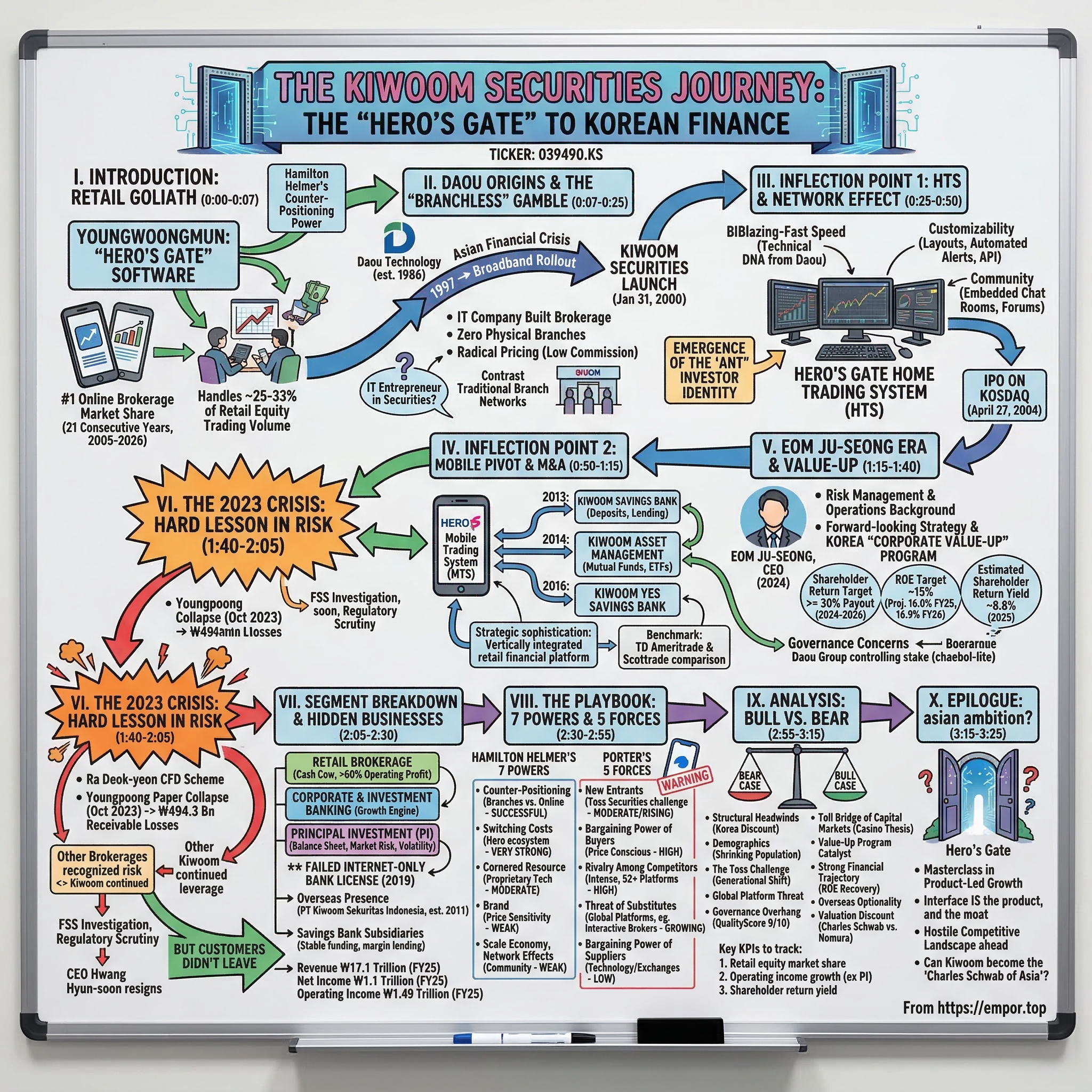

Kiwoom Securities: The "Hero's Gate" to Korean Finance

I. Introduction: The Retail Goliath (0:00-0:07)

Picture Seoul's Yeouido financial district on a volatile Monday morning. The KOSPI is swinging wildly, foreign institutional money is flooding out, and across the country, millions of Koreans are glued not to Bloomberg terminals or bank-issued apps but to a piece of software called Youngwoongmun—literally, "Hero's Gate." They are tapping furiously on their phones, buying the dip, selling the rip, and arguing in chatrooms embedded directly into their brokerage platform. The company behind that software is not Samsung Securities. It is not KB Financial or Mirae Asset. It is Kiwoom Securities, a 26-year-old company with zero physical branches, roughly 642 full-time employees, and a market capitalization that recently touched ₩11.6 trillion (approximately $8.5 billion). Kiwoom handles somewhere between a quarter and a third of all retail equity trading volume in South Korea on any given day. It has held the number one position in online brokerage market share for 21 consecutive years, since 2005.

In most countries, the dominant retail brokerage is an appendage of a century-old bank—a legacy institution that bolted on a trading app sometime around 2015 and called it innovation. In South Korea, the story ran in reverse. An IT company built a brokerage from scratch, stripped out every cost that legacy competitors took for granted, and turned a commoditized transaction—buying and selling stocks—into a product experience so sticky that traders developed what can only be described as muscle memory. That software platform, the Hero series, became the literal interface of capitalism for an entire generation of Korean retail investors, affectionately (and sometimes derisively) known as the "Ants."

The thesis on Kiwoom is deceptively simple. The company used what Hamilton Helmer would call a "Counter-Positioning" power—going fully online when every incumbent was anchored to expensive branch networks—and layered on genuine switching costs through a proprietary trading system that users learned so deeply they could execute orders in their sleep. The open question, and the one that makes Kiwoom fascinating for long-term investors in 2026, is whether that brokerage dominance can serve as a springboard into something larger: a full-spectrum financial technology conglomerate that captures not just the trading commissions but the lending, asset management, and banking wallet of Korea's increasingly sophisticated retail investor base. Or whether the company that once disrupted the dinosaurs is itself becoming one, as a new generation of mobile-first challengers like Toss Securities nips at its heels.

This is the story of how a tech company became the gatekeeper of Korean wealth—and what it means for investors trying to understand the most retail-driven stock market in the developed world.

II. The Daou Origins and the "Branchless" Gamble (0:07-0:25)

To understand Kiwoom, you have to start not with finance but with databases. In 1986, a Korean engineer named Kim Ik-rae founded Daou Technology, an IT services company focused on localizing foreign software products for the Korean market. Through the 1990s, Daou made its name by bringing Informix's relational database management system and Netscape's web browser to Korean enterprises—work that sounds mundane in retrospect but was genuinely pioneering in a pre-internet Korea still building out its digital infrastructure. Kim took Daou public on the Korea Stock Exchange in August 1997, just months before the Asian Financial Crisis would devastate the country's financial system and force an IMF bailout. That crisis, paradoxically, planted the seed for everything that followed.

The aftermath of the 1997 crisis reshaped Korean finance in ways that are hard to overstate. Dozens of securities firms, merchant banks, and mutual savings institutions collapsed or were forcibly merged. The government deregulated aggressively, opening the door for new entrants. And crucially, Korea embarked on one of the most ambitious broadband rollouts in history. By the early 2000s, South Korea had the highest broadband penetration rate on Earth. Every apartment building was wired. PC bangs (internet cafes) were on every corner. The infrastructure for online finance didn't need to be built—it already existed for gaming and communication.

Kim Ik-rae saw the opening. On January 31, 2000—right at the peak of the global dot-com bubble—he launched Kiwoom Securities as a subsidiary of Daou Technology. The timing looked suicidal. The NASDAQ was weeks away from its crash. The KOSDAQ, Korea's tech-heavy exchange, was about to lose more than 80% of its value. Venture-backed internet companies across Korea were imploding. And here was an IT services entrepreneur launching a new securities firm?

But Kim's bet was structural, not cyclical. He was not betting on the market going up. He was betting on the method of trading shifting permanently online. And his structural advantage was devastating. Every incumbent Korean brokerage—Samsung Securities, Daewoo Securities, Hyundai Securities, the entire old guard—operated through networks of physical branches staffed by licensed salespeople in expensive Gangnam and Yeouido real estate. Those branches were not just costly; they were the organizing principle of the entire business model. Client relationships ran through branch managers. Research was distributed in paper reports. Orders were placed by phone.

Kiwoom launched with none of it. No branches. No floor traders. No glossy offices with leather chairs. Just servers, software, and a radical pricing proposition. While incumbents charged commission rates of 50 to 100 basis points per trade—standard for the Korean market at the time—Kiwoom entered the market at a fraction of that cost. The pitch was blunt: why pay a branch manager's salary when the software can do everything faster? This was the Korean equivalent of what Charles Schwab did in the United States in the 1970s when he introduced discount brokerage, or what ETRADE attempted in the 1990s. But Kiwoom had an advantage that neither Schwab nor ETRADE enjoyed: it was entering a market where the broadband infrastructure was already ubiquitous and the population was already digitally native. Korea didn't need to be convinced to go online. It was already there.

The early years were a grind. Kiwoom had to build trust in a market where retail investors associated "real" brokerages with physical presence. Korean culture placed enormous weight on face-to-face relationships, particularly in finance. The company hemorrhaged money initially, subsidizing commissions to acquire customers, investing heavily in the trading platform, and fighting for regulatory credibility. But the math was relentless. Without branches, Kiwoom's cost-to-income ratio was structurally lower than any competitor. Every customer acquired was more profitable at the margin. And in a commoditized business like equity brokerage, where the product—executing a buy or sell order—is fundamentally identical across providers, the lowest-cost operator with adequate technology eventually wins on volume.

By the mid-2000s, the gamble was paying off. Kiwoom's market share in online equity trading was climbing steeply, and the company was approaching a milestone that would cement its transformation from scrappy startup to a force that the Gangnam old guard could no longer ignore.

III. Inflection Point 1: Creating the "Network Effect" via HTS (0:25-0:50)

Walk into any Korean day trader's home office in the mid-2000s—and there were hundreds of thousands of them—and you would find a multi-monitor setup running a single piece of software: Kiwoom's Youngwoongmun, the "Hero's Gate" Home Trading System, known in industry shorthand as HTS. The name itself was clever marketing. In Korean, youngwoong means "hero," and mun means "gate" or "door." The implication was aspirational: this software was your gateway to becoming a market hero, a self-made investor who didn't need a broker whispering in your ear.

But the software's stickiness went far beyond branding. To understand why traders refused to leave Kiwoom's platform, you need to understand what an HTS actually is and why it matters so much in the Korean trading ecosystem. Think of it as a Bloomberg Terminal for the masses—except instead of costing $24,000 a year, it was free. An HTS is a desktop application that provides real-time stock quotes, charting tools, order execution, portfolio management, news feeds, and increasingly, algorithmic trading capabilities. In Korea, unlike in the United States where web-based platforms dominated early, the HTS became the standard interface for retail trading. Every brokerage offered one. But Kiwoom's was different.

First, speed. Kiwoom inherited deep systems engineering talent from its parent Daou Technology, which had spent years optimizing database and network infrastructure for Korean enterprises. That technical DNA showed up in Hero's Gate as blazing-fast order execution and near-zero latency on quote updates—critical for the kind of rapid-fire day trading that was becoming a national pastime. In a market where milliseconds could mean the difference between catching a limit-up stock and missing it entirely, Kiwoom's speed advantage was real and measurable.

Second, customizability. Hero's Gate allowed users to create their own screen layouts, build custom indicators, set up automated alerts, and eventually, through the Kiwoom Open API+, write their own trading algorithms. This was a profound decision. By opening up the platform to user customization and even third-party development, Kiwoom turned Hero's Gate from a tool into an ecosystem. Power users invested dozens or even hundreds of hours configuring their personal setups. Every custom chart layout, every personalized watchlist, every automated trigger became an invisible switching cost. Leaving Kiwoom didn't just mean opening a new account somewhere else—it meant rebuilding an entire workflow from scratch.

Third, and perhaps most importantly, community. Korean HTS platforms embedded chat rooms, discussion boards, and real-time commentary directly into the trading interface. Kiwoom's user base became a self-reinforcing community of traders sharing tips, debating stocks, and developing a shared vocabulary and culture. This was Reddit's WallStreetBets a decade before Reddit's WallStreetBets existed. The platform became a social experience, and social experiences create network effects. The more traders used Hero's Gate, the more valuable the community became, which attracted more traders.

This was the era when the "Ant" investor identity crystallized. Korean retail investors had long been called "ants"—a term that carried a slight condescension, implying they were small, easily crushed by the institutional elephants and foreign whales that dominated the KOSPI. But during the mid-2000s bull market that lifted the KOSPI from under 800 points after the 2003 credit card crisis to over 2,000 by 2007, the ants discovered collective power. And their weapon of choice was Kiwoom's Hero's Gate. The company became synonymous with retail trading in Korea the way Robinhood would later become synonymous with retail trading in America—except Kiwoom actually made money doing it.

The company's IPO on the KOSDAQ on April 27, 2004, was a coming-of-age moment. Just four years after founding, Kiwoom had gone from a zero-branch experiment to a publicly listed company with rapidly growing market share. The listing provided capital for further platform development and gave the broader market a way to bet on the secular shift from branch-based to online trading. By 2005, Kiwoom had achieved the number one market share position in online retail brokerage—a throne it has never relinquished.

The significance of this period cannot be overstated. Kiwoom didn't just build a low-cost brokerage. It built the default interface through which an entire generation of Koreans learned to interact with capital markets. When millions of people learn to trade stocks through the same piece of software, when their muscle memory is wired to a specific set of keyboard shortcuts and screen layouts, you have created something far more durable than a price advantage. You have created what Helmer would call switching costs—not contractual, not financial, but cognitive and habitual. That moat would prove remarkably resilient, surviving market crashes, scandals, and the most disruptive technology shift of the 21st century: the smartphone.

IV. Inflection Point 2: The Mobile Pivot and M&A Strategy (0:50-1:15)

When Apple's iPhone launched globally and Samsung's Galaxy series began transforming Korea into the world's most smartphone-saturated market in the early 2010s, it posed an existential question for Kiwoom: could a company whose entire competitive advantage was built on a desktop application survive the shift to mobile? The answer was not obvious. Korea's incumbent brokerages, despite being slow to adopt online trading, actually had an opportunity to leapfrog Kiwoom by building mobile-first experiences unburdened by legacy desktop architecture. If the playing field reset to mobile, Kiwoom's HTS moat could dissolve overnight.

Kiwoom moved fast. The company launched its Mobile Trading System (MTS), branded Hero S, and invested aggressively in making the mobile experience as close to the desktop's power-user capabilities as a smartphone screen would allow. This was not trivial. Compressing the information density of a multi-monitor HTS setup into a 5-inch screen required genuine product thinking, not just responsive design. Kiwoom solved it by creating a modular interface that let users drill into the specific functions they needed—order execution, charting, watchlists, news—without overwhelming them with everything at once. Critically, the mobile app maintained the same account infrastructure, the same API access, and the same community features that desktop users relied on. A trader could set up a complex conditional order on their desktop at home and monitor it from their phone on the subway. The seamlessness mattered.

The incumbents, by contrast, were predictably slow. Samsung Securities, KB Securities, and NH Investment were still running their mobile initiatives through traditional IT departments embedded in banking bureaucracies. Their apps felt like afterthoughts—clunky, slow, designed by committee. Kiwoom's tech-company DNA, inherited from Daou, gave it a speed advantage in mobile development that extended the company's lead rather than narrowing it.

But Kiwoom's leadership understood that being the best brokerage app was necessary but not sufficient. The brokerage business, even at massive scale, has a fundamental ceiling: it is transaction-dependent. When markets are hot and retail investors are trading actively, Kiwoom prints money. When markets cool and volumes contract, revenue drops sharply. The 2008 global financial crisis had demonstrated this vulnerability painfully. To build a more durable business, Kiwoom needed to capture more of the financial value chain—lending, deposits, asset management—so that it could earn revenue even when its customers weren't trading.

This strategic logic drove a series of acquisitions in the 2013-2016 period that transformed Kiwoom from a pure-play online broker into a diversified financial group. The most significant was the acquisition of what became Kiwoom Savings Bank in 2013 (formerly Samshin Savings Bank, originally established in 1983). A savings bank in the Korean financial system is a specialized institution that serves individuals and small-to-medium enterprises with deposit accounts, personal loans, and credit products. It operates under a different regulatory framework than a full commercial bank, with lower capital requirements but also restrictions on the types of customers it can serve.

Why would an online brokerage want a savings bank? The answer reveals Kiwoom's strategic sophistication. The savings bank license gave Kiwoom the ability to take deposits—a stable, low-cost funding source that doesn't evaporate when stock markets decline. More importantly, it allowed Kiwoom to offer margin lending and credit products directly to its existing trading customer base. Instead of losing those customers to other institutions when they needed leverage or personal credit, Kiwoom could keep them in-house. The savings bank was followed by Kiwoom YES Savings Bank (formerly TS Savings Bank) in 2016, doubling down on the deposit-gathering strategy.

The acquisition of Woori Asset Management in early 2014 for ₩75.5 billion extended the ecosystem further. Rebranded as Kiwoom Asset Management, this gave the company a platform to offer mutual funds, ETFs, and managed investment products directly through the Hero trading interface. A trader who started with Kiwoom to buy individual stocks could now also park money in Kiwoom-managed funds during periods when they wanted professional management. Every product added to the ecosystem increased the share of wallet captured from each customer and raised the switching costs further. Leaving Kiwoom no longer meant just losing your screen layouts—it meant untangling your savings account, your margin loan, and your fund holdings.

To benchmark this strategy globally: it mirrors what TD Ameritrade did in the United States when it acquired Scottrade in 2017 for $4 billion, adding Scottrade's branch network and customer accounts to TD Ameritrade's digital platform. The logic was the same—consolidate the retail brokerage customer base and then cross-sell additional financial products. Kiwoom executed a similar playbook at a fraction of the price in a smaller market, and arguably with greater strategic coherence because it didn't need to absorb a branch network it had no use for.

By the mid-2010s, Kiwoom had quietly assembled something that looked less like a discount broker and more like a vertically integrated retail financial platform: brokerage, savings banking, asset management, and an increasingly sophisticated research and advisory capability, all unified by the Hero ecosystem. The question was whether the management team could execute on this vision without overreaching—a question that would be answered, brutally, by the events of 2023.

V. Current Management: The Eom Ju-seong Era (1:15-1:40)

Every technology company eventually faces the founder transition—the moment when the visionary who built the thing from nothing must step aside and let professional operators scale it. For Kiwoom, this transition was neither clean nor voluntary. It was forced by crisis.

Kim Ik-rae, the Daou Technology founder who launched Kiwoom Securities, had long operated in the background of the company's public persona. Unlike the charismatic founder-CEOs of Silicon Valley lore, Kim was an engineer and dealmaker who preferred to exercise influence through the holding company structure rather than direct operational control. Daou Technology (and its data subsidiary, Daou Data) maintained a controlling stake in Kiwoom Securities—approximately 48.9% as of the most recent disclosures—giving the Daou Group effective control over the brokerage without Kim needing to sit in the CEO's chair.

The CEO role at Kiwoom was held for years by Hwang Hyun-soon, a company veteran who oversaw the mobile transition and the diversification M&A strategy. Hwang's tenure was marked by consistent growth in market share and revenue, and under his leadership, Kiwoom solidified its position as the undisputed leader in retail online brokerage. But Hwang's era ended abruptly in late 2023, when a cascade of scandals—most critically the Youngpoong Paper debacle—forced his resignation and triggered a leadership overhaul that the company is still navigating.

The man who stepped into this breach was Eom Ju-seong, nominated as CEO in January 2024. Eom is the archetype of the "career company man"—a Kiwoom lifer whose background is in risk management and operations rather than sales or dealmaking. His appointment was a deliberate signal. After a period in which Kiwoom's risk controls had catastrophically failed, the board chose a CEO whose entire professional identity was built around managing risk. The choice reflected both internal recognition that the company's growth-at-all-costs culture needed guardrails and external regulatory pressure from the Financial Supervisory Service, which had been investigating Kiwoom's oversight failures with increasing intensity.

Eom's first year was consumed by crisis management and rebuilding credibility with regulators, but by 2025, he began articulating a forward-looking strategy anchored in Korea's broader "Corporate Value-Up" program. Launched by the Financial Services Commission in February 2024, the Value-Up program was South Korea's answer to Japan's famous corporate governance reforms—an attempt to close the persistent "Korea Discount" by pressuring listed companies to improve shareholder returns, boost ROE, and increase transparency. For securities firms like Kiwoom, the program was both a direct tailwind (more market activity means more trading volume) and a challenge (the company itself needed to demonstrate Value-Up credentials to investors).

Kiwoom's response has been a shareholder return framework targeting a 30% or higher payout ratio over the 2024-2026 period, combined with an ROE target of approximately 15%. Analyst forecasts suggest the company is on track, with projected ROE of 16.0% for fiscal 2025 and 16.9% for 2026, and a shareholder return yield estimated at 8.8% for 2025. These are not abstract financial targets. They represent a conscious shift in corporate philosophy from the growth-and-reinvestment mentality of the Hwang era to a more balanced approach that rewards shareholders while maintaining investment in technology and new business lines.

The governance structure, however, remains a persistent concern for institutional investors. The Daou Group's controlling stake in Kiwoom, exercised through a web of cross-holdings between Daou Technology, Daou Data, and related entities, creates what governance analysts call a "chaebol-lite" structure. ISS assigned Kiwoom a Governance QualityScore of 9 out of 10 (where 10 is the worst) as of January 2026, with particularly poor scores in Audit (10) and Shareholder Rights (10). The "governance discount"—the gap between what Kiwoom's earnings power would warrant in a market with strong shareholder protections and what investors are actually willing to pay given the controlling group structure—is a real and material factor in the stock's valuation. Whether Eom Ju-seong, as a career insider who owes his position to the controlling shareholders, can meaningfully reform governance from within remains one of the central questions hanging over the investment case.

For now, the management transition appears to be working at the operational level. The company stabilized after the 2023 crisis, resumed earnings growth, and is executing on its diversification strategy. But the true test of the Eom era will not be managing calm waters. It will be how the company navigates the next crisis—and whether the risk management culture he represents has genuinely been embedded in the organization or remains a veneer applied after the last disaster.

VI. The 2023 Crisis: A Hard Lesson in Risk (1:40-2:05)

The story of Kiwoom's worst year begins not in Seoul's financial district but in the offices of an unregistered investment consulting firm run by a man named Ra Deok-yeon. Ra operated a scheme that exploited a financial product called a Contract for Difference, or CFD—a leveraged derivative that allows investors to bet on stock price movements without actually owning the underlying shares. CFDs are the financial equivalent of trading on steroids: they amplify both gains and losses, sometimes by a factor of ten or more. In Korea, CFDs had become increasingly popular among aggressive retail traders looking for outsized returns, and brokerages were happy to facilitate them because the commissions and financing fees were lucrative.

Ra's scheme allegedly involved using CFDs and other leveraged products to accumulate massive positions in a group of small and mid-cap Korean stocks, artificially inflating their prices. When the manipulation eventually unwound, the stocks collapsed, and the trail of destruction led straight to Kiwoom Securities, which had served as a primary broker for many of the tainted transactions. The Financial Supervisory Service (FSS) launched a formal investigation into whether Kiwoom had engaged in unfair sales practices related to CFDs and whether its consumer protection measures were adequate.

But the CFD scandal was merely the appetizer. The main course came in October 2023, when Youngpoong Paper—a small paper company whose stock price had inexplicably surged 730% over the preceding months on the basis of a bonus share issue—suddenly collapsed. The price plunge was catastrophic and triggered a cascade of margin calls on leveraged positions. Kiwoom reported that ₩494.3 billion (approximately $365 million) in outstanding receivables were incurred in customer consignment accounts due to the Youngpoong Paper debacle.

Here is what made the Youngpoong Paper loss particularly damaging for Kiwoom's reputation: while every other major Korean brokerage—Mirae Asset Securities, Korea Investment & Securities, NH Securities, Samsung Securities—had recognized the elevated risk in Youngpoong Paper's parabolic stock price and stopped allowing leveraged investments in the stock during the first half of 2023, Kiwoom continued to permit margin trading and CFD positions in the name right up until the crash. The failure was not one of bad luck. It was a failure of risk management, of exactly the kind of oversight that a mature financial institution is supposed to have in place. Other firms saw the danger and acted. Kiwoom did not.

The political and regulatory fallout was swift. CEO Hwang Hyun-soon, who had led the company through its most successful growth period, was compelled to step down. Prosecutors opened investigations into potential stock manipulation connections. The FSS intensified its scrutiny of Kiwoom's internal controls, and the scandal dominated Korean financial media for weeks. For a company that had built its brand on being the trustworthy home of the retail investor, the optics were devastating. The "Hero's Gate" had let in the villains.

And yet—and this is perhaps the most telling detail of the entire episode—the customers did not leave. Kiwoom's market share in retail brokerage barely budged. The scandal that dominated headlines, forced out the CEO, and cost the company hundreds of billions of won in losses did not trigger a meaningful exodus of trading accounts. Why? Because of exactly the switching costs described earlier. A Korean trader who has spent years customizing their Hero's Gate setup, who has their savings bank accounts, margin facilities, and fund holdings all within the Kiwoom ecosystem, and whose trading muscle memory is wired to Kiwoom's interface, faces enormous friction in switching to a competitor. The scandal tested the durability of those switching costs in the harshest possible environment, and they held.

This does not excuse the risk management failure, and investors should weigh it heavily. A company that allows leveraged trading on a stock that every peer has flagged as dangerous is a company that either lacks adequate risk controls or deliberately ignores them in pursuit of revenue—both of which are serious red flags. The appointment of Eom Ju-seong, with his risk management background, is the organizational response to that failure. But one personnel change does not guarantee that the institutional culture has changed. The 2023 crisis is the most important data point in evaluating whether Kiwoom deserves the kind of premium valuation that its market position might otherwise command.

The company survived the crisis. It remains dominant. But the scar tissue matters—both as a reminder of what can go wrong when a brokerage prioritizes volume over prudence, and as a baseline against which to measure whether the new management team has genuinely reformed the culture of risk.

VII. Hidden Businesses and Segment Breakdown (2:05-2:30)

Beneath the headline retail brokerage business, Kiwoom operates several less visible but strategically important segments that are worth understanding for anyone trying to build a complete picture of the company's earnings power and growth trajectory.

The retail brokerage remains the foundation. It accounts for more than 60% of operating profit and is the segment most investors associate with the Kiwoom name. This is the cash cow—high-margin, volume-dependent, and deeply entrenched. In fiscal 2024, Kiwoom generated total revenue of approximately ₩3.14 trillion, with net income of ₩835 billion. These numbers represented a meaningful recovery from the crisis-dampened 2023, when net income was ₩436 billion, and reflected both a recovery in market trading volumes and the absence of the exceptional Youngpoong Paper loss. The 2025 fiscal year showed further acceleration, with revenue jumping to ₩17.1 trillion and net income reaching ₩1.1 trillion—though the revenue figure requires careful interpretation as it includes gross financial revenue (interest income, trading gains) that is not directly comparable to net operating revenue. The key metric to watch is operating income, which climbed to ₩1.49 trillion in 2025, up from ₩1.09 trillion the prior year, demonstrating genuine earnings leverage as volumes recovered.

The corporate and investment banking segment represents Kiwoom's growth engine. The company has been steadily building capabilities in debt capital markets—underwriting corporate bonds, asset-backed securities, and structured products—as well as equity capital markets, including IPO underwriting. This segment does not yet rival the brokerage in profitability, but it diversifies the revenue base away from pure retail transaction dependency. In a Korean capital markets environment where corporate bond issuance has been growing and the IPO pipeline remains active, this segment provides countercyclical stability. When retail volumes are soft, institutional advisory and underwriting fees can partially offset the decline.

The principal investment (PI) segment is perhaps the most intriguing and least understood piece of the Kiwoom puzzle. Like many large securities firms globally, Kiwoom uses its own balance sheet—which stood at ₩81.2 trillion in total assets as of the end of 2025—to make proprietary investments in equities, bonds, real estate, and alternative assets. This is, in effect, a hedge fund embedded inside a brokerage. The PI book can generate substantial returns when markets cooperate and substantial losses when they do not. It is the segment most directly exposed to market risk and the one that requires the most careful monitoring from investors. The returns from PI can swing operating profit materially from quarter to quarter, making it critical to distinguish between "core" brokerage earnings and PI-driven volatility when assessing Kiwoom's underlying earnings quality.

Beyond the three core segments, Kiwoom has been quietly building an overseas presence that could become meaningful over a longer time horizon. The most developed international operation is PT Kiwoom Sekuritas Indonesia, which Kiwoom took majority control of in 2011. Indonesia—with its young, rapidly digitizing population of 280 million and an emerging middle class hungry for investment products—represents exactly the kind of market where Kiwoom's low-cost, technology-first brokerage model could replicate its Korean success. Kiwoom Indonesia launched the Hero trading platform locally and has been growing its customer base, though the subsidiary remains small relative to the Korean parent. The broader opportunity to export the "Korean fintech model" to Southeast Asian markets with favorable demographics but underdeveloped retail brokerage infrastructure is a genuine long-term optionality in the stock—one that the market assigns essentially zero value to today.

The savings bank subsidiaries—Kiwoom Savings Bank and Kiwoom YES Savings Bank—round out the financial ecosystem. These provide stable deposit funding, serve as platforms for consumer and SME lending, and crucially, enable Kiwoom to offer integrated financial services (margin lending, credit products) to its brokerage customers without relying on external financing. They are the quiet plumbing of the Kiwoom ecosystem—rarely discussed by analysts but essential to the company's ability to capture full wallet share from its customers.

One notable gap in the portfolio: Kiwoom applied for a license to operate an internet-only bank in 2019 as part of Korea's "fourth mobile bank" race but failed to win approval from the Financial Services Commission. The winners of Korea's internet bank licenses—KakaoBank and K bank—have gone on to become massive success stories, demonstrating the enormous value of a full banking license in a digitally advanced market. Had Kiwoom won that license, the company's trajectory might look very different. As it stands, the savings bank licenses provide a partial substitute, but the absence of a full banking charter limits Kiwoom's ability to compete in deposits, payments, and mainstream consumer banking—all areas where its customer base and technology could theoretically give it an edge.

For investors parsing the segment data, the key insight is that Kiwoom is less monolithic than it appears. The brokerage cash cow funds growth investments in IB, overseas expansion, and financial services diversification. The PI book adds volatility. And the savings banks provide a stable funding base. Evaluating Kiwoom requires looking at each of these pieces separately rather than relying solely on consolidated numbers.

VIII. The Playbook: Hamilton's 7 Powers and Porter's 5 Forces (2:30-2:55)

Evaluating Kiwoom Securities through the lens of competitive strategy frameworks reveals a company with genuine structural advantages—but also important vulnerabilities that are often underappreciated.

Hamilton Helmer's 7 Powers

The most powerful force in Kiwoom's history was Counter-Positioning. When the company launched in 2000 as a branchless, online-only brokerage, the incumbents faced a classic innovator's dilemma. Samsung Securities, Daewoo Securities, and the other legacy firms could see that online trading was the future, but they could not rationalize their branch networks without destroying their existing business models. Every branch they closed would anger existing customers who valued in-person service, reduce their physical brand presence, and trigger union pushback. Kiwoom had no such constraints. It could offer dramatically lower prices precisely because it had no legacy infrastructure to protect. The incumbents eventually built competitive online platforms, but by the time they did, Kiwoom had already captured the most price-sensitive, highest-volume retail traders—the exact customers that drive brokerage profitability.

Switching Costs represent Kiwoom's most enduring power. The Hero's Gate ecosystem—with its customizable desktop layouts, proprietary API for algorithmic trading, integrated community features, and linked savings bank and asset management accounts—creates multi-layered friction that goes far beyond simple account transfer costs. Traders who have spent years building personalized setups face cognitive switching costs (learning a new interface), workflow switching costs (rebuilding their trading environment), and financial switching costs (transferring margin accounts, fund holdings, and credit facilities). The 2023 crisis tested these switching costs under extreme stress, and they held firm. This is probably the single most important structural advantage Kiwoom possesses today.

Cornered Resource applies partially. Kiwoom's proprietary technology stack, developed over two decades with deep roots in Daou Technology's systems engineering expertise, is a genuine competitive advantage—but it is not irreplicable. A well-funded competitor with strong engineering talent could build a comparable trading platform given enough time and investment. What they cannot easily replicate is the accumulated user base, the community network effects, and the institutional knowledge embedded in 25 years of platform iterations.

The powers Kiwoom does not possess are equally instructive. There is no meaningful Scale Economy power in Korean brokerage beyond basic infrastructure amortization—the market is large enough to support multiple profitable players. There is no Brand power in the traditional sense; Korean retail investors are notoriously price-sensitive and will switch for meaningful commission differences, as Toss Securities has demonstrated. And Network Effects, while present in the community features, are weaker than in true platform businesses because trading itself is not inherently a network activity—one person's buy order does not become more valuable because more people are on the same platform.

Porter's 5 Forces

The Threat of New Entrants in Korean digital brokerage is moderate and rising. The most significant recent entrant is Toss Securities, launched in 2020 by Viva Republica (the company behind Korea's ubiquitous Toss payments app). Toss entered the brokerage market with a mobile-first, commission-free approach specifically designed to appeal to younger investors who find Kiwoom's Hero's Gate complex and intimidating. Toss amassed over 5 million customers rapidly and, by October 2024, actually overtook Kiwoom in overseas stock trading market share for the first time—a shocking milestone given Kiwoom's 21-year dominance. Kiwoom's CEO Eom Ju-seong explicitly acknowledged this threat in his 2025 New Year's address, warning that "light and nimble pursuers are threatening our business model." The company responded with a "Hero Membership" loyalty program offering cash rewards to high-volume traders—a defensive play that implicitly concedes Toss's competitive pressure on commissions and user experience.

Bargaining Power of Buyers is high. Korean retail investors are among the most price-conscious in the world, comparison-shopping commission rates and switching for basis-point differences. Yet Kiwoom's switching costs and platform habituation allow it to maintain slight pricing premiums over pure discount competitors without losing its core power-user base. The tension between buyer price sensitivity and platform stickiness is the central competitive dynamic in Korean brokerage.

Rivalry Among Existing Competitors is intense. South Korea's digital brokerage market includes over 52 platforms—an extraordinary number for a country of 52 million people. Kiwoom competes not only with Toss but with Samsung Securities (backed by Korea's largest conglomerate), Mirae Asset Securities (the largest by total assets), KB Securities (part of the KB Financial Group banking empire), and NH Investment & Securities (backed by the agricultural cooperative network). This is a knife fight for market share, and aggressive promotional offers—signup bonuses, temporary zero-commission periods, cash rewards—regularly erode industry margins.

Threat of Substitutes is growing. The most significant substitute threat comes not from other Korean brokerages but from international platforms. As Korean retail investors increasingly shift their attention to U.S. stocks (the "overseas stock boom"), platforms like Interactive Brokers that offer direct access to global markets represent a potential bypass of the Korean brokerage system entirely. If a Korean investor can trade Tesla shares directly through a U.S.-regulated platform with lower costs and broader market access, the value proposition of going through Kiwoom diminishes. Regulatory barriers currently limit this threat, but they are not permanent.

Bargaining Power of Suppliers is low. Kiwoom's key suppliers are technology vendors, exchange connectivity providers, and data feeds—none of which hold pricing power over a buyer of Kiwoom's scale.

The net assessment: Kiwoom operates in a structurally competitive market with genuine but eroding advantages. Its switching costs are real but face a generational challenge as younger investors whose habits have not yet calcified may default to Toss or other mobile-first platforms. Its counter-positioning advantage is historical, not ongoing—everyone is online now. The company's durability rests on whether it can leverage its installed base and financial ecosystem into something stickier than any single competitor can replicate.

IX. Analysis: The Bull vs. Bear Case (2:55-3:15)

The Bear Case

Bears will start with the structural headwinds facing the Korean market itself. The "Korea Discount"—the persistent gap between valuations of Korean stocks relative to global peers with comparable profitability—has been one of the most discussed topics in Asian investing for over a decade. Korean stocks trade at roughly 0.8-1.0x book value on average, compared to 1.5-2.0x for comparable Japanese firms and 3-4x for U.S. financial companies. The causes are well-documented: chaebol governance structures, weak shareholder protections, cross-shareholdings, and a regulatory environment that has historically prioritized economic stability over investor returns. Kiwoom both suffers from this discount (its own stock trades cheaply relative to its earnings power) and is partially defined by it (if Korean stocks were valued more fairly, there might be less frantic retail trading to generate commission revenue).

Demographics pose a longer-term challenge. South Korea's fertility rate, at approximately 0.7, is the lowest in the OECD and arguably the lowest in human history for a large, developed nation. The population is expected to decline significantly over the coming decades. Fewer Koreans means, eventually, fewer retail trading accounts. This is not an imminent threat—the current generation of investors is large and active—but it sets a ceiling on long-term domestic volume growth.

The Toss challenge is real. Toss Securities has demonstrated that a mobile-native platform with sleek UX and commission-free trading can rapidly capture market share from Kiwoom, particularly among investors under 35. If the generational shift in trading preferences continues, Kiwoom's 21-year market share leadership could erode meaningfully. The company's response—loyalty programs and cash rewards—amounts to paying customers to stay, which is a margin-destructive strategy that an attacker like Toss, backed by venture capital and willing to lose money to grow, can sustain longer.

The global platform threat adds another vector of concern. As Korean investors pour record amounts into U.S. stocks—retail investors invested a record $12.7 billion in overseas stocks in a single month in early 2026—the question arises whether Korean brokerages are the best conduit for that activity or whether investors will eventually migrate to platforms with direct U.S. market access and lower FX conversion costs.

And the governance overhang persists. Kiwoom's ISS Governance QualityScore of 9 out of 10 is among the worst for a company of its size on the Korean exchange. The Daou Group's controlling structure, the complex cross-holdings, and the lack of truly independent board oversight create ongoing uncertainty about whether management decisions will prioritize minority shareholders' interests.

The Bull Case

Bulls see Kiwoom as the toll bridge of Korean capital markets. The company does not need to pick winning stocks or predict market direction. It needs Koreans to trade—and Koreans trade a lot, in bull markets and bear markets, in domestic stocks and increasingly in foreign ones. Every time a Korean retail investor buys or sells a share of Samsung, SK Hynix, or Tesla, there is roughly a one-in-four chance that transaction flows through Kiwoom. This is the "casino" thesis: the house wins regardless of which gambler gets lucky.

The Value-Up program is the most significant potential catalyst. If the Korean government's efforts to close the Korea Discount succeed even partially—through improved governance standards, higher dividend payout ratios, and active share buyback programs—the effect on Korean equity market turnover could be substantial. Higher stock valuations attract more retail participation, which generates more trading volume, which directly benefits Kiwoom. The company is arguably the single largest beneficiary of a successful Value-Up program, which is why analysts have flagged it as a core "Value-Up trade."

Kiwoom's own financial trajectory supports the bull case. The recovery from 2023's crisis year has been strong, with operating income nearly doubling from ₩585 billion in fiscal 2023 to ₩1.09 trillion in 2024 and reaching ₩1.49 trillion in 2025. ROE has climbed back toward the mid-teens, and the 30%+ shareholder return target provides a meaningful yield floor for the stock. At recent trading levels, the stock offers an estimated shareholder return yield of approximately 8.8%—an attractive combination of dividends and buybacks that compensates investors for the governance risk.

The overseas expansion optionality—particularly in Indonesia and potentially other Southeast Asian markets—represents unpriced upside. If Kiwoom can replicate even a fraction of its Korean success in markets with far more favorable demographic profiles, the growth story extends well beyond the constraints of Korea's shrinking population. This is a free option embedded in the current stock price.

On valuation, Kiwoom trades at a significant discount to global peers. Charles Schwab, the closest U.S. analogue, trades at roughly 4-5x book value. Japan's Nomura Holdings, a more comparable Asian peer, trades at approximately 0.8-1.0x book. Kiwoom's price-to-book ratio sits somewhere in between, but its profitability metrics—particularly its ROE trajectory—are closer to Schwab's than to Nomura's. If the Korea Discount narrows even modestly, the re-rating potential is substantial.

Key KPIs to Track

For investors monitoring Kiwoom's ongoing performance, three metrics matter most:

First, retail equity market share by trading value on KOSPI and KOSDAQ. This is the single most important competitive metric. Kiwoom has held the number one position for 21 consecutive years, but the Toss challenge makes this metric critical to watch quarterly. Any sustained decline below 20% would signal a structural shift in competitive dynamics.

Second, operating income growth (excluding principal investment gains and losses). Because the PI book can swing profitability wildly, investors should track the "core" operating income from brokerage, savings banking, and IB activities separately. This reveals whether the underlying franchise is growing or merely riding market volatility.

Third, shareholder return yield (dividends plus buybacks as a percentage of market cap). In the Value-Up era, management's willingness to actually return capital rather than just promise to do so is the clearest signal of governance quality and shareholder alignment. The 8.8% projected yield for 2025 sets a high bar; any retreat from this level would raise questions about management credibility.

X. Epilogue and Closing (3:15-3:25)

Twenty-six years ago, an IT entrepreneur in Seoul looked at the Korean brokerage industry—a world of Gangnam offices, leather-bound client portfolios, and telephone order desks—and saw it for what it was: a commodity business drowning in unnecessary cost. Kim Ik-rae did not invent online trading. He did not invent discount brokerage. He did not invent the Home Trading System. What he did was execute the integration of all three with ruthless efficiency in a market that was uniquely ready for it—a country with universal broadband, a culturally embedded passion for stock speculation, and a post-crisis financial system that had been forced open to new entrants.

The result was a company that became the default interface of Korean capitalism. Millions of Koreans learned to buy their first stock through Hero's Gate. Millions more learned to day trade, to read candlestick charts, to argue about P/E ratios in chatrooms, to feel the adrenaline of a limit-up notification—all through Kiwoom's software. The "Ant" investors who collectively moved trillions of won during the Donghak Ant Movement of 2020, who pushed the KOSPI above 3,000 for the first time in January 2021, who poured a record $12.7 billion into overseas stocks in a single month in early 2026—they overwhelmingly did so through Kiwoom.

For founders and entrepreneurs, the Kiwoom story is a masterclass in product-led growth in a heavily regulated industry. The company did not succeed by lobbying for regulatory favors or partnering with banks. It succeeded by building software so good, so fast, and so customizable that users chose it despite the lack of physical branches, glossy marketing, or brand heritage. It succeeded by understanding that in a commoditized business, the interface is the product, and the product is the moat.

The next act is less certain. Kiwoom faces a competitive landscape that is more hostile than at any point in its history. Toss Securities is stealing share among younger investors. Global platforms are luring Korean money overseas. The demographic headwinds are real and worsening. The governance structure remains a drag on valuation. And the memory of the 2023 risk management failure lingers as a reminder that operational excellence in technology does not automatically translate into operational excellence in risk oversight.

Can Kiwoom become the "Charles Schwab of Asia"—a multi-product financial technology conglomerate that transcends its brokerage origins to become the central financial platform for hundreds of millions of retail investors across Asia? The ambition is there. The technology foundation is there. The question is whether the management team, the governance structure, and the corporate culture are equal to the aspiration. The Hero's Gate is open. What walks through it next will determine whether Kiwoom Securities remains a Korean success story or becomes an Asian one.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube