NAVER Corporation: The Search for the Global Soul

I. Introduction: The "Anti-Google"

In 2024, NAVER Corporation did something that seemed almost structurally impossible: it became the first Korean internet company to cross ten trillion won in annual revenue. That number, roughly seven and a half billion dollars at prevailing exchange rates, might not raise eyebrows in Silicon Valley, where a handful of companies measure revenue in hundreds of billions. But consider the context. South Korea is a nation of fifty-two million people. NAVER built this business almost entirely within that market, and it did so while fending off the most dominant company in the history of the internet.

Google controls over ninety percent of search in most developed countries. In the United Kingdom, Germany, France, Brazil, India, and Australia, no local competitor even comes close. The pattern is so consistent that it feels like a law of nature. But in South Korea, as of early 2026, NAVER commands nearly sixty-three percent of the search market. Google sits at under thirty percent. That gap has actually widened over the past two years, not narrowed.

This is not a "Korean Google" story. That framing misses everything interesting about NAVER. This is a story about a company that used online gaming revenue to subsidize search engine research when search had no business model. A company that turned a natural disaster into the launch of Japan's most important messaging platform. A company that realized the Korean internet was empty, so instead of searching the web, it built the web. A company that spun off its gaming division, its webtoon division, and its Japanese messaging division into separate entities, not because they were failing, but because the parent company was too good at incubation.

The themes that run through NAVER's history are unusual. There is the "walled garden" strategy, where every service feeds every other service, locking users into an ecosystem that is less like Google's open web and more like a digital city-state. There is the corporate spin-off as a strategic weapon, deployed with a frequency and precision that would make a private equity firm envious. And there is the ongoing transition from Lee Hae-jin's founder era to what insiders call the "Choi-Kim" era, a generational handoff happening at the exact moment when artificial intelligence threatens to redraw every competitive boundary in the industry.

The story begins, as many great Korean business stories do, in the wreckage of a financial crisis.

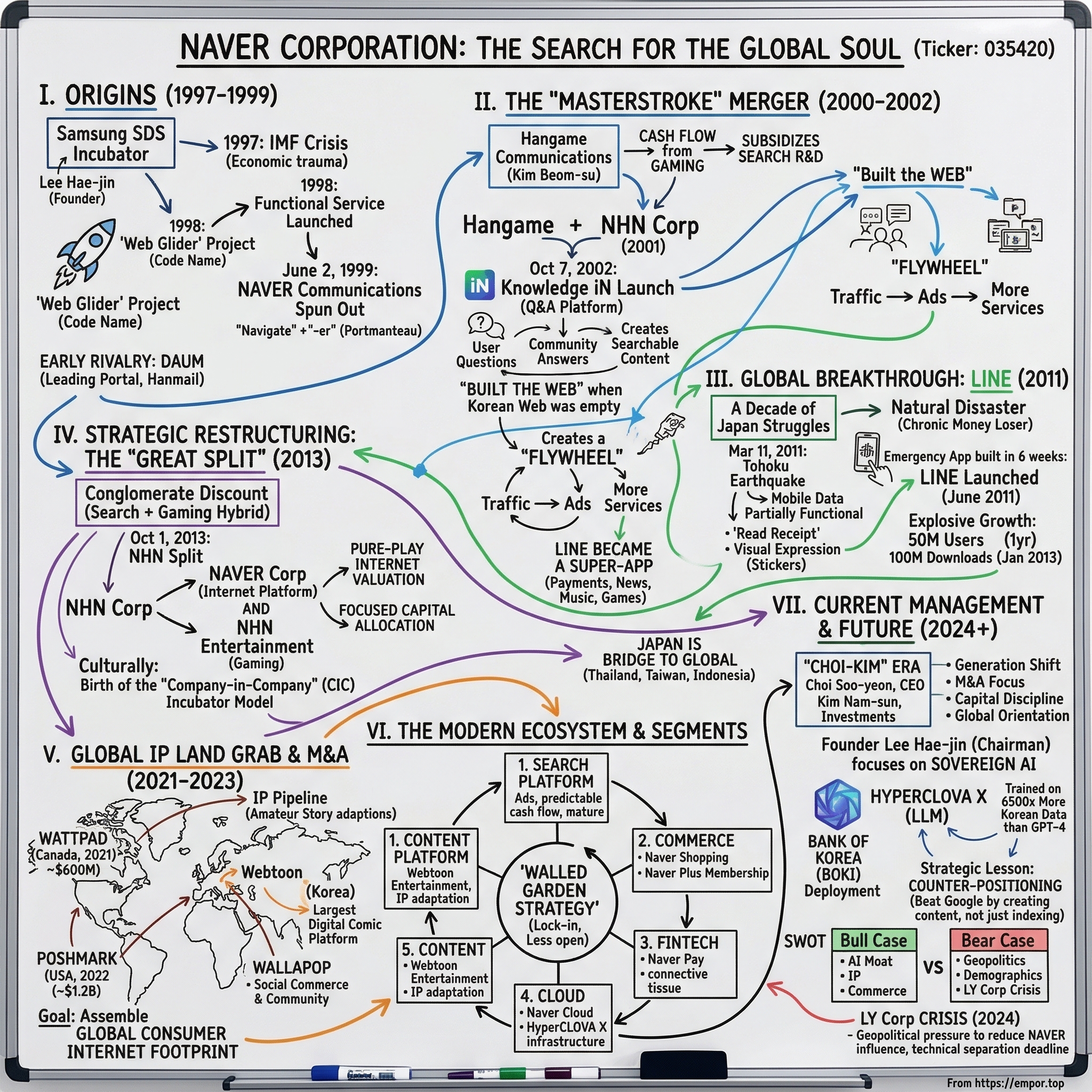

II. Origins: The Samsung SDS Incubator (1997–1999)

In late 1997, the International Monetary Fund effectively took control of South Korea's economy. The Asian Financial Crisis had hit the country with the force of a tidal wave. The Korean won lost half its value. Unemployment tripled. Companies that had seemed invincible, including Daewoo and Ssangyong, simply ceased to exist. It was, by any measure, the most traumatic economic event in modern Korean history.

Inside Samsung SDS, the information technology services arm of the Samsung empire, a quiet engineer named Lee Hae-jin was working on something that seemed almost absurdly disconnected from the national emergency. He was building a search engine. Lee had started the project in October 1997, just weeks before the IMF crisis erupted, under the codename "Web Glider." His first functional service launched in January 1998, when most Koreans were focused on whether their banks would survive the week.

Lee Hae-jin was not the archetype of a Silicon Valley founder. He did not drop out of school, did not work out of a garage, and did not have a reputation for charismatic disruption. He was methodical, patient, and deeply technical. Colleagues from that era describe him as the kind of engineer who would spend weeks understanding a problem before writing a single line of code. In a country where the dominant business culture rewarded speed and hierarchy, Lee's temperament was unusual. It would prove to be exactly what was needed.

The problem Lee was trying to solve was more subtle than it appeared. In 1999, search engines were essentially directories. Yahoo, the dominant player globally, organized the web into categories that human editors maintained. AltaVista and Lycos offered keyword search, but the results were crude. These systems worked tolerably well for English, a language with relatively simple morphology. Korean was a different beast entirely. Hangul, the Korean alphabet, is an agglutinative writing system where meaning changes dramatically with suffixes and particles. The word "school" in Korean can take dozens of forms depending on grammatical context, and early Western algorithms had no idea how to handle this. A Korean user searching for information about their child's school might get results about fish, construction, or nothing at all.

This linguistic complexity created an opening. Google, which was just incorporating in September 1998, was brilliant at indexing English-language web pages. But Korean? The Korean web was tiny, poorly indexed, and linguistically hostile to the algorithms that were making Google dominant in the West.

Samsung SDS, to its credit, had established an internal venture program that allowed engineers like Lee to operate with some degree of autonomy. On June 2, 1999, NAVER Communications was formally spun out as a separate company. The name was a portmanteau of "Navigate" and the suffix "-er," meaning "one who navigates." It was a tiny operation, a lifeboat launched from a corporate aircraft carrier into the choppy waters of the Korean internet.

The early competition was fierce. Daum, founded in 1997, had already established itself as Korea's leading portal with its email service, Hanmail. Daum had the users, the brand recognition, and the advertising revenue. NAVER was the underdog, and in the summer of 1999, almost nobody was betting on the navigator.

But Lee Hae-jin had seen something that Daum had not. The Korean web did not need a better directory. It needed someone to create the content that a search engine could then organize. That insight, which would take several years to fully execute, would change everything. First, though, NAVER needed to survive. And survival, as it turned out, would come from an unexpected source.

III. The "Masterstroke" Merger: Hangame and Search (2000–2002)

In the year 2000, search engines did not make money. Not in America, not in Europe, and certainly not in South Korea. Google was still two years away from launching AdWords. Yahoo relied on display advertising and directory listings. The idea that search queries themselves could be monetized was still theoretical. NAVER had a technically impressive product and almost no revenue to show for it.

Online gaming, however, was a different story entirely. South Korea in the early 2000s was arguably the most important gaming market in the world. The country had invested heavily in broadband infrastructure after the IMF crisis, and by 2000, high-speed internet penetration was the highest on the planet. PC bangs, the Korean internet cafes where young people gathered to play games, were everywhere. And the company that had figured out how to monetize this phenomenon was Hangame.

Hangame Communications had been founded by Kim Beom-su, a figure who deserves a brief aside because his subsequent career would intersect with NAVER's story in dramatic fashion. Kim would go on to found Kakao, which would become NAVER's fiercest domestic rival. But in 2000, Hangame was a pure-play online gaming company with something NAVER desperately needed: cash flow.

In July 2000, NAVER merged with Hangame (along with two smaller entities, Oneque and Search Solutions). The combined company was renamed NHN Corporation in 2001, standing for "Next Human Network." To outside observers, this looked like an odd marriage. What did casual gaming have to do with internet search? The answer was everything.

Hangame's gaming revenue provided the financial float that kept NAVER's search engine research and development alive during the years when search had no viable business model. While Google in Mountain View was burning through venture capital to build its index, NAVER in Seongnam was using gaming profits to do the same thing. It was a cross-subsidy strategy that would prove remarkably effective, though it took years to pay off.

The true inflection point came on October 7, 2002, with the launch of Knowledge iN. This was the product that demonstrated Lee Hae-jin's fundamental insight about the Korean internet. The problem was not that NAVER's search algorithm was bad. The problem was that there was almost nothing to search. The Korean web was sparse. Compared to the English-language internet, there simply was not enough content in Korean for any search engine to be useful.

Knowledge iN solved this problem in a way that was both elegant and, in retrospect, obvious. It was a question-and-answer platform where Korean users could ask questions and other users could provide answers. NAVER did not search the existing web. It built the web. Every question asked and every answer provided became searchable content within NAVER's ecosystem. Users created the corpus that the search engine then organized.

The timing was critical. Knowledge iN launched three full years before Yahoo Answers. Bradley Horowitz, then a vice president at Yahoo, would later publicly cite Knowledge iN as the direct inspiration for Yahoo's own Q&A product. By May 2016, Knowledge iN had accumulated over one hundred million questions and two hundred million answers, a staggering repository of Korean-language knowledge that no competitor could replicate.

This was the moment NAVER stopped being a search engine and became a platform. The Q&A content drove search traffic. The search traffic drove advertising revenue. The advertising revenue funded the development of additional services, including Naver Blog, Naver Cafe (community forums), and eventually Naver News, each of which generated more content, which drove more search traffic. It was a flywheel, and once it started spinning, it proved nearly impossible to stop.

For investors, the Hangame merger established a pattern that would define NAVER for the next two decades: use cash flow from one business to fund the development of the next, even when the next business has no obvious monetization path. It is a strategy that requires patience, institutional trust, and a founder willing to sacrifice short-term earnings for long-term positioning. Lee Hae-jin had all three.

IV. Inflection Point: The Birth of LINE and the Tohoku Miracle (2011)

For ten years, NAVER tried to crack Japan. The company opened offices, launched products, ran marketing campaigns, and partnered with local firms. Nothing worked. The Japanese internet market was massive, the second largest in Asia, but it was also insular, culturally distinct, and dominated by domestic players like Yahoo Japan and Mixi. NAVER's Korean search model, built on user-generated content and a walled-garden ecosystem, could not gain traction against entrenched incumbents operating in a language and culture that NAVER did not fully understand.

By early 2011, the Japanese operation was a chronic money-loser and an increasingly awkward line item in NHN's financial statements. Internally, there were growing questions about whether the Japan strategy should be abandoned entirely.

Then, on March 11, 2011, a magnitude 8.9 earthquake struck off the Pacific coast of Tohoku, Japan. It was the most powerful earthquake ever recorded in Japan and the fourth most powerful in the world since modern record-keeping began. The subsequent tsunami killed nearly twenty thousand people, displaced hundreds of thousands, and triggered the Fukushima Daiichi nuclear disaster.

In the immediate aftermath, Japan's cellular networks collapsed under the weight of desperate call attempts. Voice calls were impossible. Text messages were unreliable. But mobile data, which used a different part of the network infrastructure, remained partially functional. People who could not call their families could, in some cases, still reach the internet.

Inside NHN Japan's offices, the small engineering team saw this not as a business opportunity but as a genuine crisis to solve. They began building a messaging application that would work over data connections rather than traditional cellular networks. The development timeline was extraordinary. In approximately six weeks, the team produced a functional messaging app. LINE launched in Japan in June 2011, just three months after the earthquake.

The initial value proposition was simple and urgent: a way to reach your loved ones when the phone system was broken. The app featured a green chat bubble interface and, critically, a "read receipt" function that told senders their message had been seen. In a nation still reeling from disaster, that small confirmation, the knowledge that someone you cared about had read your message, carried enormous emotional weight.

What happened next was one of the most remarkable growth stories in mobile internet history. LINE reached fifty million users within its first year. By January 2013, it had surpassed one hundred million downloads. It became the dominant messaging platform not only in Japan but also in Thailand, Taiwan, and Indonesia. In Japan specifically, LINE achieved a market penetration that even WhatsApp could only envy. It became the default communication infrastructure for an entire nation.

But the insight that transformed LINE from a messaging app into a business empire was stickers. NAVER's team discovered that East Asian communication culture placed enormous value on visual expression. Japanese and Korean users did not just want to type words to each other. They wanted to send expressive, often humorous, illustrations that conveyed emotions more precisely than text could. NAVER created a marketplace where artists could design and sell digital sticker packs, and users devoured them.

The sticker economy became a billion-dollar business. What seems like a trivial feature, sending cartoon bears and cats to your friends, was actually a profound insight about the cultural differences in digital communication between East Asia and the West. In markets where direct emotional expression is often culturally modulated, stickers provided a socially acceptable way to say "I love you," "I'm sorry," or "I'm angry" without the vulnerability of spelling it out.

LINE evolved rapidly from messaging into a super-app. LINE Pay for mobile payments. LINE News for media. LINE Music for streaming. LINE Games for entertainment. LINE Shopping for commerce. Each additional service deepened the platform's hold on its users and expanded the data NAVER could collect about Japanese consumer behavior.

The Tohoku earthquake was a human tragedy of immense proportions. But for NAVER, it was also the "black swan" event that accomplished in six weeks what a decade of deliberate strategy could not. It gave the company a global platform, a bridge into the world's third-largest economy, and a proof of concept that NAVER's core competency, building ecosystems rather than individual products, could work outside Korea.

The question of what happens to that bridge is one of the most consequential issues facing NAVER today, but that story comes later.

V. Inflection Point: The 2013 "Great Split" (NHN to NAVER)

By 2012, NHN Corporation had a problem that many conglomerates face but few solve well. The company was simultaneously a high-growth internet platform (search, LINE, content) and a mature gaming business (Hangame). Wall Street analysts call this a "conglomerate discount," the tendency of investors to value a diversified company at less than the sum of its parts because the different businesses require different management approaches, different capital allocation strategies, and different investor bases.

The decision to split was announced in August 2013 and executed on October 1 of that year. NHN Corporation divided into two separate entities. The internet services business, including search, LINE, and content platforms, became NAVER Corporation. The gaming business retained the Hangame brand and became NHN Entertainment. In a parallel move, NHN Japan was similarly split into Line Corporation (web services) and Hangame Japan (games).

The mechanics of the split were clean, but the strategic implications were profound. NAVER Corporation could now be valued by investors as a pure-play internet platform company, comparable to Google, Baidu, or Yahoo Japan, rather than as a hybrid gaming-internet conglomerate. The stock re-rated accordingly. Growth investors who had been reluctant to own a company where a significant portion of earnings came from casual gaming could now buy NAVER without the baggage.

More importantly, the split freed NAVER's management to allocate capital with a singular focus. Every won of investment could now flow toward search, commerce, fintech, content, and the increasingly important LINE ecosystem, without the competing demands of game development studios and gaming server infrastructure.

For Lee Hae-jin personally, this was a turning point. With NAVER now a focused platform company and LINE growing explosively in Japan, Lee began shifting his attention from day-to-day operations to what he called "global strategy." He had always been more comfortable as a strategic thinker than as an operational executive, and the split gave him the organizational permission to operate at the altitude he preferred.

The split also established a cultural pattern at NAVER that would recur: the "Company-in-Company" or CIC model, where NAVER incubates a business internally, allows it to reach scale, and then separates it into an independent entity. The gaming split was the first execution of this playbook. Webtoon would be the next. The underlying philosophy was that great businesses are built by focused teams with focused missions, and that the parent company's role is to provide capital, infrastructure, and strategic guidance, not operational control.

For the market, the message was clear: NAVER was no longer a Korean internet conglomerate. It was a platform company with global ambitions, and it was willing to restructure itself as aggressively as needed to pursue them.

VI. M&A and Capital Deployment: The Global IP Land Grab (2021–2023)

The period between 2021 and early 2023 marked the most aggressive stretch of international acquisitions in NAVER's history. In roughly two years, the company deployed over two billion dollars across three continents, buying companies that, on the surface, seemed to have little in common. A Canadian storytelling platform. An American secondhand fashion marketplace. A Spanish classifieds app. The common thread was not obvious, and that was precisely the point.

The Wattpad acquisition, completed in 2021 for approximately six hundred million dollars, was the first major move. Wattpad was a Toronto-based platform where amateur writers published serialized stories and readers consumed them, often on mobile devices, often in genres like romance, fantasy, and fan fiction that mainstream publishers had historically neglected. At roughly thirteen times revenue, NAVER paid a significant premium.

The skeptics focused on the revenue multiple and missed the strategy. NAVER was not buying Wattpad's revenue. It was buying an intellectual property pipeline. Wattpad had demonstrated something that NAVER's own Webtoon platform had already proven in Korea: that user-generated serialized content could be systematically converted into professional media. Wattpad stories had already been adapted into Netflix films and Hulu series. Combined with Webtoon's library of Korean comics, NAVER was assembling the largest repository of pre-validated, audience-tested story IP outside of traditional Hollywood studios and publishing houses.

Think of it this way: Hollywood spends hundreds of millions of dollars developing scripts, testing concepts, and producing pilots, most of which fail. NAVER's model inverts this. Millions of creators publish stories for free. Readers vote with their attention. The stories that attract the most engagement become candidates for adaptation into dramas, films, and animated series. The audience has already validated the concept before a single dollar of production money is spent. It is, in effect, the world's largest and lowest-cost content development lab.

The Poshmark acquisition, announced on October 3, 2022, was more controversial. NAVER agreed to acquire the American social commerce platform for approximately 1.2 billion dollars in cash, at seventeen dollars and ninety cents per share, representing a fifteen percent premium to the pre-announcement stock price. The deal closed in the first quarter of 2023, and Poshmark was delisted from Nasdaq.

Critics argued that NAVER overpaid for a company in a depressed sector. The US resale market was cooling, Poshmark's growth had decelerated, and the integration challenges of running an American consumer marketplace from Seoul seemed daunting. But NAVER's logic was more nuanced than the critics appreciated. Poshmark was not just a retailer. It was a community with millions of active users who created listings, styled outfits, shared recommendations, and built social followings around fashion. That community and its behavioral data represented a training set for NAVER's commerce AI and a beachhead in the American market that would have taken years to build organically.

The European piece of the puzzle was Wallapop, a Spanish consumer-to-consumer marketplace. NAVER initially acquired a minority stake in 2021 for one hundred and fifteen million euros, followed by an additional seventy-five million euros in 2023. Then, in August 2025, NAVER moved to acquire the remaining seventy-point-five percent of the company for three hundred and seventy-seven million euros, valuing Wallapop at approximately six hundred million euros. The deal was approved by Spain's CNMC competition authority and completed in January 2026. NAVER's total investment in Wallapop reached approximately seven hundred and eleven million dollars for full ownership.

Wallapop reported one hundred and one million euros in revenue for 2024, growing thirteen percent year over year, with losses narrowing by eighteen percent. It was not yet profitable, but the trajectory was improving, and more importantly, it gave NAVER full control of a consumer marketplace with strong positions in Spain and Italy.

Step back and look at the portfolio. NAVER now owns the dominant secondhand fashion marketplace in the United States (Poshmark), the leading C2C marketplace in southern Europe (Wallapop), and two of the world's largest user-generated content platforms (Webtoon and Wattpad). Combined with its dominant position in Korean commerce through Naver Shopping and its growing Naver Plus membership program, the company has assembled a global consumer internet footprint that no other Korean company possesses.

The risk, of course, is execution. Managing consumer marketplaces across three continents, four languages, and radically different regulatory environments is enormously complex. Whether these acquisitions generate returns commensurate with their cost remains one of the key open questions for NAVER investors.

VII. The "Hidden" Engines: Segments and Data

The financial architecture of NAVER is more complex than most investors realize, and understanding how the segments interact is essential to understanding why the company is more defensible than any individual business line would suggest.

In fiscal year 2025, NAVER generated total revenue of 12.35 trillion won, approximately 9.15 billion dollars, representing growth of just over twelve percent from the prior year's landmark ten-point-seven-four trillion won. Operating profit reached 2.21 trillion won with operating margins of approximately nineteen percent in the fourth quarter. These are not Google-level margins, but they are impressive for a company investing as aggressively as NAVER across AI, commerce, and international expansion.

The search platform remains the financial bedrock. Advertising revenue, primarily from search ads and display advertising on the NAVER portal, accounted for just under four trillion won in 2024, growing at nearly ten percent annually. This is a mature business with high margins and predictable cash flows, and it serves the same function that gaming revenue served two decades ago: it provides the financial stability that funds everything else. Critically, AI has begun to accelerate this segment. In 2025, artificial intelligence accounted for fifty-five percent of the nearly nine percent growth in platform advertising revenue, a signal that NAVER's AI investments are already generating measurable returns in its core business.

Commerce is the fastest-growing major segment and the one that most excites growth-oriented investors. At nearly three trillion won in 2024 and surging thirty-six percent year over year in the fourth quarter of 2025, NAVER's commerce business is building toward a scale that demands attention. The engine here is Naver Shopping, which functions less like Amazon and more like a giant marketplace connecting Korean consumers with millions of small and medium-sized merchants. The "Naver Plus" membership, NAVER's answer to Amazon Prime, bundles free shipping, point accumulation, and exclusive deals to drive repeat purchases and lock in customer loyalty.

The fintech segment, anchored by Naver Pay, generated roughly 1.5 trillion won in 2024, also growing at nearly fifteen percent. Naver Pay is not just a payment wallet. It is the connective tissue between search and commerce. When a user searches for a product on NAVER, clicks through to a merchant, and pays with Naver Pay, NAVER captures the entire transaction chain: the intent (search query), the consideration (browsing behavior), and the conversion (payment). This closed-loop data is extraordinarily valuable for advertising targeting and is something that Google, which lacks a comparable payments infrastructure in most markets, cannot easily replicate.

The cloud segment, while the smallest at roughly five hundred and sixty-four billion won in 2024, was also the fastest-growing at over twenty-six percent year over year. NAVER Cloud is the infrastructure layer for HyperCLOVA X, the company's large language model, and increasingly for Korean government and enterprise customers who want AI capabilities but are uncomfortable routing their data through American hyperscalers. The "sovereign cloud" pitch, essentially "your data stays in Korea and is processed by Korean AI," resonates powerfully with both government regulators and enterprise CIOs.

And then there is Webtoon Entertainment, the segment that defies easy categorization. NAVER's content business generated approximately 1.8 trillion won in 2024, and Webtoon Entertainment, which IPO'd on Nasdaq in June 2024 at twenty-one dollars per share, is the crown jewel within it. NAVER retains approximately sixty-three percent ownership of WBTN post-IPO. The Webtoon business is simultaneously NAVER's highest-potential and highest-risk asset. Revenue for fiscal 2025 reached 1.38 billion dollars but growth was modest at two and a half percent, and the company reported a net loss of 373 million dollars, driven primarily by goodwill impairments related to the Wattpad acquisition.

The bull case for Webtoon is the Disney analogy. Webtoon is the world's largest platform for digital comics, with a massive library of original IP that can be adapted into dramas, films, and animated series across global markets. A partnership expansion with Disney announced in 2025, which included Disney acquiring a two percent equity interest, triggered a forty-two percent single-day stock surge and illustrated the market's excitement about Webtoon's content licensing potential. The bear case is that the path from "largest comic platform" to "globally monetized IP powerhouse" is long, uncertain, and capital-intensive.

What makes NAVER's segment architecture distinctive is the degree of cross-pollination. Search drives commerce. Commerce drives fintech. Fintech generates data that improves search. Cloud provides the AI infrastructure that enhances all of the above. And content drives engagement that keeps users within the NAVER ecosystem rather than drifting to YouTube, TikTok, or Google. Each segment is defensible individually, but the real moat is the system.

VIII. Current Management: The "Choi-Kim" Era

In March 2025, Lee Hae-jin returned to NAVER's board of directors as chairman after a seven-year absence. The move surprised some observers, who had expected the founder to continue his gradual withdrawal from the company's formal governance structures. But Lee's return was not a step backward. It was a strategic repositioning. He resigned his role as Global Investment Officer to focus specifically on NAVER's sovereign AI strategy, the area he believed would determine the company's competitive position for the next decade.

Lee Hae-jin at sixty is a different figure than the quiet engineer who built Web Glider at Samsung SDS. He is widely regarded as one of the most influential technology figures in Korean history, and his return to the board sent a clear signal to both employees and investors: the AI transition is too important to delegate.

The day-to-day leadership of NAVER, however, rests with CEO Choi Soo-yeon, who was approved for a second term at the same March 2025 annual general meeting. Choi represents a generational and stylistic shift from the founder era. A former lawyer and M&A specialist, she rose through NAVER's corporate development organization, where she helped structure many of the international acquisitions that now define the company's global footprint. Fortune Asia named her to its 2025 Most Powerful Women list, recognizing her role in transforming NAVER from a Korean internet portal into a multinational platform company.

Choi's leadership style is analytical, governance-focused, and explicitly global in orientation. Where Lee Hae-jin built NAVER through engineering intuition and product vision, Choi is building the next phase through disciplined capital allocation, portfolio management, and an emphasis on corporate governance standards that meet global institutional investor expectations. She speaks fluently about shareholder returns, capital efficiency, and ESG metrics in a way that would have been unusual for a Korean tech CEO a decade ago.

Kim Nam-sun, who served as CFO before moving to his current role as President of Investments, oversees NAVER Ventures, the company's Silicon Valley venture arm, and the broader portfolio of international investments. Kim's background in M&A, having risen from head of mergers and acquisitions to SVP before becoming CFO in 2021, makes him the natural steward of NAVER's global acquisition strategy.

The compensation structure at NAVER has undergone significant modernization under this leadership team. The company has moved aggressively toward restricted stock units and performance-linked compensation, aligning with global tech industry standards and moving away from the traditional Korean corporate pay model that emphasized seniority over results. This shift is not merely cosmetic. It affects who NAVER can recruit, particularly in the brutally competitive global AI talent market, and it signals to international investors that the company's governance is converging with Western best practices.

The shareholder structure creates an unusual governance dynamic. Lee Hae-jin's personal stake in NAVER is approximately two and a half percent, far below the controlling positions held by founders at many Korean and global tech companies. The largest single shareholder is the National Pension Service of Korea, which holds approximately nine and a quarter percent and has been steadily increasing its position. Foreign investors collectively own nearly forty-eight percent of shares outstanding, with BlackRock at six and a half percent and Vanguard at three and a half percent. The company maintains a one-share-one-vote structure with no dual-class shares or founder super-voting rights.

This creates what some governance experts have called a "glass house" structure. No single shareholder has control. The founder has influence through his chairman role but lacks the ownership to act unilaterally. The National Pension Service, as the largest holder, has the weight to influence board composition and strategic direction but operates under a fiduciary mandate to maximize returns for Korean pensioners, not to pursue any particular industrial policy. And foreign institutional investors, who collectively hold the largest block, bring the expectations and governance standards of global capital markets.

For investors, the management transition raises a fundamental question: can a company that was built on the instincts of a visionary founder sustain its competitive advantage under professional managers? The early evidence under Choi and Kim has been encouraging. Revenue growth has accelerated, margins have stabilized, and the international portfolio is beginning to cohere. But the true test will come as AI reshapes the competitive landscape and the LY Corp situation demands resolution.

IX. Analysis: Strategic Frameworks

To understand NAVER's competitive position rigorously, it helps to examine the company through two established strategic frameworks: Hamilton Helmer's Seven Powers and Michael Porter's Five Forces.

Starting with Helmer's framework, NAVER possesses at least three distinct powers, each operating in a different part of the business.

The first is network effects, which operate most powerfully in LINE and Webtoon. LINE's value increases with every user who joins, because each new user expands the network of people you can message. In Japan, where LINE has achieved near-universal adoption among smartphone users, this network effect has reached a density that makes switching to a competitor practically inconceivable. You cannot leave LINE without leaving your social graph. Webtoon exhibits a different flavor of network effect, a two-sided marketplace dynamic between creators and readers. More readers attract more creators, who produce more content, which attracts more readers. This creator-reader flywheel has made Webtoon the default platform for digital comics globally.

The second power is switching costs, and this is where NAVER's walled garden strategy pays its highest dividends. A Korean user who has invested years in the NAVER ecosystem has a blog on Naver Blog, years of Q&A history on Knowledge iN, communities on Naver Cafe, a payments history on Naver Pay, a shopping membership through Naver Plus, email on Naver Mail, and cloud storage on Naver Cloud. Every one of these services is tied to a single NAVER ID. The aggregate switching cost is enormous, not because any individual service is irreplaceable, but because the totality of the digital life stored within NAVER's walls is practically impossible to recreate elsewhere.

The third and perhaps most strategically significant power is what Helmer calls a "cornered resource." In NAVER's case, that resource is the Korean language itself, or more precisely, the corpus of Korean-language data that NAVER has accumulated over a quarter century. HyperCLOVA X, NAVER's large language model, was trained on sixty-five hundred times more Korean-language data than GPT-4. On the KMMLU benchmark, a standardized test of Korean-language knowledge and reasoning, HyperCLOVA X outperforms GPT-4. The most recent iteration, HyperCLOVA X Think, released in 2025, scored forty-eight point nine on the KoBALT-700 benchmark, compared to thirty-three for Exaone Deep and thirty-two point four for QwQ-32B.

These are not abstract technical comparisons. They have direct commercial implications. When a Korean business wants to deploy an AI assistant that can understand Korean regulatory filings, Korean medical records, Korean legal precedents, or Korean customer service conversations, HyperCLOVA X is measurably superior to any foreign alternative. NAVER has translated this advantage into concrete deployments, most notably BOKI, the Bank of Korea Intelligence system launched in January 2026. BOKI is described as the world's first central bank sovereign AI service, developed over eighteen months in partnership with Korea's central bank. When your nation's central bank trusts your AI model with its data, that is a cornered resource.

Now, applying Porter's Five Forces, the picture is more complex and less uniformly favorable.

The threat of substitutes is high and growing. YouTube and TikTok are increasingly where younger Koreans go to "search" for information, particularly product reviews, restaurant recommendations, and how-to content. This is not unique to Korea; it is a global phenomenon. But in a market where NAVER has historically captured the vast majority of search intent, the erosion of search queries to video platforms represents a structural challenge that AI integration alone may not fully address.

The intensity of rivalry is arguably NAVER's most pressing competitive concern. Kakao, NAVER's fierce domestic rival, competes in virtually every segment: messaging (KakaoTalk dominates Korean messaging), payments (KakaoPay), banking (KakaoBank), mobility (Kakao T), content, and search (through its ownership of Daum). While Kakao has stumbled recently, suffering three consecutive quarters of revenue decline through the first quarter of 2025, it remains a well-funded, aggressive competitor with deep consumer penetration. Google, meanwhile, continues to invest in Korean-language capabilities and has the resources to be patient. And in the AI era, global players like OpenAI and Microsoft represent a new class of potential competitors who could disrupt the search and cloud businesses simultaneously.

The bargaining power of suppliers is moderate. NAVER depends on semiconductor manufacturers for AI training chips, cloud infrastructure providers for supplemental capacity, and content creators for the Webtoon and Knowledge iN ecosystems. The global AI chip shortage has given suppliers like NVIDIA significant pricing power, though NAVER has partially mitigated this through its own cloud infrastructure investments.

The bargaining power of buyers is relatively low in search and content, where NAVER's scale creates few alternatives for Korean advertisers and content consumers, but higher in commerce, where merchants can distribute through multiple platforms and consumers can easily price-compare.

The threat of new entrants is moderate domestically but higher internationally. Within Korea, the regulatory environment, the network effects of existing platforms, and the Korean-language data moat create significant barriers to entry. Internationally, however, NAVER's acquisitions (Poshmark, Wallapop, Wattpad) compete in markets where barriers are lower and incumbents are strong.

X. The LINE Yahoo (LY Corp) Crisis (2024)

In the autumn of 2023, what appeared to be a routine cybersecurity incident escalated into the most significant geopolitical crisis in NAVER's corporate history. Approximately five hundred and ten thousand pieces of personal information, belonging to LINE users, business partners, and employees, were leaked through a breach that traced back to a subcontractor of Naver Cloud, the infrastructure provider for LINE's Japanese operations.

To understand why this breach became a crisis rather than merely an incident, some structural context is necessary. In October 2023, Line Corporation and Yahoo Japan had merged to form LY Corporation, owned by A Holdings, a fifty-fifty joint venture between NAVER and SoftBank. This structure meant that NAVER effectively co-controlled one of Japan's most important digital infrastructure platforms. LINE was not just a messaging app in Japan. It was the communication backbone for millions of businesses, the payment platform for millions of consumers, and increasingly, a gateway for government services.

Japan's Ministry of Internal Affairs and Communications responded to the breach with unusual force, demanding that LY Corporation restructure its ownership to reduce NAVER's influence. The ministry's argument was that the fifty-fifty control structure left LINE's infrastructure vulnerable because critical systems were managed through NAVER's Korean cloud services. The implicit message was less subtle: Japan wanted its critical digital infrastructure under Japanese control.

SoftBank CEO Junichi Miyakawa confirmed in May 2024 that negotiations with NAVER over control of LY Corp were underway. The discussions centered on whether NAVER would reduce or sell its stake in the joint venture, effectively ceding control of LINE to SoftBank and Japanese interests. LY Corporation CEO Takeshi Idezawa committed to dissolving the technical relationship with Naver Cloud and achieving full technological independence by March 2026, a deadline that is now imminent.

NAVER CEO Choi Soo-yeon stated publicly that NAVER would not sell its LY Corp stake in the "short term," a carefully calibrated statement that preserved optionality without committing to a permanent position. The South Korean government weighed in, with officials publicly vowing to protect Korean companies operating abroad and calling for "fair treatment," framing the situation as a matter of national economic sovereignty.

As of March 2026, no final resolution on a complete stake sale has been announced. The technical separation is approaching its deadline, and negotiations continue. In August 2024, A Holdings had planned to reduce its ownership percentage through a LY Corp share buyback of one hundred and fifty billion yen, with LY repurchasing up to five percent of outstanding shares to meet the Tokyo Stock Exchange Prime Section's thirty-five percent free-float requirement.

The stakes could hardly be higher. If NAVER loses control of or divests from LINE Japan, it loses its largest international asset, its bridge to the Japanese market, and a significant portion of its global narrative. LINE is not just a revenue line item. It is the proof that NAVER can build and operate a dominant platform outside Korea. Without it, the "global NAVER" story becomes significantly harder to tell.

At the same time, the LY Corp situation illustrates a risk that few technology investors adequately price: the geopolitical vulnerability of cross-border digital infrastructure. In an era where governments from Washington to Brussels to Tokyo are increasingly asserting sovereignty over their digital ecosystems, owning critical infrastructure in a foreign country creates exposures that no amount of product excellence can eliminate.

XI. The Sovereign AI Bet and Lessons for the Playbook

In August 2025, South Korea's Ministry of Science and ICT selected five consortia for its "AI for Everyone" sovereign AI project, backed by three hundred and eighty-one million dollars in government funding. NAVER was among the five, alongside SK Telecom, LG Group, NCSoft, and Upstage. Lee Hae-jin's return to NAVER's board as chairman was explicitly motivated by his desire to lead the company's sovereign AI push, and the government's selection validated the strategic bet.

Sovereign AI is a concept that deserves unpacking, because it is central to NAVER's competitive thesis for the next decade. The basic idea is simple: nations want AI systems that are trained on their own data, optimized for their own languages, and operated within their own borders. The motivation is partly practical, Korean-language AI simply works better when it is trained on Korean data, and partly geopolitical, governments are increasingly uncomfortable with the idea that their citizens' data flows through American cloud infrastructure to train American AI models.

NAVER's position in sovereign AI is remarkably strong. The company has spent twenty-five years accumulating the largest corpus of Korean-language content in existence: every Knowledge iN question and answer, every Naver Blog post, every Naver Cafe discussion, every news article, every product review, every shopping query. This data, combined with the company's own cloud infrastructure, gives NAVER a structural advantage in Korean-language AI that would take any foreign competitor years and billions of dollars to approximate.

The BOKI deployment with the Bank of Korea is the most visible manifestation of this strategy, but it extends far deeper. Korean enterprises across healthcare, finance, legal services, and government are increasingly choosing NAVER Cloud and HyperCLOVA X not because they are cheaper than AWS or Azure, but because they offer Korean-language performance that no foreign alternative can match, with data residency guarantees that no foreign provider can credibly offer.

Looking at NAVER's history through the lens of strategic lessons, several patterns emerge that are instructive for both founders and investors.

The first is counter-positioning. NAVER beat Google in Korea not by being a better Google, but by doing what Google refused to do. Google's philosophy was to organize the existing web. NAVER's philosophy was to create the web. Knowledge iN, Naver Blog, Naver Cafe: these were not search features. They were content creation platforms that happened to feed a search engine. Google could have built similar products, but doing so would have contradicted its core belief that the search engine should be a neutral organizer of information, not a creator of it. This philosophical difference gave NAVER a structural advantage that persisted for over two decades.

The second pattern is what might be called the "spin-off culture." NAVER has demonstrated a repeatable ability to incubate businesses internally, nurture them to scale within the "Company-in-Company" structure, and then separate them when independence would unlock more value than integration. Gaming became NHN Entertainment. LINE became Line Corporation, then part of LY Corp. Webtoon became Webtoon Entertainment and IPO'd on Nasdaq. Each separation was executed at a moment when the subsidiary's growth trajectory justified standalone valuation, and each time, the parent company retained a significant ownership stake that preserved its economic interest while giving the subsidiary the autonomy to compete.

The third pattern is adaptability. Over its twenty-seven-year history, NAVER has transitioned from search to gaming to search-plus-content to mobile messaging to commerce to fintech to AI. Each transition involved substantial risk, significant capital deployment, and the organizational willingness to cannibalize existing revenue streams. The company that generates twelve trillion won in annual revenue today looks almost nothing like the search engine that launched from Samsung SDS in 1999, and that is precisely the point.

XII. What to Watch: KPIs, Cases, and the Road Ahead

For investors tracking NAVER's ongoing performance, three metrics matter most.

The first is domestic search market share. NAVER's share rose from fifty-eight percent in 2024 to nearly sixty-three percent in 2025, a move in the right direction. But this metric is under structural pressure from video platforms and AI-native search experiences. If NAVER's search share begins declining, it signals erosion of the core moat that funds everything else.

The second is commerce gross merchandise volume growth, particularly through the Naver Plus membership program. Commerce surged thirty-six percent year over year in the fourth quarter of 2025. The trajectory of this business, more than search, will determine whether NAVER can sustain double-digit revenue growth as the search business matures.

The bull case for NAVER rests on three pillars. First, the company owns an unparalleled Korean-language data moat that becomes more valuable, not less, as AI transforms every industry. Second, the Webtoon and Wattpad content libraries represent a globally scalable IP portfolio at a time when the entertainment industry is desperate for proven content. The Disney partnership validates this thesis. Third, the commerce and fintech businesses are growing at rates that suggest NAVER can diversify its revenue base before search maturity becomes a binding constraint.

The bear case is equally compelling. South Korea's demographic trajectory is among the most challenging in the world, with a fertility rate that has fallen below one child per woman, putting a hard ceiling on the domestic user base that generates the majority of NAVER's revenue. The LY Corp situation could result in the loss of NAVER's most important international asset. International acquisitions like Poshmark and Wallapop remain unproven and require years of investment before they contribute meaningfully to earnings. And the competitive environment is intensifying, with Kakao, Google, and AI-native challengers all vying for the same Korean consumers.

One material legal and regulatory overhang deserves explicit mention: the LY Corp technology separation deadline of March 2026 is imminent as of this writing, and the outcome of NAVER's negotiations with SoftBank over the ownership structure will have significant implications for NAVER's revenue, earnings, and strategic narrative. Investors should monitor developments closely.

NAVER Corporation is, in the end, a company defined by its contradictions. It is a local champion with global ambitions. A search engine that builds content rather than indexing it. A technology company run by a lawyer. A founder-inspired culture governed by institutional shareholders. These contradictions are not weaknesses. They are the source of the strategic complexity that has allowed NAVER to thrive in a market where simpler companies have been crushed. The question is whether that complexity can scale beyond Korea's borders, or whether the navigator will always find its way back home.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube