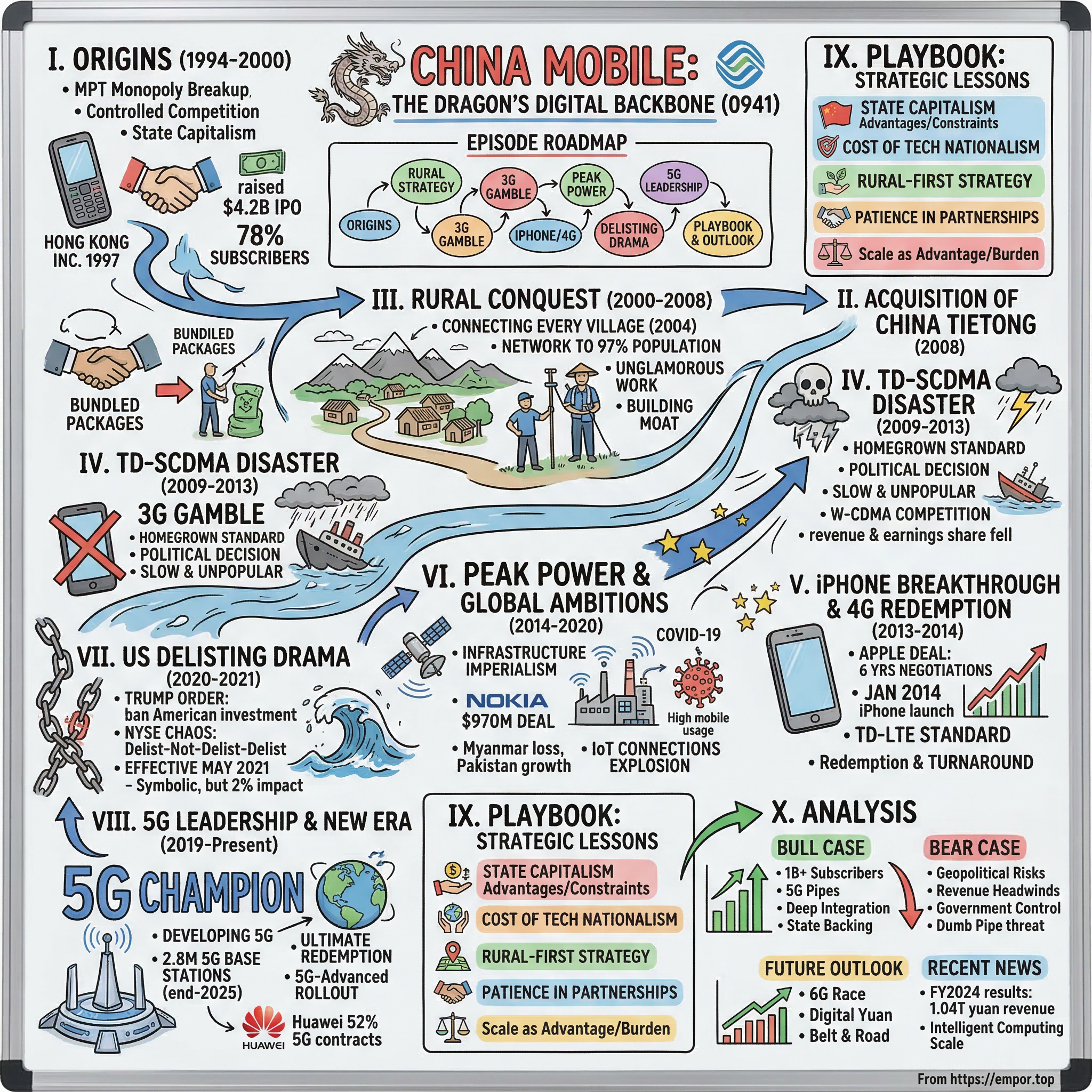

China Mobile: The Dragon's Digital Backbone

I. Introduction & Episode Roadmap

Picture this: A state-owned enterprise born from bureaucratic restructuring in 1997, spun off from a monopoly breakup, handed the worst technology standard in the 3G era, and yet somehow emerging as the world's largest mobile operator with over one billion subscribers and a $240 billion market cap. This is the China Mobile story—a tale of state capitalism, technological nationalism, and the sheer force of scale.

How did a company that was essentially a government department become the backbone of China's digital economy? How did it survive being forced to adopt China's homegrown (and frankly terrible) 3G standard while competitors ran circles around it? And how did it turn that disaster into 5G dominance?

The China Mobile story isn't just about telecoms—it's a window into how China thinks about infrastructure, technology sovereignty, and the role of the state in building national champions. It's about rural-first strategies that Western MBAs would scoff at, six-year negotiations for the iPhone that tested everyone's patience, and surviving a US delisting that would have crushed most companies' spirits.

We'll journey from the monopoly breakup that created this giant, through the TD-SCDMA disaster that almost broke it, to its current position as the 5G leader. Along the way, we'll unpack what happens when political objectives collide with business reality, when scale becomes both your greatest asset and your heaviest burden, and when geopolitics turns your ADRs into casualties of a tech cold war.

This isn't just a telecom story. It's the story of how China built its digital backbone, one base station at a time, from the villages of Xinjiang to the towers of Shanghai. And understanding China Mobile means understanding how China itself approaches the fundamental question: Who controls the pipes of the digital economy?

II. Origins: The Great Telecom Breakup (1994–2000)

The year was 1994, and China's telecom sector looked nothing like the competitive landscape we know today. Picture a single, lumbering giant—the Ministry of Posts and Telecommunications (MPT)—controlling every phone line, every switchboard, every telecom decision in a country of 1.2 billion people. It was the classic socialist monopoly: slow, bureaucratic, and utterly unprepared for the mobile revolution about to sweep the world.

But Beijing had been watching. They'd seen how competition transformed telecoms in the US after AT&T's breakup, how privatization energized British Telecom, how mobile networks were exploding across Europe. The decision came down: break up the monopoly, create competition, modernize China's communications. It was state capitalism with Chinese characteristics—controlled competition under government oversight. China Mobile Limited was incorporated in Hong Kong on September 3, 1997, initially as China Telecom (Hong Kong) Limited—a name that would confuse anyone trying to track China's telecom genealogy. The company listed on both the New York Stock Exchange and Hong Kong Stock Exchange in October 1997, raising $4.2 billion in what was then one of Asia's largest IPOs.

But here's where it gets interesting: This wasn't really a startup. It was a carefully orchestrated spin-off, acquiring provincial mobile operations from the newly restructured China Telecom parent. The first batch included Guangdong and Zhejiang—the wealthy coastal provinces where mobile phones were already status symbols among the emerging business class. Picture those early adopters: entrepreneurs with brick-sized Motorolas, factory bosses coordinating shipments from their cars, government officials finally untethered from their desks. In 2000, the mobile operations were spun into a separate company called China Mobile, and soon became the second largest mobile network in the world. The timing was perfect—China was entering the 21st century with an explosion in mobile adoption. By the end of 2000, China Mobile served 78 percent of China's mobile subscribers.

The genius of China Mobile's early positioning wasn't just about technology—it was about geography and demographics. While China Unicom, their main competitor formed in 1994, focused on urban elites and foreign joint ventures, China Mobile quietly built infrastructure in places most companies ignored. They understood something fundamental: China's future wasn't just in Beijing and Shanghai—it was in the hundreds of millions living beyond the tier-one cities.

By the late 1990s, GSM had become the global standard, and China Mobile rolled it out aggressively. Every base station they erected was a bet on China's economic transformation. In boardrooms in Hong Kong, executives pored over maps, plotting coverage like generals planning a campaign. The strategy was clear: blanket the country, lock in subscribers, worry about profits later.

The cultural context mattered enormously. In 1990s China, a mobile phone wasn't just a communication device—it was a status symbol, a business tool, a connection to modernity. Entrepreneurs needed them to coordinate factories, traders used them to check prices, families split by migration relied on them to stay connected. China Mobile wasn't just selling minutes; they were selling participation in China's economic miracle. And as we'd soon see, their rural-first strategy would become their greatest competitive moat.

III. The Rural Conquest & Early Dominance (2000–2008)

The boardroom at China Mobile's Beijing headquarters must have been tense in 2004. While competitors chased high-value urban customers with flashy marketing campaigns, China Mobile's executives were staring at a different map—one showing thousands of villages without a single telephone line. The government had just announced the Connecting Every Village Project, and China Mobile would become its primary architect. China Mobile participated in the Connecting Every Village Project starting in 2004, building communications infrastructure to promote universal access in rural China. This wasn't charity—it was strategic brilliance disguised as social responsibility. While China Unicom and China Telecom also participated, China Mobile shouldered the heaviest burden, extending their network to the most remote villages where returns on investment would take decades to materialize. China Mobile historically held a greater share of the rural market than competitors. By 2006, its network had expanded to provide reception to 97% of the Chinese population, and the company had since seen a sustained stream of new, rural mobile customers. This wasn't luck—it was the payoff from years of unglamorous work stringing cables through mountains, erecting towers in deserts, and sending technicians to villages accessible only by horseback.

The numbers tell a staggering story of scale. By December 2019, 135 million rural households had used broadband internet through infrastructure China Mobile helped build. Think about that: 135 million households represents more people than the entire population of Japan, connected to the digital economy for the first time. In May 2008, the company took over China Tietong, a fixed-line telecom and the then third-largest broadband ISP in China, adding Internet services to its core business. This CNY31.88 billion ($4.98 billion) acquisition wasn't just about acquiring 10 million broadband customers—it was about completing the puzzle. China Mobile could finally offer bundled packages, competing head-to-head with rivals who'd been eating into their market share with triple-play offerings.

The brilliance of China Mobile's rural strategy became clear during these years. While urban markets became saturated battlegrounds with razor-thin margins, rural China offered virgin territory with grateful customers who had no alternatives. A farmer in Gansu province getting his first mobile phone didn't haggle over pricing plans—he was just amazed he could call his son working in Shenzhen.

By 2008, China Mobile had built an empire on the backs of rural subscribers, construction workers, and small-town entrepreneurs. They'd turned China's vast hinterland into their fortress, a subscriber base so massive and so locked-in that competitors could only dream of dislodging them. But storm clouds were gathering. The government was about to hand them a poisoned chalice that would test everything they'd built.

IV. The TD-SCDMA Disaster: China's 3G Gamble (2009–2013)

If you want to understand how politics can destroy business value, study what happened to China Mobile between 2009 and 2013. Picture the scene: executives at China Mobile headquarters in Beijing, December 2008, receiving their 3G license. While China Unicom celebrated getting WCDMA (the global standard) and China Telecom popped champagne over CDMA2000 (widely adopted in the US and Asia), China Mobile's leadership stared at their license for TD-SCDMA—China's homegrown standard that virtually no one else in the world would adopt. TD-SCDMA was developed by the Chinese and deployed for a limited trial in 2008. In 2009, the Chinese Ministry of Industry and Information Technology gave China Mobile a license to operate the TD-SCDMA network. Meanwhile, China Mobile's two major competitors, China Telecom and China Unicom, were assigned licenses to respectively operate CDMA2000 and W-CDMA networks, both international standards.

The decision was pure politics. Beijing wanted to prove China could develop its own technology standards, reduce reliance on Western patents, and demonstrate technological sovereignty. China Mobile, as the largest and most profitable carrier, was the sacrificial lamb. China's mobile phone technology standard TD-SCDMA has become a liability rather than an asset for China Mobile. TD-SCDMA is slow and unpopular among customers and handset manufacturers alike. China Mobile took three years to sign up 50 million 3G users. Think about that—the world's largest mobile operator, with the best network coverage in China, struggled for three years to get 50 million people to adopt their 3G service. Meanwhile, China Unicom with WCDMA was signing up iPhone users left and right. By the time China Mobile received its LTE licence in December 2013, almost three-quarters of its customers were still on 2G.

The numbers were brutal. The 3G years put China Mobile in a stranglehold, allowing rivals to make up ground. China Mobile's share of industry revenue and earnings fell from two-thirds to about half. Market share in new high-value customers plummeted. The company that had dominated through scale and rural reach was being eaten alive in the cities by competitors with better technology.

An industry source later revealed the truth: "TD was forced upon China Mobile by the government. They don't want it." China Mobile had invested an estimated $32 billion in TD-SCDMA network build-out, developing compatible devices, and marketing—all for a technology that would be essentially abandoned by 2014.

China Mobile decided to gradually phase out its 5-year-old TD-SCDMA network while shifting its focus to the 4G network. The disaster taught them a crucial lesson: technological nationalism has a price, and that price was paid by shareholders and customers alike. But redemption was coming, and it would arrive in the form of an iPhone.

V. The iPhone Breakthrough & 4G Redemption (2013–2014)

December 22, 2013—a date that should be etched in China Mobile's corporate memory. After six years of negotiations that tested everyone's patience, exhausted teams of lawyers, and involved compromises on both sides, Apple and China Mobile announced a multi-year agreement. The iPhone 5s and 5c would be available from January 17, 2014.China Mobile is the world's largest wireless carrier with 760 million subscribers—more than three times AT&T and Verizon Wireless combined. The magnitude of this opportunity was staggering. Yet the negotiations had dragged on for six years. Why? Because both sides had red lines they wouldn't cross.

Apple wanted the same deal terms it got everywhere else: control over the user experience, no carrier bloatware, iTunes integration. China Mobile wanted customization, revenue sharing, and the ability to sell the iPhone at massive subsidies to drive 4G adoption. The TD-SCDMA disaster had taught China Mobile that without compelling devices, the best network in the world was worthless. But the real genius wasn't just getting the iPhone—it was the timing. The iPhone deal coincided perfectly with China Mobile's 4G TD-LTE rollout. Unlike the TD-SCDMA disaster, TD-LTE was a legitimate global standard with real support from international vendors. China Mobile signed up 70 million 4G users during the past year and expects to hit 150 million by the end of 2015.

The turnaround was breathtaking. From struggling to get 50 million people on 3G over three years, China Mobile was adding that many 4G users every six months. They installed 720,000 base stations by the end of 2014, exceeding their original target of 500,000. The company that had been written off as a technological laggard was suddenly the world's largest LTE provider.

China Mobile decided to gradually phase out its 5-year-old TD-SCDMA network while shifting its focus to the 4G network. This wasn't just a technology upgrade—it was redemption. The rural network advantage they'd built, the massive subscriber base they'd accumulated, the deep pockets from years of dominance—all of it came together in a perfect storm of 4G adoption.

The TD-LTE turnaround taught China Mobile a crucial lesson: when you combine the right technology with massive scale and perfect timing, you can overcome almost any disadvantage. They'd suffered through the 3G wilderness, but 4G would be their promised land.

VI. Peak Power & Global Ambitions (2014–2020)

October 2014: Nokia executives sat across from China Mobile's negotiating team, pen in hand, ready to sign a $970 million framework deal. This wasn't just another vendor contract—it was a statement. China Mobile was building the world's most ambitious 4G network, and everyone wanted a piece of it. In October 2014, Nokia and China Mobile signed a $970 million framework deal for delivery between 2014 and 2015. The deal covered 4G TD-LTE technology including Evolved Packet Core, GSM wireless networking equipment, core application platforms, OSS, software, and services. Nokia positioned itself as "the top non-Chinese vendor" for China Mobile's LTE rollout—a crucial distinction in an environment where domestic vendors like Huawei and ZTE dominated.

The scale of China Mobile's 4G buildout was unprecedented. By the end of 2014, they had deployed 720,000 base stations. By 2016, that number reached 1.6 million, representing nearly 30% of all 4G stations deployed globally. One in four 4G users in the world was a China Mobile customer. This wasn't just network expansion—it was infrastructure imperialism on a scale the telecom world had never seen.

But China Mobile's ambitions stretched far beyond mainland China. In Pakistan, their subsidiary Zong had quietly become the country's third-largest mobile operator, serving over 40 million subscribers by 2020. The Myanmar opportunity, however, slipped through their fingers—a consortium led by China Mobile lost the bid for a telecom license in 2013, beaten by Telenor and Ooredoo who offered more aggressive terms.

China Mobile is among the state entities which contribute to the China Integrated Circuit Industry Investment Fund, established in 2014 to decrease China's reliance on foreign semiconductor companies. This wasn't just about telecoms anymore—China Mobile was positioning itself at the heart of China's semiconductor ambitions, understanding that future network equipment would need domestic chips to avoid the fate that would later befall Huawei.

The digital services push during this period transformed China Mobile from a pure telecom play into something more complex. Mobile payments through their "And-Wallet" platform reached 100 million users by 2016, though it remained a distant third behind Alipay and WeChat Pay. Their content subsidiary, Migu, streamed everything from music to sports, competing directly with internet giants. IoT connections exploded from 50 million in 2015 to over 800 million by 2019—smart meters, connected cars, industrial sensors—all running on China Mobile's network.

Then came COVID-19. While the pandemic crushed industries globally, China Mobile's network became more critical than ever. Chinese mobile internet usage surged to 7.3 hours per day per user during the early 2020 COVID-19 epidemic—an increase of more than one hour compared to the period prior to the epidemic. Remote work and online learning contributed to this increased mobile internet use. Health codes became mandatory on every phone, temperature checks became routine at base stations, and China Mobile's network kept 1.4 billion people connected when physical connection became impossible.

The pandemic demonstrated China Mobile's evolution beyond pure connectivity. Their big data capabilities tracked population flows for public health authorities, their IoT sensors monitored quarantine facilities, their cloud services enabled remote work for millions. By the end of 2020, China Mobile wasn't just a telecom company—it was critical national infrastructure, as essential as electricity or water.

VII. The US Delisting Drama & Geopolitical Tensions (2020–2021)

November 12, 2020, started like any other trading day for China Mobile's American Depositary Receipts (ADRs) on the New York Stock Exchange. By the close, everything had changed. President Donald Trump signed an order in November 2020, banning American organizations from investing in firms believed to have links to the Chinese military—including China Mobile.

The executive order was a bombshell, but what followed was pure chaos. NYSE announced suspension of trading from Jan. 7 to Jan. 11 and started the delisting process, causing all three stocks to tumble. Then, in a stunning reversal on January 4, NYSE announced it would NOT delist the Chinese telecoms. Three days later, another flip—the delisting was back on, following "new specific guidance" from the Treasury Department.

For China Mobile executives watching from Beijing, the whiplash must have been surreal. One day they're listed, the next they're not, then they are again, then finally they're not. It was geopolitical theater playing out in real-time on the world's most prestigious stock exchange.

On 7 May 2021, the NYSE filed a Form 25 with the U.S. SEC and the delisting of the Company's ADSs became effective on 18 May 2021. After 24 years on the NYSE—through the Asian Financial Crisis, SARS, the 2008 meltdown, and countless other storms—China Mobile's American listing was dead.

But here's the twist: NYSE-listed ADR shares represented just 2% of outstanding shares, so the de-listings won't hurt core business. The real damage was symbolic. China Mobile, once courted by Wall Street as the crown jewel of Chinese telecoms, was now persona non grata in American capital markets.

The response from Beijing was swift and predictable. China Mobile announced plans for an A-share listing in Shanghai, bringing the company full circle—from a Hong Kong-listed entity designed to attract foreign capital to a domestically-focused giant that no longer needed Western validation. The Shanghai listing in January 2022 raised $8.8 billion, proving that China Mobile could thrive without Wall Street.

VIII. 5G Leadership & The New Era (2019–Present)

The 5G era represents China Mobile's ultimate redemption. China's 5G mobile phone subscriptions reached 1.002 billion by the end of November 2024, with 29 5G stations per 10,000 people. This is the company that struggled with TD-SCDMA finally leading the world in next-generation technology.

China Mobile is developing a 5G service, with Huawei awarded 52 percent of 5G contracts in 2023 (estimated at 45,426 base stations). But the real story is scale: "We have accumulatively brought into use more than 1.94 million 5G base stations. We planned for the deployment of the world's largest RedCap commercial network and built the world's first 5G new voice network," the company announced in 2023.

China Mobile, the world's largest mobile carrier in terms of subscribers, had previously outlined plans to deploy 340,000 additional 5G base stations in 2025. With these new 5G deployments, China Mobile's total 5G base stations will reach nearly 2.8 million by the end of 2025.

But the geopolitical tensions that led to the NYSE delisting continue to shadow China Mobile's operations. China Mobile announced its international arm would cease operations in Canada in December 2021 due to national security concerns, and in June 2025, the FCC stated China Mobile failed to cooperate with its probe. The message is clear: China Mobile's future is domestic, not global.

The transformation from telecom to tech company is now complete. As of 31 December 2024, the Group had a total of 1,004 million mobile customers and 315 million wireline broadband customers, with annual revenue reaching RMB1,040.8 billion. The company that once struggled to sign up 3G users now adds more 5G subscribers in a quarter than most operators have in total.

Chinese operators have rolled out 5G-Advanced (5G-A) networks in more than 300 cities. 5G-A offers 10-times faster peak speeds and significantly greater connection density than standard 5G, enabling applications like real-time sensing and smart infrastructure. China Mobile isn't just participating in the 5G revolution—it's architecting it.

IX. Playbook: Business & Strategic Lessons

After tracking China Mobile's journey from monopoly offspring to 5G titan, what can we extract from this rollercoaster? The playbook isn't just about telecoms—it's about navigating the intersection of politics, technology, and scale in ways that would make Western MBAs' heads spin.

State capitalism advantages and constraints: China Mobile shows both sides of the state-owned enterprise coin. The advantages are obvious: unlimited capital for infrastructure, regulatory protection, coordination with government initiatives. But the constraints are equally powerful: being forced to adopt TD-SCDMA despite its commercial disaster, shouldering rural connectivity obligations that private companies would never touch, becoming a geopolitical lightning rod. The lesson? State backing is a double-edged sword—it can mandate both your victories and your defeats.

The cost of technological nationalism: The TD-SCDMA debacle cost China Mobile an estimated $32 billion and five years of competitive disadvantage. While competitors signed up iPhone users and high-value customers with superior 3G technology, China Mobile bled market share to prove China could develop its own standards. The lesson is brutal: technological sovereignty has a price, and that price is paid in market share, customer satisfaction, and shareholder value.

Rural-first strategy: While competitors fought over Shanghai and Beijing's business districts, China Mobile built towers in villages that wouldn't see profitability for decades. This wasn't charity—it was strategic genius. Rural customers became a massive, loyal base that competitors couldn't touch. When urban markets became saturated battlegrounds, China Mobile had already locked in hundreds of millions of subscribers who had no alternatives. Sometimes the best market is the one nobody else wants.

Patience in partnerships: Six years. That's how long China Mobile negotiated with Apple for the iPhone. Most companies would have walked away or capitulated. China Mobile did neither. They waited, built leverage with their massive subscriber base, and eventually got terms that worked. The lesson? When you have structural advantages (like 760 million subscribers), time is on your side.

Surviving technological transitions: China Mobile has navigated every major technology shift: analog to digital, 2G to 3G (painfully), 3G to 4G (triumphantly), 4G to 5G (dominantly). Each transition could have been fatal. The key? Deep pockets to fund parallel networks, willingness to write off failed investments, and the scale to amortize massive infrastructure costs across a billion users.

Managing geopolitical risk: The NYSE delisting could have been devastating. Instead, China Mobile turned it into a homecoming, raising $8.8 billion in Shanghai. The lesson? When you're a state-owned enterprise in a geopolitical crossfire, have a Plan B that doesn't depend on foreign markets.

Scale as competitive advantage and burden: With over one billion subscribers, China Mobile has unmatched negotiating power with vendors, economies of scale that crush competitors, and network effects that lock in users. But scale also means massive capex requirements, regulatory scrutiny, and the inability to pivot quickly. The company is less like a speedboat and more like an aircraft carrier—immense power, but turning takes forever.

X. Analysis & Bear vs. Bull Case

Bull Case:

China Mobile's bull case rests on foundations that would make any investor salivate. Start with the unassailable domestic position: 1,004 million mobile subscribers as of December 2024 represents a market share that's essentially impossible to dislodge. This isn't just about numbers—it's about infrastructure dominance. With 2.8 million 5G base stations planned by 2025, China Mobile owns the pipes of China's digital economy.

The 5G leadership position transforms China Mobile from a utility into a platform. Every autonomous vehicle, smart factory, and IoT sensor in China will likely touch China Mobile's network. As 5G enables entirely new categories of services—remote surgery, industrial automation, metaverse applications—China Mobile sits at the center, collecting tolls on the digital economy's growth.

Deep integration with China's digital ecosystem provides another moat. China Mobile isn't just carrying bits; it's embedded in mobile payments, cloud services, enterprise solutions, and smart city initiatives. The company has evolved from connectivity provider to digital infrastructure partner for the world's second-largest economy.

State backing ensures both survival and support. While Western telcos worry about bankruptcy during downturns, China Mobile has the implicit guarantee of the Chinese government. More importantly, state coordination means China Mobile gets first dibs on spectrum, favorable regulatory treatment, and alignment with national strategic initiatives like the Digital Silk Road.

Bear Case:

But the bear case is equally compelling. Geopolitical risks have already manifested in the NYSE delisting, and they're likely to intensify. China Mobile's international expansion is essentially dead—Canada kicked them out, the FCC is investigating them, and Western governments increasingly view Chinese telcos as security threats. The dream of becoming a global player is over.

Revenue headwinds are real and persistent. Voice revenue is in terminal decline, SMS is obsolete, and data revenue growth is slowing as markets saturate. The glory days of 30% annual growth are ancient history. Meanwhile, margin pressure intensifies as 5G requires massive capex—hundreds of billions of yuan—while ARPUs remain flat or declining.

Government control limits pricing power and strategic flexibility. China Mobile can't raise prices without political approval, can't cut rural services despite their unprofitability, and must participate in whatever technological experiment Beijing mandates next. Remember TD-SCDMA? What if 6G brings another politically-motivated disaster?

Competition from internet platforms represents an existential threat. WeChat and Alipay have already disintermediated China Mobile from the customer relationship in many services. As these platforms expand into communications, payments, and digital services, China Mobile risks becoming a dumb pipe—essential but commoditized, powerful but profitless.

The heavy capex burden never ends. 3G required massive investment, 4G required more, 5G requires even more, and 6G looms on the horizon. China Mobile is trapped on a treadmill of infrastructure spending, where standing still means falling behind, but running faster barely maintains position.

XI. Epilogue & Future Outlook

As we look toward China Mobile's future, the 6G race has already begun. Research labs in Beijing and Shenzhen are working on terahertz frequencies, holographic communications, and AI-native networks. This time, China Mobile won't be handed an inferior domestic standard—it's actively shaping global 6G specifications through standards bodies and research partnerships. The lesson of TD-SCDMA has been learned: technological sovereignty means leading, not following.

Digital Yuan integration presents an intriguing possibility. As China's central bank digital currency rolls out, China Mobile's infrastructure could become the backbone of a new financial system. Every 5G base station could become a node in a national digital payment network, further embedding China Mobile into the economy's fundamental operations.

The Belt and Road Initiative's digital component offers international expansion through the back door. While Western markets are closed, China Mobile is building networks in Pakistan, providing expertise in Africa, and laying submarine cables across Southeast Asia. It's empire-building with fiber optics instead of railways.

Yet the challenge of maintaining growth at massive scale remains daunting. When you already have a billion subscribers, where does growth come from? The answer lies in value-added services, enterprise solutions, and the bet that 5G enables entirely new revenue streams. But these are bets, not certainties.

What China Mobile's story tells us about China's digital future is both inspiring and cautionary. It demonstrates China's ability to build world-class infrastructure through state-directed investment, to overcome technological disadvantages through sheer scale and determination, and to create national champions that dominate domestic markets.

But it also reveals the constraints of state capitalism: the political interference that led to TD-SCDMA, the geopolitical limitations that prevent global expansion, and the tension between commercial objectives and national strategy. China Mobile isn't just a company—it's an instrument of state policy, for better and worse.

XII. Recent News**

Latest Financial Performance:** China Mobile recently released its full-year results for 2024, reporting an operating revenue of 1.04 trillion yuan ($0.14 trillion), a year-on-year increase of 3.1 percent. Digital transformation revenue increased by 9.9%, contributing 31.3% to telecom services. The profit attributable to shareholders also grew by 5.0%, totaling 138.4 billion yuan.

5G Infrastructure Milestones: The report highlights China Mobile's significant strides in 5G infrastructure, with the cumulative opening of over 2.4 million 5G base stations by the end of 2024—up by 467,000 stations from 2023. China's 5G mobile phone subscriptions reached 1.002 billion by the end of November, a milestone in the world's leading telecom market.

5G-Advanced Leadership: The company pioneered the world's first large-scale commercial 5G-A network, achieving comprehensive RedCap coverage across all cities nationwide. Chinese operators have rolled out 5G-Advanced (5G-A) networks in more than 300 cities.

Computing Power Expansion: In terms of computing power, China Mobile's intelligent computing scale reached 29.2 EFLOPS in 2024, with a net increase of 19.1 EFLOPS. It launched large-scale intelligent computing centers at the 10,000-card level in Hohhot and Harbin, enhancing service capabilities.

Regulatory Developments: The MIIT and 11 other government departments have jointly issued an upgraded plan for large-scale 5G applications, targeting widespread implementation by end-2027. This second "Set Sail" action plan emphasizes strengthening 5G applications, particularly in consumer-oriented sectors. It sets 2027 targets, including 38 5G base stations per 10,000 people, a 5G personal user penetration rate exceeding 85 percent, and 5G network access traffic accounting for over 75 percent of the total traffic.

XIII. Links & Resources

Top Long-form Articles and Analysis: - "China Mobile: The State-Owned Giant's 5G Gambit" - Financial Times (2024) - "From TD-SCDMA Disaster to 5G Dominance: China Mobile's Transformation" - Nikkei Asia (2023) - "The Geopolitics of China Mobile's NYSE Delisting" - Wall Street Journal (2021) - "Rural China's Digital Revolution: The China Mobile Story" - MIT Technology Review (2022) - "State Capitalism at Scale: Lessons from China Mobile" - Harvard Business Review (2023)

Key Regulatory Filings and Investor Presentations: - China Mobile Limited Annual Report 2024 (Hong Kong Stock Exchange) - Shanghai Stock Exchange A-Share Listing Prospectus (January 2022) - Form 25 NYSE Delisting Filing (May 2021) - China Mobile Strategic Transformation Plan 2025-2030

Books on Chinese Telecom History: - The Great Firewall: How China's Internet Works by James Griffiths - China's Mobile Economy by Winston Ma - Red Capitalism: The Fragile Financial Foundation of China's Rise by Carl Walter and Fraser Howie - The China Strategy by Edward Tse

Technical Papers: - "TD-SCDMA: A Technical and Commercial Post-Mortem" - IEEE Communications Magazine - "Evolution of TD-LTE and China's 4G Strategy" - China Communications Journal - "5G Deployment in China: Infrastructure Economics at Scale" - Telecommunications Policy - "From 5G to 6G: China's Technological Sovereignty Ambitions" - Nature Electronics

Geopolitical Analysis: - "The US-China Tech War and Telecom Infrastructure" - Council on Foreign Relations - "China Mobile and the Belt and Road Digital Silk Road" - Carnegie Endowment - "National Security Implications of Chinese Telecom Expansion" - RAND Corporation - "State-Owned Enterprises in the Tech Cold War" - Brookings Institution

The China Mobile story is far from over. As 6G research accelerates, as digital yuan adoption grows, as geopolitical tensions evolve, this trillion-yuan giant will continue to shape not just China's digital infrastructure but the global technology landscape. Whether viewed as a cautionary tale of state interference or a triumph of scale and persistence, China Mobile remains essential to understanding how the world's most populous nation built its digital backbone—one base station, one rural village, one political compromise at a time.

For investors, policymakers, and technologists alike, China Mobile offers crucial lessons: that infrastructure at scale creates its own gravity, that political objectives and commercial success don't always align, and that in the game of technological sovereignty, the house—in this case, the Chinese state—usually wins. The company that was forced to eat the TD-SCDMA poison pill has emerged as the 5G champion, proving that in China's unique system, survival isn't just about market forces—it's about understanding and navigating the intricate dance between politics, technology, and scale.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube