Hanwha Aerospace: The Rise of the K-Defense Titan

I. The Hook: The "K-Defense" Moment

Picture Warsaw in the summer of 2022. Europe is panicking. Russia has invaded Ukraine five months earlier, and NATO's eastern flank is suddenly the most dangerous piece of real estate on the continent. Poland, which shares a border with both Ukraine and the Russian exclave of Kaliningrad, has been donating its Soviet-era tanks and howitzers to Kyiv at a pace that is draining its own arsenal.

The Polish Ministry of Defense needs replacements—not in five years, not in three years, but now. They pick up the phone, and the call does not go to Lockheed Martin, or Rheinmetall, or BAE Systems. It goes to Seoul.

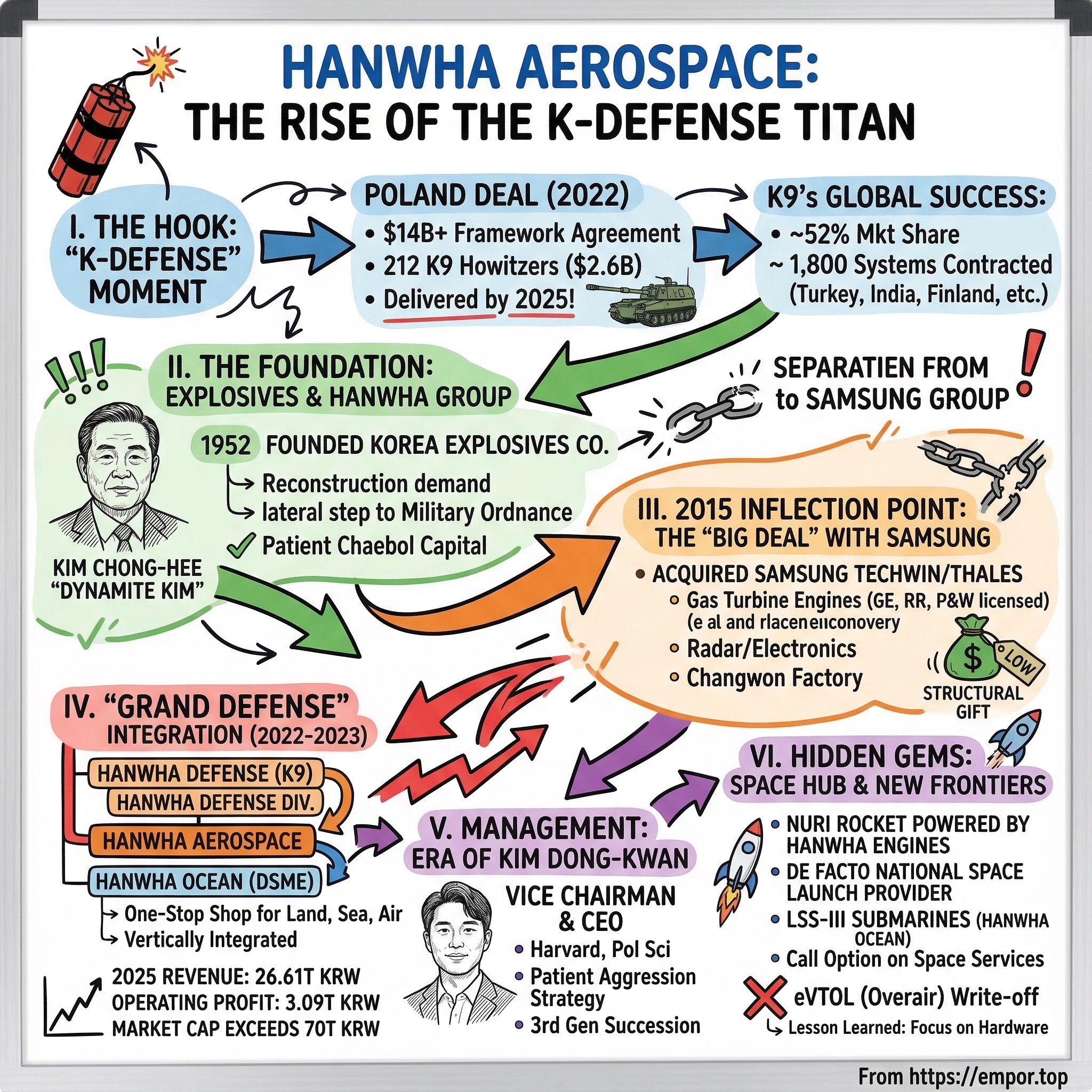

In July 2022, South Korea and Poland signed a framework agreement for what would become the largest arms export package in Korean history—a deal ultimately valued at upwards of fourteen billion dollars. The package included K9 self-propelled howitzers from Hanwha Aerospace, K2 Black Panther tanks from Hyundai Rotem, and FA-50 light combat aircraft from Korea Aerospace Industries.

But the centerpiece, and the deal that moved fastest, was Hanwha's K9. The first executive contract followed in August 2022: 212 howitzers worth roughly two and a half billion dollars. By early 2025—just two and a half years later—every single one of those howitzers had rolled off the production line and into Polish hands.

Let that sink in. Two hundred and twelve complex, forty-seven-ton self-propelled artillery systems, each one a marriage of precision engineering, advanced metallurgy, and digital fire-control electronics—delivered in roughly thirty months. Try getting that kind of delivery speed from a Western defense prime. You would still be negotiating the offset agreements. You would still be debating which fiscal year to book the first milestone payment. The Poles knew this. That is why they called Seoul.

And Hanwha was not done. In December 2023, a second executive contract followed: six additional K9A1 howitzers plus 146 of the upgraded K9PL variant, worth another $2.6 billion. Then in late 2025, the Chunmoo multiple-launch rocket system contract landed—roughly four billion dollars, with a joint venture for Polish production. Hanwha's total share of the Poland framework deal has grown to somewhere north of nine billion dollars, making it one of the largest defense export relationships in the world for a single company.

This is the question at the heart of the Hanwha Aerospace story: how did a company that started making dynamite for post-war construction in 1952 become the arsenal of democracy for the twenty-first century? And what does its trajectory tell us about the shifting tectonic plates of global defense—away from the slow, cost-plus incumbents of the West and toward the fast, export-hungry manufacturers of East Asia?

The thesis is straightforward but profound. Hanwha is executing a "land, sea, and air" integration strategy that mirrors what the great American defense primes did during the post-Cold War consolidation of the 1990s—when Lockheed merged with Martin Marietta, when Boeing absorbed McDonnell Douglas, when Raytheon swallowed Hughes Electronics.

But Hanwha is doing it faster, cheaper, and with a manufacturing efficiency that the West has largely lost. And unlike those American consolidations, which happened in a shrinking defense market, Hanwha is consolidating in a world where defense budgets are surging across Europe, the Middle East, and the Indo-Pacific simultaneously.

There is a phrase that has gained currency in defense circles since 2022: "K-Defense." It is a riff on "K-Pop" and "K-Drama"—the Korean cultural exports that conquered global markets through a combination of quality, value, and relentless marketing. The parallel is deliberate and surprisingly apt. Just as K-Pop groups like BTS and Blackpink succeeded by offering a polished, accessible product to audiences that were underserved by Western entertainment, Korean defense companies are succeeding by offering reliable, affordable, and immediately available weapons systems to militaries that are underserved by Western defense primes.

The global defense industrial base has become bifurcated. On one side sit the traditional Western primes—Lockheed Martin, BAE Systems, Rheinmetall, Thales—with the best technology but limited production capacity, long delivery timelines, and high costs driven by decades of cost-plus contracting. On the other side sits Korea, with production capacity built for export scale, delivery timelines measured in months, and cost structures shaped by decades of competing in price-sensitive Asian and Middle Eastern markets.

Hanwha Aerospace sits at the center of this bifurcation, and it has made itself the standard-bearer for K-Defense. The company that once blasted rock for Korean highways now builds the howitzers that defend NATO's eastern border, the rocket engines that put Korean satellites into orbit, and the naval vessels that patrol some of the most contested waters on Earth. This is the story of how they got there—and where the trajectory points next.

II. The Foundation: Explosives and the Hanwha Group

To understand Hanwha Aerospace, you have to start with a man nicknamed "Dynamite Kim."

Kim Chong-hee was born in 1922 in what is now North Korea. He trained as a gunpowder engineer at a Japanese-era explosives factory during the colonial period, learning the chemistry of detonation in one of the most volatile industries on the planet. This was not theoretical knowledge—it was the kind of hands-on, factory-floor expertise where a single miscalculation could be lethal.

When the Korean War erupted in 1950, and then the armistice brought an uneasy peace in 1953, Kim saw something that most people missed: the devastation of war had created an unprecedented demand for reconstruction, and reconstruction required explosives. You cannot build roads through mountains, blast foundations for bridges, or clear rubble from cities without industrial dynamite.

In October 1952, while the war still raged, Kim founded Korea Explosives Co.—Hanguk Hwayak in Korean. The abbreviated form, "Hanwha," would eventually become one of the most recognizable corporate names in Asia. The name itself tells the story: "Han" from Hanguk, meaning Korea. "Hwa" from Hwayak, meaning explosives—or more literally, "fire medicine." From the very beginning, this was a company whose identity was forged in controlled combustion. That DNA would prove remarkably durable across seven decades of corporate evolution.

Kim Chong-hee was not content to remain in the explosives business. He was a classic chaebol founder—relentlessly ambitious, politically connected, and willing to diversify into any industry where he sensed opportunity. The South Korean government's export-driven industrialization strategy, which funneled cheap credit and preferential treatment to large conglomerates in exchange for hitting national economic targets, provided the perfect environment for this kind of empire-building.

Through the 1960s and 1970s, Korea Explosives expanded into petrochemicals, construction, financial services, and trading. By the time Kim passed away in 1981, the Hanwha Group had metastasized from a single explosives factory into a sprawling conglomerate. Today it ranks as South Korea's seventh-largest chaebol, with over 460 affiliates spanning aerospace, defense, clean energy, finance, shipbuilding, and hospitality—a Fortune Global 500 enterprise.

But here is the thread that matters for our story: the pivot from civilian explosives to military ordnance was not a leap. It was a lateral step. The chemistry of commercial dynamite and the chemistry of artillery propellant are cousins. The manufacturing discipline required to produce explosives safely—where a single quality control failure can kill your entire workforce—translates directly into the precision required for ammunition production.

When South Korea began building its indigenous defense industry in the 1970s, driven by President Park Chung-hee's fear that the United States might abandon the Korean Peninsula after its withdrawal from Vietnam, Hanwha was a natural partner. The company began producing propellants, warheads, and eventually complete munitions systems for the Korean military.

This is a pattern you see again and again in defense industry history. DuPont went from gunpowder to the Manhattan Project. Alfred Nobel went from dynamite to the foundation that bears his name. Hanwha went from blasting Korean hillsides to building the most exported howitzer on the planet. The common thread is expertise in energetic materials—the science of making things go boom in a controlled, reliable, and precise manner. It is, quite literally, rocket science. And Hanwha would eventually build actual rocket engines.

There is a deeper historical context that matters here. South Korea's decision to build an indigenous defense industry in the 1970s was not merely an economic policy—it was an existential response to a perceived threat of American abandonment. When President Nixon withdrew a U.S. infantry division from South Korea in 1971 as part of the broader post-Vietnam retrenchment, Seoul was terrified. The Korean War was only eighteen years in the past. North Korea's military spending was, on a per-capita basis, among the highest in the world. And here was America, the security guarantor, pulling back.

President Park Chung-hee responded with the "Yulgok Project"—a massive defense modernization program that directed the chaebols to develop indigenous weapons manufacturing capabilities. Samsung was assigned precision machinery and electronics. Hyundai got shipbuilding and vehicles. Daewoo got rifles and armored cars. And Hanwha, with its explosives heritage, got ammunition and propellants. These assignments, made by government fiat in the 1970s, would echo through the next five decades of Korean defense industrial development. The specializations assigned by Park's technocrats would determine which companies were positioned to capitalize when the global defense market opened up half a century later.

Hanwha's assigned role—ammunition and propellants—was not glamorous. It did not get the headline-grabbing assignments like fighter jets or warships. But it was foundational. Every weapon system in the Korean military inventory needed Hanwha's products to function. Rifles needed bullets. Artillery needed shells. Rockets needed propellant. This unglamorous but essential role would give Hanwha an unshakeable position in the Korean defense ecosystem and, more importantly, would develop the production discipline and quality-control culture that would later differentiate the K9 howitzer program.

The chaebol structure deserves a moment of explanation for those unfamiliar with Korean corporate governance, because it is essential to understanding how Hanwha operates and why it can do things that Western defense companies cannot.

A chaebol is a family-controlled conglomerate, held together not by a single holding company in the Western sense, but by a web of cross-shareholdings, circular ownership stakes, and family trusts that give the founding family effective control despite owning a relatively small fraction of total equity. Think of it as a corporate solar system, with the founding family as the sun and dozens of affiliates orbiting at various distances—each one gravitationally bound to the center, but operating in its own orbit.

For Hanwha, the architecture works like this: the Kim family controls Hanwha Energy, a private company that holds roughly twenty-two percent of Hanwha Corporation, the flagship holding entity. The three sons of Chairman Kim Seung-youn hold additional direct stakes, bringing total family control of Hanwha Corp to over forty percent. Hanwha Corp, in turn, holds about thirty-four percent of Hanwha Aerospace. And Hanwha Aerospace now holds forty-two percent of Hanwha Ocean, the shipbuilding subsidiary. This cascading pyramid means that the Kim family, with perhaps ten to fifteen percent economic ownership of the total enterprise, exercises effective governance over a defense and industrial empire worth tens of billions of dollars.

The advantage of this structure, from the perspective of a defense company, is patience. Western publicly traded defense firms operate on quarterly earnings cycles and answer to activist shareholders who want share buybacks and dividend increases. Chaebol families operate on generational timescales.

When Hanwha decided to spend over a decade building expertise in gas turbine engines through licensed production agreements with GE, Rolls-Royce, and Pratt & Whitney—knowing the payoff would not come for twenty years—no institutional investor was demanding they "return capital to shareholders" instead. When the group decided to pour capital into a shipyard that had been losing money for years, no activist fund was threatening a proxy fight. That patient capital would prove decisive in assembling the integrated defense platform that exists today.

The bridge from explosives to aerospace was built one capability at a time: propellants led to ammunition, ammunition led to artillery systems, artillery led to rocket motors, and rocket motors led to jet engines and eventually space launch vehicles. Each step was incremental, each built on the last, and each was underwritten by a corporate structure that could absorb short-term losses in pursuit of long-term strategic position.

There is an important lesson here about the nature of competitive advantage in defense manufacturing. The Western defense industry's current capacity crisis is not an accident—it is the predictable result of thirty years of prioritizing shareholder returns over industrial capacity. After the Cold War ended, Western defense companies were encouraged to consolidate, reduce capacity, and return capital to shareholders. They did exactly that. Production lines were shuttered. Skilled workers were let go. Supply chains were rationalized for efficiency rather than resilience. The result was a defense industrial base that could produce exquisitely capable systems in small quantities, but that had lost the ability to produce anything at scale.

Korea took the opposite path. Because the threat from North Korea never went away, Korea never had a "peace dividend" moment. The defense industrial base was maintained, modernized, and expanded throughout the 1990s and 2000s—the very decades when Western capacity was being hollowed out. Hanwha's Changwon facility was not built for the current export boom. It was built to survive a North Korean invasion. The fact that it is now the most sought-after howitzer factory in the world is a consequence of that sustained investment, not a lucky accident.

By the time the outside world noticed what Hanwha had become, the transformation was already complete. But it was the acquisition of a lifetime, in 2015, that truly changed the trajectory.

III. The 2015 Inflection Point: The "Big Deal" with Samsung

In the annals of Korean corporate history, few transactions have been as consequential—or as underappreciated by the global investment community—as Hanwha's acquisition of Samsung's defense and aerospace assets. To understand why, you need to understand what Samsung was discarding, and why it was willing to let go of crown jewels.

The year was 2014. Samsung Group, South Korea's largest and most powerful chaebol, was in the middle of a once-in-a-generation succession crisis. Lee Kun-hee, the patriarch who had transformed Samsung from a mid-tier conglomerate into a global electronics titan, had suffered a heart attack in May and lay incapacitated in a hospital bed.

His son, Lee Jae-yong—often called "Jay Y. Lee" in the Western press—was maneuvering to consolidate control over the empire, and that meant simplifying the labyrinthine web of cross-shareholdings that held Samsung together. Non-core assets had to go—not because they were bad businesses, but because they were complicating the succession math. When you are restructuring a corporate empire worth hundreds of billions of dollars to ensure generational control, a defense electronics subsidiary worth a few billion is a rounding error. A very valuable rounding error, as it turned out.

Samsung Techwin was one of those "non-core" assets. Originally established in 1977 as Samsung Precision Industries in the industrial city of Changwon, the company had evolved over nearly four decades into South Korea's premier manufacturer of gas turbine engines, surveillance systems, and defense electronics.

To understand its value, you need to understand what a gas turbine engine represents in the aerospace industry. A gas turbine engine is arguably the most complex manufactured object on Earth. At its core, it is a spinning assembly of thousands of precision-machined parts operating at temperatures exceeding 1,500 degrees Celsius, with tolerances measured in thousandths of a millimeter. For non-engineers, imagine a metal tube where air is sucked in at the front, compressed to enormous pressures, mixed with jet fuel and ignited, and the resulting exhaust blasts out the back at supersonic speed—all while spinning blades withstand forces that would tear apart ordinary steel.

The metallurgy alone—developing exotic nickel-based superalloys and single-crystal turbine blades that can withstand extreme heat, pressure, and centrifugal force simultaneously—represents decades of accumulated know-how that cannot be reverse-engineered or leapfrogged by throwing money at the problem. This is why there are only a handful of companies on Earth—GE, Rolls-Royce, Pratt & Whitney, Safran—that can independently design and manufacture modern jet engines. It is one of the highest barriers to entry in any industry.

Samsung Techwin produced the engines that powered the Korean Air Force's T-50 advanced jet trainers and F-15K fighters under license from General Electric. It had partnerships with every major Western engine OEM, supplying fan blades, compressor discs, combustor modules, and low-pressure turbine components to global supply chains. It had decades of accumulated expertise in precision machining, metallurgy, and the kind of high-temperature materials science that separates serious aerospace manufacturers from pretenders.

Samsung Thales, a joint venture with the French defense electronics giant Thales, added another critical dimension: radar systems, communications equipment, fire-control systems, and the digital backbone that transforms a dumb artillery tube into a precision weapon. Together, Techwin and Thales represented the two capabilities that Hanwha lacked—propulsion and electronics—and that no amount of explosive chemistry could replicate.

In November 2014, Hanwha Group announced it would acquire Samsung Techwin along with Samsung General Chemicals. The combined deal was valued at approximately two trillion Korean won, or roughly $1.8 billion at the time. The defense-specific portion—the controlling stake in Samsung Techwin plus Samsung Thales—came in at roughly 1.6 trillion won.

The deal closed on June 29, 2015. Samsung Techwin was renamed Hanwha Techwin—a transitional identity that acknowledged the heritage while planting the Hanwha flag. Three years later, in 2018, the company was renamed again to Hanwha Aerospace, a signal that management saw the future not in surveillance cameras and industrial equipment (Samsung Techwin's legacy consumer businesses, which were later divested) but in the high-value aerospace and defense core. Samsung Thales became Hanwha Systems, retaining the French partnership while rebranding under the Hanwha umbrella.

Now, step back and appreciate the magnitude of what Hanwha acquired at that price. For roughly $1.5 billion, they bought South Korea's only gas turbine engine manufacturer—a company with relationships with every major Western engine OEM. A company that had produced over ten thousand engines across nearly five decades. They acquired the defense electronics capabilities that would become the digital nervous system of the K9 howitzer's fire-control system, making it one of the most accurate and responsive artillery platforms in the world.

They acquired a talent base of thousands of aerospace engineers—metallurgists, thermodynamicists, avionics specialists—who would otherwise have been scattered to the winds as Samsung exited the defense business. And they acquired the Changwon production facilities that would later become the most efficient howitzer factory on the planet.

To put the valuation in context, consider what was happening in Western defense M&A during the same era. When United Technologies acquired Rockwell Collins in 2018, it paid $30 billion. The L3 Technologies and Harris Corporation merger in 2019 created a combined enterprise valued at $34 billion. The Raytheon and United Technologies aerospace merger in 2020 produced a company valued at over $100 billion.

Hanwha paid roughly one percent of those figures for assets that, in the Korean context, were just as strategically important. This was not a bargain discovered through brilliant analysis—it was a structural gift created by Samsung's succession dynamics, the limited pool of Korean buyers capable of absorbing defense assets, and a global market that had not yet woken up to the export potential of Korean defense technology.

Why was the price so low? Three reasons converged. Samsung was a motivated seller operating under succession pressure—this was a cleanup operation, not a competitive auction designed to maximize value. The Korean defense market was relatively small at the time, with modest export revenue, so the assets were valued on their domestic earnings, not their future export potential. And very few Korean companies had the capability, the capital, and the political relationships to absorb defense-sensitive assets. Hanwha was essentially the only credible buyer, which gave them extraordinary leverage in a market with one seller and one buyer.

The comparison to Lockheed Martin's formation is irresistible. When Lockheed merged with Martin Marietta in 1995, the logic was identical: consolidate fragmented defense capabilities into a single entity that could offer governments an integrated portfolio. The "Last Supper" of 1993—when Defense Secretary Les Aspin told defense CEOs that the Pentagon's budget could only support a handful of prime contractors—set off a wave of consolidation that created the modern American defense industry.

Hanwha's Samsung acquisition was the Korean version of that consolidation moment. It gave them the missing pieces—engines, electronics, and precision manufacturing—that they needed to graduate from an ammunition and ground-systems supplier into a full-spectrum aerospace and defense company.

The market did not immediately recognize what had happened. Hanwha Aerospace (then Hanwha Techwin) traded at modest valuations for years, priced as a mid-cap Korean industrial with limited export exposure. International investors barely noticed. Defense analysts in Washington and London were focused on the familiar names—Lockheed, Raytheon, BAE—and could not be bothered to follow a Korean conglomerate subsidiary with a complicated corporate structure and financial statements in Korean won.

It would take the geopolitical earthquake of 2022 to reveal the true value of what had been assembled. But the foundation was laid here, in 2015, in what may prove to be the most consequential defense M&A transaction of the twenty-first century outside the United States.

There is a myth in Western defense circles that Korean weapons systems are cheap copies of Western originals—knockoffs that trade quality for price. The reality, post-Samsung acquisition, is almost the opposite. The K9 howitzer's fire-control system, built on technology inherited from Samsung Thales, is among the most advanced in the world—capable of receiving a fire mission, computing ballistic solutions, aiming the gun, and firing the first round in under sixty seconds. The gas turbine engines that Hanwha produces for Korean military aircraft meet the same specifications as those produced by GE and Pratt & Whitney, because they are manufactured under license using the same tooling, the same materials, and the same quality standards.

What Korean manufacturers add is something the Western defense industry has largely lost: the ability to produce at high volume, at consistent quality, and at a cost structure that reflects industrial efficiency rather than cost-plus contracting. The Samsung acquisition did not just give Hanwha technology—it gave them the manufacturing platform to deliver that technology to the world at a pace and price that Western primes cannot match.

IV. The "Grand Defense" Integration (2022–2023)

If the Samsung acquisition was the moment Hanwha gathered the pieces of its defense puzzle, the 2022-2023 reorganization was the moment it assembled them into a single, coherent picture. And the timing was anything but coincidental.

Russia invaded Ukraine on February 24, 2022. Within weeks, the global defense landscape underwent its most dramatic transformation since the fall of the Berlin Wall. European nations that had spent three decades cutting their military budgets suddenly announced massive rearmament programs.

Germany pledged a one-hundred-billion-euro special defense fund—the Zeitenwende, or "turning point," as Chancellor Scholz called it. Poland committed to spending four percent of GDP on defense—double the NATO target, making it proportionally one of the highest defense spenders in the alliance. Finland and Sweden abandoned decades of neutrality and applied to join NATO. And every one of these countries needed weapons systems that could be delivered quickly, reliably, and in large quantities.

The era of "peace dividend" procurement—small batches, long timelines, cost-plus contracts, and endless customization cycles—was over. The new era demanded industrial-scale defense manufacturing at speed. And Hanwha had been building exactly that capability for decades, largely unnoticed by the Western defense establishment.

To understand how profoundly the market shifted, consider this: before 2022, South Korea's total annual defense exports averaged roughly three to four billion dollars. In 2022 alone, that figure surged to over seventeen billion dollars in new contracts signed—a five-fold increase driven almost entirely by European demand. And Hanwha was the largest single beneficiary. The company went from being a respected but niche supplier to a handful of Asian and Middle Eastern customers to becoming one of the most sought-after defense exporters on the planet, practically overnight.

The corporate reorganization happened in two swift moves. In November 2022, Hanwha Defense Co.—the subsidiary responsible for the K9 howitzer and the Redback infantry fighting vehicle—merged into Hanwha Aerospace. Five months later, in April 2023, Hanwha Corporation's defense division, which included the company's ammunition, precision-guided munitions, and energetic materials businesses, also folded in.

The result was a single, vertically integrated defense entity that could offer a customer everything from 155mm artillery shells to self-propelled howitzers to jet engines to defense electronics to guided missiles, all under one corporate roof.

The strategic logic was the "one-stop shop" concept that had driven American defense consolidation in the 1990s, translated into Korean. When Poland wanted to rearm at scale, it did not want to negotiate with five different companies for five different systems across five different maintenance contracts. It wanted a single point of contact, a single logistics chain, and a single long-term maintenance relationship.

Hanwha could now provide exactly that. The K9 howitzer, the Chunmoo multiple-launch rocket system, the 155mm ammunition to feed the howitzers, the guided rockets for the Chunmoo, the fire-control electronics to aim all of it, and the comprehensive training and maintenance packages to sustain these systems in the field for decades—one phone call, one contract, one relationship.

But the most audacious piece of the reorganization was not the defense consolidation. It was the acquisition of a troubled shipyard that most of corporate Korea had given up on.

Daewoo Shipbuilding and Marine Engineering—DSME—was one of the "Big Three" Korean shipbuilders, alongside Hyundai Heavy Industries and Samsung Heavy Industries. Together, these three companies dominate global shipbuilding, responsible for roughly seventy percent of the world's large commercial vessels.

But DSME had become the problem child of the Korean shipbuilding industry. Through the 2010s, it accumulated staggering losses from cost overruns on offshore platforms, requiring multiple government bailouts through the state-owned Korea Development Bank. By 2022, DSME was a poster child for troubled state-linked industrial assets that Korean policymakers desperately wanted off their books.

The Korea Development Bank had tried to sell DSME to Hyundai Heavy Industries in 2019, but European regulators blocked the deal on competition grounds, fearing the merger would create an unacceptable monopoly in LNG carrier construction. The shipyard was stuck in limbo—too strategically important to shut down, too troubled to attract a buyer, and too large to ignore.

Enter Hanwha. In December 2022, the group announced it would acquire a 49.3 percent controlling stake in DSME through a two-trillion-won rights offering—roughly $1.5 billion. South Korea's Fair Trade Commission approved the acquisition in April 2023 with conditions, and the deal closed the following month. DSME was rebranded as Hanwha Ocean—a name that signaled the ambition: not just a shipyard, but a company that would dominate an entire domain.

On the surface, this looked like a risky bet. DSME's track record of serial losses was well-documented, and shipbuilding is a notoriously cyclical, capital-intensive business with thin margins even in good years. The workforce was demoralized after years of government-mandated restructuring. Why would a defense company want this headache?

Because Hanwha was looking at a different set of variables than the conventional wisdom suggested.

First, global demand for LNG carriers was surging as Europe scrambled to replace Russian pipeline gas with liquefied natural gas shipped from Qatar, Australia, and the United States. DSME was one of only three shipyards in the world capable of building the advanced membrane-type LNG carriers—massive vessels that keep natural gas cooled to minus 162 degrees Celsius for oceanic transport. Order books were stretching out years into the future, and pricing power had shifted decisively from buyers to builders.

Second, and more importantly for the defense thesis, DSME had decades of experience building submarines, destroyers, and frigates for the South Korean Navy. Its Geoje Island shipyard—one of the largest in the world, with drydocks capable of handling vessels up to 500,000 deadweight tons—had produced some of the most advanced naval vessels in Asia, including the KSS-III class submarines that represent the pinnacle of Korean naval engineering.

This was the "sea" leg that Hanwha needed to complete its land-sea-air portfolio—the missing domain that would allow it to offer a comprehensive sovereign defense package to foreign customers who needed armies, navies, and air forces, not just one of the three. Imagine an Indo-Pacific nation facing a maritime territorial dispute: it needs patrol frigates to assert sovereignty, howitzers to defend its coastline, air defense radars to protect its ports, and the ammunition to supply all of them. Before the reorganization, that customer would need to engage multiple companies across multiple countries. After the reorganization, one call to Hanwha covers land, sea, air, and the supply chain to sustain all three.

Third, the price was right. The Korea Development Bank was a motivated seller with no other options after the Hyundai deal collapsed. Hanwha paid $1.5 billion for control of a shipyard that, given the LNG order cycle, was about to enter the most profitable period in its history. This was classic Hanwha opportunistic buying—acquiring a troubled asset at a cyclical trough, when no one else wanted it, and riding the subsequent recovery.

The results validated the thesis faster than almost anyone expected. In fiscal year 2025, the first year of full twelve-month consolidation, Hanwha Ocean contributed 12.69 trillion won in revenue and 1.11 trillion won in operating profit to Hanwha Aerospace's consolidated results. To put that in perspective, Hanwha Ocean alone generated more revenue in 2025 than all of Hanwha Aerospace's consolidated businesses had generated just two years earlier. The enterprise value implied by those earnings dwarfs the acquisition price several times over.

The consolidated Hanwha Aerospace that emerged from this reorganization is a fundamentally different company from what existed before. Total consolidated revenue surged from 7.89 trillion won in fiscal 2023 to 11.24 trillion in 2024 and then to 26.61 trillion in 2025—more than tripling in two years. Operating profit hit a record 3.09 trillion won.

The company's market capitalization, which had been roughly five trillion won as recently as 2020, now exceeds seventy trillion won—more than a fourteen-fold increase in five years. The stock has been one of the best-performing defense names globally, with a five-year return exceeding 2,800 percent.

One important accounting note that investors should understand: net income actually declined from 2.30 trillion won in fiscal 2024 to 2.14 trillion won in fiscal 2025, despite the massive revenue and operating profit growth. This apparent contradiction is explained by a one-time accounting event.

The 2024 net income figure was inflated by a large revaluation gain that occurred when Hanwha Aerospace's existing minority stake in Hanwha Ocean was marked to fair value upon full consolidation—a non-cash accounting adjustment required by Korean IFRS standards, not an operating result. Think of it this way: Hanwha already owned a piece of Hanwha Ocean before acquiring full control. When they consolidated, accounting rules required them to revalue that existing piece at current market prices and book the difference as a gain. It was a paper windfall, not cash flowing into the business. Stripping out that noise, the underlying operating earnings power of the business grew substantially year over year, which is the number that matters.

And the order backlog—the single most important leading indicator for any defense company—reached 37.2 trillion won in the land defense segment alone, securing revenue visibility through approximately 2030. Roughly seventy percent of that backlog consists of export contracts, which carry significantly higher margins than domestic Korean military orders.

Hanwha had built, in the space of a decade, the vertically integrated, multi-domain defense champion that the South Korean government had always wanted and that the global market suddenly needed. The management vision articulated during the reorganization was even more ambitious than what the numbers alone suggest. In announcing the defense consolidation, Hanwha Aerospace unveiled a new corporate vision targeting forty trillion won in consolidated revenue by 2030, built on three pillars: defense solutions, space and aerospace technology, and new mobility. The defense pillar was already delivering. The space pillar was being assembled. And the new mobility pillar—well, that would prove to be more complicated, as we will see.

But the segmental breakdown of fiscal 2025 results tells the story of a genuinely diversified defense and industrial conglomerate. Land defense generated 8.13 trillion won in revenue and 2.01 trillion won in operating profit—a margin of roughly twenty-five percent that reflects the pricing power of export contracts signed during the peak of European urgency. The aerospace and propulsion segment contributed 2.51 trillion won. And Hanwha Ocean added its massive top line. This is no longer a single-product company—it is a multi-domain platform.

The question was who was driving this transformation—and the answer leads to a forty-two-year-old Harvard graduate with a plan to take the company from artillery shells to the stars.

V. Management: The Era of Kim Dong-kwan

Every great corporate transformation has a human architect, and Hanwha's transformation has Kim Dong-kwan.

Born on October 31, 1983, the eldest son of Hanwha Group Chairman Kim Seung-youn, Dong-kwan was educated in the United States in a way that was designed, from the start, to prepare him for global leadership. He attended the elite St. Paul's School in Concord, New Hampshire—one of America's most prestigious boarding schools, whose alumni include John Kerry, Robert Mueller, and a constellation of Wall Street titans.

From there, he went to Harvard University, where he studied political science—not engineering, not business, but the discipline that teaches you to think about power, institutions, and the structures that shape how societies make decisions. It was, in retrospect, the perfect preparation for someone who would need to navigate the intersection of government procurement, geopolitical strategy, and corporate empire-building.

He is often referred to simply as "Dong Kim" in international business circles, a deliberate informality that reflects his efforts to project a different image than the stereotypical Korean chaebol heir. Where his father's generation of Korean conglomerate leaders built empires through heavy industry, political connections, and sheer force of will, Kim Dong-kwan styles himself as a globally minded strategist with a vision for technology-driven transformation.

He speaks fluent English, is comfortable on stages at Davos and in meetings in Washington as well as in Seoul boardrooms, and cultivates relationships with Western technology executives and defense officials that would have been unthinkable for earlier generations of chaebol heirs who rarely ventured beyond Korean business circles. In an industry where personal relationships between corporate leaders and government procurement officials can determine the outcome of billion-dollar competitions, Kim Dong-kwan's international network is itself a strategic asset.

He joined the Hanwha Group at age twenty-seven and rose quickly through the organization, taking on leadership roles across multiple subsidiaries. He currently holds the title of Vice Chairman and serves as CEO of strategy divisions across Hanwha Corporation, Hanwha Solutions, Hanwha Aerospace, and Hanwha Impact.

That breadth of titles is not decorative—it reflects the reality that in a chaebol structure, the strategic direction of the entire group is set by the controlling family, and Kim Dong-kwan is the family member setting that direction.

There is an anecdote that circulates in Korean business circles about Kim Dong-kwan's management style. When he took over strategic oversight of the defense business, he reportedly visited the Changwon production facility and spent days on the factory floor, asking engineers detailed questions about cycle times, bottlenecks, and quality metrics. This is unusual for a chaebol heir, who typically operates at a strategic altitude far above the production line. But Kim understood that in defense manufacturing, the competitive advantage lives on the factory floor, not in the boardroom.

The anecdote reveals something important about how defense companies compete. In consumer technology, competitive advantage comes from design and software—things that happen in offices and labs. In defense manufacturing, competitive advantage comes from the production floor—from knowing which tolerances matter and which can be relaxed, from understanding how to sequence assembly steps to minimize rework, from maintaining the tribal knowledge that keeps a complex production line running at full capacity. Kim understood this intuitively, and it shaped his approach to every subsequent acquisition.

In practice, he has been the strategic brain behind the group's most consequential moves of the past decade: the defense consolidation, the DSME acquisition, the space initiative, and the push into renewable energy through Hanwha Q Cells, one of the world's largest solar cell manufacturers.

Kim Dong-kwan's leadership style is defined by what might be called "patient aggression"—the willingness to make large, contrarian bets on long time horizons, backed by the chaebol's ability to absorb near-term losses, combined with a ruthless speed of execution when the moment arrives. The Samsung Techwin acquisition was a prime example: patient in the sense that Hanwha had been building defense capabilities for decades before the opportunity arose, aggressive in the speed with which they moved to acquire when Samsung's succession dynamics created the opening. The DSME deal followed the same pattern.

The succession dynamics are worth understanding because they are material to the investment thesis. In March 2025, Chairman Kim Seung-youn transferred 11.32 percent of his Hanwha Corporation stake to his three sons. Kim Dong-kwan, as the eldest, received the largest individual portion—4.86 percent—bringing his combined direct and indirect holdings to roughly twenty-one percent of Hanwha Corp's voting power.

His two younger brothers, Kim Dong-won and Kim Dong-seon, received 5.37 percent each and are responsible for other parts of the group—Dong-won oversees the financial services affiliates, while Dong-seon manages the leisure and services businesses. The division is deliberate: each son has a domain, but Dong-kwan's domain—aerospace, defense, energy, and the holding company itself—represents the vast majority of the group's strategic value and public market capitalization.

This transfer was widely interpreted as the formal beginning of the third-generation succession—the moment when the patriarch signaled to the market, the Korean government, and the family itself that Dong-kwan would lead the group into its next chapter.

The market is pricing in what some analysts call a "succession dividend"—the expectation that Kim Dong-kwan's leadership will unlock value that the market has historically discounted due to chaebol governance concerns. His reputation is particularly tied to two initiatives: the defense transformation, which has already delivered spectacular results, and the "Space Hub," which represents the group's longest-duration, highest-ambition bet.

The cultural transformation he is attempting should not be underestimated—or taken for granted. Hanwha's legacy businesses—explosives, ammunition, heavy machinery—were run with a traditional, hierarchical, military-industrial culture that valued seniority, conformity, and process above creativity and speed. That culture was well-suited to producing artillery shells and howitzer hulls, where the premium is on zero-defect manufacturing and rigid quality control. It is not well-suited to attracting the kind of software engineers, data scientists, satellite architects, and space systems designers that Hanwha needs for its next phase.

Kim Dong-kwan has pushed to modernize the corporate culture, introducing flatter organizational structures in key divisions, English-language internal communications for internationally focused teams, and compensation packages competitive with the Korean technology sector. He has brought in executives with backgrounds at global technology companies and encouraged a startup-within-a-conglomerate mentality for the space and new mobility businesses.

Whether a seventy-year-old chaebol can truly reinvent its cultural DNA is an open question—but the effort is genuine, the resources committed are substantial, and the stakes could not be higher.

The family control structure creates both strengths and risks for investors. The strength is strategic continuity—the ability to pursue decade-long bets without quarterly earnings pressure, to hold assets through cyclical troughs, and to make acquisitions that optimize for long-term strategic position rather than near-term accretion.

The risk is the classic chaebol concern: that family interests may not always align with minority shareholder interests, particularly when it comes to related-party transactions between group affiliates, capital allocation decisions that prioritize family control over economic efficiency, and the potential for governance scandals. Chairman Kim Seung-youn himself served time in prison for embezzlement in the 2000s before receiving a presidential pardon—a biographical detail that underscores the governance risks inherent in the chaebol model.

Korean corporate governance has improved significantly over the past decade, driven by the government's "Corporate Value-Up" program aimed at reducing the so-called "Korea Discount." But the tension between family control and public shareholder value remains a structural feature of the investment.

It is worth noting one area where Kim Dong-kwan's personal bet has been conspicuous: Hanwha Solutions and its Q Cells solar energy subsidiary. This is the non-defense side of his portfolio, and it represents a significant strategic commitment to the energy transition. Q Cells is one of the largest solar cell manufacturers in the world, with production facilities in Korea, China, Malaysia, and a major new factory in Dalton, Georgia—a facility that benefited from the Inflation Reduction Act's domestic manufacturing incentives.

The solar bet is relevant to the Hanwha Aerospace story because it reveals something about Kim Dong-kwan's strategic philosophy: he is willing to commit capital to long-duration, capital-intensive bets in industries where manufacturing scale is the primary competitive advantage. Solar cells, jet engines, howitzers, and rockets have more in common than you might think—all of them require enormous upfront capital investment, all of them reward production efficiency, and all of them have learning curves where cumulative production volume drives down per-unit costs. The solar bet has not always been profitable—Hanwha Solutions has struggled with Chinese competition and oversupply—but it demonstrates the same pattern of patient, contrarian capital deployment that characterizes the defense transformation.

The question investors must answer is whether Kim Dong-kwan is a genuine visionary—using an inherited platform to build something genuinely transformative—or a well-credentialed heir executing a playbook that was inevitable given the geopolitical environment. The honest answer is probably somewhere in between.

The geopolitical tailwinds are real and would have benefited any Korean defense company. But it is worth asking: why has Hanwha outperformed so dramatically compared to other Korean defense names? Korea Aerospace Industries, Hyundai Rotem, and LIG Nex1 have all benefited from the same geopolitical environment. None has delivered the same degree of value creation. The difference is the speed and ambition of the integration strategy, the quality of the M&A execution, and the willingness to make bets—like the DSME acquisition—that others considered too risky. That is execution, and execution is a function of leadership.

VI. Hidden Gems: The Space Hub and New Frontiers

In March 2021, Kim Dong-kwan unveiled something that sounded, frankly, outlandish for a company known for making howitzers and ship hulls: a "Space Hub" that would coordinate the Hanwha Group's push to become a vertically integrated space services provider.

Not a parts supplier to someone else's space program. Not a subcontractor building components. A company that would build the rockets, manufacture the satellites, launch them into orbit, and sell the data and connectivity services they provided back on Earth. Think SpaceX meets Planet Labs, but Korean—and backed by a seventy-year-old industrial conglomerate with the manufacturing DNA to actually build the hardware.

The ambition makes more sense when you understand the hidden gem at the core of Hanwha Aerospace's business: its propulsion monopoly.

Hanwha Aerospace is the only company in South Korea that manufactures gas turbine engines. Not one of a few. The only one. To appreciate what this means, consider an analogy. Imagine if there were only one company in Germany that could make automotive engines, and every car manufacturer in the country had to source their powertrains from that single supplier. That company would have unassailable pricing power, visibility into every major program, and a guaranteed revenue base that no competitor could threaten. That is Hanwha's position in Korean aerospace.

If the Korean Air Force wants engines for its F-15K fighters, it works with Hanwha. If Korea Aerospace Industries needs turbines for the KF-21 Boramae, South Korea's ambitious next-generation stealth fighter, it works with Hanwha. If the Korean Army needs engines for its Surion helicopters, Hanwha supplies them.

The company started in the engine business back in 1979 with licensed production for GE, Pratt & Whitney, and Rolls-Royce, performing basic maintenance and gradually moving up the value chain—from simple overhaul to component manufacturing to full engine assembly. Over nearly five decades, Hanwha has produced more than ten thousand engines and accumulated the kind of metallurgical and thermodynamic expertise that cannot be acquired quickly, cheaply, or by reading textbooks. This is knowledge that lives in the hands of experienced engineers and in the institutional memory of production lines that have been running continuously for decades.

This monopoly generates significant and predictable cash flows from the domestic market—cash flows that effectively subsidize the riskier, longer-duration bets in space. It is the same structural advantage that allows a company like Lockheed Martin to fund the F-35 program: the government-guaranteed base business provides the foundation for commercial and export-driven growth. Hanwha's propulsion segment generated 2.51 trillion won in revenue in fiscal 2025—a substantial business in its own right.

The space strategy builds directly on this engine expertise, because rocket engines and jet engines are technological cousins. Both involve controlled combustion at extreme temperatures and pressures. Both require the same exotic superalloys and precision manufacturing. The critical difference is that a jet engine uses atmospheric air as its oxidizer—it sucks in air, compresses it, mixes it with fuel, and ignites the mixture. A rocket engine carries its own oxidizer because there is no air in space. But the materials challenges, the precision machining, and the quality-control discipline are fundamentally the same.

The Nuri rocket—South Korea's first domestically developed space launch vehicle—is powered by Hanwha-built liquid-propellant engines. Each Nuri uses six engines: four seventy-five-ton thrust engines clustered on the first stage, one on the second stage, and a smaller seven-ton engine on the third stage.

When the Nuri successfully placed operational satellites into orbit on its third launch in May 2023, it marked South Korea's entry into the exclusive club of nations capable of independent space access—a club that includes the United States, Russia, China, Japan, India, and the European Space Agency, and very few others.

But the commercial milestone was even more significant than the national achievement. The Korea Aerospace Research Institute transferred the full technology package for the Nuri's engines—design, manufacturing processes, testing procedures, and launch operations—to Hanwha Aerospace. From the fourth launch onward, Hanwha oversees production and launch operations, with KARI in an advisory role. The company holds exclusive rights to manufacture and launch the KSLV-II through 2032.

Think about what that means. Hanwha is becoming South Korea's de facto national space launch provider—the Korean equivalent of SpaceX's relationship with NASA, except with an even more explicit government mandate and a contractual monopoly on the launch vehicle itself.

The path from government space contractor to commercial space company is well-trodden—SpaceX itself started with NASA contracts before building the Falcon 9 into a commercial workhorse. The question for Hanwha is whether the Nuri platform can evolve into something commercially competitive. The current Nuri is a capable but modest launcher—it can place roughly 1.5 tons into low Earth orbit, compared to the Falcon 9's twenty-two tons. But for the growing market of small and medium satellite deployments, particularly for Earth observation and communications constellations, the Nuri's payload capacity is well-suited. And Hanwha has the advantage of a captive domestic customer base—the Korean government's satellite programs—that provides guaranteed launch demand while the commercial market develops.

The Korean government has announced plans to invest heavily in space through the 2030s, including a lunar exploration program and a military satellite constellation. Every one of those programs will require Hanwha's launch vehicles and engines. This provides the same kind of assured demand base that NASA contracts provided to SpaceX in its early years—a financial floor that allows the company to invest in next-generation capabilities without betting the farm on commercial demand that may not materialize for years.

The satellite dimension adds another layer. Hanwha Systems, a sister company within the group, announced plans to deploy a constellation of two thousand low-Earth orbit communications satellites by 2030—a Korean answer to Starlink, with a planned investment of roughly 500 billion won.

Meanwhile, Satrec Initiative, a satellite manufacturer that Hanwha Aerospace formally absorbed in January 2025, has a distinguished pedigree that adds immediate credibility to the space push. Satrec developed South Korea's first satellite, KITSAT-1, back in 1992—a milestone that put Korea on the space map at a time when the country was still considered a developing economy. The company is now working on the SpaceEye-T constellation, a planned fleet of four satellites designed to provide sub-daily Earth observation coverage by 2028.

Hanwha Systems is also competing for the Korean military's forty-satellite synthetic aperture radar constellation contract—a program that would provide all-weather, day-and-night surveillance capability over the Korean Peninsula and surrounding waters. In January 2026, Hanwha signed a memorandum of understanding with Canada's Telesat for sovereign LEO satellite connectivity tied to Korea's national K-LEO constellation initiative, adding yet another thread to the web of space partnerships.

The full-stack vision is ambitious but internally consistent: Hanwha Aerospace builds and operates the launch vehicles, Satrec builds the satellite buses and imaging payloads, Hanwha Systems provides the communications payloads and ground infrastructure, and the whole system is coordinated under the Space Hub.

If it works, Hanwha would be one of a very small number of entities globally capable of offering end-to-end space services—from manufacturing the rocket, to building the satellite, to launching it, to operating the communications network, to delivering data to end users. The only company that does this today at meaningful scale is SpaceX. The Chinese state-linked space enterprises are building similar capabilities, but they are constrained by export controls and geopolitical alignment issues that limit their commercial addressable market. Hanwha would be the only non-American, non-Chinese option for countries seeking integrated space services from a trusted allied partner—a positioning that carries enormous strategic value in a fragmenting world.

A word of candor is warranted about the Urban Air Mobility bet, which has been a less flattering chapter. Between 2019 and 2022, Hanwha invested approximately $170 million in Overair, a US-based company developing the Butterfly electric vertical takeoff and landing aircraft—a six-seat air taxi designed for urban commutes.

The technology was promising on paper: speeds up to 320 kilometers per hour, a range exceeding one hundred kilometers, and the kind of quiet, electric operation that regulators might actually approve for flight over congested cities. But by 2024, Overair had effectively collapsed. Prototype development stalled, capital ran dry, and most employees departed. Hanwha wrote off approximately 140 billion won on the investment.

The failure is instructive, and worth dwelling on for a moment. The eVTOL sector has been littered with casualties—Archer Aviation, Joby Aviation, Lilium, and dozens of smaller players have all struggled to translate compelling PowerPoint presentations into certified, commercially viable aircraft. The physics of electric flight are unforgiving: batteries are heavy, energy density is low relative to jet fuel, and the certification requirements for passenger-carrying aircraft are among the most stringent regulatory hurdles in any industry. Hanwha's $170 million loss on Overair is painful but not existential—it represents roughly five percent of a single year's operating profit at current levels.

More importantly, the failure suggests that Hanwha's competitive advantage lies in hardware-intensive manufacturing—engines, munitions, hulls, rocket motors—not in the software-and-battery-intensive world of electric aviation. The company's management appears to have absorbed this lesson, doubling down on propulsion and space where their decades of manufacturing DNA are a genuine and durable differentiator, rather than chasing speculative mobility concepts where the competitive dynamics favor Silicon Valley venture-backed startups over industrial conglomerates.

There is a useful way to think about Hanwha Aerospace's business portfolio using a framework that any consumer of Acquired episodes will recognize. The defense export business—K9 howitzers, Chunmoo rockets, ammunition—is the "cash cow." It generates massive, growing, and increasingly predictable revenue with expanding margins, driven by a backlog that stretches to 2030. This is the engine (pun intended) that funds everything else.

The gas turbine engine business is the "moat"—the structural competitive advantage that no competitor can replicate quickly. It provides guaranteed domestic revenue, sustains critical engineering talent, and serves as the technological foundation for both aerospace and space initiatives.

The space business is the "call option"—high risk, high potential reward, and early enough in its development that the market cannot yet assign it a reliable valuation. If it works, it transforms the company's identity and valuation multiple. If it does not, the defense cash cow and engine moat remain intact.

For investors evaluating this portfolio, the key question is whether the current market capitalization—north of seventy trillion won—fairly reflects the sum of these parts, or whether the market is either under-pricing the space option or over-paying for the defense cycle. The defense business alone, with its record backlog, provides a strong fundamental foundation. The space and propulsion businesses represent upside optionality grounded in real assets, not a startup pitch deck.

VII. The Playbook: Competitive Moats and Strategic Positioning

To understand whether Hanwha Aerospace's current trajectory is sustainable—or whether it represents a cyclical peak that will mean-revert—it helps to apply two analytical frameworks: Hamilton Helmer's Seven Powers and Michael Porter's Five Forces.

Start with Helmer's framework, which identifies the structural advantages that enable a company to sustain differential returns over time. Three of the seven powers apply to Hanwha with particular force.

Scale Economies are Hanwha's most tangible and measurable power. The K9 howitzer production line at the Changwon facility is, by multiple accounts, the most efficient self-propelled artillery manufacturing operation in the world. The company can reportedly produce a complete K9 system in approximately thirty days.

That figure sounds impossible if you are accustomed to Western defense procurement timelines, where a comparable system might take twelve to eighteen months from order to delivery. The difference lies in facility design philosophy. Western howitzer manufacturers—BAE Systems with the Archer, Krauss-Maffei Wegmann with the PzH 2000, KNDS with the Caesar—designed their facilities to produce small annual batches for their home armies, with export orders as occasional bonuses.

Hanwha designed its facility for the opposite: continuous high-volume production for a growing global customer base, with domestic Korean military orders as the baseline. The difference is analogous to a craft brewery versus an industrial brewing operation—both make beer, but the cost structures, cycle times, and scalability are fundamentally different.

The K9 claims approximately fifty-two percent of the global market for 155mm self-propelled howitzers—a staggering share for what is supposed to be a competitive, multi-supplier market. Roughly 1,800 systems have been contracted across more than a dozen countries: South Korea, Turkey (produced under license as the "Firtina"), India (the "Vajra"), Poland, Finland, Norway, Estonia, Egypt, Australia (the AS9 "Huntsman"), Romania, and Vietnam.

Each customer relationship generates decades of aftermarket revenue—spare parts, maintenance, upgrades, and ammunition—that is far more profitable than the initial platform sale. And each additional customer provides revenue to invest in production efficiency, lowering per-unit costs and making Hanwha more competitive for the next bid. The flywheel spins faster with every contract signed.

Cornered Resource operates on two levels. Nationally, Hanwha's relationship with the South Korean government is sovereign in nature. South Korea faces an existential military threat from North Korea—a country with the world's fourth-largest standing army, nuclear weapons, and thousands of artillery pieces aimed at Seoul. The Korean government treats its defense industrial base as a national security asset, not a set of commercial vendors.

Hanwha's monopoly on gas turbine engines, its role as primary Korean Army ground-systems manufacturer, and its position as national space launch provider create a relationship with the state that no foreign competitor can replicate. Internationally, the "cornered resource" is manufacturing capacity itself—in a world where Western defense producers are quoting delivery timelines in years, Hanwha's ability to produce at scale and deliver in months is a resource that desperate buyers cannot find elsewhere.

Switching Costs may be the most durable power of all. Once a country adopts the K9, it buys into an ecosystem: training curricula for thousands of gun crews, maintenance facilities with specialized tooling, ammunition supply chains optimized for the K9's autoloader, fire-control software integrated with specific command architectures, and upgrade pathways that keep the platform relevant for decades.

Poland's commitment to 672 K9 systems was not a purchase order—it was a multi-decade relationship. Switching to a competitor would mean retraining soldiers, rebuilding infrastructure, and accepting years of reduced readiness. In practice, countries almost never switch artillery platforms at scale. This is defense industry lock-in with even higher switching costs than enterprise software, because the stakes involve national security.

There is one additional dimension to the switching cost analysis that is worth highlighting: ammunition. The K9 howitzer fires NATO-standard 155mm rounds, but the automated loading system is optimized for specific ammunition configurations. Countries that adopt the K9 will procure hundreds of thousands—potentially millions—of rounds over the platform's lifetime. And who makes those rounds? Hanwha's ammunition division, which was folded into Hanwha Aerospace during the 2023 reorganization. The razor-and-blade model applies with particular force in defense: sell the howitzer (the razor) and then supply the ammunition (the blades) for thirty years. The ammunition revenue alone, over the lifetime of a major K9 contract, can rival the value of the initial platform sale.

Now turn to Porter's Five Forces.

Bargaining Power of Buyers is low. Defense procurement is driven by security imperatives, not price optimization. In the current environment—active war in Ukraine, rising Taiwan Strait tensions, Middle Eastern instability—governments are shopping for availability, not bargains. When the buyer needs delivery in months and the only supplier who can meet that timeline is Hanwha, pricing power tilts decisively toward the seller.

Threat of New Entrants is negligible. Building a credible defense manufacturing capability from scratch requires billions in capital investment, decades of accumulated engineering know-how, government security clearances at multiple levels, complex export license regimes, and established relationships with military procurement bureaucracies that take years to develop. The barriers to entry are among the highest in any industry. China is the only country that has built a new, large-scale defense industrial base in recent decades, and it did so with the resources of the world's second-largest economy and a willingness to appropriate Western intellectual property on a massive scale—a path that is not available to commercial competitors.

Threat of Substitutes deserves nuance. The war in Ukraine has emphatically demonstrated that artillery remains the dominant killer on the modern battlefield. You cannot replace tube artillery with drone swarms when the objective is sustained, high-volume firepower across a wide front. In the longer term, autonomous systems and precision-guided munitions are changing warfare, but Hanwha's investments in the Chunmoo rocket system and guided munitions position it to ride this transition rather than be displaced.

Rivalry Among Existing Competitors is moderate but shifting in Hanwha's favor. Western primes have the technology and brand recognition but lack production capacity and delivery speed. They were optimized for the post-Cold War environment of small batches and long timelines. Hanwha was built for volume and speed. As European rearmament accelerates, the competitive dynamic favors the manufacturer who can actually deliver.

The key risk to watch: whether European governments successfully rebuild domestic defense industrial capacity. Rheinmetall's announced expansions are significant. If European manufacturers can scale up within five to seven years, the Korean export supercycle could moderate. The counter: even with new capacity, Western cost structures are unlikely to match Korean efficiency, and non-European customers in the Middle East, Southeast Asia, and South America will continue to prefer Korean systems on price, availability, and the absence of political conditions that Western governments sometimes attach to arms sales.

One additional power from Helmer's framework deserves mention: Process Power. This is the advantage that comes from deeply embedded organizational capabilities that have been refined over decades and cannot be easily replicated by competitors. Hanwha's manufacturing processes—the ability to produce a K9 in thirty days, the quality control systems inherited from the Samsung Techwin engine business, the logistics infrastructure for managing global export deliveries—represent accumulated institutional knowledge that exists in the organization's muscle memory, not in any document or blueprint. You could give a competitor Hanwha's factory blueprints, and they still could not match the output for years, because the knowledge lives in the people and the processes, not on paper.

This is particularly relevant when evaluating the competitive threat from European manufacturers. Rheinmetall can build new factories. It can hire engineers. It can invest billions. But it cannot instantly replicate fifty years of production experience, thirty years of export relationships, and a supply chain that has been optimized across dozens of customer configurations. Process power takes decades to build and cannot be acquired—only earned.

The synthesis across both frameworks: Hanwha possesses genuine, multi-layered competitive advantages that are structural rather than purely cyclical. The risk is not that these advantages will evaporate—it is that the geopolitical urgency turbocharging them may eventually normalize, shifting the competitive dynamics from "who can deliver fastest" back to "who has the best technology at the best price." Even in that scenario, Hanwha's cost advantage and scale position it well. But the premium that urgency provides—the ability to charge higher prices and negotiate favorable terms because the buyer has no alternative—would diminish.

VIII. Bear vs. Bull Case

Every investment thesis has two sides, and Hanwha Aerospace is no exception. The bull and bear cases are both intellectually honest.

The Bear Case rests on three pillars.

First, the geopolitical thaw scenario. Hanwha's valuation reflects an assumption that the defense supercycle will persist for years. A negotiated settlement in Ukraine, a diplomatic breakthrough on Taiwan, or simple "defense spending fatigue" among European electorates could slow budget growth. The K9 backlog is impressive, but backlog is not revenue—framework agreements can be modified, executive contracts delayed, and quantities reduced. The Poland deal stretches across multiple contracts signed over several years, and a future government with different priorities could scale back later tranches.

Second, integration risk. Hanwha has absorbed enormous organizational complexity in a short period: Samsung Techwin, Hanwha Defense, Hanwha Corp's defense division, Satrec Initiative, and the former DSME. Each integration carries execution risk—clashing cultures, redundant operations, legacy liabilities, and management bandwidth strain. Hanwha Ocean's history of periodic catastrophic losses from shipbuilding cost overruns is well-documented, and a major mishap could create earnings volatility the market has not priced in.

Third, governance and succession risk. The Kim family's chaebol control structure concentrates decision-making power in ways that create key-person risk. Korean chaebol history provides ample cautionary tales—Samsung's succession scandal, the Lotte family feud, the Hanjin collapse. The elder Chairman Kim's own prison term for embezzlement, though followed by a pardon, is a reminder that these risks are historical and recurring, not hypothetical.

Fourth, and often overlooked: currency risk. Hanwha reports in Korean won, but a growing share of its revenue is denominated in euros, US dollars, and other currencies through export contracts. A strengthening won would compress reported margins on these contracts. More subtly, many export contracts include price escalation clauses that may not fully offset raw material cost inflation—steel, nickel, and the exotic superalloys used in engine manufacturing are all subject to commodity cycles that Hanwha cannot control. The record margins of fiscal 2025 may reflect an unusually favorable alignment of pricing power and input costs that is difficult to sustain indefinitely.

There is also a regulatory and political dimension. South Korea's defense exports are subject to government approval, and Seoul has historically been cautious about selling weapons to conflict zones or to countries that might create diplomatic complications with major trading partners like China. A future Korean government with a different foreign policy orientation could impose tighter export restrictions, limiting the addressable market for Hanwha's products. The current permissive export environment should not be taken as a permanent state of affairs.

The Bull Case is equally forceful.

The "New Cold War" thesis argues that the structural shift toward higher defense spending will persist for a generation. NATO countries have committed to minimum spending targets that most have not reached. Indo-Pacific nations are arming at an accelerating pace. The Middle East remains an arms bazaar. Hanwha is uniquely positioned as the high-volume, cost-competitive alternative to capacity-constrained Western primes. Management's target of forty trillion won in consolidated revenue by 2030 appears achievable given the backlog trajectory.

The "engine monopoly" thesis focuses on propulsion as an underappreciated asset. Gas turbine engine programs last forty to fifty years, and the aftermarket generates some of the highest margins in industrial manufacturing. As Hanwha moves toward indigenous engine design, the value of this business could increase dramatically.

The "Space Hub" thesis treats space investments as a call option on a multi-trillion-dollar addressable market. If Hanwha can commercialize Nuri technology, deploy satellite constellations, and become Asia's premier space services provider, the upside would dwarf the current defense business. This is speculative but grounded in demonstrated technology, exclusive manufacturing rights, and a domestic monopoly.

The "technology transfer" thesis adds another dimension. As Hanwha executes its export contracts, many of which include technology transfer and local production agreements—Poland is producing K9PL variants domestically, Turkey has manufactured the Firtina for decades, India assembles the Vajra locally—the company is building a global network of manufacturing partners and service relationships. Each technology transfer deal creates a long-term dependency: the local production partner needs Hanwha's proprietary components, technical support, and upgrade packages for decades. What looks like Hanwha "giving away" technology is actually a strategy for creating permanent revenue streams and deepening switching costs across multiple geographies simultaneously.

The financial trajectory supports the bull case in the near term. Revenue has tripled in two years. Operating profit hit a record. The backlog provides years of visibility with the higher-margin export mix at seventy percent. The stock's five-year return of over 2,800 percent reflects a fundamental re-rating of Korean defense.

The honest assessment: both cases contain substantial truth. The geopolitical tailwinds are real but not permanent. Integration risks are real but manageable. Governance risks are real but partially mitigated by improving Korean standards. The space opportunity is real but early-stage. A useful comparison helps frame the scale of what Hanwha has become. In fiscal year 2025, Hanwha Aerospace's consolidated revenue of 26.61 trillion won—roughly $19 billion at current exchange rates—puts it in the same revenue tier as companies like L3Harris Technologies or General Dynamics' combat systems and marine divisions combined. Five years ago, it was a fraction of that size. The speed of this transformation has no real precedent in the global defense industry. The American defense consolidation of the 1990s took a decade. Hanwha achieved something comparable in half that time.

What is indisputable is that Hanwha occupies a structural position in global defense—as the most vertically integrated, highest-volume, fastest-delivering non-Western defense prime—that did not exist five years ago and will be very difficult for competitors to replicate. Whether that position commands a premium or a discount in the next market cycle depends on variables—geopolitical tension, European industrial policy, Korean governance reform—that are genuinely uncertain. That uncertainty is, in itself, perhaps the most honest conclusion one can reach about a company that has been on the right side of history for seven decades and counting.

IX. Epilogue: From the Rubble to the Stars

For those who have followed the Hanwha story from the beginning—from a small explosives factory in war-torn Korea to a seventy-trillion-won defense and aerospace conglomerate—the scale of the transformation is almost disorienting. The company's stock traded below 50,000 won as recently as 2020. It now trades above 1,300,000 won. The market capitalization has grown from a rounding error in global defense terms to a figure that puts Hanwha in the same conversation as companies that have been building aircraft carriers and stealth fighters for generations.

But market capitalization is a snapshot. What matters for long-term investors is whether the underlying business can sustain its current trajectory—or whether the stock has priced in a decade of growth that may not fully materialize. Two numbers matter more than any others for tracking Hanwha Aerospace's ongoing performance.

The first is order backlog, particularly in the land defense segment. At 37.2 trillion won as of end of fiscal 2025, it represents roughly four to five years of defense segment revenue at current run rates. The critical metric to monitor is the book-to-bill ratio—whether new orders continue to exceed revenue recognition each quarter.

A ratio consistently above one signals the supercycle is still accelerating. A ratio declining toward one signals maturation. The composition matters too: export contracts at roughly seventy percent of the mix carry significantly higher margins than domestic Korean orders, so a shift in mix toward domestic would compress profitability even if total backlog remains stable.

The second is Hanwha Ocean's operating margin trajectory. The shipbuilding subsidiary is the newest, largest, and most volatile piece of the consolidated entity. Shipbuilding margins are notoriously cyclically sensitive—a single problematic vessel, a steel price spike, or a currency swing can erase a quarter's profit.

Whether Hanwha Ocean can sustain the margin it demonstrated in its first full consolidation year—roughly eight to nine percent operating margin—or revert to the volatility of the DSME era will be a critical determinant of earnings quality and investor confidence going forward.