Hanmi Semiconductor: From Korean Backyard Startup to HBM Equipment Monopoly

I. Introduction & Cold Open

The conference room at SK Hynix's Icheon campus was tense. In March 2025, executives from South Korea's memory giant sat across from representatives of Hanmi Semiconductor—a company that had been their exclusive TC bonder supplier for eight years. Since 2017, Hanmi Semiconductor has been the exclusive supplier of TC Bonder equipment to SK Hynix, a major manufacturer of high-bandwidth memory (HBM). But something had changed. SK Hynix's procurement team has visited Hanmi Semiconductor's headquarters to implore them to change course, desperate to prevent what could become the most dramatic supplier relationship breakdown in the semiconductor industry.

The numbers told a story of extraordinary transformation. Hanmi Semiconductor has a market cap or net worth of 13.90 trillion as of October 16, 2025. Its market cap has increased by 50.08% in one year. For a company that started in a Korean industrial district when the country barely had a semiconductor industry, this represented one of the most remarkable ascents in technology history.

What unfolded in those meeting rooms wasn't just a negotiation—it was a power reversal four decades in the making. The small equipment supplier had become the kingmaker, capable of determining winners and losers in the AI chip race. The rapid growth of the HBM market has increased the negotiation powers of equipment makers that supply kits needed for the production of the memory chips and caused a power shift in the relationship between the customer and equipment supplier.

This is the story of how Hanmi Semiconductor transformed from an obscure Korean equipment maker into the bottleneck that could throttle the entire AI revolution. Every ChatGPT query, every autonomous vehicle calculation, every AI model training session ultimately depends on memory chips that can't be made without Hanmi's machines. In an industry where being first matters less than being essential, Hanmi had achieved something even more valuable than market dominance—they had become irreplaceable.

II. Origins: 1980s Korea & The Founder's Vision

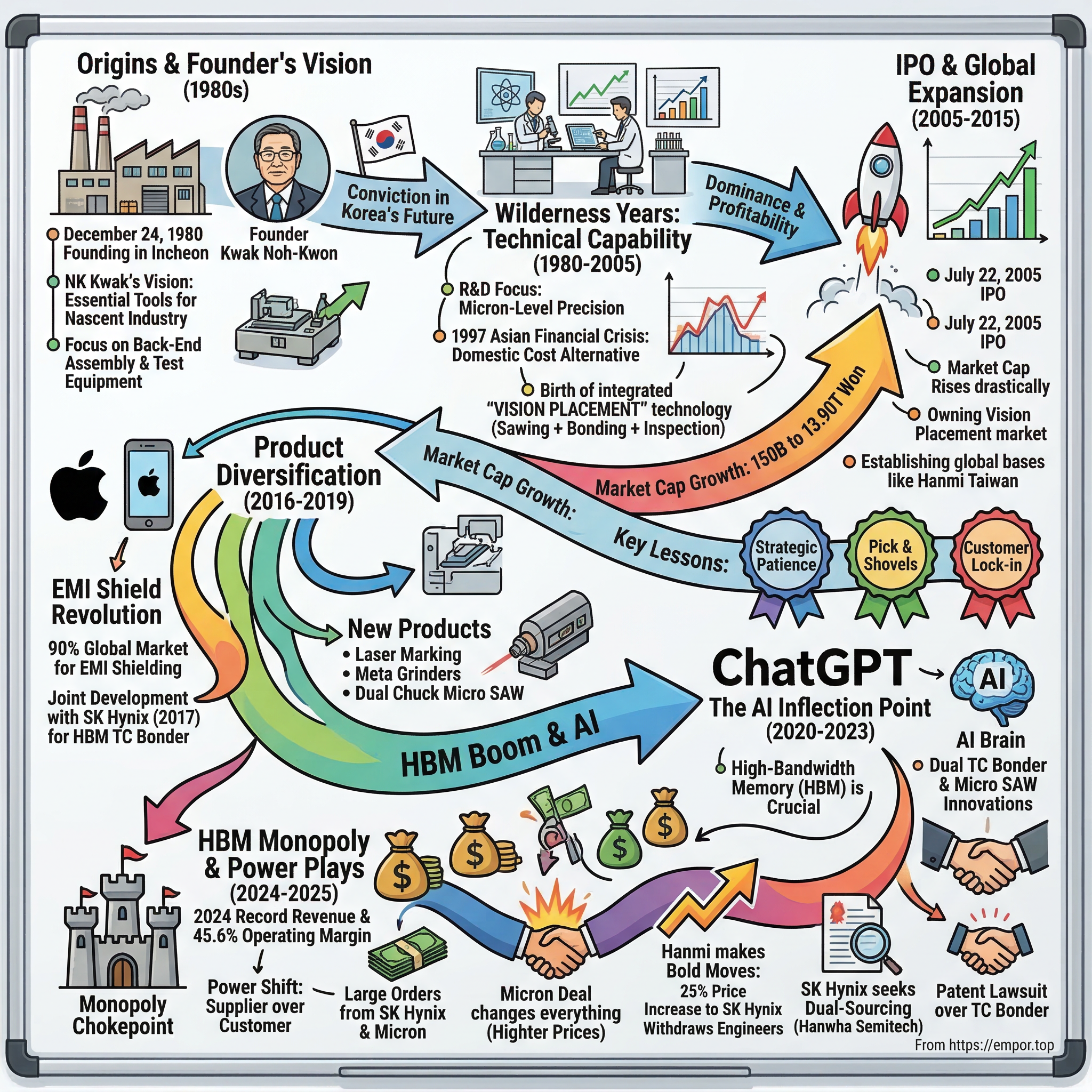

The company was founded by Kwak Noh-Kwon on December 24, 1980 and is headquartered in Incheon, South Korea. Picture South Korea in 1980: a nation still rebuilding from war, with per capita GDP barely above $1,600. Samsung had just entered the semiconductor business that very year. The idea of Korea becoming a semiconductor powerhouse seemed as far-fetched as suggesting that kimchi would become a global superfood.

Yet NK Kwak saw something others didn't. Founded in Korea by Chairman NK Kwak, HANMI Semiconductor launched the semiconductor equipment industry in Korea and raised the country's semiconductor equipment technology to the world level. While Samsung and other conglomerates were focused on building fabs and making chips, Kwak recognized a fundamental truth: someone needed to supply the tools.

The timing seemed almost absurd. Korea's semiconductor industry was essentially non-existent. There were no domestic customers, no ecosystem, no supply chain. Kwak was building equipment for factories that didn't exist yet, preparing for an industry that Korea hadn't even properly entered. It was the business equivalent of opening a gas station in a country that hadn't invented cars.

The early focus was deliberately narrow: assembly and test equipment. Not the glamorous front-end wafer processing tools that companies like Applied Materials dominated, but the back-end equipment that packaged and tested finished chips. It was unglamorous work—the semiconductor industry's equivalent of making the boxes rather than the products inside them. But Kwak understood that every chip, no matter how advanced, eventually needed to be cut, packaged, and tested.

The company started with a handful of employees in Incheon, operating more like a machine shop than a future technology leader. They reverse-engineered foreign equipment, improved upon designs, and slowly built competencies that would take decades to mature. While Japanese competitors like Disco dominated global markets, Hanmi quietly developed capabilities in equipment that others overlooked.

The decision to stay focused on equipment rather than becoming a chip manufacturer—a path many Korean companies took in the 1980s—would prove prescient. As Kwak would later tell employees, "We don't compete with our customers. We enable them." This philosophy of being the arms dealer rather than the warrior would define Hanmi's strategy for the next four decades.

What sustained them through those early years wasn't revenue—there was precious little of that—but conviction. NK Kwak believed that Korea would eventually become a semiconductor powerhouse, and when it did, domestic equipment suppliers would have advantages that foreign competitors couldn't match: proximity, cultural understanding, and the ability to provide round-the-clock support. He was building for a future that existed only in his imagination, betting everything on Korea's industrial transformation.

III. The Wilderness Years: Building Technical Capability (1980-2005)

Twenty-five years. That's how long Hanmi labored in relative obscurity, perfecting technologies that most people couldn't pronounce, let alone understand. While the tech world obsessed over Moore's Law and processor speeds, Hanmi's engineers huddled in clean rooms, obsessing over micron-level precision in chip placement and bonding equipment.

The 1990s brought Korea's semiconductor boom, with Samsung and Hynix (then Hyundai Electronics) emerging as global memory leaders. Finally, Hanmi had domestic customers with real volume. But having customers and making money were two different things. The company poured every won of profit back into R&D, developing their signature Vision Placement technology—essentially a hyper-precise robot with eyes that could place semiconductor components with sub-millimeter accuracy.

Particularly applauded for their Vision Placement technologies, HANMI has been ranked #1 worldwide for 17 consecutive years. But this dominance didn't happen overnight. Through the 1990s and early 2000s, Hanmi engineers worked grueling hours perfecting their vision alignment systems, developing proprietary algorithms that could compensate for microscopic variations in chip dimensions.

The Asian Financial Crisis of 1997 nearly killed them. While chaebols got government bailouts, small equipment suppliers like Hanmi had to survive on their own. They cut salaries, executives worked without pay, and engineers doubled as salespeople. One veteran employee recalled eating instant ramen for months because the company cafeteria had been shuttered to save money.

Yet the crisis also created opportunity. As Korean semiconductor companies desperately sought to reduce costs, importing expensive Japanese equipment became less attractive. Hanmi positioned itself as the domestic alternative—not quite as sophisticated as Disco or Shinkawa, but good enough and significantly cheaper. They won contracts not through superior technology but through proximity and price.

The real breakthrough came with a seemingly minor innovation: integrating multiple process steps into single machines. While competitors sold separate equipment for sawing, cleaning, inspection, and sorting, Hanmi combined them. VISION PLACEMENT is equipment that performs washing, drying, inspection, screening, and loading in the semiconductor packaging process in combination with Saw equipment in charge of sawing. It is a key equipment that accounts for more than 60% of total sales and ranked first in the global market share for 17 consecutive years from 2004 to last year.

By the early 2000s, Hanmi had quietly built something remarkable: a profitable, growing business in one of the world's most capital-intensive industries. They weren't making headlines or attracting venture capital, but they were generating consistent cash flow and building relationships with every major semiconductor company in Asia.

The decision to stay private for 25 years wasn't about avoiding scrutiny—it was about patience. NK Kwak understood that equipment businesses required enormous upfront investment with payoffs measured in decades, not quarters. Going public too early would have meant pressure for immediate returns, potentially derailing the long-term technology development that would eventually make them indispensable.

When other Korean equipment companies diversified into displays, solar panels, or LEDs, chasing whatever market was hot, Hanmi stayed focused on semiconductor assembly equipment. This wasn't stubbornness—it was strategic patience.

IV. IPO & The Vision Placement Dominance (2005-2015)

Hanmi semiconductor co., ltd completed its initial public offering (IPO) on July 22 ,2005. The timing was deliberate. After 25 years of building in obscurity, the company finally had a story worth telling to public markets. Since July 22, 2005, HANMI Semiconductor's market cap has increased from 150.57B to 13.90T, an increase of 9,128.91%.

The IPO roadshow presentations focused on one key message: Hanmi owned the Vision Placement market. Not competed in it, not participated in it—owned it. A company spokesperson said the company had an 80% global market share in the equipment. Investment bankers initially struggled to understand how a Korean company no one had heard of could dominate a critical semiconductor equipment category.

The 2008 financial crisis provided a brutal test of their public market readiness. 042700 reached its all-time high on Jun 14, 2024 with the price of 196,200 KRW, and its all-time low was 400 KRW and was reached on Oct 28, 2008. The stock lost over 90% of its value in a matter of months. Orders evaporated as semiconductor companies slashed capital spending.

But Hanmi did something counterintuitive: they accelerated R&D spending. While competitors laid off engineers, Hanmi hired them. While others canceled development projects, Hanmi doubled down on next-generation equipment. VP Dong-Shin Kwak, who had joined the family business, pushed for development of equipment for emerging packaging technologies that didn't even have commercial applications yet.

The bet paid off spectacularly. When the semiconductor industry roared back in 2010, Hanmi had equipment ready for advanced packaging techniques that competitors were still developing. They captured design wins at ASE, Amkor, and JCET—the world's three largest OSAT companies.

New innovative equipment lines are consistently being added to their roster – most recently the TSV Dual Stacking TC Bonder, Flip Chip Bonder and EMI Shield. The TSV (Through-Silicon Via) Dual Stacking TC Bonder represented a massive technological leap. This wasn't just an improvement on existing equipment—it was enabling entirely new chip architectures that would become critical for high-performance computing.

International expansion accelerated. 2016 Received 'THE BEST Award' and '10 BEST Award' selected by VLSI Research / Established 'Hanmi Taiwan'. Setting up Hanmi Taiwan wasn't just about being closer to TSMC—it was about embedding themselves in the world's most advanced semiconductor ecosystem.

By 2015, a remarkable transformation had occurred. The company that started as a Korean domestic supplier now generated the majority of revenue from international customers. They had over 300 customers globally, from massive IDMs to tiny specialty packagers. The student had become the master, with Japanese competitors now trying to copy Hanmi's integrated equipment approach.

Yet despite this success, Hanmi remained largely unknown outside the semiconductor industry. They didn't make chips that went into iPhones or processors that powered gaming consoles. They made the equipment that made those components possible. It was profitable anonymity, and management seemed perfectly content with it. The real revolution was still to come.

V. The EMI Shield Revolution & Product Diversification (2016-2019)

Apple changed everything. When the iPhone maker started demanding electromagnetic interference (EMI) shielding in their components in 2016, it triggered a cascade that would reshape Hanmi's trajectory. In 2016, global smartphone manufacturers such as Apple, Qualcomm and Broadcom introduced this process, and HANMI Semiconductor also presented EMI SHIELD equipment for the first time in 2016.

The EMI shielding process itself sounds almost alchemical: sputtering ultrathin layers of metal onto semiconductor packages to prevent electromagnetic waves from interfering with neighboring chips. As smartphones packed ever more radios, processors, and antennas into impossibly small spaces, EMI shielding became not just useful but essential.

HANMI owns 90% of the world market share for EMI shielding equipment. But this dominance wasn't accidental. When the EMI opportunity emerged, most equipment companies saw it as a niche market. Hanmi saw it as the future.

The development story was classic Hanmi: while competitors debated market potential, Hanmi's engineers were already in the lab. They developed eight different models in three years, each targeting specific applications. The EMI SHIELD VISION ATTACH 2.0 DRAGON became their flagship, combining vision inspection with precision attachment in a single platform.

The numbers validated the strategy. Last year sales and operating profit recorded record-high earnings of 373.1 billion won(USD 311.4M) and 122.4 billion won(USD 102.1M), respectively—and this was before the HBM boom that would soon transform the company.

2017 marked another pivotal moment with two seemingly unrelated developments. First, Establishment of 'Hanmi China'—a move that would later prove crucial for accessing the world's largest semiconductor market. Second, and far more consequentially, Hanmi began joint development of TC bonders with SK Hynix.

Hanmi Semiconductor jointly developed the TC bonder with SK Hynix in 2017. This wasn't just a supplier relationship—it was a technology partnership. SK Hynix needed equipment for their emerging HBM technology, and traditional bonders couldn't handle the thermal and precision requirements. Hanmi's engineers essentially embedded themselves at SK Hynix facilities, developing equipment in real-time alongside the memory giant's process engineers.

The collaborative development created an almost impenetrable moat. The TC bonders weren't just machines—they were customized to SK Hynix's specific processes, materials, and workflows. Every adjustment, every optimization, every software tweak created deeper lock-in. Since 2017, Hanmi Semiconductor has been the exclusive supplier of TC Bonder equipment to SK Hynix.

Product diversification accelerated. Beyond EMI and TC bonders, Hanmi launched meta grinders for AR/VR glass substrates, laser marking systems for automotive chips, and micro SAW equipment for package cutting. Each product line leveraged core competencies in vision systems and precision placement while targeting specific growth markets.

The transformation was remarkable. In 2016, Hanmi was primarily a Vision Placement company with a dominant but mature market position. By 2019, they had multiple product lines, each with leading market positions. Revenue exceeded 200 billion won, margins expanded, and the stock began its steady climb.

But the biggest change was psychological. Hanmi stopped thinking of itself as an equipment supplier and started seeing itself as an enabler of next-generation semiconductor technologies. They weren't just selling machines—they were selling capabilities that didn't exist anywhere else.

VI. The AI Inflection Point: HBM & The SK Hynix Partnership (2020-2023)

November 30, 2022. ChatGPT launched. Within five days, it had a million users. Within two months, 100 million. The world suddenly understood what those in the semiconductor industry had known for years: AI's hunger for memory was insatiable. And that memory needed to be special—not just fast, but architecturally revolutionary. Enter HBM.

High-Bandwidth Memory was not new. SK Hynix had been producing it since 2013. But it occupied a small niche, primarily for high-end graphics cards and supercomputers. The volumes were tiny, the customers limited. Then ChatGPT changed everything. Suddenly, every hyperscaler needed HBM. Not wanted—needed.

TC bonders play a pivotal role in HBM production by employing thermal compression to bond and stack chips on processed wafers, thereby significantly influencing HBM yield. Without TC bonders, you couldn't stack the eight, twelve, or sixteen DRAM dies that make up an HBM chip. And without HBM, you couldn't build the AI accelerators that power large language models.

Hanmi's 2017 joint development with SK Hynix suddenly looked prophetic. While competitors scrambled to develop HBM-capable equipment, Hanmi had been refining their TC bonders for six years. They understood not just the technology but the subtle process variations, the yield-limiting factors, the microscopic tolerances that separated success from expensive scrap.

The micro SAW breakthrough of 2021 proved equally timely. In 2021 HANMI outstepped their competitors by applying a dual chuck to micro SAW equipment improving productivity by more than 40%. This wasn't just an incremental improvement—it fundamentally changed the economics of HBM production. The dual chuck system could process wafers almost twice as fast as single chuck systems, critical when demand was exploding and every unit of capacity mattered.

Recognition followed performance. 2022 'micro SAW R&D Center' opened / micro SAW won 'IR52 Jang Young-sil Award'. The Jang Young-sil Award—Korea's most prestigious recognition for technological innovation—validated what customers already knew: Hanmi had leapfrogged Japanese competitors who had dominated saw equipment for decades.

The financial transformation was staggering. Last year, Hanmi Semiconductor achieved record sales (558.9 billion won) and an operating profit margin of 45.6%, while SK Hynix solidified its global No. 1 market share in HBM using Hanmi Semiconductor's TC bonder technology. A 45.6% operating margin in the equipment business was almost unheard of—more typical of software companies than industrial machinery manufacturers.

But success bred complications. As HBM became critical to AI infrastructure, depending on a single equipment supplier became a strategic vulnerability for SK Hynix. The memory giant began exploring dual-sourcing options, reaching out to ASMPT and eventually Hanwha Semitech. Hanmi's executives initially dismissed these efforts—their equipment was too specialized, too customized, too embedded in SK Hynix's processes for anyone else to replicate quickly.

The partnership that had seemed unshakeable began showing cracks. SK Hynix wanted supply chain resilience. Hanmi wanted recognition for their indispensable role—and compensation to match. The stage was set for one of the most dramatic supplier confrontations in semiconductor history.

VII. The HBM Monopoly: Power Plays & Supply Chain Drama (2024-2025)

The stock chart tells the story of 2024 better than any financial statement. 042700 reached its all-time high on Jun 14, 2024 with the price of 196,200 KRW. Investors finally understood what Hanmi executives had known for years: they held the keys to the AI kingdom.

The numbers were extraordinary. In March 2024 alone, SK Hynix placed orders totaling over 200 billion won. South Korean chip equipment company Hanmi Semiconductor Co. announced on Friday that it has received an order from SK Hynix Inc. for its dual TC bonder Griffin equipment used in high-bandwidth memory (HBM) manufacturing. The contract amount is 149.9 billion won ($109.5 million). But the real shock came from an unexpected source: Micron.

Hanmi Semiconductor has won a large order from US chipmaker Micron to supply thermal compression (TC) bonders used in the production of high-bandwidth memory (HBM). Hanmi Semiconductor has reportedly landed a major order from Micron for around 50 TC bonders lately, which would be significantly larger than the dozens of units shipped to the U.S. memory maker in 2024.

The Micron deal changed everything. Hanmi Semiconductor's TC bonders to Micron are 30% to 40% more expensive than the ones it supplies to SK Hynix. This is because Micron and SK Hynix use different methods to manufacture HBM. Micron uses non-conductive film, which requires a more sophisticated head on the bonders than SK Hynix's mass reflow-molded underfill.

Armed with a high-margin alternative customer, Hanmi made their move. In April 2025, they announced a 25% price increase for SK Hynix, effective immediately. Hanmi Semiconductor also notified that its unit prices for the bonders has gone up by 25% to 28% to the South Korean chipmaker. They withdrew their dedicated service engineers from SK Hynix fabs. They converted free maintenance services to paid contracts.

The move by Hanmi Semiconductor, where engineers are recalled and unit prices jump by double digits, is extremely rare in the chip industry. In the semiconductor world, where supplier relationships are measured in decades and built on trust, Hanmi's actions were the equivalent of a declaration of war.

The trigger was SK Hynix's decision to dual-source. SK Hynix's decision last month to sign contracts with Hanwha Semitek for the supply of around ten units of HBM TC Bonders worth 42 billion won. From SK Hynix's perspective, depending entirely on one supplier for critical HBM equipment was an existential risk. From Hanmi's perspective, it was betrayal.

The patent lawsuit added another dimension to the conflict. Hanmi Semiconductor filed a patent infringement lawsuit against Hanwha Semitech at the end of last year over the TC Bonder technology. The message was clear: Hanmi considered their TC bonder technology proprietary, developed through years of collaboration with SK Hynix, and would defend it aggressively.

The drama escalated through spring 2025. Hanmi Semiconductor announced on April 18 that it had canceled its investor relations (IR) meeting initially scheduled for April 22. Industry observers interpreted this as avoiding uncomfortable questions about the SK Hynix relationship.

By May, both companies were attempting damage control. Hanwha Vision, the parent company of Hanwha Semitech, said on Friday that its subsidiary signed a 38.5 billion won deal to supply TC bonders to SK Hynix. Hanmi Semiconductor announced on the same day that it signed a 42.8 billion won contract to do the same.

But the power dynamics had fundamentally shifted. Hanmi was no longer a supplier grateful for orders. They were a strategic asset with pricing power, alternative customers, and the confidence to challenge their largest client.

VIII. The Numbers: From Garage to Glory

The transformation of Hanmi from startup to semiconductor equipment giant reads like a financier's fairy tale, but the numbers are real, audited, and staggering.

In 2024, HANMI Semiconductor's revenue was 558.92 billion, an increase of 251.50% compared to the previous year's 159.01 billion. To put this in perspective, Hanmi's 2024 revenue growth rate exceeded that of Nvidia, the poster child of the AI boom. This wasn't gradual growth—it was an explosion.

The market cap evolution tells an even more dramatic story. Since July 22, 2005, HANMI Semiconductor's market cap has increased from 150.57B to 13.90T, an increase of 9,128.91%. That is a compound annual growth rate of 25.04%. For nearly two decades, Hanmi delivered returns that most venture capitalists only dream about, yet they did it as a public company making industrial equipment.

Operating margins reached levels typically associated with software companies, not machinery manufacturers. Last year, Hanmi Semiconductor achieved record sales (558.9 billion won) and an operating profit margin of 45.6%. This wasn't just profitability—it was pricing power manifested in financial statements.

HANMI Semiconductor grew its EBIT by 210% over twelve months. The EBIT growth rate of 210% in a mature industrial company defied conventional wisdom about equipment businesses. This wasn't a startup scaling from a small base—this was a 44-year-old company tripling its earnings.

For all of 2024, the operating profit soared more than sevenfold to 255.4 billion won, versus the same period in 2023. Seven-fold growth in operating profit meant that Hanmi was capturing extraordinary value from the HBM boom, converting revenue growth into even faster profit growth through operational leverage.

The stock performance reflected this fundamental transformation. 042700 stock has risen by 17.44% compared to the previous week, the month change is a 62.73% rise, over the last year Hanmi Semiconductor Co., Ltd has showed a 46.52% increase. In a year when most semiconductor stocks struggled with inventory corrections and demand uncertainties, Hanmi defied gravity.

Cash generation followed profits. For 2024, it will pay a total of 68.3 billion won in dividends, or 720 won per share – its largest-ever annual dividend payout. That compares with the dividend payment of 40.5 billion won in 2023, or 420 won per share. The 70% dividend increase signaled management's confidence in sustainable cash flows.

The balance sheet remained remarkably clean despite explosive growth. HANMI Semiconductor has net cash of ₩12.8b, as well as more liquid assets than liabilities. it had cash of ₩37.8b as well as receivables valued at ₩211.0b due within 12 months.

But perhaps the most telling number was customer concentration. Despite having over 300 customers globally, the top three—SK Hynix, Micron, and major OSATs—likely represented over 70% of revenue. This concentration was both Hanmi's greatest strength and most significant risk, a dynamic that would define their strategic choices going forward.

IX. Playbook: Lessons in Strategic Patience

Forty-four years. That's how long it took Hanmi to become an overnight success. Their playbook reads like a masterclass in strategic patience, written in machinery oil and clean room protocols.

Lesson 1: The Power of Strategic Myopia While competitors chased every hot market—displays, solar, LEDs—Hanmi stayed ruthlessly focused on semiconductor assembly equipment. They resisted diversification not from lack of imagination but from strategic discipline. As one executive explained, "We'd rather be the best at one thing than mediocre at many."

Lesson 2: Timing Beats Speed Hanmi wasn't first to market with most of their breakthrough products. Japanese competitors had TC bonders before them. American companies pioneered vision systems. But Hanmi had something more valuable than first-mover advantage: perfect timing. They entered markets just as inflection points emerged—EMI shielding as smartphones densified, TC bonders as HBM exploded, dual-chuck saws as AI drove volume.

Lesson 3: Customer Lock-in Through Co-development The SK Hynix partnership exemplified Hanmi's approach to customer relationships. By co-developing equipment, they created switching costs that went beyond economics. Hanmi Semiconductor jointly developed the TC bonder with SK Hynix in 2017. Every optimization, every customization, every process tweak created deeper interdependence. The equipment wasn't just purchased—it was woven into the customer's technological DNA.

Lesson 4: The Picks-and-Shovels Premium During gold rushes, sell picks and shovels. Hanmi understood this perfectly. While memory makers faced brutal cyclicality and commodity pricing, Hanmi's equipment commanded steady margins. They captured value from the semiconductor boom without the capital intensity of running fabs or the market risk of selling chips.

Lesson 5: Build Before Demand Exists Hanmi's greatest strategic insights came from building capabilities before markets existed. They developed HBM equipment before ChatGPT made it critical. They created EMI shielding systems before 5G made them essential. This required not just patience but conviction—funding R&D for products without clear customers.

Lesson 6: Vertical Specialization vs. Horizontal Expansion Rather than building broad equipment portfolios like Applied Materials or LAM Research, Hanmi went deep in specific niches. Particularly applauded for their Vision Placement technologies, HANMI has been ranked #1 worldwide for 17 consecutive years. They preferred 80% market share in narrow segments over 8% share in large markets.

Lesson 7: Managing Concentration Risk Through Indispensability Having customer concentration would typically be seen as a weakness. Hanmi turned it into strength by becoming so essential that customers couldn't afford to leave. The recent tensions with SK Hynix proved the point—even with the relationship strained, SK Hynix continued placing orders because they had no real alternatives.

Lesson 8: Price Like a Monopolist, Service Like a Startup Despite their market power, Hanmi maintained the service intensity of a hungry startup. Engineers remained on-site at customer facilities. Support was 24/7. Customization requests were accommodated. They charged monopoly prices but delivered startup-level attention.

X. Power Dynamics: The New Semiconductor Kingmaker

The semiconductor industry has always been about power—electrical power, processing power, market power. But the rise of AI added a new dimension: the power to determine who could even participate in the race.

Hanmi's position in 2025 resembled ASML's in extreme ultraviolet (EUV) lithography, but with a crucial difference. While ASML's monopoly was protected by decades of R&D and billions in investment, Hanmi's emerged almost accidentally, through the unexpected explosion of HBM demand. They didn't plan to become a chokepoint—they simply happened to be holding the right technology when the world needed it desperately.

The rapid growth of the HBM market has increased the negotiation powers of equipment makers that supply kits needed for the production of the memory chips and caused a power shift in the relationship between the customer and equipment supplier. This wasn't just about pricing. It was about determining production schedules, technology roadmaps, even competitive dynamics between memory makers.

Consider the cascade effects. When Hanmi decided to prioritize Micron orders over SK Hynix, they weren't just shifting production schedules—they were potentially altering the competitive balance in the HBM market. Hanmi Semiconductor's move may be a strategy to prioritize highly profitable orders from Micron. Every TC bonder allocated to Micron was one not available to SK Hynix, directly impacting who could supply Nvidia, AMD, and other AI chip designers.

The geopolitical implications were equally profound. As U.S.-China technology tensions escalated, control over HBM production equipment became a strategic consideration. Hanmi, a Korean company, found itself in the middle of great power competition. Their decisions about customer allocation and technology transfer had national security implications.

The attempted dual-sourcing by SK Hynix revealed the limits of Hanmi's power—and its extent. This signals the end of Hanmi Semiconductor's dominance in supplying TC bonder to SK Hynix as it was effectively the sole supplier of the equipment. Even as SK Hynix brought in alternative suppliers, they couldn't abandon Hanmi. The alternatives weren't drop-in replacements—they required process requalification, yield optimization, and months of parallel running.

The pricing power Hanmi wielded was almost unprecedented in semiconductor equipment. A 25-28% price increase, implemented unilaterally, with immediate effect. Hanmi increased TC bonder prices for SK hynix by 25–28% and withdrew all engineers from its Icheon HBM line to focus more on Micron. In an industry where annual price reductions were the norm, Hanmi's price increases were a shock to the system.

But power in semiconductors is never permanent. Japanese equipment makers, stung by Hanmi's success, accelerated their own HBM equipment development. Chinese companies, backed by government funding, targeted TC bonder technology as a strategic priority. Even Hanmi's legal action against Hanwha suggested vulnerability—if the technology could be replicated, even imperfectly, their monopoly would erode.

The most intriguing dynamic was Hanmi's potential partnership with Samsung. Amid the tensions with SK hynix, the potential collaboration between Hanmi and Samsung seems to be brought back at the table recently. Samsung, currently redesigning HBM3E to address yield issues, is considering the cooperation with Hanmi as one of its key improvement strategies.

XI. Bull vs. Bear Case & Future Scenarios

The Bull Case: The AI Revolution Has Just Begun

Bulls see Hanmi as selling arms in a war that's just starting. AI model complexity doubles every few months. Each generation requires exponentially more memory bandwidth. HBM4, HBM5, and beyond will need even more sophisticated equipment. Hanmi isn't just riding the wave—they're building the surfboards.

The Micron relationship validates the bull thesis. Micron is even mulling to double down on Hanmi, with another order of 20 to 30 TC bonders expected in the second half of this year. If Micron, with its sophisticated internal equipment development, chooses to depend on Hanmi, it suggests the technical moat is deeper than skeptics believe.

Geographic expansion provides another growth vector. Samsung's potential adoption would nearly double Hanmi's addressable market. Chinese memory makers, despite trade restrictions, desperately need HBM capability. Even Intel, reentering the foundry business, could become a customer.

The financial fortress Hanmi has built—nearly 46% operating margins, net cash position, minimal capital requirements—provides enormous flexibility. They could acquire complementary technologies, fund next-generation R&D, or simply return massive cash to shareholders while maintaining growth investments.

Bulls point to the multi-decade semiconductor supercycle. Every connected device, every autonomous vehicle, every AR/VR headset needs advanced packaging. Hanmi's equipment enables not just HBM but the entire heterogeneous integration trend. They're not betting on one technology but on the fundamental trend toward system-level integration.

The Bear Case: Concentration Creates Vulnerability

Bears see existential risks hiding in plain sight. Customer concentration remains extreme despite the Micron wins. If SK Hynix successfully dual-sources and reduces dependence, Hanmi's pricing power evaporates. The current margins aren't sustainable—they're an aberration caused by temporary supply-demand imbalance.

Technology transitions pose another threat. HBM might be the answer today, but what about tomorrow? New memory architectures—processing-in-memory, compute-express-link, optical interconnects—could obsolete current packaging approaches. Hanmi's TC bonders, optimized for current HBM structures, might become expensive paperweights.

Competition is intensifying. Global companies like Besi and ASMPT, which dominate the hybrid bonder market in non-memory fields such as image sensors (CIS), have also conducted preliminary tests to supply sample equipment to SK Hynix. ASMPT and Besi are intensifying their research to bring hybrid bonder technology cultivated in the system semiconductor domain into the memory sector. These aren't startups—they're established players with deep pockets and global reach.

The legal battle with Hanwha reveals another vulnerability. If Hanmi's patents can be challenged or designed around, their moat becomes a fence. The fact that SK Hynix was willing to risk the relationship by dual-sourcing suggests they believe alternatives are viable.

Bears also worry about the semiconductor cycle. The industry's boom-bust patterns are well established. Current HBM shortages and AI euphoria mirror previous cycles that ended in tears. When the music stops—and it always does—equipment makers suffer first and worst as customers slash capital expenditure.

The Most Likely Scenario: Profitable Erosion

Reality will likely land between extremes. Hanmi maintains leadership but at lower margins as competition emerges. SK Hynix successfully dual-sources but can't abandon Hanmi entirely. Pricing power diminishes but remains above historical equipment industry averages. The company transitions from monopolist to dominant player—still highly profitable but no longer untouchable.

The key variable isn't technology or competition—it's time. How long can Hanmi maintain their current position? Every quarter of monopoly profits funds more R&D, builds higher switching costs, and extends their lead. But every quarter also gives competitors time to catch up, customers time to qualify alternatives, and new technologies time to emerge.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube