline of sovereign export contracts—the bread and butter that had built the company—was not being replenished at the same pace. Whether this was a conscious strategic choice (focus on the flagship product, then sell it globally) or a management gap (insufficient attention to business development) is a question that investors will need to evaluate as the SpaceEye-T constellation expands and new international contracts materialize.

The recent European leasing contract signed by SIIS in September 2025, covering multi-year capacity on SpaceEye-T, suggests that the international revenue picture is beginning to shift. The Etihad-SAT radar satellite partnership with the UAE, also announced in 2025, signals a return to the sovereign export model with a more sophisticated product offering. If Kim can successfully navigate the dual challenge of scaling the constellation and rebuilding the international order book, the investment thesis changes fundamentally. But for now, the management story is one of a technically brilliant leader steering a company through the most consequential transition in its history—from a lean, independent satellite builder to a corporate-backed powerhouse with ambitions spanning Earth observation, defense, and artificial intelligence.

VI. The "Hidden" Businesses: Beyond the Hardware

There is a well-worn pattern in technology investing. A company builds its reputation—and its initial valuation—on hardware. Investors think of it as a hardware company and value it on hardware multiples. Then, quietly, the company begins building software and services businesses that grow faster, carry higher margins, and generate recurring revenue. By the time the market notices, the company has transformed itself, and the valuation has to be recalibrated. Think of Apple in 2016, when Services was a small fraction of revenue; today, it is the highest-margin segment and arguably the most valuable part of the business. Think of John Deere, which sells tractors but increasingly makes its money from precision agriculture data and subscriptions.

Satrec Initiative is in the early stages of this transformation, and the market has not yet fully priced it in.

The hardware business—designing and building Earth observation satellites—remains the core of Satrec's revenue. It is a good business, with high barriers to entry and a deep moat built on three decades of engineering heritage. But it is also cyclical and lumpy. A major satellite contract generates significant revenue during the multi-year development and build phase, then revenue drops until the next contract is signed. This creates the kind of earnings volatility that makes institutional investors nervous and depresses valuation multiples.

The first layer of the transformation is SI Imaging Services, or SIIS, founded in 2014. SIIS is, in essence, the commercial arm that monetizes the imagery captured by Satrec-built satellites. In November 2012, the Korea Aerospace Research Institute appointed Satrec as the exclusive worldwide representative for KOMPSAT-2, KOMPSAT-3, and KOMPSAT-5 imagery sales. This was a significant mandate—the KOMPSAT series represents South Korea's flagship Earth observation satellites, and exclusive global distribution rights meant that any government, enterprise, or research institution anywhere in the world that wanted high-resolution Korean satellite imagery had to go through Satrec.

SIIS expanded this role with DubaiSat-2 imagery distribution, and most importantly, it is now the entity that will operate and commercialize data from the SpaceEye-T constellation. The September 2025 European leasing contract—a multi-million-euro, multi-year deal—represents the kind of revenue that investors should pay close attention to. This is not a one-time hardware sale. This is a recurring services contract, where a European customer is leasing access to SpaceEye-T's imaging capacity over multiple years. The economic profile is fundamentally different from hardware: higher margins, greater predictability, and the potential for contract renewals and expansion.

SIIS's financial trajectory tells the story. In recent years, the subsidiary was generating roughly 7.5 billion won in annual sales while still operating at a loss as it invested in building out its distribution infrastructure and commercial relationships. Analyst projections for 2026 pointed to approximately 15 billion won in revenue—nearly doubling year-over-year—with a profitability turnaround. As the SpaceEye-T constellation grows from one satellite to the planned four by 2028, SIIS's addressable capacity—and therefore its revenue potential—will scale proportionally.

But SIIS is not the hidden gem. That distinction belongs to SI Analytics, or SIA.

SIA is an AI-native geospatial intelligence company. To understand what it does and why it matters, consider the fundamental problem with satellite imagery. A single high-resolution Earth observation satellite generates terabytes of imagery data every day. Historically, extracting useful intelligence from that data required human analysts—trained photo interpreters who would spend hours poring over images, looking for changes, identifying objects, and writing reports. This approach does not scale. There are not enough trained analysts in the world to process the volume of imagery that modern satellite constellations produce. And even the best human analysts make mistakes, get tired, and can only look at one image at a time.

SIA's approach is to replace human analysts with machine learning algorithms that can automatically detect and classify objects in satellite imagery—ships in port, aircraft on runways, vehicles at military installations, changes in crop health, construction progress at building sites, even missile launcher activity. Think of it as computer vision applied to Earth observation. The algorithms do not just identify what is in an image; they track changes over time, flag anomalies, and generate predictive analytics. This turns raw satellite imagery—essentially very expensive photographs—into actionable intelligence that can be delivered as a software service.

The implications are profound. Raw satellite imagery is a commodity. Multiple companies—Planet Labs, Maxar, Airbus, and now Satrec with SpaceEye-T—can sell you a picture of any spot on Earth. The margins on imagery alone are decent but not transformative. But processed intelligence—"there are three new ships in this port compared to last week," or "crop yields in this province are projected to decline by 12 percent based on vegetation index changes"—is a fundamentally different product. It is higher-value, harder to replicate (because the algorithms require both domain expertise and training data), and can be delivered as a subscription service with SaaS-like economics.

SIA's revenue was approximately 4.7 billion won in 2023—still modest relative to the overall business. But the growth trajectory is what matters. This segment was generating negligible revenue just a few years ago, and it is growing significantly faster than the hardware division. The customer base spans defense and intelligence agencies (where the applications include maritime domain awareness and military activity monitoring), agriculture (crop yield prediction and land use analysis), and infrastructure (construction monitoring and urban planning).

The strategic logic for Satrec is clear. If the company can build a constellation of four SpaceEye-T satellites providing daily revisit imaging at 25-centimeter resolution, and pipe that imagery through SIA's AI processing pipeline, it creates a vertically integrated intelligence platform. Satrec builds the satellite (hardware margin), SIIS distributes the imagery (services margin), and SIA extracts intelligence from the imagery (software margin). Each layer captures additional value from the same underlying asset—the satellite in orbit.

The historical revenue mix tells the story of a company in transition. In its earlier years, hardware accounted for roughly 90 percent of total revenue. As SIIS and SIA scale, the mix is shifting toward a growing 30 to 40 percent contribution from data and services. This is the re-rating catalyst that long-term investors should be watching. A pure hardware company trades on low-teens multiples of earnings. A company with a significant and growing recurring-revenue, AI-driven intelligence business deserves a materially higher multiple. The market has not yet fully recognized this shift, in part because the absolute revenue numbers from SIIS and SIA are still relatively small. But the trajectory is unmistakable.

The hidden businesses are not hidden because Satrec is trying to conceal them. They are hidden because the market has a tendency to anchor on what a company was, rather than what it is becoming. For investors willing to look past the "satellite manufacturer" label, the emerging data and analytics businesses represent the most interesting part of the Satrec Initiative story.

VII. The Playbook: Competitive Moats and Industry Dynamics

To understand whether Satrec Initiative's competitive position is durable—whether it can sustain and grow its advantages over time—it helps to apply two complementary analytical frameworks: Hamilton Helmer's 7 Powers, which focuses on the sources of persistent differential returns, and Michael Porter's Five Forces, which maps the competitive dynamics of the industry itself.

Cornered Resource: The KAIST Talent Pipeline

The single most important competitive advantage Satrec possesses is its people. This is not a platitude. In satellite engineering, there is no substitute for experience. Building a high-performance Earth observation satellite is not like building a software application—you cannot iterate rapidly, ship a minimum viable product, and fix bugs in production. A satellite gets one chance. If the optical payload is misaligned by a fraction of a millimeter, or if a thermal design flaw causes the imaging sensor to overheat, or if a software error in the attitude control system sends the spacecraft into an unrecoverable spin, the result is a multi-million-dollar piece of space debris. The margin for error is effectively zero.

Satrec's engineering team represents over three decades of accumulated expertise, tracing directly back to the KAIST SaTReC program and the KITSAT series. These are engineers who have designed, built, tested, and operated more than thirty satellites—a flight heritage that very few companies in the world can match. More importantly, KAIST continues to produce graduates with the specialized skills in spacecraft systems engineering, optical payload design, and orbital mechanics that Satrec needs. This creates a self-reinforcing talent pipeline that competitors cannot easily replicate. You cannot simply throw money at the problem and hire a comparable team. The knowledge is tacit, embedded in institutional practices and hard-won lessons from decades of mission experience.

Satrec also benefits from a significant cost advantage in this regard. The average salary at Satrec is approximately 71 million won per year—roughly $50,000 to $55,000 at current exchange rates. Compare that to the $120,000 or more that a comparable satellite engineer commands in the United States. This means Satrec can maintain a world-class engineering workforce at roughly half the labor cost of its American competitors—an advantage that flows directly to the bottom line on every program.

Switching Costs: The Infrastructure Lock-In

The sovereign export model, discussed earlier, creates formidable switching costs for Satrec's international customers. When a nation builds its ground station network, mission control center, and data processing infrastructure on Satrec's software and systems architecture, and when its engineers are trained in Satrec's design methodology, the cost of transitioning to a different provider is prohibitive. It is not just a matter of buying a different satellite; it is a matter of retraining an entire engineering workforce, rebuilding ground infrastructure, and accepting the risk inherent in transitioning to an unfamiliar system. The switching costs are measured not just in money but in years of institutional learning that would have to be repeated.

Process Power: Lean Heritage Manufacturing

Satrec has spent decades refining its manufacturing processes to deliver high-performance satellites at price points that undercut larger competitors. This is not easily replicable. The company's ability to produce a satellite like SpaceEye-T—with 25-centimeter resolution from a relatively compact platform—reflects deep process knowledge in areas like optical fabrication, thermal management, and spacecraft integration. Competitors with higher cost structures, less efficient processes, or less experienced workforces would struggle to match Satrec's price-performance ratio without years of investment.

Porter's Five Forces Analysis

The Earth observation satellite industry presents a distinctive competitive landscape that helps explain why Satrec has been able to thrive despite its relatively small size.

Barriers to Entry: Extremely high. Building an Earth observation satellite is, quite literally, rocket science—or more precisely, the science of building instruments that ride on rockets. The barriers are not just technological but regulatory (export controls on high-resolution imaging technology), financial (each satellite represents a capital investment measured in tens of millions of dollars), and reputational (no country wants to entrust its sovereign space program to an unproven company). The result is an industry with a small number of established players and very limited new entry.

Bargaining Power of Buyers: This is where the Hanwha acquisition changes the equation most significantly. As an independent small company, Satrec was heavily dependent on a small number of sovereign customers, each wielding significant negotiating leverage. If the UAE or Malaysia decided to negotiate aggressively on price, Satrec had limited alternatives. Now, as part of Hanwha's ecosystem, Satrec has the South Korean government itself as a major customer—and South Korea's space budget is expanding rapidly, with plans to double spending by 2027. The bargaining dynamic has shifted. Satrec is no longer a small vendor competing for scarce international contracts; it is a national champion with a guaranteed domestic customer base and the strategic backing to compete globally from a position of strength.

Threat of Substitutes: Moderate and increasing. The emergence of large-scale constellations like Planet Labs, which provides lower-resolution but higher-frequency imagery from hundreds of small satellites, represents a partial substitute for Satrec's high-resolution, single-satellite approach. For applications where timeliness matters more than resolution—tracking deforestation, monitoring large-scale weather patterns—Planet's daily global coverage may be sufficient. But for applications requiring the kind of detail that 25-centimeter resolution provides—intelligence, defense, infrastructure monitoring—there is no substitute for the quality that SpaceEye-T delivers. The planned expansion to a four-satellite constellation by 2028 will address the revisit frequency gap while maintaining the resolution advantage.

Rivalry Among Existing Competitors: Concentrated but intensifying. The Earth observation satellite imagery market, estimated at approximately $3.9 billion in 2025 and expected to grow to $5.1 billion by 2030, is dominated by a handful of players. Maxar Technologies held roughly 37.7 percent market share in 2024, followed by Airbus Defence and Space at approximately 20 percent. The remaining share is divided among Planet Labs, ImageSat International (Israel's ISI, perhaps Satrec's most direct comparable), BlackSky, Satellogic, and Satrec itself. Competition is intensifying as more players enter the market and existing players expand their constellations, but the market is also growing—driven by increasing demand for satellite intelligence from defense agencies, agricultural enterprises, financial institutions, and climate monitoring organizations.

Bargaining Power of Suppliers: The launch industry, which was once a significant cost and bottleneck, has been transformed by SpaceX's rideshare program. Satrec launched SpaceEye-T on a SpaceX Falcon 9 Transporter mission, which offers access to orbit at a fraction of the cost of a dedicated launch. Additionally, with Hanwha Aerospace taking over production of South Korea's Nuri rocket, Satrec may eventually have access to a domestic launch option—further reducing its dependence on foreign launch providers.

Competitive Positioning Summary

Satrec occupies a distinctive position in the global Earth observation landscape. It is not the largest player (that distinction belongs to Maxar), nor the most prolific in terms of satellite count (Planet Labs operates hundreds of spacecraft). What it offers is a combination of ultra-high resolution, proven flight heritage, competitive pricing driven by Korean labor cost advantages, and a sovereign export model that creates deep, recurring relationships with national customers. The addition of AI-driven analytics through SIA adds a software dimension that most pure-play hardware competitors lack.

The most apt comparison may be to ImageSat International, the Israeli company that similarly sells high-resolution Earth observation satellites and services to sovereign customers. ISI derives roughly 95 percent of its revenue from international sales, compared to Satrec's current sub-10 percent international revenue share. This comparison cuts both ways: it highlights Satrec's current weakness in international business development, but it also demonstrates the size of the addressable market for companies pursuing the sovereign satellite export model. If Satrec can rebuild its international sales to even a fraction of ISI's proportional level, the revenue implications would be substantial.

VIII. Bear vs. Bull Case and the Future

The Bear Case

The most immediate risk facing Satrec Initiative is concentration. With international revenue having collapsed from two-thirds of total sales in 2019 to below 10 percent in recent years, the company is overwhelmingly dependent on the South Korean government for revenue. This creates a classic defense contractor vulnerability: if the government budget tightens, or if procurement priorities shift toward other programs, Satrec's top line could come under significant pressure. The company is, in effect, a single-customer business—and single-customer businesses trade at a discount for good reason.

The second risk is competitive. SpaceX's vertically integrated model—building rockets, launching satellites, operating the Starlink constellation, and increasingly entering the Earth observation market—represents a potential long-term threat to every company in the space value chain. If SpaceX decides to offer high-resolution Earth observation services (and its acquisition of Swarm Technologies and partnership patterns suggest it may), it could leverage its cost advantages in launch and its massive constellation infrastructure to undercut specialized players like Satrec on price. The integration of launch and satellite services under one roof creates efficiencies that standalone satellite manufacturers cannot match.

Third, there is the space debris risk. As low Earth orbit becomes increasingly congested—with thousands of satellites from Starlink, OneWeb, and other constellations—the probability of collision events increases. A major debris event could damage or destroy satellites worth tens of millions of dollars, with no insurance covering the full replacement cost and timeline. This is an industry-wide risk, but it disproportionately affects companies like Satrec that operate a small number of high-value satellites rather than large constellations of less expensive spacecraft.

Finally, there is execution risk around the constellation buildout. Satrec has announced plans to deploy four SpaceEye-T satellites by 2028, at an estimated total cost of roughly $100 million. The company has demonstrated its ability to build and launch one satellite successfully. Scaling to four—while simultaneously developing the ground infrastructure, data distribution network, and AI analytics platform to commercialize the constellation—is a materially different challenge. The history of space companies is littered with ambitious constellation plans that foundered on execution, financing, or market demand.

The Bull Case

The bull case for Satrec Initiative rests on a single, powerful thesis: the transition from hardware to data.

As SIA—the AI analytics subsidiary—scales its capabilities and customer base, Satrec has the potential to transform from a cyclical satellite manufacturer trading at hardware multiples into a recurring-revenue intelligence platform trading at software multiples. The difference in valuation is enormous. A satellite hardware company might trade at 10 to 15 times earnings. A high-growth, AI-driven intelligence company with recurring revenue and strong retention metrics could command 30 to 50 times earnings—or more. Even a modest re-rating of Satrec's multiple, driven by growing recognition of the data business, would translate into significant upside from current levels.

The SpaceEye-T constellation is the catalyst. With 25-centimeter native resolution—currently the highest available commercially—Satrec has a product that is differentiated on the single dimension that matters most in Earth observation: image quality. When customers need to count vehicles, identify equipment types, or assess damage at specific facilities, they need the best resolution available. SpaceEye-T delivers that. As the constellation grows to four satellites, the daily revisit capability will address the frequency limitation that currently constrains the business case. A constellation offering both the best resolution and daily revisit would be an extraordinarily compelling product for defense, intelligence, and commercial customers worldwide.

The Hanwha ecosystem multiplies the opportunity. With Hanwha Aerospace operating the Nuri rocket, Hanwha Systems developing defense communications satellites, and the group's broader defense procurement relationships spanning land systems, naval weapons, and aerospace, Satrec is embedded in a vertically integrated value chain that can capture opportunities across the full spectrum of space applications. The group's stated ambition to develop lunar lander propulsion systems and deploy a sovereign defense satellite constellation (the K-LEO program, in partnership with MDA Space and Telesat) creates additional adjacencies that Satrec can address with its satellite manufacturing expertise.

South Korea's expanding space budget provides a secular tailwind. The government has announced plans to double space spending by 2027, develop reusable launch vehicles, deploy ultra-high-resolution satellites, and pursue a moon landing by 2032. As the country's only proven satellite exporter and now a key component of the Hanwha Space Hub, Satrec is positioned as the primary domestic beneficiary of this spending increase. The lifting of missile development restrictions in 2021, which unlocked a $13 billion space power initiative, further expanded the addressable opportunity.

And then there is the international opportunity. The sovereign export model that built the company has been dormant in terms of revenue contribution, but the Etihad-SAT radar satellite partnership with the UAE, announced in 2025, signals a return to international business development with more sophisticated product offerings. The European leasing contract for SpaceEye-T capacity opens a new market in the West. If Satrec can rebuild international revenue to even 30 or 40 percent of total sales—well below the 66 percent peak—the revenue diversification alone would justify a higher multiple.

Key Performance Indicators to Watch

For investors tracking Satrec Initiative's evolution, two metrics matter more than any others.

First: the revenue mix between hardware and data/services. This is the single most important indicator of the company's transformation. As SIIS and SIA grow as a percentage of total revenue—from the current roughly 10-15 percent toward 30 percent and beyond—the market will be forced to reconsider what kind of company Satrec actually is. Watch this number quarterly.

Second: international revenue as a percentage of total sales. The collapse from 66 percent to below 10 percent represents the company's greatest vulnerability. A sustained recovery in this metric—driven by SpaceEye-T constellation sales, European leasing contracts, and new sovereign export partnerships—would signal that the business is diversifying away from its dangerous dependence on the South Korean government. This is the metric that separates a national champion from a global platform.

IX. Epilogue and Reflections

In 1989, when Dr. Soon-dal Choi sent a handful of KAIST students to the University of Surrey to learn how to build a satellite, he was not just investing in a space program. He was investing in a generation. Those students returned to Korea carrying something more valuable than technical drawings or component specifications. They carried the confidence that comes from having built something real—from having held a spacecraft in their hands, tested it, debugged it, and watched it survive the violent ascent into orbit. That confidence, transmitted from teacher to student across three decades, is the invisible thread that connects KITSAT-1's 48-kilogram frame to SpaceEye-T's 25-centimeter resolution.

The Satrec Initiative story challenges several comfortable assumptions about how technology companies succeed. It challenges the assumption that meaningful space companies can only emerge from the United States, Europe, or China—countries with massive government budgets and established aerospace industrial bases. South Korea had neither when SaTReC was founded in 1989. It challenges the assumption that you need venture capital or billionaire backing to build a space company. Satrec was bootstrapped from a university lab and grew on the proceeds of actual satellite contracts, not investor enthusiasm. And it challenges the assumption that "New Space" is a twenty-first-century phenomenon born in Silicon Valley. The philosophy of building small, capable, affordable satellites using commercial components and lean engineering teams was alive and well in Daejeon before most of today's space startups were even conceived.

What makes the Satrec story instructive for founders and investors alike is the concept of the cornered resource. In an industry where the barriers to entry are measured not just in capital but in decades of accumulated expertise, having a self-reinforcing talent pipeline—fed by one of the world's best science and technology universities, trained in a culture of extreme precision and accountability, and retained through meaningful equity participation—is an advantage that money alone cannot buy. Competitors can raise more capital, build bigger factories, and deploy larger marketing budgets. They cannot replicate thirty years of institutional knowledge in satellite systems engineering.

The open question—and it is a significant one—is whether Satrec can successfully navigate the transition from a hardware-centric business to a data-centric one while simultaneously rebuilding its international revenue base. The pieces are in place: the world's highest-resolution commercial optical satellite, a growing AI analytics capability, the financial and strategic backing of one of South Korea's largest conglomerates, and a domestic market that is expanding rapidly. The execution is what remains to be proven.

South Korea's space industry stands at an inflection point. The Nuri rocket is transitioning from government development to commercial operations under Hanwha Aerospace. The space budget is set to double. National ambitions now extend to the moon. At the center of this transformation sits a company that began as a university project, grew into a global exporter of sovereign space capability, and is now attempting to reinvent itself as an AI-driven intelligence platform. Whether that reinvention succeeds will determine whether Satrec Initiative remains a fascinating but niche Korean space company, or becomes the kind of global platform that defines an industry. The eye in the sky is watching. The question is whether investors are watching back.

X. Top 10 References for Further Reading

- KITSAT-1 and the Birth of Korean Space — KAIST SaTReC Archives and commemorative publications documenting South Korea's first satellite program.

- Hanwha's "Space Hub" Strategy and the Kim Dong-kwan Vision — Hanwha Group corporate communications and industry analysis of the conglomerate's vertical integration strategy.

- The Evolution of SmallSats: A 30-Year Retrospective — Surrey Space Centre and SSTL publications tracing the microsatellite revolution from UoSAT to modern constellations.

- SI Analytics: AI-Driven Geospatial Intelligence — Company publications and defense industry analyses of machine learning applications in Earth observation.

- Sovereign Space: Why Emerging Nations Buy Satellite Programs — Academic and industry research on the technology transfer model pioneered by Surrey, SSTL, and Satrec Initiative.

- The KAIST Satellite Technology Research Center (SaTReC) Heritage — University archives documenting the KITSAT series and the engineers who built them.

- Global Space M&A Benchmarking: 2018-2026 — Investment banking analyses comparing SPAC-era valuations with strategic acquisitions like Hanwha-Satrec.

- From Satellite Imagery to Geo-Intelligence: The Margin Delta — Industry research on the value chain economics of raw imagery versus processed intelligence products.

- South Korea's Nuri Rocket and National Space Ambitions — Government policy documents and Hanwha Aerospace disclosures on the KSLV-II commercialization program.

- 7 Powers: The Foundations of Business Strategy by Hamilton Helmer — The analytical framework for evaluating durable competitive advantages, applied throughout this analysis.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube