Soulbrain: The Invisible Giant of the AI & EV Revolution

I. The Most Important Company You've Never Heard Of

Picture the summer of 2019. Inside Samsung's sprawling semiconductor campus in Hwaseong, South Korea, engineers stared at a logistics spreadsheet with growing dread. Japan had just announced export restrictions on three chemicals critical to chipmaking. One of them, high-purity hydrogen fluoride, was the lifeblood of every wafer Samsung produced. Without it, the most advanced memory fabs on the planet would grind to a halt within weeks. Japan controlled roughly seventy percent of the global supply for this material. Stella Chemifa alone held more than sixty percent. For thirty years, this had been Japan's quiet leverage over Korea's crown jewel industry. Now, in the middle of a bitter diplomatic dispute rooted in wartime forced labor rulings, Tokyo decided to pull the lever.

The semiconductor world collectively held its breath. Samsung and SK Hynix together produce more than half of the world's memory chips. If their fabs went dark, every smartphone, server rack, and laptop on earth would feel the impact within a quarter. Global supply chains, already strained, faced the prospect of a chemical chokepoint triggering a hardware famine.

One company stepped into the breach. Its name was Soulbrain.

Within six months, Soulbrain achieved what the industry considered impossible: producing hydrogen fluoride at "twelve-nines" purity, meaning 99.9999999999 percent pure. To put that number in perspective, at twelve-nines purity, for every trillion molecules of hydrogen fluoride, only one molecule is an impurity. This is the chemical equivalent of finding a single grain of sand on an entire beach and removing it. Before 2019, this level of purity was considered a Japanese monopoly, not just commercially but technically. The prevailing wisdom was that only decades of accumulated Japanese fluorine chemistry know-how could achieve it.

Soulbrain broke that assumption in under half a year. The company doubled capacity at its Gongju plant, fast-tracked quality validation with Samsung and Hynix, and emerged not merely as an alternative supplier but as a geopolitical necessity. The Korean government hailed the achievement as a matter of national security. Industry analysts called it the most significant supply chain disruption in semiconductor history.

This is the story of how a specialty chemicals company most people have never heard of became the invisible infrastructure of the digital age. Soulbrain does not make the chips that power artificial intelligence. It does not make the batteries that drive electric vehicles. It makes the chemicals without which neither of those things can exist. It is the ultimate "pick-and-shovel" play in the modern gold rush, and its story stretches from a small Korean startup in 1986 to a holding company now positioning itself at the intersection of AI, EVs, and geopolitics.

The journey runs through four decades, a founder who bet on Korean self-sufficiency before anyone else, a geopolitical crisis that transformed a mid-tier supplier into a national champion, a strategic corporate split designed to unlock hidden value, and a series of acquisitions that reveal a management team playing a very long game. Understanding Soulbrain means understanding why the most important companies in technology are often the ones nobody talks about.

II. Foundation and The Rise of the Asian Tigers (1986-2010)

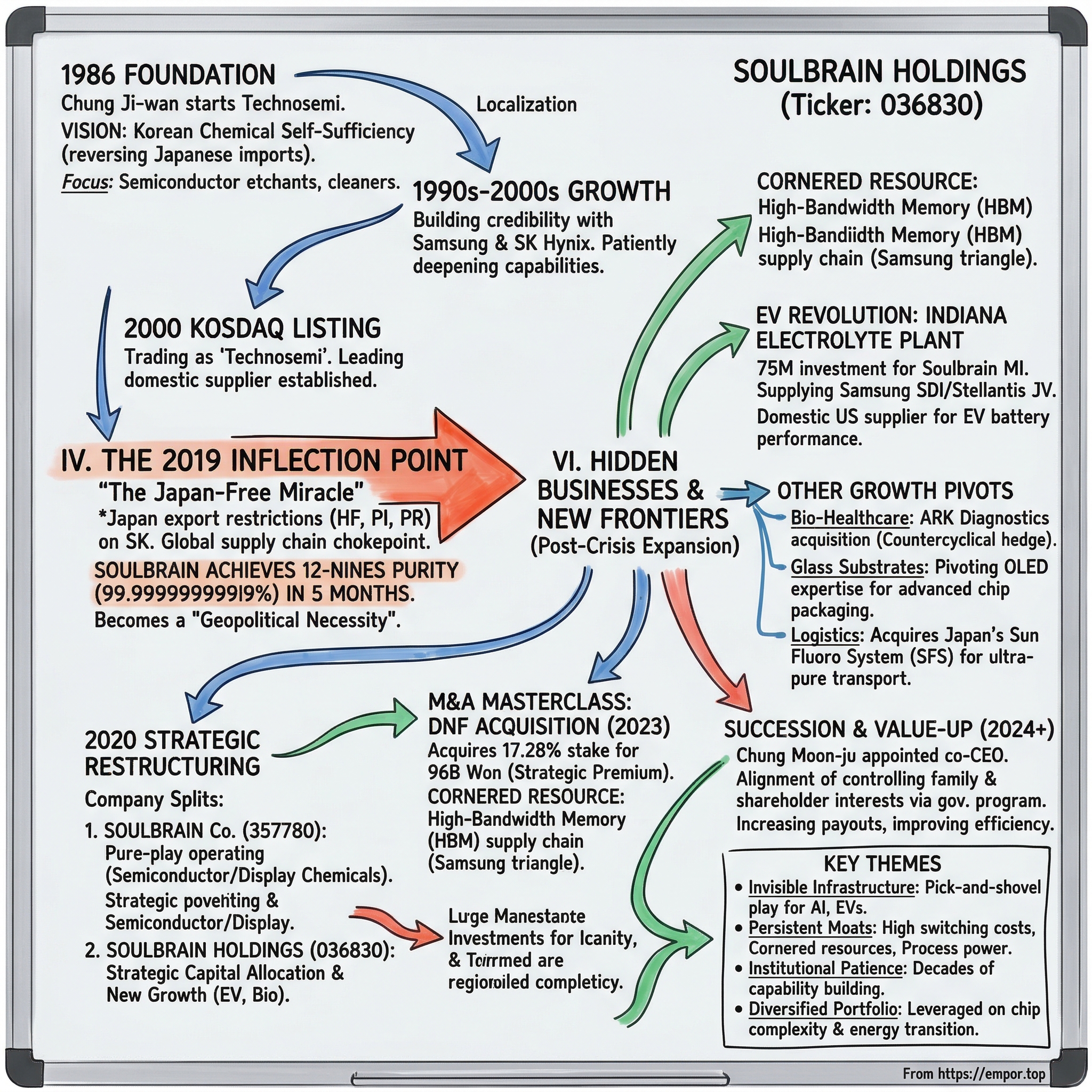

In 1986, South Korea was a nation in transformation. The country was still a decade away from joining the OECD, still shaking off the legacy of military dictatorship, and still figuring out whether its "Miracle on the Han River" economic strategy could evolve from heavy industry and shipbuilding into something more sophisticated. Samsung had entered the memory chip business just three years earlier, in 1983, with a bold and somewhat reckless bet on 64K DRAM that most industry observers expected to fail. It did not fail. By 1986, Samsung was gearing up for 256K and 1M DRAM production, and it needed chemicals. Lots of chemicals.

This was the world into which Chung Ji-wan launched Technosemi, the company that would eventually become Soulbrain. Chung was a chemist by training, and he saw something that few others in Korea were paying attention to: the country's entire semiconductor ambition rested on a foundation of imported Japanese chemicals. Every etchant, every cleaner, every high-purity solvent that Samsung and the emerging Korean chipmakers needed came from Japan. The irony was thick. Korea was building a world-class chip industry, but the most basic inputs, the chemicals that etched circuits onto silicon, came from the former colonial power. If Japan ever decided to restrict supply, Korea's semiconductor dream would evaporate overnight.

Chung's insight was not just commercial; it was patriotic. He set out to reverse-engineer Japanese semiconductor chemicals and prove they could be made domestically. This was extraordinarily difficult work. Semiconductor-grade chemicals are not like industrial chemicals. A tiny impurity, measured in parts per billion or even parts per trillion, can destroy an entire batch of wafers. The manufacturing process requires not just chemical expertise but obsessive quality control, specialized equipment, and an intimate understanding of how each chemical interacts with the specific processes used by each customer. There is no generic "semiconductor-grade hydrofluoric acid." Each formulation is tuned to a specific fab, a specific process node, a specific customer's requirements.

Through the late 1980s and 1990s, Technosemi slowly built credibility with Samsung and what would become SK Hynix. The company started with lower-purity etchants and cleaners, the less demanding applications where Korean-made chemicals could compete on cost even if they could not yet match Japanese quality at the highest end. Each successful qualification at a Samsung fab was a small victory. Each new product line was a brick in the wall of a competitive moat that would take decades to become truly formidable.

The company's strategy during this period was essentially "localization as a business model." Korea was spending billions of won importing chemicals. Technosemi offered a domestic alternative that reduced supply chain risk and import costs. The Korean government, increasingly aware of the strategic vulnerability of depending on Japanese inputs, quietly encouraged this import substitution. Samsung and Hynix, for their part, were willing to work with domestic suppliers as long as quality met specifications, because having a local chemical supplier meant shorter lead times, lower logistics costs, and, crucially, a hedge against the very scenario that would play out decades later.

By the time the company listed on KOSDAQ in 2000, riding the dot-com wave like so many Asian tech-adjacent companies, Technosemi had established itself as the leading domestic supplier of wet etchants and cleaning solutions to the Korean semiconductor industry. It was not yet a household name. It was not yet a "national champion." But it had done something profoundly important: it had proved that Korean chemistry could serve Korean chips. The relationships forged during these years, the deep technical integration with Samsung and Hynix engineers, the institutional trust built through thousands of qualification tests and millions of liters of chemical delivered without incident, would become the bedrock of everything that followed.

The first two decades of Soulbrain's existence were, in many ways, the quiet act of a much louder story. Chung Ji-wan was not building a company to flip or to grow fast. He was building a capability. The difference matters enormously. A company that grows fast can be copied. A capability that deepens over decades cannot. When the crisis came in 2019, Soulbrain had thirty-three years of accumulated knowledge, relationships, and process expertise. That is not the kind of advantage you can buy, replicate, or shortcut. It is the kind of advantage that only patience produces.

But patience, as it turned out, was about to be tested in the most dramatic fashion imaginable.

III. The 2019 Inflection Point: The "Japan-Free" Miracle

On July 4, 2019, while Americans were lighting fireworks, Japan's Ministry of Economy, Trade and Industry lit a different kind of fuse. Tokyo announced that exports of three critical semiconductor materials to South Korea would now require individual export licenses instead of the streamlined bulk licenses that had been standard for years. The three materials were high-purity hydrogen fluoride, fluorinated polyimide, and extreme ultraviolet photoresist. The diplomatic trigger was a series of South Korean Supreme Court rulings in 2018 ordering Japanese companies to compensate victims of forced labor during Japan's colonial occupation of Korea from 1910 to 1945. But the real story was about leverage. Japan was reminding South Korea, and the world, who controlled the chemical bottleneck of the semiconductor supply chain.

The impact was immediate and severe. Japanese hydrogen fluoride exports to South Korea plummeted nearly eighty-eight percent. The three targeted materials were not chosen randomly. Each sat at a critical chokepoint where Japanese companies held dominant market share. In hydrogen fluoride specifically, Stella Chemifa controlled roughly sixty-three percent of the global market, Daikin Industries another twenty-one percent, and Morita Chemical Industries about nine percent. Together, Japanese producers controlled more than ninety percent of the high-purity hydrogen fluoride used in advanced chipmaking.

To understand why this mattered so much, it helps to understand what hydrogen fluoride actually does in a semiconductor fab. Think of chip manufacturing as an enormously complex process of building up and carving away microscopic layers on a silicon wafer. Hydrogen fluoride is the primary carving tool. It selectively dissolves silicon dioxide, the insulating layer between circuit elements, with extraordinary precision. If the hydrogen fluoride is not pure enough, if it contains even a few parts per billion of metallic contaminants, those contaminants embed themselves in the circuit and destroy the chip's electrical properties. A single contaminated batch can ruin thousands of wafers worth millions of dollars.

The purity standard for advanced chipmaking is not "very pure" or "extremely pure." It is "cosmically pure." At twelve-nines, the level required for the most advanced processes, the ratio of impurity molecules to hydrogen fluoride molecules is one in a trillion. Achieving this requires not just sophisticated chemistry but obsessive control over every element of the production environment: the raw materials, the reaction vessels, the piping, the storage containers, even the air in the cleanroom. The Japanese companies had spent decades perfecting this, building on a tradition of fluorine chemistry that stretched back to Daikin's entry into fluorochemicals in 1933. The accumulated know-how was regarded as essentially unreproducible.

Soulbrain entered this crisis already producing hydrogen fluoride at five-nines purity, a good commercial grade but seven orders of magnitude away from the twelve-nines standard. In August 2019, the company launched what amounted to a wartime mobilization of its R&D and manufacturing capabilities. Engineers worked around the clock at the Gongju plant south of Seoul. The company doubled its production capacity for hydrogen fluoride. And by January 2020, roughly five months after the crisis began, Soulbrain announced that it had achieved twelve-nines purity hydrogen fluoride in commercial volumes.

This was not just a technical achievement. It was a geopolitical event. Samsung and SK Hynix, which under normal circumstances would have required twelve to twenty-four months of rigorous qualification testing before approving a new chemical supplier, fast-tracked Soulbrain's validation cycle. The urgency of the situation compressed years of process into months. This was an extraordinary concession from the chipmakers, and it revealed something crucial about the 2019 crisis: the pain of potential fab shutdowns was so severe that even the most conservative, risk-averse semiconductor manufacturers on earth were willing to bend their own rules.

The consequences of this moment rippled far beyond Soulbrain's revenue line. Before 2019, Soulbrain was a "preferred supplier," one option among several, a domestic hedge against import risk. After 2019, Soulbrain was a "geopolitical necessity," a company that had proved it could do what the entire world thought only Japan could do. The fast-tracked validation meant that Soulbrain's chemicals were now embedded in Samsung and Hynix production lines at the deepest level. Ripping them out and going back to Japanese suppliers would require yet another qualification cycle, costing time and money with no guarantee of improvement. Soulbrain had, in the space of months, transformed a crisis into the most durable competitive moat in the specialty chemicals industry.

Korea's government took note. The 2019 crisis became a galvanizing event for Korean industrial policy, prompting billions of won in government investment in domestic materials, parts, and equipment industries. Soulbrain was the poster child for this national effort. The company that Chung Ji-wan had founded with a vision of Korean chemical self-sufficiency had vindicated that vision in the most dramatic way possible, thirty-three years after it seemed like a quixotic ambition.

But Soulbrain's leadership was already thinking about the next move. The 2019 crisis had revealed not just the company's strength but also its limitations. It was still structured as a single operating entity, with its fast-growing semiconductor business, its emerging battery electrolyte business, and its various other ventures all housed under one roof. To capitalize on the post-crisis opportunity, Soulbrain needed a new corporate architecture. What followed was one of the most strategically consequential restructurings in Korean corporate history.

IV. Strategic Restructuring: The 2020 Spinoff and Capital Allocation

In the boardrooms of Korean conglomerates, the concept of "splitting up to grow faster" has a complicated history. The chaebol model, Korea's version of the Japanese keiretsu, was built on the opposite principle: keep everything together, cross-subsidize, and use the group's collective weight to dominate. But by 2020, a new logic was emerging. The most sophisticated Korean companies were recognizing that different businesses require different capital allocation strategies, different risk profiles, and different investor bases. Soulbrain's leadership decided it was time to unbundle.

The company split into two entities. Soulbrain Co., trading under ticker 357780, became the pure-play operating company focused on the cyclical semiconductor and display chemicals business. This was the cash cow, the engine that generated the steady stream of revenue from selling etchants, cleaners, and specialty chemicals to Samsung and SK Hynix fabs. Soulbrain Holdings, retaining the original KOSDAQ ticker 036830, became the strategic holding company, the entity responsible for managing the group's portfolio of investments, pursuing M&A, and incubating the next generation of growth businesses including EV battery electrolytes and bio-healthcare.

The logic was elegant. Semiconductor chemicals are a cyclical business, tied to memory chip capex cycles that swing dramatically from boom to bust. When Samsung is expanding capacity, Soulbrain Co. prints money. When the memory market slumps, as it does every few years, revenue contracts. Investors who want exposure to that cycle can buy Soulbrain Co. But the Holdings company is a different animal entirely. It is a capital allocation vehicle, more like a focused industrial holding company than a chemical supplier. Its job is to take the cash generated by its stake in Soulbrain Co. and deploy it into long-duration growth opportunities that do not fit neatly inside a cyclical operating company.

The capital allocation story became dramatically more interesting in 2025, when Holdings executed a major asset divestiture. The specifics of the transaction sent net income soaring by roughly seven hundred and fifty-seven percent year-over-year, a headline number so extreme that it requires context. This was not organic growth in any traditional sense. It was a strategic monetization event, converting a portfolio asset into cash that could be redeployed into the company's next wave of investments. Think of it less as "earnings" and more as "reloading the war chest."

The beauty of this structure is that it allows Holdings to be patient and opportunistic simultaneously. Patient, because the steady dividend income from its stake in Soulbrain Co. covers operating expenses. Opportunistic, because the cash from asset sales gives it the firepower to make bold acquisitions when the right target appears at the right price. The Holdings structure also provides a natural governance mechanism: the operating company's management can focus entirely on running fabs, managing customer relationships, and optimizing chemical production without being distracted by M&A or venture-style investments.

For investors, the key question about any holding company is whether management is a skilled capital allocator or a value-destroying empire builder. The answer, in Soulbrain's case, depends largely on how one evaluates the company's most significant acquisition to date.

V. M&A Masterclass: The DNF Acquisition and Benchmarking

In 2023, Soulbrain Holdings made a move that divided the analyst community. The company acquired a 17.28 percent stake in DNF Co. for ninety-six billion won. DNF is a Korean specialty chemicals company that produces precursors for semiconductor deposition processes, specifically the chemicals used in chemical vapor deposition and atomic layer deposition to build the microscopic layers inside chips. What made DNF strategically interesting, and what made the acquisition controversial, was its position in the emerging high-bandwidth memory supply chain.

To understand why this matters, a brief detour into the world of HBM is necessary. High-bandwidth memory is the technology that makes modern AI possible. When NVIDIA ships a GPU designed to train large language models, that GPU needs to be paired with stacks of HBM chips that can feed data to the processor fast enough to keep up. HBM is manufactured by stacking multiple DRAM dies on top of each other, connecting them with thousands of tiny vertical wires called through-silicon vias, or TSVs. Each layer requires its own set of deposition, etching, and cleaning steps. According to Applied Materials, HBM manufacturing adds approximately nineteen additional materials engineering steps beyond what conventional DRAM requires. The result is that each gigabyte of HBM consumes roughly three times the wafer capacity of standard DDR5 memory. For chemical suppliers, HBM is a bonanza: more layers means more chemistry per chip, and the chemistry itself is more demanding and therefore higher-margin.

DNF sits at a critical node in this supply chain. Its precursors are used in the deposition steps that build the thin films inside DRAM and, increasingly, inside HBM. Samsung, notably, is also a major shareholder in DNF, creating a triangle of mutual investment and strategic alignment between the chipmaker, its chemical supplier, and the precursor company that feeds the chemical supplier.

Now, the controversy. Soulbrain paid a management premium of roughly one hundred and forty-three percent over DNF's prevailing market price. On a trailing price-to-earnings basis, the acquisition implied a valuation of approximately ninety-six times earnings. On an enterprise-value-to-EBITDA basis, about twenty-four times. By any conventional valuation metric, this was expensive. Critics called it a classic case of "strategic premium" being used to justify overpayment. Defenders argued that the premium reflected the scarcity value of DNF's position: there are very few companies in the world that can produce the specific precursors needed for advanced DRAM and HBM deposition, and even fewer that are already qualified at Samsung and Hynix fabs.

The strategic rationale becomes clearer when viewed through the lens of Hamilton Helmer's "Cornered Resource" framework. A cornered resource is an asset that a company controls which competitors cannot replicate. DNF's precursor chemistry, validated and embedded in Samsung's most advanced production processes, is exactly that kind of asset. Soulbrain was not buying DNF's current earnings. It was buying a seat at the table in the most explosive growth segment of the semiconductor industry. If HBM volumes follow the trajectory that analysts project, with the market potentially reaching one hundred billion dollars by 2028, then the chemicals and precursors that enable HBM production will scale proportionally. A seventeen percent stake in one of the key precursor companies is, in this light, less an acquisition and more an insurance policy against being locked out of the AI supply chain.

The DNF deal also reveals something about Soulbrain Holdings' M&A philosophy. This was not a hostile takeover or a control acquisition. It was a minority strategic investment, the kind of move that creates optionality without requiring full integration. Holdings can deepen the relationship over time, potentially increasing its stake, or it can simply collect dividends and benefit from the appreciation of its investment as HBM volumes grow. The flexibility is the point.

Whether the price was right remains an open question that only time can answer. What is not in question is the strategic logic: in a world where AI is consuming an ever-larger share of semiconductor production, controlling the chemistry that enables that production is a position of enormous leverage. Soulbrain, through the DNF acquisition, has placed a significant bet that this leverage will only grow.

The DNF deal was not Soulbrain's only strategic bet, however. Across the Pacific, the company was making an even larger wager on a different kind of chemistry entirely.

VI. Hidden Businesses and New Frontiers

Twelve time zones west of Soulbrain's Korean headquarters, in the industrial heartland of Indiana, a different kind of factory was taking shape. Soulbrain MI, the company's American subsidiary, broke ground on a seventy-five-million-dollar electrolyte manufacturing facility in Kokomo, designed to supply the nearby Samsung SDI and Stellantis battery joint venture. This was not a tentative toe-dip into the American market. It was a full-scale commitment to becoming a domestic supplier of one of the most critical components in electric vehicle batteries.

Battery electrolytes are to EVs what hydrogen fluoride is to semiconductors: invisible, essential, and surprisingly difficult to get right. An electrolyte is the liquid medium through which lithium ions travel between a battery's anode and cathode. Think of it as the highway system inside a battery. The quality of the electrolyte, its specific formulation of organic solvents, lithium salts, and proprietary additives, directly determines the battery's performance, lifespan, safety, and charging speed. A poorly formulated electrolyte can cause a battery to degrade prematurely, charge slowly, or, in the worst case, catch fire. Getting the chemistry right requires the same kind of obsessive quality control and deep customer integration that characterizes semiconductor chemicals, and Soulbrain has decades of experience doing exactly that.

The global battery electrolyte market was valued at roughly fourteen to fifteen billion dollars in 2025 and is projected to reach twenty-six to twenty-eight billion by 2030, growing at a compound annual rate of about thirteen percent. The market is currently dominated by Chinese producers, particularly Shenzhen Capchem Technology and Guangzhou Tinci Materials, which benefit from scale and proximity to China's enormous battery manufacturing base. Soulbrain's bet is that as EV battery production shifts to the United States, driven by Inflation Reduction Act subsidies and geopolitical pressure to build non-Chinese supply chains, American-based electrolyte production will command a premium. The Kokomo facility, with its IATF 16949 automotive certification and its rapid prototyping capability, delivering custom electrolyte samples in seventy-two hours, is designed to be the supplier of choice for the emerging American battery ecosystem.

But electrolytes are only one piece of the Holdings portfolio. The company's segment breakdown reveals a diversification strategy that is more ambitious than most investors realize.

The semiconductor chemicals business, housed primarily in Soulbrain Co., represents roughly eighty percent of consolidated revenue. This is the core engine: high-margin etchants and cleaning solutions for 3D NAND flash and, increasingly, HBM production. The growth trajectory here is tied directly to the AI infrastructure buildout. As chipmakers add more layers to their 3D NAND stacks and more dies to their HBM stacks, chemical consumption per wafer rises proportionally. Soulbrain Co. is essentially a leveraged bet on the physical complexity of modern chips, and that complexity only moves in one direction.

The bio-healthcare segment, representing about twenty-one percent of holdings revenue, is the most surprising piece of the portfolio. Soulbrain acquired ARK Diagnostics, an American company specializing in clinical diagnostic reagents, as a deliberate diversification play. The logic was countercyclical hedging: when the semiconductor cycle turns down, healthcare diagnostics, which are driven by hospital volumes and regulatory requirements rather than chip capex cycles, provide a stable revenue floor. It is an unusual combination, a specialty chemicals company and a diagnostic reagent business, but the underlying competency is the same: formulating and manufacturing highly precise chemical products under strict quality controls.

The display materials business is undergoing a strategic pivot that may prove to be the most forward-looking move in the entire portfolio. Soulbrain has historically supplied thin glass and etching solutions for OLED panel manufacturing, primarily to Samsung Display. But the company is now redirecting this expertise toward glass substrates for semiconductor packaging, a technology that could fundamentally reshape how chips are assembled.

Glass substrates replace the traditional organic, resin-based substrates onto which chips are mounted and interconnected. The advantages are substantial: glass maintains its shape across temperature ranges far better than organic materials, which tend to warp; glass has superior electrical properties that minimize signal delay; and glass's thermal expansion rate closely matches silicon's, reducing stress at the interface where chip meets substrate. Intel announced plans for glass substrates in September 2023. Absolics, an SKC affiliate, received seventy-five million dollars in CHIPS Act funding for a glass substrate facility in Georgia. Samsung Electro-Mechanics and Soulbrain are targeting mass production by 2027. For Soulbrain, the beauty of this pivot is that the chemistry is transferable. The etching solutions, polishing liquids, and deposition materials used for display thin glass are directly applicable to processing glass substrates for chip packaging. It is a classic case of redeploying existing capabilities into a higher-growth adjacent market.

Finally, there is the 2025 acquisition of Sun Fluoro System, a Japanese company specializing in the logistics and transport of ultra-pure fluorine chemicals. This might seem like a minor deal, but it is strategically significant. Transporting chemicals at twelve-nines purity is itself a specialized capability. The chemicals can be contaminated by the containers they are shipped in, the trucks they ride in, or the pipes they flow through. By acquiring SFS, Soulbrain secured control over a critical piece of the value chain that most competitors outsource: the ability to move hazardous, ultra-pure chemicals from factory to fab without compromising their quality. In Helmer's framework, this is "Process Power" made tangible.

The common thread across all of these businesses is a single competency: the ability to formulate, manufacture, and deliver ultra-precise chemical products to the most demanding customers on earth. Whether the end market is semiconductors, batteries, diagnostics, or display panels, the underlying skill set is the same. Soulbrain's diversification is not random conglomeration. It is the systematic exploitation of a core capability across multiple high-growth end markets.

The question, of course, is whether the leadership team steering this portfolio has the skill and judgment to allocate capital wisely across so many opportunities. That question leads directly to the most consequential corporate governance story in Soulbrain's history.

VII. Management and Succession: The Value-Up Era

Chung Ji-wan is not a figure who shows up in global business magazines. He does not keynote at Davos or tweet about innovation. He is a chemist who built a chemical company, and he has run it for four decades with the kind of quiet, methodical consistency that tends to produce enormous wealth rather than enormous fame. As of the most recent disclosures, Chung and his family control approximately fifty-five to seventy-five percent of Soulbrain Holdings' outstanding shares, a concentration of ownership that is remarkable even by Korean standards.

In March 2025, the succession plan that industry watchers had been anticipating for years finally materialized. Chung's daughter, Chung Moon-ju, was appointed co-CEO of Soulbrain Holdings. The appointment signaled two things simultaneously. First, that the founding family intends to maintain control across generations, a common pattern in Korean business dynasties. Second, and more subtly, that the succession is being structured as a gradual transition rather than an abrupt handoff, with the founder remaining active while the next generation takes on increasing operational responsibility.

The timing of the succession announcement coincided with a broader shift in Korean corporate governance that is worth understanding in detail, because it has profound implications for Soulbrain's shareholder value trajectory. In 2024, South Korea launched its "Corporate Value-up Program," a government-backed initiative modeled loosely on Japan's successful push to close the "Japan discount" in its equity markets. The program encourages Korean companies to improve capital efficiency, increase shareholder returns, and close the persistent valuation gap between Korean equities and their global peers.

For Soulbrain's controlling family, the Value-up Program creates a powerful alignment of interests with minority shareholders that did not previously exist. Here is why. Korea's inheritance tax rate is among the highest in the world, reaching fifty percent on large estates with an additional surcharge for controlling shareholders, effectively pushing the marginal rate above sixty percent. When the patriarch of a Korean business dynasty passes on control to the next generation, the tax bill is calculated based on the company's stock price. For decades, this created a perverse incentive: Korean controlling families actually benefited from keeping their stock prices low, because a lower stock price meant a lower inheritance tax bill.

The Value-up Program is designed to break this cycle. By encouraging companies to pay higher dividends, pursue share buybacks, and improve transparency, the program gives controlling families a path to generating enough cash flow to pay the inheritance tax without selling down their controlling stake. The calculus flips: instead of suppressing the stock price, the family is now incentivized to increase it, because higher dividends generate the cash needed to cover the tax obligation. For Soulbrain, with its massive family ownership stake, this alignment is not trivial. Management has signaled a target payout ratio of thirty percent or higher, a meaningful increase from historical levels.

The governance picture is not without risk. Concentrated family ownership always carries the possibility of related-party transactions, empire-building acquisitions that serve the family's interests rather than shareholders', or succession disputes that distract management from operations. These risks are worth monitoring. But the structural incentive alignment created by the Value-up Program, combined with the demonstrated track record of disciplined capital allocation over the past decade, provides a reasonable basis for cautious optimism.

The management story at Soulbrain is ultimately a story about institutional patience. Chung Ji-wan spent thirty-three years building a company that was ready for a crisis that no one predicted. He then spent the years after that crisis restructuring the company to capture the next generation of opportunities. Now, with his daughter at the helm and a government program aligning the family's financial interests with those of outside shareholders, the question is whether the next generation of leadership can deploy the accumulated capital and credibility as effectively as the founder built them.

VIII. The Strategy Framework: Seven Powers and Five Forces

To evaluate whether Soulbrain's competitive position is durable or fragile, it is useful to apply two complementary frameworks: Hamilton Helmer's Seven Powers, which identifies the sources of persistent competitive advantage, and Michael Porter's Five Forces, which maps the structural attractiveness of the industry.

Starting with Helmer. Of the seven sources of competitive power, three stand out as exceptionally strong for Soulbrain.

Switching costs are the company's most powerful moat. Qualifying a new chemical supplier at a semiconductor fab is not like switching from one brand of office paper to another. It is a process that typically takes twelve to twenty-four months, involves running thousands of test wafers, measuring yield impacts at the parts-per-billion level, and subjecting the new supplier's chemicals to the full spectrum of reliability testing. The cost of a failed qualification, in terms of wasted wafers, delayed production, and potential yield degradation, can run into tens of millions of dollars. Meanwhile, the cost of the chemicals themselves is a tiny fraction of total wafer fabrication cost, typically two to five percent. This creates a deeply asymmetric dynamic: the downside risk of switching suppliers is enormous, while the potential cost savings are minimal. Once Soulbrain is qualified at a Samsung or Hynix fab, the rational decision for the chipmaker is to never change suppliers unless forced to.

Cornered resource is the second major source of power. Soulbrain is the only Korean domestic producer capable of supplying roughly two-thirds of the country's semiconductor-grade hydrogen fluoride needs at twelve-nines purity. This capability, validated under crisis conditions in 2019 and subsequently embedded in production lines, is not something a competitor can replicate by writing a check. It requires decades of accumulated process knowledge, proprietary purification techniques, and institutional relationships with the chipmakers. The DNF investment adds another dimension to this cornered resource: access to the precursor chemistry that feeds into HBM and advanced DRAM production.

Process power is the third pillar. The tacit knowledge required to handle fluorine compounds at extreme purities is extraordinarily difficult to codify or transfer. Fluorine is among the most reactive and corrosive elements on the periodic table. Working with it at twelve-nines purity means controlling not just the chemistry but every material surface, piping joint, and container that the chemical contacts. Soulbrain's journey from five-nines to twelve-nines in five months demonstrated a depth of process expertise that represents decades of learning compressed into a single demonstration. The SFS acquisition further strengthened this pillar by securing control over the logistics of transporting these dangerous, ultra-pure materials.

Scale economies are moderate. Soulbrain dominates the Korean domestic market but remains mid-sized globally compared to Entegris, which commands a market capitalization north of sixteen billion dollars, or the Japanese chemical giants. Network effects and branding power are weak, as is typical for B2B chemical suppliers. Counter-positioning shows moderate strength: Soulbrain's geographic proximity to Korean fabs, combined with its post-2019 "national champion" status, creates a position that Japanese competitors are reluctant and Western competitors are unable to easily replicate.

Turning to Porter's Five Forces, the structural picture is favorable.

The threat of new entrants is extremely low. The barriers to entry in semiconductor-grade chemicals are formidable: the capital expenditure required to build ultra-pure chemical production facilities, the twelve-to-twenty-four-month qualification timelines at each customer fab, the regulatory and environmental compliance burden for handling hazardous materials, and the decades of accumulated process know-how all combine to make new entry essentially impractical. The semiconductor chemicals market is projected to reach roughly twenty-nine billion dollars by 2030, but the path to capturing any meaningful share of that market requires investment measured in decades, not years.

Supplier power is moderate. The raw material inputs for Soulbrain's products, such as fluorspar for hydrogen fluoride and lithium salts for electrolytes, are largely commoditized and available from multiple sources. However, certain specialized inputs, particularly the perfluoroalkoxy materials used in chemical delivery systems, are produced by a very small number of suppliers, creating potential pinch points.

Buyer power is the most nuanced force. Samsung and SK Hynix are enormous customers with significant purchasing leverage. They can and do dual-source to maintain competitive tension among suppliers. However, the 2019 crisis fundamentally altered the buyer-supplier dynamic. Samsung and Hynix learned, painfully, that their ability to pressure suppliers on price means nothing if those suppliers are the only ones who can keep the fabs running. The cost of chemicals is so small relative to total wafer cost that buyers are far more sensitive to quality and reliability than to price. This limits the practical exercise of buyer power.

The threat of substitutes is very low. Wet etching chemistry, the core of Soulbrain's semiconductor business, has no viable substitute for many critical process steps. While dry etching using plasma has expanded its role, wet chemistry remains essential for cleaning, oxide removal, and numerous etching applications. There is no fundamentally different technology on the horizon that could replace high-purity chemical processing.

Competitive rivalry is moderate. The semiconductor chemicals market is consolidated, with a handful of major players competing in each chemical category. Competition is based primarily on quality, reliability, and co-development capability rather than on price. The industry trend toward consolidation, exemplified by Entegris's six-and-a-half-billion-dollar acquisition of CMC Materials, suggests that rivalry may become less intense over time as the market concentrates further.

Taken together, the Seven Powers and Five Forces analyses paint a picture of a company with durable competitive advantages operating in a structurally attractive industry. The moats are real, deep, and unlikely to be eroded by competition or disruption in the foreseeable future.

IX. Bear vs. Bull Case Analysis

Every investment thesis has two sides, and the most valuable exercise is to steelman both before drawing conclusions. Soulbrain's story is compelling, but compelling stories do not always translate into good investments, and it is important to look squarely at the risks.

The bear case begins with customer concentration. Approximately eighty percent of Soulbrain's core semiconductor chemical revenue comes from Samsung and SK Hynix. This is not diversification; it is dependency. If Samsung decided to aggressively dual-source or bring chemical production in-house, Soulbrain's revenue and margin structure would come under severe pressure. The counter-argument, that switching costs make this unlikely, is valid but not absolute. Samsung is one of the most vertically integrated companies on earth. It makes its own chips, its own displays, its own memory. The assumption that it would never choose to make its own chemicals is an assumption, not a certainty.

The EV bet introduces a different kind of risk. Soulbrain MI's investments in Indiana and Michigan are predicated on a specific vision of the American EV future: one in which domestic battery production scales rapidly, driven by IRA subsidies and automaker commitments. If the US EV transition stalls, whether due to policy changes, consumer resistance, or a shift toward hybrid vehicles, these investments could become stranded assets. The electrolyte manufacturing facility in Kokomo is designed to serve the Samsung SDI-Stellantis joint venture. If that joint venture underperforms, Soulbrain's electrolyte plant underperforms with it. The company is, in effect, making a concentrated bet on a single customer relationship in a nascent market with significant political and consumer uncertainty.

There is also the holding company discount to consider. Holding companies in Korea historically trade at significant discounts to the sum of their parts, because investors worry about opaque capital allocation, related-party transactions, and governance risk. The Value-up Program may narrow this discount over time, but structural market skepticism about Korean holding companies is not easily overcome.

Finally, there is currency and geopolitical risk. Soulbrain's revenue is predominantly in Korean won, but its costs for US-based operations are in dollars, and its growth is tied to geopolitical dynamics between Japan, Korea, China, and the United States. Any escalation in trade restrictions, particularly those affecting semiconductor materials or EV supply chains, could create both opportunities and risks that are difficult to predict.

The bull case is equally forceful. The AI tailwinds for Soulbrain's semiconductor chemicals business are substantial and structural. HBM production is projected to be one of the fastest-growing segments in the entire semiconductor industry, with Bank of America forecasting a market reaching fifty-four billion dollars in 2026. Each generation of HBM adds more layers, and each layer requires more chemical processing steps. The HBM market could reach one hundred billion dollars by 2028 on the most optimistic projections. Soulbrain's position as the primary domestic supplier of etchants and cleaning solutions to the world's two largest memory manufacturers places it directly in the path of this growth.

The M&A war chest provides optionality. With the 2025 divestiture generating a massive cash influx, Holdings has the firepower to execute additional "DNF-style" strategic acquisitions. In a consolidating industry, the ability to move quickly and decisively on acquisition targets is itself a competitive advantage. Management's track record, while limited in sample size, suggests a disciplined approach to strategic investment rather than indiscriminate empire-building.

The glass substrate opportunity, while still early, represents a potential step-function expansion of Soulbrain's addressable market. If glass substrates gain adoption in advanced chip packaging as expected by 2027 and beyond, Soulbrain's existing expertise in glass chemistry positions it to capture a meaningful share of an entirely new market segment without requiring fundamentally new capabilities.

And the Value-up alignment, while intangible, is structurally significant. When a controlling family's financial interests shift from suppressing stock price to maximizing it, the behavioral change can be profound. Higher dividends, improved transparency, and a willingness to return capital to shareholders could catalyze a re-rating of the stock over time.

For investors tracking Soulbrain's ongoing performance, three KPIs deserve particular attention. First, semiconductor chemical revenue growth relative to the broader memory capex cycle, which reveals whether Soulbrain is gaining share or merely riding the cycle. Second, the holding company's dividend payout ratio, which serves as a proxy for governance quality and Value-up commitment. Third, the ramp trajectory of US electrolyte revenue, which will indicate whether the EV bet is paying off or stalling.

X. Epilogue and Playbook Lessons

The story of Soulbrain distills into three lessons that extend well beyond a single Korean chemical company.

The first is that crisis is the most powerful catalyst for competitive advantage, but only for companies that have spent decades preparing for it. When Japan restricted hydrogen fluoride exports in July 2019, Soulbrain did not start from zero. It started from thirty-three years of accumulated chemistry expertise, customer relationships, and manufacturing infrastructure. The crisis did not create Soulbrain's capability; it revealed it. The analogy to every "overnight success" story in business history is exact: the overnight part is visible to outsiders, but the decades of quiet preparation are not. Companies that want to be positioned for their own version of the 2019 moment need to be investing in capabilities long before those capabilities are needed.

The second lesson is that in high-technology industries, the most durable competitive positions often belong to the most boring companies. The world's attention focuses on the chipmakers, the AI companies, the electric vehicle brands. These are the glamorous players. But the companies that supply the chemicals, the gases, the materials without which none of the glamorous players can function often enjoy superior economics. Their products are a tiny fraction of their customers' costs, making them price-insensitive. Their qualification processes create switching costs that last for years. Their technical requirements create barriers to entry that are measured in decades of accumulated knowledge. Soulbrain is a perfect example of this dynamic: a company that makes chemicals nobody talks about for an industry everybody talks about, and profits handsomely from the asymmetry.

The third lesson is about strategic patience and the architecture of corporate structure. Soulbrain's 2020 split into Holdings and Co. was not a financial engineering trick. It was a structural decision designed to let different businesses operate with different time horizons. The semiconductor chemicals business runs on one clock, driven by memory capex cycles. The M&A and incubation business runs on a different clock, driven by long-duration strategic opportunities. Putting both clocks inside the same corporate entity creates tension and sub-optimal capital allocation. Separating them allows each to operate according to its natural rhythm.

Chung Ji-wan founded Technosemi in 1986 with a chemist's conviction that Korea should not depend on Japan for the chemicals that made its technology dreams possible. Nearly four decades later, that conviction has been vindicated beyond anything he could have imagined. His company does not design processors. It does not build data centers. It does not manufacture the smartphones and servers that define modern life. But without the chemicals it produces, measured in parts per trillion and delivered under conditions of extraordinary precision, none of those things would exist.

Soulbrain is the invisible infrastructure of the digital age. It always has been. The difference now is that after 2019, the world knows it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube