ISU PETASYS: Korea's Hidden PCB Champion Riding the AI Wave

I. Introduction & Episode Roadmap

[8 minutes]

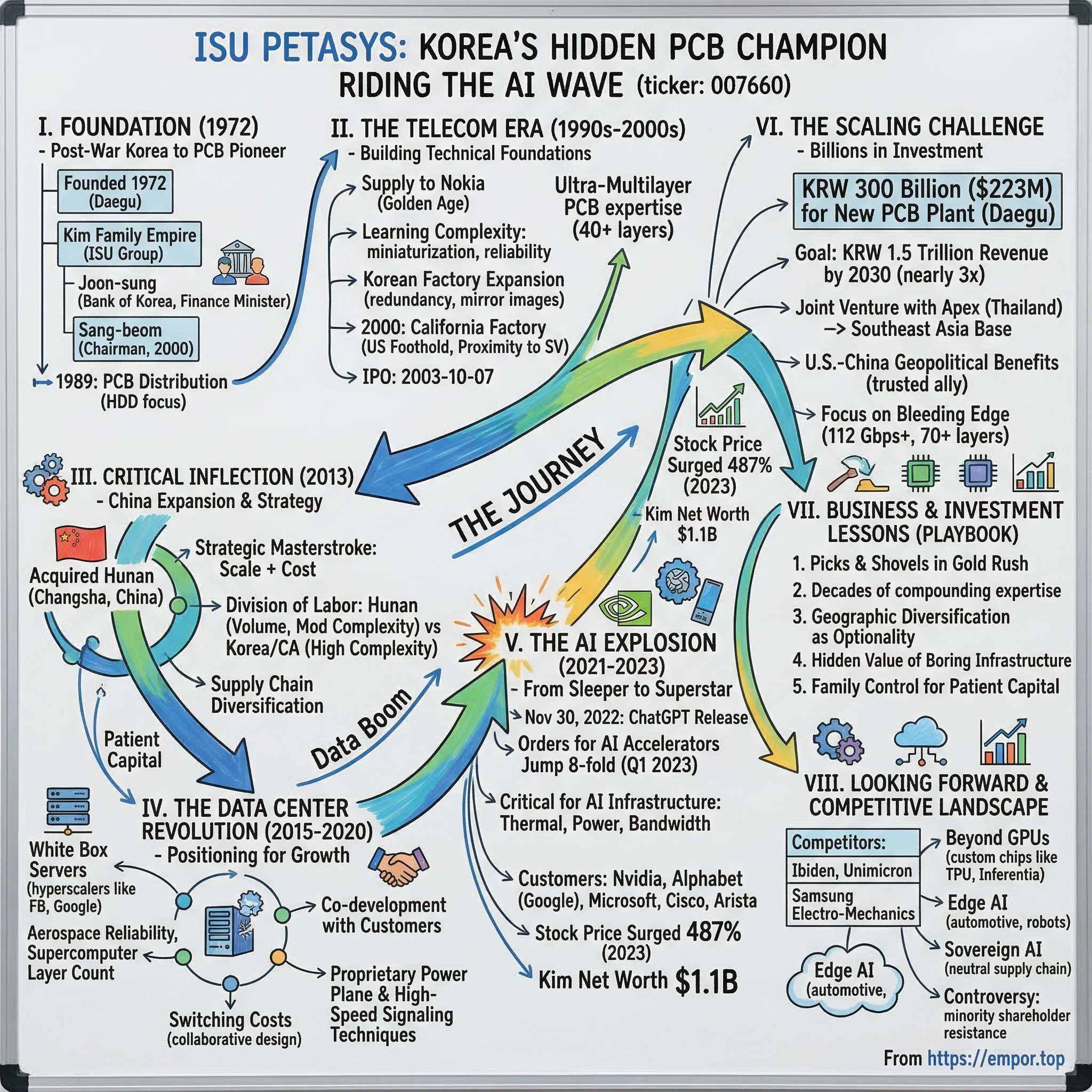

Picture this: A Korean printed circuit board manufacturer that most of Silicon Valley had never heard of suddenly sees its stock price explode 487% in a single year. Not because of a flashy product launch or viral marketing campaign, but because they quietly became the backbone of the AI revolution. This is the story of ISU PETASYS, a company founded in 1972 and headquartered in Daegu, South Korea, that transformed from an obscure industrial supplier into one of the most critical players in the global AI infrastructure boom.

In the summer of 2023, as ChatGPT mania gripped the world and every tech company scrambled to build AI capabilities, a curious thing happened in the unglamorous world of printed circuit boards. ISU Petasys Co., which counts Alphabet Inc., Nvidia Corp. and Microsoft Corp. as customers of its multilayered boards, had seen its share price surge 487% this year – among the biggest gainers on South Korea's benchmark stock index. The family behind this quiet giant suddenly found themselves thrust into the billionaire ranks, with Forbes estimates putting Kim's net worth at $1.1 billion.

But here's what makes this story remarkable: ISU PETASYS didn't pivot to AI. They didn't rebrand themselves as an "AI company" or hire a flashy Silicon Valley CEO. They simply kept doing what they'd been doing for decades—making incredibly complex, ultra-multilayer printed circuit boards—and suddenly the world needed exactly what they had been perfecting since the days of Nokia flip phones.

The question that should captivate every investor and tech enthusiast is this: How did a 50-year-old Korean PCB manufacturer become so critical to the AI revolution that orders for its boards used for AI accelerators jumped almost eight-fold to 47.3 billion won ($36.4 million) in the first quarter of 2023? And perhaps more importantly, what does their journey tell us about identifying the next wave of infrastructure plays in technology revolutions?

Today, we're diving deep into the ISU PETASYS story—from its origins in post-war Korea to its current position as a critical supplier to the world's most valuable tech companies. We'll explore how decades of unglamorous work in telecommunications infrastructure positioned them perfectly for the AI boom, why their technical moat is so difficult to replicate, and what their massive expansion plans tell us about where the AI infrastructure market is headed.

This isn't just a story about PCBs and semiconductors. It's about how boring infrastructure companies can become the biggest winners in technology revolutions, why geography and geopolitics matter more than ever in tech supply chains, and how a Korean family conglomerate outmaneuvered global giants to capture one of the most valuable positions in the AI value chain. Buckle up—this is going to be a fascinating ride through the hidden layers of the AI revolution.

II. Foundation Story: From Post-War Korea to PCB Pioneer

[12 minutes]

The monsoon rains of 1972 were particularly heavy in Daegu, South Korea's fourth-largest city, tucked into the southeastern corner of the peninsula. While Seoul was racing toward modernity and hosting global events, Daegu remained an industrial heartland—a place where the real work of building Korea's economic miracle happened, far from the spotlight. It was here, in this manufacturing hub, that ISU Petasys Co., Ltd. was founded in 1972.

But to understand ISU PETASYS, you first need to understand the Kim family and the ISU Group empire they built. ISU Group was started by Kim's late father, Joon-sung, who founded South Korea's first regional bank, Daegu Bank, in 1967. Joon-sung went on to serve as governor of the Bank of Korea, head of the Korea Development Bank and then as South Korea's Minister of Finance and Economy. He also served as chairman of Samsung Electronics and Daewoo, which was once the country's second-largest conglomerate before collapsing in 1999.

This wasn't just any industrialist family—Kim Joon-sung was Korean business royalty, a man who had literally helped architect the country's financial system. His connections ran deep through every corridor of Korean power, from the Blue House to the chaebols. When he looked at the future of Korea in the early 1970s, he saw opportunity in technology and manufacturing.

The company that would become ISU PETASYS started modestly, focusing initially on various industrial components. But the real transformation came in 1989, when Isu Petasys, founded in 1972, began distributing printed circuit boards, mainly for hard disk drives, in 1989. This was a prescient move—the personal computer revolution was just beginning to accelerate, and every computer needed hard drives, and every hard drive needed PCBs.

The 1990s brought a critical inflection point. ISU Group acquired a controlling stake in ISU Petasys in 1995, marking the beginning of a new era. The younger Kim, Kim Sang-beom, had watched his father navigate the treacherous waters of Korean business and politics. Kim became the group's chairman in 2000 after his father, Joon-sung, stepped down after four years. Before joining Isu, the younger Kim worked at the now-defunct industrial conglomerate, Daewoo Group, which was founded by his father-in-law Kim Woo-choong, according to local newspaper Korea Joongang Daily.

The family connections were everything in Korean business, but they also brought pressure. Kim Sang-beom inherited not just a company, but a legacy—and the weight of expectation that came with being the son of one of Korea's most influential businessmen.

The company was formerly known as Petasys Co., Ltd. and changed its name to ISU Petasys Co., Ltd. in March 2002. This wasn't just a rebranding—it was a declaration. The ISU name carried weight in Korea, signaling to customers and competitors alike that this PCB manufacturer was backed by serious capital and connections.

The IPO came swiftly after. The company went IPO on 2003-10-07, opening up the company to public markets but keeping the Kim family firmly in control. This dual structure—public company accountability with family control—would prove crucial in allowing ISU PETASYS to make long-term bets that pure public companies might shy away from.

By the early 2000s, ISU PETASYS had established itself as a serious player in the Korean PCB industry. They weren't the largest, and they certainly weren't the most famous. But they were building something that would prove far more valuable: deep technical expertise in ultra-multilayer PCBs, the kind of complex boards that would one day be needed for the most demanding computing applications in the world.

III. The Telecom Era: Building Technical Foundations (1990s-2000s)

[15 minutes]

The late 1990s were the golden age of telecommunications, and nowhere was this more apparent than in the gleaming Nokia headquarters in Espoo, Finland. The Finnish giant was riding high, selling hundreds of millions of phones annually, each one a marvel of miniaturization. And deep in the supply chain, providing the critical PCBs that made these devices possible, was ISU PETASYS.

In recent years, Isu Petasys has leaned into the AI craze, diversifying its customer base from predominantly telecommunications manufacturers like Nokia Oyj, and adding technology giants such as Alphabet and Nvidia, according to Park Hyung-woo, an analyst at SK Securities Co. in Seoul. But this recent pivot tells only part of the story. The relationship with Nokia and other telecom giants in the 1990s and 2000s wasn't just about revenue—it was about learning to build the world's most complex PCBs under the most demanding conditions.

Think about what a Nokia phone PCB had to do in the late 1990s: pack increasingly powerful processors, memory, radio frequencies, and power management into a space smaller than a credit card, all while being dropped, exposed to moisture, and used constantly. This was the crucible that forged ISU PETASYS's technical capabilities.

The Korean operations underwent massive expansion during this period. From 1987 to 1997, we doubled the size of the Korean factory by cloning the first factory to build the second. From the standpoint of a business continuity plan, the two buildings are mirror images of each other, so if one building is damaged in some manner, we can still continue our operations in the other. This wasn't just about scale—it was about redundancy and reliability, qualities that would later make ISU PETASYS invaluable to hyperscalers who couldn't afford supply chain disruptions.

The California expansion marked a critical milestone. In 2,000 we opened our California factory, giving the company a foothold in the United States and, more importantly, proximity to the emerging tech giants of Silicon Valley. While the facility was smaller than the Korean operations, it served a crucial role: rapid prototyping and close collaboration with U.S. customers who wanted their most sensitive designs kept onshore.

The technical capabilities ISU PETASYS developed during the telecom era were staggering. They learned to manufacture PCBs with layer counts that seemed impossible just years earlier. Where consumer electronics might use 4-8 layer boards, ISU PETASYS was pushing into 20, 30, even 40+ layers, each one perfectly aligned, with traces measured in micrometers. This wasn't just manufacturing—it was precision engineering at a microscopic scale.

In 2015, we built a third building in Korea to house all of our state-of-the art plating facilities because there was no physical room in Factory 1 or Factory 2. This third facility represented a major technical upgrade. Plating—the process of depositing thin layers of conductive material—is perhaps the most critical and difficult part of PCB manufacturing. The new facility incorporated advanced technologies that would prove essential for the next generation of high-speed, high-frequency boards.

But perhaps the most important development during this era was the relationships ISU PETASYS built. They weren't just a vendor to Nokia; they were a partner, involved in the design process from the earliest stages. When Nokia engineers were designing a new phone, ISU PETASYS engineers were right there with them, figuring out how to make the impossible possible. This collaborative approach, so different from the arm's-length supplier relationships common in the industry, would later prove invaluable when ISU PETASYS began working with companies like Nvidia and Google.

The telecom era also taught ISU PETASYS about the importance of quality at scale. Nokia wasn't ordering thousands of boards—they were ordering millions. A defect rate of even 0.1% would mean thousands of failed phones. The company developed quality control processes that were legendary in the industry, with multiple inspection points, advanced testing equipment, and a culture of zero-defect manufacturing that permeated every level of the organization.

As the 2000s progressed and the smartphone revolution began to reshape the telecom industry, ISU PETASYS faced a choice. They could double down on mobile, competing for lower-margin business as phones became commoditized. Or they could take their hard-won expertise and apply it to new, more demanding applications. They chose the latter, a decision that would position them perfectly for the coming data center boom.

IV. The Critical Inflection: China Expansion & Acquisition Strategy (2013)

[18 minutes]

November 4, 2013, marked a day that would fundamentally alter ISU PETASYS's trajectory, though few recognized its significance at the time. On November 4, 2013, the Company acquired a 60% stake in Kingboat Technology Limited, engaged in the manufacturing of printed circuit board. This wasn't just another acquisition—it was a strategic masterstroke that would give ISU PETASYS the scale and cost structure needed to compete globally.

The China expansion actually began earlier that year with another crucial move. In 2013, we acquired Hunan (MFS Technology based in Changsha, China). The Hunan facility, located in central China, represented ISU PETASYS's first major manufacturing footprint in the Middle Kingdom. But why China, and why then?

Kim Sang-beom and his leadership team saw what many others missed: China wasn't just about cheap labor anymore. It was becoming the world's electronics manufacturing hub, with an entire ecosystem of suppliers, equipment makers, and skilled technicians. More importantly, it was where their customers' customers were. Apple was manufacturing iPhones in China. Dell, HP, and Lenovo were building servers there. Being close to final assembly meant faster turnaround times and lower logistics costs.

Hunan does mainstream technology, but not at the level of complexity that we do in Korea and California. This division of labor was deliberate and brilliant. The Hunan facility would handle high-volume, moderate-complexity boards—the bread and butter products that generated steady cash flow. This freed up the Korean facilities to focus on the ultra-high-complexity boards that commanded premium prices and required the most advanced equipment and expertise.

The strategic reasoning went deeper than just cost optimization. By 2013, it was becoming clear that the future of technology would be increasingly about data—big data, cloud computing, and the infrastructure needed to support it all. And the companies building this infrastructure were primarily American and Chinese. ISU PETASYS needed to be in both markets, not just as an exporter but as a local manufacturer who could respond quickly to customer needs.

The integration of these Chinese facilities revealed something important about ISU PETASYS's management approach. Unlike many Western companies that struggled with Chinese acquisitions, ISU PETASYS brought a distinctly Korean management style that proved highly effective. They understood hierarchy and respect, concepts deeply embedded in both Korean and Chinese business culture. They also brought advanced technology and training, upgrading the Chinese facilities rather than simply exploiting them for low costs.

The financial engineering behind these acquisitions was equally sophisticated. Rather than loading up on debt or diluting shareholders, the Kim family used the broader ISU Group's resources to fund expansion. This patient capital approach meant they could focus on long-term capability building rather than short-term financial returns.

But perhaps the most prescient aspect of the 2013 expansion was the timing. This was before the U.S.-China trade war, before technology became a geopolitical battleground. ISU PETASYS established itself in China when it was still relatively easy for Korean companies to do so, giving them a footprint that would become increasingly valuable—and difficult to replicate—as tensions rose.

The acquisitions also brought new customer relationships. The Chinese facilities had existing contracts with local companies, including some that would later become major players in AI and cloud computing. These relationships, combined with ISU PETASYS's technical capabilities, created a powerful network effect. Customers would come for the China manufacturing, discover the advanced capabilities in Korea, and end up moving their most complex designs there.

By 2015, the China strategy was clearly paying dividends. The company had successfully integrated its acquisitions, improved their capabilities, and was seeing strong growth in both revenue and profitability. The Hunan facility, in particular, had become a profit center, churning out millions of boards for the booming Chinese electronics industry.

The geographic diversification also provided an unexpected benefit: resilience. When the Korean won strengthened, making Korean exports more expensive, the Chinese facilities could pick up the slack. When Chinese environmental regulations tightened, raising costs, the Korean facilities could absorb more volume. This flexibility would prove invaluable during the COVID-19 pandemic and subsequent supply chain disruptions.

Looking back, the 2013 expansion into China represents a textbook example of strategic foresight. ISU PETASYS didn't just follow their customers to China; they anticipated where the industry was going and positioned themselves accordingly. They built capabilities before they were desperately needed, established relationships before they became precious, and created optionality before uncertainty made it invaluable. It was boring, patient, and brilliant—quintessentially ISU PETASYS.

V. The Data Center Revolution: Positioning for Growth (2015-2020)

[20 minutes]

By 2015, something fundamental was shifting in the technology industry. The smartphone revolution had plateaued, Moore's Law was slowing, but data was exploding exponentially. Every click, every swipe, every photo uploaded to Instagram was creating demand for more servers, more storage, more network capacity. And at the heart of every server, connecting CPUs to memory, GPUs to motherboards, lay printed circuit boards of unprecedented complexity.

ISU PETASYS's entry into the data center market wasn't a dramatic pivot—it was more like a door quietly opening to reveal a room full of gold. The company had been making boards for network equipment for years, but servers represented a different beast entirely. Where a network switch might need a 20-layer board, a high-end server could require 40, 50, even 60 layers, each one perfectly aligned, with signal integrity maintained across frequencies measured in gigahertz.

The shift began with what the industry calls "white box" servers—generic, unbranded servers that companies like Facebook and Google were designing themselves rather than buying from Dell or HP. These hyperscalers had realized they could optimize every component for their specific workloads, achieving better performance at lower cost. But they needed manufacturing partners who could turn their radical designs into reality.

The Company's main products are PCBs, which are used in telecommunication systems, super computers, data centers, aerospace areas and others. This diversification wasn't accidental. Each market taught ISU PETASYS something valuable. Aerospace demanded perfect reliability—a single failure could be catastrophic. Supercomputers pushed the boundaries of layer count and signal integrity. Data centers required all of this, but at scale and cost points that seemed impossible.

The technical challenges of data center PCBs were unlike anything the industry had seen. Consider the problem of power delivery: a modern server CPU can consume 300 watts or more, with current demands that can spike in microseconds. The PCB must deliver this power cleanly, without voltage drops or electromagnetic interference that could corrupt data. ISU PETASYS developed proprietary techniques for power plane design, using advanced materials and geometries that their competitors struggled to replicate.

Then there was the challenge of high-speed signaling. As data rates climbed from 10 Gbps to 25 Gbps to 56 Gbps and beyond, traditional PCB design rules broke down. Signals at these frequencies don't behave like simple electrical currents—they're electromagnetic waves, subject to reflection, attenuation, and crosstalk. ISU PETASYS invested heavily in simulation software and testing equipment, building capabilities that put them in an elite group of manufacturers capable of producing boards for the fastest interfaces in the world.

The relationships ISU PETASYS built during this period would prove invaluable when the AI boom arrived. They weren't just working with the procurement departments of tech giants—they were embedded with the engineering teams, participating in design reviews, suggesting optimizations, solving problems that the customers didn't even know they had. When a hyperscaler's engineer hit a wall trying to route signals in a particularly dense design, ISU PETASYS's engineers would work through the night to find a solution.

This collaborative approach extended to the business model as well. Rather than simply bidding on specifications, ISU PETASYS would often co-develop products with customers, sharing the risk and reward of new designs. This created switching costs that went beyond simple economics—when you've spent months working with ISU PETASYS engineers to perfect a design, you don't easily move to another supplier to save a few percentage points on cost.

The period from 2015 to 2020 also saw ISU PETASYS make critical investments in advanced manufacturing equipment. They installed new laser drilling machines capable of creating vias (the tiny holes that connect different layers) with diameters smaller than a human hair. They upgraded their plating lines to handle the exotic materials required for high-frequency applications. They implemented advanced optical inspection systems that could detect defects invisible to the human eye.

But perhaps the most important development during this period was cultural. ISU PETASYS transformed from a company that made PCBs to a company that solved impossible problems. Engineers took pride not in meeting specifications, but in exceeding them. Quality wasn't just about low defect rates—it was about understanding how boards performed in real-world conditions and continuously improving designs.

The financial results during this period were solid but not spectacular. Revenue grew steadily, margins improved gradually. To outside observers, ISU PETASYS looked like a competent but unremarkable industrial company. The stock price reflected this perception, trading at modest multiples, attracting little attention from investors focused on flashier technology companies.

What the market missed was that ISU PETASYS was building optionality. Every new capability, every customer relationship, every technical challenge overcome was creating potential energy that would be released when the right catalyst appeared. They were like a Formula 1 team during winter testing—not trying to set fast lap times, but methodically preparing for the race they knew was coming.

As 2020 drew to a close, with the world in the grip of a pandemic and digital transformation accelerating everywhere, the data center market was exploding. But even this growth would pale in comparison to what was about to come. Unknown to all but a few insiders, a new type of computing workload was emerging that would demand PCBs of unprecedented complexity and value. The age of artificial intelligence was about to begin, and ISU PETASYS was perfectly positioned to capitalize on it.

VI. The AI Explosion: From Sleeper to Superstar (2021-2023)

[25 minutes]

November 30, 2022. OpenAI releases ChatGPT to the public. Within five days, it has a million users. Within two months, 100 million. The world suddenly wakes up to artificial intelligence not as a distant promise but as a present reality. In the boardrooms of every tech company, the same question echoes: "What's our AI strategy?" And in Daegu, South Korea, Kim Sang-beom and his team at ISU PETASYS watch their order books explode.

Orders for its boards used for AI accelerators jumped almost eight-fold to 47.3 billion won ($36.4 million) in the first quarter from a year earlier, according to a June presentation. Eight-fold. In a single quarter. For a company that had been growing steadily but unspectacularly for decades, this was like a rocket strapped to a bicycle.

But to understand why ISU PETASYS became so critical to the AI boom, you need to understand what makes AI infrastructure different from traditional computing. A typical server CPU might have a few dozen cores, operating at high frequency, optimized for sequential processing. An AI accelerator like Nvidia's H100 has thousands of cores, operating in parallel, consuming 700 watts of power, generating enough heat to literally cook an egg, and requiring data bandwidth that would have seemed like science fiction just years ago.

The PCB for an AI accelerator isn't just a platform to mount components—it's an integral part of the system's performance. The traces carrying data between the GPU and high-bandwidth memory must be precisely matched in length to the millimeter, or signals arrive out of sync and data corrupts. The power delivery network must handle current swings of hundreds of amperes without voltage drooping. The thermal management must dissipate kilowatts of heat without warping the board or creating hotspots.

These switches utilise 40+ layer MLBs, which are ISU's most advanced and lucrative product. Within the network segment, we expect 40+ layer MLB mix to be 22% in FY25E growing to 43% in 2026E. The layer count tells only part of the story. Each layer must be perfectly aligned—a misregistration of even 50 micrometers can cause failures. The materials must maintain dimensional stability across temperature ranges from sub-zero to over 100°C. The drilling, plating, and lamination processes must be controlled to tolerances that push the boundaries of what's physically possible.

ISU PETASYS had spent years preparing for this moment, even if they didn't know exactly when or how it would come. Their work with supercomputers had taught them about extreme layer counts. Their aerospace experience had instilled an obsession with reliability. Their data center customers had pushed them to achieve ever-higher speeds and lower losses. When AI accelerators emerged requiring all of these capabilities simultaneously, ISU PETASYS was one of perhaps a dozen companies globally that could deliver.

In recent years, Isu Petasys has leaned into the AI craze, diversifying its customer base from predominantly telecommunications manufacturers like Nokia Oyj, and adding technology giants such as Alphabet and Nvidia, according to Park Hyung-woo, an analyst at SK Securities Co. in Seoul. But "leaning in" understates the transformation. ISU PETASYS reorganized entire production lines around AI products. They hired engineers with expertise in electromagnetic simulation. They invested in new equipment specifically for the ultra-thick boards required by AI accelerators.

The customer concentration that emerged was both a blessing and a risk. Its customers include Alphabet, Nvidia, Microsoft, Cisco, Arista Networks and Celestica. This is essentially a who's who of AI infrastructure. When Nvidia designs a new accelerator, ISU PETASYS is in the room. When Google needs boards for its TPUs, ISU PETASYS gets the call. When Microsoft is building out Azure's AI capacity, ISU PETASYS's factories run three shifts.

The stock market's reaction was swift and dramatic. Isu Petasys Co., which counts Alphabet Inc., Nvidia Corp. and Microsoft Corp. as customers of its multilayered boards, has seen its share price surge 487% this year – among the biggest gainers on South Korea's benchmark stock index. From sleepy industrial to AI darling in months. The transformation was so rapid that many investors struggled to understand what ISU PETASYS actually did. "They make PCBs" seemed too simple an explanation for such dramatic growth.

The financial impact went beyond just revenue growth. AI accelerator boards command premium prices—sometimes 10x or more than standard server boards. The complexity creates natural barriers to entry; even if a competitor had the equipment, developing the expertise takes years. The criticality to customers means price is often secondary to capability and reliability. ISU PETASYS had stumbled into the perfect business: high growth, high margins, high barriers to entry, and customers with essentially unlimited budgets.

Park said he expects AI-related business to make up 20% of the company's revenue this year and at least 30% in 2024. These projections, made in mid-2023, would prove conservative. The AI boom wasn't just changing ISU PETASYS's income statement—it was transforming the company's identity and position in the technology ecosystem.

The human story behind the numbers is equally dramatic. Engineers who had spent careers perfecting incremental improvements suddenly found themselves at the center of the technology world's most important revolution. The Daegu facilities, long seen as a backwater compared to Seoul, became destinations for executives from Silicon Valley. Kim Sang-beom, who had run the company quietly for over two decades, found himself with Forbes estimating his net worth at $1.1 billion.

But perhaps the most remarkable aspect of ISU PETASYS's AI boom was how unsurprising it was in hindsight. They had spent 50 years building capabilities that turned out to be exactly what the AI revolution needed. They hadn't pivoted or transformed or disrupted. They had simply continued doing what they did best—solving the hardest problems in PCB manufacturing—and the market had finally come to them.

VII. The Scaling Challenge: Billions in Investment (2024-Present)

[22 minutes]

The conference room in Daegu City Hall was packed on the day ISU PETASYS announced its largest investment in company history. ISU Petasys will invest KRW300 billion ($223.3 million) here to build a PCB manufacturing plant. The mayor was there, regional officials, local media—everyone understood this wasn't just another factory expansion. This was a bet that the AI revolution was just beginning.

The new plant to manufacture multi-layer circuit boards. The company said the investment is in response to an increase in product demand from global big tech companies due to the rapid growth of the AI accelerator and data center market. The language was carefully corporate, but the ambition was staggering. ISU PETASYS wasn't just adding capacity—they were building an entirely new facility designed from the ground up for AI-era PCBs.

The scale of ambition becomes clear in the revenue projections. When the new plant is completed, ISU Petasys said it plans to become a leading company in the global market by raising sales of KRW579 billion ($430.9 million) as of last year to KRW1.5 trillion ($1.12 billion) by 2030. Nearly tripling revenue in six years. For a 52-year-old industrial company, this would be remarkable growth under any circumstances. In the context of their conservative Korean corporate culture, it was almost revolutionary.

CEO Choi Chang-bok's comments revealed the underlying dynamics: "The number of orders has continued to increase, focusing on next-generation products such as AI accelerators and 800GB switches, which have recently emerged as a key topic in data centers". The mention of 800GB switches is particularly telling. These ultra-high-speed network devices are essential for connecting thousands of AI accelerators into the massive clusters required for training large language models. They represent the bleeding edge of networking technology, and their PCBs are among the most complex ever manufactured.

But the Daegu plant was just one piece of a larger expansion puzzle. In October 2024, ISU PETASYS made another strategic move that surprised industry watchers. Today (14th), Apex's major subsidiary Apex Circuit(Thailand) Co., Ltd. signed a joint venture agreement with Isu Petasys, the South Korean networking and server PCB manufacturer, to establish a joint venture subsidiary ISU-APEX. Both parties will share business resources, production capacity, and technology to create a higher industrial value. Apex will invest THB 15.3 million, holding 15% equity in ISU-APEX, while Isu Petasys will invest THB 86.7 million, holding 85% equity in ISU-APEX.

The Thailand joint venture represented a crucial piece of supply chain diversification. Isu Petasys, founded in 1972, operates factories in South Korea, China, and the US, but has not established a production base in Southeast Asia yet. Southeast Asia was becoming increasingly important as companies sought to reduce their dependence on China amid geopolitical tensions. Thailand offered skilled workers, established infrastructure, and friendly relations with both the U.S. and China.

The partnership with Apex was particularly clever. As the largest Taiwanese PCB supplier in Thailand, Apex has a maximum monthly production capacity of approximately 1 million square meters. With over 20 years of operations experience in Thailand, Apex will offer stable Southeast Asia production capacity support for Isu Petasys' international customers. Rather than building from scratch, ISU PETASYS gained immediate access to established operations and local expertise.

The company's revenue rose 22% year-over-year to 494 billion won (about $350 million) in the first half of this year, while net income increased 76% from the previous year to 70 billion won in the same period. These numbers from 2024 showed the AI boom was translating into real financial performance. But they also highlighted the capital-intensive nature of the opportunity. To capture the growth, ISU PETASYS needed to invest aggressively, and that meant taking on new risks.

The investment challenges went beyond just building factories. The equipment required for manufacturing AI-grade PCBs was extraordinarily expensive and often had lead times measured in years. A single advanced drilling machine could cost millions of dollars. The clean rooms required for high-layer-count boards rivaled those used in semiconductor fabs. The testing equipment needed to verify signal integrity at 100+ Gbps speeds was so specialized that only a handful of companies worldwide made it.

There was also the human capital challenge. ISU PETASYS needed engineers who understood not just PCB manufacturing but also high-frequency electromagnetic theory, thermal dynamics, and advanced materials science. The company launched aggressive recruiting programs, partnering with universities, offering generous packages to lure talent from competitors. The Daegu facility, long seen as a career backwater, suddenly became a destination for ambitious engineers who wanted to work on the most challenging problems in the industry.

The competitive dynamics were intensifying as well. Its competitors include Japan's Ibiden, Taiwan's Unimicron Technology and South Korea's Samsung Electro-Mechanics. Each of these companies was also investing aggressively, trying to capture their share of the AI boom. The race wasn't just about capacity but about capability—who could manufacture the highest layer counts, the finest traces, the best signal integrity.

ISU PETASYS's response was to focus relentlessly on the highest end of the market. While competitors might be satisfied with 30 or 40-layer boards, ISU PETASYS pushed toward 50, 60, even 70 layers. While others targeted 25 Gbps signaling, ISU PETASYS designed for 112 Gbps and beyond. It was a high-risk, high-reward strategy—the volumes would be lower, but the margins and competitive moats would be much higher.

The geopolitical dimension added another layer of complexity. Increasing tensions between the US and China may have also contributed to Isu Petasys's expansion, as US companies prefer non-Chinese suppliers, according to analyst Baik. ISU PETASYS found itself benefiting from its Korean identity—trusted by the West as a democratic ally, but not seen as a direct competitor like Japan or Taiwan. The company carefully navigated these waters, maintaining its Chinese operations while assuring Western customers about supply chain security.

As 2024 drew to a close, ISU PETASYS faced a paradox. They had more orders than they could fill, more opportunities than they could pursue, more growth than they had ever imagined. But executing on this potential required betting billions on a future where AI demand continued to explode. It was the kind of bet that could define a company for generations—or destroy it if they got it wrong.

VIII. The Competitive Landscape & Market Position

[15 minutes]

The global PCB industry in 2024 resembles a pyramid, with thousands of companies at the base making simple boards for consumer electronics, hundreds in the middle producing moderate-complexity boards for computers and telecommunications, and perhaps a dozen at the apex capable of manufacturing the ultra-high-complexity boards required for AI accelerators and high-end data center equipment. ISU PETASYS had clawed its way to that apex, but staying there required constant vigilance.

Its competitors include Japan's Ibiden, Taiwan's Unimicron Technology and South Korea's Samsung Electro-Mechanics. Each competitor brought different strengths to the battle. Ibiden, with its deep relationships with Intel and long history in the semiconductor industry, had unmatched experience in package substrates—the ultra-fine-pitch boards that sit directly beneath processor chips. The Japanese company's reputation for quality was legendary, but their costs were high and their capacity limited.

Unimicron Technology represented Taiwanese efficiency and scale. As the world's largest PCB manufacturer by revenue, they had the resources to invest heavily in new technology and the volumes to amortize those investments quickly. Their proximity to TSMC and the Taiwanese electronics ecosystem gave them advantages in understanding emerging technologies. But they also faced challenges—customer concentration risk with Apple and growing concerns about Taiwan's geopolitical vulnerability.

Samsung Electro-Mechanics was perhaps the most formidable competitor, backed by the vast resources of the Samsung empire. They could afford to lose money for years to gain market share, and their internal customer—Samsung Electronics—provided guaranteed volume for new technologies. Yet being part of Samsung was also a weakness; many customers were wary of sharing their designs with a supplier owned by a potential competitor.

Against these giants, ISU PETASYS had carved out a unique position. They weren't the largest, the most technologically advanced, or the best connected. But they had something perhaps more valuable: focus and flexibility. While competitors juggled consumer electronics, automotive, and industrial markets, ISU PETASYS concentrated relentlessly on high-end computing. While others maintained rigid corporate structures, ISU PETASYS could pivot quickly when customers needed something new.

The market dynamics were shifting in ISU PETASYS's favor. The traditional PCB industry was deflationary—prices dropped every year as technology matured and competition increased. But AI accelerator boards broke this pattern. Prices were actually rising as complexity increased faster than manufacturing technology could improve. A board that might have sold for $100 in 2020 could command $500 or more in 2024, and customers would gladly pay it because the alternative was not having AI capabilities at all.

The current market capitalization of ISU Petasys is $3.14B. This valuation, reached in mid-2024, represented a remarkable transformation from the sub-billion-dollar company of just a few years earlier. But in the context of the AI infrastructure boom, some analysts argued it was still undervalued. After all, this was a company supplying critical components to trillion-dollar tech giants racing to build AI supremacy.

The competitive moats ISU PETASYS had built were formidable. Technical capability was the most obvious—it would take a new entrant years to learn how to manufacture 50+ layer boards reliably. But equally important were the customer relationships. When a hyperscaler's engineers had worked with ISU PETASYS to solve particularly difficult signal integrity problems, that created trust that couldn't easily be replaced. The collaborative development model meant ISU PETASYS often knew about new products years before they launched, giving them time to prepare while competitors were caught flat-footed.

There was also the matter of capacity allocation. With demand exceeding supply across the industry, ISU PETASYS could choose its customers and products. They increasingly focused on the highest-margin, most technically challenging boards, leaving commodity products to others. This strategy required saying no to business, something that went against every instinct of a growth-oriented company, but it was essential for maintaining margins and technological leadership.

The geographic distribution of ISU PETASYS's facilities had become a major competitive advantage. ISU Petasys owns four factories in Daegu and one in Hunan in central China. Korean production for the most sensitive, highest-complexity products. Chinese production for volume and cost efficiency. The planned Southeast Asian operations for supply chain resilience. American facilities for customer intimacy and rapid prototyping. Each location served a specific strategic purpose, creating a network that was greater than the sum of its parts.

The rise of AI also changed how customers evaluated suppliers. In the past, purchasing decisions were primarily about cost, quality, and delivery. Now, technological roadmap mattered just as much. Could a supplier handle the next generation of products? Did they understand where the technology was heading? Were they investing ahead of the curve? ISU PETASYS's aggressive capacity expansion and technical investments sent a clear signal: they were committed to leading, not following.

But challenges remained. The Chinese operations, while profitable and strategically important, were becoming a liability with some customers. The U.S. government's restrictions on technology transfer to China created complications. Some customers wanted assurances that their designs wouldn't be manufactured in China or that Chinese engineers wouldn't have access to their intellectual property. ISU PETASYS had to navigate these demands carefully, maintaining operational efficiency while respecting customer concerns.

The talent war was another battlefield. Every competitor was trying to hire the same specialized engineers. ISU PETASYS's location in Daegu, while advantageous for costs and quality of life, made it harder to attract international talent compared to competitors in Silicon Valley or Taipei. The company responded with aggressive compensation packages and unique benefits, but the challenge persisted.

As the competitive landscape evolved, one thing became clear: the PCB industry was bifurcating. At one end, commodity producers competed on cost in a race to the bottom. At the other end, a handful of elite manufacturers competed on capability in a race to the top. ISU PETASYS had firmly positioned itself in the latter group, betting that in the AI era, performance would matter more than price. It was a bet that had paid off handsomely so far, but the race was far from over.

IX. Playbook: Business & Investment Lessons

[18 minutes]

If you had told investors in 2020 that one of the best-performing stocks of the AI boom would be a Korean PCB manufacturer founded when Nixon was president, most would have laughed. Yet ISU PETASYS's 487% surge in 2023 outperformed virtually every AI software company, every chip designer save Nvidia, and every other "obvious" AI play. The lessons from this unlikely success story are worth examining closely.

Lesson 1: The Power of Being "Picks and Shovels" in a Gold Rush

During the California Gold Rush, the biggest fortunes weren't made by miners but by those who sold them picks and shovels. ISU PETASYS embodies this principle perfectly. While everyone focused on the glamorous AI companies—the OpenAIs and Anthropics of the world—ISU PETASYS quietly provided the essential infrastructure that made it all possible. They didn't need to bet on which AI model would win or which company would dominate. They just needed AI to require massive amounts of computing power, which required complex PCBs. It was a bet on the entire ecosystem rather than any single player.

Lesson 2: Technical Capabilities Built Over Decades Compound Exponentially

ISU PETASYS didn't suddenly become capable of making AI accelerator boards when ChatGPT launched. They had spent decades incrementally building capabilities, each generation of products slightly more complex than the last. The expertise gained from making 20-layer boards in the 1990s enabled 30-layer boards in the 2000s, which enabled 40-layer boards in the 2010s, which positioned them for 50+ layer AI boards in the 2020s. This is the power of compounding in human capital and technical knowledge—it's slow and invisible for years, then suddenly explosive.

Lesson 3: Geographic Diversification as Optionality, Not Just Risk Mitigation

The conventional view of geographic diversification is defensive—spread operations to reduce risk. But ISU PETASYS showed how it can be offensive. Their Korean facilities gave them quality and innovation. Chinese facilities provided scale and cost. U.S. facilities offered customer intimacy. The planned Southeast Asian operations would bring supply chain flexibility. Each location wasn't just a backup for the others; it was a different tool for capturing different types of value. When geopolitical tensions rose, this diversification became a massive competitive advantage.

Lesson 4: The Hidden Value of "Boring" Infrastructure

ISU PETASYS's obscurity was a feature, not a bug. While flashy companies attracted competition and scrutiny, ISU PETASYS quietly built dominant positions. Investors ignored them because PCBs seemed boring and commoditized. Competitors underestimated them because they weren't seen as innovative. Customers initially overlooked them because they weren't a household name. This allowed ISU PETASYS to build capabilities and relationships without triggering competitive responses. By the time everyone realized their importance, the moats were already built.

Lesson 5: Family Control Can Be an Advantage in Capital-Intensive Industries

The conventional wisdom in Silicon Valley is that family-controlled companies are backwards and slow. But ISU PETASYS showed the advantages of patient family capital. The Kim family could make decade-long bets that public company CEOs focused on quarterly earnings couldn't. They could invest in capabilities before demand materialized. They could maintain strategic focus even when it meant lower short-term profits. The combination of family control with public market discipline created an optimal governance structure for long-term value creation.

Lesson 6: When Boring Becomes Beautiful

The transition from boring to beautiful happened almost overnight for ISU PETASYS, but the preparation took decades. This is perhaps the most important lesson: in technology revolutions, the companies that benefit most are often those that have been preparing longest, even if they didn't know exactly what they were preparing for. ISU PETASYS hadn't anticipated ChatGPT or the specific requirements of AI accelerators. But they had consistently pushed the boundaries of what was possible in PCB manufacturing. When the world suddenly needed those extreme capabilities, ISU PETASYS was ready.

Lesson 7: Timing Luck vs. Preparation Meeting Opportunity

Was ISU PETASYS lucky that AI exploded when it did? Absolutely. But as the saying goes, luck is when preparation meets opportunity. ISU PETASYS had been building AI-relevant capabilities since before the term "artificial intelligence" was trendy. Their work with supercomputers taught them about high-performance computing. Their data center experience prepared them for hyperscale customers. Their aerospace work instilled the quality standards AI hardware would demand. When the AI boom arrived, it looked like luck. But it was actually the culmination of decades of preparation.

The Meta-Lesson: Look for Technical Depth in Unfashionable Industries

The overarching lesson from ISU PETASYS is that extraordinary investment opportunities often hide in plain sight in unfashionable industries. The key is to look for companies with genuine technical depth—not just manufacturing capability, but real engineering expertise and problem-solving ability. These companies often trade at industrial multiples despite possessing technology moats that would make software companies envious. They're ignored because their industries seem mature and boring. But when technology shifts create new demands for their capabilities, the revaluation can be swift and dramatic.

ISU PETASYS also demonstrates the importance of understanding technology supply chains deeply. Most investors focus on the visible layer—the Nvidias and OpenAIs. But often the biggest opportunities are one or two layers down, in the companies that enable the enablers. These companies have less customer concentration risk, more diversified revenue streams, and often more sustainable competitive advantages.

Finally, ISU PETASYS shows that in technology investing, it's not enough to identify trends—you need to understand the physical infrastructure those trends require. AI needed more than just algorithms and data; it needed exotic cooling systems, advanced packaging, high-bandwidth memory, optical interconnects, and yes, incredibly complex printed circuit boards. The investors who understood these physical requirements and identified the companies best positioned to meet them were rewarded far more than those who simply bought "AI stocks."

X. Bear vs. Bull Case Analysis

[15 minutes]

The Bull Case: Riding the Multi-Decade AI Infrastructure Supercycle

The bulls see ISU PETASYS as sitting at the sweet spot of a generational investment opportunity. AI infrastructure spending isn't just beginning—we're in the first innings of what could be a multi-decade supercycle. Every major technology company has announced massive AI infrastructure investments. Microsoft alone committed $50 billion to AI infrastructure in 2024. Google, Amazon, Meta—they're all racing to build AI capabilities, and every dollar they spend flows through to companies like ISU PETASYS.

The technical moat is perhaps even more important than the market growth. These switches utilise 40+ layer MLBs, which are ISU's most advanced and lucrative product. The expertise required to manufacture these boards reliably cannot be quickly replicated. It's not just about having the right equipment—it's about years of accumulated knowledge, trained engineers, refined processes. Even if a competitor wanted to enter this market, they would be years behind, and by then ISU PETASYS would have moved even further up the complexity curve.

Customer concentration, often viewed as a risk, is actually a strength in this context. Its customers include Alphabet, Nvidia, Microsoft, Cisco, Arista Networks and Celestica. These aren't just any customers—they're the winners of the AI race, companies with essentially unlimited budgets for AI infrastructure. Being embedded with these customers gives ISU PETASYS early visibility into product roadmaps and ensures they're always working on the next generation of technology.

The geographic expansion strategy is already paying dividends. The Thailand joint venture provides options as companies seek supply chain resilience. The massive Korean expansion positions them for volume growth. The maintained presence in China keeps them relevant in the world's largest electronics market. This isn't just diversification—it's strategic positioning for multiple growth vectors.

Margin expansion could surprise to the upside. As AI boards become an even larger percentage of revenue and ISU PETASYS moves further up the complexity curve, margins should expand. The company has pricing power in a market where demand far exceeds supply. The billions being invested in capacity will depreciate over many years, but the revenue impact will be immediate.

The bull case extends beyond just AI accelerators. The same capabilities required for AI boards—high layer counts, superior signal integrity, thermal management—are increasingly needed across the data center. 400G and 800G networking, computational storage, advanced memory systems—all require the kind of complex PCBs that ISU PETASYS specializes in.

The Bear Case: Peak AI Hype Meets Structural Challenges

The bears see multiple red flags that bulls are ignoring in their enthusiasm. First and foremost is the cyclical nature of the semiconductor industry. Every boom in history has been followed by a bust, and the current AI infrastructure build-out shows classic signs of overcapacity in the making. When every hyperscaler is building massive AI clusters simultaneously, what happens when that demand is satisfied?

Customer concentration is a massive risk that bulls underplay. If even one major customer reduces orders or switches to a competitor, the impact on ISU PETASYS would be severe. The company has become dependent on a handful of customers who, while currently spending aggressively, could change priorities quickly. Remember how quickly the cryptocurrency mining boom turned to bust—AI could follow a similar pattern.

Competition is intensifying rapidly. Samsung Electro-Mechanics has essentially unlimited resources and could decide to buy market share. Chinese competitors, while currently held back by geopolitical concerns, are investing aggressively in capabilities and will eventually catch up. Even new entrants could emerge—if the margins are as attractive as bulls suggest, why wouldn't every PCB manufacturer try to enter this market?

The AI bubble concerns are real and growing. Valuations across the AI ecosystem have reached extreme levels. Companies are spending billions on AI with unclear paths to profitability. If we see an "AI winter" similar to previous cycles, the impact on infrastructure spending could be severe. ISU PETASYS's valuation assumes continued explosive growth, but any disappointment could lead to a violent re-rating.

Margin pressure is likely as products mature. Today's 50-layer AI board commanding premium prices will be tomorrow's commodity product. History shows that in electronics manufacturing, margins always compress over time as processes standardize and competition increases. The current margins might be peak margins, not sustainable margins.

Execution risk on the expansion is significant. Building new factories, scaling operations, maintaining quality—these are enormously complex challenges. The company is attempting to nearly triple revenue in six years while maintaining the quality standards that made them successful. One major quality issue with a key customer could unravel years of relationship building.

The geopolitical situation adds another layer of risk. ISU PETASYS is caught between U.S.-China tensions, trying to serve both markets while navigating increasingly complex regulations. The wrong move could alienate crucial customers or result in regulatory sanctions.

The Balanced View: Structural Growth with Cyclical Risks

The reality likely lies somewhere between the extremes. AI infrastructure investment is real and will continue for years, but not at the current frenetic pace indefinitely. ISU PETASYS has genuine competitive advantages, but they're not insurmountable. The company will likely continue to grow and prosper, but the path won't be linear.

The key variables to watch are AI model scaling laws (do larger models continue to deliver better results?), competitive dynamics in AI boards (does commoditization happen faster than expected?), and geopolitical developments (does the U.S.-China tech split accelerate?). Investors should also monitor customer diversification efforts and margin trends closely.

The valuation reflects both the opportunity and the risks, trading at multiples that would have seemed impossible for a PCB manufacturer just years ago but perhaps reasonable for a critical AI infrastructure player. For long-term investors who believe in the AI megatrend, ISU PETASYS offers exposure with less technical risk than chip designers and less business model risk than AI application companies. For those worried about an AI bubble, the customer concentration and valuation present clear risks.

XI. Looking Forward: The Next Chapter

[12 minutes]

As we stand at the precipice of 2025 and look toward the end of the decade, ISU PETASYS faces a future that is both more promising and more uncertain than at any point in its 53-year history. The company that once made simple boards for hard disk drives now finds itself at the center of humanity's attempt to create artificial general intelligence. Where this journey leads will determine not just ISU PETASYS's fate, but perhaps the trajectory of the entire technology industry.

Beyond GPUs: The Next Generation of AI Chips

The current AI boom has been driven primarily by GPUs, but the future will be more diverse. Custom AI chips from Google (TPUs), Amazon (Inferentia), and others are gaining traction. Emerging architectures like neuromorphic chips and quantum-classical hybrid systems are moving from research to reality. Each new architecture brings different PCB requirements—some need even higher layer counts, others require novel materials for cryogenic operation or photonic integration.

ISU PETASYS is already preparing for this future. Their R&D teams are working with customers on boards for chips that won't launch for three to five years. They're experimenting with new materials like liquid crystal polymers for ultra-high-frequency applications and thermally conductive substrates for chips that generate even more heat than today's monsters. The company that mastered 50-layer boards is now pushing toward 70, 80, even 100 layers—complexities that would have seemed physically impossible just years ago.

Edge AI: A Different Challenge, A Bigger Opportunity

While data center AI gets the headlines, edge AI might ultimately be the larger market. Autonomous vehicles, robots, smart factories, augmented reality devices—all require AI processing at the edge, where latency and power consumption matter more than raw performance. Edge AI boards have different requirements: they must be smaller, more power-efficient, more resistant to environmental stresses, but still capable of high-performance computing.

ISU PETASYS's diverse background positions them well for this transition. Their automotive experience taught them about reliability in harsh environments. Their consumer electronics heritage gave them expertise in miniaturization. Their aerospace work developed capabilities in thermal cycling and vibration resistance. As AI moves from climate-controlled data centers to the chaotic real world, these capabilities become invaluable.

Sovereign AI and the New Geopolitics of Technology

Countries around the world are awakening to AI's strategic importance. The EU, Japan, India, Saudi Arabia—all are launching sovereign AI initiatives, building domestic AI capabilities independent of U.S. or Chinese technology. This creates enormous opportunities for companies like ISU PETASYS that can serve multiple markets without the baggage of being American or Chinese.

The Southeast Asian expansion through the Thailand joint venture looks particularly prescient in this context. ASEAN countries are trying to chart a neutral path in the U.S.-China tech war, and having production capacity in Thailand allows ISU PETASYS to serve both sides while maintaining neutrality. The company could become the Switzerland of AI infrastructure—trusted by all, aligned with none.

Can They Maintain Margins as Volumes Scale?

The million-dollar question—or rather, the billion-dollar question—is whether ISU PETASYS can maintain its current margins as AI boards become more mainstream. History suggests that all electronic components eventually commoditize, but AI boards might be different. The complexity continues to increase faster than manufacturing technology improves. The customer requirements become more stringent, not less. The barriers to entry keep rising, not falling.

ISU Petasys said it plans to become a leading company in the global market by raising sales of KRW579 billion ($430.9 million) as of last year to KRW1.5 trillion ($1.12 billion) by 2030. Achieving this nearly 3x revenue growth while maintaining margins will require careful execution. The company must resist the temptation to chase volume at the expense of profitability. They must continue investing in next-generation capabilities even as they scale current-generation production. They must balance the needs of demanding customers with the realities of manufacturing economics.

The Succession Question and Corporate Governance Evolution

Kim Sang-beom has led ISU PETASYS through its transformation from obscure component supplier to AI infrastructure champion. But he won't lead forever, and the succession question looms large for family-controlled Korean companies. Will the next generation of the Kim family take the reins? Will the company professionalize management by bringing in outside leadership? How will they balance family control with the governance demands of international investors and customers?

The recent controversy over the proposed JEIO acquisition highlights these tensions. The company's attempt to diversify into battery materials faced fierce resistance from minority shareholders who saw it as empire-building rather than strategic expansion. The episode revealed both the benefits of family control (ability to make bold strategic moves) and its drawbacks (potential conflicts of interest).

The Convergence of AI and Other Exponential Technologies

Looking further ahead, ISU PETASYS might benefit from the convergence of AI with other exponential technologies. Quantum computing will require exotic PCBs that can maintain superconducting connections. Brain-computer interfaces will need biocompatible boards that can operate inside the human body. Space-based data centers will require boards that can withstand radiation and extreme temperature swings.

Each of these markets might seem like science fiction today, but then again, so did AI accelerators consuming 700 watts and costing $40,000 each. ISU PETASYS's history shows that the company has consistently positioned itself for technologies that seemed exotic but became essential. Their current investments in advanced manufacturing capabilities could position them for opportunities we can't yet imagine.

The next chapter of ISU PETASYS will be written not in Daegu's boardrooms but in the clean rooms where engineers push the boundaries of physics, in the customer meetings where next-generation architectures are designed, and in the markets where investors bet on the future of technology infrastructure. It's a chapter that promises to be even more dramatic than the last, with higher stakes, bigger opportunities, and greater challenges.

XII. Epilogue & Reflections

[10 minutes]

Standing in the ISU PETASYS facility in Daegu today, you can almost feel the weight of history and the pull of the future in equal measure. The same building that once produced boards for Nokia phones now crafts the silicon substrates that power humanity's attempt to create artificial intelligence. It's a transformation that speaks to something profound about technology, business, and the nature of innovation itself.

What Silicon Valley Can Learn from Korean Manufacturing Excellence

Silicon Valley loves to talk about disruption, about moving fast and breaking things, about software eating the world. But ISU PETASYS represents a different philosophy—one of patient excellence, incremental improvement, and deep technical mastery. While Silicon Valley was busy creating and destroying social media companies, ISU PETASYS was quietly perfecting the art of embedding copper traces in fiberglass, getting slightly better every year, until suddenly they were irreplaceable.

There's a humility in this approach that feels foreign to the contemporary tech culture but might be exactly what's needed as we enter the age of atoms, not just bits. AI might be trained in software, but it runs on hardware. Electric vehicles might be defined by their algorithms, but they move on batteries and motors. The future might be digital, but it will be built on a foundation of advanced materials and precision manufacturing—capabilities that take decades to develop and can't be downloaded from GitHub.

The Hidden Infrastructure Layer of the AI Revolution

ISU PETASYS's story reveals something important about how we think about technology revolutions. We focus on the visible layer—the ChatGPTs and Stable Diffusions—but miss the invisible infrastructure that makes it all possible. For every AI researcher tweaking model architectures, there are hundreds of engineers ensuring power delivery, managing thermals, maintaining signal integrity. For every headline about AI breakthroughs, there are thousands of hours spent perfecting the manufacturing processes for the boards those AIs run on.

This hidden layer is where much of the value in technology revolutions actually accrues. The companies that build the infrastructure often capture more value than those who use it. AWS is more valuable than most of the startups that run on it. TSMC is worth more than many of the chip designers who depend on it. And ISU PETASYS, in its own way, has become indispensable to the AI revolution while remaining largely unknown to those who benefit from it.

Why This Story Went Unnoticed Until 2023

The ISU PETASYS story was hiding in plain sight for years. The capabilities were there. The customer relationships were there. The technical moat was there. But it took the ChatGPT moment—that sudden collective realization that AI was real and transformative—for the market to recognize what had been building for decades.

This delayed recognition is actually common in infrastructure plays. The value is created slowly, invisibly, through countless small improvements and solved problems. Then, suddenly, a catalyst appears—a new use case, a demand spike, a technology transition—and what seemed like a sleepy industrial company is revealed as a critical enabler of the future.

Parallels to Previous Technology Infrastructure Booms

The ISU PETASYS story echoes through technology history. During the railroad boom, the biggest fortunes were made not by railroad operators but by steel producers and land owners along the routes. In the internet boom, the optical fiber manufacturers and network equipment makers captured enormous value while many dot-coms went bust. During the mobile revolution, tower companies and backhaul providers generated steady returns while handset makers struggled.

Each time, the pattern is the same: a visible technology captures imagination and investment, but the invisible infrastructure that enables it captures value. The infrastructure providers have more diverse customers, more sustainable moats, and more predictable business models. They're boring until they're not, overlooked until they're essential.

Finding the Next ISU PETASYS

So where is the next ISU PETASYS hiding? It's probably not where you're looking. It won't be at tech conferences or in TechCrunch headlines. It will be in some industrial park, in some unfashionable industry, quietly solving hard problems that don't seem important yet.

Look for companies with real technical depth, not just manufacturing scale. Look for patient capital structures that allow long-term thinking. Look for customer relationships that go beyond vendor-buyer to true collaboration. Look for capabilities that take years to develop and can't be easily replicated. Look for markets where complexity is increasing faster than automation can simplify.

Most importantly, look for companies positioned at the intersection of multiple technology trends. ISU PETASYS wasn't just a PCB company—they were at the intersection of high-performance computing, telecommunications, and advanced materials. When AI emerged requiring all three capabilities simultaneously, ISU PETASYS was uniquely positioned to benefit.

Final Thoughts: The Beautiful Mundanity of Making Things

In an age of virtual reality and digital twins, of metaverses and large language models, there's something profoundly grounding about ISU PETASYS's story. They make physical objects. They solve real engineering problems. They turn copper and fiberglass into the substrates that power our digital dreams.

Their success reminds us that for all our digital sophistication, we still live in a physical world governed by physical laws. Electrons still need paths to flow. Heat still needs to be dissipated. Signals still need to maintain integrity. These mundane realities create opportunities for companies that master them.

The ISU PETASYS story is ultimately about the value of deep expertise, patient capital, and perfect timing. It's about being ready when opportunity arrives, even if you don't know exactly what form it will take. It's about building capabilities that compound over decades until they become irreplaceable.

As we stand on the brink of an AI-transformed world, ISU PETASYS reminds us that transformation requires not just vision and algorithms, but also copper traces and fiberglass layers, clean rooms and plating baths, engineers who understand Maxwell's equations and workers who can operate machines with nanometer precision.

The future might be artificial intelligence, but it will be built on very real, very physical, very human foundations. And somewhere in Daegu, South Korea, in factories that smell of solder and chemicals, the future is being manufactured one layer at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube