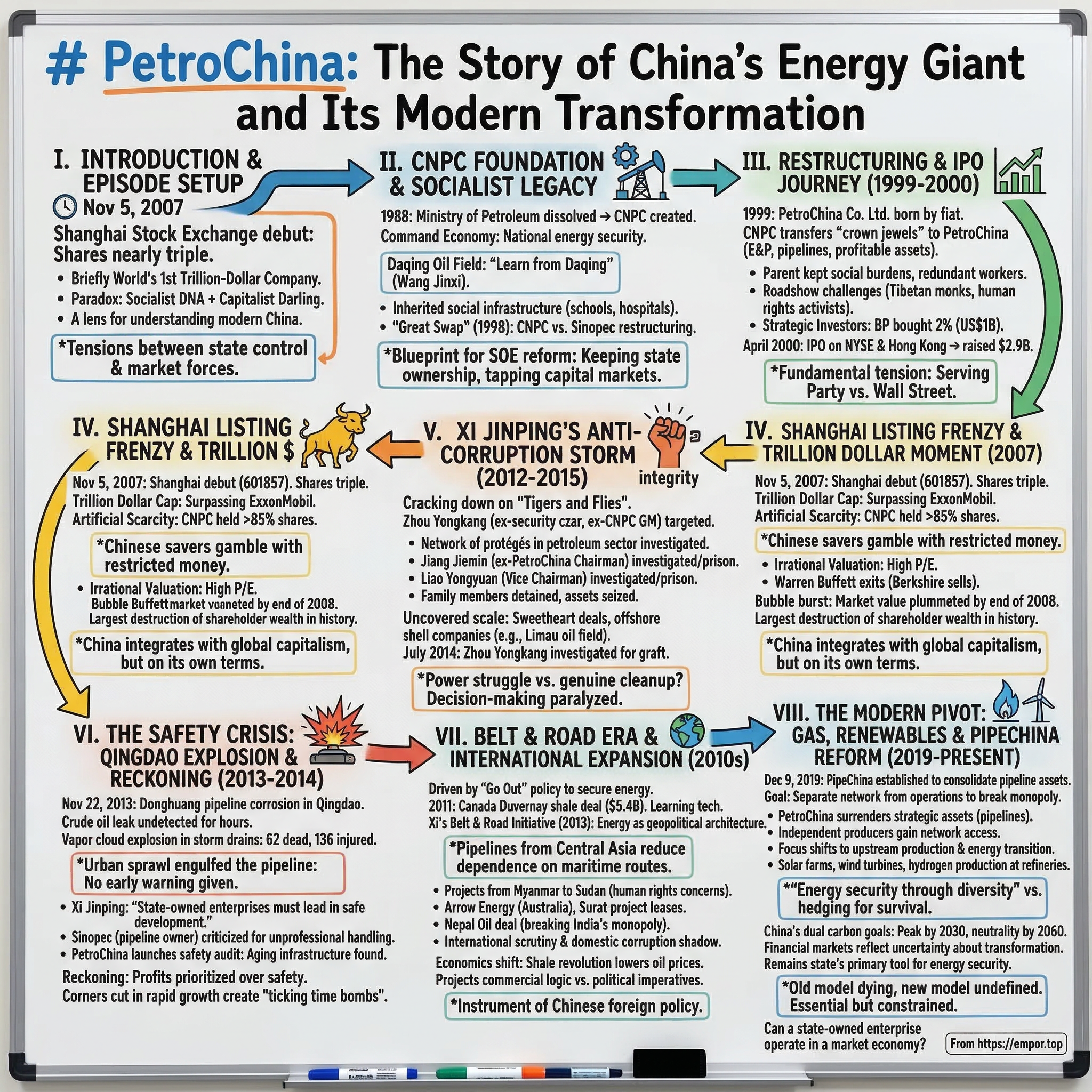

PetroChina: The Story of China's Energy Giant and Its Modern Transformation

I. Introduction & Episode Setup

Picture this: November 5, 2007. Shanghai's financial district buzzes with an electricity that transcends the usual market opening bell. Retail investors—teachers, shopkeepers, retirees—crowd around screens in brokerage offices, watching as PetroChina's shares begin trading on the Shanghai Stock Exchange. Within minutes, the stock price nearly triples. By day's end, this state-owned oil company briefly becomes the world's first trillion-dollar company by market capitalization, surpassing ExxonMobil, a company that had dominated global energy markets for decades.

Yet this moment of triumph masks a deeper paradox. Here was a company born from China's socialist restructuring, carrying the DNA of central planning, somehow becoming a darling of capitalist markets. A company that would soon face corruption scandals that reached the highest echelons of Chinese politics, suffer deadly accidents that killed dozens, and navigate China's seemingly contradictory goals of energy security and carbon neutrality.

PetroChina Company Limited, incorporated in 1999 and headquartered in Beijing, stands as more than just another energy giant. It's a lens through which we can understand modern China itself—the tensions between market forces and state control, between rapid growth and safety, between global ambitions and domestic priorities. As a subsidiary of China National Petroleum Corporation (CNPC), it carries both the weight of China's energy security and the expectations of international investors.

Today, with a market value of $456.6 billion based on its Hong Kong share price, PetroChina remains one of the world's largest energy companies. But numbers tell only part of the story. The real narrative spans from the oil fields of Daqing to the boardrooms of Goldman Sachs, from pipeline explosions in Qingdao to gas terminals along the Belt and Road. It's a story of transformation, scandal, redemption, and the ongoing question: Can a state-owned enterprise truly operate in a market economy?

Our journey begins not with PetroChina itself, but with its parent—CNPC—and the socialist legacy that would shape everything that followed.

II. The CNPC Foundation & Socialist Legacy

The year was 1988, and China's economy was opening, but its oil industry remained firmly in the grip of central planning. In September of that year, the State Council dissolved the Ministry of Petroleum Industry and created something new: China National Petroleum Corporation. This wasn't just bureaucratic reshuffling—it was the beginning of a radical experiment in marketizing socialism.

CNPC emerged from the ashes of China's command economy with a clear mandate: secure the nation's energy supply while maintaining absolute state control. Headquartered in Beijing's Dongcheng District, the corporation inherited not just oil fields and refineries, but an entire social infrastructure—hospitals, schools, housing complexes. In places like Daqing, China's most famous oil field, CNPC wasn't just an employer; it was the state itself, manifested in crude oil and social services.

The socialist model had its logic. Oil was too strategic to leave to market forces. During the Cold War, energy security meant survival. Mao's famous directive—"In industry, learn from Daqing"—elevated oil workers to revolutionary heroes. The Iron Man Wang Jinxi, who famously jumped into freezing cement to prevent a well blowout, became a national icon. This wasn't just resource extraction; it was nation-building through petroleum.

But by the 1990s, this model was creaking. China's oil consumption was exploding—from 2.3 million barrels per day in 1990 to projections that would soon exceed 5 million. The vertically integrated ministries couldn't keep pace. Foreign oil majors like BP and Shell were knocking at the door, offering technology and capital. Something had to give.

The breakthrough came in 1998 with what insiders called the "great swap." In a stroke of administrative genius—or madness, depending on your perspective—the government restructured the entire petroleum sector. CNPC would focus on upstream operations (exploration and production) in the north and west. Sinopec would handle downstream (refining and marketing) in the south and east. Then, in a twist that would have made capitalists scratch their heads, they swapped assets to create two vertically integrated giants, each with upstream and downstream capabilities.

This wasn't privatization in any Western sense. It was something uniquely Chinese: maintaining state ownership while creating entities that could compete, raise capital, and operate with market discipline. The stage was set for the next act—creating publicly traded subsidiaries that could tap international capital markets while keeping the state firmly in control.

The mechanism was elegant: CNPC would transfer its best assets—the profitable oil fields, the modern refineries, the prime gas stations—into a new entity called PetroChina. The parent would keep the social burdens, the unprofitable wells, the legacy costs. Foreign investors would get exposure to China's booming energy market without the messy socialism. Goldman Sachs drew up the blueprints. The investment bankers promised a new model for state-owned enterprise reform.

But could it work? Could you really separate commercial operations from political control? As 1999 dawned, PetroChina was about to find out.

III. The Great Restructuring & IPO Journey (1999-2000)

November 5, 1999. The boardroom at CNPC headquarters in Beijing buzzes with tension. Chairman Ma Fucai sits at the head of a massive mahogany table, surrounded by party officials, ministry bureaucrats, and—incongruously—investment bankers from Goldman Sachs in their Hermès ties and Italian suits. The task before them: carve up a socialist oil giant to create something that Wall Street could digest.

"We need clean assets," the lead Goldman banker explains through a translator, his PowerPoint slides showing neat boxes and arrows. "No schools, no hospitals, no retired workers." The CNPC executives exchange glances. How do you explain to a Wall Street banker that in Daqing, the oil company is the hospital, the school, the entire social fabric?

The solution they crafted was audacious in its simplicity, breathtaking in its scope. On November 5, 1999, PetroChina Company Limited was born—not through organic growth or market competition, but through administrative fiat. CNPC would transfer its crown jewels to this new entity: 66% of crude oil production, 72% of natural gas output, all the profitable refineries, the best gas stations. The parent would keep everything else—500,000 redundant workers, social obligations, money-losing wells.

It would serve as a blueprint for China's ongoing efforts to privatize its state-owned enterprises (SOEs). But this wasn't privatization in any conventional sense. China National Petroleum would retain 90% ownership in the company now valued at roughly US$30 billion. The state would maintain iron control while tapping international capital markets for funding and—perhaps more importantly—forcing some measure of market discipline onto a bloated bureaucracy.

The roadshow that followed reads like a corporate thriller. It was not only a massive, landmark offering for Goldman Sachs but would serve as a blueprint for China's ongoing efforts to privatize its state-owned enterprises. Goldman's team crisscrossed the globe, pitching to pension funds in Boston, sovereign wealth funds in Singapore, oil majors in London. From 1989 to 2000, demand for crude oil in China doubled. While China had massive supply—over 50% of Asia's oil reserves—domestic demand soon outstripped the capacity of China's state-owned oil companies to harness domestic oil. By 1994, China had become a net importer of oil.

But the timing couldn't have been worse. The dotcom bubble was reaching its frenzied peak—investors wanted the next Amazon, not a Chinese state oil company. When Goldman Sachs opened its "roadshow" to sell the investment, the AFL-CIO answered with its own. Goldman wheeled out analysts; the AFL-CIO fired back with a Tibetan monk and Harry Wu, a former prisoner in a Chinese labor camp. Human rights activists attacked CNPC's investments in Sudan, where oil revenues allegedly funded civil war atrocities.

"PetroChina has been a very grueling process for both the company and the underwriters," said Goldman Sachs's managing director, Paul S. Schapira. The offering faced tremendous regulatory and political resistance, weakening demand. Major U.S. pension funds, including TIAA-CREF and CalPERS, publicly announced they would boycott the offering.

The deal was saved by strategic investors making calculated bets on China's future. BP purchased 2% of PetroChina's stock for US$1 billion, while another group of investors purchased US$350 million in shares. BP's motivation was clear: In exchange, it won the right to establish a gas-marketing joint venture in eastern China—a major coup.

On April 6, 2000, PetroChina's American Depositary Receipts began trading on the New York Stock Exchange at $16.44—the low end of the expected range. The next day, H shares commenced trading in Hong Kong. PetroChina's IPO raised US$2.9 billion. With proven oil reserves of 10.3 billion barrels, it immediately ranked as the fourth-largest publicly-listed oil company in the world.

The numbers told a remarkable story of value creation. PetroChina's earnings would grow from US$3.3 billion in 1999 to US$21 billion by 2013. But beneath the financial engineering lay a fundamental tension that would define PetroChina's next chapter: How long could a company serve two masters—the Communist Party and Wall Street—before something had to give?

IV. The Shanghai Listing Frenzy & Trillion Dollar Moment (2007)

The morning of November 5, 2007, Shanghai's Lujiazui financial district hummed with an energy that bordered on hysteria. In tea shops and brokerage offices, retail investors—housewives, taxi drivers, shopkeepers—huddled around computer screens, watching the countdown to 9:30 AM. When the bell rang and PetroChina's stock code 601857 flashed green on the Shanghai Stock Exchange, the opening price stunned even the optimists: 48.60 yuan, nearly triple the IPO price of 16.70 yuan.

Within minutes, trading volume exploded. PetroChina executives, investment bankers and brokers cheered at the Shanghai Stock Exchange as the stock's opening price of 48.60 yuan flashed on an electronic screen. By day's end, PetroChina's new shares listed in Shanghai surged to 43.96 yuan ($5.90) Monday, nearly triple the IPO price of 16.70 yuan ($2.24).

The mathematics of the moment defied logic. Adding the value of PetroChina shares traded in Shanghai, Hong Kong and New York, and the 157.9 billion shares held by CNPC, the company's total market capitalization rose to just over $1 trillion, far surpassing No. 2 Exxon Mobil Corp.'s $488 billion. PetroChina had become the world's first trillion-dollar company—a distinction that would prove both fleeting and instructive.

But this wasn't a simple triumph. The state-controlled firm sold only a 2.2% stake in its Shanghai offering, which was insufficient to meet the appetite of retail investors on the mainland who are prevented from buying the company's shares in New York or Hong Kong, where PetroChina first went public in 2000. This artificial scarcity created a perfect storm. Chinese savers, earning negative real returns in bank accounts as inflation outpaced deposit rates, had nowhere else to put their money. Capital controls prevented them from investing overseas. The domestic stock market became their only escape valve.

The absurdity of the valuation was apparent to anyone who looked beneath the surface. PetroChina's massive market value bears little relation to its profitability, however. In the first half of this year, the company's net income was about $10.9 billion. ExxonMobil earned $19.5 billion during the same period. "From an operational perspective, we see little reason for this disparity," the investment bank said.

Warren Buffett, the Oracle of Omaha, had seen enough. Warren Buffett's investment company, Berkshire Hathaway, made a $3.5 billion profit on its recent sale of the bulk of its holdings in PetroChina. His timing was impeccable—selling into the frenzy just before the Shanghai listing. While Buffett claimed the sale was purely based on valuation, not the company's controversial Sudan connections, the message was clear: when retail mania reaches fever pitch, smart money heads for the exits.

The Shanghai listing raised 66.8 billion yuan ($8.94 billion), making it the biggest IPO in China at that time. But the real story wasn't the money raised—it was what the listing revealed about China's distorted capital markets. More than 85 percent of shares outstanding - 157.9 billion shares - are held by PetroChina's parent company CNPC and are unlikely to trade in the market any time soon.

Howard Gorges of South China Holdings captured the moment perfectly: "There's a huge amount of money in Shanghai that's willing to buy literally anything - quality or speculative." The Shanghai Composite had doubled in 2007 after doubling in 2006. This wasn't investing; it was gambling with Chinese characteristics.

The international disconnect was stark. While Shanghai investors bid PetroChina shares to the stratosphere, PetroChina's H-shares fell 7.3% in Hong Kong on the same day it was making its spectacular Shanghai listing. In New York, the ADRs plummeted nearly 13%. The same company, the same assets, the same earnings—but wildly different prices depending on which market you accessed.

According to Reuters, PetroChina's opening price in Shanghai valued the company at 60 times analysts' forecasts for its 2007 earnings per share, above the global average of 18 times for oil company's at the time. This wasn't just expensive; it was delusional.

Prime Minister Wen Jiabao watched nervously from Beijing. "Preventing asset bubbles is like preventing inflation, and it is the government's responsibility to ensure a fair, healthy and transparent stock market," he said. But the government was trapped. Opening capital markets would trigger capital flight. Maintaining controls guaranteed bubble formation. They chose the bubble.

PetroChina's market value plummeted to less than $260 billion by the end of 2008, representing the largest destruction of shareholder wealth in world history, according to Bloomberg. The trillion-dollar moment had lasted mere weeks. The Shanghai retail investors who bought at the peak would lose 80% of their investment within a year.

Yet the 2007 listing succeeded in its real purpose: demonstrating that China's capital markets had arrived, that Chinese companies could achieve valuations that dwarfed their Western counterparts, that the Middle Kingdom was reclaiming its place at the center of global finance. The fact that it was all built on artificial scarcity and retail speculation was beside the point. Or perhaps that was the point—China would integrate with global capitalism, but on its own terms, with its own rules.

As 2007 drew to a close, oil prices approached $100 per barrel, China's economy roared ahead at double-digit growth, and PetroChina executives basked in their trillion-dollar moment. They couldn't know that within five years, their company would become the epicenter of the largest corruption purge in modern Chinese history.

V. Xi Jinping's Anti-Corruption Storm (2012-2015)

The Zhongnanhai leadership compound, Beijing. Late evening, November 2012. The 18th National Congress had just concluded, and Xi Jinping stood at the helm of the world's most populous nation. Meanwhile, in the latter half of 2013, a separate operation began to investigate officials with connections to Zhou Yongkang, former Politburo Standing Committee member and national security chief. What would unfold over the next three years would shake PetroChina—and China's entire energy sector—to its core.

In his first days in office, Xi vowed to crack down on "tigers and flies", meaning extremely powerful officials as well as petty ones. But everyone knew the real question: Would he dare touch the untouchables? Would he break the unwritten rule that Politburo Standing Committee members enjoyed immunity from prosecution?

The answer came through PetroChina's executive suites like a slow-motion earthquake. Three sectors in which Zhou was known to carry immense influence were targeted for investigation, including the national oil sector (where Zhou was once a chief executive), Sichuan province (where Zhou was party chief), and security organs (once under the jurisdiction of the Central Political and Legal Affairs Commission, which Zhou headed).

Zhou Yongkang wasn't just any official. He had risen through China's oil industry over decades, serving as CNPC's general manager from 1996-1998. His power base ran deep through the petroleum sector—a network of protégés, business partners, and family members who had grown fabulously wealthy from China's oil boom. Zhou's family reportedly made billions of dollars by investing in the oil industry, of which Zhou had headed the largest company, China National Petroleum Corp.

The first domino fell in August 2013. In August 2013, the Party began a corruption investigation into Zhou. But Xi's investigators didn't go directly for Zhou—that would have been too shocking, too destabilizing. Instead, they began with his network, methodically dismantling the petroleum empire he had built.

September 1, 2013, marked a turning point. On September 1, the CDIC announced that it was investigating an even more prominent individual – Jiang Jiemin, the director of the State-Owned Assets Supervision and Administration Commission (SASAC), which is the controlling shareholder in the approximately 100 enterprises in strategic industries ranging from automobiles to petroleum to telecommunications that are owned by the Chinese government. Jiang, a career oil man, held top jobs at CNPC in the late 2000s, including chairman of CNPC's internationally-listed subsidiary, PetroChina, from 2011 to 2013, from which he assumed the top position at SASAC.

Jiang Jiemin's arrest sent shockwaves through PetroChina's headquarters. This wasn't some mid-level bureaucrat—he had been PetroChina's chairman, the face of the company to international investors. In October 2015, he was found guilty and sentenced to 16 years in prison. The message was unmistakable: no one was safe.

The investigation expanded like an oil spill, contaminating everyone it touched. At least 11 other former top CNPC group officials are under arrest. March 2015 brought another bombshell: Liao Yongyuan, vice chairman of PetroChina and general manager of CNPC, was placed under investigation. By January 2017, he was sentenced to 15 years in prison for abuse of power and accepting nearly $2 million in bribes.

The human toll went beyond prison sentences. Careers built over decades evaporated overnight. Executives who had once commanded respect found themselves under house arrest, their assets frozen, their families investigated. In December, Zhou, his son Zhou Bin and his daughter-in-law Huang Wan were taken into custody. The home of Zhou's younger brother Zhou Yuanxing (周元兴) was searched by the authorities twice. Yuanxing died in December 2013 after a battle with cancer. Zhou Yongkang and his son Zhou Bin were not present at the funeral, fueling speculation that Zhou and his family members were all in custody.

The corruption uncovered was staggering in scale. Take the Limau oil field deal in Indonesia—a case that exemplified the rot. A subsidiary of China National Petroleum (CNPC), PetroChina Daqing Oilfield, paid $85 million to pump from three blocks in the ageing Limau field under a 2013 contract with Indonesia's state-owned oil company, Pertamina, according to senior Chinese oil industry officials with knowledge of the transaction. Today, the three Limau blocks squeeze out less than three percent of the oil pumped when output peaked in the 1960s. "We all know it is a ridiculous investment, but I have no idea where the money has actually ended up," says a senior Chinese oil industry official who has seen budget figures for the Limau wells.

The investigation revealed a pattern: sweetheart deals, offshore shell companies, family members enriching themselves through insider knowledge. Reuters also reported in March that Chinese authorities had seized assets worth at least 90 billion yuan ($14.56 billion) from family members of Zhou Yongkang and his associates.

But the corruption crackdown wasn't just about cleaning house—it was about power. Sources with ties to the Chinese leadership have previously told Reuters that Xi has been determined to bring down Zhou for allegedly plotting appointments to retain influence ahead of the 18th Party Congress in November 2012, when Xi took over the party. Zhou had nominated Bo Xilai, a charismatic politician with leadership ambitions, to succeed him as domestic security chief and had tried to orchestrate the younger man's promotion to the Standing Committee, the sources have said.

The climax came in July 2014. On July 29, the Central Commission for Discipline Inspection of the Chinese Communisty Party announced it was investigating ex-security czar Zhou Yongkang "on suspicion of grave violations of discipline." Indeed, Zhou is the most senior Chinese official to be ensnared in a graft scandal since the party swept to power in 1949. He was a member of the Politburo Standing Committee - China's apex of power - and held the post of security tsar until he retired in 2012.

The impact on PetroChina was devastating. Morale collapsed. Decision-making ground to a halt as executives feared that any action might be construed as corrupt. International partners grew nervous—if the chairman could be arrested, who was next? Stock prices reflected the uncertainty, with PetroChina's Hong Kong shares underperforming peers throughout the investigation period.

Yet there was a deeper question that the corruption purge raised but couldn't answer: Was this really about fighting graft, or was it political warfare dressed up as anti-corruption? "Zhou has always been an enemy of the people," said Hu Jia, one of China's most prominent human rights activists. "But Xi Jinping's investigation of Zhou isn't for human rights or to oppose corruption. This is a power struggle."

The petroleum sector's reckoning had only just begun. As executives picked through the wreckage of careers and reputations, another crisis was about to explode—literally—that would force PetroChina to confront an even more fundamental question: In the rush for growth and profit, had they forgotten the most basic responsibility of all—keeping people safe?

VI. The Safety Crisis: Qingdao Explosion & Reckoning (2013-2014)

November 22, 2013. 3:00 AM. Qingdao, Shandong Province. In the pre-dawn darkness, crude oil begins seeping from a corroded section of the Donghuang pipeline, built in 1985 when this area was rural farmland. Now, three decades later, urban sprawl has engulfed the pipeline—apartment buildings, chemical plants, and busy roads sit atop what was once a remote oil artery. The pipeline leaked for about 15 minutes before shut off, spilling oil onto street and sea.

No alarms sound. No warnings are issued. Workers discover the leak and shut off the flow at 3:15 AM, but the damage is done—thousands of liters of Saudi light crude have already seeped into the city's storm drains, creating an invisible bomb beneath Qingdao's streets. For the next seven hours, cleanup crews work in ignorance of the danger accumulating beneath their feet.

10:25 AM. Without warning, the oil vapors ignite. A devastating crude oil vapor explosion accident, which killed 62 people and injured 136, occurred on November 22, 2013. It was one of the most disastrous vapor cloud explosion accidents that happened in Qingdao's storm drains in China. The explosion tears through the Huangdao district with such force that it lifts entire sections of road, flips cars like toys, and blows out windows kilometers away. A crater 30 meters wide and 6 meters deep appears where a busy street once stood.

The images that emerge are apocalyptic. Bodies scattered across torn pavement. A truck fallen into the massive crater. Black smoke billowing over residential apartments. Oil burning on the surface of Jiaozhou Bay. This wasn't just an industrial accident—it was an urban catastrophe, bringing the dangers of China's breakneck industrialization literally to people's doorsteps.

The immediate cause was clear enough: The leakage was caused by the accidental rupture of the pipeline which was owned by China Crude oil and Chemical Corporation (Sinopec). But the deeper causes ran through the heart of China's development model. Due to China's acceleration of urbanization expansion, more and more oil/natural gas transmission pipelines, which were originally laid in the urban outskirts, are now in the densely populated urban areas.

Local residents' fury was palpable. Local residents and workers are also demanding to know why no warning was given immediately after the oil leak was first discovered in the early hours of the morning. Many had no idea about the potential danger or even the fact that the pipeline was located so close to their workplace. Seven hours had elapsed between discovery and explosion—seven hours when evacuations could have saved lives.

President Xi Jinping arrived in the city on Sunday afternoon to inspect the rescue efforts. The symbolism was unmistakable—just as the anti-corruption campaign was decimating PetroChina's leadership, here was visceral proof that the rot went beyond financial malfeasance. He said State-owned enterprises must take the lead in the "safe development" of Chinese industry and stressed that local governments should reject any project that poses a potential safety hazard to the general public. Xi also emphasized that officials should learn the lessons of previous accidents and said safety inspections must be carried out nationwide, especially on underground pipelines and networks.

While the Qingdao explosion was Sinopec's disaster, not PetroChina's, the entire petroleum sector was implicated. Yang Dongliang, director of the state administration of work safety and head of an investigation team for the accident, said the poor planning and supervision, and "unprofessional handling of oil leakage before the blasts", contributed to the tragedy.

The human dimension of the tragedy went beyond statistics. Human behaviors should be taken into account in the evaluation of project management. Cleland identified 19 underlying causes of project failure, in which 9 of them are behaviors of the principal participants. This wasn't just mechanical failure—it was human failure at every level, from the corroded pipe that nobody had properly maintained to the communication breakdown that left residents unwarned.

The Qingdao explosion forced a reckoning across China's energy sector. A Sinopec safety review found 8,000 issues across its sites. PetroChina, watching its rival's crisis, launched its own comprehensive safety audit. The findings were damning: aging infrastructure, lax oversight, profits prioritized over safety. The same corners cut in the rush for growth that had enabled corruption had also created ticking time bombs beneath China's cities.

For PetroChina executives already reeling from the corruption purge, the Qingdao disaster added a new dimension of vulnerability. It wasn't enough to avoid graft investigators; now they had to prove they weren't presiding over the next catastrophe. Investment decisions slowed to a crawl. International partners demanded enhanced safety protocols. Insurance premiums skyrocketed.

The broader implications were profound. China's energy infrastructure, built during decades of breakneck growth, was aging faster than it was being maintained. Urban expansion had turned remote pipelines into urban hazards. The same state-owned enterprises that were supposed to be the backbone of China's economy were becoming its greatest liability.

Yet even as the smoke cleared in Qingdao and the last bodies were recovered, PetroChina's leadership knew they couldn't afford to slow down. China's energy demands were still growing. The government still expected them to secure oil supplies from Central Asia to Africa. The Belt and Road Initiative was about to be announced, promising a new era of international expansion. Safety was important, but energy security was existential.

The tension between these imperatives—safety versus growth, caution versus ambition—would define PetroChina's next chapter as it embarked on its most ambitious international expansion yet.

VII. The Belt & Road Era & International Expansion (2010s)

February 2011. The Fairmont Hotel, Calgary. In a conference room overlooking the Canadian Rockies, PetroChina executives signed papers that would have been unthinkable just a decade earlier. In February 2011, PetroChina agreed to pay $5.4 billion for a 49% stake in Canada's Duvernay shale assets owned by Encana. It was China's biggest investment in shale gas to date.

This wasn't just another acquisition. It was a declaration of intent—PetroChina was going global, and it was willing to pay premium prices to learn the technologies that could unlock China's own vast shale reserves. Driven by China's increasing energy needs and supported by government's Go Out policy, CNPC expanded internationally, entering less politically stable countries with greater political and security risks

The Duvernay deal exemplified PetroChina's new playbook. Rather than simply buying oil fields for production, they were acquiring knowledge. Neil Beveridge, oil analyst at Bernstein in Hong Kong, said PetroChina's investment in the Duvernay project would give it experience in developing "very deep shales" that are similar to China's own deposits. The technology transfer was as valuable as the resources themselves.

But the Canadian foray also revealed the challenges of Chinese state capital going abroad. Encana and PetroChina have a history: an earlier $5.4-billion joint-venture deal for Encana's lands in the Montney region fell apart in mid-2011 after they failed to see eye-to-eye on how that project would operate. Cultural differences, operational disagreements, and political sensitivities turned what should have been straightforward business deals into diplomatic minefields.

The timing was crucial. In December 2012, just as PetroChina was finalizing another major Canadian deal, Prime Minister Stephen Harper announced new restrictions on state-owned enterprise acquisitions, effectively slamming the door on future Chinese takeovers. PetroChina had gotten in just under the wire, but the message was clear: Western governments were growing wary of Chinese state capital.

Yet Canada was just one piece of a much larger puzzle. Across the globe, PetroChina was weaving a web of energy infrastructure that would fundamentally reshape global oil flows. The crown jewel of this strategy was the Belt and Road Initiative, announced by Xi Jinping in 2013, which turned energy infrastructure into geopolitical architecture.

The Central Asia gambit was particularly audacious. It is mainly supplied by the Central Asia-China gas pipeline. Pipelines from Kazakhstan and Turkmenistan would reduce China's dependence on maritime oil routes that could be blockaded by the U.S. Navy. This wasn't just energy security—it was rewriting the Eurasian energy map.

In February 2019, as part of the Arrow Energy joint venture with Royal Dutch Shell, the company was granted leases for $10 billion (AUS) towards the Surat project in Queensland, Australia. From Canada's oil sands to Australia's gas fields, from Myanmar's pipelines to Sudan's oil wells, PetroChina was everywhere, often in places Western companies wouldn't touch.

The Nepal deal illustrated both the ambition and the complications. China signed a deal in 2016 with the Nepal Oil Corporation to sell 30% of the total Nepalese petroleum consumption. China plans to build a pipeline to Nepal's Panchkhal along with a storage depot. On paper, it was straightforward commerce. In reality, it was about breaking India's monopoly on Nepal's energy supplies, inserting China into South Asian energy politics.

But international expansion brought international scrutiny. In 2011, Earthrights International accused PetroChina of complicity in serious human rights abuses in Burma, a country known for militarily furthering its economic interests through the use of forced labor. Every pipeline in a conflict zone, every deal with an authoritarian regime, became a reputational liability.

The corruption investigations back home cast a shadow over international operations. When executives were being arrested in Beijing, who would sign off on billion-dollar deals in Calgary or Caracas? The anti-corruption campaign didn't just clean house; it paralyzed decision-making at crucial moments in PetroChina's global expansion.

Moreover, the economics were shifting. The shale revolution that PetroChina had spent billions to understand was now flooding global markets with cheap oil and gas. Projects that made sense at $100 oil looked foolish at $50. The Duvernay assets that seemed so strategic in 2011 became a burden by 2017, with PetroChina agreed to pay $1.18-billion up front, plus carry another $1-billion in development costs over four years. That period has expired, however, meaning Encana would have to shoulder a greater share of any future drilling expenses.

Yet PetroChina couldn't retreat. Energy security remained China's top priority, and the government's Go Out policy demanded continued expansion. The company found itself caught between commercial logic and political imperatives, between the need for returns and the demand for resources.

The Belt and Road Initiative gave this expansion a new framework and urgency. Energy infrastructure wasn't just business—it was statecraft. Every pipeline was a link in China's new Silk Road, every gas terminal a node in Xi Jinping's vision of Chinese global leadership. PetroChina wasn't just an oil company anymore; it was an instrument of Chinese foreign policy.

As the 2010s drew to a close, PetroChina's international footprint was vast but vulnerable. It had assets on every continent, technology from the world's best operators, and pipelines linking China to energy supplies from Russia to Myanmar. But it also faced rising resource nationalism, environmental opposition, and the growing realization that the fossil fuel era might be ending sooner than expected.

The question was no longer whether PetroChina could go global—it already had. The question was whether it could transform itself fast enough to survive in a world increasingly turning away from the very product it was built to deliver.

VIII. The Modern Pivot: Gas, Renewables & PipeChina Reform (2019-Present)

December 9, 2019. Beijing. In a bland government building, officials gathered to witness what might be the most radical restructuring of China's energy sector since 1998. On December 9, 2019, Beijing legally established a new player in China's oil and natural gas industry, the China Oil & Gas Piping Network Corporation (PipeChina). The establishment of PipeChina is the most ambitious reform of China's oil and natural gas industry undertaken in more than 20 years.

This wasn't just corporate reorganization—it was surgery on China's energy anatomy. China consolidated the pipeline assets of three State-owned energy giants in 2019 into PipeChina, amid efforts to accelerate pipeline construction and ensure energy security. The company now operates over 100,000 kilometers of oil and gas pipelines across the country. For PetroChina, it meant surrendering its most strategic assets: the pipelines that had been its moat against competition.

The logic was compelling but painful. PetroChina made it difficult for third parties to access pipelines, preferring to purchase gas from independent producers at 70-80% of retail value then sell at full price to earn profit and prevent competition. This vertical integration had made PetroChina powerful, but it had also strangled China's gas market development. Independent producers couldn't reach customers. International suppliers faced monopolistic terms. The entire system was optimized for the incumbents, not for energy security.

Xi Jinping had been planning this since taking power. Xi's blueprint for economic reform, unveiled in November 2013, laid the groundwork for the birth of the national pipeline company with its goal of separating "networks from operations" in natural monopolies controlled by SOEs. But it took six years to overcome resistance from the oil giants who understood they were being asked to amputate their own limbs.

The timing wasn't coincidental. Natural gas consumption rose 8 percent to 426.1 billion cubic meters last year. China's carbon neutrality pledge required a massive shift from coal to gas. The Chinese government considers natural gas the preferred transition energy resource during China's transformation from fossil fuel-intensive to renewable energy. But how could China triple gas consumption when PetroChina controlled the pipes?

PipeChina was the answer—a neutral carrier that would treat all gas equally, whether from PetroChina, independent producers, or Russian imports. The creation of PipeChina, through acquiring the pipeline assets from the national oil companies, is an essential part of the reform agenda to increase natural gas supply and consumption through a monopoly and independent midstream sector.

For PetroChina, the impact was immediate and brutal. Revenue streams from pipeline tolls disappeared overnight. The ability to squeeze competitors through pipeline access vanished. Market share in gas distribution began eroding as independents gained access to infrastructure. However, affected by the unreasonable pricing of refined product pipelines, oil shippers reduce the demand for pipeline transportation, resulting in low pipeline turnover and poor profitability of PipeChina.

But PetroChina had no choice but to adapt. The company pivoted toward what it could still control: upstream production and the energy transition itself. In 2017, the shares of PetroChina upped after the rise of natural gas prices for commercial use. The company doubled down on gas exploration, particularly in unconventional resources like shale and tight gas that required its technical expertise.

The renewable pivot was even more dramatic. Operating through Oil, Gas and New Energy Resource segment for exploration, development, production, marketing of crude oil, natural gas, and new energy resource business, PetroChina began transforming itself from an oil company that produced some gas into an energy company that happened to produce oil.

Solar farms sprouted next to oil derricks. Wind turbines appeared along pipeline routes. Hydrogen production facilities emerged at refineries. This wasn't greenwashing—it was survival. China's dual carbon goals—peak emissions by 2030, neutrality by 2060—meant fossil fuel demand would eventually decline. PetroChina needed new businesses before the old ones died.

Yet the contradictions were stark. PetroChina was simultaneously drilling for more oil while building solar farms, expanding gas production while investing in hydrogen, maintaining fossil infrastructure while pledging net zero. The company tried to frame this as "energy security through diversity," but everyone understood the reality: PetroChina was hedging, trying to be everything to everyone because it didn't know what it should become.

The international dimension added complexity. Russia's Power of Siberia pipeline, operational since 2019, delivered gas directly to PipeChina's network, not PetroChina's. Central Asian suppliers could now negotiate with multiple Chinese buyers. LNG importers could access any market through PipeChina's terminals. PetroChina's monopolistic leverage in international negotiations evaporated.

Meanwhile, local governments and independent companies rushed to build their own gas infrastructure, knowing PipeChina would provide access. By 2023, China's National Development and Reform Commission (NDRC) released new tariffs for inter-provincial natural gas transmission pipelines that PipeChina operates. The new rules simplify the number of tariffs from 15 previously to 4. The market was being liberalized whether PetroChina liked it or not.

The financial markets reflected this uncertainty. PetroChina's stock price languished as investors struggled to value a company losing its monopoly while facing energy transition. Was it an oil company? A gas company? A renewable energy company? A bit of everything meant it excelled at nothing.

Inside PetroChina, the cultural shift was wrenching. Engineers who had spent careers maximizing oil production were now asked to develop solar projects. Pipeline operators who had controlled access were reduced to customers of PipeChina. The company that had embodied China's resource nationalism was being dismembered in the name of market reform.

Yet there was also opportunity in the chaos. With PipeChina handling midstream logistics, PetroChina could focus on what it did best: finding and producing hydrocarbons. The company's technical expertise, honed over decades, remained valuable. Its relationships with international partners endured. Its understanding of China's energy needs was unmatched.

More importantly, PetroChina remained the Chinese government's primary tool for energy security. When gas supplies tightened in winter, Beijing turned to PetroChina. When new fields needed development, PetroChina got the call. When China needed someone to negotiate with Russia or Central Asia, PetroChina led the talks. The company might have lost its pipeline monopoly, but it remained indispensable.

As 2025 dawns, PetroChina stands at a crossroads. The old model—vertical integration, state monopoly, fossil fuel dominance—is dying. The new model—market competition, energy transition, carbon neutrality—remains undefined. The company operates in a strange twilight, too important to fail but too constrained to dominate, too fossil to be green but too invested in renewables to be brown.

IX. Playbook: Lessons from State Capitalism

The PetroChina story offers a masterclass in the paradoxes of state capitalism—a system that promises market efficiency with socialist control but delivers neither fully. As we've seen through corruption scandals, safety disasters, and forced restructuring, the attempt to serve two masters—the market and the Party—creates unique pathologies that neither pure capitalism nor pure socialism would produce.

The Paradox of Market Listing with State Control

When More than 85 percent of shares outstanding - 157.9 billion shares - held by parent company CNPC unlikely to trade in market, what exactly is being traded? PetroChina's listing created a bizarre creature: a publicly traded company where public shareholders have no real say. The state controlled appointments, strategy, and capital allocation while minority shareholders provided capital and legitimacy.

This arrangement worked during boom times. International investors accepted limited influence in exchange for exposure to China's growth. But when crisis hit—corruption scandals, safety disasters, forced restructuring—minority shareholders discovered they had no recourse. They couldn't change management, influence strategy, or even get accurate information. They were passengers on a ship steered by political winds.

The 2007 Shanghai listing epitomized this dysfunction. Mainland retail investors, barred from international markets, bid PetroChina to a trillion-dollar valuation while sophisticated investors in Hong Kong and New York sold. Same company, same assets, wildly different prices—all because the state created artificial scarcity through capital controls. This wasn't price discovery; it was price manipulation through market segmentation.

Managing Corruption in a State-Owned Enterprise

The anti-corruption campaign revealed a fundamental truth: when your largest shareholder is the government, corruption isn't a bug—it's a feature. Zhou Yongkang didn't just steal money; he built an entire shadow governance system within PetroChina. His network controlled promotions, contracts, and investments based on loyalty rather than performance.

Traditional corporate governance mechanisms failed completely. Independent directors weren't independent. Auditors reported to management, not shareholders. Regulators were often former PetroChina executives. The board of directors was subordinate to the Party committee. Every safeguard was compromised because everyone answered to the same political master.

The cleanup wasn't really about eliminating corruption—it was about changing who controlled it. Xi Jinping's campaign destroyed Zhou's network but immediately replaced it with Xi's own loyalists. The new executives were just as political as the old ones, just aligned with different faction. Corruption decreased not because systems improved but because everyone was terrified of being next.

Safety vs. Growth Trade-offs in Rapid Industrialization

The Qingdao explosion exposed the lethal mathematics of state capitalism: growth targets are mandatory, safety standards are optional. Local officials knew pipelines built for rural areas now ran under cities. They knew corrosion was accelerating. They knew safety systems were inadequate. But meeting GDP targets mattered more than preventing disasters.

This wasn't simple negligence—it was systemic. Human behaviors should be taken into account in evaluation of project management, with 9 of 19 underlying causes of project failure being behaviors of principal participants. In PetroChina's case, those behaviors were shaped by political incentives that rewarded volume over safety, speed over sustainability.

After Qingdao, the government mandated comprehensive safety reviews. But the fundamental tension remained: how do you slow down for safety when your political legitimacy depends on economic growth? The answer was theater—visible safety campaigns that didn't actually slow production, new regulations that weren't enforced, investigations that blamed individuals rather than systems.

Competition Dynamics When Your Largest Shareholder is the Government

PetroChina never truly competed—it performed competition. When foreign companies entered China, PetroChina partnered with them, learned from them, then used regulatory changes to marginalize them. When domestic competitors emerged, PetroChina used its pipeline control to strangle them. When market forces threatened profitability, the government adjusted regulations to protect margins.

The establishment of PipeChina revealed this pseudo-competition. Once pipeline access was neutralized, PetroChina suddenly faced real competition for the first time. Its response was telling: instead of becoming more efficient, it sought new forms of protection through environmental regulations, local content requirements, and strategic sector designations.

International expansion followed similar patterns. PetroChina didn't compete for assets—it overwhelmed them with state capital. Projects that made no commercial sense proceeded because they served political objectives. The company paid premiums Western companies couldn't justify because profit wasn't the only metric. This wasn't competition—it was mercantilism with corporate characteristics.

International Expansion Under Geopolitical Constraints

Every PetroChina international deal carried invisible political baggage. The company couldn't just buy oil fields—it had to advance China's foreign policy. Assets in Sudan supported China's Africa strategy. Pipelines from Russia embodied the Sino-Russian partnership. Investments in Iran defied American sanctions. PetroChina was simultaneously a company and an instrument of statecraft.

This dual identity created constant friction. Commercial teams negotiated deals that political officials vetoed. Countries welcomed PetroChina's capital but feared its government connections. Partners wanted PetroChina's money but not its politics. Every transaction became a diplomatic negotiation, every contract a potential international incident.

The Belt and Road Initiative crystallized these contradictions. PetroChina built pipelines that made no commercial sense because they created political dependencies. It accepted returns below market rates because influence mattered more than profit. It invested in unstable countries because instability created opportunity for Chinese influence. This was resource imperialism with Chinese characteristics—softer than Western colonialism but harder than pure commerce.

The Innovation Paradox

State ownership should theoretically enable long-term thinking and patient capital for innovation. In practice, PetroChina exemplified the opposite. Political cycles drove short-term thinking. Five-year plans locked in outdated strategies. Bureaucratic culture stifled creativity. The company excelled at copying Western technology but struggled to innovate beyond it.

The shale gas experience was instructive. PetroChina spent billions acquiring North American shale assets not for production but for knowledge transfer. It hired Western experts, bought Western equipment, copied Western techniques. But when it tried to apply these methods to China's more complex geology, results disappointed. Innovation requires failure tolerance that political systems can't provide.

The renewable energy pivot faces similar challenges. PetroChina can build solar farms and wind turbines—that's engineering. But can it innovate in energy storage, hydrogen production, or carbon capture? History suggests it will excel at deployment but struggle with breakthrough innovation. State capitalism optimizes for scale, not creativity.

The Governance Impossibility

PetroChina's governance structure defies Western corporate logic. The board of directors is subordinate to the Party committee. The CEO reports to political officials who may know nothing about energy. Strategic decisions require approval from multiple ministries with conflicting agendas. International investors demand transparency that political sensitivity forbids.

This isn't mismanagement—it's dual management. Every decision must satisfy commercial logic and political requirements. Every executive must serve shareholders and the Party. Every disclosure must inform markets without revealing state secrets. The result is paralysis disguised as process, opacity disguised as oversight.

Reform attempts consistently fail because they address symptoms, not causes. Independent directors can't be independent when the state controls their appointment. Audit committees can't ensure accuracy when political considerations override accounting principles. Risk management can't function when the biggest risks are political and undiscussable. Governance reform without political reform is theater.

The Efficiency Trap

State capitalism promises to combine market efficiency with state capacity. PetroChina demonstrates the opposite: market listing didn't improve efficiency, and state ownership undermined capacity. The company remains bloated despite repeated restructuring. Productivity lags international peers despite massive investment. Returns on capital consistently disappoint despite monopolistic advantages.

This inefficiency isn't accidental—it's structural. PetroChina must maintain employment even when automation would improve efficiency. It must support local suppliers even when imports are cheaper. It must develop marginal fields that private companies would abandon. It must maintain strategic reserves that generate no return. Every inefficiency serves a political purpose that trumps commercial logic.

The PipeChina separation epitomized this dynamic. Separating pipelines from production should improve efficiency through specialization. Instead, it created two inefficient companies where there was one, duplicate bureaucracies, and coordination problems. The reform improved market access but reduced system efficiency—a perfect metaphor for state capitalism's contradictions.

The Accountability Vacuum

When everyone is responsible, no one is responsible. PetroChina's disasters—corruption, explosions, environmental damage—consistently reveal the same pattern: elaborate responsibility matrices where accountability disappears. The Qingdao explosion involved PetroChina, local government, safety regulators, urban planners—all responsible, none accountable.

This vacuum isn't oversight—it's design. Clear accountability would require clear authority, which would threaten Party control. Better to maintain ambiguous responsibility that preserves political flexibility. When disasters occur, blame individuals rather than systems. When successes happen, credit the system rather than individuals. This asymmetry ensures the Party wins regardless of outcomes.

The corruption crackdown illustrated this perfectly. Hundreds of executives were prosecuted, but the system that enabled corruption remained unchanged. Zhou Yongkang was imprisoned, but the fusion of political and corporate power continued. Individual accountability substituted for systemic reform, allowing the Party to claim victory while preserving the structures that enable future corruption.

Lessons for Global Investors

For international investors, PetroChina offers sobering lessons about state capitalism's realities. Minority shareholders have no real rights regardless of legal structures. Political risk overwhelms commercial risk. Transparency is impossible when state secrets are involved. Governance is theatrical when real power lies elsewhere.

Yet walking away isn't simple either. PetroChina remains one of the world's largest energy companies, controlling resources every economy needs. Its transformation—or failure to transform—will shape global energy markets. Its pivot to renewables could accelerate or retard the energy transition. Investors can't ignore it even if they can't influence it.

The key insight is that investing in state-owned enterprises isn't really equity investment—it's political arbitrage. Returns depend more on government policy than corporate performance. Success requires reading political tea leaves rather than financial statements. This isn't traditional investing—it's betting on state capitalism's contradictions resolving favorably.

The Sustainability Contradiction

PetroChina now claims leadership in China's energy transition while remaining its largest fossil fuel producer. This isn't hypocrisy—it's the logical outcome of state capitalism. The government demands carbon neutrality and energy security simultaneously. PetroChina must deliver both, regardless of their incompatibility.

The company's renewable investments are real but contextually marginal. Solar and wind projects generate headlines but minimal revenue. Hydrogen research proceeds slowly while oil production continues at full pace. Carbon capture pilots operate while new gas fields are developed. This isn't transition—it's addition. PetroChina isn't replacing fossil fuels with renewables; it's adding renewables to fossil fuels.

This contradiction reflects China's broader challenge: how to maintain growth while reducing emissions, ensure energy security while transitioning from fossil fuels, compete globally while restructuring domestically. PetroChina embodies these tensions without resolving them. It's simultaneously part of the problem and the solution, too big to fail and too fossil to succeed.

X. Bear vs. Bull Case & Investment Analysis

Standing in 2025, PetroChina presents one of the most complex investment puzzles in global markets. In the 2020 Forbes Global 2000, PetroChina was ranked as the 32nd-largest public company in the world, yet its valuation tells a different story—one of persistent discounts, governance concerns, and fundamental questions about its future in a decarbonizing world.

The Bear Case: Structural Headwinds Intensifying

The bear thesis starts with corruption's long shadow. Despite the anti-corruption campaign's official conclusion, its impact persists. The destruction of entire management layers created a expertise vacuum. Risk-taking evaporated as executives prioritized political safety over commercial performance. Decision-making slowed to a crawl as every choice required political clearance. The company lost not just corrupt executives but institutional knowledge, international relationships, and operational dynamism.

The safety record remains alarming. While Qingdao happened to Sinopec, PetroChina operates similar aging infrastructure across China. Thousands of kilometers of pipelines built decades ago now run through urban areas. Maintenance has been deferred to meet production targets. Safety culture remains subordinate to growth mandates. The next disaster isn't if but when—and markets know it.

State interference has intensified, not decreased. The PipeChina separation wasn't liberalization but reorganization of state control. Price controls persist when inflation threatens. Production quotas override commercial logic. International investments require political approval that may never come. The company operates less like a corporation and more like a ministry with a stock listing.

The energy transition poses existential threats. China's 2060 carbon neutrality pledge means peak oil demand within a decade. Stranded asset risks are massive—thousands of wells, refineries, and petrochemical plants that may never recover their investments. The company's renewable investments are too small to offset declining fossil fuel revenues. PetroChina is structured for a world that's disappearing.

International tensions compound every challenge. Technology restrictions limit access to advanced extraction techniques. Financial sanctions threaten dollar funding. Market access barriers constrain expansion options. Every geopolitical friction between China and the West hits PetroChina directly. The company is uniquely vulnerable to deglobalization.

Massive market value bears little relation to profitability—first half net income $10.9 billion vs. ExxonMobil's $19.5 billion during same period. This isn't just lower margins—it's structural inefficiency that no amount of reform has fixed. Returns on capital remain below cost of capital. Free cash flow barely covers dividends. Growth requires capital that generates inadequate returns.

The Bull Case: Irreplaceable Strategic Value

The bull thesis rests on a simple reality: China needs energy, and PetroChina controls it. Demand may peak, but it won't disappear. Even in 2050, China will consume millions of barrels of oil daily. Someone must produce, refine, and distribute it. PetroChina's infrastructure is irreplaceable, its expertise unmatched, its government relationship unbreakable.

China's energy security imperatives trump everything else. No Chinese leader will allow energy dependence on potentially hostile nations. PetroChina is the guarantee against energy blackmail. Its value isn't just commercial but strategic. The government will support it regardless of economics because the alternative—energy vulnerability—is unacceptable.

The infrastructure monopoly, even post-PipeChina, remains formidable. Thousands of gas stations, refineries, storage facilities, and distribution networks can't be replicated. Competitors need decades and trillions of yuan to match PetroChina's physical presence. This infrastructure becomes more valuable as China shifts to gas and eventually hydrogen—both requiring PetroChina's assets.

The gas transition benefits PetroChina disproportionately. Gas demand will double by 2035 as coal plants close. PetroChina controls most domestic gas production and long-term import contracts. PipeChina separation actually helps by providing neutral access to PetroChina's gas at regulated returns. The company pivots from oil major to gas utility—lower growth but stable returns.

Government support remains unconditional. When markets need stabilization, PetroChina provides it. When strategic assets become available, PetroChina acquires them. When national champions are needed, PetroChina answers. This isn't subsidy—it's symbiosis. The government needs PetroChina as much as PetroChina needs the government.

The renewable option value is underappreciated. PetroChina's land holdings, rights of way, and grid connections position it perfectly for renewable development. Oil fields become solar farms. Pipelines carry hydrogen. Refineries produce chemicals for batteries. The energy transition doesn't obsolete PetroChina—it transforms it.

International expansion, while constrained, isn't finished. Belt and Road continues despite Western opposition. Energy relationships with Russia, Central Asia, and the Middle East deepen. Technology restrictions accelerate domestic innovation. Deglobalization creates protected markets where PetroChina dominates. Isolation becomes insulation.

The Mainland Premium Puzzle

The valuation disparities between PetroChina's listings reveal market segmentation's persistence. Shanghai trades at premiums to Hong Kong, which trades at premiums to New York. Same company, same assets, different prices. This isn't efficiency—it's evidence that politics trumps economics in pricing PetroChina.

The mainland premium reflects captive demand. Chinese retail investors have limited alternatives. Capital controls prevent international diversification. Domestic institutions must hold state-owned enterprises. PetroChina benefits from forced buyers who accept lower returns. This isn't sustainable, but it's proven durable.

Arbitrage opportunities exist but can't be exploited. Dual-listing arbitrage requires capital mobility that doesn't exist. Regulatory restrictions prevent shorting in Shanghai while buying in Hong Kong. The price disparities that shouldn't exist in efficient markets persist because these aren't efficient markets—they're politically segmented markets.

Scenario Analysis: Three Futures

Scenario 1: Managed Decline (40% probability) Oil demand peaks by 2030. PetroChina manages gradual production declines while growing gas modestly. Renewable investments remain marginal. The company becomes a utility—stable but uninspiring. Dividends continue but growth ends. Stock prices drift lower as investors rotate to growth sectors. This is the most likely path—slow adjustment to a lower-carbon world without dramatic transformation.

Scenario 2: Energy Transformation (35% probability) China accelerates decarbonization. PetroChina genuinely pivots to renewables and hydrogen. Stranded assets are written off, but new energy investments compensate. The company emerges as China's renewable energy champion. Valuations recover as transformation credibility builds. This requires political will and capital that may not materialize, but it's possible if energy security fears drive radical change.

Scenario 3: Geopolitical Crisis (25% probability) Taiwan conflict or energy blockade forces China into autarky. PetroChina becomes a war economy enterprise. Production maximizes regardless of economics. Government support becomes unlimited. International investors are forced out. The company survives but becomes uninvestable for foreigners. This is the tail risk that could destroy international shareholder value overnight.

Investment Recommendation: Structural Underweight

PetroChina is uninvestable for traditional equity investors seeking risk-adjusted returns. Governance will never meet Western standards. Transparency will remain limited. Minority shareholders will never have real influence. Political risk overwhelms commercial opportunity. The company is a sovereign proxy, not an independent enterprise.

For index investors, PetroChina is unavoidable but should be minimized. Hold market weight in emerging market indices but avoid overweight positions. The company's size ensures index inclusion, but its characteristics argue against active positions. This is a ticket you hold, not a stock you own.

For sovereign wealth funds and strategic investors, PetroChina offers different calculus. Energy security, government relationships, and strategic access may justify investments that pure financial returns don't support. But these investors are buying political options, not equity returns.

For retail investors, especially in China, PetroChina represents something beyond investment—it's participation in national development. The financial returns may disappoint, but the psychological returns of owning China's energy champion compensate. This isn't investing—it's patriotism with dividends.

The Valuation Paradox

PetroChina trades at deep discounts to global peers on every metric—price-to-earnings, price-to-book, enterprise value to reserves. Bears say this reflects governance discounts and transition risks. Bulls argue it represents deep value in strategic assets. Both are right, which is why the discount persists.

The market can't properly value PetroChina because it's not really a market company. Its assets have strategic value beyond commercial worth. Its liabilities include political obligations not on any balance sheet. Its future depends on government decisions that markets can't predict. Traditional valuation models break down when applied to state capitalist enterprises.

This valuation paradox won't resolve until PetroChina's fundamental identity clarifies. Is it a commercial enterprise or policy instrument? A fossil fuel company or energy transition vehicle? A national champion or international competitor? Until these questions are answered, the stock will trade at discounts that reflect not just risk but fundamental uncertainty about what PetroChina really is.

The investment conclusion is unsatisfying but unavoidable: PetroChina is too important to ignore but too compromised to embrace. It's a company caught between worlds—public and state, commercial and political, fossil and renewable, Chinese and global. Investors must decide not whether PetroChina is a good investment, but whether they can accept the contradictions that define it. For most, the answer remains no.

XI. Epilogue: The Future of Chinese Energy

As dawn breaks over Beijing in 2025, PetroChina's headquarters stands as a monument to China's energy contradictions. The company that once symbolized China's resource nationalism now embodies its energy uncertainties. The transformation from oil ministry to market enterprise to whatever comes next remains incomplete, perhaps incompletable.

PipeChina's Role in Market Liberalization

The great pipeline experiment continues to evolve in unexpected ways. PipeChina, intended as a neutral carrier, has become another tool of state planning. Instead of creating a competitive gas market, it's created a different monopoly—one that controls access rather than production. The promise of third-party access remains partially fulfilled. Independent producers gained entry, but terms still favor incumbents. International suppliers find PipeChina easier to work with than PetroChina, but still encounter bureaucracy, political interference, and arbitrary rule changes.

Yet something has changed. The mere existence of PipeChina proves that China can restructure state enterprises when necessity demands. The precedent is set: if pipelines can be separated, what else might be unbundled? Refining? Distribution? The possibility of further reform, however remote, alters calculations for everyone—PetroChina, competitors, and investors alike.

The Renewable Energy Pivot and Dual Carbon Goals

China's 2060 carbon neutrality pledge transforms PetroChina from energy solution to climate problem. The company producing 3.7 million barrels of oil equivalent daily can't simply become a solar farm operator. The transition mathematics don't work—renewable investments can't offset fossil fuel revenues quickly enough to maintain financial viability while meeting climate goals.

PetroChina's response reveals state capitalism's advantages and limitations. The company can mobilize massive capital for renewable projects because profitability isn't the only metric. It can build infrastructure that private companies wouldn't touch because government support is assured. But it can't innovate quickly because bureaucracy strangles creativity. It can't pivot radically because employment and energy security constrain flexibility.

The dual carbon goals create temporal tensions PetroChina can't resolve. Peak emissions by 2030 requires maximum fossil fuel production now to power the renewable infrastructure build-out. Carbon neutrality by 2060 demands those same assets become stranded. PetroChina must simultaneously accelerate and decelerate, expand and contract, invest and divest. This isn't strategy—it's schizophrenia.

Geopolitical Implications

Every PetroChina pipeline is a geopolitical statement. The Power of Siberia declares Sino-Russian energy partnership. Central Asian pipelines embody China's Eurasian strategy. Myanmar connections project influence into the Indian Ocean. These aren't just energy infrastructure—they're the physical manifestation of China's worldview.

But infrastructure creates vulnerabilities alongside opportunities. Pipelines can be sabotaged. Shipping lanes can be blockaded. Supplier relationships can be severed. PetroChina's international expansion, meant to enhance energy security, has created new insecurities. Every foreign asset is a potential hostage in geopolitical conflicts.

The Russia relationship epitomizes these dynamics. China needs Russian gas to replace coal. Russia needs Chinese markets as Europe decouples. This mutual dependence should create stability, but instead generates friction. Price negotiations become political battles. Pipeline routes carry strategic implications. Energy cooperation merges with military alignment. PetroChina finds itself not just buying gas but underwriting Putin's regime.

Middle Eastern relationships grow more complex as China's energy needs evolve. Saudi Arabia and Iran compete for Chinese market share while PetroChina navigates their regional rivalry. Every oil contract requires diplomatic balancing. Every investment decision has political ramifications. The company operates less like a corporation and more like an energy embassy.

Competition with International Oil Companies and New Energy Players

PetroChina faces competition it never anticipated from companies that didn't exist a decade ago. Tesla's charging networks threaten gas station revenues. BYD's electric vehicles reduce gasoline demand. Contemporary Amperex Technology's batteries enable distributed energy that bypasses PetroChina's infrastructure entirely. The threat isn't from ExxonMobil or Shell—it's from technology companies that make oil irrelevant.

International oil companies, meanwhile, undergo their own transformations that pressure PetroChina. BP promises net-zero emissions. Shell expands into electricity trading. Total rebrands as TotalEnergies. These aren't just marketing exercises—they're fundamental pivots that make PetroChina's incrementalism look antiquated. The company that once led through scale now lags through inertia.

New energy players—solar manufacturers, wind developers, battery producers—operate with advantages PetroChina can't match. They're unburdened by stranded assets, legacy workforces, or political obligations. They attract capital that flees fossil fuels. They embody the future while PetroChina represents the past. Competition isn't about who produces energy cheapest but who enables the energy transition fastest.

What PetroChina Tells Us About China's Economic Model

PetroChina is China in corporate form—ambitious yet constrained, modern yet traditional, market-oriented yet state-controlled. Its struggles mirror China's broader challenges: How to maintain growth while reducing emissions? How to ensure security while integrating globally? How to preserve control while enabling innovation?

The company's trajectory reveals state capitalism's limitations. Political control prevents true corporate governance. Employment obligations constrain efficiency improvements. Strategic responsibilities override commercial logic. The model that enabled rapid industrialization now impedes necessary transformation. PetroChina can't evolve beyond what China's political economy allows.

Yet PetroChina also demonstrates state capitalism's resilience. Despite corruption scandals, the company continues operating. Despite inefficiencies, it meets energy needs. Despite contradictions, it generates returns. The model may be suboptimal, but it's proven durable. PetroChina survives not despite state ownership but because of it.

The Unresolved Questions

As PetroChina approaches its third decade, fundamental questions remain unanswered:

Can a state-owned enterprise truly operate commercially when political imperatives dominate? PetroChina's history suggests no, but China's development demands yes.

Is gradual energy transition possible, or does decarbonization require disruption that destroys incumbent advantages? PetroChina bets on evolution, but revolution may be unavoidable.

Will geopolitical tensions force energy autarky, or can interdependence survive strategic competition? PetroChina plans for cooperation but prepares for conflict.

Can China achieve energy security and carbon neutrality simultaneously? PetroChina must deliver both, but physics and economics suggest they're incompatible.

Does PetroChina's future lie in transformation or replacement? The company assumes it will adapt, but history is littered with industrial giants that couldn't evolve quickly enough.

The Path Forward

PetroChina's next chapter depends less on corporate strategy than political decisions beyond its control. If China prioritizes energy security, PetroChina remains central. If climate dominates, the company becomes obsolete. If reform accelerates, PetroChina might genuinely transform. If political control tightens, it remains a ministry with shareholders.

The most likely path is typically Chinese—pragmatic adaptation without fundamental reform. PetroChina will become less oil-focused without abandoning oil. It will invest in renewables without leading the transition. It will improve governance without achieving independence. It will remain important but diminished, essential but struggling.

For investors, PetroChina offers a window into China's energy future—cloudy, contradictory, but consequential. The company's fate matters beyond financial returns. Its success or failure shapes global energy markets, influences climate outcomes, and reflects China's development model viability.

For China, PetroChina represents both achievement and challenge. The company that helped power China's rise now complicates its future. The enterprise that symbolized resource strength now embodies energy weakness. The corporation that was solution has become problem.

For the world, PetroChina embodies the complexity of energy transition in developing economies. The company can't simply abandon fossil fuels when billions depend on them. It can't ignore climate change when its emissions threaten everyone. It must navigate between imperatives that developed countries never faced simultaneously.

Final Thoughts

PetroChina's story isn't finished—it's entering its most critical phase. The next decade will determine whether it transforms into a new energy company or manages decline as a legacy fossil fuel producer. Whether it helps China achieve carbon neutrality or becomes the biggest obstacle. Whether it proves state capitalism can adapt or demonstrates its ultimate limitations.

The company stands at the intersection of every major global challenge—energy security, climate change, technological disruption, geopolitical competition. Its responses will ripple far beyond China's borders. PetroChina may have begun as China's national oil company, but it's become something more: a test case for whether incumbent energy giants can navigate the greatest transition in industrial history.

As night falls again over Beijing, PetroChina's headquarters illuminates the skyline—a beacon of China's energy ambitions and anxieties. Inside, engineers and executives grapple with challenges that have no easy solutions, pursuing strategies that may prove impossible, serving masters whose demands conflict fundamentally.

This is PetroChina's burden and opportunity: to reconcile the irreconcilable, to transform while maintaining stability, to decline while growing, to end while beginning. It's an impossible task that must somehow be accomplished. The alternative—failure—is unthinkable for China and consequential for everyone.

The story continues, uncertain but urgent, with PetroChina at its center—no longer the solution but still essential, no longer dominant but still indispensable, no longer the future but not yet the past.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube