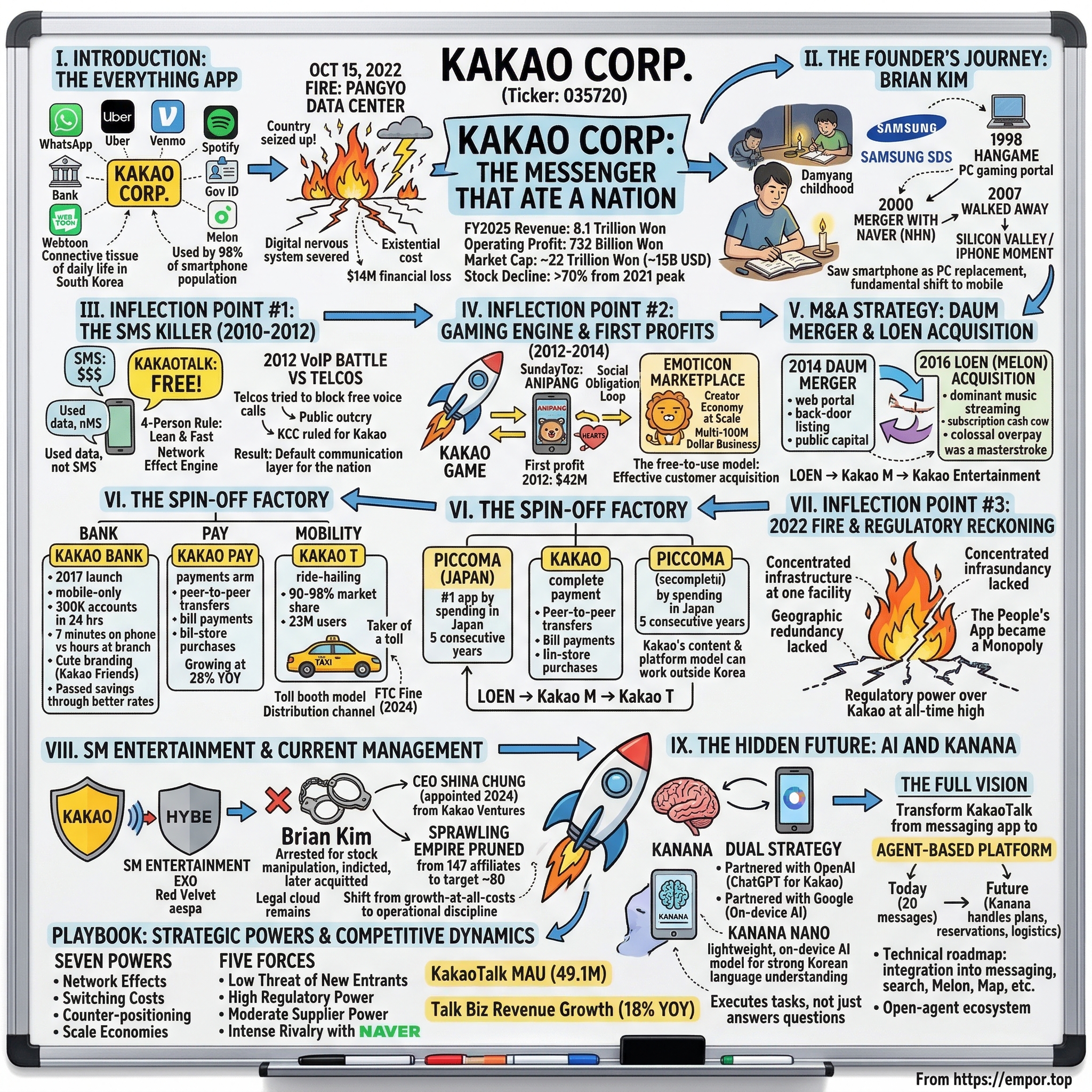

Kakao Corp: The Messenger That Ate a Nation

I. Introduction: The "Everything" App

Picture this thought experiment: take WhatsApp, Uber, Venmo, Spotify, a retail bank, a government ID system, and a webtoon publisher, and collapse them into a single app used by virtually every person in a country of 52 million. That is not a hypothetical. That is Kakao.

In South Korea, KakaoTalk is not merely a messaging app. It is the connective tissue of daily life. You wake up and check your group chats on KakaoTalk. You hail a taxi through Kakao T. You pay for your morning coffee with Kakao Pay. You check your bank balance on KakaoBank. You read webtoons on Kakao Webtoon. You listen to music on Melon. You verify your identity for government services with Kakao Certificate. By the time you go to bed, you have interacted with Kakao's ecosystem a dozen times without thinking about it. The penetration rate hovers around 98 percent of the smartphone-owning population. To put that in perspective, no Western tech company comes close to that level of saturation in a single market. Not Apple in the United States. Not Google in Europe. Not even WeChat in China, where alternatives like Alipay maintain serious competitive footing.

The scale of this dependency became terrifyingly apparent on October 15, 2022, when a fire at a data center in Pangyo knocked out Kakao's services for the better part of a day. The entire country seized up. People could not pay for groceries. They could not call taxis. They could not log in to government portals. Businesses lost the ability to communicate with employees and customers. For roughly eleven hours, South Korea experienced what it would feel like to have its digital nervous system severed. The estimated direct financial loss to Kakao was a modest 20 billion won, roughly 14 million dollars. But the real cost was existential: it forced an entire nation to confront the question of whether a private company should have this much power over public life.

Kakao Corp, listed on the Korea Exchange under ticker 035720, reported record consolidated revenue of approximately 8.1 trillion won in fiscal year 2025, with operating profit of 732 billion won, its highest operating margin in four years. The company commands a market capitalization of roughly 22 trillion won, around 15 billion dollars. It operates through more than 90 subsidiaries spanning messaging, fintech, mobility, entertainment, gaming, music streaming, and artificial intelligence. At its peak in June 2021, the stock traded near 173,000 won per share. As of mid-March 2026, it sits around 50,600 won, a decline of more than 70 percent from those highs, reflecting a cocktail of regulatory pressure, governance concerns, and the legal troubles of its founder.

This is the story of how a free SMS replacement built by four people in 2010 metastasized into the closest thing to a national operating system that any democracy has ever produced. It is the story of Brian Kim, the poverty-born son of a pen factory worker who built the number one search engine in Korea, walked away from it, moved to Silicon Valley, saw the iPhone, came back, and did it all over again with mobile. It is a story of breathtaking ambition, brilliant platform strategy, and the growing tension between private innovation and public accountability. And it is the story of a company that now stands at its most consequential crossroads: can Kakao evolve from a messaging app into an AI-powered personal agent, or will the regulatory reckoning and the Korea Discount trap it as a utility forever?

To understand where Kakao is going, we need to start with where Brian Kim came from.

II. The Founder's Journey: Brian Kim and the "Empty Chair"

Kim Beom-soo, known internationally as Brian Kim, was born on March 8, 1966, in Damyang County, a rural area in South Korea's Jeolla Province. His childhood was defined by deprivation. He was the third of five children. His father worked in a pen factory. His mother, who had only a grade-school education, worked as a hotel maid. The family eventually moved to Seoul, where Brian was raised largely by his grandmother in a cramped one-bedroom apartment. Money was so tight that he frequently skipped meals. He funded his education through private tutoring, the hustle of a kid who understood that the only path out of poverty ran through a classroom.

He made it to Seoul National University, Korea's most prestigious institution, the Harvard and MIT of the country rolled into one. He earned both a bachelor's and a master's degree in engineering. For a kid from Damyang, this was roughly equivalent to winning the lottery, except it was earned through sheer force of will. His first professional role was at Samsung SDS, Samsung's IT services arm, where he worked as a developer on online communication services. This was the mid-1990s, and the internet was beginning to stir in Korea. Samsung SDS gave Brian his first exposure to the mechanics of building digital platforms at scale, and it planted a seed: the internet was going to change everything.

But Brian Kim was not the type to stay inside a chaebol forever. In 1998, with 184,000 dollars scraped together from friends and family, he founded Hangame, South Korea's first online gaming portal. The timing was impeccable. Korea was in the grips of the Asian Financial Crisis, but it was also in the early stages of a broadband revolution that would make it the most connected country on earth. Hangame rode that wave. The portal attracted millions of users with free casual games and a social community model that was years ahead of its Western counterparts.

In 2000, Hangame merged with Naver, the web portal founded by Lee Hae-jin. The combined entity, NHN Corporation, became the undisputed champion of Korea's internet. Naver was already on its way to becoming the "Google of Korea," and with Hangame's gaming traffic bolted on, NHN had both the search dominance and the engagement machine. Brian served as co-CEO alongside Lee Hae-jin. He had effectively co-built the most powerful internet company in the country by the time he was 34.

And then he walked away.

In 2007, Brian Kim departed NHN. The official line was differences with Lee Hae-jin, but people who knew him said something more revealing: he was bored. He had conquered the PC internet. Search was solved. Gaming was humming. The machine was running. Brian Kim was not a manager. He was a builder. And there was nothing left to build at NHN.

He moved his family to Silicon Valley. He had already been spending time there, and in December 2006, he had founded IWILAB, a startup incubator for Korean entrepreneurs based in Mountain View, California. The idea was to bridge the gap between Korean technical talent and the Silicon Valley ecosystem. But IWILAB became something far more important than an incubator. It became the laboratory where Brian Kim's next act was born.

The year was 2007, and Steve Jobs had just unveiled the iPhone. Brian watched the launch and had the kind of insight that separates good entrepreneurs from transformational ones. He did not see a better phone. He saw the death of the PC era. The smartphone was not an accessory to the desktop. It was the replacement. Everything that had been built for the web, every business model, every user behavior, every assumption about how people interacted with the internet, was about to be rewritten for a four-inch screen in your pocket.

Brian returned to Korea with a conviction: the next great platform company would be built on mobile, and it would start with the most fundamental human behavior on a phone. Communication. Not search. Not gaming. Not e-commerce. Talking to people. IWILAB launched three experimental apps. Two failed and have been forgotten by history. The third was KakaoTalk. It was March 2010, and the app that would eat a nation had just been born.

But what made it explode was not technology. It was price.

III. Inflection Point #1: The SMS Killer (2010-2012)

To understand why KakaoTalk spread through South Korea like a wildfire, you need to understand what the telecom landscape looked like in 2010. Korea's three major carriers, SK Telecom, KT, and LG Uplus, were charging per SMS. Every text message cost money. For a culture that was obsessively social, that communicated in groups more than almost any other society on earth, this was a tax on human connection. Families had group texts. School friends had group texts. Work teams had group texts. Church groups, hobby clubs, military service cohorts, all of them were texting constantly, and every message dinged the bill.

KakaoTalk made it free. The app used data instead of SMS, which meant that on Korea's world-class broadband and 3G networks, messaging cost effectively nothing. It was not the first app to do this globally; WhatsApp had launched a year earlier. But KakaoTalk was built specifically for the Korean market, with Korean-language optimization, Korean social norms baked into the product, and a deep understanding of how Koreans actually communicated.

Brian Kim's philosophy was what he called the "four-person rule." Keep the team lean. Move fast. Ship quickly. The initial KakaoTalk team was exactly that: four engineers building at a pace that would make most Silicon Valley startups jealous. The leanness was not just about speed. It was about focus. Every feature decision was filtered through a single question: does this make group communication better?

And this is where KakaoTalk diverged from WhatsApp in a way that would prove strategically decisive. While WhatsApp in its early days focused primarily on one-to-one messaging, a Silicon Valley product for a Western, individualist culture, KakaoTalk leaned hard into group chats. The product was designed from the ground up for the Korean reality that social life was organized around groups. Your family group. Your college alumni group. Your work department group. Your apartment building group. This was not just a feature. It was the network effect engine. Because once your group was on KakaoTalk, you could not leave without severing yourself from the conversation. And because Korean social norms made leaving a group chat a minor act of social violence, once you were in, you were in forever.

The growth was extraordinary. KakaoTalk hit 20 million users within its first year. By March 2012, it had 42 million users in a country of 52 million. In practical terms, every Korean with a smartphone was on KakaoTalk.

The telcos saw the threat and tried to fight back. In June 2012, when Kakao launched a free VoIP calling service, the carriers went to the Korea Communications Commission and demanded it be blocked. SK Telecom argued that free voice calls would "deal a mortal blow" to their business and "hinder investment for further advancement of Korea's ICT." The carriers wanted the regulator to throttle Kakao's data usage, effectively killing the app by making it slow and unreliable.

They failed spectacularly. The public outcry was overwhelming. KakaoTalk had become the People's App, and any attempt to restrict it was perceived as an attack on the public interest. The KCC sided with Kakao, ruling that free voice calls were legal and beneficial for consumers. The telcos had lost the battle, and in losing it, they had inadvertently reinforced Kakao's most powerful narrative: that Kakao was on the side of the people, and the incumbents were on the side of extractive monopoly. This was textbook counter-positioning. The established players could not copy Kakao's model without destroying their own revenue base, and they could not block it without turning the public against them. Kakao had found the strategic sweet spot where its interests and the public interest were perfectly aligned.

By the end of 2012, KakaoTalk had not just won the messaging war in Korea. It had achieved something far more significant: it had established itself as the default communication layer for an entire nation. Every subsequent business Kakao would build, from gaming to banking to mobility, would be built on top of this layer. The messenger was not the product. The messenger was the platform. And the platform was about to figure out how to make money.

IV. Inflection Point #2: The Gaming Engine and First Profits (2012-2014)

Fifty million users and zero revenue is a wonderful and terrifying place to be. Wonderful because you have attention, the most valuable resource in the digital economy. Terrifying because attention without monetization is just an expensive hobby. By 2012, Kakao was burning cash to maintain its servers and grow its team, and the pressure to find a business model was mounting. Brian Kim, who had built Hangame into Korea's first gaming portal, knew exactly where to look.

In July 2012, Kakao launched the Kakao Game platform. The concept was deceptively simple: third-party game developers could build mobile games and distribute them through KakaoTalk's social graph. Players would log in with their Kakao accounts, see which of their friends were playing, compare scores, and send each other in-game items. Kakao would take a revenue share on all in-app purchases. It was the Facebook gaming playbook, but executed on mobile, in a market where mobile was already dominant, and with a social graph that was essentially the entire country.

The breakout hit was Anipang, a Candy Crush-style puzzle game developed by SundayToz. Anipang was simple, addictive, and brilliantly designed for viral growth. But what made it a cultural phenomenon was not the gameplay. It was the social mechanics. To keep playing, you needed "hearts," which were essentially lives. When you ran out, you had to wait, or you could ask your KakaoTalk friends to send you hearts. This created a social obligation loop that was almost impossible to resist. Refusing to send a heart to your friend, your coworker, your mother-in-law, was a minor social faux pas. Anipang did not just go viral. It became a social obligation.

The revenue impact was immediate and staggering. By October 2012, games on the Kakao platform were grossing over 35 million dollars per month. Anipang's own revenues reportedly increased 400-fold after joining the platform. KakaoTalk reported its first profit of 42 million dollars in 2012. By 2013, revenue had climbed to 200 million dollars. The company had gone from zero to two hundred million in revenue in eighteen months, powered almost entirely by taking a cut of games that other people built.

This was the moment that revealed Kakao's true nature. It was not a messaging company. It was a platform company. KakaoTalk was the distribution channel, the social graph, and the identity layer. Games were just the first product to be piped through it. The model would be replicated across every subsequent vertical: build on top of KakaoTalk's user base, leverage the social graph for distribution, and take a toll on the transactions.

Alongside gaming, Kakao introduced its emoticon marketplace, and this deserves more attention than it typically receives. Emoticons, the animated stickers that Koreans use in their chats, are not trivial. They are a multi-hundred-million dollar business and one of the earliest examples of a creator economy at scale. Kakao allowed independent artists and studios to design and sell emoticon sets, taking a revenue share. The emoticons became a form of self-expression, a way to signal personality and mood in a culture where indirect communication is prized. Some popular emoticon creators earned hundreds of thousands of dollars. The market grew to the point where Kakao Friends, the company's own line of characters, including the beloved Ryan the lion, became a brand unto themselves, spawning retail stores, merchandise, and licensing deals.

By 2014, Kakao had proven that it could monetize its platform without charging users for the core messaging service. The free-to-use model was not charity. It was the most effective customer acquisition strategy in Korean tech history. Now the question was whether Kakao could extend beyond gaming and emoticons into businesses that were bigger, stickier, and more defensible. The answer would come in the form of two transformative deals.

V. M&A Strategy: The Daum Merger and LOEN Acquisition

Brian Kim had proven he could build a mobile-first platform with unrivaled distribution. But KakaoTalk had a gap. It was a mobile app, born on the smartphone, and it lacked the web presence, the content library, and the institutional credibility that a public listing would provide. To fill all three gaps at once, Kim engineered one of the cleverest transactions in Korean tech history.

On May 26, 2014, Kakao announced a merger with Daum Communications, South Korea's second-largest web portal after Naver. The structure was revealing. Daum issued 43 million new shares to Kakao's shareholders at a valuation of approximately 72,910 won per share, valuing Kakao at roughly 3.1 trillion won, about 3 billion dollars. On paper, Daum was acquiring Kakao. In reality, Kakao's implied valuation was nearly four times Daum's estimated 2 trillion won. This was a back-door listing, a way for Kakao to go public without the delays, scrutiny, and pricing uncertainty of a traditional IPO. Kim emerged as the largest shareholder of the combined entity with a 22.2 percent stake.

When the deal closed on October 1, 2014, the combined company, initially called Daum Kakao and later renamed simply Kakao in 2015, was valued at close to 10 trillion won, roughly 9.5 billion dollars. For Kakao, the merger delivered three things. First, a public listing and access to public market capital. Second, Daum's web portal, which gave Kakao a presence beyond the smartphone screen. Third, and perhaps most importantly, the institutional infrastructure and cash flow that would fund the next phase of expansion.

Two years later, Kakao made the deal that its critics said was a colossal overpay and that history has judged as a masterstroke. In January 2016, Kakao acquired a 76.4 percent stake in LOEN Entertainment for 1.87 trillion won, approximately 1.6 billion dollars. LOEN operated Melon, South Korea's dominant music streaming platform. At the time of the deal, Melon had roughly 3.6 million paid subscribers and 28 million total users, commanding approximately 70 percent of the domestic streaming market.

The valuation was rich. At roughly six times revenue, skeptics argued Kakao was paying a premium that it could never earn back. Music streaming was a notoriously low-margin business globally. Spotify was losing money. Pandora was struggling. Why would Melon be any different?

The answer lay in what Melon represented within the Kakao ecosystem. Melon was not just a music app. It was a subscription cash cow. Unlike gaming revenue, which was lumpy and dependent on hit titles, Melon generated predictable, recurring subscription revenue every single month. In a portfolio of high-growth, high-volatility businesses, Melon was the steady heartbeat. Its cash flow would fund the aggressive expansions into banking, payments, and mobility that would define Kakao's next chapter. LOEN was subsequently rebranded as Kakao M, and later folded into Kakao Entertainment, becoming the anchor of Kakao's content empire alongside its webtoon and gaming businesses.

The Daum merger gave Kakao the web and the public markets. The Melon acquisition gave it the cash flow engine. Together, these two deals transformed Kakao from a messaging app with a gaming side hustle into a diversified technology conglomerate with the resources and the ambition to verticalize into every major sector of the Korean digital economy. The spin-off factory was about to start running at full speed.

VI. The Spin-Off Factory: Bank, Pay, and Mobility

If the first act of Kakao's story was about building the messenger and the second was about proving it could monetize, the third act was about something far more ambitious: replicating the platform playbook across every major consumer vertical in Korea. The strategy was consistent and ruthless. Identify a sector where incumbents were complacent, launch a Kakao-branded service that leveraged the messaging platform for instant distribution, undercut on price and friction, and grow until you owned the market. Banking, payments, and mobility were the three biggest bets. All three paid off.

KakaoBank launched in July 2017 as South Korea's first mobile-only bank, and the adoption numbers bordered on the absurd. Over 300,000 accounts were opened in the first 24 hours. Within five days, the bank had crossed one million customers. Within two weeks, two million customers had deposited 1 trillion won in savings and taken out 770 billion won in loans. By the end of its first year, KakaoBank had five million accounts, 5.19 trillion won in deposits, and 4.76 trillion won in loans issued.

To appreciate why KakaoBank spread this fast, you need to understand the banking experience it was replacing. Korean traditional banking was dominated by chaebols, the family-controlled conglomerates like KB Financial, Shinhan, and Hana. Opening an account at a traditional bank meant physically visiting a branch, producing identification, filling out paperwork, and waiting. The process could take the better part of an afternoon. KakaoBank compressed it to seven minutes on your phone. No branch visit. No paperwork. Verification was handled through the KakaoTalk identity layer.

But speed was only half the disruption. The other half was cultural. KakaoBank used the Kakao Friends characters, the cute, instantly recognizable mascots from the emoticon business, as the brand identity. Your debit card featured Ryan the lion or Apeach the peach. Banking, historically one of the most staid, impersonal industries in Korea, suddenly became cute and approachable. This was not a gimmick. It was a deliberate strategy to lower the psychological barrier to switching. Traditional bank branches could account for up to 60 percent of a bank's operating costs. KakaoBank stripped all of that away and passed the savings to customers through better rates and lower fees.

By 2025, KakaoBank had grown to 26.7 million customers, with 68.3 trillion won in deposits, up 24 percent year-over-year. It posted a record net profit of 480.3 billion won, and its non-interest income surpassed one trillion won for the first time. The bank is now targeting 30 million customers and 90 trillion won in deposits by 2027. It has also begun developing a Korean won-pegged stablecoin, a move that signals where the next frontier of digital finance may lie.

Kakao Mobility followed a similar playbook. Kakao T, the ride-hailing app, launched on top of the KakaoTalk platform and rapidly dominated the taxi market. Its current market share is estimated at 90 to 98 percent of South Korea's ride-hailing market, with over 23 million registered users and 13.2 million monthly active users. For comparison, Uber, which is attempting a deeper push into Korea, has roughly 700,000 monthly active users. The gap is not competitive. It is categorical. In December 2024, South Korea's Fair Trade Commission fined Kakao Mobility 10.5 million dollars for anti-competitive behavior, specifically for pressuring franchise competitors to either pay fees or sign partnership agreements to access driver supply on the platform. The fine was financially insignificant relative to Kakao's revenues, but it signaled a broader regulatory posture that would come to define the current era.

Kakao Pay, the payments arm, rounds out the trifecta. Integrated directly into KakaoTalk, it enables peer-to-peer transfers, bill payments, and in-store purchases. Its revenue has been growing at 28 percent year-over-year, with financial services revenue up 72 percent.

Looking at the segment-level economics, Kakao's business splits into two broad categories. The Platform segment, which includes KakaoTalk, the portal, Mobility, and Pay, is the high-margin toll booth. It generates revenue from advertising, commissions, and transaction fees with relatively low marginal costs. In Q4 2025, Platform revenue hit 1.22 trillion won, up 17 percent year-over-year, with Talk Biz advertising growing 18 percent. The Content segment, which includes gaming, music via Melon, webtoons, and the SM Entertainment portfolio, is the high-growth engagement engine. It drives user time and subscription revenue but at lower margins due to content costs and talent spending. Q4 Content revenue was 911 billion won, roughly flat year-over-year.

And then there is what might be Kakao's most underappreciated asset: Piccoma. Launched in Japan, Piccoma is Kakao's webtoon and manga platform, and it has achieved something that almost no Korean tech company has managed. It dominates a foreign market. Piccoma was the number one app by consumer spending in all of Japan, including games, for five consecutive years from 2020 through 2024. In 2024, it surpassed 105 billion yen in total sales, roughly 700 million dollars. It beat every native Japanese app, including giants from companies like Sony, Nintendo, and LINE. In the first half of 2025, LINE Manga overtook Piccoma for the top revenue spot, but Piccoma remains a formidable force and Kakao's most successful international export by a wide margin.

Piccoma matters because it answers the most common criticism of Kakao: that it is trapped in the Korean market. Piccoma proves that Kakao's content and platform model can work outside Korea. Whether that success can be replicated in other markets and other verticals remains the open question, but the proof of concept exists. The spin-off factory had built an empire. The question was whether the empire was too big for its own good.

VII. Inflection Point #3: The 2022 Fire and Regulatory Reckoning

October 15, 2022, began as an ordinary Saturday in Pangyo, the tech hub south of Seoul that locals call Korea's Silicon Valley. The SK C&C data center, a nondescript building that housed the servers for dozens of companies, hummed along as it always did. Sometime that afternoon, lithium-ion batteries in the facility's third basement floor caught fire. The flames spread quickly through the battery room. By early evening, critical servers were offline.

For Kakao, it was a catastrophe. The Pangyo data center was not one of many. It was the center. Kakao had concentrated its core infrastructure, including user verification systems, essential data storage, and service routing, at this single facility without adequate geographic redundancy or disaster recovery. When the servers went down, everything went down. KakaoTalk. Kakao Pay. Kakao T. Daum. Kakao Map. The Kakao Certificate system that millions of Koreans used to verify their identity for government and financial services. All of it, dark.

The impact on daily life was immediate and visceral. People could not send messages. They could not pay for transactions. They could not hail taxis. Small businesses that depended on Kakao Pay lost the ability to process sales. Government services that relied on Kakao Certificate for identity verification became inaccessible. Hospitals that used KakaoTalk for patient communication went silent. For a country where 98 percent of smartphone users relied on KakaoTalk, the outage did not feel like a tech glitch. It felt like a power outage, except it was worse, because at least during a power outage you can still talk to people face to face. Kakao's services were so embedded in the very mechanics of human interaction that their absence created a kind of social paralysis.

Core messaging services took over eight hours to restore. Full recovery stretched beyond five days. The company ultimately paid 27.5 billion won in compensation to affected users and businesses. But the real damage was not financial. It was political.

The fire transformed the public narrative around Kakao. Before October 2022, Kakao was the scrappy underdog that had taken on the telcos and the chaebols, the People's App that made communication free and banking accessible. After October 2022, Kakao was a monopoly. A single point of failure for an entire nation. A private company that had accumulated so much power over public infrastructure that its negligence could paralyze the country. The shift was not entirely fair, and it was not entirely unfair either. The truth was that Kakao had been building at breakneck speed for a decade, spinning off subsidiaries, expanding into new verticals, and the boring, expensive work of building redundant infrastructure had fallen behind.

The government's response was swift and structural. The National Assembly enacted what became informally known as the "Kakao Outage Prevention Act," mandating geographic backup redundancy for critical digital services. Regulators began scrutinizing Kakao's market dominance across multiple verticals with a rigor that had not existed before. The conversation had shifted from "How do we support Korean tech champions?" to "How do we regulate Korean tech monopolies?" Brian Kim stepped down as chairman of Kakao in the aftermath, acknowledging the gravity of the crisis and taking personal responsibility. The era of unregulated growth, the move-fast-and-build-everything philosophy that had defined Kakao for a decade, was over.

For investors, the data center fire was the inflection point that redefined Kakao's risk profile. Before the fire, regulatory risk was priced as moderate. After the fire, it became the dominant variable. The Korean government had signaled that it viewed Kakao not as a private tech company operating in competitive markets, but as a quasi-public utility with corresponding obligations. That distinction has enormous implications for future margin expansion, pricing power, and strategic flexibility. And as if the regulatory reckoning were not enough, Kakao was about to deliver a self-inflicted wound that would make things considerably worse.

VIII. The SM Entertainment Saga and Current Management

If the data center fire exposed Kakao's structural vulnerabilities, the SM Entertainment acquisition exposed its governance ones. The story begins in early 2023, when SM Entertainment, the legendary K-pop agency behind acts like EXO, Red Velvet, and aespa, became the prize in a bidding war between two of Korea's most powerful entertainment companies.

The first mover was HYBE, the company behind BTS and the most commercially successful K-pop enterprise in the world. In February 2023, HYBE agreed to buy a 14.8 percent stake from SM founder Lee Soo-man and launched a tender offer for an additional 25 percent of SM's shares. The strategic logic was sound: HYBE wanted to consolidate the K-pop industry's two most valuable talent rosters under one roof.

Kakao was not going to let that happen. Also in February, Kakao agreed to buy a 9.05 percent stake in SM via new shares and convertible bonds for 220 billion won, roughly 170 million dollars. When HYBE launched its tender offer, Kakao responded with a counter-tender on March 6 at 150,000 won per share, a 25 percent premium over HYBE's bid. The message was clear: Kakao would pay whatever it took. On March 12, HYBE withdrew from the contest after reaching a separate agreement with Kakao. By March 28, Kakao had confirmed control of SM Entertainment with approximately 40 percent of the company's shares.

The victory was real. SM's portfolio of artists, intellectual property, and fandom infrastructure was genuinely valuable, and integrating it into Kakao's content ecosystem created meaningful synergies. SM's operating profit surged 262 percent year-over-year in Q3 2025, suggesting the integration was bearing fruit. Plans for a North American joint venture, a fandom platform merger combining SM's Bubble with Kakao's Berries, and the launch of SMiniz, an AI-powered game, all pointed to an operational thesis that was working.

But the cost of victory went far beyond the roughly 1.2 billion dollars Kakao spent acquiring its stake. In the months following the acquisition, prosecutors alleged that Brian Kim had orchestrated a scheme to inflate SM's stock price during the bidding war, funneling approximately 240 billion won, about 172 million dollars, across more than 300 individual transactions. SM shares had spiked from roughly 75,000 won to over 147,000 won during the contest period. Prosecutors charged Kim with violating the Capital Markets Act.

On July 23, 2024, Brian Kim was arrested and held at Seoul Nambu Detention Centre. He was indicted on August 8 and remained in detention until a court granted bail on October 31. Prosecutors demanded a 15-year prison sentence and 500 million won in fines. For a founder who had built two of Korea's most important internet companies, who was worth over 3 billion dollars, and who was South Korea's sixth richest person, the spectacle of being led into a detention center in handcuffs was a stunning fall from grace.

Then came the twist. On October 21, 2025, the Seoul Southern District Court acquitted Kim and all co-defendants of all charges, ruling that prosecutors had failed to prove their case. Prosecutors subsequently appealed, and the legal saga continues. In March 2025, Kim had already stepped down as co-chair of Kakao's Corporate Alignment Council, citing a diagnosis of early-stage bladder cancer. He retains his role as head of Kakao's Future Initiative Center, focused on long-term strategy, and still controls approximately 24 percent of Kakao through personal holdings and K Cube Holdings, his investment vehicle.

The operational leadership of Kakao now rests with Shina Chung, who was appointed CEO in March 2024. Chung is Kakao's first female CEO and brings a markedly different profile from the founder-driven era. She holds an MBA from the University of Michigan and previously worked at Naver, eBay, and Boston Consulting Group before joining Kakao Ventures in 2014 and leading it as CEO since 2018, where she invested in AI, robotics, and gaming startups. Since Kim's departure from the Corporate Alignment Council, Chung is now its sole leader, overseeing the strategic direction of Kakao and all subsidiaries. Her strategic priorities for 2026 center on two pillars: human-centered AI and what she calls "Global Fandom OS."

Under Chung's leadership, the sprawling subsidiary empire has been pruned. At its peak, Kakao had 147 affiliates. That number has been reduced to 94 as of the end of 2025, with a target of roughly 80. Major divestitures include the sale of the Daum portal to AI company Upstage in January 2026 for approximately 200 billion won, along with the divestiture of IST Entertainment and Next Level Studio. The message is clear: the era of growth at all costs is being replaced by a focus on operational efficiency, governance, and shareholder value. Whether the market will reward this discipline, or whether the Korea Discount will continue to weigh on the stock, depends in large part on the success of one audacious bet.

IX. The "Hidden" Future: AI and Kanana

Every major platform company in the world is racing to integrate artificial intelligence into its core products. For most of them, the challenge is distribution. They have the AI models, but they need to get them in front of users. Kakao has the opposite problem. It has 49 million monthly active users on KakaoTalk and near-total penetration of South Korea, but it needs the AI models to make the next leap.

The company's answer is Kanana, a proprietary AI platform that represents Kakao's most important strategic bet since the launch of KakaoTalk itself. At the foundation is Kanana Nano, a lightweight, on-device AI model designed specifically for strong Korean language understanding. Think of it like this: large AI models such as GPT-4 or Claude run on massive server farms and communicate with your phone over the internet. An on-device model runs directly on the phone itself, which means it can work faster, maintain privacy, and operate even with a spotty connection. Kakao is building Kanana Nano to understand Korean at a native level, not as a translation from English, but as a model that thinks in Korean from the ground up. Korean is a linguistically complex language with honorific levels, agglutinative grammar, and context-dependent meaning that general-purpose models handle adequately but not natively. A model built specifically for Korean, trained on Korean conversation patterns, and integrated into the app where all Korean conversation already happens, has a structural advantage that no foreign competitor can easily replicate.

Kakao has pursued a dual strategy on AI. Rather than trying to build frontier models alone, a resource-intensive proposition that would pit it against companies spending tens of billions of dollars, Kakao partnered with OpenAI. In October 2025, the company launched "ChatGPT for Kakao," integrating OpenAI's models directly into the KakaoTalk interface. The service reached 8 million users quickly, demonstrating that the demand for AI-powered communication tools within the Korean market was substantial. Simultaneously, Kakao partnered with Google to enhance on-device AI services, hedging its bets across multiple model providers.

The full vision for Kanana goes far beyond a chatbot bolted onto a messenger. Kakao's plan, which is rolling out in the first half of 2026, is to transform KakaoTalk from a messaging app into an agent-based platform. What does "agent" mean in this context? Think of the difference between a search engine and a personal assistant. A search engine answers your question. An agent does the task. Kanana will not just answer questions. It will read your group chat history, understand your social context, manage your calendar, make restaurant reservations through Kakao's commerce platform, suggest gifts based on your friends' preferences using Kakao's gifting service, and coordinate group plans by analyzing the availability and preferences of multiple people simultaneously.

Here is a concrete example. Today, a group chat about dinner plans involves twenty messages of "Where should we eat?" and "When are you free?" and "I cannot do Thursday." In Kakao's vision, Kanana handles that. It knows everyone's schedules from Kakao Calendar, it knows their food preferences from past Kakao orders, it knows the group's price range from past spending on Kakao Pay, and it proposes a plan that everyone can accept or modify. The messenger does not just facilitate the conversation. It resolves the conversation.

The technical roadmap supports this ambition. Kanana is being integrated into KakaoTalk messaging and Kanana Search in the first half of 2026. Subsequent phases will extend to Melon, Kakao Map, gifting, and reservation services. Kakao has also open-sourced Kanana-2 models on Hugging Face and launched "Kanana Scholar," an academic cooperation program for research collaboration announced in March 2026. A planned open-agent ecosystem would allow third-party developers to build on the Kanana platform, potentially creating an app-store-like environment for AI agents within KakaoTalk.

Whether Kanana succeeds at this level of ambition is genuinely uncertain. The technical challenges of building a reliable, context-aware AI agent that manages social interactions without making embarrassing mistakes are significant. But the distribution advantage is undeniable. Every other AI company in the world has to convince people to download a new app or visit a new website. Kakao just has to ship an update to the app that every Korean already has on their phone. If Kanana works, Kakao will have accomplished something no company in the world has yet achieved: turning a messenger into a functioning AI personal assistant at national scale. And that possibility raises the question of how to analyze Kakao's competitive position using a more rigorous strategic framework.

X. Playbook: Strategic Powers and Competitive Dynamics

To understand why Kakao has been able to build and defend its position, and where it remains vulnerable, it helps to analyze the company through the lens of Hamilton Helmer's Seven Powers framework and Michael Porter's Five Forces.

Kakao's cornerstone power is network effects, and the strength of these effects may be the highest of any technology company on earth, relative to its addressable market. KakaoTalk is not popular because it is the best messenger. It is popular because everyone else is already on it. In a country of 52 million people, 49 million are monthly active users. Your family is there. Your boss is there. Your children's school teachers are there. Your apartment building management committee is there. The network effect is not just about scale. It is about completeness. In most markets, a social network reaches 30 or 40 percent of the population and then growth slows as it hits diminishing marginal returns. KakaoTalk reached 95 percent and kept going. At that penetration level, not being on KakaoTalk is not a preference. It is a disability. You cannot function in Korean society without it.

The switching costs that follow from this completeness are formidable. It is not just that your social graph is on KakaoTalk. Your banking is on KakaoBank, which is accessed through KakaoTalk. Your ride-hailing is on Kakao T. Your identity verification for government services runs through Kakao Certificate. Your payment history, your chat memories, your digital life, all of it is locked into the Kakao ecosystem. Switching from KakaoTalk to another messenger would require simultaneously switching your bank, your ride-hailing app, your payment app, and your government ID system. The switching cost is not high. It is effectively infinite for the average Korean consumer.

Counter-positioning was the power that enabled Kakao's initial disruption. When KakaoTalk launched, the telcos could not respond without cannibalizing their own SMS revenue. When KakaoBank launched, traditional banks could not match its frictionless mobile experience without undermining their branch-based cost structures. When Kakao T launched, traditional taxi dispatch systems could not compete with an app that was pre-installed on every smartphone in the country. In each case, Kakao positioned itself where the incumbents could not follow without self-harm.

There is also an element of scale economies in Kakao's platform businesses. The marginal cost of adding one more user to KakaoTalk is essentially zero, while the value of the network to all existing users increases. This creates a flywheel where the largest platform gets better economics, which allows it to invest more, which makes it even larger. The dynamic is self-reinforcing and extremely difficult to disrupt.

Turning to Porter's Five Forces, the competitive landscape reveals why Kakao's current strategic position is both powerful and precarious.

The threat of new entrants in Kakao's core Korean market is near zero for messaging and extremely low for the integrated services. No new messenger app can realistically challenge KakaoTalk's penetration. The social graph lock-in creates a barrier that no amount of marketing or product superiority can overcome. However, the threat is more meaningful in specific verticals where the integration advantage is weaker. Uber's push into Korean ride-hailing and the emergence of challenger banks show that no individual Kakao subsidiary is invincible, even if the core messenger remains impregnable.

The bargaining power of buyers is theoretically low. Individual consumers have no leverage over a platform used by the entire nation. But there is a crucial nuance: the Korean government has positioned itself as the proxy buyer, exercising bargaining power on behalf of the population through regulation. Since the 2022 fire, regulatory power over Kakao has been at an all-time high. The "Kakao Outage Prevention Act," the antitrust fines on Kakao Mobility, and the heightened scrutiny of the SM acquisition all reflect a government that views Kakao as too important to be left to market forces alone. This regulatory dynamic is now the single most important external force acting on Kakao's business.

Supplier power is moderate. Kakao depends on content creators for its webtoon and music businesses, and on drivers for Kakao T. In content, the SM Entertainment acquisition was partly an effort to reduce supplier power by bringing marquee talent in-house. In mobility, the 90-plus percent market share means drivers have little choice but to use the platform, though regulatory intervention could change that calculus.

Competitive rivalry with Naver, the Google of Korea, is intense and spans multiple fronts. Naver dominates search with roughly 50 percent of the Korean market. Kakao dominates messaging. They compete directly in maps, where Naver Map leads with 28.8 million monthly active users to Kakao Map's 12.6 million. They compete in fintech, with KakaoPay versus NaverPay. They compete in webtoons, with Kakao's Piccoma versus Naver Webtoon. They compete in AI, with Kakao's Kanana versus Naver's HyperCLOVA and Agent N. And they are both reportedly developing Korean won-pegged stablecoins, setting up a potential clash in digital currency. The rivalry is multidimensional and unlikely to produce a clear winner across all verticals, which means both companies will continue to invest heavily to defend their respective strongholds.

For investors tracking Kakao's ongoing performance, two metrics matter more than any others. The first is KakaoTalk monthly active users. This number, currently at 49.1 million, is the foundation upon which every Kakao business is built. If MAUs decline, it signals erosion of the most important competitive moat in the entire ecosystem. The second metric is Talk Biz revenue growth. This measures Kakao's ability to monetize the messaging platform through advertising, commerce, and services. Q4 2025 showed 18 percent year-over-year growth, a healthy acceleration. Together, these two numbers tell you whether the platform is retaining its users and whether Kakao is getting better at extracting value from them. Everything else, the banking, the mobility, the content, flows from the health of those two metrics.

XI. Analysis: Bull vs. Bear Case

The bear case against Kakao is straightforward and compelling. Start with the Korea Discount, the persistent undervaluation of Korean equities relative to global peers driven by complex cross-shareholdings, weak governance, and regulatory unpredictability. Kakao trades at roughly 50,600 won per share, down more than 70 percent from its 2021 peak of 173,000 won. Even after the acquittal of Brian Kim on stock manipulation charges, the legal cloud has not fully dissipated. Prosecutors have appealed, and the founder's cancer diagnosis adds uncertainty about long-term leadership continuity.

The regulatory environment has structurally shifted since the 2022 fire. Kakao is now treated as a quasi-public utility, which limits pricing power, mandates infrastructure spending, and subjects every major strategic decision to government scrutiny. The antitrust fine on Kakao Mobility, while small, was a shot across the bow. Each new vertical Kakao enters now faces a higher bar of regulatory acceptance than it would have five years ago.

The geographic concentration is another bear concern. Kakao generates the overwhelming majority of its revenue from a single market, South Korea, a country of 52 million people with a mature smartphone market and a declining population. Piccoma's success in Japan proves that international expansion is possible, but it remains the only significant international business. Attempts to expand KakaoTalk beyond Korea have not gained meaningful traction. In an era where global AI platforms like ChatGPT and Claude are being built for billions of users worldwide, Kakao's Korean-language moat could become a Korean-language cage.

There is also the structural complexity of the conglomerate. Even after pruning from 147 to 94 subsidiaries, Kakao remains a sprawling empire with cross-holdings, related-party transactions, and opacity that make it difficult for outside investors to assess the true earnings power of the core business. The Korea Discount is not arbitrary. It reflects real governance concerns that Kakao has only begun to address.

The bull case requires looking past these headwinds to what Kakao actually owns. First and most fundamentally, Kakao owns the digital identity of a G10 nation. Nearly 50 million monthly active users on KakaoTalk. Nearly 27 million KakaoBank customers. Near-total dominance in ride-hailing. The network effects are not eroding. They are deepening as more services integrate into the ecosystem. No competitor, domestic or foreign, has a realistic path to displacing KakaoTalk from its position as the default communication layer of Korean society.

Second, the financials are improving under new management. FY2025 delivered record revenue of approximately 8.1 trillion won and operating profit of 732 billion won, the highest operating margin in four years. The subsidiary pruning is real and ongoing. The sale of the Daum portal, the divestiture of non-core assets, and the target of reducing affiliates to roughly 80 all suggest that CEO Shina Chung is serious about the shift from growth-at-all-costs to operational discipline. If the margin expansion continues, the stock's current valuation could begin to look increasingly disconnected from fundamental earnings power.

Third, Piccoma is a genuine global asset. Generating roughly 700 million dollars in annual consumer spending in Japan, dominating the non-game app charts for five consecutive years, and building an original content pipeline, Piccoma demonstrates that Kakao's content model translates across borders. If the webtoon market continues to grow globally, and all signs suggest it will, Piccoma is positioned to be a major beneficiary.

Fourth, and most speculatively, Kanana. If Kakao successfully transforms KakaoTalk from a messenger into an AI-powered personal agent, it will have achieved something no company has yet done at national scale. The distribution advantage is massive: every Korean already has the app. The data advantage is real: Kakao has years of conversation history, social graph data, and behavioral signals to train on. The risk is execution, but the potential payoff is a fundamental re-rating of the entire company from "Korean messaging utility" to "AI-powered platform."

The tension at the heart of Kakao's investment case is identity. Is it a tech company, with the multiple expansion that implies, or is it a regulated national utility, priced for stability rather than growth? The answer probably lies somewhere in between. Kakao is too innovative and too diversified to be merely a utility, but it is too embedded in national infrastructure to be treated as a pure-play tech stock. The next two years, as Kanana rolls out, as the regulatory framework stabilizes, and as the legal proceedings against Brian Kim reach their conclusion, will determine which identity prevails.

XII. Epilogue

Brian Kim's biography reads like a Korean novel. Born into poverty in a rural province. Educated himself into Seoul National University through sheer will. Built the number one internet company in Korea, then walked away. Moved to Silicon Valley, saw the future in a phone, came back, and built the number one mobile platform in Korea. Was arrested, imprisoned, tried, acquitted, diagnosed with cancer, and stepped back from the empire he created, all within the span of two years.

The company he left behind is simultaneously one of the most dominant technology platforms in any democracy on earth and one of the most scrutinized. It generates over eight trillion won in annual revenue, touches the daily lives of virtually every Korean citizen, and faces a regulatory reckoning that will reshape its operating freedom for years to come. Its new CEO, Shina Chung, has the mandate and the management consulting toolkit to rationalize the empire, but she also inherits the fundamental tension between Kakao's identity as a private innovator and its reality as a public necessity.

The Kanana bet looms over everything. In a world where every platform company is racing to embed AI into its products, Kakao has one advantage that no amount of compute spending can replicate: it already owns the conversation. Fifty million people talk to each other on KakaoTalk every day. If Kakao can insert an intelligent agent into those conversations, one that understands context, manages logistics, and makes daily life frictionless, it will have built something without precedent. If it cannot, it will remain what it already is: a superbly dominant national platform, priced like a utility, and capped by the boundaries of the Korean market.

For further reading, Korean-language sources such as "The Kakao Story" provide valuable founder-era context. App Annie and Sensor Tower reports on Piccoma offer the best quantitative view of Kakao's Japan operations. The 2025 Q3 and Q4 earnings transcripts contain management's most detailed commentary on the Corporate Alignment Council restructuring, and the Kanana integration timeline, and both are essential reading for anyone building a forward-looking thesis on the company.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube