Samsung Electro-Mechanics: The Ceramic Moat and the AI Frontier

I. Introduction: The Most Important Company You've Never Heard Of

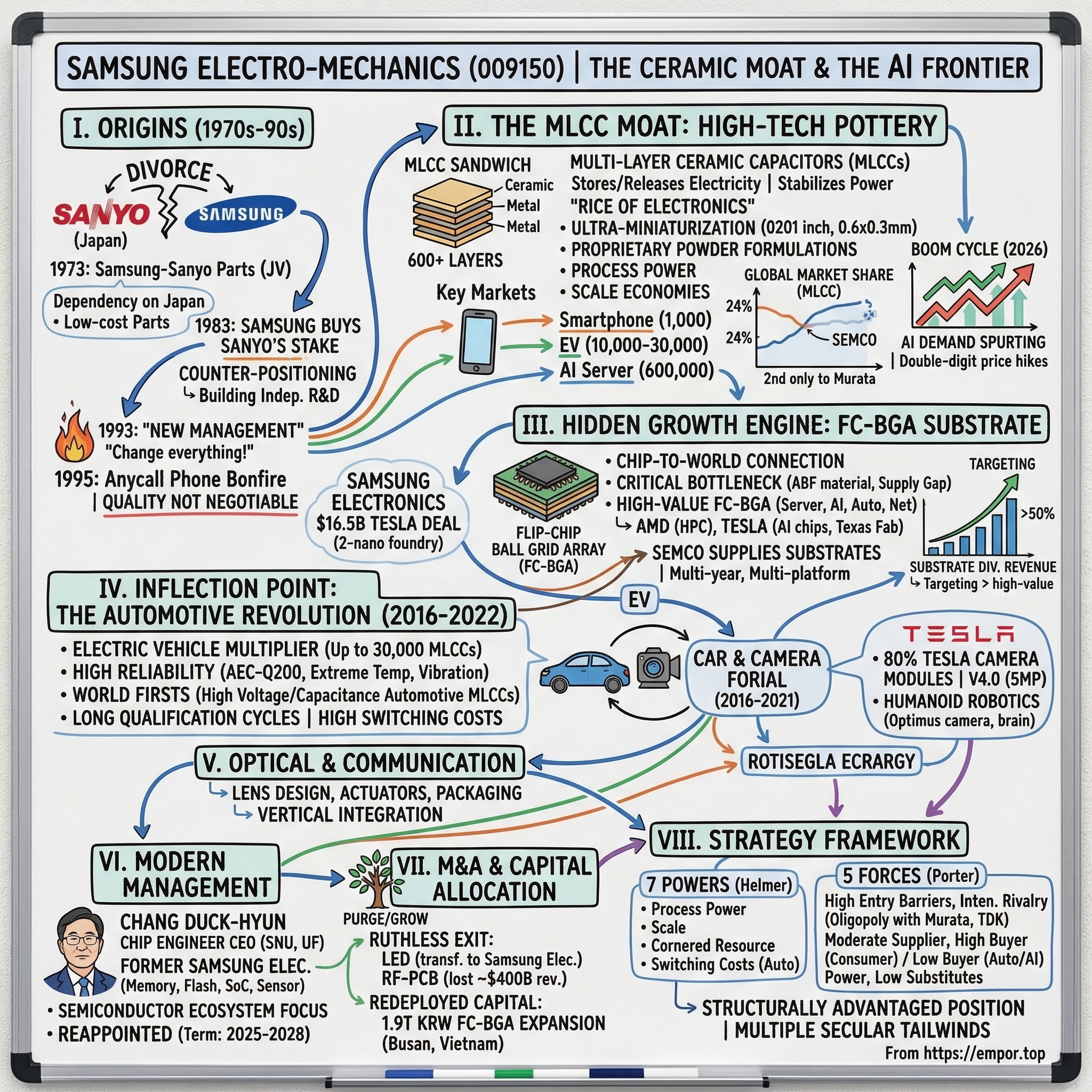

Pick up your smartphone. Look at it. Inside that sleek slab of glass and aluminum, there are roughly a thousand tiny components so small they resemble grains of sand. They do not glow, vibrate, or display pixels. They sit silently on the circuit board, storing and releasing infinitesimal bursts of electricity to keep every chip, antenna, and sensor functioning in perfect harmony. Most people have never heard of them. They are called MLCCs, multi-layer ceramic capacitors, and the world runs on them.

Now consider this: every Tesla rolling off the line in Fremont or Shanghai contains not a thousand of these components, but thirty thousand. Every NVIDIA AI server rack powering the generative AI revolution uses over six hundred thousand. And the company that makes more of these tiny ceramic bricks than anyone except one Japanese rival is not a household name. It is Samsung Electro-Mechanics, known in the industry as SEMCO, a Suwon-based subsidiary of Samsung Group that most people have never thought about, even as it quietly became one of the most important industrial companies on the planet.

The numbers tell one story. SEMCO crossed ten trillion Korean won in annual revenue for the first time in 2024, roughly seven and a half billion US dollars. In 2025, it pushed past eleven trillion won and set another record. Operating profit surged twenty-four percent year over year. Analysts now project the company will earn over 1.3 trillion won in operating profit in 2026, a figure that would have seemed fanciful just three years ago. But the numbers alone miss the deeper narrative. SEMCO is not merely big. It is strategically irreplaceable.

The company holds roughly twenty-four percent of the global MLCC market, second only to Japan's Murata Manufacturing. It supplies an estimated eighty percent of Tesla's camera modules for its Full Self-Driving system. It recently secured a role as the substrate supplier for Tesla's next-generation AI chips, manufactured at Samsung Electronics' two-nanometer foundry in Taylor, Texas. It is shipping MLCCs into low-earth-orbit satellites for a major American aerospace company widely understood to be SpaceX. And it is doing all of this from a position that took fifty years, hundreds of billions of dollars in cumulative investment, and a mastery of materials science so esoteric that fewer than five companies on Earth can replicate it.

The thesis of this story is deceptively simple. Samsung Electro-Mechanics started life in 1973 as a joint venture assembling parts for a Japanese electronics giant. Over five decades, it transformed itself into a high-margin materials science powerhouse that owns what the industry calls the "Rice of Electronics," a component so ubiquitous and indispensable that modern civilization literally cannot function without it. And now, as the world pivots toward electric vehicles, autonomous driving, and artificial intelligence, SEMCO finds itself sitting at the exact intersection of every major technology trend that matters. The question is whether this ceramic moat is as durable as the materials it produces, or whether the cycles, geopolitics, and rising competition from China will erode it before the full promise is realized.

To understand where SEMCO is going, you have to understand where it came from. And that story begins in a Korea that no longer exists.

II. Origins: The Sanyo Divorce and the Identity Crisis (1973-1990s)

In the early 1970s, South Korea was an electronics desert. The country that would one day produce Samsung Galaxy phones, LG OLED televisions, and SK Hynix memory chips was almost entirely dependent on Japanese imports for the basic components that made electronic devices work. Capacitors, resistors, tuners, speakers, every small part that went inside a radio or television had to be shipped across the Sea of Japan. For Samsung Group's ambitious founder Lee Byung-chul, this dependency was both a humiliation and an opportunity.

The solution was a technology transfer deal with Sanyo Electric, one of Japan's leading consumer electronics companies. On March 20, 1973, Samsung and Sanyo signed a joint venture contract. Five months later, on August 8, Samsung-Sanyo Parts Co., Ltd. was formally incorporated. The arrangement was typical of the era: the Korean side provided labor and land, the Japanese side provided technology and expertise. Samsung-Sanyo Parts would manufacture audio and video components, essentially serving as a low-cost production arm for Sanyo's supply chain.

For a decade, this was the company's identity. It made parts. It followed specifications handed down from Osaka. It competed on cost, not on capability. The name itself told the story: Samsung-Sanyo Parts. Not "Electronics," not "Technology," just "Parts." In the taxonomy of industrial ambition, it was barely above contract manufacturing.

The first inflection came in 1977, when the company was renamed Samsung Electronic Parts, a subtle but meaningful assertion of identity separate from Sanyo. But the truly transformative moment arrived in 1983, when Samsung bought out Sanyo's stake entirely. In the language of Hamilton Helmer's strategic framework, this was a classic act of counter-positioning. Samsung was not merely acquiring equity. It was severing the umbilical cord to Japanese technology dependence and betting that its own engineers could develop proprietary processes.

This was not an obvious bet. Korea's electronics industry in the early 1980s was still decades behind Japan. Samsung's engineers had been trained on Sanyo's methods, using Sanyo's materials, building Sanyo's designs. Striking out alone meant building an independent R&D infrastructure from scratch, recruiting scientists who could develop proprietary ceramic formulations, and somehow competing against companies like Murata and TDK that had been refining their craft since the 1940s. It was the industrial equivalent of a medical resident deciding to open their own hospital.

The 1987 name change completed the symbolic transformation. Samsung Electronic Parts became Samsung Electro-Mechanics, a name that signaled ambition to move up the value chain from simple components to integrated modules and advanced materials. The goal was no longer to be the cheapest maker of commodity parts. It was to become a materials science company that happened to make electronic components.

Then came the event that changed everything for every Samsung subsidiary. In June 1993, Samsung Group chairman Lee Kun-hee convened a meeting with senior executives in Frankfurt, Germany, and delivered what became known as the "New Management" declaration. His directive was blunt and now legendary: "Change everything except your wife and children." Lee believed Samsung had become complacent, producing high volumes of mediocre products while Japanese competitors dominated on quality. He wanted nothing less than a complete cultural revolution within the group.

The message hit SEMCO hard and productively. Two years later, Lee visited a Samsung plant in Gumi and ordered employees to incinerate one hundred and fifty thousand defective Anycall cellphones worth fifty billion won. They built a bonfire of phones and watched them burn. The symbolism was unmistakable: quality was no longer negotiable.

For SEMCO, the New Management philosophy meant that being a competent assembler of Japanese-designed components was no longer acceptable. The company had to develop world-class capabilities in materials science, push into higher-margin product categories, and compete head-to-head with Murata and TDK on technical specifications, not just price. The journey from Samsung-Sanyo Parts to a genuine MLCC powerhouse had officially begun. But it would take another two decades of relentless investment in ceramic powder formulations, lamination techniques, and manufacturing scale before the company could credibly claim a seat at the top table.

The transformation from parts assembler to materials science leader set the stage for SEMCO's most important product category, the one that would eventually account for more than seventy percent of its earnings and earn the nickname that defines the entire passive components industry.

III. The MLCC Moat: High-Tech Pottery

Imagine a sandwich. Not the kind you eat, but one built at the molecular level. Start with a sheet of ceramic so thin it is measured in microns, roughly one-fiftieth the thickness of a human hair. Screen-print a layer of metal paste onto it, forming an electrode. Stack another ceramic sheet on top. Another electrode. Repeat this process six hundred times or more. Now compress the entire stack into a block smaller than a grain of rice. Fire it in a kiln at over twelve hundred degrees Celsius to fuse the ceramic layers into a single crystalline structure. Apply terminal electrodes to each end. Congratulations, you have just made one multi-layer ceramic capacitor, and the world manufactures approximately one trillion of them every year.

An MLCC does something deceptively simple: it stores electrical charge and releases it on demand. Think of it as a tiny dam in an electrical circuit. When voltage spikes, the capacitor absorbs the excess. When voltage drops, it releases stored energy to maintain a steady flow. Without this function, the processors in your phone would crash, the sensors in your car would malfunction, and the GPUs training large language models would produce garbage. Every electronic circuit needs stable power, and MLCCs are the primary mechanism for delivering it.

The reason they are called the "Rice of Electronics" is not just a poetic flourish. It is a precise analogy. Rice is the staple food of half the world's population: cheap in unit cost, consumed in enormous quantities, and absolutely essential to survival. MLCCs occupy the same position in electronics. A single 5G smartphone contains over a thousand of them. A modern electric vehicle uses up to ten thousand. An NVIDIA NVL72 AI server rack, the kind powering the largest generative AI training runs, contains approximately six hundred thousand. No other electronic component is manufactured in such astronomical volumes or deployed across such a vast range of applications.

What makes the MLCC business so defensible is not the concept, which any engineering student can understand, but the execution. Stacking six hundred layers of ceramic and metal in a space the size of a needle tip requires manufacturing precision that borders on the absurd. The ceramic powder must be refined to nano-scale particles with proprietary surface coatings to prevent clumping. The slurry must be cast into uniform sheets with zero defects. The metal paste must be printed with sub-micron accuracy. The lamination process must align hundreds of layers without any misregistration. A single speck of dust entering the cleanroom at the wrong moment can ruin an entire batch. And then the whole thing has to survive a kiln at temperatures that would melt aluminum, emerging as a dense, crack-free ceramic monolith with predictable electrical properties.

This is what Hamilton Helmer would call Process Power. The knowledge required to achieve high yields on ultra-small, ultra-high-capacitance MLCCs is accumulated over decades and embedded in tacit know-how that cannot simply be licensed or reverse-engineered. Only a handful of companies on Earth, Murata, SEMCO, TDK, and Taiyo Yuden, can do this at scale with yields high enough to be economically viable. Murata leads with roughly forty percent global market share. SEMCO holds approximately twenty-four percent. Together, the top four or five producers control seventy to seventy-five percent of the high-end market. Chinese manufacturers, led by companies like Fenghua Advanced Technology, have reached ten percent total share, but remain concentrated in commodity-grade products where the technical barriers are lower.

SEMCO rode the smartphone revolution of the 2010s to build its MLCC business into a global force. As Samsung Electronics and Apple pushed for thinner phones with more features, the demand for smaller, higher-capacitance MLCCs exploded. SEMCO responded by driving miniaturization to levels that seemed physically impossible. Its engineers developed the world's first 0201-inch industrial MLCC, a capacitor measuring just 0.6 by 0.3 millimeters, about the size of a grain of fine sand. They created 0402-inch MLCCs for AI server power delivery that save more than fifty percent of mounting area compared to the prior generation. They pushed automotive MLCCs to forty-seven microfarads in the 0805 form factor, the highest capacitance automotive MLCC ever produced.

The competitive dynamics of this market are revealing. During the supply crisis of 2018, when surging demand collided with Japanese manufacturers strategically shifting capacity toward automotive-grade products, MLCC prices spiked forty to fifty percent in some categories. SEMCO, Murata, and Taiyo Yuden collectively held sixty percent of the market and had enormous pricing power. SEMCO used the cycle to expand its market share from twenty-two percent in 2019 to twenty-five percent by early 2021, demonstrating the classic oligopoly dynamic: in a market with extreme barriers to entry, supply crunches benefit incumbents disproportionately.

One critical and underappreciated aspect of SEMCO's MLCC moat is its proprietary ceramic powder formulations. The dielectric material inside an MLCC determines its capacitance, voltage rating, temperature stability, and reliability. These powder recipes, developed over decades of iterative refinement, represent what Helmer would call a Cornered Resource. CEO Chang Duck-hyun has stated that the company will develop and manufacture core MLCC raw materials in-house to enhance technological competitiveness, effectively verticalizing into the most strategically sensitive input of its own manufacturing process.

In early 2026, the MLCC market entered what analysts describe as a boom cycle. SEMCO began weighing double-digit price increases effective April 2026, driven by insatiable demand from AI server manufacturers. Spot prices had already risen fifteen to twenty percent by February. High-end MLCC prices were expected to climb thirty to forty percent through the year. Murata confirmed its own April price hike. The structural dynamic driving this cycle is straightforward: AI servers consume three to four thousand MLCCs each, compared to fewer than a thousand in traditional servers, and the buildout of AI data center capacity is accelerating, not decelerating.

For investors tracking SEMCO, the MLCC business is the center of gravity. It accounts for more than seventy percent of projected 2026 earnings. Its margins expand during upcycles because pricing power accrues to the incumbents who control scarce high-end capacity. And its growth is now being driven by three simultaneous structural tailwinds, smartphones, electric vehicles, and AI servers, a combination that has never existed before in the history of passive components.

But MLCCs are not the only story. Hidden in SEMCO's financial statements is a segment that barely registered five years ago and is now attracting the attention of every AI infrastructure investor in the world.

IV. The Hidden Growth Engine: The Substrate Story (FC-BGA)

To understand why SEMCO's substrate business matters, you first need to understand a problem that almost nobody outside the semiconductor industry thinks about: how do you connect a chip to the rest of the world?

A modern AI processor like NVIDIA's H100 or AMD's MI300 is an extraordinary piece of engineering, billions of transistors etched onto a sliver of silicon smaller than a postage stamp. But a bare chip is useless by itself. It needs to be connected to a circuit board that supplies power, routes signals, and dissipates heat. The piece of technology that performs this critical intermediary function is called a substrate, specifically an FC-BGA substrate, which stands for Flip-Chip Ball Grid Array. Think of it as the foundation upon which the chip sits, a multi-layered circuit board made of specialized resin and copper that translates the chip's thousands of microscopic connections into a format the rest of the system can work with.

For decades, substrates were an afterthought, a commodity purchased by the truckload from a handful of Japanese and Taiwanese specialists. But as chips have grown more complex, denser, and more power-hungry, the substrate has become a critical bottleneck. The AI chips going into next-generation data centers require substrates with more layers, finer line widths, and tighter tolerances than anything previously manufactured. And demand is so far ahead of supply that a twenty percent supply gap persists in the ABF substrate market, the specific material system used for high-end FC-BGAs. Some electronics manufacturers report that even commodity product lines are being delayed because their packaging subcontractors are fully booked filling lucrative AI chip substrate orders.

This is the market SEMCO is charging into. The company has invested approximately 1.9 trillion Korean won, roughly 1.6 billion US dollars, to build FC-BGA production capacity at new factories in Busan, South Korea, and Vietnam. Both facilities use AI-driven deep learning technology for automated recipe optimization and real-time quality analysis. Customer orders currently exceed production capacity by more than fifty percent. Two years' worth of next-generation FC-BGA production volume is essentially sold out.

SEMCO's three business segments tell a clear strategic story. The Component Solutions division, anchored by MLCCs, is the cash cow generating the majority of earnings. The Optical and Communication Solutions division, centered on camera modules, serves as the bridge to automotive and robotics customers. And the Package Solutions division, built around FC-BGA substrates, is the hidden gem that analysts are rapidly re-rating.

The customer wins in substrates have been dramatic. In mid-2024, SEMCO signed a high-performance computing FC-BGA supply agreement with AMD, with mass production commencing for hyperscale data center computing substrates. Then came the deal that changed the narrative entirely. In July 2025, Samsung Electronics signed a sixteen-and-a-half-billion-dollar chip manufacturing agreement with Tesla, running through 2033. Under that arrangement, Samsung's foundry will manufacture Tesla's AI5 and AI6 processors at two-nanometer process technology at Samsung's massive thirty-seven-billion-dollar fab in Taylor, Texas. And SEMCO is expected to supply the ABF substrates that those chips sit on.

The implications are staggering. Tesla's AI chips power its Full Self-Driving systems across every vehicle in its lineup, from Model 3 to Cybertruck to Semi. They power the Optimus humanoid robot. They power the Grok AI inference clusters in Tesla's data centers. This is not a one-product relationship. It is a multi-platform, multi-year integration into Tesla's entire silicon ecosystem.

The competitive landscape in FC-BGA substrates is dominated by Japanese and Taiwanese companies. The top five players, Unimicron, Ibiden, Nan Ya PCB, Shinko Electric Industries, and Kinsus Interconnect, collectively hold an estimated sixty to sixty-five percent of the market by revenue. SEMCO is the challenger, playing catch-up in a market with a massive and growing supply deficit. The company's target is to increase high-value FC-BGA, meaning substrates for servers, AI accelerators, automotive, and networking, to more than fifty percent of substrate division revenue by 2026.

Is SEMCO overpaying for this expansion? The benchmarks suggest not. Ibiden and Shinko have both invested billions in capacity expansion with similar lead times and capital intensity. AT&S of Austria has committed over a billion euros to its own substrate buildout. The difference is that SEMCO benefits from a captive relationship with Samsung Electronics' foundry business, which provides a degree of demand visibility that standalone substrate makers lack. When Samsung Foundry wins a major chip contract, SEMCO has an inside track on the substrate orders that follow.

The Package Solutions division is expected to grow sales twenty-three percent year over year in 2026. The semiconductor substrate market overall is projected to expand from 4.8 trillion won in 2024 to eight trillion won by 2028. SEMCO's bet is that the insatiable demand for AI compute will make high-end substrates a structural growth business for the rest of the decade, and its early investments in capacity will translate into share gains against entrenched incumbents.

This is the part of the SEMCO story that the market is just beginning to price in. But the substrate narrative dovetails with an even older strategic pivot, one that started with a simple arithmetic problem about electric cars.

V. Inflection Point: The Automotive Revolution (2016-2022)

The math is what gets you. A smartphone contains roughly a thousand MLCCs. An electric vehicle contains up to ten thousand, and some industry estimates push the number as high as thirty thousand when you include every subsystem from battery management to advanced driver-assistance to infotainment. But it is not just the volume that matters. Automotive-grade MLCCs sell for a dramatic premium over their consumer-grade counterparts.

The reason is survival. A capacitor inside your smartphone operates in a climate-controlled pocket at temperatures between zero and forty degrees Celsius. If it fails, your phone reboots. A capacitor inside an electric vehicle's battery management system operates in environments ranging from negative fifty-five to one hundred and fifty degrees Celsius, enduring constant vibration, thermal shock, and mechanical stress. If it fails, the car could lose power steering, brake assist, or battery regulation. This is a component utilized in machinery responsible for human life, as the automotive qualification standards put it. Every automotive MLCC must comply with AEC-Q200 stress test qualification, a regime so demanding that the design concepts, material formulations, cover plate thickness, side margins, and terminal electrode construction are fundamentally different from consumer parts.

The qualification cycle alone creates enormous switching costs. Getting an MLCC qualified for a specific automotive platform takes years of testing and validation. Once a supplier is designed into a vehicle's safety-critical systems, replacing them is extraordinarily difficult. The automaker would need to re-qualify the replacement part through the same multi-year process, with all the engineering resources and schedule risk that implies. This is the switching cost dynamic that makes automotive MLCCs so strategically valuable: the initial design win creates a revenue stream that persists for the entire production life of the vehicle platform, typically five to seven years.

SEMCO recognized this dynamic earlier than most and began systematically building its automotive MLCC portfolio in the mid-2010s. Its Philippine factories in Calamba had been producing automotive MLCCs since 2000, developing deep expertise in the reliability engineering required for powertrains, ABS systems, and ADAS sensors. But the real acceleration came with the rise of electric vehicles, which dramatically increased both the volume of MLCCs per vehicle and the technical requirements for high-voltage, high-temperature operation.

The company's engineering achievements in automotive MLCCs are genuinely remarkable. SEMCO developed the world's first 0805-inch automotive MLCC with forty-seven microfarads of capacitance at four volts, rated for the X7T temperature range of negative fifty-five to one hundred and twenty-five degrees Celsius. It created a 1210-inch high-voltage MLCC delivering thirty-three nanofarads at one thousand volts for CLLC resonant circuits in EV charging systems, solving the notoriously difficult simultaneous challenge of high voltage and high capacitance through proprietary dielectric material design. It pushed miniaturization to the 0402-inch form factor for automotive applications, achieving twenty-two nanofarads at one hundred volts in X7S temperature rating, a world first that enables dramatic space savings on increasingly crowded automotive circuit boards.

The Tesla relationship, however, is what transformed SEMCO's automotive business from an engineering story into a financial one. The camera module supply agreement, estimated at four to five trillion won in total contract value, established SEMCO as the dominant supplier of Tesla's vision system. SEMCO provides approximately eighty percent of Tesla's camera modules, with LG Innotek supplying the remaining twenty percent. The modules are Version 4.0 generation with five-megapixel resolution, a five-fold improvement over the roughly 1.2-megapixel cameras that Tesla previously used for Autopilot. These cameras are installed across every Tesla model: Model 3, Model S, Model X, Model Y, Cybertruck, and Tesla Semi.

What makes this deal strategically significant is not just its size but its scope. SEMCO is not merely selling commodity components to Tesla. It is the "vision" for Tesla's Full Self-Driving system, providing the eyes through which the car perceives the world. As Tesla expanded into humanoid robotics with the Optimus project, SEMCO followed. The company now supplies camera modules for Optimus as well, reflecting its broadening role as a core hardware partner in Tesla's physical AI ecosystem.

The camera module business also illustrates a distinctive SEMCO capability. The company is the only major camera module manufacturer that internalizes all core technologies: lens design, actuator mechanisms, and packaging. Most competitors outsource at least one of these functions. This vertical integration gives SEMCO greater control over performance, quality, and cost, and it creates a technical relationship with customers that is much stickier than a simple buy-sell transaction.

Samsung Group heir Lee Jae-yong personally inspected SEMCO's MLCC plant in the Philippines in October 2024, a visit that signaled the strategic importance of the automotive MLCC business to the broader Samsung empire. Plans are underway to expand AI server MLCC production at the Philippine facilities in 2026, alongside the automotive ramp.

The automotive revolution transformed SEMCO's earnings profile. Instead of being primarily a smartphone component supplier riding consumer upgrade cycles, the company now has a large and growing revenue base in automotive that carries higher margins, longer contract durations, and structural growth driven by EV adoption and ADAS proliferation. The shift from consumer to automotive MLCCs is SEMCO's version of the classic value migration playbook: move up the reliability and margin curve, accept longer design cycles in exchange for stickier customer relationships, and let the secular growth of electrification do the heavy lifting on volume.

The strategic pivot toward automotive and AI required a specific type of leader, someone who understood semiconductors deeply enough to see where the component industry was heading. That leader arrived in 2022.

VI. Modern Management: The Engineer-in-Chief

Chang Duck-hyun is not the kind of CEO who came up through sales, finance, or strategy consulting. He is a chip engineer. He holds a bachelor's and master's degree in electronic engineering from Seoul National University, South Korea's most prestigious technical institution, and a doctorate from the University of Florida. Before arriving at SEMCO, he spent his entire career at Samsung Electronics in the most technically demanding divisions of the company.

His resume reads like a tour of Samsung's semiconductor operation. He ran the controller development team in the memory division. He led flash memory development. He headed the solution development office and the system LSI development division, where Samsung designs the Exynos processors that power its own phones and the custom chips it manufactures for Apple, Qualcomm, and others. He ran the SoC development team, the component platform business, and the sensor business. In short, Chang spent decades building the exact types of chips that SEMCO's substrates now package and that SEMCO's MLCCs now power.

His appointment as President and CEO of Samsung Electro-Mechanics in 2022 was a signal to the market. SEMCO was no longer positioning itself as a passive components company that happened to have some semiconductor-adjacent businesses. It was positioning itself as a semiconductor ecosystem company led by someone who understood the technology roadmap of Samsung's foundry and memory divisions at the deepest level. When Chang talks about FC-BGA substrates for AI accelerators, he is not reading from a briefing document. He spent years designing the chips those substrates are built for.

Chang's leadership has been characterized by aggressive investment in high-value product categories and equally aggressive divestment of low-margin businesses. Under his tenure, SEMCO has committed 1.9 trillion won to FC-BGA substrate capacity, pushed into aerospace-grade MLCCs for satellite applications, and positioned the company as a "one-stop" component solution for humanoid robotics, a market that barely existed when he took over. He was reappointed by shareholders in 2024, with his current term running from March 2025 through March 2028, giving him a clear runway to execute the multi-year capacity buildout.

His strategic philosophy, while not publicly branded under a single initiative name, centers on shifting SEMCO's product mix toward what the company internally describes as "high-value" categories: automotive, AI servers, aerospace, and robotics. The management incentive structure reinforces this. Samsung Electronics, which owns approximately 23.7 percent of SEMCO, does not merely want its subsidiary to grow revenue. It wants SEMCO to grow the proportion of revenue coming from structurally advantaged product categories where margins are higher and competitive moats are deeper.

The corporate governance structure is worth understanding for investors. Samsung Electronics is the single largest shareholder at 23.7 percent. Institutional investors hold roughly thirty-one percent. Retail investors hold approximately forty-six percent. The Lee family exercises indirect influence through the classic Samsung chaebol structure: Samsung C&T holds a stake in Samsung Life Insurance, which holds a stake in Samsung Electronics, which holds a stake in Samsung Electro-Mechanics. This cross-holding structure creates alignment between SEMCO and the broader Samsung ecosystem, particularly Samsung Electronics' foundry and memory businesses, but it also introduces the governance complexity and minority shareholder concerns that are endemic to Korean chaebol structures.

What Chang brings that his predecessors did not is an intuitive understanding of where the semiconductor industry is heading and what that means for the component layer below. His bet is that the next decade of value creation in electronics will be driven by AI compute, autonomous systems, and advanced packaging, and that SEMCO's combination of ceramic materials expertise, substrate manufacturing, and optical systems positions it to capture a disproportionate share of that value. Whether he is right depends on the capital allocation decisions being made right now.

VII. M&A and Capital Allocation: Disciplined Focus

The most underappreciated aspect of SEMCO's strategy is not what the company has acquired, but what it has thrown away.

In a corporate world that celebrates empire-building, where conglomerates routinely accumulate divisions like trophies, SEMCO has been ruthlessly surgical about exiting businesses that do not fit its vision. The two most significant divestitures tell the story of a management team willing to sacrifice revenue in pursuit of margin and strategic focus.

The first was the LED business. SEMCO historically operated an LED division that was eventually transferred to Samsung Electronics' Device Solutions unit as part of a broader Samsung Group rationalization. Samsung Electronics itself subsequently announced in October 2024 that it would exit the mainstream LED business entirely by 2030, citing inability to compete against lower-cost Chinese producers. For SEMCO, shedding LEDs years before this industry-wide capitulation freed up capital, factory space, and management attention for higher-return investments. The decision looks prescient in retrospect.

The second and more dramatic exit was the RF-PCB business, which manufactured rigid-flexible printed circuit boards primarily for Apple's flexible OLED displays. This was not a tiny operation. The RF-PCB business generated roughly four hundred billion won in annual revenue. But it was losing approximately fifty billion won per year. The margins were structurally negative, the competitive dynamics were brutal, and the technology roadmap offered no path to profitability. In late 2020, SEMCO notified customers of its intent to cease supply, completed remaining contractual obligations through the first half of 2021, and fully exited the business by late that year.

The willingness to walk away from four hundred billion won in revenue, to tell Apple that you are shutting down a product line rather than continue subsidizing it, requires a particular kind of corporate discipline. Many companies would have restructured, pivoted, or simply absorbed the losses to maintain the customer relationship. SEMCO chose clarity over comfort.

The capital freed by these exits was redeployed into the 1.9 trillion won FC-BGA substrate expansion. This was not incremental investment. It was a bet-the-segment commitment to build world-class substrate manufacturing capacity in Busan and Vietnam, targeting the AI accelerator market that was just beginning to emerge at the time the investment decision was made.

How does this capital allocation compare to industry peers? Ibiden, one of the dominant Japanese substrate makers, has invested billions in its own capacity expansion to meet AI-driven demand. Shinko Electric Industries has done the same. AT&S of Austria committed over a billion euros to substrate capacity in Southeast Asia. SEMCO's 1.6 billion dollars in substrate investment is not an outlier in the context of these peers. If anything, it represents necessary catch-up spending in a market where structural supply deficit has persisted for years and shows no signs of closing.

The key question for investors is whether SEMCO is arriving too late to a market already dominated by entrenched players. The evidence suggests the timing is actually favorable. The FC-BGA market is projected to roughly double from eight billion dollars in 2022 to over sixteen billion by 2030. The AI-driven expansion of compute capacity means that even as incumbent suppliers ramp their own factories, total demand is growing fast enough to absorb new entrants. And SEMCO's captive relationship with Samsung Foundry provides a built-in demand floor that standalone substrate companies cannot match.

The combination of disciplined divestiture and concentrated reinvestment has produced a company with a cleaner, more focused portfolio than at any point in its history. Every dollar of capital is now directed at businesses where SEMCO has genuine technical differentiation and structural growth tailwinds. The question is not whether the strategy is coherent. It is whether the moats that protect these businesses are as durable as management believes.

VIII. Strategy Framework: 7 Powers and 5 Forces

To evaluate the durability of SEMCO's competitive position, it helps to apply two of the most rigorous frameworks in business strategy: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces.

Start with Helmer. The 7 Powers framework identifies the specific sources of persistent differential returns that allow a business to maintain profitability over time. SEMCO demonstrates at least three of them clearly, and arguably a fourth.

The first and most obvious is Process Power. The ability to manufacture six hundred-layer MLCCs at nano-scale precision with commercially viable yields is not something that can be acquired, licensed, or replicated quickly. It is the accumulated product of decades of iterative refinement in materials science, manufacturing engineering, and quality control. The tacit knowledge embedded in SEMCO's production lines, the proprietary recipes for ceramic powder, the precise parameters for kiln temperatures, the lamination alignment techniques, represents a form of institutional memory that would take a new entrant decades to replicate even with unlimited capital. This is why Chinese MLCC manufacturers, despite enormous government subsidies and aggressive capacity buildout, remain concentrated in commodity grades and have not yet cracked the high-end automotive and server-grade segments where SEMCO competes.

The second is Scale Economies. SEMCO operates massive MLCC fabrication facilities across South Korea, China, and the Philippines. These factories produce billions of capacitors annually, spreading fixed costs across volumes that smaller competitors simply cannot match. The scale advantage compounds with the process power advantage: higher volumes enable more iterations, more iterations improve yields, better yields reduce costs, and lower costs fund further investment in next-generation products. It is a virtuous cycle that widens the gap over time.

The third is Cornered Resource, specifically SEMCO's proprietary ceramic dielectric formulations. The dielectric material is the heart of an MLCC, determining its capacitance, voltage rating, temperature stability, and reliability. SEMCO's powder formulations were developed over decades and are not available for purchase on the open market. CEO Chang's stated intention to vertically integrate into raw material manufacturing further strengthens this cornered resource by eliminating dependence on external suppliers who might also sell to competitors.

A fourth power, Switching Costs, operates primarily in the automotive segment. Once SEMCO's MLCCs or camera modules are qualified and designed into a vehicle platform, replacing them requires years of re-qualification testing. This creates a natural lock-in that extends across the entire production life of the platform, typically five to seven years. The same dynamic applies in aerospace, where qualification cycles are even longer and failure tolerances even tighter.

Now apply Porter's 5 Forces to assess the industry structure.

Barriers to Entry are extraordinarily high. Building a competitive MLCC factory requires not just capital, which is substantial, but thirty-plus years of accumulated materials science expertise. The Chinese experience is instructive: despite massive investment, Chinese manufacturers have reached only ten percent of global market share and remain unable to compete in high-end segments. The barrier is not financial; it is knowledge-based.

The Intensity of Rivalry between existing competitors is high but manageable. SEMCO's primary competitor is Murata, which holds roughly forty percent of the global MLCC market. TDK, Taiyo Yuden, and Yageo round out the top five. However, the market is expanding so rapidly across EVs, AI servers, and 5G infrastructure that the competitive dynamic is less zero-sum than it appears. Both Murata and SEMCO are simultaneously raising prices in 2026, a coordinated pricing behavior that reflects oligopoly dynamics rather than destructive price competition. In the AI server MLCC segment specifically, SEMCO holds approximately forty percent share versus Murata's forty-five percent, a much tighter race than the overall market suggests.

Supplier Power is moderate and declining. SEMCO's move to in-house ceramic powder manufacturing directly addresses the risk of supplier leverage over critical raw materials. For FC-BGA substrates, the key input is ABF resin film, which remains controlled by a small number of Japanese chemical companies, representing an area of residual supplier risk.

Buyer Power varies by segment. In consumer electronics, large OEMs like Apple and Samsung Electronics have significant leverage. In automotive and AI servers, the balance shifts toward the supplier because qualification barriers and supply scarcity give MLCC and substrate makers pricing power. SEMCO's deliberate shift toward automotive and AI is partly a strategy to move toward market segments where buyer power is structurally lower.

The Threat of Substitutes is low for MLCCs. There is no commercially viable alternative to ceramic capacitors for most applications. Tantalum and aluminum electrolytic capacitors serve different functions and cannot replace MLCCs in the high-frequency, high-density applications where they are critical. This is a genuinely irreplaceable technology.

The strategic picture that emerges from both frameworks is one of a company operating in an industry with exceptionally favorable structural characteristics: high barriers, limited substitutes, growing demand, and concentrated supply. SEMCO's specific moats, process power, scale, cornered resources, and switching costs, position it to capture a disproportionate share of the value created by three simultaneous technology transitions. The question is not whether the moats exist, but whether the growth opportunity is large enough to justify the investment required to exploit it.

IX. The Playbook: Lessons for Founders and Investors

SEMCO's fifty-year journey from Samsung-Sanyo Parts to a globally critical materials science company contains several lessons that transcend the specific dynamics of the passive components industry.

The first and most counterintuitive lesson is that you do not need a consumer brand to have one of the best moats in technology. SEMCO has no brand recognition outside the electronics industry. No consumer has ever asked for a Samsung MLCC by name. Yet the company's competitive position is arguably more durable than many consumer-facing technology companies that spend billions on marketing. The invisibility is itself a feature: because end consumers do not think about MLCCs, there is no consumer-driven pressure to commoditize or switch suppliers. The buying decision happens deep in the engineering departments of automakers and server manufacturers, where technical specifications and qualification history matter infinitely more than brand awareness.

The second lesson is about the courage to cut. SEMCO's exit from the LED and RF-PCB businesses was not cosmetic pruning. It was the amputation of revenue-generating operations that were structurally unprofitable. Many companies, particularly Asian conglomerates with cultural pressure to maintain scale and headcount, struggle to make these cuts. SEMCO's willingness to walk away from four hundred billion won in annual revenue to concentrate on higher-return opportunities is a textbook case of disciplined capital allocation. The freed resources funded the FC-BGA expansion that is now the company's most exciting growth vector.

The third lesson concerns the dynamics of "semiconductor-adjacent" cycles. SEMCO is not a semiconductor company. It does not design or fabricate chips. But its business is so tightly correlated with semiconductor industry dynamics that it functions as a leading indicator for the broader electronics ecosystem. When AI server buildouts accelerate, SEMCO's MLCC and substrate orders spike before the semiconductor companies report their own revenue growth. When smartphone markets soften, SEMCO's consumer MLCC volumes decline before handset makers adjust their guidance. This leading indicator quality makes SEMCO a useful barometer for investors tracking the broader technology hardware cycle.

The fourth lesson is about the power of patient vertical integration. SEMCO's decision to in-house ceramic powder manufacturing, to own all three core technologies in camera modules, and to build captive substrate capacity for Samsung Foundry's chip customers reflects a deliberate strategy of controlling the most strategically sensitive links in its own value chain. Each act of vertical integration reduces dependence on external suppliers, deepens technical expertise, and creates additional switching costs for customers. It is the slow, unglamorous work of building competitive advantage one process step at a time.

Finally, there is the transformation from "follower" to "leader" as a strategic archetype. SEMCO spent its first decade as a contract assembler executing Japanese designs. It spent its second decade learning to compete independently. It spent its third decade catching up to Japanese incumbents on quality. And it is now, in its fifth decade, leading the industry in certain categories like high-voltage automotive MLCCs and AI substrate integration. This arc, from imitation to adaptation to innovation, mirrors the trajectory of Korean industry more broadly but remains instructive for any company attempting to transition from a follower position to a leadership position in a technology-intensive market.

These lessons converge on a single insight: the most durable competitive advantages in hardware technology are not built on speed, marketing, or even raw intellectual property. They are built on the slow accumulation of process knowledge, the disciplined allocation of capital toward the highest-barrier opportunities, and the patience to invest for decades in capabilities that cannot be replicated on any shorter timeline.

X. Analysis: Bull vs. Bear Case

The bull case for Samsung Electro-Mechanics rests on a thesis that could be called the Triple Crown: the simultaneous structural growth of AI server infrastructure, autonomous driving systems, and humanoid robotics. If all three of these technology transitions unfold as their proponents expect, SEMCO is positioned as a primary arms dealer to every participant.

In AI servers, the math is overwhelming. Traditional servers required fewer than a thousand MLCCs each. AI servers need three to four thousand. NVIDIA's NVL72 rack platform consumes approximately six hundred thousand. Every new data center built by Microsoft, Google, Amazon, or Meta requires millions of high-end MLCCs and dozens of FC-BGA substrates for each AI accelerator. SEMCO holds roughly forty percent of the AI server MLCC market, neck and neck with Murata, and its substrate business is locked into the Samsung Foundry-Tesla ecosystem through 2033. If AI capital expenditure continues at its current trajectory, this segment alone could drive years of double-digit earnings growth.

In autonomous driving, the demand multiplier is equally compelling. Each electric vehicle already uses up to ten thousand MLCCs, but as ADAS systems become more sophisticated, the count rises further. SEMCO's camera module relationship with Tesla provides visibility into the most aggressive autonomy program in the industry, while its automotive MLCC qualifications across multiple platforms create a diversified exposure to the broader EV market. The pricing premium on automotive MLCCs, combined with the multi-year lock-in created by qualification cycles, means that each design win generates recurring, high-margin revenue for the life of the vehicle platform.

Humanoid robotics is the most speculative of the three legs, but potentially the most consequential. SEMCO has positioned itself as a "one-stop" component provider for humanoid robots, supplying camera modules for vision, MLCCs for power regulation, substrates for the computing brain, and potentially actuator-related components for motion control. If Tesla's Optimus or competing humanoid platforms achieve commercial-scale production, the component content per robot could exceed that of an electric vehicle.

The bear case is not about SEMCO's technology or competitive position. It is about concentration, cyclicality, and geopolitics.

Manufacturing concentration is the most immediate risk. SEMCO's production footprint spans South Korea, the Philippines, Vietnam, and historically China. A significant portion of the company's highest-growth businesses depend on factories in Southeast Asia, where geopolitical tensions, supply chain disruptions, or regulatory changes could impact production. The Vietnam facilities are critical to the FC-BGA expansion. The Philippine plants are central to automotive MLCC production. Any disruption to either geography would materially impact the company's ability to meet customer commitments.

Cyclicality is the structural challenge that SEMCO has never fully escaped. The MLCC business, despite its formidable moats, remains tied to the broader electronics cycle. The 2023 downturn, when revenue fell and operating profit contracted as post-COVID demand normalization hit the consumer electronics market, is a reminder that even the best-positioned component companies cannot fully insulate themselves from cyclical demand swings. If AI server buildout slows, or if global smartphone demand enters a prolonged downturn, SEMCO's earnings could decline sharply even as its competitive position remains intact.

The China variable cuts both ways. Chinese MLCC manufacturers have reached ten percent global market share, and their ambitions extend well beyond commodity grades. Government subsidies, technology transfer programs, and sheer scale of domestic demand give Chinese producers a long runway to improve their capabilities. While the high-end segments remain beyond their reach today, the history of Chinese manufacturing in other industries, from solar panels to batteries to displays, suggests that technological catch-up is a matter of when, not whether. The question for SEMCO is whether the pace of Chinese advancement will erode its pricing power in mid-range segments before the automotive and AI segments grow large enough to offset the competitive pressure.

There is also the Samsung Group governance overhang. As a subsidiary of Samsung Electronics, which is itself part of the broader Samsung chaebol, SEMCO's strategic decisions can be influenced by group-level priorities that may not always align perfectly with minority shareholder interests. Related-party transactions, transfer pricing between Samsung entities, and capital allocation decisions driven by group strategy rather than SEMCO-specific returns are perennial concerns for investors in Korean chaebol subsidiaries. The cross-shareholding structure provides strategic benefits but introduces governance complexity.

For investors monitoring SEMCO's performance, two KPIs stand above all others. The first is the high-value product mix ratio, specifically the percentage of MLCC revenue coming from automotive and AI server applications versus consumer and general-purpose grades. This ratio captures the essential strategic transformation in a single number: as it rises, margins expand, customer relationships become stickier, and cyclical exposure diminishes. The second is FC-BGA substrate capacity utilization. Given the enormous capital committed to substrate expansion, the rate at which new capacity is filled with paying customers is the most direct measure of whether the substrate bet is paying off. Together, these two metrics tell you whether SEMCO is successfully executing the transition from a cyclical components company to a structurally advantaged materials science platform.

XI. Epilogue: The Ceramic Alchemists

There is a factory in Busan where machines stack ceramic sheets thinner than a human hair into towers six hundred layers high. The ceramic powder was formulated from recipes refined over three decades. The metal electrodes were printed with precision measured in fractions of a micron. The kilns run at temperatures above twelve hundred degrees Celsius. What emerges at the other end is a component so small it is invisible to the naked eye, and so essential that without it, no phone rings, no car drives, no AI model thinks.

Samsung Electro-Mechanics has spent fifty years perfecting this particular form of alchemy, transforming ceramic powder and metal paste into the indispensable building blocks of modern civilization. It has done so largely in the shadow of its parent company, Samsung Electronics, which commands the headlines, the consumer brand recognition, and the market capitalization that dwarfs its subsidiary many times over. But in the world of electronic components, where the battles are fought not with marketing campaigns but with dielectric formulations and lamination yields, SEMCO has earned a position that only a handful of companies on Earth can claim.

The Suwon-based company is now at the confluence of the three most powerful technology currents of this era: the buildout of AI computing infrastructure, the electrification of transportation, and the nascent emergence of humanoid robotics. Its MLCCs are the rice that feeds every circuit. Its camera modules are the eyes that guide autonomous systems. Its substrates are the foundations on which the next generation of AI processors will sit. Whether the next decade proves as transformative as the current trajectory suggests, or whether cycles, geopolitics, and competition intervene, Samsung Electro-Mechanics will remain what it has been for fifty years: the company that makes the invisible things that make everything else possible.

Top 10 Long-Form Resources for Further Reading:

-

Samsung Electro-Mechanics 50-Year History - The official corporate retrospective available on the SEMCO investor relations site, documenting the evolution from Samsung-Sanyo Parts to the current company.

-

"The Rice of Electronics" - Technical white papers from Murata and SEMCO explaining MLCC technology, manufacturing processes, and the engineering challenges of ultra-miniaturization.

-

Samsung Group "New Management" Declaration (1993) - The Lee Kun-hee philosophy articulated in Frankfurt that forced every Samsung subsidiary, including SEMCO, to pivot from volume manufacturing to quality leadership.

-

"Chip War" by Chris Miller - Essential context for understanding the broader Asian semiconductor and component ecosystem in which SEMCO operates, including the geopolitical dynamics shaping supply chains.

-

FC-BGA Market Reports by Yole Developpement - Detailed analysis of the high-end substrate market, supply-demand dynamics, and the competitive landscape among Ibiden, Shinko, Unimicron, and SEMCO.

-

Tesla AI Day Presentations - Primary source material for understanding the camera module, compute, and sensor requirements driving Tesla's Full Self-Driving and Optimus programs.

-

"7 Powers" by Hamilton Helmer - The strategic framework most applicable to understanding SEMCO's competitive moats, particularly Process Power and Cornered Resource.

-

The Sanyo-Samsung Joint Venture Archives - Historical records documenting the technology transfer arrangements of the 1970s that launched SEMCO's journey.

-

Korea Exchange (KRX) Filings for 009150 - Detailed segment-level financial data, related-party transaction disclosures, and management discussion that provide granular visibility into SEMCO's business evolution.

-

"Samsung Rising" by Geoffrey Cain - Cultural context for how Samsung subsidiaries compete and cooperate within the chaebol structure, and the internal dynamics that shape strategic decisions at companies like SEMCO.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube