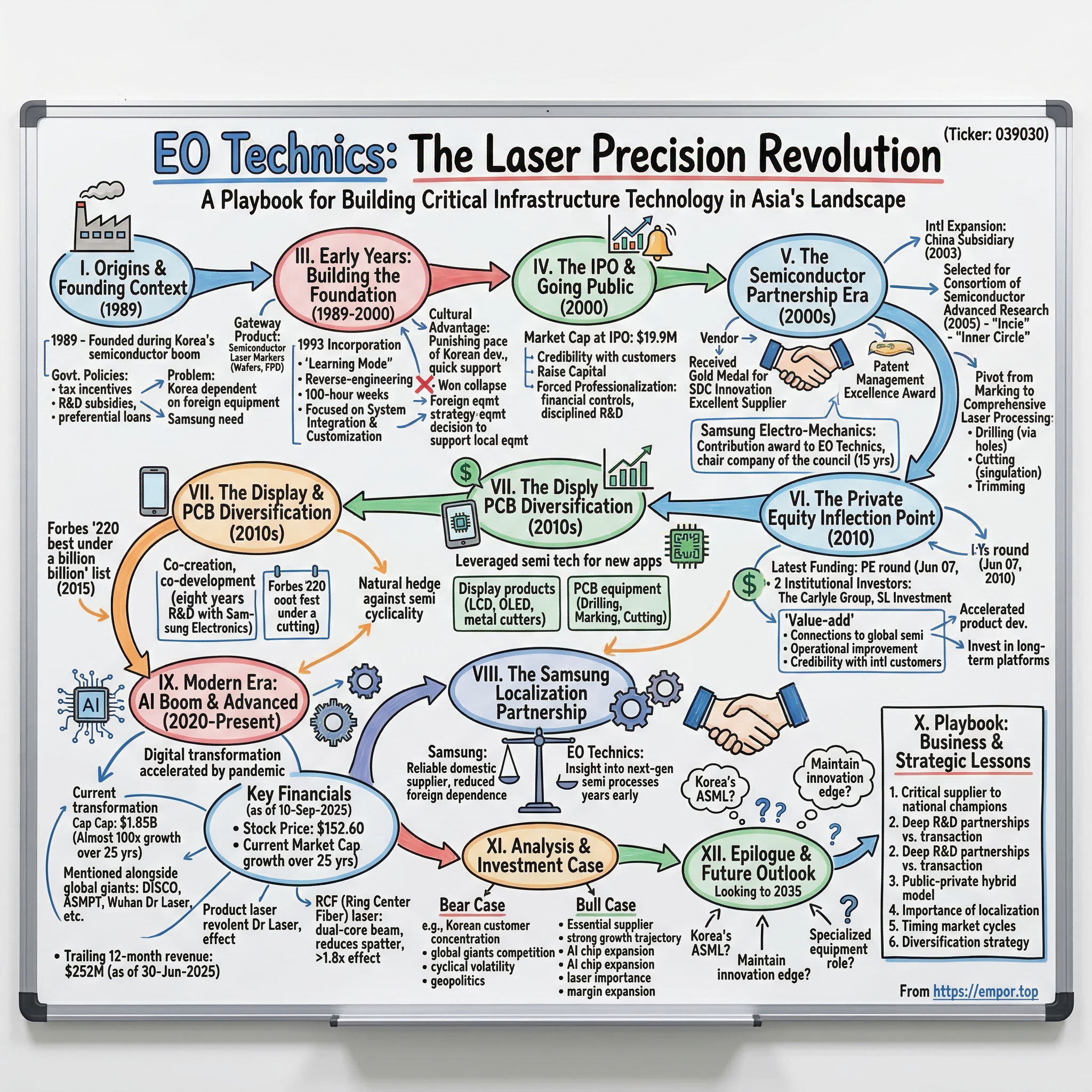

EO Technics: The Laser Precision Revolution

I. Introduction & Episode Roadmap

Picture this: It's 1989, and Korea's semiconductor industry is in its infancy, desperately dependent on foreign equipment that costs millions and takes months to deliver. A small team of engineers decides to build laser marking equipment locally - not because it's easy, but because Samsung needs it yesterday. Fast forward to 2025, and that startup, EO Technics, has become a $19.9M market cap at IPO transformed into a multi-billion dollar enterprise, essential to the global semiconductor supply chain.

Today we're diving into EO Technics, Korea's laser processing equipment pioneer that supplies top-quality laser solutions for cutting, drilling, patterning, grooving, and welding. This is the story of how a Korean startup founded in the shadow of Samsung became indispensable to the world's most advanced chip manufacturers.

The central question we'll explore: How did a company from a non-traditional semiconductor geography build world-class technology that even industry giants couldn't ignore? It's a playbook for building critical infrastructure technology in Asia's hypercompetitive landscape, where being second means being last, and where partnerships with national champions can make or break your future.

What you'll learn today goes beyond just one company's journey. This is about understanding how geopolitics shapes technology supply chains, why patient capital and decade-long R&D investments create moats that money alone can't buy, and how the symbiotic relationship between equipment makers and chip manufacturers drives innovation forward.

II. Origins & Founding Context

The year 1989 marked a pivotal moment in Korea's technological ascent. The Berlin Wall was falling, the world was globalizing, and Korea was transitioning from a manufacturing hub for foreign companies to a creator of its own technological destiny. Samsung had just become a major player in DRAM production, but there was a critical problem: every piece of advanced equipment had to be imported from Japan, the United States, or Europe.

Into this environment stepped the founders of EO Technics. The company was founded in 1989 during what would become known as Korea's semiconductor boom. The timing wasn't accidental - the Korean government had launched ambitious industrial policies promoting high-tech manufacturing, offering tax incentives, R&D subsidies, and preferential loans to companies willing to localize critical technologies.

The laser technology landscape in the late 1980s was dominated by a handful of players. CO2 lasers were the workhorses of industrial processing, but semiconductor manufacturing demanded something more precise. The challenge wasn't just technical - it was existential. How do you compete with companies that had decades of experience and patent portfolios worth billions?

The answer lay in a specific niche: semiconductor laser marking. Every chip needed identification - lot numbers, date codes, manufacturer information. This wasn't glamorous work, but it was essential. And crucially, it was a gateway. Master marking, and you earn the trust to move into drilling. Master drilling, and cutting becomes possible. It was a deliberate, methodical approach to climbing the value chain.

III. Early Years: Building the Foundation (1989-2000)

The company was incorporated in 1993, marking its formal beginning as a legal entity. Those first four years between founding and incorporation were spent in what the founders would later describe as "learning mode" - studying imported equipment, reverse-engineering where legally possible, and most importantly, understanding what Korean manufacturers actually needed versus what foreign suppliers were offering.

The initial focus on semiconductor laser markers proved prescient. The Company's main offerings are laser markers, which are used to record information like date, name and sorts on the surface of wafers, inside of flat panel displays (FPDs) and other materials. But breaking into Samsung's supply chain - the holy grail for any Korean equipment maker - required more than just technical competence.

The local advantage was real but nuanced. Yes, Korean engineers could visit Samsung's fabs within hours instead of requiring international flights. Yes, they could provide support in Korean. But the real advantage was cultural: understanding the punishing pace of Korean semiconductor development, where "quickly" meant yesterday and "good enough" was never good enough.

Technical challenges mounted daily. American and Japanese equipment makers had decades of accumulated knowledge. They had relationships with laser source manufacturers, specialized optics suppliers, and software developers. EO Technics had enthusiasm and proximity. The company's engineers often worked 100-hour weeks, sleeping in the office, driven by a mixture of national pride and startup desperation.

Building R&D capabilities from scratch meant making hard choices. Instead of trying to develop every component internally, EO Technics focused on system integration and customization. They would import laser sources but develop their own beam delivery systems. They would use foreign control software but create custom interfaces for Korean fab requirements.

Then came the Asian Financial Crisis of 1997-1998. The Korean won collapsed, losing half its value against the dollar. Foreign equipment became prohibitively expensive overnight. Companies that had been hesitant about local suppliers suddenly had no choice. It was a brutal period - many of EO Technics' competitors went bankrupt - but for those who survived, it was transformative. Samsung and other chaebols, burned by their dependence on foreign suppliers who demanded payment in suddenly-expensive dollars, made strategic decisions to support local equipment makers. EO Technics was perfectly positioned to benefit.

IV. The IPO & Going Public (2000)

EO Technics got listed on Korea Exchange (KRX) on Aug 24, 2000. Its market capitalization at IPO was $19.9M. The timing seemed either brilliant or insane - the company went public at the absolute peak of the dot-com bubble, when investors were throwing money at anything technology-related.

The decision to go public wasn't driven by founder liquidity desires or employee option exercises. This was about credibility and capital. In the semiconductor equipment business, customers needed to know you'd be around in five years to service the equipment you sold today. Being a public company, with audited financials and regulatory oversight, provided that assurance.

The IPO raised capital that would prove critical for the next phase of growth. But perhaps more importantly, it forced professionalization. Public company reporting requirements meant better financial controls, clearer strategic planning, and more disciplined R&D spending. These weren't constraints - they were competitive advantages in an industry where customers valued predictability almost as much as performance.

Early public market reception was mixed. Korean retail investors, caught up in dot-com fever, initially bid up the stock. But when the bubble burst in 2001, reality set in. EO Technics wasn't a software company with 90% gross margins. It was a hardware manufacturer in a cyclical industry, competing with giants. The stock price reflected this sobering realization, trading below IPO price for much of 2001 and 2002.

V. The Semiconductor Partnership Era (2000s)

The 2000s marked EO Technics' transformation from vendor to partner. Received the Gold Medal for SDC Innovation Excellent Supplier - recognition that meant more than any financial metric. The company also Received the Patent Management Excellence Award [Commissioner of the Korean Intellectual Property Office], signaling its evolution from imitator to innovator.

International expansion accelerated during this period. The company established a presence in key semiconductor manufacturing hubs across Asia. The China subsidiary, established in 2003, proved particularly prescient as China began its massive investment in semiconductor capacity.

The real breakthrough came in 2005 when EO Technics was selected as a member of the Consortium of Semiconductor Advanced Research. This wasn't just membership in another industry group - it was admission to the inner circle where next-generation semiconductor technologies were being developed.

Samsung Electro-Mechanics awarded a contribution award to EO Technics for its role as the chair company of the council, which has been active in promoting cooperative relations and enhancing competitiveness for 15 years. This relationship went far beyond typical customer-supplier dynamics.

The pivot from just marking to comprehensive laser processing solutions was driven by customer needs. As semiconductors became more complex, simple marking wasn't enough. Customers needed drilling for via holes, cutting for singulation, trimming for precision adjustments. Each capability required massive R&D investment, but also opened new revenue streams.

VI. The Private Equity Inflection Point (2010)

Its latest funding round was a PE round on Jun 07, 2010 for an undisclosed amount. EO Technics has 2 institutional investors including The Carlyle Group and SL Investment. For a public company to take private equity investment was unusual, but the logic was compelling.

Carlyle brought more than capital. They brought connections to global semiconductor companies, experience in operational improvement, and credibility with international customers who might have hesitated to work with a purely Korean company. The partnership represented a new phase of ambition - EO Technics wasn't content being a regional player.

The PE investment accelerated product development cycles. Instead of incremental improvements, EO Technics could now invest in platform technologies that might take years to pay off. They could afford to fail, learn, and try again - a luxury in the semiconductor equipment business where one bad product generation could destroy customer relationships built over decades.

VII. The Display & PCB Diversification (2010s)

The 2010s brought a critical strategic insight: the technologies developed for semiconductors had applications far beyond silicon wafers. It also provides display products, such as LCD markers, align key markers, OLED/TFT/CF trimmers, metal sheet cutters. PCB equipment for drilling, marking, and cutting applications.

It was selected by Forbes in its '220 best under a billion' list in 2015. This recognition came as the company was hitting its stride in diversification. The smartphone boom created unprecedented demand for advanced displays and complex PCBs. Every iPhone, every Samsung Galaxy needed precision laser processing.

The display market offered different dynamics than semiconductors. Product cycles were shorter, allowing faster iteration. Margins were sometimes better because competition was less intense. And critically, success in displays created a natural hedge against semiconductor industry cyclicality.

VIII. The Samsung Localization Partnership

The geopolitical context of the late 2010s and early 2020s fundamentally changed EO Technics' strategic importance. As trade tensions escalated and supply chain vulnerabilities became apparent, Korea's push for technological sovereignty intensified.

As part of its localization agenda, Samsung has been working closely with domestic companies and industry partners like EO Technics, which produces high-performance laser equipment used in the manufacture of DRAM chips... "EO Technics employees are proud of being able to develop laser equipment after eight years of research and development activities with Samsung Electronics," EO Technics CEO Sung Kyu-dong told Korea Times.

Eight years of joint development - that's the reality of semiconductor equipment innovation. This wasn't a vendor relationship where Samsung specified requirements and EO Technics delivered. This was co-creation, with Samsung's process engineers and EO Technics' equipment designers working side by side.

The partnership transformed both companies. Samsung gained a reliable domestic supplier for critical equipment, reducing dependence on Japanese and American companies that could be affected by trade restrictions. EO Technics gained insights into next-generation semiconductor processes years before they went into production, allowing them to develop equipment proactively rather than reactively.

IX. Modern Era: AI Boom & Advanced Semiconductors (2020-Present)

The COVID-19 pandemic initially seemed like a disaster. Fabs shut down, equipment orders were cancelled, and the entire semiconductor industry braced for collapse. Instead, the opposite happened. Digital transformation accelerated by years, creating unprecedented demand for semiconductors. The shortage that followed made everyone - governments, companies, consumers - acutely aware of how dependent modern life had become on these tiny pieces of silicon.

As of 10-Sep-2025 the stock price of EO Technics is $152.60. The current market capitalization of EO Technics is $1.85B. The company's market cap has grown from that initial $19.9M IPO valuation to nearly $2 billion, representing almost 100x growth over 25 years.

The AI revolution has created new demands on semiconductor manufacturing. Advanced packaging technologies like 3D stacking and chiplet architectures require precision that pushes laser processing to its limits. Leading companies in the market include DISCO, ASMPT, EO Technics, Wuhan Dr Laser Technology, Delphi Laser, Synova, and Han's Laser Techno - EO Technics now mentioned alongside global giants as a market leader.

Current financial performance reflects this strategic position. As of 30-Jun-2025, EO Technics has a trailing 12-month revenue of $252M. While specific growth rates aren't disclosed in recent quarters, the company's inclusion in major industry analyses and partnerships with leading semiconductor manufacturers indicates continued strong performance.

The product portfolio has evolved far beyond those early marking systems. RCF is a special fiber laser that has a center beam and a ring beam. It reduces the spatter with a laser beam from dual-core. Each fiber has maximum 4kW output from center beam and ring beam at the same time and 80% more effective than a general fiber laser for reducing spatter. This kind of innovation - solving specific manufacturing challenges with novel approaches - exemplifies EO Technics' evolution from equipment supplier to technology partner.

X. Playbook: Business & Strategic Lessons

The EO Technics story offers several powerful lessons for building critical technology companies:

The power of being a critical supplier to national champions: EO Technics didn't try to compete globally from day one. They focused on becoming indispensable to Samsung and other Korean companies first. This provided steady revenue, deep learning opportunities, and credibility that eventually enabled global expansion.

Building deep R&D partnerships vs. transactional relationships: That eight-year development program with Samsung wasn't unusual - it was the norm. Real innovation in semiconductor equipment requires patient collaboration, where both parties invest time, money, and expertise with uncertain returns.

Navigating the public-private hybrid model: Being a public company with private equity backing created unique advantages. Public listing provided credibility and access to capital markets. PE investment brought operational expertise and global connections. Together, they enabled growth that neither alone could have achieved.

The importance of localization in strategic industries: As geopolitics increasingly shapes technology markets, being a domestic supplier in strategic industries becomes a massive competitive advantage. EO Technics benefited from Korea's push for supply chain independence in ways that no amount of technical superiority alone could have achieved.

Timing market cycles: Semiconductor equipment is notoriously cyclical. EO Technics survived multiple downturns by diversifying into related markets (displays, PCBs) and maintaining strong balance sheets during good times. They invested counter-cyclically, ramping R&D during downturns when competitors were cutting back.

Diversification strategy: Every new market EO Technics entered - displays, PCBs, solar cells - leveraged core laser processing expertise while reducing dependence on any single end market. This wasn't random diversification; it was systematic expansion into adjacent opportunities.

XI. Analysis & Investment Case

Bear Case:

The concentration risk with Korean customers remains significant. While partnerships with Samsung and SK Hynix provide steady revenue, any shift in their strategies or fortunes would dramatically impact EO Technics. The company has expanded internationally, but Korea still represents the majority of revenue.

Competition from global giants intensifies daily. Applied Materials, Tokyo Electron, and ASML have resources that dwarf EO Technics. They can invest billions in R&D, acquire promising startups, and offer complete fab solutions that no single-product company can match.

The cyclicality of semiconductor equipment spending creates ongoing volatility. When chip demand drops, equipment orders can fall 50% or more within quarters. This makes financial planning difficult and stock price volatility inevitable.

Geopolitical risks in the semiconductor supply chain continue escalating. Trade restrictions, technology transfer limitations, and national security concerns could limit EO Technics' ability to serve certain markets or access critical components.

Bull Case:

EO Technics has achieved essential supplier status in Korea's semiconductor ecosystem. This isn't easily replaceable - decades of co-development, customization, and integration create switching costs that go beyond mere financial considerations.

The growth trajectory speaks for itself. From a $19.9M IPO valuation to nearly $2 billion today represents sustained value creation over 25 years. The company has survived multiple crises, adapted to technological shifts, and consistently grown market share.

Expansion opportunities in AI chip manufacturing present massive potential. As semiconductors become more complex, laser processing becomes more critical. Advanced packaging, heterogeneous integration, and 3D architectures all require capabilities that EO Technics has spent decades developing.

The growing importance of laser processing in advanced nodes creates a secular tailwind. As traditional scaling slows, manufacturers need alternative approaches to improve performance. Laser processing enables techniques that weren't possible with conventional methods.

Margin expansion potential exists as products become more sophisticated. Software, automation, and AI-enhanced processing can command premium prices while reducing manufacturing costs. The transition from equipment vendor to solution provider typically brings significant margin improvement.

XII. Epilogue & Future Outlook

Looking toward 2035, several questions will determine EO Technics' trajectory:

Can the company maintain its innovation edge as Chinese competitors emerge with government backing and cost advantages? The playbook that worked against Japanese and American competitors might not work against state-supported Chinese firms willing to operate at losses for market share.

Will EO Technics become Korea's ASML - a national champion in critical semiconductor equipment? ASML's dominance in EUV lithography shows what's possible when technical excellence combines with strategic positioning. EO Technics has elements of both, but the path from $2 billion to $200 billion market cap requires more than incremental improvement.

How will the role of specialized equipment makers evolve in the AI era? As chip designs become more application-specific and manufacturing becomes more flexible, equipment makers who can enable rapid customization might capture disproportionate value.

The lessons for building critical technology companies outside Silicon Valley are clear: leverage local advantages, build deep partnerships with anchor customers, invest patiently in R&D, and recognize that in strategic industries, being good isn't enough - you must become indispensable.

Success in 2035 would mean EO Technics equipment enabling breakthrough technologies we can't yet imagine. Just as their laser markers seemed like a niche product in 1989 but became essential to global semiconductor production, today's R&D investments might create tomorrow's critical infrastructure.

The story of EO Technics ultimately demonstrates that building world-class technology companies requires more than capital and talent. It requires patience, strategic positioning, and the ability to transform customer relationships into innovation partnerships. In an industry where yesterday's breakthrough becomes today's commodity, the only sustainable advantage is the ability to continuously evolve.

As semiconductor manufacturing pushes toward atomic-scale precision and AI drives demand for unprecedented computing power, companies like EO Technics become increasingly vital. They're the toolmakers enabling the toolmakers, the companies building the equipment that builds the future. Their success or failure doesn't just affect stock prices or market caps - it shapes the technological capabilities of entire nations and the progress of human innovation itself.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube