China Construction Bank: Financing the Chinese Century

I. Introduction & Episode Thesis

Picture the trading floor reaction. A portfolio manager pulls up CCB's 2025 results: net profit of RMB 339.79 billion — call it RMB 340 billion, up a barely-there 1.04% — on a return on equity of 10.04%.[^1] The bank paid out RMB 101.68 billion in dividends, a 30% payout, offering a yield in the neighborhood of 5.5% to 6%.1 The capital adequacy ratio was a fortress-like 19.69%.[^1] By any Western yardstick, this is a systemically important, hugely profitable, over-capitalized bank. So why did it trade at roughly 0.4 times book value — the price you assign to a business the market believes is quietly destroying capital?

The short answer is the "policy discount," and understanding it is the whole point of this story. CCB is not run the way JPMorgan is run. It is majority-owned, through 中央汇金投资 Central Huijin Investment, by the Chinese state.7 When Beijing wants mortgage rates cut to relieve homeowners, CCB cuts them. When local governments need their debts rolled over for another twenty years, CCB rolls them. The bank is simultaneously a commercial enterprise answerable to minority shareholders in Hong Kong and an instrument of national economic policy answerable to the Party. Those two masters do not always want the same thing, and the gap between them is exactly what the discount is pricing.

Our core thesis is this: China Construction Bank is the clearest financial mirror of modern China that exists. It is the physical embodiment of the country's infrastructure-led growth model — the highways, the high-speed rail, the port cities that rose from rice paddies — and of the residential property boom that turned a generation of Chinese households into homeowners and CCB into the dominant mortgage lender in the world. Now, as China deliberately transitions away from debt-fueled expansion toward what the leadership calls "high-quality growth," CCB is being forced to reinvent the very engine that made it enormous.

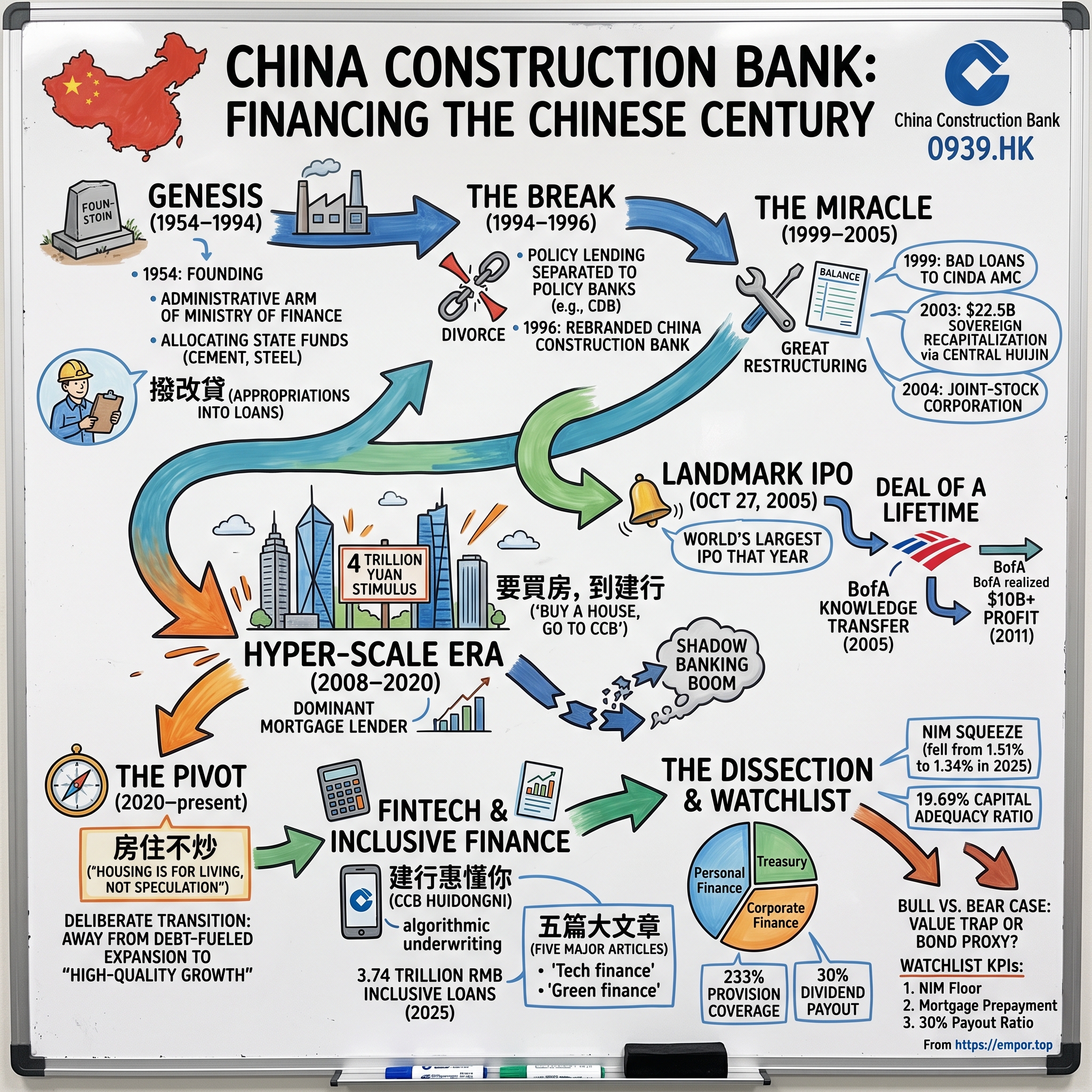

Here is the roadmap for how we get there. We start with the genesis — a bank that wasn't a bank, tracking tons of steel instead of credit risk. We move to the joint-stock miracle, the astonishing 2004 rescue in which the state recapitalized a functionally insolvent banking system and floated it, leading to the landmark 2005 Hong Kong IPO. We examine the deal of a lifetime — Bank of America's strategic investment and its multi-billion-dollar exit, one of the great bank trades in history. We chronicle the hyper-scale era — the four-trillion-yuan stimulus, the shadow banking boom, and the mortgage frenzy. We turn to the pivot — how CCB is trying to convert regulatory obligation into genuine competitive advantage through platforms like 建行惠懂你 CCB Huidongni. We dissect the numbers — the segments, the net interest margin squeeze, the high-dividend case. And we close with the question every investor eventually asks about this stock: is CCB a value trap, or a high-yielding, state-backed bond proxy hiding in plain sight?

To answer that, we have to go back to a country that had just finished a revolution and had almost no capital at all.

II. The Genesis: Managing State Capital (1954–1994)

On October 1, 1954 — five years to the day after Mao Zedong declared the founding of the People's Republic from the gate of Tiananmen — a new institution opened its doors under the name the People's Construction Bank of China. It is tempting to imagine tellers and vaults and passbooks. There were none of those things, at least not in any sense a modern banker would recognize. The People's Construction Bank was not, in the capitalist meaning of the word, a bank at all. It was an administrative arm of the Ministry of Finance, and its job was to allocate money the state had already decided to spend.

Consider what China was in 1954. It was a poor, largely agrarian country attempting, with Soviet advisers at its elbow, to build heavy industry from almost nothing under the First Five-Year Plan. Steel mills, coal mines, rail lines, hydroelectric dams — the sinews of an industrial economy — had to be financed. But there was no market to set prices, no risk to be assessed, no return on equity to be earned. Instead, the central plan decided which projects would be built, and the People's Construction Bank made sure the budgeted funds flowed to them and that the money was spent on what it was supposed to be spent on. Its officers were, in effect, government auditors of the physical world.

Engineers, not loan officers

This is the crucial thing to hold in your mind, because its residue lingers in CCB's DNA to this day. The people who staffed the early Construction Bank were engineers and bureaucrats, not credit analysts. Their metrics were physical: tons of steel poured, kilometers of railway laid, cubic meters of concrete set. The concept of a "non-performing loan" was literally meaningless, because these were not loans — they were budgetary appropriations, gifts from the state to state-owned enterprises building state-owned assets. Nobody was expected to pay anything back. The Construction Bank tracked whether the cement arrived, not whether the borrower could service the debt.

For twenty-five years, this was the entire business model: a disbursement and supervision agency for capital construction under central planning. It made the institution deeply competent at one thing — understanding infrastructure and construction projects at a granular, physical level — and completely innocent of the discipline that defines commercial banking: pricing and bearing risk.

The bend in the river: 拨改贷

Then came 邓小平 Deng Xiaoping and the reforms that began in 1978. The whole logic of the Chinese economy started to shift, and one dry piece of financial plumbing captured the change perfectly. It was called 拨改贷 — literally, "changing appropriations into loans." Beginning in the early 1980s, the state decided that infrastructure projects should no longer be handed free money from the budget. Instead, they would receive interest-bearing loans that were, at least on paper, supposed to be repaid.

For the Construction Bank, this was a profound identity crisis dressed up as a policy tweak. Overnight, it was told to behave like a commercial lender — to book loans, to expect repayment, to think about return. But it was still being directed to fund the same politically chosen projects, many of which had no commercial viability whatsoever. A dam built for regional development or a factory built to guarantee local employment does not generate the cash flows to repay a market-rate loan. The Construction Bank was being asked to run a lending book while having almost no ability to say no to bad loans. The seeds of the crisis to come were planted right here.

The 1994 divorce

By the early 1990s, Beijing understood it had created an untenable hybrid: state banks stuffed with policy loans that would never be repaid, dressed up as commercial institutions. The solution, in 1994, was a divorce. The government created a set of dedicated "policy banks" — most importantly 国家开发银行 China Development Bank — to take over the explicitly policy-directed, non-commercial infrastructure lending.9 This was meant to cleave the good from the bad: let the policy banks carry the mandate lending, and free the Construction Bank to become a genuine commercial bank competing for deposits and making loans on their merits.

Two years later, in 1996, the institution formalized its new ambition by dropping "People's" from its name and becoming, simply, China Construction Bank.9 The rebrand signaled intent. But intent is not the same as a clean balance sheet. The divorce of 1994 had drawn a line between future policy lending and future commercial lending — it had done nothing about the mountain of dead loans already sitting on the books from decades of 拨改贷 mandates. That mountain was about to reveal just how large it truly was, and the reckoning would nearly break the entire Chinese banking system.

III. The Great Restructuring: Functional Insolvency to HKSE IPO (1994–2005)

In the late 1990s, if you had opened the books of China's "Big Four" state commercial banks — CCB alongside 中国工商银行 ICBC, 中国农业银行 ABC, and 中国银行 Bank of China — and applied honest international accounting standards, you would have reached a conclusion the Chinese government could not afford to state out loud: they were insolvent. Not troubled. Not undercapitalized. Insolvent.

The rot was in the loan book. Decades of directed lending to dying state-owned enterprises — loans made not because the borrower could repay but because a factory had to keep its workers employed — had produced non-performing loan ratios that outside economists estimated at somewhere between 30% and 40% of the entire system.11 Think about what that means. For every three yuan a bank had lent out, perhaps one was simply never coming back. In any market economy, banks with holes that size collapse, depositors panic, and the contagion spreads. China had no deposit insurance, no experience managing a banking crisis, and a population that kept its life savings almost entirely in these banks.

So the crisis stayed silent. The government's implicit guarantee — everyone knew Beijing stood behind the Big Four — kept depositors calm even as the institutions were, by the numbers, underwater. But silence is not a solution. To bring these banks to the point where they could raise capital from foreign investors and stand on their own, the state had to actually fix the balance sheets. What followed was one of the most consequential financial engineering exercises of the modern era, executed in three moves.

Move one: build the bad banks (1999)

In 1999, the government created four Asset Management Companies — "bad banks" — each paired with one of the Big Four. CCB's designated partner was 中国信达 China Cinda Asset Management, the very first of the four to be established.8 The mechanism was elegant in its simplicity. Cinda bought CCB's worst loans and took them off CCB's balance sheet, paying with bonds rather than cash. The toxic assets — an estimated RMB 373 billion of them over the restructuring — moved to Cinda, whose entire job was to spend years grinding through the wreckage, recovering whatever pennies on the yuan it could.812 CCB's balance sheet got dramatically cleaner; the losses did not vanish, they were simply parked in a state-owned vehicle where they would not threaten the banking system.

Move two: the sovereign recapitalization (2003–2004)

Cleaning out the bad loans left a hole where capital should be. Filling it required real money, and here the state reached for its most prized resource: its foreign exchange reserves. In late 2003, Beijing created 中央汇金投资 Central Huijin Investment — a state holding vehicle designed to act as the controlling shareholder of the recapitalized banks — and used it to inject roughly $22.5 billion of forex reserves directly into CCB's capital base.712 In one stroke, CCB went from functionally insolvent to comfortably capitalized, and Central Huijin became its dominant owner, a position that endures to this day and explains much of the "policy discount" we will return to.

Move three: become a corporation (2004)

Money alone does not make a modern bank. In 2004, CCB was reorganized from a bureaucratic state agency into a joint-stock corporation with the trappings of governance that international investors demand: a board of directors, a genuine risk-management function, and international auditors in the form of PricewaterhouseCoopers.[^13] The goal was to graft the discipline of commercial banking onto an institution whose entire history had trained it to disburse funds rather than price risk. Whether that graft fully took is a question the rest of this story keeps asking.

The debut: October 27, 2005

With a clean balance sheet, fresh capital, and a corporate structure, CCB did what none of its Big Four siblings had yet dared. On October 27, 2005, it listed on the Hong Kong Stock Exchange under the ticker 0939.HK, raising approximately $9.2 billion.34 It was the largest IPO anywhere in the world that year and the biggest financial-sector flotation in history to that point.3 The symbolism dwarfed even the dollars. A bank that had spent its first four decades allocating cement under a command economy was now selling shares to global investors in the freest capital market in Asia. For Beijing, it was proof of concept: the Chinese state-bank model could be scrubbed, recapitalized, and sold to the world.

But CCB did not walk onto that stage alone. Standing beside it was one of America's largest banks, holding a stake it had bought just months earlier — a bet that would become one of the most profitable trades in banking history.

IV. The Deal of a Lifetime: The BofA Strategic Alliance & Cross-Border Expansion

In the summer of 2005, months before the IPO, Bank of America wrote a check for $3 billion and bought roughly 9% of China Construction Bank, with an option to build toward nearly 20%.4 On its face, it was a capital injection that helped anchor the flotation. In reality, it was two things at once — a technology-transfer partnership and a financial call option on the rise of China — and both paid off spectacularly, though for very different reasons.

The knowledge transfer

The part that mattered to CCB in 2005 was not the money; the state had already recapitalized the bank. It was the expertise. Bank of America, then a titan of American retail banking, sent teams to train thousands of CCB employees in the disciplines the Construction Bank had never needed to learn: consumer credit scoring, retail branch management, risk modeling, corporate governance, product design. For an institution whose staff had spent generations counting tons of steel, this was a crash course in how a modern consumer bank actually runs. The strategic logic for BofA was equally clear — a seat at the table of the fastest-growing large economy on earth, and a window into a banking market it could never have entered on its own.

The arbitrage of the century

Then history intervened, and the alliance turned into something neither party had scripted. When the Global Financial Crisis tore through Bank of America's own balance sheet between 2008 and 2011 — the disastrous Countrywide and Merrill Lynch acquisitions, the mounting losses, the desperate need for capital — its CCB stake transformed from a strategic partnership into an emergency liquidity reserve. BofA sold down its holding in stages, and the gains were enormous. In a single 2011 transaction alone, it agreed to sell roughly 13.1 billion CCB shares for about $8.3 billion in cash, booking an after-tax gain of around $3.3 billion — capital it desperately needed to shore up its Basel ratios at the worst possible moment.5 Across all its staged exits, BofA realized well over $10 billion in cumulative profit on an initial $3 billion outlay.

The lesson for investors is worth sitting with. Bank of America made more money buying and selling a piece of a Chinese bank during the boom years than it did from vast swaths of its domestic franchise — and it did so precisely because the crisis forced its hand at a time when the Chinese banks were still riding the up escalator. It was the right trade for the wrong reason, monetized under duress. For CCB, the partner's exit was not a rejection; it was simply an American bank taking its winnings home. The knowledge had already been transferred, and CCB kept it.

Planting a flag in Hong Kong

The alliance flowed in both directions. On August 24, 2006, CCB agreed to acquire 100% of Bank of America (Asia) — BofA's Hong Kong and Macau retail operation — for HK$9.71 billion, roughly $1.25 billion.[^8]6 The bank was rebranded 中国建设银行(亚洲) China Construction Bank (Asia) and became CCB's offshore beachhead.

Did CCB overpay? The discipline is in the multiple. The price represented about 1.3 times the unit's book net assets of HK$7.38 billion — a restrained figure at a moment when other Hong Kong bank acquisitions were changing hands at 1.5 to 2 times book.[^8]6 For a Chinese state bank flush with IPO proceeds and eager to plant a flag on foreign soil, paying a below-market multiple for an established retail franchise was a genuinely disciplined move, and it instantly handed CCB a ready-made platform in Hong Kong from which to build its offshore treasury and wealth business. It is one of the cleaner strategic acquisitions in the group's history, and a useful counterpoint to the narrative that Chinese state banks simply overpay for trophies.

With capital raised, expertise absorbed, and an offshore footprint secured, CCB entered the next decade at full sprint. What followed was not disciplined growth. It was the most explosive balance-sheet expansion the banking world had ever seen.

V. The Era of Hyper-Scale: GFC, Shadow Banking, and Property Boom (2008–2020)

In November 2008, as the Global Financial Crisis vaporized demand across the Western world and China's export orders collapsed overnight, Beijing did something that would reshape the global economy and CCB's balance sheet for the next fifteen years. It announced a stimulus package of four trillion yuan — and then, crucially, told the banks to lend. The headline number was the government's; the real firepower came from the credit the state banks were instructed to unleash on top of it.

CCB was born for this moment. No bank in China had deeper institutional memory of infrastructure and construction — it was, after all, the reason the bank existed. When the order came to fund highways, high-speed rail, airports, subway systems, and property developments, CCB's loan book went vertical. This was the hyper-scale era, and it is when the bank became the giant we know today. Balance-sheet growth stopped being incremental and became exponential, financed by the vast, cheap, sticky deposit base that Chinese households — with few other places to put their savings — kept pouring into the Big Four.

"要买房,到建行"

If corporate infrastructure lending built CCB's scale, it was the Chinese homeowner who built its profitability. Over the 2010s, CCB established itself as the undisputed leader in residential mortgages in China, marketing itself with a slogan that became genuinely famous: 要买房,到建行 — "If you want to buy a house, go to CCB." As hundreds of millions of Chinese citizens moved from rural areas into cities and from renting into owning, CCB captured the single largest asset on the middle-class balance sheet: the family mortgage.

Why did this matter so much? Because mortgages, in the China of the 2010s, were close to a perfect banking product. They were enormous in aggregate — trillions of RMB. They were high-margin, priced comfortably above the bank's near-zero cost of deposits. And above all they were stable: Chinese households treated repaying the mortgage as a near-sacred obligation, default rates were minuscule, and a cultural preference for large down payments meant the loans were deeply collateralized. CCB accumulated a mortgage book that was, for a decade, arguably the highest-quality large pool of consumer credit anywhere on earth. This is the crown jewel whose slow erosion we will examine later — but in this era, it was pure gold.

The shadow banking maze

Not all of the era's lending was so wholesome. Between roughly 2013 and 2018, Chinese banks confronted a problem: regulators capped how much they could lend and imposed quotas on where credit could flow, but the demand for credit — from property developers, local governments, and speculative ventures — was insatiable. The banks' answer was to route money around the rules. Credit was repackaged into off-balance-sheet Wealth Management Products (WMPs) and channeled through trust companies and interbank structures, creating a vast "shadow banking" system where risk migrated into the dark corners of the financial plumbing, invisible to the official loan statistics.

The reckoning came when regulators finally decided the shadow system had become a systemic threat. The newly consolidated banking and insurance regulator, the CBIRC, under the forceful 郭树清 Guo Shuqing, launched a sweeping crackdown, forcing banks to drag hidden assets back onto their balance sheets and account for them honestly. Here CCB's conservative institutional temperament served it comparatively well. It had leaned into WMPs less aggressively than some peers and smaller joint-stock banks, so the process of re-absorbing shadow assets was less traumatic, and it emerged with capital adequacy still comfortably above requirements. The episode is a recurring theme in the CCB story: as a Big Four incumbent with a bottomless deposit base, it rarely needs to reach for the riskiest sources of growth, and that structural comfort tends to show up as relative stability when the cycle turns.

By 2020, CCB stood as one of the largest and best-capitalized banks in history. But the twin engines that had powered the hyper-scale decade — infrastructure and property — were both running out of road. The property boom was about to become a property crisis, and CCB would have to find an entirely new story to tell.

VI. The Pivot to High-Quality & Fintech: The "Huidongni" Powerhouse

The turning point had a slogan too, and it was the opposite of "go buy a house." Beginning in 2016 and hardening into unbreakable policy by the end of the decade, the leadership declared that 房住不炒 — "housing is for living in, not for speculation." Read plainly, it was a directive to deflate the very property bubble that CCB's mortgage machine had spent a decade inflating. When the property developer 恒大 Evergrande began its slow-motion collapse and home prices in many cities stopped rising, the message was unmistakable: the old growth engine was being switched off on purpose.

For CCB, this was existential in a quiet way. If mortgages and property-linked lending could no longer be the primary source of growth and margin, where would the next decade of earnings come from? The state's answer arrived in the form of a strategic to-do list.

The "五篇大文章"

Chinese financial policy is often communicated through numbered lists, and the framework now governing CCB's strategic direction is the 五篇大文章 — the "five major articles" of finance. Each represents a national priority the banks are expected to serve, and together they define what "high-quality growth" is supposed to look like inside a bank:

- Tech finance (

科技金融) — lending to advanced manufacturing, semiconductors, and the hard-technology sectors Beijing wants to nurture as it seeks self-sufficiency. - Green finance (

绿色金融) — funding solar, wind, and carbon-reduction projects in service of China's双碳 dual carbon goals. - Inclusive finance (

普惠金融) — reaching the micro and small enterprises historically starved of bank credit. - Pension finance (

养老金融) — building products for a country whose demographics are aging faster than almost any in history. - Digital finance (

数字金融) — using technology to serve customers more cheaply and efficiently.

It would be easy to dismiss this as a bureaucratic wish list — obligations imposed from above that dilute returns. And an independent investor should hold exactly that skepticism, because much national-service lending genuinely is low-margin. But CCB's most interesting move of the past decade was taking one of these obligations and trying to turn it into a weapon.

Huidongni: turning a chore into a moat

Historically, lending to micro and small enterprises was every big bank's least favorite activity. The loans were tiny, the borrowers had no audited financials or collateral, the credit risk was opaque, and the cost of manually underwriting each one dwarfed the interest earned. Inclusive finance was, in short, a money-losing regulatory chore. CCB's bet was that technology could invert that math.

The vehicle is 建行惠懂你 CCB Huidongni, a mobile platform that underwrites small-business loans not by sending a loan officer to inspect a shop, but by ingesting data: a company's tax records, its transaction and payment histories, its supply-chain relationships. The system scores the borrower algorithmically and can approve and disburse a working-capital loan in minutes rather than weeks. The unit cost of a loan collapses; the same platform that serves one borrower serves ten million at almost no incremental cost.

The scale it has reached is genuinely material, not cosmetic. By mid-2025, CCB's inclusive-finance loan balance to micro and small enterprises stood at RMB 3.74 trillion across 3.66 million borrowers, and by year-end 2025 it had climbed to RMB 3.83 trillion — well over a tenth of the entire loan book.[^4]1 That is no longer a compliance line item; it is one of the largest small-business lending operations in the world.

Here is the analytical point, stated neutrally. Whether Huidongni is a durable competitive advantage or simply a subsidized volume machine depends on a question the disclosures do not fully answer: are these loans actually profitable after credit losses across a full economic cycle, or does their attractive pricing rest on state direction and cheap funding? The bull reading is that CCB has converted a regulatory obligation into a low-cost, data-driven distribution moat that smaller regional banks — which lack the deposit base, the data, and the technology budget — cannot match, thereby defending CCB's cheap funding against nimbler competitors. The bear reading is that inclusive finance concentrates exposure to exactly the borrowers most vulnerable in a downturn, and that the true loss experience will only be visible after the current cycle fully turns. Both can be partly true. What is not in dispute is that CCB has made this platform central to its post-property identity.

That identity now has to prove itself in the numbers — and the numbers, as of 2025, tell a story of a bank running hard just to stand still.

VII. Dissecting the Balance Sheet: Segment Earnings & The NIM Squeeze

Strip away the slogans and the strategic frameworks, and a bank is ultimately an arithmetic machine: it borrows money cheaply, lends it out at a higher rate, and tries to keep the losses small. In 2025, that machine produced RMB 339.79 billion in net profit for CCB — a rounding error above the prior year, up just 1.04% — on operating income of RMB 740.87 billion.[^1] For an institution this size, near-flat earnings are not a failure; in the context of collapsing lending margins and a property hangover, holding profit roughly flat was itself an achievement. But it is an achievement built on visibly narrowing foundations, and the segment map shows where the weight sits.

Where the profit comes from

CCB reports its pre-tax profit across four segments, and the mix is revealing.[^13] Personal finance — retail banking, home to that legendary mortgage book and the fast-growing wealth-management business — remains the crown jewel, contributing the largest share of pre-tax profit at roughly RMB 154.6 billion, on the order of 40% of the total. Treasury and asset management, the bank's markets and proprietary investment operation, is the surprising number two at around RMB 127.8 billion, roughly a third of profit — a reminder that in an era of interest-rate volatility, a bank this large earns serious money simply managing its own vast pool of assets and liabilities. Corporate finance — the historic heart of the Construction Bank, the infrastructure and SOE lending — has been squeezed down to about RMB 84.5 billion, roughly 22%, its low-yielding loans and debt-restructuring drag eroding what was once the core. A residual "others" category rounds out the rest.[^13]

The story the segments tell is a bank in transition. The business the Construction Bank was literally founded to do — corporate infrastructure lending — is now its most margin-pressured segment, while the consumer franchise it had to learn from Bank of America is its profit engine. The institution has, in a real sense, inverted its own DNA.

The single most important number: NIM

If you track only one metric on CCB, make it the net interest margin — NIM — and in 2025 it flashed red. NIM measures the spread between what the bank earns on its assets and what it pays for its funding, and CCB's fell from 1.51% in 2024 to 1.34% in 2025.[^1] Seventeen basis points may sound trivial. On an asset base above RMB 45 trillion, it is anything but — it is the difference that turned what should have been solid earnings growth into a near-flat result.

The mechanism is worth explaining simply, because it is the crux of the entire bear case. Imagine the bank as a business with two prices: the rate it charges borrowers and the rate it pays savers. To stimulate a slowing economy, the People's Bank of China — 中国人民银行 PBOC — repeatedly cut the benchmark Loan Prime Rate, and CCB was required to pass those cuts through, even repricing the interest on mortgages households had already taken out. The asset side of the ledger, in other words, kept getting cheaper by decree. Meanwhile the liability side proved stubborn: depositors, spooked by falling property values and a weak stock market, competed for the safety of bank deposits and resisted accepting much lower rates on their savings. Asset yields fell faster than funding costs, and the spread — the bank's oxygen — thinned. Deposit rates are "sticky" precisely when a bank most needs them to fall.

The fortress that offsets the squeeze

Against that margin erosion, CCB set a genuinely formidable balance-sheet fortress. Its total capital adequacy ratio stood at 19.69% — capital far in excess of regulatory minimums — with core Tier 1 capital at 14.63%.[^1] Its reported non-performing loan ratio was 1.31%, and, most tellingly, it carried a provision coverage ratio of 233.15%, meaning it had set aside more than two yuan of loss reserves for every yuan of loans it classified as bad.[^1]

An independent reading holds two thoughts at once. First, this is real strength: a bank this well-provisioned and well-capitalized has enormous capacity to absorb losses without threatening its dividend or its solvency, which is the foundation of the "bond proxy" bull case. Second, the reported NPL ratio deserves professional skepticism. In a system where banks are routinely directed to extend and refinance the debts of local-government financing vehicles rather than classify them as non-performing, a headline 1.31% almost certainly understates the true stress hiding in the corporate and local-government book. The heavy provisioning can be read two ways: as prudent conservatism, or as a quiet acknowledgment that the reported NPL number is not the whole story. Both readings coexist in the market's 0.4-times-book valuation.

Understanding those competing readings requires stepping back from the income statement and asking a structural question: what, exactly, protects a bank like CCB — and what does not?

VIII. Playbook: The 7 Powers of the Big Four Incumbent

Hamilton Helmer's "7 Powers" framework asks a deceptively simple question about any business: what is the source of persistent differential returns that a competitor cannot easily copy? Applied to CCB, the exercise is illuminating precisely because it separates the powers that are real and durable from the ones that are, on closer inspection, borrowed from the state and therefore conditional.

Cornered Resource: the implicit state guarantee

The deepest source of CCB's advantage is not on any product roadmap. It is the universal, unspoken understanding that the Chinese state stands behind the Big Four. In moments of financial stress — a regional bank run, a local-government debt scare, a property developer's default — Chinese savers do not flee the banking system. They flee toward the Big Four, and CCB is a prime destination. This flight-to-safety reflex hands CCB a permanent, ultra-low-cost, ultra-sticky deposit base that no private or regional competitor can replicate, because no competitor carries the same implicit sovereign backstop. It is the closest thing in banking to a cornered resource, and it is the engine behind CCB's cheap funding.

But note the double edge, because it is the whole investment debate in miniature. The same state relationship that guarantees the deposits also dictates the lending. The cornered resource and the "national service discount" are two faces of one coin: you cannot have the ultra-cheap funding without the obligation to lend where the state directs. This is why CCB's competitive advantage cannot be cleanly valued the way a Western bank's franchise can.

Scale Economies: amortized technology and distribution

CCB spent billions building proprietary digital infrastructure — its "CCB Cloud," its underwriting platforms, the Huidongni engine. The economics of software are unforgiving in the incumbent's favor: those are largely fixed costs, and CCB amortizes them across an asset base north of RMB 45 trillion and hundreds of millions of customers. A regional bank trying to build comparable technology must spread the same fixed cost over a tiny fraction of the assets, rendering it structurally uncompetitive on unit cost. This is a genuine, self-generated power — not one borrowed from the state — and it is the mechanism by which platforms like Huidongni actually defend CCB's turf against smaller lenders.

Switching Costs: the embedded consumer

Consider a typical CCB retail customer: her salary is deposited into a CCB payroll account, her home loan sits on CCB's mortgage book, and her daily spending runs through the 建行生活 CCB Lifestyle app. To leave, she would have to redirect her income, refinance her mortgage, and rebuild her financial life elsewhere for marginal benefit. The friction is enormous, and it compounds across the tens of millions of households wired into CCB's ecosystem. These switching costs are real, though they are more a defense of the existing base than a source of new growth.

Process Power: underwriting at national scale

Finally, there is the sheer institutional machinery required to underwrite, monitor, and service hundreds of millions of loans simultaneously across a continent-sized economy — a capability built over decades that a new entrant simply cannot stand up quickly.

What the 7 Powers analysis exposes, though, is a bank whose most powerful advantages are inseparable from the state. Strip out the sovereign backstop and the picture changes entirely. That is the fault line on which the entire bull-versus-bear debate is fought.

IX. The Investor Dilemma: Bull vs. Bear Case & Skeptic Stress Test

Every serious analysis of CCB eventually collides with one uncomfortable fact, and an activist investor would put it bluntly: this bank is not primarily run to maximize shareholder value.

The skeptic's stress test: the national-service discount

Imagine a short-seller building the bear thesis. Her central charge would not be fraud or hidden losses — it would be governance, structural and by design. CCB, she would argue, is an instrument of macroeconomic policy first and a profit-maximizing enterprise second. When Beijing decided in recent years to cut the rates on existing mortgages to relieve household budgets, CCB complied, absorbing the margin hit on its most valuable asset — a decision no shareholder-first bank would ever make voluntarily. When local-government financing vehicles cannot repay, CCB extends and restructures rather than foreclosing. Each of these is, in effect, a tax levied on minority shareholders in the name of national stability. You are not buying a bank, she would say; you are buying a public utility that happens to have a stock listing, and you should pay a utility's price — or less. This is the intellectual core of the persistent discount to book value, and it is not irrational. It is the market pricing a real, structural claim that the state holds on CCB's earnings.

Run this through Porter's Five Forces and the competitive picture is genuinely benign — which is part of why the discount is a governance discount, not a franchise discount. Rivalry among the Big Four is oligopolistic and orderly rather than cutthroat. The threat of new entrants is near zero; you cannot charter a new bank of this scale in China. Supplier power — the cost of deposits — is low thanks to the sticky retail base, though it is rising as savers turn choosy. Buyer power is fragmented across hundreds of millions of borrowers. The one force that bites is the threat of substitutes and disintermediation — the fintech platforms and direct-financing channels nibbling at the edges — but for now the Big Four's dominance of the core deposit-and-lending business is close to unassailable. The problem for shareholders was never competition. It was, and remains, the identity of the controlling owner.

The bull case: the state-backed bond proxy

The bull does not really dispute the skeptic's facts. He reframes them. Yes, CCB is run for stability rather than aggressive growth — and that, he argues, is precisely what makes it a compelling income instrument. Consider the shape of the return. CCB has consistently paid out 30% of its net profit as cash dividends — RMB 3.887 per ten shares for 2025, roughly RMB 101.7 billion in total.1 Bought at around 0.4 times book value, that payout translates into a dividend yield in the mid-single digits, backed by the single most creditworthy entity in the country, the Chinese state itself.1 The bull's insight is that CCB behaves less like an equity and more like a perpetual, state-guaranteed bond with a modest growth kicker — a "bond proxy." In a Chinese economy of falling interest rates, collapsing property returns, and a moribund domestic stock market, a secure high-single-digit income stream backed by Beijing is genuinely scarce and genuinely valuable. That scarcity is exactly why these stocks were bid up by income-hungry domestic investors even as foreign investors shunned them.

He adds a second point: the worst is arguably behind. The most painful property write-downs have largely been taken, the balance sheet is armored with a 19.69% capital ratio and 233% provision coverage, and the bank has enormous capacity to keep paying its dividend through further stress.[^1]

The bear case: the yield squeeze and the LGFV drag

The bear's rebuttal targets the sustainability of exactly that dividend. His first mechanism is the yield squeeze already visible in the NIM. Dividends are paid out of profits, and profits at a bank are the margin multiplied by the asset base. If NIM keeps bleeding — from 1.51% to 1.34% and potentially toward 1.20% or lower — profit growth stalls or reverses, ROE slides from 10% toward single digits, and the arithmetic that supports a growing dividend starts to break. A bond proxy is only as good as the coupon behind it, and the coupon is thinning every year.

His second mechanism is the local-government drag. Across China, banks including CCB have been enlisted to refinance the debts of local-government financing vehicles, often by stretching maturities out twenty or thirty years at deliberately low interest rates. Every yuan locked into a decades-long, ultra-low-yield, illiquid LGFV loan is a yuan that cannot be redeployed into something profitable. Over time, this quietly poisons the asset mix, capping the bank's earning power for a generation even if headline NPLs never spike. The losses, in this reading, do not arrive as a dramatic default; they arrive as decades of foregone return.

The honest conclusion is that the bull and the bear are not really disagreeing about the facts — they are disagreeing about what a state-controlled, income-generating financial utility is worth. That makes the decisive variables unusually easy to name.

X. Epilogue & Watchlist: The 1-3 KPIs

Sitting atop this RMB 45-trillion machine is a leadership team that embodies the central tension of the whole story. Chairman 张金良 Zhang Jinliang and President 张毅 Zhang Yi are, by all accounts, highly capable technocrats — career financial-system professionals rather than empire-builders.[^13] But their incentives are not the incentives of a Western bank CEO. There is no mega-grant of stock options tying their fortunes to the share price; they own no meaningful personal stake in the bank they run. Their mandate flows from the state, and their performance is judged against political-strategic goals bundled under the banner of 共同富裕 common prosperity as much as against earnings per share.

Read through the lens of management credibility, that is not entirely a negative. On the evidence, Zhang Jinliang's tenure has been marked by restraint rather than ambition — no splashy overseas acquisitions, no speculative dash for growth, but a steady focus on stabilizing the deposit base, absorbing the property downturn, and building out digital underwriting. For a bank whose greatest historical risk has always been being ordered to grow recklessly, a management team temperamentally inclined toward caution is arguably an asset. The credibility question that remains unanswerable from the outside is the one that defines every Chinese state bank: when the interests of Beijing and the interests of minority shareholders diverge — as they did on mortgage repricing — management will side with Beijing, because that is who they answer to. An investor is not underwriting the judgment of these individuals so much as the priorities of their ultimate employer.

What to watch

If you follow CCB from here, three indicators will tell you almost everything about whether the bull or the bear case is winning. You do not need to compute them; you need to watch which way they move.

1. The net interest margin floor. This is the master variable. Does NIM stabilize somewhere around 1.30%, signaling that funding costs have finally caught up with the rate cuts and the profit engine has found a bottom? Or does it keep bleeding toward 1.15%, in which case the earnings — and eventually the dividend growth — come under real pressure? Every basis point matters on a base this size.

2. The mortgage prepayment rate. For years, Chinese households, unnerved by falling property values and offered little worth investing in, chose to pay down their mortgages early — voluntarily retiring CCB's highest-quality, highest-margin loans. Watch whether that early-repayment wave subsides and, better still, whether fresh mortgage demand returns. A revival in retail credit appetite would be the clearest sign that the Chinese consumer's confidence — and CCB's crown-jewel franchise — is healing.

3. The 30% dividend payout ratio. The entire bond-proxy thesis rests on this single policy. Because Central Huijin and the state depend on those dividends as a source of fiscal revenue, there is a powerful alignment keeping the payout intact — the government wants the check as much as minority shareholders do. But watch it. Any move to trim the payout, whether to conserve capital against mounting LGFV losses or to fund some new national priority, would strike directly at the reason most investors own the stock at all.

China Construction Bank began as a ministry that counted tons of steel, became the largest financier of the greatest infrastructure and urbanization boom in human history, and now stands as a colossal, over-capitalized, state-directed income machine feeling its way through the end of the growth model that made it. Whether it proves to be a value trap slowly grinding down its own margins, or a resilient, state-backed cash cow throwing off one of the few secure yields left in China, will not be settled by any single earnings report. It will be settled slowly, in the drift of a margin, the mood of a homeowner, and the willingness of the state to keep writing the same dividend check. For now, CCB remains what it has always been: the most honest financial mirror of China that exists — reflecting, in one balance sheet, both the extraordinary ambition and the unresolved contradictions of the Chinese century.

References

-

Announcement of Annual Results 2025 — China Construction Bank, 2026-03-27 ↩↩↩↩

-

China Construction Bank reports 1pc profit rise in 2025 — The Standard, 2026-03-27 ↩

-

Asian deal of the year: China Construction Bank $9 billion IPO — Euromoney, 2006 ↩↩

-

Construction Bank raises 8b dollars in IPO — China Daily, 2005-10-21 ↩↩

-

Bank of America Form 8-K, sale of China Construction Bank shares — U.S. Securities and Exchange Commission, 2011-08-29 ↩

-

CCB acquires Bank of America's Hong Kong-Macau business — FinanceAsia, 2006-08-25 ↩↩

-

China Cinda Asset Management Co., Ltd. — Corporate Overview & History ↩↩

-

China Construction Bank Corporation (0939.HK) Company Profile — Reuters ↩↩

-

The People's Bank of China (PBOC) — Monetary Policy and Interest Rate Announcements ↩

-

China's Financial System: Past, Present, and Future — National Bureau of Economic Research Working Paper w17828, 2012 ↩

-

Lessons from China's past banking bailouts — BBVA Research Working Paper 20/04, 2020-03 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube