Eugene Technology: The Quiet Giant Behind Korea's Semiconductor Revolution

I. Introduction & Opening

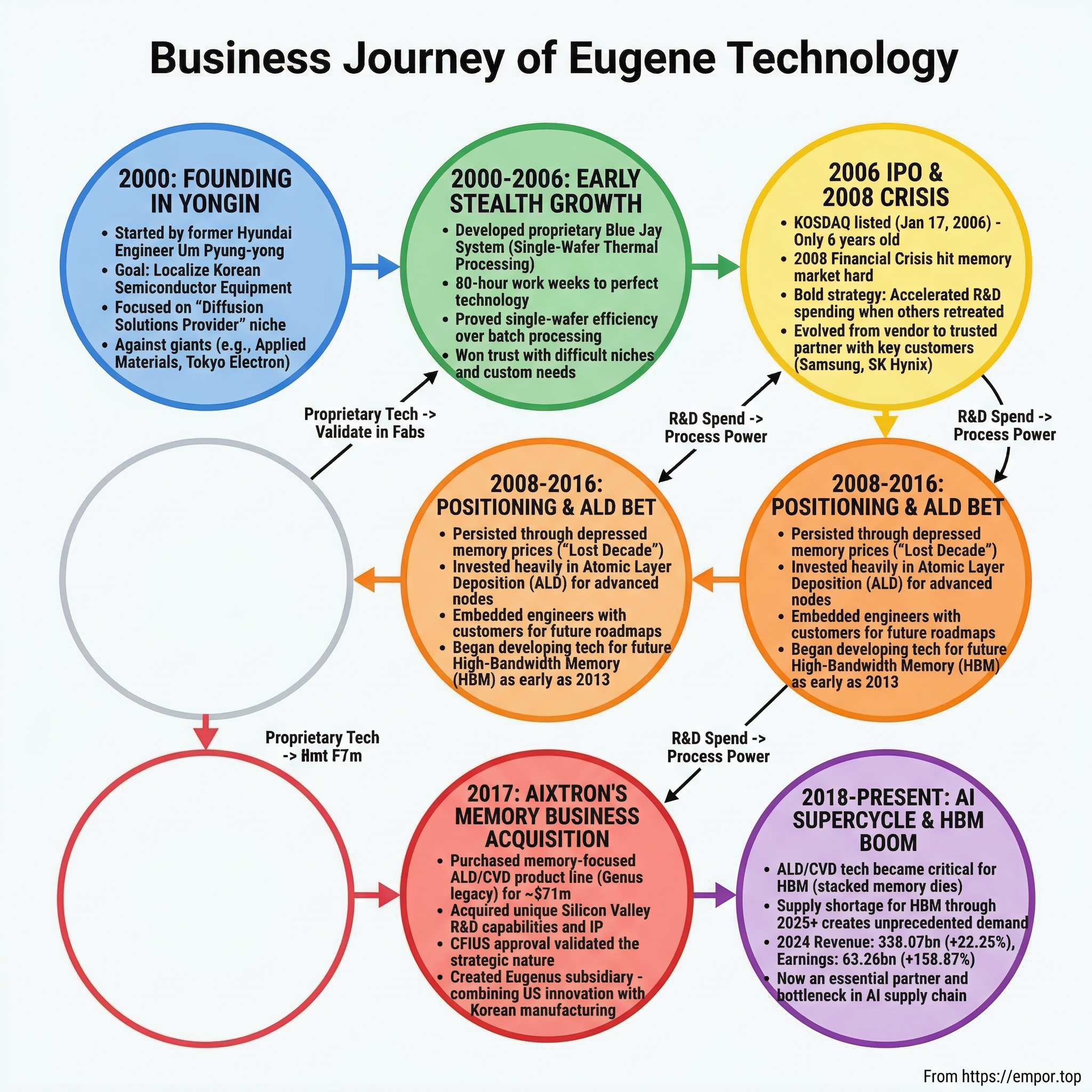

Picture the rain-soaked streets of Yongin in January 2000, where a small group of engineers gathered in a nondescript office building with an audacious dream: to build Korea's answer to the global semiconductor equipment oligopoly. They had no brand recognition, no established customer base, and were up against giants like Applied Materials and Tokyo Electron who had decades of experience and billions in resources. Yet within six years, they would be publicly listed, and within two decades, they'd become a critical supplier to the memory titans powering the AI revolution.

Eugene Technology Co.,Ltd. was founded in 2000 and is headquartered in Yongin, South Korea, emerging at a pivotal moment when Korea's semiconductor industry was transforming from fast follower to global leader. The timing was no accident—Samsung and SK Hynix (then Hyundai Electronics) were beginning their ascent to memory dominance, but they remained dangerously dependent on foreign equipment suppliers who could dictate terms, timelines, and prices.

The central question that drives our story today isn't just how a startup cracked one of the hardest markets in semiconductors—it's how Eugene Technology positioned itself perfectly for not one, but two major industry inflections: the mobile revolution that drove memory demand in the 2010s, and now the AI supercycle that's creating unprecedented shortages of advanced memory equipment. This is a tale of David versus Goliath, strategic patience, and the power of being in the right place at precisely the right time.

What makes Eugene's journey particularly fascinating is their counter-intuitive strategy: while competitors chased broad market opportunities, Eugene doubled down on single-wafer diffusion technology—a niche that seemed limited in 2000 but would become critical as semiconductor nodes shrank and precision became paramount. They bet their entire company on the idea that Korean memory makers would eventually need a trusted local partner who could match global equipment standards while providing the responsiveness and customization that distant suppliers couldn't.

II. The Pre-History: Korea's Semiconductor Awakening

The late 1990s were a crucible for Korea's semiconductor industry. The Asian Financial Crisis had just swept through the region, leaving corporate giants like Hyundai and LG bloodied but not beaten. Hyundai faced near collapse during the chip industry's downturn in 2001, when global memory chip prices dropped by 80 percent, resulting in a 5 trillion won annual loss for the company. Yet from this chaos emerged opportunity—the crisis forced brutal consolidation that would ultimately strengthen Korea's position.

In this tumultuous environment, a former Hyundai Electronics engineer named Um Pyung-yong saw a gap that no one else was addressing. After graduation, he began his career in the semiconductor industry by working at Hyundai Electronics (now SK Hynix). In 2000, he founded Eugene Technology as an independent venture. Um had witnessed firsthand how Korean chipmakers were held hostage by foreign equipment suppliers—not just on price, but on something far more valuable: time. When Samsung or Hyundai needed custom modifications for their processes, they'd wait months for responses from suppliers in California or Tokyo.

Established on January 5, 2000, it was designated as a venture company in July, and a corporate research center was established in November, recognized by the Korea Industrial Technology Association in January of the following year. This wasn't just another semiconductor startup—it was a deliberate attempt to build Korea's first truly independent equipment capability.

The founding vision was elegantly simple yet technically ambitious: becoming a "Diffusion Solution Provider." While the term might sound generic, it represented a specific bet on single-wafer processing technology—a radical departure from the batch processing that dominated the industry. Eugene's engineers believed that as chips became more complex and costly, manufacturers would need equipment that could process each wafer individually with atomic-level precision.

The equipment gap facing Korea was stark. In 2000, over 90% of semiconductor equipment in Korean fabs came from foreign suppliers. This dependency wasn't just about money flowing overseas—it was about innovation speed. Every time Samsung wanted to tweak a process, they had to convince a supplier in San Jose that it was worth their time. Every time SK Hynix needed urgent support, they waited for technicians to fly in from Tokyo. Eugene Technology was born from the conviction that Korea needed to own its semiconductor destiny, one critical piece of equipment at a time.

III. Early Days: Building in Stealth Mode (2000-2006)

The conference room at Eugene Technology's first facility was spartan—just a whiteboard, mismatched chairs, and a single poster showing the architecture of a memory chip. But what happened in that room between 2000 and 2006 would lay the foundation for one of the most successful David-versus-Goliath stories in semiconductor history.

Launched with our own proprietary technology, we have grown rapidly to become a KOSDAQ-listed company in only 6 years. But "rapidly" understates the intensity of those early years. The team worked 80-hour weeks developing their flagship Blue Jay System, a single-wafer thermal processing tool that represented a complete reimagining of how diffusion should work in advanced memory production.

The technical challenge was immense. EUGENE TECHNOLOGY, starting with novel 'Nitride' processes, and soon adding Poly and Oxide steps, became the only company providing 'Single Wafer' diffusion solutions. This wasn't just about building equipment—it was about convincing memory manufacturers to abandon batch processing methods they'd used for decades. Eugene's engineers had to prove that processing wafers one at a time could actually be more efficient, more precise, and ultimately more profitable than the traditional approach.

Our flagship product line, the 'Blue Jay System' has been in volume production on core Front End of Line (FEOL) processes at leading global for 5 years, meeting stringent quality, technology, and productivity requirements. The breakthrough came when Samsung's engineers, frustrated with the inflexibility of their existing equipment, agreed to test Eugene's prototype. The results were revelatory: not only did the Blue Jay System match the performance of established equipment, but its single-wafer architecture allowed for process adjustments that were impossible with batch systems.

Breaking into global semiconductor fabs required more than just good technology—it demanded a level of trust that typically took decades to build. Eugene's strategy was brilliantly subversive: instead of trying to compete head-on with established players for major contracts, they targeted the most challenging, least profitable niches that big suppliers ignored. These "problem child" processes—where yields were low and customization needs were high—became Eugene's training ground.

Eugene technology co.,ltd completed its initial public offering (IPO) on January 17 ,2006, just six years after founding. The IPO raised modest funds by global standards, but it represented something far more valuable: validation. A Korean equipment company had gone from zero to public listing faster than any of its domestic competitors, and major memory manufacturers were now using its equipment in production.

IV. Going Public During Turbulence: The 2006 IPO and 2008 Crisis

January 17, 2006 should have been a day of pure celebration for Eugene Technology. The company had just completed its IPO on the KOSDAQ, achieving in six years what most semiconductor equipment companies never accomplish. Yet CEO Um Pyung-yong spent that morning not at celebration parties, but in Samsung's fab, personally overseeing a critical installation. This dual focus—capital markets and customer floors—would define Eugene's approach through the coming turbulence.

The timing of the IPO seemed perfect. Memory markets were booming, driven by the explosion of consumer electronics. Every flip phone needed memory, every digital camera required storage, and Eugene's equipment was helping produce these chips. The company's order book was full, and investors were enthusiastic about Korea's first pure-play semiconductor equipment story.

Then came 2008. The global financial crisis hit semiconductor markets like a tsunami. Memory prices collapsed by 85% in six months. Samsung and SK Hynix, Eugene's primary customers, slashed capital expenditures. International equipment giants like Applied Materials and Lam Research laid off thousands of workers. For a young public company with concentrated customer exposure, this should have been fatal.

Instead, Eugene did something counterintuitive: they accelerated R&D spending. While competitors retreated, Eugene's engineers worked on next-generation atomic layer deposition (ALD) technology that wouldn't be needed for years. The crisis had given them something precious—time with customers who were suddenly very interested in cost reduction and process optimization. Samsung's engineers, freed from the relentless pace of capacity expansion, could actually collaborate on long-term technology development.

The relationship transformation during this period was profound. Eugene evolved from vendor to partner. When SK Hynix needed to extend the life of older equipment to preserve cash, Eugene's engineers practically lived in their fabs, developing modifications that squeezed extra performance from aging tools. When Samsung wanted to experiment with new materials but couldn't justify buying new equipment, Eugene provided test systems at cost.

This countercyclical investment philosophy—spending when others retreated—would become Eugene's signature strategy. By the time markets recovered in 2010, Eugene had a portfolio of new technologies ready just as customers resumed spending. More importantly, they had earned something that money couldn't buy: trust forged in crisis.

V. The Lost Decade That Wasn't: Positioning for the Future (2008-2016)

The period from 2008 to 2016 is often called the "lost decade" for semiconductor equipment companies. Memory prices stayed depressed, China emerged as a competitive threat, and the industry seemed stuck in a low-growth equilibrium. Eugene Technology's stock price languished, and analysts questioned whether Korea really needed domestic equipment suppliers. Yet beneath this seemingly stagnant surface, Eugene was executing one of the most prescient strategic pivots in the industry.

While others retreated, Eugene doubled down on R&D, particularly in atomic layer deposition (ALD)—a technology that seemed unnecessarily complex for contemporary memory production but would become absolutely critical for AI-era chips. The company's engineers worked in relative obscurity, perfecting techniques for depositing films just atoms thick with perfect uniformity across entire wafers.

The partnership cultivation during this period reads like a masterclass in strategic patience. In 2024, Eugene Technology's revenue was 338.07 billion, an increase of 22.25% compared to the previous year's 276.53 billion—but this success was built on foundations laid during these "lost" years. Eugene's engineers became embedded in their customers' development teams, learning not just what equipment Samsung and SK Hynix needed today, but understanding their roadmaps for the next decade.

One particularly telling moment came in 2013. When it developed HBM chips for the first time in the world in 2013, demand for the high-performance chips was low. Most equipment suppliers dismissed high-bandwidth memory as a niche product for supercomputers. Eugene's engineers, working closely with SK Hynix, saw something different: the physical stacking of memory dies would require deposition precision that only advanced ALD could provide. They began developing specialized equipment for processes that wouldn't reach volume production for years.

The patient capital approach during these years was almost zen-like in its discipline. While investors clamored for growth, Eugene's management insisted on maintaining R&D spending at over 15% of revenue—extraordinary for an equipment company. They hired PhD physicists to work on plasma dynamics that wouldn't be commercialized for half a decade. They built cleanroom facilities for technologies that didn't yet have markets.

By 2016, Eugene had quietly assembled one of the most advanced portfolios of deposition and surface treatment technologies outside of the major global players. They had 125 patents, deep relationships with Korea's memory champions, and—crucially—expertise in the exact technologies that would be needed for the coming AI revolution. The lost decade wasn't lost at all; it was preparation for the biggest opportunity in semiconductor history.

VI. The Game-Changing Acquisition: Aixtron's Memory Business (2017)

The call came at 3 AM Seoul time in May 2017. An M&A advisor in Frankfurt had a proposition that seemed too good to be true: Aixtron, the German deposition equipment giant, was divesting its entire memory-focused ALD and CVD product line based in Silicon Valley. For Eugene Technology, this wasn't just an acquisition opportunity—it was a chance to leapfrog decades of development and establish a beachhead in the United States.

Aixtron SE of Herzogenrath, near Aachen, Germany has completed the sale of its atomic layer deposition (ALD) and chemical vapor deposition (CVD) memory product line – which is based in San Jose, CA, as part of its US subsidiary Aixtron Inc – to Eugene Technology Inc. The complexity of the deal was staggering. This wasn't just buying equipment designs—it was acquiring an entire ecosystem of intellectual property, customer relationships, and most importantly, Silicon Valley DNA.

The numbers were significant but manageable: Aixtron will receive about $60m for the assets being transferred and $11m for open supplier orders for which it retains the liability to pay. For Eugene, this represented their largest-ever investment, but the strategic value far exceeded the price tag. They were acquiring technology that Aixtron's Genus division had pioneered—the very company that first commercialized ALD for semiconductors.

Then came the regulatory maze. The Committee on Foreign Investment in the United States (CFIUS) had just blocked Chinese acquisitions of semiconductor assets, and Korean companies were under increased scrutiny. Eugene's executives spent months in Washington, demonstrating that their acquisition would actually strengthen American semiconductor capabilities by ensuring continued investment in Silicon Valley R&D. The approval finally came in October, after what insiders describe as one of the most thorough CFIUS reviews of that year.

In 2017, Eugene Technology saw the potential of its ALD and CVD products and acquired the divisions, creating Eugenus as a wholly-owned subsidiary. The integration strategy was unconventional: rather than moving technology to Korea, Eugene decided to maintain and expand the Silicon Valley operation. They renamed it Eugenus, positioning it as a "Silicon Valley startup with Korean manufacturing muscle."

Our Silicon Valley legacy began at Genus, which first commercialized atomic layer deposition (ALD), and grew its family of thin film applications for advanced semiconductors. This heritage mattered enormously. Suddenly, Eugene wasn't just a Korean equipment supplier—they owned the original ALD technology that companies like Intel and TSMC had been using for decades. The acquisition transformed Eugene from regional player to global technology holder overnight.

VII. The AI Memory Supercycle: Right Place, Right Time (2018-Present)

The transformation began quietly in 2018. A few AI researchers at OpenAI and Google started requisitioning unusual amounts of computing power for experiments with something called "transformers." Within Nvidia's Santa Clara headquarters, engineers were sketching designs for chips that would need memory bandwidth previously thought impossible. And in the conference rooms of Samsung and SK Hynix, executives were beginning to realize that artificial intelligence wasn't just another computing trend—it was about to trigger the largest demand shock in memory history.

Eugene Technology found itself at the epicenter of this revolution, though few outside Korea's semiconductor industry noticed at first. The ALD and CVD equipment they'd been perfecting for years—technology that seemed over-engineered for conventional memory—suddenly became indispensable for producing the high-bandwidth memory (HBM) that AI chips required.

South Korean memory manufacturer SK Hynix has announced that its supply of high-bandwidth memory (HBM) has been sold out for 2024 and for most of 2025. Basically, this means that demand for HBM exceeds supply for at least a year, and any orders placed now won't be filled until 2026. This shortage created a feeding frenzy among equipment suppliers. Every memory manufacturer needed to expand HBM capacity immediately, and Eugene's tools were essential for several critical process steps.

The numbers tell a story of explosive growth. In 2024, Eugene Technology's revenue was 338.07 billion, an increase of 22.25% compared to the previous year's 276.53 billion, while Earnings were 63.26 billion, an increase of 158.87%. This wasn't just riding a wave—it was validation of decades of strategic positioning.

The relationship dynamics had completely inverted from Eugene's early days. Now, Samsung and SK Hynix executives were visiting Eugene's facilities, eager to understand their technology roadmap. Samsung decided to build a PH3 production line for DRAM and other components at its semiconductor manufacturing complex in Pyeongtaek, while suspending the construction of a foundry clean room. The factory is expected to produce DRAM chips for high-bandwidth memory (HBM) chips, which will be equipped in Advanced Micro Devices Inc.'s (AMD) AI accelerators.

What made Eugene particularly valuable wasn't just their equipment, but their institutional knowledge. Their engineers had been working with Korean memory makers for over two decades, understanding not just the technology but the culture, the decision-making processes, and the unwritten rules of Korean semiconductor fabs. When SK Hynix needed to ramp HBM production at unprecedented speed, Eugene's teams could implement solutions in weeks that would take foreign suppliers months.

The current market dynamics reveal the strategic brilliance of Eugene's focus. SK Hynix took over 70% of global HBM sales in the January-March quarter after exclusively delivering 12-layer HBM3E chips, the most up-to-date HBM, to the world's most valuable AI firm Nvidia Corp.'s AI accelerators. The South Korean chip giant's victory comes after its undeterred investment in HBM development over the past 10 years. When it developed HBM chips for the first time in the world in 2013, demand for the high-performance chips was low. But the chipmaker has continued pouring in funds to advance its HBM technology.

VIII. Product Portfolio & Technical Moat

Inside Eugene Technology's demonstration facility in Yongin, a single wafer moves through the BlueJay system with balletic precision. The chamber fills with precursor gases measured in parts per billion, temperatures rise to exactly 750°C, and atomic layers deposit with uniformity measured in angstroms. This isn't just manufacturing—it's materials science at the edge of physical possibility.

It offers thermal LPCVD under the BlueJay name; plasma treatment under the Albatross name; large and mini batch thermal ALD under the Harrier-L and Harrier-M names; and dry cleaning systems under the Hawk name. Each system represents years of iterative development, thousands of customer feedback loops, and patents covering everything from gas flow dynamics to plasma generation methods.

The Albatross plasma treatment system showcases Eugene's innovation prowess. Albatross is a high density, low electron temperature, single-wafer system that meets a wide range of plasma surface treatment process needs. Advantages include patented, DUROSA antenna technology, excellent film uniformity, and lower particle generation. The DUROSA (Dual Rotated) antenna technology represents a breakthrough in plasma uniformity—a problem that had plagued the industry for decades.

Why Eugene's single-wafer approach matters becomes clear when you understand modern memory architecture. In HBM, dies are stacked like a layer cake, connected by thousands of through-silicon vias (TSVs) each thinner than a human hair. Any variation in film thickness or composition can cause electrical failures. Batch processing, where multiple wafers are processed simultaneously, introduces variabilities that become catastrophic at these scales. Eugene's single-wafer systems provide the atomic-level control that makes 12-layer and 16-layer HBM possible.

The intellectual property moat is formidable. Founded in 2000 in Korea, Eugene Technology brings a legacy of customer focus, strong R&D, and deep expertise across a wide range of semiconductor manufacturing solutions. With more than 125 patents to our name and multiple customer and industry awards, we consistently push the limits in semiconductor innovation. But patents tell only part of the story. The real moat is process knowledge—understanding exactly how to tune hundreds of parameters to achieve the perfect deposition for each customer's specific needs.

Eugene's equipment enables something remarkable: Eugene Tech's CVD and ALD systems enable precise and ultra-thin layering, meeting the industry's requirements for producing advanced semiconductor nodes with high performance. As the industry pushes toward 3-nanometer and beyond, the ability to deposit films just a few atoms thick with perfect uniformity becomes the difference between yielding chips and expensive silicon waste. Eugene has quietly become indispensable to this transition.

IX. Playbook: Strategic Lessons

Lesson 1: Being the "picks and shovels" in a gold rush

During the California Gold Rush, the real fortunes were made not by miners but by those selling them supplies. Eugene Technology understood this principle deeply. While the world focused on the memory chip makers and their astronomical profits, Eugene quietly provided the essential tools that made those profits possible. When HBM demand exploded, they didn't need to bet on which AI company would win—they were selling to everyone who needed to make memory.

Lesson 2: Geographic and customer concentration as a feature, not bug

Conventional wisdom says customer concentration is dangerous. Eugene flipped this logic. By focusing exclusively on Korean memory makers, they could embed themselves so deeply into Samsung and SK Hynix's operations that switching costs became prohibitive. They knew every process quirk, every engineer's preference, every unwritten rule. This intimacy became their competitive advantage—global competitors simply couldn't match their responsiveness and customization.

Lesson 3: Timing acquisitions for maximum strategic value

The Aixtron acquisition wasn't about getting a good price—it was about perfect timing. Eugene waited until they had the technical capability to integrate advanced ALD technology, the financial strength to make a credible bid, and most importantly, when the market was about to inflect toward technologies that Aixtron's memory division had pioneered. They paid $60 million for assets that would generate billions in revenue over the following years.

Lesson 4: The power of being a fast follower with better execution

Eugene rarely invented entirely new categories of equipment. Instead, they took existing concepts—single-wafer processing, plasma treatment, ALD—and executed them better for specific customers. They could move faster than global giants because they had fewer bureaucratic layers, deeper customer relationships, and no legacy systems to protect. This "fast follower" strategy let them avoid the risks of pioneering while capturing the rewards of superior execution.

Lesson 5: Building for the cycle after next, not the current one

The masterstroke of Eugene's strategy was always building for the future beyond the visible horizon. When they invested in HBM technology in 2013, the market was tiny. When they developed advanced ALD during the "lost decade," applications were unclear. But they understood a fundamental truth: semiconductor cycles are predictable in their unpredictability. By the time a technology becomes obviously important, it's too late to develop expertise. Eugene's discipline in building capabilities before markets emerged gave them unassailable positions when those markets exploded.

X. Power Analysis & Competitive Position

Eugene Technology's competitive moat isn't built on any single advantage but rather an interlocking system of reinforcing powers that become stronger over time. Understanding these dynamics reveals why a relatively small Korean company can compete effectively against giants with 50 times their resources.

Scale economies in semiconductor equipment work differently than in chip manufacturing. While Applied Materials can spread R&D costs across thousands of customers, Eugene's focused approach creates a different kind of scale: depth rather than breadth. Every hour of engineering time improves products for the exact processes that Samsung and SK Hynix need. This targeted scale means Eugene's R&D dollars are incredibly efficient—they're not wasting resources developing equipment for processes their customers don't use.

The switching costs embedded in Eugene's customer relationships go far beyond simple requalification expenses. When Samsung's engineers have spent years optimizing processes on Eugene's equipment, switching to another supplier means rebuilding that institutional knowledge from scratch. The cost isn't just money—it's time, yield losses during transition, and the risk of falling behind competitors. One Samsung executive privately described it as "technical marriage"—divorce is theoretically possible but practically devastating.

Network effects within the Korean semiconductor ecosystem amplify Eugene's position. Korean equipment suppliers, materials companies, and chip manufacturers have developed an intricate web of cooperation that outsiders struggle to penetrate. When SK Hynix develops a new process, Eugene's engineers are in the room from day one. When Samsung needs a Korean equipment vendor to meet local content requirements for government subsidies, Eugene is the default choice. These relationships create a virtuous cycle: the more embedded Eugene becomes, the more valuable they are to the ecosystem, which leads to even deeper embedding.

Counter-positioning against global giants represents Eugene's most subtle strategic achievement. Applied Materials and Lam Research optimize for global scale and standardization—they need products that work for hundreds of customers across dozens of countries. Eugene deliberately chose the opposite path: extreme customization for a small number of critical customers. This isn't a weakness they're trying to fix; it's their core strategy. Global competitors literally cannot match Eugene's model without destroying their own business model.

Process power through decades of learning curves compounds in ways that are nearly impossible to replicate. Eugene's engineers have seen every possible failure mode in Korean memory fabs. They know that SK Hynix's Icheon facility has slightly different contamination patterns than their Cheongju plant. They understand how Samsung's engineers think about risk. This tacit knowledge, accumulated over millions of wafer runs, creates a form of expertise that no amount of hiring or acquisition can quickly replicate.

As of the previous close price of KR₩47,950, shares in Eugene Technology Co had a market capitalisation of KR₩1tn, placing it among Korea's mid-cap technology champions. But market cap understates Eugene's strategic importance—they're a critical bottleneck in the supply chain for chips that power the entire AI revolution.

XI. Bear Case vs. Bull Case

Bear Case:

The concentration risk is undeniable and keeps Eugene's executives awake at night. With Samsung and SK Hynix representing over 80% of revenue, Eugene is essentially a derivative bet on Korean memory leadership. If China successfully develops competitive memory technology, or if American companies like Micron gain share, Eugene's growth could evaporate overnight. The company has made efforts to diversify, but the reality is that their fate remains tied to two customers.

Eugene Tech relies heavily on specialized suppliers for high-purity chemicals, precision components, and cleanroom-compatible materials. Any supply chain disruptions or quality issues with these suppliers could significantly impact production and timelines. This vulnerability was exposed during the pandemic when a single supplier's contamination issue caused weeks of delays. As equipment becomes more complex, these dependencies multiply.

Competition from larger global equipment makers intensifies every year. Applied Materials has resources to invest billions in R&D for next-generation equipment. Tokyo Electron can leverage relationships with TSMC and Intel. Chinese equipment companies, backed by government subsidies, are rapidly improving their capabilities. Eugene must run faster every year just to maintain position.

Geopolitical risks in the semiconductor industry have moved from theoretical to immediate. Export controls, technology restrictions, and the potential for forced technology transfer create constant uncertainty. If tensions between the U.S. and China escalate, Eugene could find itself caught between its need for American technology and its proximity to China.

Bull Case:

The structural shortage in advanced memory equipment could persist for years. Industry analysts project that HBM demand will grow at 40% CAGR through 2027, while equipment capacity expands at maybe 20%. This supply-demand imbalance creates pricing power that Eugene has never previously enjoyed. They can be selective about projects, demand better terms, and invest more in R&D.

AI is driving unprecedented memory demand that goes far beyond current projections. Every large language model requires massive amounts of HBM for training. Every autonomous vehicle needs high-performance memory for real-time processing. Every data center expanding for AI workloads needs more memory servers. This isn't a bubble—it's a fundamental architectural shift in computing that places memory at the center rather than the periphery.

Eugene's deep technical moat in ALD/CVD for advanced nodes becomes more valuable as Moore's Law slows. As geometric scaling reaches physical limits, the industry shifts to materials innovation—exactly where Eugene's expertise lies. Their ability to deposit exotic materials with atomic precision positions them for technologies that don't yet exist.

The valuation remains compelling despite recent gains. Trading at just 16x earnings while growing revenue at 22% and earnings at 159%, Eugene offers growth at a reasonable price in a market where AI-adjacent companies trade at astronomical multiples. The company has minimal debt, consistent cash generation, and reinvestment opportunities that should drive superior returns for years.

XII. Epilogue: The Future of Memory and Eugene's Role

Standing in Eugene Technology's R&D facility today, you can glimpse the future of computing. Engineers are working on deposition techniques for materials that didn't exist five years ago—compounds that could enable memory to operate at the speed of cache while retaining data without power. They're developing processes for 3D architectures that stack not just dies but entire functional blocks, creating computers that are more biology than electronics.

The next frontier pushes beyond traditional physics. Gate-all-around transistors, ruthenium interconnects, and ferroelectric memory require deposition precision measured not in atomic layers but in atomic positions. Eugene's engineers are developing equipment that can place individual atoms with the precision of a Swiss watchmaker and the speed of a Formula 1 pit crew. This isn't incremental improvement—it's reimagining what semiconductor manufacturing means.

Eugene's positioning for the next decade reflects hard-learned lessons about technology transitions. They're not betting on any single architecture or material winning. Instead, they're building flexible platforms that can adapt as the industry discovers what works. When Samsung announces a breakthrough in processing-in-memory architecture, Eugene's equipment is ready. When SK Hynix develops a new HBM variant, Eugene has the process technology to enable it.

What the Eugene story teaches us transcends semiconductors. It's a meditation on the value of strategic patience in an impatient world. While markets demand quarterly growth, Eugene spent decades building capabilities for opportunities that didn't yet exist. While competitors chased global scale, Eugene chose local depth. While investors questioned their customer concentration, Eugene turned dependence into symbiosis.

The company that started in a small Yongin office with dreams of semiconductor independence has become something more profound: a demonstration that in industries dominated by giants, there's still room for focused excellence. Eugene Technology didn't disrupt the semiconductor equipment industry—they did something harder. They carved out a position so essential, so precisely fitted to their customers' needs, that they became irreplaceable.

As AI drives computing toward architectures we can barely imagine, as quantum and neuromorphic processors demand new types of memory, as the industry pushes toward sustainable production, Eugene Technology stands ready. Not as the largest player, not as the most innovative, but as the partner who understands that in semiconductors, success isn't measured in quarters or even years—it's measured in decades of trust, built one atomic layer at a time.

The quiet giant of Korean semiconductor equipment may never achieve the recognition of an Applied Materials or the scale of a Tokyo Electron. But for those who understand the intricate choreography of semiconductor production, who appreciate the criticality of every process step, Eugene Technology represents something invaluable: proof that in the age of giants, there's still room for those who choose depth over breadth, patience over speed, and execution over exposition.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube