Shinhan Financial Group: Overtaking Giants & Navigating the "Korea Discount"

I. Introduction & The "Value-Up" Revolution

Picture a trading floor in Seoul in the autumn of 2023. South Korea has just produced Samsung, the world's most valuable memory-chip maker. It has given the planet K-pop, K-dramas, and shipyards that build a third of the world's largest vessels. And yet, on the screens of the foreign fund managers watching the 한국거래소 Korea Exchange (KRX), one number refuses to behave. The country's largest, most profitable, most systemically important banks—institutions sitting on hundreds of trillions of won in assets—trade at price-to-book ratios of 0.3x to 0.4x.[^1]

Let's sit with what that means, because it is genuinely strange. A price-to-book ratio of 0.4x says the stock market believes a bank is worth less than half the accounting value of its own equity. In plain terms: if you could liquidate the bank tomorrow, collect the loans, sell the buildings, and hand the cash back to shareholders, you would theoretically make more than two and a half times your money. The market was effectively pricing these banks as if a large chunk of their reported capital would simply evaporate. This persistent, structural undervaluation of Korean equities relative to global peers has a name that has haunted Seoul's policymakers for two decades: the 코리아 디스카운트 Korea Discount.[^1]

The causes were a tangled knot. Decades of chaebol cross-shareholdings that protected founding families at minority investors' expense. Stingy dividend payouts. The ever-present geopolitical shadow of North Korea. And a corporate culture that prized empire-building and asset scale over the boring discipline of returning cash to the people who actually owned the company. By early 2024, the government had seen enough. Drawing direct inspiration from Japan's Tokyo Stock Exchange reforms, Korean regulators launched the 기업 밸류업 프로그램 Corporate Value-up Program—a national campaign to shame, cajole, and incentivize listed companies into caring about their share price.[^2]4

Every revolution needs a poster child. The company that stepped most aggressively into that role was 신한금융지주회사 Shinhan Financial Group Co., Ltd., trading in Seoul under the ticker 055550.KS.2 Under a new generation of professional leadership, Shinhan made a decision that, by the standards of Korean banking history, amounted to heresy. It declared that the decades-long race to be the biggest bank was over. The new race was to be the most efficient bank—the one that generated the highest return on every won of capital and handed the most of it back to shareholders. Shinhan committed to "uncapped" shareholder returns tied directly to profitability, a phrase that would have been unthinkable from a Korean financial holding company a decade earlier.1

This is a story about how an institution born from outsiders—Korean-Japanese immigrants with no chaebol backing and no government sponsorship—clawed its way into one of the most protected oligopolies on earth, and then, forty years later, tried to lead that same oligopoly out of the valuation cellar.

So here is our roadmap. First, we'll go back to 1982 and meet the 재일교포 Zainichi Koreans who founded a bank on the radical premise that customers should be treated well. Then we'll walk through the high-stakes M&A playbook—조흥은행 Chohung Bank, LG카드 LG Card, and 오렌지라이프 Orange Life Insurance—and ask the question every Acquired listener wants answered: did they overpay to build their empire? We'll go inside the brutal "Big Four" oligopoly that forms the core engine, examine the hidden jewel of Shinhan's overseas franchises in Vietnam and Japan that throw off an outsized share of profits, and finally meet the man steering the modern transformation, 진옥동 Jin Ok-dong. We'll close with the strategic frameworks and the bull-bear debate that any long-term owner of this stock has to wrestle with.

Let's begin where every good origin story does: with the underdogs nobody bet on.

II. The Zainichi Genesis & The Customer-First DNA

To understand why Shinhan exists, you have to understand a peculiar diaspora. After Japan's colonization of Korea ended in 1945, hundreds of thousands of ethnic Koreans remained in Japan. They became known as the 재일교포 Zainichi Koreans—a community caught between two countries, holding neither full acceptance in Japan nor an easy path home. Excluded from much of corporate Japan, many turned to entrepreneurship. They built businesses in pachinko, real estate, restaurants, and small-scale finance, accumulating capital while remaining, in a deep emotional sense, Korean.

By the late 1970s, a group of these Zainichi businessmen had something most homeland Koreans of the era did not: pools of private capital and a burning desire to contribute to their ancestral country's economic miracle. In 1982, they pooled that capital and founded 신한은행 Shinhan Bank.[^4] The name "Shinhan" itself carried meaning—roughly, "new Korea." This was a bank built not by the state, not by a chaebol, but by outsiders who wanted in.

That founding circumstance mattered enormously, and here's why. In 1982, South Korean banking was a sleepy, state-directed affair. The major commercial lenders were extensions of government industrial policy—their job was to funnel cheap credit to the chaebol conglomerates the state had chosen to build up. Customer service was an alien concept. You went to a bank, you waited, you were processed, and you left grateful. Bankers were bureaucrats. The customer was an inconvenience.

Shinhan had no choice but to be different. It had no government mandate forcing deposits its way. It had no captive chaebol parent guaranteeing a loan book. It couldn't out-muscle the incumbents on scale or political connections. The only lever available to a scrappy newcomer was the one everyone else ignored: the customer. So Shinhan did things that sound trivial today but were genuinely radical in 1980s Seoul. Tellers greeted customers warmly and stood to receive them. Branches stayed open longer. Staff were trained—drilled, really—in courtesy and responsiveness. The bank marketed itself aggressively as the place that actually wanted your business.

This became known internally as the "Shinhan Way," and it created a flywheel. Better service won retail deposits. Retail deposits—the sticky, low-cost savings of ordinary households—gave Shinhan a cheaper and more stable funding base than rivals dependent on volatile corporate money. Cheaper funding meant healthier margins. Healthier margins funded more branches and more service. A bank that started with nothing but immigrant capital and good manners was, quietly, compounding.

Two enduring competitive advantages were seeded in this period, and both still define the company in 2026. The first is a near-obsessive focus on the retail customer experience—a cultural DNA that would later make Shinhan formidable in digital banking, where the entire game is convenience and user trust. The second is more unusual and arguably more valuable: a deep, structural relationship with Japan. The Zainichi founders never severed their Japanese roots. Those relationships—the shareholders, the business networks, the cultural fluency on both sides of the strait—would eventually let Shinhan do something no other Korean bank could replicate: build a genuinely profitable banking franchise inside Japan itself, SBJ은행 SBJ Bank. We'll return to that cornered resource later, because it's one of the most underappreciated parts of the entire investment case.

But an immigrant retail bank, however well-mannered, was still a minnow. To become a giant, Shinhan would have to do something far more dangerous than smile at customers. It would have to swallow institutions far older and larger than itself—and risk choking on them.

III. The M&A Blitz: Building a Conglomerate

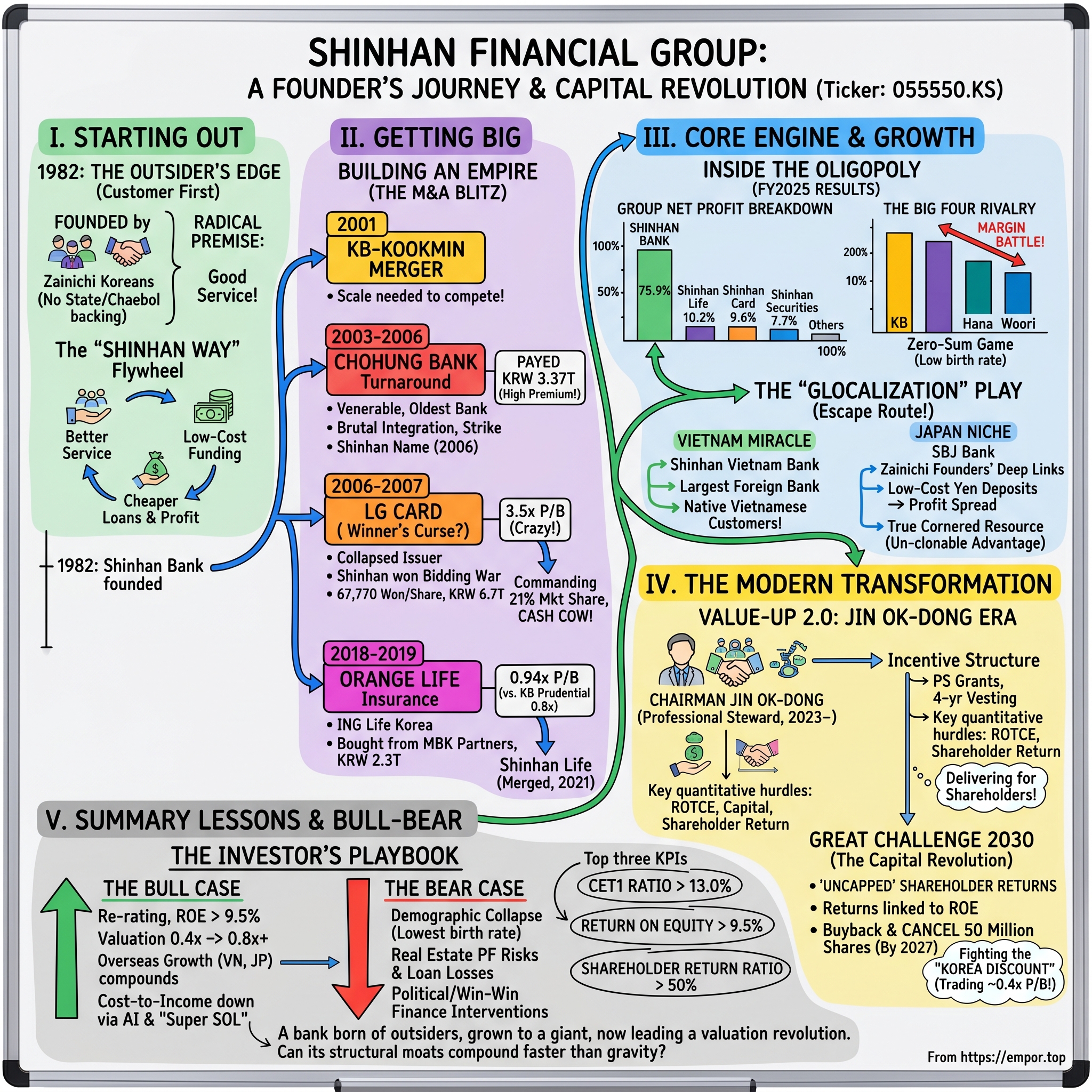

In 2001, two of Korea's biggest banks merged to form KB금융그룹 KB Financial Group's banking heart, KB Kookmin—an instant retail behemoth. For Shinhan, which had spent two decades clawing up from outsider status, the message was blunt: get big or get eaten. Scale in banking is not vanity. It determines your funding costs, your ability to absorb technology spending, and your relevance to the largest corporate clients. Shinhan's leadership concluded that organic growth would never close the gap fast enough. They would have to buy their way into the top tier. What followed was one of the boldest M&A campaigns in Korean financial history—three landmark deals across fifteen years, each carrying a premium that made analysts wince.

The Chohung Turnaround (2003–2006)

The first target was, on paper, almost absurd. 조흥은행 Chohung Bank was the oldest financial institution in Korea, tracing its lineage back to 1897—a venerable, proud, and deeply unionized institution. It was also bigger than Shinhan in important respects. The acquirer was younger and smaller than its prey. Shinhan agreed to pay roughly KRW 3.37 trillion to take control, a deal that would roughly double its asset base in a single stroke.[^4]

The integration was brutal. Chohung's powerful labor union saw the upstart Shinhan as a threat to a century of identity and went on strike. Customers got jittery. The cultural collision between Chohung's old-guard banking establishment and Shinhan's service-obsessed challenger culture could have torn the combined entity apart. Many mergers of this kind—two large banks, one hostile workforce—end in years of dysfunction and lost market share.

Shinhan's management handled it with patience rather than brute force, phasing the integration over years rather than forcing an overnight cultural conquest. By the time the combined bank operated fully under the Shinhan name in 2006, the gamble had paid off. The merger had vaulted Shinhan into the front rank of Korean commercial banking, giving it the branch density and balance-sheet heft to credibly compete with KB. The lesson Shinhan internalized here would echo through its later deals: it was willing to pay up and absorb short-term pain for a structural, permanent change in its competitive position.

The Winner's Curse of LG Card (2006–2007)

If Chohung was about scale, the next deal was about something more seductive: a cash machine. To understand it, you have to rewind to the Korean credit card crisis of the early 2000s. The government, eager to boost consumption, had encouraged a wild expansion of credit cards. Issuers handed out plastic to anyone with a pulse. Then the bubble burst. Defaults exploded, and the country's largest monoline issuer, LG카드 LG Card, collapsed into creditor receivership—a ward of its lenders, hemorrhaging value.

Out of that wreckage came one of the most aggressive bidding wars Korean finance had seen. Shinhan and Hana Bank both wanted LG Card, and both understood why: a credit card business, when healthy, is a phenomenal generator of fee income and high-yield consumer lending, the kind of non-interest revenue that diversifies a bank away from the grind of mortgage margins. The auction turned into a knife fight. Shinhan won—narrowly—by bidding 67,770 won per share, a total of roughly KRW 6.7 trillion (about $7.2 billion) for a 78.6% stake.[^4]

And then the criticism started. The deal closed at an astonishing 3.5x price-to-book ratio.[^4] Let that land for a moment: Shinhan paid three and a half times the accounting net worth for a company that had, just a few years earlier, been a smoking crater. Rating agencies were unimpressed. They downgraded Shinhan and warned that the acquisition premium would strain the holding company's capital adequacy for years. By the cold arithmetic of the moment, Shinhan had committed the classic sin of M&A: the winner's curse, where the "winner" of an auction is simply the bidder who most overestimated the prize.

But here is where the story gets interesting, and where short-term benchmarking and long-term strategy part ways. The acquisition was folded into what became 신한카드 Shinhan Card. And Shinhan Card did not turn out to be a one-time overpayment—it turned out to be an annuity. Commanding a market share of roughly 21%, it became the dominant card issuer in Korea and an absolute cash cow.[^5] Year after year, it threw off the kind of stable, high-margin fee income that cushioned the entire group through interest-rate cycles that battered pure lenders. The 3.5x P/B headline aged into a footnote; the cash flows compounded for the better part of two decades.

The pattern is worth naming, because Shinhan would repeat it: pay a premium that looks indefensible on a spreadsheet today, in exchange for a structural, durable earnings stream tomorrow. Whether that's disciplined long-term thinking or a habit of overpaying is exactly the debate that surrounds the third deal.

The Life Insurance Play (2018–2019)

By 2018, the strategic gap in Shinhan's portfolio wasn't scale or cards—it was insurance. Life insurance offered something a bank balance sheet structurally lacked: long-duration, higher-yielding assets and a different earnings cycle that could smooth the group's overall profitability. The target was 오렌지라이프 Orange Life Insurance, the company formerly known as ING Life Korea, which the private equity firm MBK Partners had bought, polished, and was now ready to sell.

In September 2018, Shinhan agreed to buy MBK's 59.15% stake for roughly KRW 2.3 trillion (about $2.05 billion), with a plan to eventually take it to 100% and merge it into the group's existing insurance arm to create 신한라이프 Shinhan Life.6 The headline valuation came in at about 0.94x price-to-book.6

Now, was that a good price? The most useful benchmark arrived two years later. In 2020, arch-rival KB금융그룹 KB Financial Group acquired Prudential Life Korea—widely regarded as one of the highest-quality life insurers in the country—at a cleaner 0.78x to 0.8x price-to-book.7 So once again, the Shinhan deal carried a relative premium: it paid more, for an asset most analysts considered no better than the one KB landed cheaper. The skeptics had a familiar feeling.

But the strategic logic held. The Orange Life acquisition meaningfully diversified the group's earnings away from pure banking, gave it access to higher-yielding insurance assets, and deepened the "One Shinhan" cross-selling machine—the idea that a single customer could be served banking, cards, insurance, and investments under one roof. The premium bought diversification and optionality, not just an insurance license.

Three deals, three premiums, one consistent philosophy: Shinhan would rather overpay for a structural position than underpay for a marginal one. That philosophy built a conglomerate. The question is whether the conglomerate it built can actually win the war it now fights every single day—inside the most concentrated banking oligopoly in the developed world.

IV. Inside the Oligopoly: The Core Business Engine

Imagine four heavyweight boxers locked in a ring that never opens its ropes. No new fighters can climb in—the regulatory barriers are too high. The crowd (Korea's depositors and borrowers) is finite and, increasingly, shrinking. So the four fighters do the only thing they can: they pound each other for market share, round after round, year after year. This is the Korean banking oligopoly, and it is the core engine of Shinhan's earnings.

The "Big Four" Battlefield

Let's introduce the contenders and their relative weight, using the freshly released fiscal 2025 results.[^5] The scale leader is KB금융그룹 KB Financial Group, which posted a net profit of KRW 5.84 trillion on total assets of roughly KRW 797.9 trillion. KB is the giant—the product of that early-2000s mega-merger, with the deepest balance sheet of the four.[^5]

Shinhan sits just behind it as the efficiency challenger, with FY2025 net profit of KRW 4.97 trillion on assets of around KRW 760 trillion.[^5] The framing matters: Shinhan is not trying to be the biggest. It is trying to extract the most profit and shareholder return per won of capital. That distinction is the entire modern strategy.

Then comes 하나금융그룹 Hana Financial Group, the nimble corporate-and-FX specialist, with net profit of KRW 4.00 trillion on assets near KRW 675 trillion. Hana punches above its weight in corporate banking and foreign exchange. And finally 우리금융그룹 Woori Financial Group, the commercial-banking pure-play still working to diversify beyond its lending core, with net profit of KRW 3.14 trillion on assets around KRW 565 trillion.[^5] Across all four, 2025 was a strong year—combined net profits for Korea's big financial groups rose about 9.4%.[^5]

What this snapshot reveals is a tight, top-heavy market. KB and Shinhan trade the top two spots back and forth; in fact, Shinhan Bank reclaimed the title of Korea's most profitable individual bank in the prior cycle, underscoring how close this race runs.[^6] There is no comfortable leader and no soft underbelly. Every basis point of margin is contested.

Where the Money Actually Comes From

Here's the part that surprises people who think of Shinhan as a sprawling financial supermarket. Strip away the holding-company complexity, and one subsidiary does the overwhelming majority of the work. In FY2025, the breakdown of group net profit looked like this.[^3]

신한은행 Shinhan Bank, the commercial bank, generated KRW 3.77 trillion—a staggering 75.9% of the entire group's net profit.[^3] Three out of every four won the group earns comes from plain old banking: taking deposits and making loans. Everything else is, in financial terms, the supporting cast.

That supporting cast is still meaningful, though. 신한라이프 Shinhan Life, the insurance arm built on the Orange Life acquisition, contributed KRW 507.7 billion, or about 10.2%—the high-yield insurance segment paying off the strategic premium.[^3] 신한카드 Shinhan Card, that decades-old cash cow, added KRW 476.7 billion, or 9.6%, in high-market-share fee income.[^3] 신한투자증권 Shinhan Securities, the capital-markets and brokerage arm, chipped in KRW 381.6 billion (7.7%)—and notably, that figure grew more than 113% year-on-year from 2024, a reminder of how leveraged the securities business is to buoyant equity markets.[^3] The remaining subsidiaries—capital, asset management, venture investment—together added roughly KRW 219.3 billion, about 4.4% combined.[^3] They're the connective tissue of the "One Shinhan" cross-sell, but they don't move the needle on their own.

The investor takeaway is blunt: as goes Shinhan Bank, so goes Shinhan Financial Group. The diversification is real and valuable for smoothing the ride, but this is fundamentally a bank.

The Economics of Korean Banking

So how does that bank actually make money? At its heart sits Net Interest Margin, or NIM—the spread between what the bank earns on its loans (chiefly mortgages and corporate credit) and what it pays for its funding (chiefly deposits). Think of it as the bank's gross profit margin. Multiply that spread across hundreds of trillions of won in loans, and you get the bulk of the bank's revenue. From that you subtract credit costs—the provisions set aside for loans that go bad. NIM up, credit costs down: that's a good year. The reverse is a bad one.

The structural problem is that Korea's domestic market is mature and, worse, demographically challenged. We'll dwell on this in the bear case, but the short version is that a country with the lowest birth rate in the world is not a growth market for mortgages and consumer loans over the long run. So domestic banking has become a zero-sum game. Shinhan cannot grow the pie much; it can only take a bigger slice from KB, Hana, and Woori. It fights for that slice through two weapons: digital convenience—a better app, a smoother loan application, fewer reasons to ever walk into a branch—and aggressive, localized pricing on mortgages and deposits.

A zero-sum domestic war is a grinding way to run a business. Which raises the obvious question: if the home market is a demographic dead end, where does the growth come from? The answer lies outside Korea entirely—in a quiet two-country franchise that competitors have spent years trying, and failing, to copy.

V. The "Glocalization" Play: Vietnam & Japan Powerhouses

In the Acquired tradition of finding the hidden engine inside a famous company, this is Shinhan's. While KB, Hana, and Woori remain largely trapped inside Korea's low-growth demographic profile, Shinhan has been quietly building something its rivals cannot easily replicate: a genuinely material overseas franchise. The numbers crossed a symbolic threshold in fiscal 2025. The group's global segment generated pre-tax profits exceeding KRW 1 trillion, with net global profit reaching KRW 824.3 billion—a remarkable 16.6% of total group net profit.[^3]

Read that again in context. Roughly one out of every six won of profit now comes from outside Korea. For a group whose domestic engine fights a zero-sum war on a shrinking field, that overseas slice isn't a rounding error or a vanity flag-planting exercise. It's the growth story. And it rests on two very different pillars.

The Vietnam Miracle

The first pillar is 신한베트남은행 Shinhan Vietnam Bank, and it's the kind of franchise foreign banks dream about and almost never achieve. Shinhan Vietnam is the largest foreign bank in the country by both assets and net profit—not one of the largest, the largest.[^11]

What makes it special is how Shinhan got there. Most foreign banks that enter an emerging market do so as a service window for their home-country multinationals. They follow Samsung and Hyundai into Vietnam, bank the Korean factories and expatriates, and call it a day. That's a small, capped business. Shinhan did something harder and far more valuable: it became a genuinely native Vietnamese commercial bank. It localized its credit scoring to assess Vietnamese consumers and small businesses on their own terms, and it built out retail and credit-card networks aimed at ordinary Vietnamese customers, not just Korean corporates.[^11]

Why does that distinction matter so much to an investor? Because Vietnam is everything Korea is not: young, fast-urbanizing, under-banked, and growing. A retail bank that has genuinely cracked native distribution in a market like that owns a high-yield, high-growth engine—the structural opposite of the saturated home market. It is, in effect, a way for Shinhan shareholders to own a slice of Vietnamese economic development without leaving the Korea Exchange.

The Japan Niche

The second pillar is the one we flagged at the very beginning: SBJ은행 SBJ Bank, Shinhan's Japanese subsidiary, and the direct descendant of the company's 재일교포 Zainichi founding. Those historical Korean-Japanese shareholder relationships didn't just seed the bank in 1982—they opened a door into Japan that no other Korean financial group has been able to walk through.[^4]5

SBJ runs profitable housing-loan and digital-deposit franchises inside Japan.5 And here's the structural beauty of it, which requires a quick word on Japanese monetary conditions. Japan spent decades in an ultra-low, often near-zero interest-rate environment. For a saver, that's miserable. But for a bank, it means access to an enormous pool of stable, almost cost-free deposit funding. SBJ taps that pool of cheap Japanese deposits and deploys it into lending, earning a healthy spread and an excellent return on equity for the parent group.5

Think of it as a funding arbitrage embedded in the group's DNA: gather money where it's cheapest and most stable (Japan), and earn returns the structure makes possible. KB, Hana, and Woori would love to have this. They can't simply buy it, because the asset isn't really the banking license—it's the half-century of Zainichi relationships and cultural fluency that underpin it. This is the closest thing in the whole Shinhan story to a genuinely un-clonable advantage, and we'll formalize exactly why when we reach the strategic frameworks.

Two overseas pillars—one a high-growth emerging-market retail engine, the other a low-cost, stable funding moat in a developed market. Together they give Shinhan something its domestic-bound rivals lack: a structural escape hatch from Korea's macro trap. But strategy doesn't execute itself. The transformation now underway is being driven by one man with an unusually personal connection to that very Japan franchise.

VI. Modern Leadership: The Era of Jin Ok-dong & "Value-Up 2.0"

Here is a detail that tells you almost everything about the man now running Shinhan. The overseas Japan franchise we just described—the one rivals can't replicate—was built and proven in no small part by the executive who today chairs the entire group. The Japan story isn't an abstraction to 진옥동 Jin Ok-dong. It's where he made his name.

Who Is Jin Ok-dong?

Jin Ok-dong is a Shinhan lifer, the embodiment of the professional-manager archetype that defines modern Korean banking. He spent years in Japan orchestrating the success of SBJ Bank, learning the cross-border franchise from the inside before rising through the organization. In 2019 he became CEO of 신한은행 Shinhan Bank, the group's core engine, and in March 2023 he ascended to Chairman of the entire holding company.1 His track record was strong enough that in late 2025 the group's board recommended him for a second three-year term, which would carry his mandate through 2029.1

This is not a founder. Shinhan has no founder-CEO sitting atop a controlling stake. It is run by professional managers who must continually earn their seats—a governance reality that shapes both the opportunity and the risk in this company, as we'll see.

Compensation & Incentive Structure

How is a professional steward of a financial empire paid, and—more importantly for investors—what is he paid to do? Chairman Jin's annual compensation runs in the range of KRW 1.2 billion to 1.5 billion, built from a base salary of roughly KRW 850 million plus performance-based bonuses of around KRW 446 million.1 By the standards of global megabank CEOs, that's modest. The interesting part is the long-term incentive design.

Jin's real wealth creation is tied to Performance-linked Stock (PS) grants—for instance, a grant of 17,841 shares in March 2025—deferred over a rigorous four-year vesting window running from 2025 through 2028.1 Deferral matters: it means the chairman cannot cash out on a good quarter and walk away. His payout depends on how the company performs over years, aligning him with the long-term shareholder rather than the short-term share price.

And the vesting isn't a rubber stamp. It's tied to hard quantitative hurdles: Total Shareholder Return measured relative to peers (beating KB, Hana, and Woori, not just rising with the tide), Return on Equity and Return on Tangible Common Equity, Common Equity Tier 1 capital safety levels, and the Cost-to-Income ratio. Layered on top are qualitative hurdles around internal risk controls and the progress of the group's AI-native transition.1 In other words, the incentive structure is itself the strategy, written into the chairman's paycheck: be more efficient than your rivals, return more capital, stay safe, and modernize.

The Professional Manager Dilemma

But this is where Korean banking gets genuinely thorny, and where an investor needs to pay attention. Because these groups have no controlling founder, they suffer acute agency problems and governance tension. The largest shareholders are institutions—above all the National Pension Service (NPS), the giant state pension fund—and they have, at various points, opposed management appointments at the big financial groups.3

Part of that friction traces to historical regulatory scars. The industry was rocked by episodes such as the Lime Asset Management fund-loss scandal, in which retail investors lost money on funds distributed through the banks, drawing regulatory warnings and reputational damage across the sector.3 When regulators issue warnings tied to a chairman or CEO, it gives ammunition to shareholders who want to block reappointments and injects political risk into what should be a straightforward governance process. Jin Ok-dong's core mandate, in a sense, is to make management independence undeniable—to deliver shareholder value so clearly that no regulator or institutional holder can credibly argue for his removal. Performance becomes a shield.

Value-Up 2.0: "Great Challenge 2030"

That brings us to the centerpiece of the modern Shinhan story. Jin took the group's initial Value-up push—call it Value-up 1.0, which delivered a 40.2% total shareholder return in 2024 and reached its 50% shareholder-return target in 2025—and escalated it into Value-up 2.0, branded "Great Challenge 2030."1

The headline policy is the one that genuinely breaks with Korean banking tradition: an "uncapped shareholder return" framework. Instead of committing to a fixed payout and stopping there, Shinhan tied its returns directly to its ROE—the more efficiently it earns, the more it gives back, with no artificial ceiling.1 Alongside it came a hard commitment to buy back and cancel 50 million outstanding shares by 2027.1 Share cancellation is the cleanest form of capital return there is—it permanently shrinks the share count, mechanically lifting earnings and book value per remaining share. For a stock languishing below book value, retiring shares below book is also wonderfully accretive: you're buying back equity for forty cents on the dollar.

This is the lever Shinhan is pulling to pry its valuation off the floor. Whether it works depends on durable structural advantages—and on risks that no amount of buybacks can buy away. To weigh both, we need to put the company through two classic strategic lenses.

VII. Strategic Frameworks: Hamilton's 7 Powers & Porter's 5 Forces

Strategy frameworks can be lazy box-checking, or they can be a disciplined way to separate durable advantage from temporary good fortune. Let's use them the second way, applying Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces to Shinhan specifically—not to banking in the abstract.

Hamilton's 7 Powers Applied to Shinhan

Scale Economies (High). The Big Four command enormous distribution networks and, crucially, enormous technology budgets. Shinhan's consolidated "Super SOL" super-app—which merged banking, credit-card, brokerage, and insurance services into a single platform—is a vivid example. Building and continuously upgrading a unified super-app is a massive fixed-cost endeavor. Spread across a giant customer base, the per-user cost is trivial; for a small regional or digital-only challenger, the same investment is crippling. Scale turns a huge expense into a competitive weapon.

Switching Costs (Moderate-High). Digital banking was supposed to make customers frictionless to poach—tap a button, move your money. In practice, the stickiness runs deeper than the checking account. A customer's primary salary deposit, mortgage, automatic bill payments, and bundled credit-card relationships form a web of small frictions. Unwinding all of it to chase a marginally better rate is a hassle most people never bother with. The relationship, not the product, is the lock-in.

Cornered Resource (High — Unique to Shinhan). This is the standout, and it's the one we've been building toward. Shinhan's 재일교포 Zainichi roots and the resulting structural dominance of SBJ은행 SBJ Bank in Japan constitute a true cornered resource—an asset competitors cannot acquire at any reasonable price because it isn't really for sale. KB, Hana, and Woori can hire bankers and apply for Japanese licenses, but they cannot retroactively be founded by Korean-Japanese entrepreneurs in 1982. The Vietnam franchise's native distribution is a softer version of the same idea: a hard-won position that took years to build and would take a rival years to challenge.

Counter-Positioning (Low-Moderate). Counter-positioning is when an incumbent can't copy a challenger without damaging its own business. For a while, the digital-native banks 카카오뱅크 KakaoBank and 토스뱅크 Toss Bank had this against the incumbents: they ran with no branch overhead, while Shinhan and its peers were saddled with expensive physical networks they couldn't abandon without alienating customers and staff. Shinhan's response has been to neutralize the disadvantage by aggressively closing underperforming branches—trimming toward roughly 660 outlets—and migrating to automated, AI-driven digital operations. It's catching up rather than out-positioning, hence the modest rating.

The remaining powers—network economies, process power, and branding—are present in milder forms (a trusted 40-year brand, some process advantages in risk management) but aren't where the durable edge lives. The edge lives in scale and, above all, the cornered Japan resource.

Porter's 5 Forces in the Korean Banking Oligopoly

Threat of New Entrants (Very Low). Banking is among the most heavily regulated industries on earth. In Korea, the Financial Services Commission (FSC) controls licensing, and obtaining a commercial banking license demands immense capital, regulatory blessing, and patience. This is the moat around the entire oligopoly—the reason our four boxers never face a fifth.

Bargaining Power of Customers (Moderate-High). Individually, a depositor is powerless. Collectively, armed with digital interest-rate comparison apps, retail consumers can now shop mortgage rates in seconds and force the banks into price wars. Transparency has handed real power to borrowers, compressing margins precisely where the banks make their money.

Bargaining Power of Suppliers (Low). A bank's primary "supplier" is the depositor providing raw funding. Individual retail depositors have virtually zero pricing power over the interest they receive. This asymmetry—weak suppliers, semi-powerful customers—is a defining feature of the business.

Threat of Substitutes (Moderate). Fintech platforms, direct stock-market investing, and non-bank wealth managers all compete for the same pool of household capital. They don't threaten the core deposit-and-lend machine outright, but they nibble continuously at fee income and at the margins of the relationship.

Competitive Rivalry (Extremely High). This is the dominant force. The contest among KB, Shinhan, Hana, and Woori is fierce, zero-sum, and obsessively focused on protecting Net Interest Margin. In a market that can't grow, every won one bank gains, another loses. This rivalry is exactly why the Value-up strategy matters: when you can't out-grow your rivals, the way to win the stock-market war is to out-return them.

Put the two frameworks together and a clear picture emerges. Shinhan sits inside a fortress (very low entry threat) but fights brutal hand-to-hand combat within it (extreme rivalry), defended by genuine scale and one irreplaceable cornered resource, while squeezed by empowered customers and demographic gravity. That tension—structural protection versus structural headwinds—is the heart of the investment debate.

VIII. The Investor's Playbook: Bull vs. Bear & Key KPIs

Every bank is, ultimately, a leveraged bet on the economy it serves and the discipline of the people running it. For a long-term owner of Shinhan, the noise of quarterly NIM moves matters far less than three numbers and one debate. Let's isolate them.

The Three KPIs That Matter Most

First, the CET1 Ratio, with a management target above 13.0%.1 Common Equity Tier 1 is the purest measure of a bank's capital cushion—the high-quality equity standing between the bank and insolvency if loans go bad. It is the guardrail on everything else. Crucially, under the Value-up framework, buybacks and dividends are only permitted if CET1 stays comfortably above this threshold. So this single ratio governs how much cash flows back to shareholders. Watch it, because it's the gate.

Second, Return on Equity (ROE/ROTCE), where Shinhan targets a level above 9.5%.1 This is the efficiency number—how much profit the bank squeezes from each won of equity capital. It is the metric most directly tied to dismantling the Korea Discount, because a bank that durably earns above its cost of capital deserves to trade at or above book value. The entire re-rating thesis lives or dies on ROE.

Third, the Shareholder Return Ratio, targeted above 50%.1 This tracks the percentage of earnings handed back via dividends and share cancellation. It is the ultimate alignment metric under Value-up 2.0—the proof, quarter after quarter, that management means what it says about returning capital rather than hoarding it for empire-building. These three move together: capital safety (CET1) permits efficiency-driven returns (ROE) to be paid out (return ratio). Track those, and you're tracking the thesis.

The Bull Case

The bull case is a re-rating story. Shinhan successfully completes its transformation from a sleepy, scale-obsessed, low-valuation bank into a disciplined capital-allocation machine. As ROE climbs above target and capital flows back through uncapped returns and share cancellation, the market is forced to re-rate the stock—dragging its price-to-book from the depressed ~0.4x of the Korea Discount era toward something closer to 0.8x.[^1] For a stock trading below book, that's a doubling of valuation without needing the underlying business to grow dramatically.

The growth, meanwhile, comes from overseas. Vietnam and Japan keep expanding their profit contribution, insulating the group from Korea's domestic plateau and giving investors a genuine engine that the purely domestic rivals lack. And on costs, the "Super SOL" app plus AI-native automation structurally lowers the Cost-to-Income ratio—doing more banking with fewer branches and fewer staff, permanently widening margins. Efficiency up, capital returned, growth imported from abroad: that's the bull's three-legged stool.

The Bear Case

The bear case is, fittingly, demographic and macroeconomic—and it's serious. The first and most profound risk is South Korea's demographic collapse. The country has the lowest birth rate in the world, and a shrinking, aging population structurally erodes the long-term domestic market for credit, mortgages, and consumer lending. You cannot grow a lending business in a country that is running out of borrowers. No app, however slick, fixes a demographic dead end. This is the slow-moving glacier beneath the entire domestic franchise.

The second risk is more acute: real-estate project financing (PF). Korea's construction and property-development sector has been a source of mounting concern, and a major wave of PF debt defaults would force Shinhan to book large loan-loss provisions—the credit-cost side of the equation we discussed, swinging violently in the wrong direction. A bad PF cycle could vaporize a year of earnings and, worse, breach the CET1 guardrail that permits shareholder returns, killing the Value-up story at its source.

The third risk is political. Korean banks operate under constant populist scrutiny. In periods of high rates, when banks post record profits while households struggle with mortgage payments, the government has leaned on the sector with "win-win finance" mandates—pressure to cap interest rates, share profits, or absorb troubled consumer debt. Such interventions directly crush profitability and can override even the best-laid capital plans. A bank's earnings, in the end, exist partly at the pleasure of the regulator.

Weigh it honestly and the debate comes down to a single question: can Shinhan's structural advantages—the cornered Japan resource, the Vietnamese growth engine, the genuine discipline of Value-up 2.0—compound faster than Korea's demographic and political gravity drags it down? That is the bet.

IX. Outro & Summary Lessons

Step back from the spreadsheets and what you have is one of the more improbable arcs in Asian finance. A bank founded in 1982 by 재일교포 Zainichi Korean immigrants—outsiders with capital but no political backing, no chaebol parent, and no government mandate—won its way into one of the most protected oligopolies on earth on the strength of something almost quaint: treating customers well. It then grew into a giant through a string of aggressive, premium-priced acquisitions—조흥은행 Chohung Bank, LG카드 LG Card, 오렌지라이프 Orange Life—each of which looked like an overpayment in the moment and, more often than not, paid off as a structural position over the decades.

And now it is attempting its most consequential transformation yet—one that has nothing to do with getting bigger. Under 진옥동 Jin Ok-dong, Shinhan is trying to rewrite the rules of Korean corporate governance and capital return, to prove that a Korean bank can earn its way out of the Korea Discount through efficiency and uncapped shareholder returns rather than asset accumulation. It has volunteered to be the test case for whether the entire 기업 밸류업 프로그램 Corporate Value-up Program can actually change how the market values Korean equities.

The enduring lesson for founders and investors is about the power of a structural advantage that the competition simply cannot clone. Shinhan's most defensible asset isn't its size—KB is bigger. It isn't its card business or its insurance arm—those can be matched. It is the un-replicable cross-border engine seeded by its immigrant founding: a profitable bank inside Japan and the largest foreign bank in Vietnam, together generating a sixth of group profit and, more importantly, an escape route from a home market hemmed in by demographics and politics. The deepest moats are often the accidents of origin that competitors can never go back and recreate. Whether that moat is wide enough to outrun Korea's gravity is the question every long-term owner of this company now holds.

References

-

Shinhan Financial Group Chairman Jin Ok-dong Recommended for Second Term — Korea Times, 2025-11-20 ↩↩↩↩↩↩↩↩↩↩↩↩

-

Shinhan Financial Group Ticker Profile & Stock Data — Reuters ↩

-

Shinhan Financial Group SEC Form 20-F Annual Filing (CIK: 0001235071) — SEC EDGAR ↩↩

-

SBJ Bank (Japan Office) Financial Highlights & Housing Loan Growth — SBJ Bank ↩↩↩

-

MBK Partners Exits Orange Life via KRW 2.3 Trillion Sale to Shinhan — Reuters, 2018-09-05 ↩↩

-

KB Financial Acquires Prudential Life Korea for KRW 2.3 Trillion at 0.8x P/B — S&P Global, 2020-04-10 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube