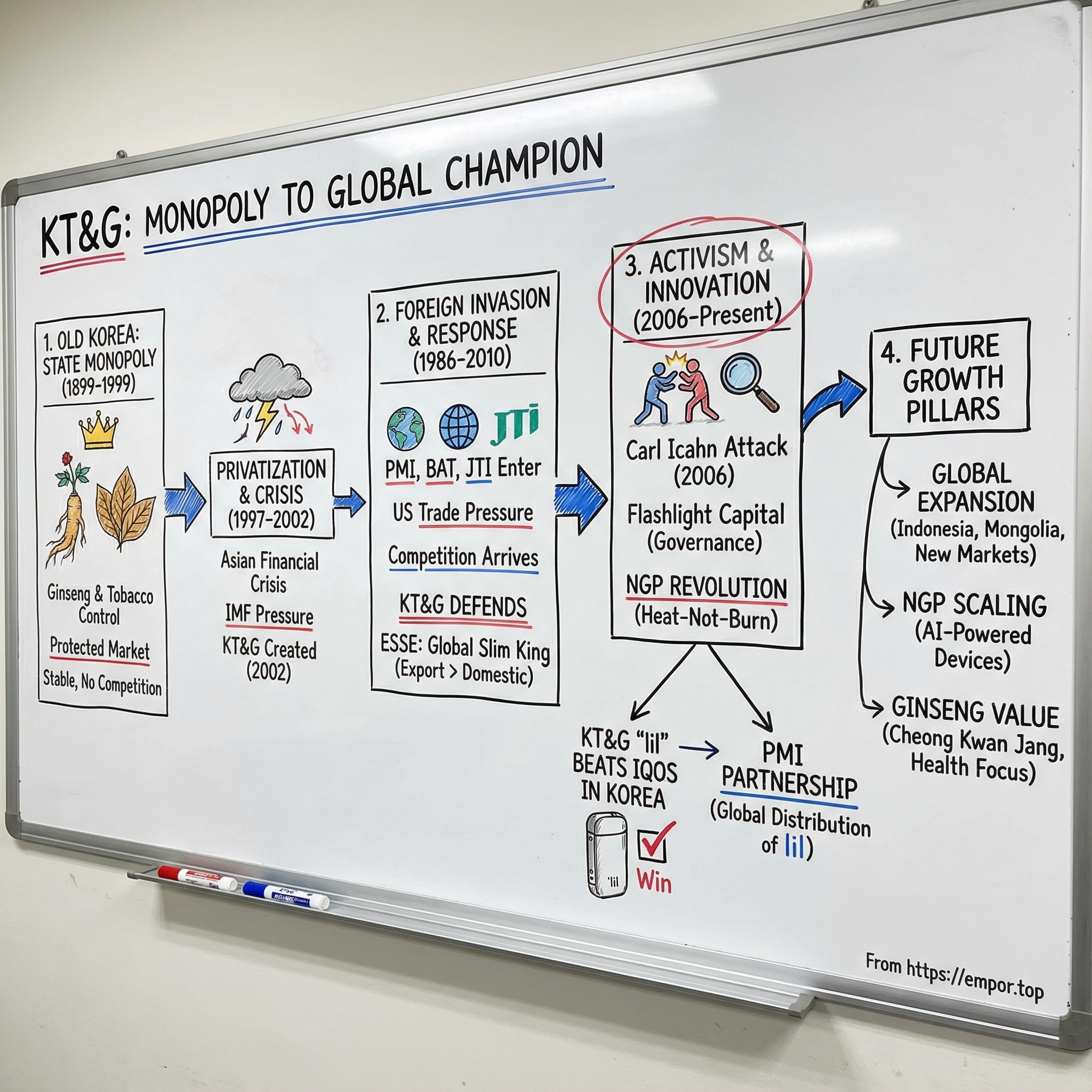

KT&G: From State Monopoly to Global Tobacco Challenger

I. Introduction & Episode Roadmap

Picture the boardroom of a sleepy government monopoly in Seoul in 1999. Outside, the Asian financial crisis is still ripping through the economy. Inside, a different kind of emergency is taking shape.

For nearly a century, this company has never really had to compete. It has been the default tobacco supplier to a nation of heavy smokers, protected by the state, insulated from global brands, and built for stability, not speed. Now the world is changing fast—and for the first time, the people running Korea’s tobacco champion have to ask a question that would’ve sounded absurd a decade earlier: can we survive in an open market, let alone win on a global stage against Philip Morris?

Meet KT&G. The name started as Korea Tobacco & Ginseng and later came to mean Korea Tomorrow & Global. Today, it’s the leading tobacco company in South Korea, with annual sales of over US$4 billion. But the numbers aren’t the story. The story is the transformation.

Because KT&G didn’t just modernize. It went from a government-owned monopoly to a privatized, publicly traded company competing head-to-head with Philip Morris International, British American Tobacco, and Japan Tobacco. It went from banning foreign cigarettes in Korea to fighting foreign giants on equal footing—and then expanding abroad.

So here’s the question that drives everything: how did a company that once made it illegal for Koreans to smoke foreign brands evolve into the world’s fifth-largest tobacco company?

We’ll trace that arc through four big themes that show up far beyond tobacco: privatization as the spark, defending home turf while going global, activist investors as unlikely catalysts, and the pivot to Next Generation Products. And then there’s the twist that makes KT&G’s story genuinely one-of-a-kind: in heated tobacco, South Korea is the only market where Philip Morris lost leadership to a local rival. KT&G’s lil took the top spot, and it has held on—reaching a 48.5 percent share.

And after all that? KT&G turned around and partnered with Philip Morris to distribute lil globally. In this industry, that’s almost unheard of.

II. Origins: The Monopoly Era (1899–1987)

The Imperial Roots

This story starts not with a cigarette, but with a root.

At the end of the Korean Empire, the royal government looked around and saw two categories of products: the ones you let markets fight over, and the ones you lock down because they’re simply too important. In 1899, it chose the second path, creating the Ginseng Management Division under the royal government. Korean red ginseng—prized across Asia for centuries for its perceived medicinal value—became a crown-controlled monopoly.

Less than a decade later, in 1908, that ginseng division moved under the Ministry of Finance. And with it came something else the state couldn’t resist controlling: tobacco. The pairing made perfect sense. Tobacco was dependable revenue. Ginseng was national identity. Together, they were fiscal policy you could grow, process, and tax.

After the Korean War, the government doubled down on centralization. In 1952, it created the Office of Monopoly, consolidating control over both ginseng and tobacco. This wasn’t a company in the modern sense. It was an instrument of the state, designed to secure revenue and help bankroll reconstruction.

The Logic of State Control

To understand why Korea held tobacco so tightly, you have to understand the country it was trying to build. In the decades after the war, South Korea ran an export-led development playbook: guard domestic industries, conserve foreign currency, and pick the sectors that would fund growth.

That logic reached all the way into people’s ashtrays. Throughout the 1980s, the government restricted entry for foreign cigarette companies. The idea was to avoid spending foreign exchange on imports or royalties—and to protect a domestic industry the state considered strategic. Opposing foreign investment in tobacco wasn’t an exception; it was the rule.

Inside Korea, the Office of Monopoly controlled everything: manufacturing, distribution, and sales. The system created a perfectly protected business—one with captive demand and no meaningful rivals.

And demand was enormous. By 1980, adult male smoking prevalence in South Korea hit 79.3%, the highest in the world. Every one of those smokers belonged, by default, to the monopoly. It was zero competition and guaranteed profits—and with that, very little pressure to innovate.

By 1987, the domestic market ranked 12th globally, with production reaching 81 billion sticks a year. The Office of Monopoly had built a fortress.

But the real question wasn’t how strong the fortress was. It was how long the walls could hold—because the pressure that would crack them wasn’t coming from within Korea. It was coming from across the Pacific.

III. Market Opening & The Foreign Invasion (1986–1999)

The U.S. Trade Pressure Bomb

The 1980s brought a reckoning, and it didn’t start in Seoul. It started in Washington.

American trade policy in the Reagan era was on a mission to pry open protected markets across Asia. And for Korea’s tobacco monopoly, the weapon of choice was Section 301 of the U.S. Trade Act—a blunt instrument that could bring real consequences if Korea didn’t play along.

In 1986, South Korea “opened” its cigarette market to foreign brands for the first time. But the opening was carefully rationed. The Korean government agreed that the Office of Monopoly would regularly buy a fixed amount of U.S.-made cigarettes—roughly 1% of the total market—starting in July 1986. The ban on public sales of imported cigarettes was lifted, meaning Koreans could finally buy foreign brands legally.

On paper, U.S.-based transnational tobacco companies now had a foothold. In reality, it was tiny. Despite the access promised, imported cigarettes accounted for just 0.06% of retail sales in the first year. The foreign companies argued that tariffs and other barriers still made the market effectively closed.

So they escalated.

Back in 1981, RJ Reynolds, Brown & Williamson (British American Tobacco’s U.S. subsidiary), and Philip Morris had formed the U.S. Cigarette Export Association. The USCEA lobbied the U.S. Trade Representative to pressure Asian governments into opening their markets. In Korea, after failing to secure joint ventures with the monopoly—and eyeing the marketing spotlight of the upcoming 1988 Seoul Summer Olympics—they accused the country of “discriminatory trade practices.”

The threat worked. Full liberalization arrived in 1988, landing right as the Olympics put Korea on the world stage.

The TTC Invasion

Once the gates were fully open, the transnational tobacco companies poured in with a playbook the monopoly had never faced: sophisticated marketing, massive advertising budgets, and brands positioned as modern, global, aspirational.

The monopoly’s initial response was defensive and distinctly Korean. It leaned on nationalism—buy domestic, support the home team—and it worked its relationships with the country’s sprawling network of standalone cigarette retailers, which controlled the vast majority of retail sales. Foreign brands were also far more expensive, which bought KT&G time.

But time was all it bought.

By the mid-1990s, the foreign players had found their footing. Through relentless marketing campaigns, growing acceptance of imported brands among younger smokers, deeper penetration into sales and distribution, and well-timed corporate social responsibility efforts, they steadily took share. Their combined market share rose from 2.9% in 1990 to 12.4% by 1995.

A cultural split formed in real time. Older Korean men tended to stay loyal to domestic brands, often out of habit and national pride. Younger smokers—especially in cities, and especially among groups more attuned to global trends—were far more willing to experiment. Philip Morris and BAT didn’t just show up; they showed up knowing exactly who to target.

The Wake-Up Call

The monopoly could now see the trajectory: a fall from essentially total control before the late 1980s to less than half the market by 2014. Inside the company, the erosion would be described as its “greatest challenge.”

And worse, the overall market was starting to contract. Smoking among Korean adult men fell sharply over time, dropping from 79.3% in 1980 to 40.4% by 2008 as health awareness rose.

So KT&G wasn’t just losing share. It was losing share in a market that was itself shrinking. The old model—protected, predictable, and slow—was no longer survivable. Something had to give.

IV. The Asian Financial Crisis & Privatization (1997–2002)

The Crisis That Changed Everything

If the 1980s were about foreign pressure, the late 1990s were about survival.

South Korea was among the countries hit hardest by the Asian financial crisis that began in 1997. After years of rapid growth fueled by easy credit, the unwind was brutal: stock prices plunged, the won weakened, major conglomerates went bankrupt, and the country’s debt burden surged—national debt-to-GDP more than doubling from 13% to 30%. By 1998, South Korea faced about US$74 billion in short-term debt coming due within two years. The government had a cash problem, fast.

The IMF bailout brought money, but it also brought conditions. One of the biggest: privatize state-owned enterprises. And suddenly the tobacco monopoly—an institution that had reliably sent cash into government coffers for nearly a century—started to look like something else entirely: a one-time, high-value asset that could be sold.

That’s when the privatization of what would become KT&G truly began.

The Privatization Playbook

KT&G didn’t flip from monopoly to modern public company overnight. The transition came in steps—and each step rewired the business.

First, Korea Tobacco & Ginseng restructured itself as a joint-stock company in 1997, a foundational move that made public ownership possible. Next came the split that clarified the story: in 1999, the company spun off its ginseng operations—already weakened by the loss of its monopoly in 1996—into a separate entity, Korea Ginseng Corporation. Crucially, Korea Ginseng stayed a wholly owned subsidiary.

Then came the public markets. Korea Tobacco & Ginseng listed on the Korea Stock Exchange at the end of 1999, and the offering drew enormous demand—11.6 trillion won in subscription margin, a national record at the time that would stand for more than a decade, until Samsung Life Insurance surpassed it in 2010. As part of the listing, the government agreed to let foreign corporations own up to 25 percent of the company. After decades of defending Korea from foreign tobacco influence, the former monopoly was now inviting foreign capital into its own cap table.

Inside the company, privatization wasn’t just a financial event—it was an operational one. The restructuring was deep and painful. KT&G’s early global strategy focused on strengthening the domestic manufacturing base, and that meant cutting costs hard: headcount fell from 9,000 employees in 1996 to around 5,000 by 2000, and some of the least efficient factories were shut down.

By 2001, the tobacco monopoly was officially over. In 2002, Korean Tobacco was fully privatized—and it took on its new name: KT&G.

The New Identity

The rebrand wasn’t just a new logo on the same machine. It was a declaration of what the company wanted to become.

Given the business, you might assume KT&G stood for Korea Tobacco & Ginseng. Officially, it didn’t. It stood for Korea Tomorrow & Global.

Chairman and CEO Joo Young Kwak put the moment in plain language: “The disposal of our remaining publicly held shares and the official renaming of the company as KT&G marked the beginning of a new era of the company. We are now prepared to forge ahead and transform KT&G into a leading player in the tobacco industry.”

And then KT&G did what privatized companies are forced to do when competitors are already inside the walls: it started building products meant to win, not just exist. By the end of 2002, the company had rolled out a wave of premium brands designed to take on imports head-to-head—Seasons, Humming Time, Lumen, Esse Lights, and the ultra low-tar Raison.

V. The Esse Phenomenon & Export Strategy (1996–2010)

Building a Global Brand

If KT&G’s survival depended on defending Korea, its growth depended on getting out of Korea. And it found its spearhead in a brand that started as a niche play and turned into the company’s crown jewel: Esse.

Esse launched in November 1996. Decades later, it had become the largest ultra-slim cigarette brand in the world. In 2023 alone, Esse sold 50.8 billion sticks—about 21.9 billion in Korea and 28.9 billion overseas. Even more telling: since 2015, Esse’s overseas sales have exceeded its domestic sales. The export engine had become the main engine.

That global push began in earnest in 2001, when Esse expanded into the Middle East and Russia. From there, the map just kept filling in—eventually reaching 90 markets, including Indonesia, Latin America, and Africa.

And the ramp was dramatic. Esse exports started in 2001 at just 6 million cigarettes. By 2006, they had reached 10 billion sticks—about 35% of KT&G’s total exports at the time. By 2011, Esse exports hit 20 billion sticks. As the company’s best-selling brand at home and abroad, Esse’s cumulative sales reached 394.1 billion sticks by 2012, including 140 billion sticks sold across 45 export markets.

The Ultra-Slim Niche

Esse didn’t win by trying to be everything to everyone. It won by owning a format.

KT&G leaned into ultra-slim cigarettes: a slim design, an ultra low-tar profile (1mg), and product innovation like odor reduction, paired with a steady expansion of taste options. Esse now accounts for about one-third of global ultra-slim cigarette sales—an astonishing share for a category that spans the world.

The appeal was specific and powerful. Ultra-slims attracted female smokers in many markets, health-conscious consumers drawn to “lower-tar” positioning, and style-driven buyers who responded to sleek packaging and an upscale image. KT&G treated Esse as a premium brand, and that premium positioning traveled well.

Over time, the company kept refreshing the line. In 2013, KT&G introduced ESSE Change, described as the world’s first superslim capsule product, where users could crush a capsule in the filter to shift the flavor. In 2017, it launched ESSE Change Slim, 0.7mm thinner than existing slim products. And in 2019 came ESSE Himalaya, featuring odor reduction technology built on KT&G’s proprietary Triple Care System.

Overseas Manufacturing Footprint

Of course, exporting cigarettes across continents comes with a tax: transportation costs, tariffs, and local-market friction that can quietly eat margins.

So KT&G started moving manufacturing closer to demand. In 2008, it completed a plant in Turkey with “ultra-modern” facilities and an annual capacity of 2.6 billion sticks, producing super-slim and regular cigarettes for local consumption and regional export.

Then in 2010, KT&G built a third plant in Russia to manage operations more directly in a key market. The facility, a 103,421-square-meter complex in the Kaluga region near Moscow, included tobacco leaf processing and ultra-slim production lines. With annual capacity of 4.6 billion sticks, it produced Esse Blue, Esse One, and Esse Menthol for Russia and the Commonwealth of Independent States.

VI. The Carl Icahn Attack (2006)

The Hostile Bid

By 2006, KT&G had done the hard part: it had survived privatization, rebuilt itself for competition, and was throwing off the kind of cash flow that makes financiers pay attention. It also had a balance sheet full of tempting “extras”—valuable real estate, and a ginseng subsidiary that didn’t fit the classic tobacco pure-play story.

To Carl Icahn, this wasn’t a Korean national champion. It was a value-unlocking puzzle.

That year, the American activist investor launched an unsolicited takeover bid for KT&G alongside Warren Lichtenstein, founder and CEO of Steel Partners. The bid ultimately went nowhere. But the point of an Icahn campaign isn’t always to buy the company—it’s to force a reaction. And in this case, it worked: KT&G pledged up to $2.9 billion in shareholder returns by 2008, a commitment that created substantial gains for the activists and put management on notice.

The move made headlines across Korea, and it sparked a backlash in some quarters: a foreign “corporate raider” targeting a company that had only recently been a state asset was bound to trigger nerves. Icahn and Steel Partners built a combined stake of 6.72% and pushed hard for a spin-off of Korea Ginseng Corporation, arguing the value wasn’t being reflected in KT&G’s share price. Icahn even floated the idea of taking over the entire company.

Then came the symbolic win. In March, Icahn’s camp secured a board seat in a shareholder vote—the first time a foreign investor had been voted onto a Korean board against management’s wishes.

The Icahn Playbook in Korea

This was classic Icahn: buy a meaningful stake, show up with a list, and use public pressure to make it expensive for management to ignore you.

His demands were familiar to anyone who’d watched his campaigns elsewhere: sell non-core assets, spin off and list Korea Ginseng Corporation, restructure KT&G’s real estate portfolio, lift dividends to look more like global tobacco peers, and buy back shares.

At the shareholder meeting, the foreign investor group won one seat and warned they’d use it to push aggressively for change. It wasn’t the sweep they wanted—they had hoped for two seats on KT&G’s 12-member board, after nominating three candidates for two outside-director slots—but it was enough to turn the fight into a national conversation.

In a market where corporate decisions were often dominated by entrenched power—especially in and around chaebol culture—this kind of activist challenge was still new. KT&G’s showdown with Icahn helped drag corporate governance and hedge fund activism into the Korean mainstream.

The Exit

Not long after, the endgame arrived in familiar fashion: Icahn took the money and left.

KT&G shares slid when news broke that he was selling out. According to sources familiar with the deal, Icahn sold 7 million shares at 60,700 won per share—a 3.8% discount to the prior close—valuing the sale at 424.9 billion won ($458 million). The exit was widely expected once KT&G had committed to returning up to $2.9 billion to shareholders under pressure from Icahn and his then-ally, Lichtenstein.

The takeaway was straightforward, and it would echo years later. Activists could force capital discipline fast. But KT&G also showed it could defend itself—by meeting investors partway with shareholder-friendly moves, while keeping strategic control. The company walked away with a sharper focus on returns, better governance, and a playbook for the next activist battle that would inevitably come.

VII. The NGP Revolution & The Lil Story (2015–Present)

The Heat-Not-Burn Wave

The tobacco industry’s biggest disruption arrived in the mid-2010s: heated tobacco, or “heat-not-burn.” Philip Morris International brought its IQOS device to Korea in June 2017, betting that Korean consumers—fast adopters of new tech and increasingly interested in “reduced smell” alternatives—would move quickly.

PMI was right about the direction of the market. Korean smokers embraced heated tobacco at speed. What PMI got wrong was assuming it would have the category to itself.

KT&G had been working for years on its own answer. In November 2017, it launched lil 1.0—its first heat-not-burn device. The name was built around a simple marketing line: “a little is a lot,” meant to signal less smoke and smell without giving up the tobacco experience.

And KT&G didn’t just ship a device. It shipped a product designed to win in its home market: priced to compete, built for convenience, and paired with Fiit tobacco sticks in a wider range of flavors. One practical advantage stood out immediately to users: lil allowed consecutive use without the forced pause that early IQOS models required.

Beating IQOS at Home

What happened next caught the industry off guard. KT&G didn’t merely hold its ground—it took the lead.

“Since taking the top position in the HNB cigarette market in February, we have been able to retain our position,” said Lim Wang-seob, chief of KT&G’s NGP Business Division. KT&G’s lil went on to command a 48.5 percent share of South Korea’s heated tobacco market.

By then, the “new tobacco” category in Korea had effectively become a heated-tobacco category. In government statistics and market reporting, lil sat at roughly 48% share, with PMI around 42% via IQOS and BAT about 10% with its Glo line.

The headline mattered far beyond Korea: South Korea became the only market where Philip Morris lost heated-tobacco leadership to a local competitor. KT&G proved that even against a global giant with a first-mover advantage, a domestic incumbent—armed with distribution, speed, and a feel for local preferences—could still win.

The PMI Partnership Twist

And then KT&G did something almost no one saw coming: it partnered with the rival it had just beaten.

In January 2020, KT&G signed an agreement with PMI to distribute lil outside South Korea—plugging KT&G’s device into PMI’s global sales machine. Then, on January 30, 2023, the relationship deepened into a new long-term deal: a 15-year agreement to expand KT&G’s next generation products overseas.

The structure was designed to last, but not to drift. The partnership runs from January 30, 2023 through January 29, 2038, with performance reviews every three years to adapt to changing market conditions.

It also wasn’t theoretical. By that point, PMI said it had already commercialized KT&G-developed products in more than 30 markets over three years of collaboration.

The logic was clean on both sides. KT&G got reach—instant access to a distribution network it would have taken decades to replicate. PMI got options: a broader lineup of innovative products, including offerings that could work in more price-sensitive and middle-income markets, and a hedge against a world where IQOS wouldn’t always be the unchallenged leader.

AI-Powered Innovation

Meanwhile, KT&G kept iterating at home. It unveiled the Lil Aible series—heat-not-burn devices equipped with what the company described as artificial intelligence features aimed at maintaining leadership in Korea’s growing e-cigarette market.

The lineup included two models, Lil Aible and Lil Aible Premium. The device came in four colors and included three “Smart AIs”—preheating AI, puff AI, and charging AI—designed to optimize heating temperature, estimate remaining puffs, and track battery status.

KT&G positioned Lil Aible as unusually flexible: one device could be used with three different tobacco sticks. Like the earlier model, it offered automatic heating, a self-cleaning system, and up to three consecutive uses. It launched in two versions—an original model priced at KRW110,000, and a premium model priced at KRW200,000, adding an OLED touchscreen for easier control of device functions.

VIII. The Flashlight Capital Battle & Modern Activism (2022–2025)

The New Activist Wave

If Carl Icahn was KT&G’s first taste of shareholder activism, Flashlight Capital Partners has been the next evolution: less of a headline-grabbing raid, more of a sustained campaign—tighter on governance, sharper on disclosure, and relentless about what it sees as trapped value.

Flashlight, a Singapore-based activist fund, moved the fight into the courts. It filed injunctions against KT&G seeking disclosure on three pressure points: how profitable the company’s export business really is, the details of its global distribution arrangements with Philip Morris International, and roughly $19 million it said was recorded as consulting fees.

Flashlight isn’t a faceless vehicle, either. The firm was founded by Sanghyun Lee, formerly the Carlyle Group’s head of Korea. It positions itself as an investor focused on corporate governance and “transformative change” at portfolio companies—which, in KT&G’s case, meant going straight at the structure management has defended for decades.

The flashpoint was Korea Ginseng. KT&G rejected a 1.9-trillion won offer from Flashlight for the business last year. Since 2022, Flashlight has argued for a horizontal spin-off and a separate stock market listing of the ginseng unit, calling it a cash cow whose value is being muted inside a tobacco conglomerate.

Korea Ginseng: The Hidden Jewel

At the center of the battle is Korea Ginseng Corporation, best known for Cheong Kwan Jang (also known as Jung Kwan Jang), the dominant brand in Korean red ginseng. Cheong Kwan Jang holds more than 80% of Korea’s ginseng market, and in 2011 it represented 35% of Korea’s total health products market.

KGC is the country’s largest supplier of red ginseng health supplements. In 2024, it posted 66.7 billion won in operating profit on 1.1 trillion won in sales.

But the financial trajectory has given activists an opening. Despite rising interest in health foods, KGC’s operating profit fell sharply—down from 202.1 billion won in 2019 to 103.1 billion won in 2023—and KT&G indicated further decline in 2024. Flashlight has used that to argue the tobacco-and-ginseng combination is a “wrong marriage,” and that KGC’s value isn’t being reflected in KT&G’s share price.

The Ongoing Saga

KT&G has drawn a hard line. In a letter rejecting the buyout proposal, the company said Korea Ginseng was not undervalued, argued that a separation would weaken business synergies, and reiterated its intention to grow ginseng into a global brand rather than carve it out.

At the same time, KT&G didn’t just ignore the pressure—it responded with a plan. The company rolled out an aggressive mid-term business program, committing to invest 3.9 trillion won through 2027 across three priorities: next generation tobacco and nicotine products, health supplement products including ginseng, and overseas expansion. And it made one point unmistakable: there would be no ginseng spin-off.

By 2025, Flashlight was still pushing—on governance reforms, transparency, and the details behind KT&G’s global business. The dispute became a familiar modern standoff: management arguing for long-term strategy and integrated scale, activists arguing that the fastest path to value is structural change and fuller disclosure.

IX. Global Expansion & The Indonesia Bet (2010–Present)

The Localization Playbook

KT&G’s overseas growth has leaned on a deceptively hard idea: don’t just export Korea. Build for the market you’re in.

That philosophy shows up most clearly in Indonesia. KT&G entered in 2011 by acquiring a local tobacco company, Trisakti—then spent the next decade learning how to sell into one of the world’s most distinctive cigarette cultures, where clove-based kretek dominates. Instead of trying to convert Indonesian smokers to Korean preferences, KT&G bent its flagship brand to local taste. Esse Berry Pop, launched in 2017, was designed specifically to fit that kretek sensibility. In 2018, it followed with Juara, inspired by the local sweet tea flavor known as Teh Manis.

The bet scaled. Indonesia’s contribution to KT&G’s overseas business nearly doubled, rising from 13.4% in 2021 to 22.5% last year. In 2023, Indonesia became KT&G’s largest market outside Korea, accounting for 22.6% of its total export volume. That year, KT&G sold about 9.55 billion cigarettes in Indonesia—roughly a 159-fold increase since the Trisakti acquisition.

The company also pushed a rapid-fire product cadence. In 2021 alone, KT&G released 21 new products, helping drive Indonesian sales volume from 4.84 billion sticks in 2021 to 8.48 billion sticks in 2022. By 2023, KT&G ranked as Indonesia’s fourth-largest tobacco company with a 4.4% market share, ahead of British American Tobacco and Japan Tobacco.

The Mongolia Success Story

If Indonesia is about scale, Mongolia is about focus—and what happens when a product fits a market so well it reshapes the pecking order.

In Mongolia, Esse offered a super-slim alternative to the traditional local lineup. Since 2020, KT&G has surpassed 50% market share there, dethroning the long-time leader, Japan Tobacco International. By 2023, KT&G’s share was above 50%, and sales kept climbing—rising from 300 million sticks in 2011 to 2.35 billion in 2024.

It’s a clean case study in KT&G’s playbook: find an under-served demand pocket, bring a differentiated format, and then execute relentlessly on distribution and brand.

Manufacturing Expansion

To support this kind of growth, KT&G has been building production capacity where demand is—so it’s not just shipping product across oceans and hoping the economics hold.

In April, the company completed a new factory in Kazakhstan with capacity of 4.5 billion sticks per year. And it has been expanding in Indonesia even more aggressively. A new plant in Surabaya, East Java—spanning 190,000 square meters—is under construction and set to begin operations in 2026. Once online, it will lift Indonesia’s annual production capacity from 14 billion cigarettes to a combined total of 35 billion, reinforcing the country as KT&G’s biggest overseas manufacturing hub.

By this point, KT&G’s global production footprint included plants in Korea, Indonesia, Russia, Turkey, and Kazakhstan. It also operated overseas corporate entities in Russia, Indonesia, Kazakhstan, Turkey, and Taiwan, with branch offices overseeing Mongolia, Uzbekistan, and Europe.

The message in all of this is simple: KT&G isn’t trying to be an exporter with a side hustle abroad. It’s building the infrastructure of a true multinational—one local market at a time.

X. Investment Thesis: Bull and Bear Cases

Bull Case: The Global Top-Tier Play

The bull case for KT&G is simple: this is a former monopoly that learned how to compete at home, then started winning abroad—and now has a credible seat at the table in next-generation nicotine.

Domestic still matters. Even after decades of pressure from Philip Morris, BAT, and Japan Tobacco, KT&G has held roughly 60% share in Korea. That’s an unusually deep home-field advantage in a global industry where “local champions” often get chipped away to minority status. It reflects distribution muscle, brand loyalty, and a feel for Korean consumer tastes that outsiders still struggle to replicate.

Then there’s the export story, which is no longer a side narrative. In the first quarter of this year, KT&G’s overseas cigarette sales reached 449.1 billion won ($327 million), surpassing domestic sales of 373.6 billion won for the first time. Overseas volume rose 23% and revenue climbed 54% from a year earlier, while domestic sales slipped by 9.3 billion won. As one Kyobo Securities analyst put it, “It underscores the shift toward an overseas-centered structure.”

Next comes NGP. KT&G already proved it could beat IQOS in the one market where that seemed impossible, and the PMI partnership gives it a path to scale those products globally without having to build a worldwide distribution system from scratch.

And finally, there’s optionality. Korea Ginseng Corporation—anchored by the Cheong Kwan Jang brand and a dominant position in Korean red ginseng—sits inside KT&G like a second business with its own economics and identity. Whether it stays integrated or not, bulls see it as value that the market may not be fully crediting.

Bear Case: Structural Headwinds

The bear case is just as straightforward: the foundations that made KT&G a cash machine are eroding, and the path forward comes with real dependencies and noise.

Start with Korea itself. Smoking rates have been falling for years as public health pressure rises and regulation tightens. Even if KT&G defends share, it’s defending a shrinking pool. The domestic cash cow is in structural decline.

Then there’s governance risk. The campaign by Flashlight Capital hasn’t been a one-off flare-up; it has turned into a sustained fight that can distract management and create uncertainty for investors. The debate over whether Korea Ginseng should be separated hasn’t gone away—it’s just been pushed down the road, and the courts have been pulled into it.

NGP also comes with a strategic wrinkle. KT&G’s global expansion in heated tobacco relies heavily on Philip Morris’s distribution—yet PMI is still a direct competitor in Korea. That’s a powerful channel, but it also means KT&G may not fully control its own destiny, or the economics, outside its home market.

And hovering over everything is regulation. Tobacco regulation keeps tightening globally, and heat-not-burn products could face tougher scrutiny as additional research on health effects accumulates.

Porter's Five Forces Analysis

Threat of new entrants is low. The industry is heavily regulated, distribution is hard, and building a brand is expensive. In Korea, KT&G’s position is especially difficult to crack.

Supplier power is moderate—and rising. As imported leaf tobacco prices have surged, costs have followed. KT&G’s manufactured cigarette division saw its cost-to-sales ratio increase from 38.6% in 2020 to 47.9% in the first half of 2025.

Buyer power is moderate. Consumers do have preferences, but they’re price-sensitive, and the government’s tax policy effectively shapes retail pricing.

The threat of substitutes is high. Vaping, heated tobacco, and cessation tools all compete for the same behavior. KT&G’s NGP portfolio helps hedge, but it doesn’t eliminate the substitution pressure—it just moves the battleground.

Competitive rivalry is high. PMI, BAT, and JTI fight aggressively in Korea, and the heated-tobacco segment has seen price competition that can squeeze margins.

Hamilton Helmer's 7 Powers Framework

Counter-positioning shows up in KT&G’s localization playbook. In markets like Indonesia, adapting products to local preferences—rather than forcing a global template—has been a durable edge against larger rivals that often move more slowly.

Cornered resource lives in Korea Ginseng Corporation. Cheong Kwan Jang’s long heritage and dominant market share give KT&G something competitors can’t easily recreate in health functional foods.

Scale economies are real but limited compared with the global majors. KT&G has meaningful manufacturing scale in Korea and is building it overseas, but it still operates against giants.

Network effects are minimal in tobacco.

Switching costs exist mostly through habit and brand loyalty, but they’re not especially sticky—smokers can and do switch when pricing and availability shift.

Branding is a clear strength: Esse as a global ultra-slim franchise, and Cheong Kwan Jang as a national icon in ginseng.

Process power is where KT&G has surprised the industry. Years of R&D in NGP—culminating in AI-featured devices and the ability to outcompete IQOS in Korea—suggest a repeatable capability in product development, not just a one-time win.

XI. Key Performance Indicators to Watch

If you want to keep score on whether KT&G’s transformation is still working, there are three numbers that matter more than the rest.

1. Overseas Cigarette Revenue Growth Rate: This is the clearest signal of whether KT&G is truly becoming a multinational, or just enjoying a temporary export bump. Overseas cigarette sales rose from 1.01 trillion won in 2022 to 1.13 trillion won in 2023, then jumped to 1.45 trillion won last year. Keep watching for sustained momentum here. If growth holds up, the global expansion story stays intact. If it fades, you start asking whether competition, regulation, or market saturation is catching up.

2. HNB Market Share in Korea: Heated tobacco is where KT&G earned its right to talk like a global challenger. Holding roughly 48% share in Korea means lil is still winning against IQOS on home turf. If that share stays stable or rises, it’s proof KT&G can keep innovating and defending its strongest market. If it slips meaningfully, it’s an early warning that the edge is dulling.

3. Korea Ginseng Corporation Operating Profit: This is the pressure point where strategy and governance collide. KGC’s declining profitability has fueled the activist case that the business doesn’t belong inside a tobacco company. If profits stabilize or rebound, management’s decision to keep KGC looks more credible. If they keep falling, the argument for separation only gets louder.

XII. Regulatory and Accounting Considerations

Tax Risk: One lever still sits outside KT&G’s control: the South Korean government. Officials have been considering a cigarette tax increase for the first time in a decade. If that happens while input costs are already rising, the combined effect likely shows up in the simplest, most painful place—higher retail prices. And in tobacco, higher prices usually mean faster volume declines.

ESG Scrutiny: KT&G also operates under a permanent spotlight that many consumer businesses never face. As a tobacco company, it draws growing ESG scrutiny from institutional investors. That pressure doesn’t just hit the product category; it often lands on governance—how the board is composed, how shareholder rights are handled, and whether management is truly accountable. It’s the same terrain activists have been fighting on, and it’s not going away.

Related-Party Transactions: Finally, the PMI partnership is strategically elegant but financially messy. When a major competitor becomes your global distribution partner, you inherit complexity in revenue recognition, profit-sharing, and disclosure. Investors have reason to press for clarity on the economics—especially given the long-term ambition KT&G has attached to the relationship, including a target of $25 billion in total sales over 15 years. Transparency here matters, because the upside of the partnership is real—but so is the need to understand who captures the value, and when.

XIII. Conclusion: The Road Ahead

KT&G’s journey—from a sleepy government monopoly to a global tobacco challenger—is one of the more surprising corporate transformations in modern Asia. It defended its home market against deep-pocketed international players, survived privatization without losing its connection to Korean consumers, built a serious export engine around a single breakout brand, then went toe-to-toe with Philip Morris in heated tobacco—won—and turned that win into a global distribution partnership with the very rival it beat.

From here, the company’s strategy rests on three pillars: keep expanding overseas cigarettes (with the biggest momentum in places like Indonesia and Central Asia, and an increasing push into Europe), scale next-generation products through the PMI partnership, and grow its health functional foods business through Korea Ginseng Corporation.

The fight with Flashlight Capital isn’t going away quietly. If anything, it keeps governance, disclosure, and capital allocation under a bright light—forcing KT&G to justify, quarter after quarter, why its current structure is the best path forward.

Ultimately, the story turns on execution: can KT&G keep building abroad fast enough to offset a long-term decline in Korean smoking, and can it translate domestic NGP leadership into meaningful global share while relying on a competitor’s distribution network? The answer will determine whether it can reach its stated ambition of becoming a global top-four tobacco company by 2027.

For investors, it’s a classic transformation setup: real upside, real risk, and a management team that has already proven it can evolve under pressure. And the final irony still holds. The company that once made it illegal for Koreans to smoke foreign cigarettes now sells its products in 148 countries—proof that in tobacco, as in business generally, the winners are the ones that adapt fastest when the rules change.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube