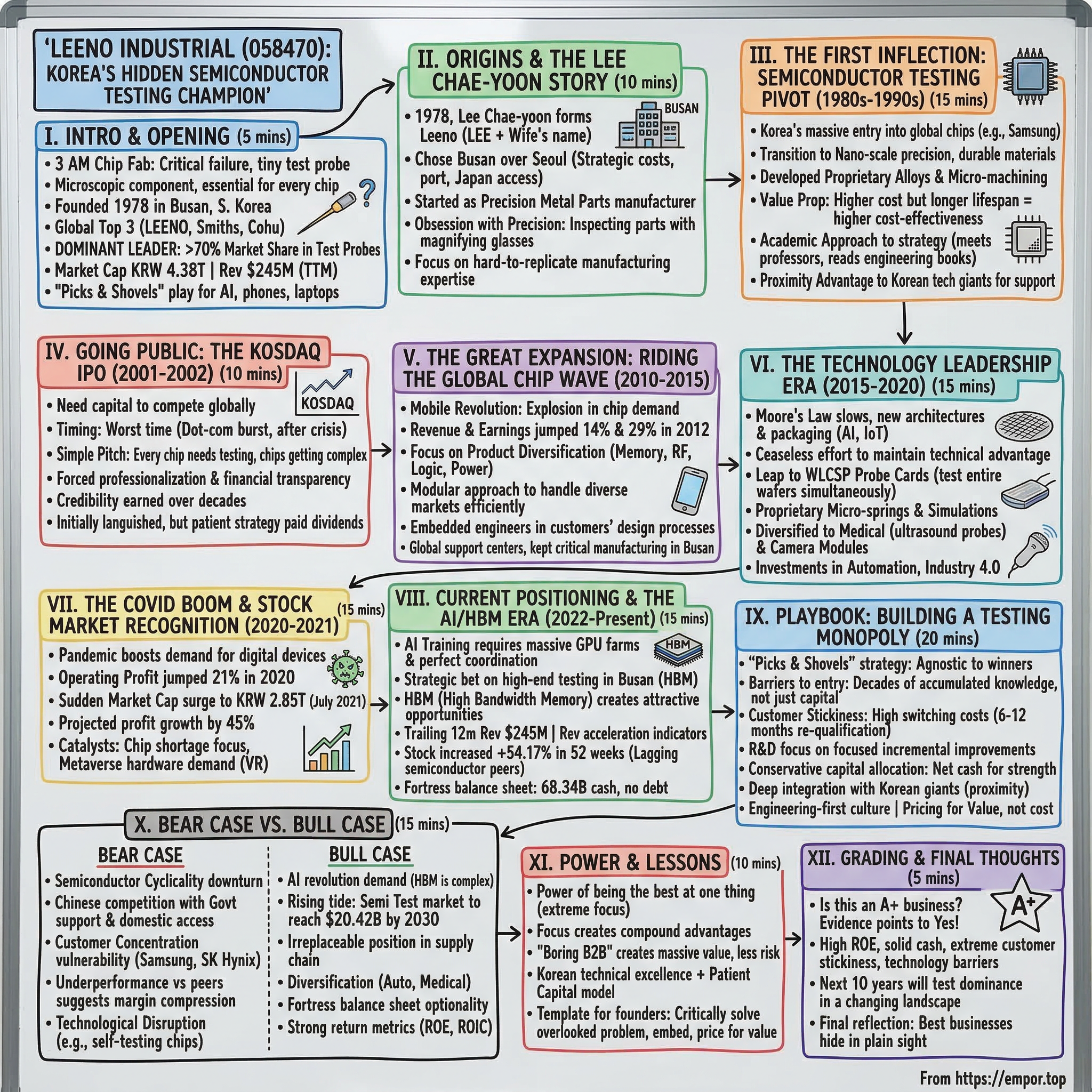

Leeno Industrial: Korea's Hidden Semiconductor Testing Champion

I. Introduction & Opening (5 minutes)

Picture a semiconductor fabrication plant at 3 AM. While automated machinery hums in clean rooms bathed in yellow light, a critical failure suddenly halts production. The problem isn't with the billion-dollar lithography equipment or the cutting-edge etching systems—it's a tiny test probe, no bigger than a human hair, that has worn out after millions of precise electrical contacts. This microscopic component, essential for verifying every chip that rolls off the production line, comes from an unlikely source: a company headquartered not in Silicon Valley or Tokyo, but in the industrial port city of Busan, South Korea.

Lee Chae-yoon founded Leeno Industrial in 1978, naming the company using a combination of his and his wife's surnames. What started as a precision manufacturing operation in Korea's second-largest city has quietly evolved into one of the semiconductor industry's most dominant players, controlling a market position that would make even the tech giants envious.

The numbers tell a story of near-monopolistic success that few outside the semiconductor supply chain have noticed. The global top three manufacturers of semiconductor test probes include LEENO, Smiths Interconnect, and Cohu, with a total market share of nearly 33%, of which the largest manufacturer is LEENO. But this understates the company's true dominance—Leeno is the dominant leader in the global market for test probes, also called test pins, used in identifying defects in semiconductor integrated circuits (ICs), with more than a 70% share.

Today, with a market capitalization of KRW 4.38 trillion and trailing 12-month revenue of $245M, Leeno Industrial represents one of the purest "picks and shovels" plays in the semiconductor industry. Every memory chip in your smartphone, every processor in your laptop, and increasingly, every AI accelerator powering ChatGPT has likely been tested by Leeno's probes. Yet mention the company's name to most investors, and you'll get blank stares.

This is the story of how a Korean engineer built an irreplaceable position in the global technology supply chain by focusing obsessively on one thing: making the best semiconductor test equipment in the world. It's a tale of patient capital, technical excellence, and the strategic wisdom of being indispensable rather than famous. In an era when everyone wants to design the next breakthrough chip, Lee Chae-yoon bet his life's work on ensuring those chips actually work.

II. Origins & The Lee Chae-yoon Story (10 minutes)

The year was 1978, and South Korea's industrial miracle was just beginning to gather steam. While Samsung was pivoting from trading company to electronics manufacturer and Hyundai was scaling up its shipbuilding operations, a young engineer named Lee Chae-yoon saw opportunity in precision. He graduated from Kwangsung Engineering High School in 1969 and later, in 1991, graduated from Dong-Eui University. Unlike many of his contemporaries who flocked to Seoul's emerging tech corridor, Lee chose Busan—a decision that would prove both contrarian and brilliant.

Busan in the late 1970s was Korea's gateway to the world, its massive port handling the raw materials and finished goods that would fuel the nation's export-led growth. But it wasn't known for high-tech manufacturing. Lee saw this differently. The city's industrial infrastructure, lower costs compared to Seoul, and proximity to Japan's advanced manufacturing sector created unique advantages for a precision parts business. The company was founded in 1978 and is headquartered in Busan, South Korea.

The choice of company name revealed both personal commitment and Korean business culture. He named the company using a combination of his and his wife's surnames—a gesture that intertwined family legacy with industrial ambition. This wasn't just another business venture; it was a family's future being wagered on precision engineering.

The early Leeno Industrial bore little resemblance to today's semiconductor testing powerhouse. The company started as a precision metal parts manufacturer, serving Korea's rapidly growing industrial base. Every component had to meet exacting standards—a philosophy that Lee enforced with almost religious fervor. Workers recall him spending hours on the factory floor, personally inspecting parts with magnifying glasses, rejecting batches that were off by mere micrometers.

This obsession with precision wasn't just about quality control; it was about building capabilities. Lee understood that Korea's competitive advantage couldn't come from cheap labor alone—that advantage would eventually erode. Instead, he focused on developing manufacturing expertise that would be difficult to replicate. The company invested heavily in measurement equipment, employee training, and process refinement, often at the expense of short-term profits.

By the early 1980s, Leeno had established a reputation among Korean manufacturers for delivering parts that others couldn't produce. But Lee wasn't satisfied with being a regional supplier. He began studying global technology trends, particularly the emerging semiconductor industry. What he discovered would transform Leeno's trajectory: as chips became more complex, testing them reliably would become exponentially more challenging. The industry would need precision at scales that made his current work look crude by comparison.

III. The First Inflection: Semiconductor Testing Pivot (1980s-1990s) (15 minutes)

The 1980s marked South Korea's audacious entry into the global semiconductor industry. Samsung announced its entry into memory chips in 1983, a move that many Western analysts mocked as overambitious. But Lee Chae-yoon saw what the skeptics missed: Korea's semiconductor ambitions would create an entire ecosystem of opportunities for suppliers who could meet the industry's demanding requirements.

The transition from precision metal parts to semiconductor testing equipment wasn't obvious or easy. Test probes for semiconductors required precision at the nanometer scale, materials that could withstand millions of contacts without degrading, and engineering expertise that few companies possessed. Lee's response was characteristic: he immersed himself in the technology, regularly meeting with professors and researchers to understand the physics and engineering challenges involved.

The LEENO PIN & IC TEST SOCKET segment provides probes and sockets used for electrical defects testing of semiconductor such as printed circuit boards (PCBs), integrated circuit (IC), memory and non-memory. The company's initial products were simple—basic probes for continuity testing. But even these required revolutionary improvements in manufacturing precision. A probe that was off by a few micrometers could damage delicate semiconductor wafers worth tens of thousands of dollars.

The breakthrough came through a combination of materials science and mechanical engineering innovation. Leeno developed proprietary alloys that maintained their shape and conductivity after millions of compression cycles. The company created micro-machining techniques that could produce probe tips with unprecedented consistency. Most importantly, they developed testing protocols for their testing equipment—a meta-level of quality control that ensured reliability.

Lee regularly conducts meetings with mechanical engineering professors in Busan, where Leeno's headquarters are located, and devises long-term corporate strategy based on engineering books rather than management books. This academic approach to industrial problems set Leeno apart from competitors who relied primarily on incremental improvements to existing designs.

By the early 1990s, Leeno's test probes were finding their way into Samsung and LG's semiconductor facilities. The initial orders were small—Korean companies still preferred established Japanese suppliers for critical equipment. But Leeno had an advantage: proximity. When problems arose, Leeno's engineers could be on-site within hours, not days. They could customize solutions for specific production lines, iterate quickly, and most importantly, they understood the unique pressures facing Korean semiconductor manufacturers.

"While our test pins are more expensive than the ones made in Japan, they are more cost-effective in that their lifespan is much longer," Lee would later explain. This value proposition—higher upfront cost but lower total cost of ownership—would become Leeno's calling card. In an industry where production line downtime could cost millions per hour, equipment reliability trumped initial price every time.

The 1990s also saw Leeno expand beyond basic probes into complete socket solutions. The Company's products consist of IC test sockets such as memory sockets, logic sockets, radio frequency (RF) sockets and hybrid sockets, and pin products such as fine pitch probes, green probes, kelvin probes, standard probes, switching probes, touch probes and battery charge probes under the brand name of LEENO. Each product category required different engineering approaches, materials, and manufacturing processes. The company was essentially running multiple specialized businesses under one roof, united only by their focus on semiconductor testing.

IV. Going Public: The KOSDAQ IPO (2001-2002) (10 minutes)

The new millennium brought a crucial decision for Leeno Industrial. After more than two decades of bootstrapped growth, the company needed capital to compete globally. The dot-com bubble had burst, Asian markets were still recovering from the 1997 financial crisis, and investor appetite for hardware companies was minimal. It was, by conventional wisdom, the worst possible time to go public.

Established in 1978 and entered Kosdaq market in 2001, Leeno's IPO represented a leap of faith in both directions. For Lee Chae-yoon, it meant opening his closely held company to public scrutiny and market pressures. For investors, it meant betting on a specialized supplier in an industry notorious for its cyclicality.

The early 2000s Korean technology market was a study in contradictions. While the country's semiconductor giants were gaining global market share, their suppliers remained largely unknown. The KOSDAQ, Korea's answer to NASDAQ, was populated with software companies and internet ventures trying to ride the digital wave. A company making test probes seemed almost quaint by comparison.

But Leeno's pitch to investors was compelling in its simplicity: every semiconductor needed testing, and as chips became more complex, testing would become more critical and more valuable. The company's financials backed up this thesis. Despite the global tech downturn, Leeno's revenues had grown steadily, driven by the relentless increase in semiconductor production and complexity.

The IPO roadshow revealed the challenge of explaining Leeno's business model. Institutional investors struggled to understand why tiny probes could command such high margins. The answer lay in the switching costs and risk profile of semiconductor manufacturing. Once Leeno's probes were designed into a testing system, changing suppliers meant re-qualifying entire production lines—a process that could take months and risk yield rates. For semiconductor manufacturers operating on razor-thin margins, the risk far outweighed any potential cost savings.

The public listing also forced Leeno to professionalize its operations. Financial reporting systems were upgraded, governance structures were implemented, and for the first time, the company had to articulate its strategy to outsiders. This transparency, initially seen as a burden, became a competitive advantage. Customers gained confidence from Leeno's public financials, competitors couldn't hide behind private company opacity, and employees could see the direct impact of their work on the company's valuation.

The early years as a public company were challenging. The stock price languished as investors favored flashier technology plays. But Lee Chae-yoon remained focused on the fundamentals: improving product quality, expanding the product portfolio, and deepening relationships with key customers. He understood that in the semiconductor industry, credibility was earned over decades, not quarters.

By 2005, this patience began paying dividends. As global semiconductor production ramped up and new memory technologies emerged, Leeno's specialized expertise became increasingly valuable. The company that had struggled to explain its value proposition to investors was now fielding calls from analysts trying to understand the semiconductor testing bottleneck.

V. The Great Expansion: Riding the Global Chip Wave (2010-2015) (15 minutes)

The 2010s opened with the mobile revolution in full swing. Every smartphone contained dozens of chips, each requiring multiple rounds of testing during production. The explosion in semiconductor demand created unprecedented opportunities for test equipment suppliers, but also new challenges. Production volumes were scaling exponentially, chip architectures were becoming more complex, and quality requirements were tightening as semiconductors moved into safety-critical applications.

In 2012, LEENO Industrial's revenue was 75.22 billion won, an increase of 13.89% compared to the previous year's 66.05 billion. Earnings were 24.86 billion, an increase of 29.05%. These numbers reflected more than just market growth—they demonstrated Leeno's ability to capture value in a rapidly expanding industry. The company's profitability was actually growing faster than revenues, a sign that their products were becoming more essential and commanding better pricing.

The strategic focus during this period was on product diversification within the testing ecosystem. Memory chips required different testing approaches than processors. Radio frequency components for wireless communication needed specialized sockets that could handle high-frequency signals without interference. Power management chips demanded probes that could handle higher currents without degrading. Each category represented a distinct engineering challenge and market opportunity.

Leeno's approach to these challenges revealed the depth of their technical capabilities. Rather than simply scaling existing designs, the company developed platform technologies that could be customized for specific applications. This modular approach allowed them to serve diverse markets efficiently while maintaining the specialization that customers valued. A memory test socket might share certain mechanical components with a logic test socket, but the contact materials, spring forces, and electrical characteristics would be optimized for each application.

The achievement of more than a 70% global market share in test probes during this period wasn't accidental. It resulted from a deliberate strategy of making switching costs prohibitively high for customers. Leeno's engineers embedded themselves in customers' development processes, helping design test protocols for new chip architectures before they reached production. By the time a new semiconductor was ready for mass production, Leeno's test solutions were already optimized and qualified.

This period also saw Leeno expand beyond its Korean base. The company established technical support centers in Taiwan, China, and Southeast Asia—following their customers' manufacturing footprints. But unlike many suppliers who moved production to lower-cost countries, Leeno kept its most critical manufacturing in Busan. The company had learned that in precision manufacturing, the accumulated expertise of experienced workers was more valuable than labor cost savings.

The competitive landscape during these years highlighted Leeno's unique position. Japanese competitors like Yamaichi Electronics and Enplas had strong technology but struggled with the cost structure and speed of Korean operations. American companies focused on high-end automatic test equipment but often overlooked the "consumable" probe market. Chinese competitors were beginning to emerge but lacked the track record and technology depth to serve leading-edge semiconductor manufacturers. Leeno occupied a sweet spot: advanced enough for cutting-edge applications, efficient enough to compete on cost, and reliable enough to be trusted with critical production lines.

VI. The Technology Leadership Era (2015-2020) (15 minutes)

By 2015, the semiconductor industry was undergoing fundamental transitions. Moore's Law was slowing, pushing the industry toward new architectures and packaging technologies. The Internet of Things promised billions of new connected devices. Artificial intelligence was moving from research labs to data centers. Each trend created new testing challenges that required not just incremental improvements, but fundamental innovations in test equipment.

The company's CEO is known in the industry for his near-ceaseless efforts to maintain its competitive advantage in technology. This wasn't just corporate rhetoric—it was visible in Leeno's R&D investments and patent filings. While many hardware companies were cutting research budgets to boost margins, Leeno was doubling down on technology development.

The expansion into WLCSP (Wafer Level Chip Scale Package) probe cards represented a major technological leap. Unlike traditional probes that tested individual chips, probe cards could test entire wafers with hundreds of chips simultaneously. The engineering challenges were formidable: maintaining consistent contact force across thousands of probe points, managing thermal expansion differences between materials, and ensuring signal integrity at increasingly high frequencies.

Leeno's solution came through a combination of materials science breakthroughs and precision manufacturing capabilities developed over decades. The company developed proprietary micro-spring technologies that could maintain consistent contact force even as materials expanded and contracted. They created new alloy compositions that balanced conductivity, durability, and manufacturability. Most importantly, they developed simulation and modeling capabilities that allowed them to predict and prevent failure modes before products reached customers.

The move into medical devices might seem like a deviation from semiconductors, but it actually leveraged core competencies in interesting ways. The Medical Device segment provides components used for ultrasonic probes. Medical ultrasound probes required similar precision manufacturing capabilities, materials expertise, and quality control systems as semiconductor test equipment. The diversification provided some insulation from semiconductor cycles while opening new growth avenues.

Camera module testing emerged as another growth driver during this period. As smartphones began incorporating multiple cameras with increasingly sophisticated sensors, testing requirements exploded in complexity. Each camera module contained not just the image sensor, but also autofocus mechanisms, optical image stabilization systems, and complex lens assemblies. Testing these integrated systems required equipment that could evaluate both electrical and optical performance simultaneously.

Leeno's response showcased their evolution from component supplier to system solution provider. The company developed integrated test sockets that could evaluate all aspects of camera module performance in a single insertion. This reduced testing time, improved yield rates, and simplified production line design for customers. The value proposition had evolved from "reliable components" to "production optimization."

The period also saw significant investments in automation and Industry 4.0 technologies. Leeno's factories in Busan began implementing advanced manufacturing execution systems, real-time quality monitoring, and predictive maintenance algorithms. The goal wasn't just efficiency—it was about capturing and analyzing data from millions of test cycles to continuously improve product design and predict failure modes before they occurred in customer facilities.

VII. The COVID Boom & Stock Market Recognition (2020-2021) (15 minutes)

The COVID-19 pandemic initially threatened to derail the semiconductor industry. Factory shutdowns, supply chain disruptions, and economic uncertainty suggested a severe downturn was imminent. But as the world shifted to remote work and digital interaction, semiconductor demand exploded beyond anyone's predictions. Every laptop for remote work, every tablet for remote learning, and every server for video conferencing needed chips—and every chip needed testing.

Leeno's operating profit last year was 77.9 billion won ($68.9 million), up by 21% from 2019 at 64.1 billion won ($56.7 million). While these numbers were impressive, they actually understated the company's momentum. Order backlogs were growing faster than production capacity, and customers were signing long-term supply agreements at premium prices to secure probe availability.

The stock market's recognition of Leeno's value was sudden and dramatic. After the trading session on July 5, Leeno has become the 13th-largest company on Kosdaq, with a market cap of 2.85 trillion won ($2.52 billion). Leeno's year-to-date stock price growth is 38%. For a company that had labored in obscurity for decades, the spotlight was both validating and challenging.

Analysts project that Leeno's operating profit in 2021 will surpass 100 billion won ($88.5 million). The optimism wasn't just about current demand—it was about structural changes in the semiconductor industry that favored Leeno's position. The chip shortage had taught the industry painful lessons about the cost of inadequate testing. Yield rates that had been acceptable when chips were plentiful became catastrophic when every functioning chip was precious.

South Korea's securities industry has recently raised Leeno's target price even further. Kiwoom Securities Co. in a recent report has raised the company's target price from 190,000 won ($168.06) to 220,000 won ($194.59) a share, projecting that this year's operating profit will grow by 45% to 106.3 billion won ($94.1 million).

The metaverse emerged as an unexpected catalyst for growth. Leeno will also benefit from the fast expansion of metaverse-related sectors that use the company's test pins. "Leeno's test pin segment will maintain strong performance with the fast growth of virtual reality (VR) devices such as Oculus Quest 2," added Pak. Virtual reality headsets required sophisticated sensors, high-resolution displays, and powerful processors—all needing extensive testing. The metaverse hype might have been overblown, but the hardware requirements were real and growing.

Beyond consumer devices, the pandemic accelerated digital transformation across industries. Automotive companies rushed to add semiconductor content for advanced driver assistance systems. Industrial companies deployed IoT sensors for remote monitoring. Healthcare providers adopted connected medical devices. Each application created incremental demand for semiconductor testing, and by extension, for Leeno's products.

The financial metrics during this period told a story of a company hitting its stride. Margins expanded as premium products grew as a percentage of sales. Return on invested capital soared as previous capacity investments paid off. Free cash flow generation accelerated, giving Leeno flexibility to invest in next-generation technologies while returning cash to shareholders. The company that had once struggled to explain its value to investors was now being studied by competitors trying to replicate its success.

But Lee Chae-yoon, now in his 70s but still actively leading the company, remained cautious about the euphoria. In earnings calls, he emphasized the cyclical nature of the semiconductor industry and the importance of preparing for eventual downturns. This conservatism, which might have frustrated growth-focused investors, reflected hard-won wisdom from decades in the industry.

VIII. Current Positioning & The AI/HBM Era (2022-Present) (15 minutes)

The artificial intelligence revolution has fundamentally altered semiconductor economics. Training large language models like GPT-4 requires thousands of high-performance GPUs running continuously for months. Each GPU contains multiple chips that must be tested not just for functionality, but for performance consistency across thousands of parallel units. The testing requirements have moved from "does it work?" to "does it work perfectly in concert with thousands of identical units?"

Leeno's most recent deal was a Corporate Asset Purchase with Korea Water Resources (Industrial Block 33 in Busan, South Korea). The deal was made on 22-Dec-2022. This expansion in Busan represented more than just capacity addition—it was a strategic bet on the longevity of the AI-driven semiconductor boom. The location in Busan, rather than following customers to Southeast Asia or China, reflected confidence that high-end testing would require the accumulated expertise concentrated at their headquarters.

The emergence of High Bandwidth Memory (HBM) has created particularly attractive opportunities for Leeno. HBM stacks multiple memory dies vertically, connected through thousands of through-silicon vias (TSVs). Testing these complex 3D structures requires equipment that can verify connections between layers, ensure thermal management across the stack, and validate high-speed signal integrity. The engineering challenges are orders of magnitude more complex than traditional memory testing.

Trailing 12-month revenue of $245M reflects the current run rate, but the forward-looking indicators suggest acceleration. Advanced packaging technologies like chiplets and heterogeneous integration require more testing, not less. As semiconductor companies decompose monolithic chips into multiple smaller dies, each die needs testing individually, and the assembled package needs system-level validation. The testing content per dollar of silicon is actually increasing.

The stock price has increased by +54.17% in the last 52 weeks. This performance, while impressive, comes with important context. A058470 underperformed the KR Semiconductor industry which returned 119.5% over the past year. The underperformance relative to semiconductor peers might seem concerning, but it actually reflects Leeno's position in the value chain. While chip designers and manufacturers saw explosive multiple expansion during the AI boom, equipment suppliers typically lag in market recognition.

A058470 exceeded the KR Market which returned 49% over the past year. This outperformance versus the broader market demonstrates that investors are beginning to recognize the structural advantages of Leeno's position. The company isn't just riding the semiconductor cycle—it's benefiting from secular trends that should persist regardless of short-term demand fluctuations.

Current financial positioning reveals a company preparing for opportunity. The company has 68.34 billion in cash and n/a in debt, giving a net cash position of 68.34 billion or 904.69 per share. This fortress balance sheet provides multiple strategic options: acquiring complementary technologies, investing in next-generation R&D, or returning capital to shareholders. In an industry where technological disruption is constant, financial flexibility is a crucial competitive advantage.

The technological roadmap ahead is both challenging and exciting. As semiconductors approach physical limits of silicon scaling, the industry is turning to new materials like gallium arsenide and silicon carbide. Each material requires different testing approaches, contact materials, and reliability standards. Quantum computing, still in its infancy, may eventually require entirely new testing paradigms. Photonic chips that use light instead of electrons will need optical and electrical testing integration.

IX. Playbook: Building a Testing Monopoly (20 minutes)

The strategic lessons from Leeno's rise offer a masterclass in building sustainable competitive advantages in industrial markets. The company's playbook contradicts much of contemporary business wisdom about disruption, platform effects, and winner-take-all dynamics. Instead, it demonstrates the enduring power of deep technical expertise, customer intimacy, and patient capital allocation.

The "picks and shovels" positioning in semiconductors represents strategic genius. During the California Gold Rush, the most reliable fortunes were made not by miners but by those selling them equipment. Similarly, Leeno prospers regardless of which semiconductor companies win or lose market share battles. Every chip needs testing, whether it's designed by Intel, TSMC, Samsung, or emerging Chinese competitors. This agnosticism to end-market winners provides remarkable stability in an inherently volatile industry.

The barriers to entry in testing equipment are more subtle but no less formidable than in chip manufacturing. While building a semiconductor fab requires billions in capital, entering the test probe market requires something potentially more difficult to acquire: decades of accumulated knowledge. The metallurgy of probe materials, the mechanics of maintaining consistent contact force across millions of cycles, the electrical characteristics required for high-frequency testing—each represents years of R&D and learning from failure.

Customer stickiness in Leeno's business model approaches the theoretical maximum. Once test probes are qualified for a production line, changing suppliers requires re-qualification that can take 6-12 months. During that time, production yields might suffer, costing millions in lost revenue. For semiconductor manufacturers operating on tight margins and delivery schedules, the risk of switching suppliers far outweighs any potential cost savings. This dynamic allows Leeno to maintain pricing power even during industry downturns.

The R&D strategy demonstrates how focused innovation can outperform broad research programs. While tech giants spread R&D across multiple moonshot projects, Leeno invests relentlessly in incremental improvements to testing technology. A probe that lasts 10% longer before replacement, a socket that reduces test time by milliseconds, a material that maintains conductivity at higher temperatures—these seemingly minor advances compound into insurmountable competitive advantages.

The capital allocation framework reflects profound understanding of industrial economics. 68.34 billion won in cash with no debt might seem overly conservative to financial engineers, but it serves multiple strategic purposes. It signals financial strength to customers who need assurance of supply continuity. It provides flexibility to invest counter-cyclically during downturns. Most importantly, it removes financial pressure that might force short-term decision-making in an industry that rewards long-term thinking.

Geographic strategy reveals sophisticated understanding of comparative advantage. By keeping critical manufacturing in Busan despite higher costs, Leeno maintains quality control and protects intellectual property. The proximity to Samsung and SK Hynix provides rapid feedback loops and collaboration opportunities that distant competitors cannot match. Technical support centers in customer locations provide presence without diluting core capabilities.

The organizational culture, shaped by Lee Chae-yoon's engineering background, prioritizes technical excellence over financial metrics. Engineers are celebrities within the company, their innovations celebrated more than quarterly earnings beats. This cultural emphasis attracts technical talent who might otherwise gravitate toward flashier technology companies. In an industry where product quality directly translates to customer value, this engineering-first culture becomes a competitive moat.

Pricing strategy demonstrates masterful value capture. "While our test pins are more expensive than the ones made in Japan, they are more cost-effective in that their lifespan is much longer." By focusing on total cost of ownership rather than unit price, Leeno shifted customer focus from procurement cost to production value. This approach requires sophisticated customers who understand lifecycle economics, but semiconductor manufacturers are precisely such customers.

The innovation pipeline management balances current optimization with future preparation. While continuously improving existing products for immediate customer needs, Leeno simultaneously invests in technologies that won't generate revenue for years. This dual-track approach ensures both current competitiveness and future relevance, a balance many technology companies struggle to maintain.

X. Bear Case vs. Bull Case (15 minutes)

Bear Case: The Shadows Lengthening

The semiconductor industry's notorious cyclicality poses the most immediate threat to Leeno's trajectory. History shows that semiconductor downturns can be swift, severe, and longer than expected. When chip demand drops, manufacturers first cut capital equipment purchases, then reduce production volumes, directly impacting test equipment utilization. Leeno's high margins and returns on capital, while impressive during upturns, could compress rapidly when customers delay probe replacements and postpone capacity expansion.

Chinese competition represents a strategic threat that's different from previous challenges. Unlike Japanese competitors who focused on quality or American companies emphasizing technology, Chinese entrants combine government support, massive domestic market access, and willingness to accept lower returns. As China pushes for semiconductor self-sufficiency, domestic test equipment suppliers receive preferential treatment, subsidies, and guaranteed orders from Chinese chipmakers. While Leeno's technology lead provides protection today, the gap will narrow as Chinese companies hire talent and license technology.

Customer concentration within Korean semiconductor manufacturers creates vulnerability. While Leeno serves global customers, Samsung and SK Hynix likely represent outsized revenue contribution. If Korean semiconductor companies lose market share to TSMC, Intel, or emerging Chinese competitors, Leeno's geographic advantage becomes a liability. The company's deep integration with Korean customers, while providing competitive advantages, also creates dependence that could limit strategic flexibility.

The underperformance versus semiconductor peers deserves scrutiny. A058470 underperformed the KR Semiconductor industry which returned 119.5% over the past year. This gap might reflect market wisdom about equipment suppliers' position in the value chain. While chip designers capture value through intellectual property and manufacturers through scale, equipment suppliers might face margin compression as customers demand cost reductions and competitors emerge.

Technological disruption, while seeming distant, could arrive suddenly. If breakthrough technologies like quantum computing or neuromorphic chips gain traction, traditional electronic testing paradigms might become obsolete. Leeno's expertise in electrical contact testing might have limited relevance in a world of photonic chips or quantum states. The company's conservative R&D approach, while successful historically, might leave it flat-footed against paradigm shifts.

Bull Case: The Compounding Advantage

The artificial intelligence revolution is creating unprecedented demand for sophisticated semiconductor testing that plays directly to Leeno's strengths. HBM testing requirements are exponentially more complex than traditional memory, requiring equipment that can verify thousands of connections in three-dimensional structures. As AI models grow larger and require more specialized silicon, testing becomes more critical, not less. The complexity barrier favors incumbents with decades of experience over new entrants trying to ride the AI wave.

The Semiconductor Test Equipment Market is expected to reach USD 15.11 billion in 2025 and grow at a CAGR of 6.20% to reach USD 20.42 billion by 2030. This market expansion provides a rising tide that should lift all participants, but market leaders typically capture disproportionate value. Leeno's dominant position means it should grow faster than the market as customers consolidate suppliers and prioritize reliability over cost savings.

The irreplaceable position in the semiconductor supply chain becomes more valuable as chips become more critical to economic competitiveness. Governments worldwide are recognizing semiconductors as strategic assets, pouring billions into domestic production capabilities. Every new fab, regardless of location or ownership, needs test equipment. Leeno benefits from semiconductor nationalism without the political complications facing chip manufacturers.

Expansion opportunities in automotive and medical devices provide portfolio diversification without abandoning core competencies. Electric vehicles require 5-10 times more semiconductor content than traditional cars, all requiring extensive testing for safety-critical applications. Medical devices, particularly diagnostic equipment and wearables, represent a growing market with quality requirements that align perfectly with Leeno's capabilities.

The financial fortress provides optionality that markets undervalue. With 68.34 billion won in cash and n/a in debt, Leeno could acquire complementary technologies, return substantial capital to shareholders, or invest counter-cyclically during downturns. This flexibility becomes particularly valuable in uncertain macroeconomic environments where access to capital might become constrained.

Return metrics suggest a business generating substantial economic value. Return on equity (ROE) is 21.35% and return on invested capital (ROIC) is 15.00%. These returns, sustained over cycles, indicate competitive advantages that translate into shareholder value. The consistency of returns matters more than absolute levels, suggesting a business model resilient to competitive pressure.

XI. Power & Lessons (10 minutes)

The power of being the best at one thing resonates throughout Leeno's story. In an era celebrating diversification and platform strategies, Leeno demonstrates that extraordinary returns can come from extraordinary focus. The company doesn't make semiconductors, design chips, or build consumer products. It makes the probes that test semiconductors—and it makes them better than anyone else in the world.

This focus creates compound advantages that broader competitors cannot match. Every engineering hour spent improving probe reliability, every customer interaction about testing challenges, every failure analysis contributes to an accumulating knowledge base. While conglomerates spread resources across multiple businesses, Leeno concentrates all organizational energy on a single mission. The result is expertise so deep that customers cannot find alternatives even if they wanted to.

The lesson about boring B2B businesses creating massive value challenges conventional wisdom about where returns originate. Consumer-facing technology companies capture headlines and imaginations, but industrial suppliers often generate superior returns with less risk. Leeno's customers are sophisticated corporations with multi-year planning horizons, not fickle consumers chasing the latest trends. The sales cycles are longer but the relationships are stickier. The growth is steadier but more predictable.

The Korean playbook of technical excellence combined with patient capital offers an alternative to Silicon Valley's growth-at-all-costs mentality. Korean industrial companies like Leeno, Samsung, and POSCO built global leadership through decades of incremental improvement rather than disruption. They invested through downturns, prioritized quality over speed, and measured success in decades rather than quarters. This approach requires cultural alignment between stakeholders that's difficult to replicate in markets demanding immediate returns.

For founders in highly technical markets, Leeno provides a template for building defensible businesses. Start with a critical but overlooked problem. Develop technical expertise that takes years to replicate. Embed yourself in customers' workflows until switching becomes unthinkable. Price for value rather than competing on cost. Invest consistently in R&D even when markets don't immediately reward it. Build financial strength that allows strategic patience. Most importantly, resist the temptation to diversify before dominating your core market.

The question of why some businesses deserve premium multiples finds a clear answer in Leeno's model. Premium valuations should attach to businesses with sustainable competitive advantages, predictable cash flows, and options for future growth. Leeno exhibits all three: technological barriers that protect market position, customers locked in through switching costs, and expansion opportunities in adjacent markets. The market's historical undervaluation of such businesses creates opportunities for patient investors who understand industrial economics.

The broader lesson about value creation in the technology supply chain deserves consideration. While semiconductor designers and software companies capture headlines, the enabling infrastructure often provides superior risk-adjusted returns. Companies providing essential tools, components, or services to technology leaders can achieve monopolistic positions without regulatory scrutiny. They benefit from industry growth without bearing technology risk. They generate cash flows through cycles rather than just at peaks.

XII. Grading & Final Thoughts (5 minutes)

Is this an A+ business? The evidence overwhelmingly suggests yes. Market dominance with more than a 70% share in critical components. Returns on capital consistently above 15% through cycles. A balance sheet with more cash than market cap percentages would suggest. Customer relationships so sticky that switching is almost unthinkable. Technology barriers that grow stronger with time rather than eroding. If these characteristics don't define business quality, what does?

Yet the market's historical skepticism contains wisdom worth considering. The stock underperformed semiconductor peers during one of history's great chip booms. Perhaps markets recognize risks that financial metrics don't capture: the vulnerability of extreme specialization, the challenges of leadership transition as founders age, the possibility that semiconductor testing becomes commoditized through automation or new technologies.

What could go wrong from here requires imagination but isn't impossible to envision. A breakthrough in self-testing chips that eliminates external probe requirements. Chinese competitors achieving technology parity through talent acquisition and IP transfer. A severe semiconductor downturn that forces customers to extend equipment life far beyond normal replacement cycles. Samsung or SK Hynix losing competitiveness to TSMC or Intel, reducing demand from Leeno's core customers. Any of these scenarios could impair the thesis, though none seem imminent.

The next ten years will test whether Leeno can maintain dominance as the semiconductor industry undergoes fundamental transitions. The shift to chiplet architectures and advanced packaging creates new testing requirements that could favor different approaches. Emerging technologies like quantum computing and photonics might require capabilities beyond Leeno's current expertise. Geographic diversification of semiconductor manufacturing could dilute Leeno's advantage of proximity to Korean customers.

But betting against focused excellence has historically been a losing proposition. Companies that achieve true mastery in critical niches tend to extend their dominance rather than lose it. They accumulate advantages that compound over time: customer relationships that deepen, expertise that accumulates, reputations that strengthen. New competitors face not just current capabilities but decades of learning curves. Customers face not just switching costs but switching risks in industries where failure is catastrophic.

The final reflection crystallizes into a profound insight about business and investing: sometimes the best businesses are hiding in plain sight, obscured by complexity, terminology, or simple lack of attention. Every investor analyzing semiconductor stocks has encountered Leeno's products, whether they know it or not. Every chip in every device has been touched by test probes, yet few investors bother to understand the companies making them. This invisibility, paradoxically, might be Leeno's greatest advantage—allowing it to compound value while competitors chase more visible but less valuable opportunities.

Leeno Industrial represents something increasingly rare in modern capitalism: a company that wins by being genuinely better at something that genuinely matters. No financial engineering, no regulatory capture, no network effects—just decades of accumulated expertise applied to solving critical problems for demanding customers. In a world of shortcuts and disruption, there's something admirable, even inspiring, about a company that built a monopoly one perfect probe at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube