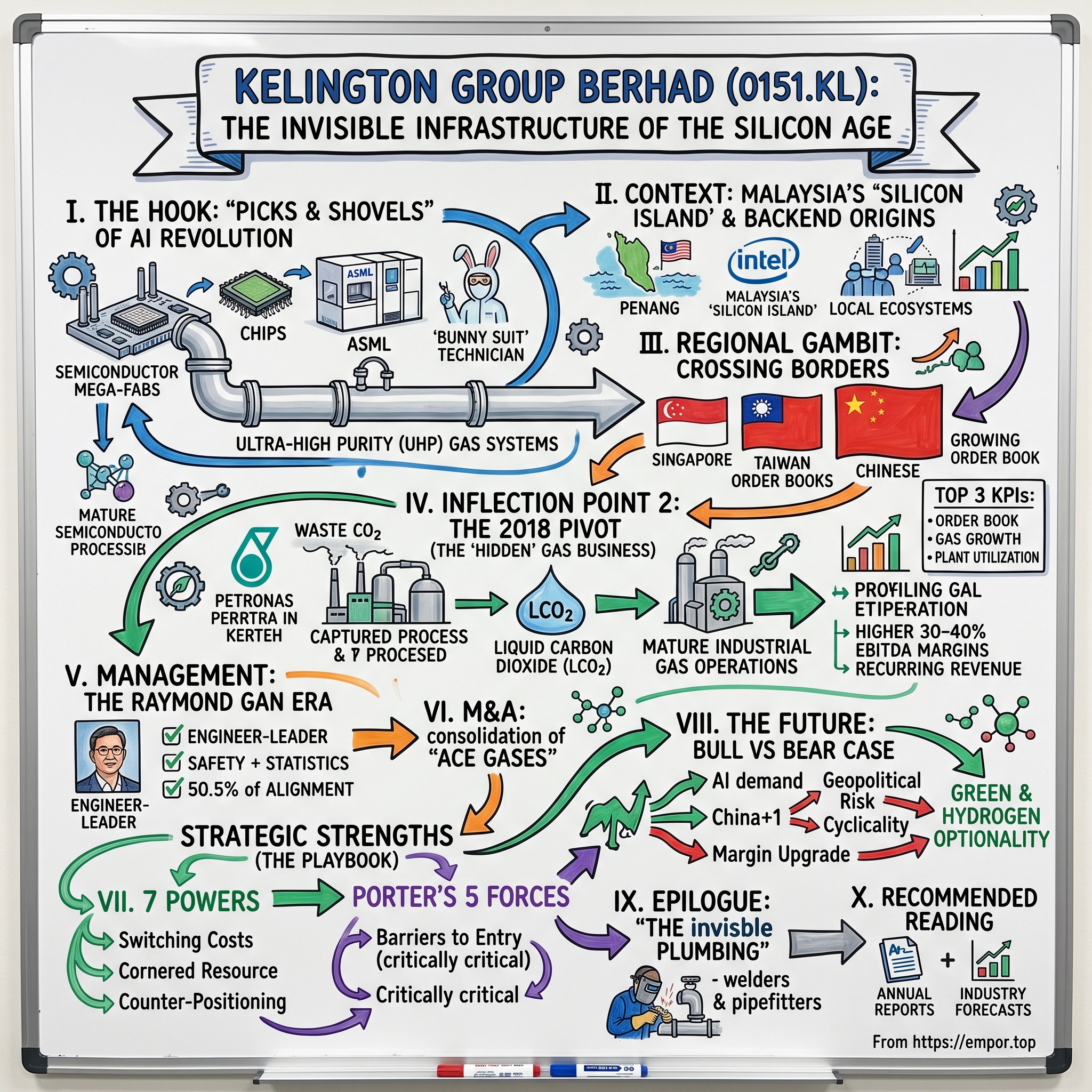

Kelington Group: The Invisible Infrastructure of the Silicon Age

I. The Hook: The "Picks and Shovels" of the AI Revolution

Picture the inside of a modern semiconductor "mega-fab"—the kind TSMC builds in Arizona for $20 billion, or the kind Intel stamped out in Chandler, or the one SMIC quietly ramped up outside Shanghai. From the outside, these buildings look almost boring. Long, low, windowless, wrapped in beige cladding. Inside, though, the cleanrooms glow that peculiar amber yellow, photolithography bays hum, and technicians in bunny suits drift past equipment that costs more than many small countries' defense budgets.

Everyone in finance has been trained, especially since the AI boom that began in earnest after ChatGPT's release in late 2022, to obsess over two names: ASML, whose EUV lithography machines print the features on the wafers, and TSMC, which owns the process recipe for doing so at volume. These are the glamour stocks of the chip era—the tools and the maker. But if you actually walk a new fab, the thing you notice is not the litho bays. It's the ceiling.

Above every tool, running for literal miles, are spotless silver pipes. They carry gases. Some are benign—ultra-pure nitrogen, used as a carrier or purge. Some are pyrophoric, bursting into flame on contact with air. Some are corrosive enough to dissolve steel. They flow at pressures and purities that have to be measured in parts per billion, sometimes parts per trillion. The specification is absurd: a single particle of contamination bigger than 50 nanometers in a gas stream can ruin a wafer that carries maybe 1,000 chips, each worth hundreds of dollars. One bad batch can silently scrap millions of dollars. A gas-system leak in the wrong place can kill people.

The companies that design, weld, pressure-test, certify, and then monitor those pipes for the life of the fab are not household names. They are what the industry calls "Ultra-High Purity" or UHP contractors. And one of the most improbable winners in that trade grew up not in Texas or in Dresden or in Shinjuku, but in Shah Alam, on the outskirts of Kuala Lumpur, Malaysia. Its name: Kelington Group Berhad. Its stock ticker: 0151.KL, on Bursa Malaysia.

This is the story of how a small Malaysian contractor—founded by a group of engineers who had no illusions about dislodging Linde or Air Liquide—embedded itself in the gas and chemical guts of fabs across Malaysia, Singapore, China, and Taiwan, then pulled a trick that would make any software investor smile: it used the low-margin installation business to bootstrap a high-margin, long-duration, recurring-revenue industrial gas operation of its own. Think of it as the "Netflix move," except the DVDs are cylinders of liquid carbon dioxide, and the streaming revenue is a bulk gas supply contract that lasts 15 years.

The stakes here are not small. Semiconductor fab capital expenditure ran well above $180 billion globally in 2024, according to SEMI. AI, automotive, and advanced packaging demand drove another leg up through 2025 and into 2026. Every dollar of that CapEx needs, somewhere in the project chart, a UHP systems integrator. And every wafer that eventually emerges needs gas—lots of it, forever.

The thesis of this episode is simple. Kelington Group is a case study in how a "boring," "old-economy" engineering company can quietly become the hidden toll collector on one of the most important megatrends of our time. It has compounded book value, earned real returns on invested capital, and done so by serving customers most of the market has never heard of, using a business model most generalist investors have never taken the time to understand.

We will walk through its origins in Penang's "Silicon Island" tradition, its bold regional expansion into Singapore and China, the pivotal 2018 gas pivot that transformed its economics, the management team that executed it, the moat it has quietly built, and the ways it could fall. It will be a long walk, but for a company that bets its whole identity on careful, patient engineering, that feels about right. Let's start where all good stories in Southeast Asian electronics start: in Penang.

II. Context: Malaysia's "Silicon Island" & The Backend Origins

If you have ever flown into Penang International Airport, you have flown over the origin story. The moment the plane banks over the Straits of Malacca, you see an archipelago of industrial parks—Bayan Lepas, Batu Kawan, Kulim just across the water on the mainland—stretched along the coastline like a ribbon of stainless steel and grey roofs. Inside those boxes, engineers package, bond, and test a meaningful slice of the world's semiconductors. Penang is not where the wafers are printed at the cutting edge; it is where they are finished, sorted, and shipped. The industry calls this "backend," and Penang has been doing it since 1972, when Intel opened its first Malaysian assembly plant and quite literally wrote the playbook for global electronics outsourcing.

For over five decades, that ecosystem grew in waves. Intel came first. Then AMD. Then Hewlett-Packard, Motorola, Robert Bosch, Osram, Infineon, Western Digital, Broadcom, and dozens of smaller specialists. By the late 1990s, Penang had earned the nickname the "Silicon Valley of the East"—a slight exaggeration, but a useful shorthand for what was, in truth, one of the densest electronics manufacturing clusters outside Taiwan and South Korea. Around this cluster grew a supporting ecosystem: precision machining shops, cleanroom panel fabricators, chemical distributors, and, most relevant to this story, mechanical and electrical contractors who specialized in the highly specific craft of building cleanrooms and their innards.

It is in this world that Kelington Group's founders cut their teeth. By the late 1990s, several Malaysian engineers had done enough years on multinational fab floors to understand an obvious truth: every time a new cleanroom was built, or an old one expanded, someone had to install the gas and chemical delivery systems. And those systems were not mere plumbing. They were engineering at the molecular level.

Consider what "ultra-high purity" actually means. When you turn on a kitchen tap and water comes out, you do not really care whether there are dissolved minerals in it. For a fab, though, a gas like hydrogen used to reduce wafers cannot be merely 99% pure—that would leave one percent of contaminants bouncing around, which is catastrophic. UHP standards demand purity like 99.9999999% ("nine nines"). Achieving that requires specialized electropolished stainless-steel tubing, orbital welding (a machine-driven welding process that produces identical, voidless welds every time), and helium leak-testing at pressures and sensitivities that a regular plumbing contractor has never seen.

It also requires an entirely different class of people. A UHP welder is not a pipefitter. They have to pass dozens of certifications, have their welds X-rayed, and—this is the kicker—have a near-zero error rate, because an invisible hairline defect inside a weld can outgas contaminants for months. Within Southeast Asia, the pool of properly certified UHP welders has always been thin. In the late 1990s, it was thinner still.

Against that backdrop, Kelington's founding team, led by Raymond Gan—an engineer who had spent years in the trade and eventually became the public face of the company—saw a classic opening. Global gas giants like Linde, Air Liquide, Air Products, and Taiyo Nippon Sanso dominated the supply of the actual gases. But the installation of the delivery systems inside a fab was a fragmented, regional, labor-intensive business that the big boys often subcontracted. If a local contractor could match their safety record and project-management quality, that contractor could earn a durable seat at the table.

In 2000, Kelington Group was incorporated with that thesis in mind. The early years were unglamorous: small retrofit jobs, gas line extensions, cleanroom modifications, and safety upgrades for the Penang multinationals. The founders rode the plane back and forth from Kuala Lumpur, pitched to purchasing managers, and lived on the razor-thin margins of subcontracted work.

The turning point for the company, financially speaking, was its listing on Bursa Malaysia's ACE Market (the smaller-cap tier) on July 8, 2009. The IPO was modest by any global yardstick—raising enough to shore up the balance sheet, buy more fabrication equipment, and hire more engineers—but it mattered. Public listing changed how prospective customers perceived them. A multinational purchasing manager evaluating who to trust with a $30 million gas-line retrofit prefers a counterparty whose financials are on display and who is regulated by a stock exchange. The ACE listing transformed Kelington from a private shop into, to borrow a phrase from Asian family business literature, a "credible small cap."

In 2015, the company graduated from the ACE Market to the Main Market of Bursa Malaysia. By this stage, it was still mostly a project-based company—revenue was lumpy, tied to the ebb and flow of new fab construction. If TSMC or Intel decided to delay a project by a quarter, Kelington's quarterly numbers wobbled. Investors who saw the name in passing pigeonholed it as a Malaysian construction stock, and that pigeonhole was, for a long time, half correct. It was an engineering firm, and the engineering firm happened to work on semiconductor projects. The "industrial gas" destiny was still below the waterline.

What set Kelington apart quietly, though, was safety culture. By the mid-2010s, the company had accumulated millions of safe man-hours on multinational sites, and it had done so with a record that matched or exceeded global peers. In a business where one bad incident can cost you an entire customer relationship for a decade, that record is a ticket to the next bid, and the one after that. Customers started to trust it with bigger jobs. Jobs outside Malaysia. And then, inevitably, with jobs in the truly gigantic fabs rising across China. Which brings us to the first real inflection point.

III. Inflection Point 1: The Regional Gambit

Here is a useful mental exercise. Imagine the board of a small Malaysian contractor sometime around 2012. Domestic fab activity is steady but not explosive. Singapore's semiconductor industry, led by GlobalFoundries and Micron, is humming but finite. Most of your customers are multinationals who are headquartered elsewhere and make global sourcing decisions. You have a reputation within the region. You have cash on the balance sheet. The question on the table is the existential one for any Southeast Asian mid-cap: do we double down at home, or do we cross the border?

The Kelington team's answer was clear, and in retrospect, correct: go where the tools are. Wherever the fabs were being built, that is where the UHP contract was being bid. Between 2011 and 2017, the center of gravity for new fab construction tilted decisively toward China, as Beijing poured money into its "Made in China 2025" semiconductor self-sufficiency push. SMIC was expanding its Shanghai and Beijing lines. Hua Hong was building out new 200mm and later 300mm capacity. New players—XMC, ChangXin Memory, YMTC—were ramping up from scratch. Each one needed gas systems.

Kelington had already opened offices in Singapore and Taiwan earlier in its history to follow its multinational customers. In China, it went further: it built a full regional operation. This was not a vanity expansion. It was, as the company eventually made clear in its filings, a deliberate strategy to follow the "China+1" wave before the words were cool. When its multinational customers expanded in both China and Southeast Asia, Kelington could be in both places. When Chinese domestic fabs came shopping for a vendor that could match multinational quality standards at regional cost, Kelington was on the short list.

The competitive chess here is worth thinking about. Why, one might ask, did the global gas giants—Linde, Air Liquide, Air Products—not simply stomp a company like Kelington in China? The answer is structural. The global giants are, at heart, gas producers with gigantic capex bases and very long-duration contracts. Their cost of operating is set up around building enormous on-site plants for anchor customers. They do install gas systems, of course, but UHP systems integration at the fab level is, for them, a relatively thin-margin, labor-intensive line of business that requires managing hundreds of welders and project managers in places where labor costs are a tenth of Europe or the U.S. Giants can do it. But they do it with the same cost structure that they use to produce atmospheric gas in Germany, which is not competitive on a project basis.

Kelington, by contrast, had the low cost base of a Malaysian contractor, the technical standards of a multinational subcontractor, and—crucially—the agility to bid on smaller, faster-moving projects that the giants were too slow to pursue. Industry veterans describe this as "Tier 2 agility with Tier 1 precision." It is a classic case of a niche competitor finding a slice of the value chain that is too small for the biggest player to defend, but too technical for a generic contractor to invade. The barrier to entry, importantly, is not IP—it is people. The welders. The project managers. The safety record. A new entrant would need a decade to replicate it.

There was another quieter advantage. Kelington was ethnically Chinese-Malaysian at the ownership and senior management level, which made building relationships in the Chinese market less culturally difficult than it was for the European giants. That is not a moat in the Porter sense, but it is a lubricant. It helped it close sales cycles that might otherwise have stretched painfully.

By the mid-to-late 2010s, Kelington's geographic mix had shifted dramatically. Where once it was a Malaysia-first company, by 2017-2019 China had become one of its largest revenue contributors. The book of work expanded to include not just UHP, but also process engineering and general contracting jobs tied to semiconductor facilities. Project sizes grew from the low tens of millions of ringgit to, on occasion, well over 100 million. Its order book—disclosed in presentations and annual reports—became the leading indicator investors watched most closely.

The regional expansion also taught the company something that became important later: the economics of being paid for installation were fundamentally different from the economics of being paid for gas. When you install a UHP system, you get paid once. You negotiate the scope, you execute, you collect, and you move on. Your margin is what it is, and if the customer decides to change a supplier next time, your recurring revenue from that site drops to zero. Every quarter, you start close to scratch. This is the core problem of every project-based engineering business: you are only as good as your next bid.

Inside Kelington's management team, by around 2015, the question had already shifted from "how do we win more projects?" to "how do we make our revenue less lumpy?" The answer would not come from the semiconductor segment at all. It would come from the unlikeliest of places: a pocket of waste carbon dioxide from Malaysia's national oil company, stranded on a remote coastline in Terengganu. That detour is where the company's story changes shape, and that is where we go next.

IV. Inflection Point 2: The 2018 Pivot – The "Hidden" Gas Business

Follow the East Coast Expressway out of Kuala Lumpur, keep the South China Sea on your right, and eventually you arrive at Kerteh. Kerteh is a small industrial town in Terengganu that most Malaysians could not place on a map, but that is where Malaysia's national oil company, PETRONAS, runs a sprawling petrochemical complex. Refineries, crackers, ammonia plants. It is a whole city of steel towers and flares, set against palm-oil plantations and empty beaches.

Every plant in a complex like Kerteh produces streams that the host does not really want. Some are valuable in the right hands; most are simply flared off or vented. Among those streams is carbon dioxide, sometimes as a byproduct of ammonia production, sometimes as a separation residue. By pure volume, there is a lot of it, and historically much of it was simply released.

For a food-and-beverage processor making soft drinks, or for a fab needing CO2 for chamber-clean or supercritical-CO2 applications, that same molecule—if properly captured, compressed, liquefied, and purified—becomes a valuable input. Liquid carbon dioxide (LCO2) has a real price, a real shelf life, and real transport economics. The trick, as always, is that the purification chain is capital-intensive and technically demanding, and it only works if you can lock in both a source and an offtake at scale.

Kelington management saw the opportunity earlier than most. Through its acquired industrial gas arm—Ace Gases Marketing, which we will come back to in Section VI—the company began running liquid carbon dioxide operations in Malaysia well before 2018. But the defining move was announced and then executed across 2018 and beyond: the decision to build and own a major LCO2 plant at Kerteh, anchored on raw CO2 sourced from PETRONAS's operations, and sized to serve both F&B and semiconductor demand across Malaysia and the wider region.

The move was strategically breathtaking for a company of Kelington's size. It was no longer a fee-for-service installation contractor. It was now, in effect, a small industrial gas producer. It would own a plant. It would own inventory. It would sign long-term supply contracts. Its revenue from this segment would not be lumpy; it would be recurring, month after month, year after year. Even better, once a plant of that scale is running well, incremental volumes come at very attractive margins—your fixed costs are sunk, and any extra tonnage is close to pure contribution.

The economic contrast between Kelington's two segments, once you understand it, is the single most important thing about this company. In the UHP engineering business, margins typically run in a band that produces an EBITDA margin somewhere in the high single digits to low-teens range on a healthy project mix. It is a good business, but it is a project business. In the industrial gas business, EBITDA margins sit in a very different universe—north of 30% for mature operations, and historically up to and above 40% in quarters when plant utilization and product mix are especially favorable. And unlike UHP, gas revenue is not a one-shot event; it compounds.

The way Kelington's management framed this pivot was characteristically understated. Publicly, they continued to describe themselves as a UHP systems specialist. Internally, though, the capital plan had tilted. Capex that would once have gone into more welding equipment and project bonds was now going into LCO2 production capacity, on-site gas generators, specialty gas cylinders, and the distribution logistics needed to move liquid gas safely and cost-effectively across Peninsular Malaysia.

It is worth dwelling briefly on why this pivot was, in effect, "hidden" for years from the average equity investor. Three reasons. First, the gas segment was small relative to total revenue in the early years—sometimes only 10% to 15% of the top line. In a lumpy UHP-dominated income statement, it was easy to miss. Second, Malaysian small-cap coverage is generally thin; only a handful of analysts dig into segment disclosures. Third, the contrast in unit economics between UHP and gas was under-communicated. If you read Kelington's annual reports and only looked at headline revenue and headline profit, you saw a semi-cyclical engineering firm. If you read the segmental breakdown and did the math, you saw something quietly different—a hybrid where a small, high-margin gas operation was driving a disproportionate share of enterprise value.

Across 2019, 2020, and then dramatically through the post-pandemic reopening, that hidden story began to surface. Industrial gas revenue grew. Semiconductor CapEx boomed—first driven by pandemic-era electronics demand, then by the chip shortage and reshoring push, and finally by the AI training buildout after late 2022. Kelington's UHP order book swelled with multi-hundred-million-ringgit awards from fabs in Singapore, Penang, Kulim, Taiwan, and China. And because the gas segment kept growing alongside, every incremental contract also created an incremental downstream gas opportunity wherever Kelington operated a plant.

The elegance of the model is the cross-pollination. When Kelington installs a UHP system for a new fab, it knows the gas flow diagrams intimately. When it later offers to supply bulk gases or specialty gases into that fab, it negotiates from the position of the vendor who literally designed the pipework. There are few ways to enter a fab customer more efficiently. And because UHP contracts create long, trust-based relationships with fab operations teams, the marginal cost of selling an adjacent gas contract drops meaningfully once the installation work has concluded.

By 2023 and 2024, industrial gas had grown into a clearly disclosed, clearly meaningful segment of group profit. Management began guiding more explicitly toward doubling gas capacity over the medium term. Investors who had started to view the company as "a Malaysian Linde in the making" began to rerate it. The narrative shifted. That is the 2018 pivot in a nutshell—a decision that, over the course of a few years, re-rated Kelington from "cyclical construction" to something much more interesting.

So the question becomes: what kind of leadership makes a pivot like that work? That is where we turn next.

V. Management: The Raymond Gan Era

The archetype of the Southeast Asian founder-engineer is a particular kind of person. Usually trained in mechanical or electrical engineering, often the product of a local university and then years on multinational shop floors. Quiet in public, deeply technical in private, more comfortable with a P&ID diagram than with an analyst-day teleprompter. The kind of person who can explain, in granular detail, why a particular orbital weld failed a helium leak test twelve years ago on a project in Shah Alam—because they remember, because details like that matter to them at a cellular level.

Ir. Raymond Gan Hung Keng, Kelington Group's Group Managing Director and the public face of the company for most of its listed life, fits that archetype precisely. His biographical details in the company's annual reports are spare: a Malaysian engineer by training, deep experience in the semiconductor and high-tech industry, one of the founding shareholders of Kelington. "Ir." in his title is the Malaysian designation for a professional engineer—a small but telling marker. He is the kind of leader who earned his credibility on the floor, not in a business-school classroom.

The most revealing thing about how Raymond Gan thinks is how he has allocated capital over time. Three tells stand out.

First, the early conservatism. In the ACE Market years after 2009, Kelington did not press the accelerator. It could have levered up, chased bigger overseas projects, opened offices in a dozen countries. It did not. It grew the book one customer at a time, accumulated safety records and reference installations, and waited. That patience is unusual in a Malaysian small-cap environment that often rewards the noisy rather than the disciplined.

Second, the pivot bet. Moving into owned industrial gas production requires a very different type of capital commitment than serving customers on a per-project basis. LCO2 plants have long payback periods, specialized equipment, and regulatory complexity. The Kerteh-anchored gas build-out was, relative to the company's balance sheet at the time, a serious bet. Management sized it appropriately, staged it carefully, and communicated about it openly enough that those who were paying attention could model it.

Third, the operating culture. Kelington has consistently avoided what Malaysian market observers call the "conglomerate discount" trap—the temptation for a mid-cap success story to drift into unrelated property, plantation, or services adjacencies that dilute focus. By 2026, the company was still fundamentally doing what it started doing: engineering for fabs and producing industrial gas. Its "adjacencies" were disciplined—mostly natural extensions such as on-site gas generation, specialty gas packaging, general contracting tied to fab projects, and, in recent years, exploratory work on hydrogen and solar, which we will come to in Section VIII.

On incentives, the picture is encouraging. Kelington's founders and management, primarily through Palace Star Sdn Bhd and related holdings, have retained meaningful equity in the company—reported in the company's annual reports at around 20% combined. In Asian mid-cap terms, that is a healthy alignment. It means the board's "north star" financial metric is long-run total shareholder return with meaningful dividends, rather than aggressive empire-building that dilutes equity.

The best test of alignment in a capital-allocation sense is actually the dividend policy. Kelington has historically paid dividends modestly rather than going dry on distributions and reinvesting every ringgit back into the plant. That choice—sharing cash flow with shareholders even while investing in a gas business with attractive project economics—is the kind of signal you want from a founder-engineer. It says: we are good at finding investment returns, but we also respect that the shareholders are our partners, not just a source of capital.

Another cultural signal worth reading is Kelington's approach to safety reporting. In the company's annual reports, safety statistics and the number of man-hours without lost-time incidents appear prominently. In an industry where one large accident can cost you a customer for ten years, this is not vanity reporting. It is a founder's reminder to the organization of what keeps the company alive. An engineer-led culture treats safety as a capital allocation issue, not a compliance exercise, because they know the tail risks.

On the negative side of management scorecards, it is fair to flag a few things as areas to monitor. The company is still run by a relatively tight founding circle. Succession planning, which is rarely discussed publicly, matters in any founder-led firm. Senior executive transitions across the engineering, procurement, and gas operations teams are worth watching year to year in annual disclosures. Board independence is typical for a Malaysian mid-cap; investors who want rigorous independent oversight will want to watch board composition over time.

A final point on "capital allocation as character." When you benchmark Kelington's LCO2 plant economics against global industrial gas peers, something striking emerges. The Kerteh facility and similar expansions have been built at capex levels in the low tens of millions of U.S. dollars per project, generating cash flow yields that are attractive in absolute terms and dramatically attractive relative to the multiples at which global majors trade their embedded plants. A plant that generates meaningful recurring EBITDA at that cost point is the kind of investment a large gas company would take every day of the week. Kelington's ability to build and operate at that cost base is itself a function of founder discipline and local engineering talent. It is, in its own way, a moat.

All of which leads to the question: how much of this was organic, and how much was bought? The answer is a mix, and the most important acquisition in the company's history is worth its own chapter.

VI. M&A & Capital Allocation: The "Ace" in the Hole

Every serious public-market pivot has at least one piece of M&A that crystallizes the strategy. For Kelington, that move was the consolidation of Ace Gases—the rebranded industrial gas business that today sits at the center of the company's recurring-revenue story.

The context. By the mid-2010s, Kelington had already experimented with industrial gases through partial stakes and joint ventures in Ace Gases Marketing. This was useful. It gave the engineering parent a look inside the gas customer base, real operating data, and a reasonable sense of margin structure. What it did not provide was full operational control or the ability to consolidate cash flow. Minority interests are informative; they are not transformational.

Moving to full ownership across a series of steps, Kelington integrated Ace Gases as a wholly-owned subsidiary and rebranded the operation under the Kelington gases umbrella. The practical effect of full ownership was significant. It allowed management to direct capex into the segment without friction, align sales and engineering incentives, and crucially, consolidate 100% of the gas business's profit—and unit economics—on the P&L.

The natural question for any disciplined investor is: did they overpay? The answer requires context. The industrial gas industry globally is famous for trading at premium multiples. Air Liquide, Linde, and Air Products have long commanded high-teens to 20+ times earnings and enterprise values that imply mid-to-high-teens EBITDA multiples. This is not surprising. The industry is structurally concentrated, has high switching costs, and generates long-duration, inflation-linked cash flows. Industrial gas is, in finance-textbook terms, infrastructure that wears a chemicals costume.

Against those benchmarks, Kelington's entry into the gas segment—through incremental acquisitions and organic build-out rather than a single large take-out of a competitor—looks like a classic "build instead of buy at peak" playbook. The company accumulated its gas footprint while the broader market was still pricing Kelington as a construction cyclical. In other words, when the gas segment was still unproven to the public, internal transfers and consolidation steps could happen at valuations set by Kelington's then-quiet story. By the time the public narrative caught up and the gas business started contributing meaningfully to profits, the internal consolidation was already done.

That is the quiet genius of the "Ace" move. It is a version of the classic carve-in where a hidden asset is brought fully inside a parent company before the market has woken up to its value. In hindsight, it looks obvious. At the time, it did not.

Post-consolidation, the capital allocation playbook has been consistent. When plant utilization at one LCO2 facility approaches capacity, management commissions the next. The projects are generally staged, funded from a mix of internal cash flow and moderate debt, and sized to match contracted demand rather than being built on spec. This "demand-anchored build" approach matches what the best operators in industrial gas have always done: sign the offtake first, pour concrete second. Kelington's smaller scale keeps it disciplined in a way that large majors sometimes lose.

Beyond gas, Kelington has also made disciplined acquisitions and partnerships on the UHP side—often acquiring small regional engineering firms or specific technical capabilities that accelerate its offering. These deals have been modest in size and tucked into annual reports without fanfare, which is again characteristic of the management style. No big names dropped, no transformational rhetoric, just the quiet accumulation of capabilities along a clear strategic line.

Now consider the company's broader balance sheet behavior. Kelington has historically avoided the "bet-the-firm" M&A impulse. Where possible, it funds growth from operating cash flow. Debt has been used, but responsibly. The balance between reinvestment and dividends has been roughly stable. In an environment where many regional firms either hoard cash out of paranoia or gamble it on adjacent-but-unrelated ventures, Kelington has stayed close to its lane—fabs and gas, with a slow and deliberate lateral expansion into general engineering and, as we will see, clean energy work.

One capital allocation decision that deserves specific mention is the choice to diversify its gas customer base beyond semiconductors. While chips are the flagship use case, Kelington's gas segment also sells to food and beverage customers, glass and metal fabricators, water treatment operators, and pharmaceutical companies. This diversification reduces segment cyclicality. If the semiconductor industry enters a cyclical trough, the F&B base keeps the plants running. If F&B softens, chip demand cushions. The portfolio construction is deliberate and, for a single-country operator, prudent.

The last element of the capital allocation story is geographic. Kelington has over time set up gas operations not just in Malaysia but also across the region, including capabilities in Singapore and China. Each expansion has to clear internal return-on-capital hurdles rather than being a vanity plant. Management has been willing to walk away from jurisdictions and project sizes that do not fit, which is the small virtue a disciplined mid-cap possesses that a large conglomerate often lacks.

Put together, the Ace consolidation, the staged plant build-outs, the moderate dividend, and the restrained use of debt describe a capital allocator who behaves like an owner. For public-market investors, this is often more valuable than quarterly earnings momentum. It is the part of the story that does not show up in consensus estimates but that shows up plainly in compounding returns over long periods. The next question is: how durable is all this? That takes us into the moat analysis.

VII. The Playbook: 7 Powers & 5 Forces

It is one thing to describe a company's strategic moves after the fact. It is another to ask, why has it sustained attractive economics, and why should those economics persist? The two frameworks that serve long-term fundamental investors best here are Hamilton Helmer's 7 Powers and Porter's Five Forces. Applied carefully, both tell a consistent story about Kelington.

Switching Costs (the primary power). Once a UHP system is installed in a fab, the integrator knows the topology better than anyone else on the planet. The gas and chemical pipework inside a modern fab is dense, layered, and, critically, not optional. Any modification, expansion, or hot-tie-in (connecting a new line to a live system) carries catastrophic risk if mishandled. Fab operators are extremely reluctant to bring in a new vendor on a working plant. The cost of error—lost production, exposure of personnel, failed wafers—dwarfs the savings of shopping around. Kelington's embedded position on hundreds of fab sites across the region is, in Helmer's language, a textbook switching-cost power. It is why the company's aftermarket and expansion revenue compounds.

Cornered Resource (labor, not IP). The second power is subtle but real. The cornered resource is not a patent; it is the pool of certified UHP welders, project engineers, and safety officers that Kelington has accumulated and trained over more than two decades. Southeast Asia does not have a factory that produces these people. They are made in the field. The lead time to train a certified UHP welder to Kelington's standard is measured in years, not weeks. A competitor who wants to match Kelington's labor pool can try to hire away people, but the safety culture, tacit knowledge, and team coordination are non-fungible. This is a power that is hard to quantify but that shows up every time a customer chooses not to switch vendors because they trust the crew that has worked on their site before.

Counter-Positioning. Kelington's third power is counter-positioning against the gas giants. The globals cannot profitably pursue the segment of the market Kelington occupies without undercutting the cost structure they depend on to serve much larger projects. It is the same dynamic that allowed Ryanair to counter-position against British Airways: the incumbent cannot replicate the challenger's cost base without imploding its own business model. For a Linde or an Air Liquide to field a project-bidding operation at Kelington's cost base would mean restructuring their own Asian operations in ways that their global P&Ls cannot absorb. So they subcontract to Kelington, or they tolerate Kelington winning the smaller-scale work, and they focus their resources on the anchor on-site plant business that Kelington cannot replicate at scale. Both companies live where they can be most profitable.

Scale Economies (secondary). Within the regional gas business, Kelington is not a global giant—but within Peninsular Malaysia's LCO2 market, it has meaningful scale relative to domestic alternatives. Distribution logistics, cylinder fleets, and fixed plant costs favor the operator with the largest local footprint. This is a regional scale economy rather than a global one, but it is still operative.

Process Power. Decades of safety and project-delivery process represent tacit know-how that is very hard to replicate. This is related to the cornered-resource power and to the track record that gets a vendor prequalified on multinational fab sites in the first place.

Now Porter's Five Forces.

Barriers to Entry — very high. You cannot walk into an Intel or TSMC fab site as a new UHP vendor. The supplier qualification process can take years. References are required. Safety track records are required. Insurance is required. Technical certifications from tool vendors are required. A new entrant would need to accumulate all of this in a market where existing vendors already have the trust. For practical purposes, the barrier is measured in years and reputational capital, not in dollars.

Supplier Power — low to moderate. Kelington's gas segment uses inputs that are either waste streams (the PETRONAS CO2 feedstock), commodity precursors, or co-products. Hardware suppliers of orbital welders, fittings, and regulators are relatively competitive. Kelington is not hostage to a single supplier.

Buyer Power — moderate, mitigated by criticality. Fab operators are large, disciplined, and price-conscious. They negotiate hard on project bids. However, the mission-critical nature of UHP work and the switching-cost dynamic discussed above mean that buyer power in practice is weaker than it appears on paper. You cannot simply pick the cheapest bidder if the cheapest bidder might blow up your fab.

Substitutes — limited. There is no practical substitute for UHP gas delivery in a semiconductor process. There are, however, different ways to source gas—bulk supply, on-site generation, cylinder supply—and Kelington competes across those modes.

Competitive Rivalry — meaningful but structured. The competitive landscape consists of a few tiers. At the top are the global majors (Linde, Air Liquide, Air Products, Taiyo Nippon Sanso). In the middle tier sit regional specialists with comparable safety records, of which Kelington is one of the most prominent in Southeast Asia. Below that are local subcontractors who compete on price but rarely on quality certification. Rivalry is real but stratified. Kelington is rarely competing head-to-head across every layer.

Put the frameworks together, and a picture of durable advantage emerges. Switching costs and cornered resources anchor the moat. Counter-positioning protects the mid-market niche. Entry barriers and low supplier power extend the runway. The result is a business that is unlikely to see rapid margin compression from new entrants, and that has reasonable pricing power with its customers when it matters most. The open question, as always, is whether macro and cyclical forces can disturb that equilibrium. That is the core of the bull and bear debate.

VIII. Bear vs. Bull Case & The Future

The bull case is the one you have been reading between the lines for the last seven sections. It rests on three legs, and each deserves to be stated plainly.

First, the semiconductor CapEx tailwind. Global fab spending has been in an extended growth phase driven by sovereign chip strategies (U.S. CHIPS Act, EU Chips Act, Japan's Rapidus, Korea's K-Chips initiative), by the AI training and inference buildout that accelerated after 2022, and by the natural product-cycle demand from advanced packaging and leading-edge logic. SEMI's published forecasts through 2025 showed multi-year strength in wafer fab equipment spending, and the ancillary UHP and facility spending tends to track equipment CapEx at a ratio that has been meaningfully positive for the industry. Every fab that opens needs UHP. Every UHP vendor with the right track record benefits.

Second, the "China + 1" migration. Over the past five years, multinational semiconductor customers have diversified production away from concentration in any single geography. Malaysia—particularly Penang and Kulim—has been a major beneficiary of that diversification. Singapore has maintained its position. Vietnam and India are emerging entrants. Kelington is geographically positioned in the winners. It is already the vendor of record for many of the multinational brands that are leading the diversification.

Third, the margin mix story. As the industrial gas segment grows, its higher EBITDA margins will flow more meaningfully into the group's consolidated margin. A company whose revenue mix shifts from UHP-dominated to a more balanced blend of UHP and gas will show operating leverage that looks striking at the group level. Every incremental ringgit of gas revenue contributes more to profit than every incremental ringgit of UHP revenue. If management can double gas capacity over the medium term, as it has indicated in public communications, the arithmetic of profit growth does not need perfect execution to be attractive.

There is a fourth, quieter leg—the green and hydrogen optionality. Industrial gas companies globally have been repositioning around the energy transition. Linde and Air Liquide have both made major plays in green hydrogen and low-carbon industrial gases. Kelington has publicly explored hydrogen and has expanded into adjacent clean-energy engineering, including solar energy-related engineering work. None of these is yet a material profit contributor. They represent optionality that could matter in the 2030s if the Southeast Asian energy transition accelerates.

The bear case, however, is not trivial. Serious investors should hold it in equal weight.

Geopolitical risk in China. A meaningful share of Kelington's revenue has historically come from projects in China. Any escalation in U.S.-China chip-related tensions—tighter export controls, forced reshoring, capital flight from the Chinese chip sector—could hit the UHP order book. Kelington's diversification across multiple geographies softens this, but does not neutralize it. A sharp, sustained slowdown in Chinese fab construction would show up in the top line.

Project lumpiness. Even with the gas segment growing, the UHP business remains inherently lumpy. Large projects have bid timing, progression milestones, and delivery schedules that can shift by quarters. Investors who index on quarterly earnings will find that Kelington's reported numbers can swing meaningfully simply because of where in a project cycle a given quarter sits. This is a cosmetic risk more than a structural one, but it is real.

Semiconductor cyclicality. Chips are a cyclical industry. Periods of oversupply and weak pricing lead fab operators to slow CapEx. If AI-driven demand cools or if a memory glut recurs, 2026-2028 fab starts could disappoint. Kelington's exposure is mostly construction-linked, so it participates in CapEx cycles rather than in wafer pricing. But a slower CapEx environment means fewer tier-one projects to bid on.

Input cost and foreign exchange. A meaningful portion of Kelington's revenue is in U.S. dollars and Chinese renminbi, while its cost base is heavily in Malaysian ringgit. Currency moves can compress or expand margins without any change in operating performance. The company's filings describe hedging and natural currency matching, but residual exposure exists.

Concentration with a few anchor customers. The company has disclosed that certain customers contribute a meaningful share of revenue in any given year, a common feature of project-based contractors. Losing a single anchor customer, or seeing one delay its CapEx, can show up quickly.

Talent scarcity in reverse. The same pool of UHP welders and engineers that is a moat can become a bottleneck if rapid growth outpaces hiring. Wage inflation in Southeast Asian skilled trades has been real over recent years. The company's ability to scale depends on its ability to train and retain people.

Execution risk on gas capex. Building LCO2 and specialty gas plants on time and on budget is not trivial. Any project overrun, safety incident, or utilization shortfall can dampen the gas segment's returns on capital. A disciplined cost base is the company's defense, but it is not infallible.

Where does this leave the medium-term framing? Kelington sits at the intersection of three favorable secular forces—semiconductor buildout, China+1 diversification, and gas-as-a-service margin upgrade—and at least three credible downside vectors—geopolitical tension, CapEx cyclicality, and talent scarcity. The range of outcomes is wide, which is a feature, not a bug, for any small-cap with exposure to both construction and recurring revenue.

The "next act" most worth watching is the company's work on hydrogen and green industrial gases. If Southeast Asia genuinely develops a hydrogen economy—for green steel, for fertilizer decarbonization, for industrial power—Kelington's engineering pedigree in handling hazardous gases at ultra-high purity is directly transferable. It already has the welders, the safety culture, and the relationships. That optionality is real, even if its timing is uncertain.

Finally, a note on KPIs. For investors tracking this company, three numbers matter more than any others. First, the order book, which is disclosed periodically and serves as the leading indicator of UHP revenue for the following four to eight quarters. Second, the industrial gas segment's revenue growth rate and margin profile, which tell you whether the pivot is continuing to compound. Third, utilization of the LCO2 plants and any new gas capacity being commissioned, which drives whether incremental capex is earning its cost of capital. Everything else—quarterly revenue, EPS, dividend yield—is derivative of those three variables.

IX. Epilogue: The "Acquired" Lens

Step back from the trenches and look at this company as a story. What is it, really?

Kelington Group is an "old economy" engineering firm—welders, pipefitters, safety inspectors, project managers—that has grafted onto itself a "new economy" financial profile. Its engineering business earns decent returns on capital, is cyclical, and lives or dies by the order book. Its gas business earns software-like margins, is recurring, and is protected by switching costs and capital intensity. The grafting of the two produces a company whose financials do not fit neatly into the construction cyclical box that most screens put it in.

The broader lesson is one that any investor in industrial companies has to absorb at some point. The glamour layers of an industry—the ASMLs, the TSMCs, the Nvidias—attract the capital and the attention. But in every glamour layer there are dependencies—tools, gases, chemicals, cleanroom panels, deionized water—that are mission-critical, deeply technical, and commercially overlooked. The companies that embed themselves in those dependencies can, in the right conditions, compound for decades on a base of fundamentals that looks almost dull.

Kelington also offers a case study in how to pivot a public company without wrecking its identity. Many engineering firms have tried to become something else and lost their cultural center in the process. Kelington leveraged its engineering identity to enter a new business where engineering discipline is directly relevant. It did not reinvent itself. It extended itself. The pivot looks in hindsight like a natural next step, rather than a jarring break.

For a student of business history, the closest analogue is probably the way small regional specialty chemicals firms in the mid-20th century evolved into industrial services giants. You do not always notice the compounding while it is happening. You notice it decades later, when the cumulative returns look obvious.

Finally, there is something quietly admirable about a company built by engineers, run by engineers, and focused on the unglamorous bottleneck of an otherwise glamorous industry. In public markets, storytelling companies often attract the highest multiples. But the companies that actually deliver durable cash compounding tend to be the ones whose story cannot really be told in a single sentence, because the truth of the business lives in a thousand small technical decisions made over a thousand project sites.

Walk a fab at night, when the operators are quiet and the tools hum at their steady baseline, and look up at the silver pipes overhead. Somewhere, a welder—badged by a certification program, trained on a Kelington crew, wearing a personal protective kit that costs more than his weekly wage—has tested every joint. That is what you are buying when you buy 0151.KL. Not a stock, really. A claim on the invisible plumbing of the silicon age.

Myth vs reality is worth a final word. The myth around Kelington, as around many Malaysian small caps, is that it is a cyclical construction name whose earnings will always be lumpy and whose multiple should always trade at a structural discount. The reality is more nuanced. The engineering segment is cyclical, yes. But the company today is a blended entity, and the gas segment's economics look structurally different. Whether the public multiple catches up to that reality depends on whether management continues to execute and on whether generalist investors take the time to look past the headline revenue line.

X. Top 5 Recommended Links for Further Reading

-

Kelington Investor Relations — Annual Reports with the Industrial Gas segmental breakdown. The most important document is the management's discussion of segment revenue, capital expenditure plans, and order book disclosures.

-

PETRONAS Kerteh Integrated Complex overviews — Public technical material on the Kerteh petrochemical cluster provides context for how Kelington's LCO2 feedstock sourcing works and why a waste-stream to specialty-gas model can be economically interesting.

-

SEMI Global Fab Equipment and Facility Spending Forecasts — The semi-annual SEMI reports track the macro backdrop for wafer fab equipment and facility investment that ultimately drives UHP demand.

-

Malaysian Investment Development Authority (MIDA) — Publications on Malaysia's Electrical & Electronics ecosystem, including investment flows into Penang and Kulim, provide the macro tailwind context in which Kelington operates.

-

Global Industrial Gas Peer Comparisons — Annual reports and investor materials from Linde plc, Air Liquide, Air Products, and Taiyo Nippon Sanso provide the benchmarking framework for understanding what mature industrial gas economics look like and how Kelington's gas segment compares on unit-level metrics.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube