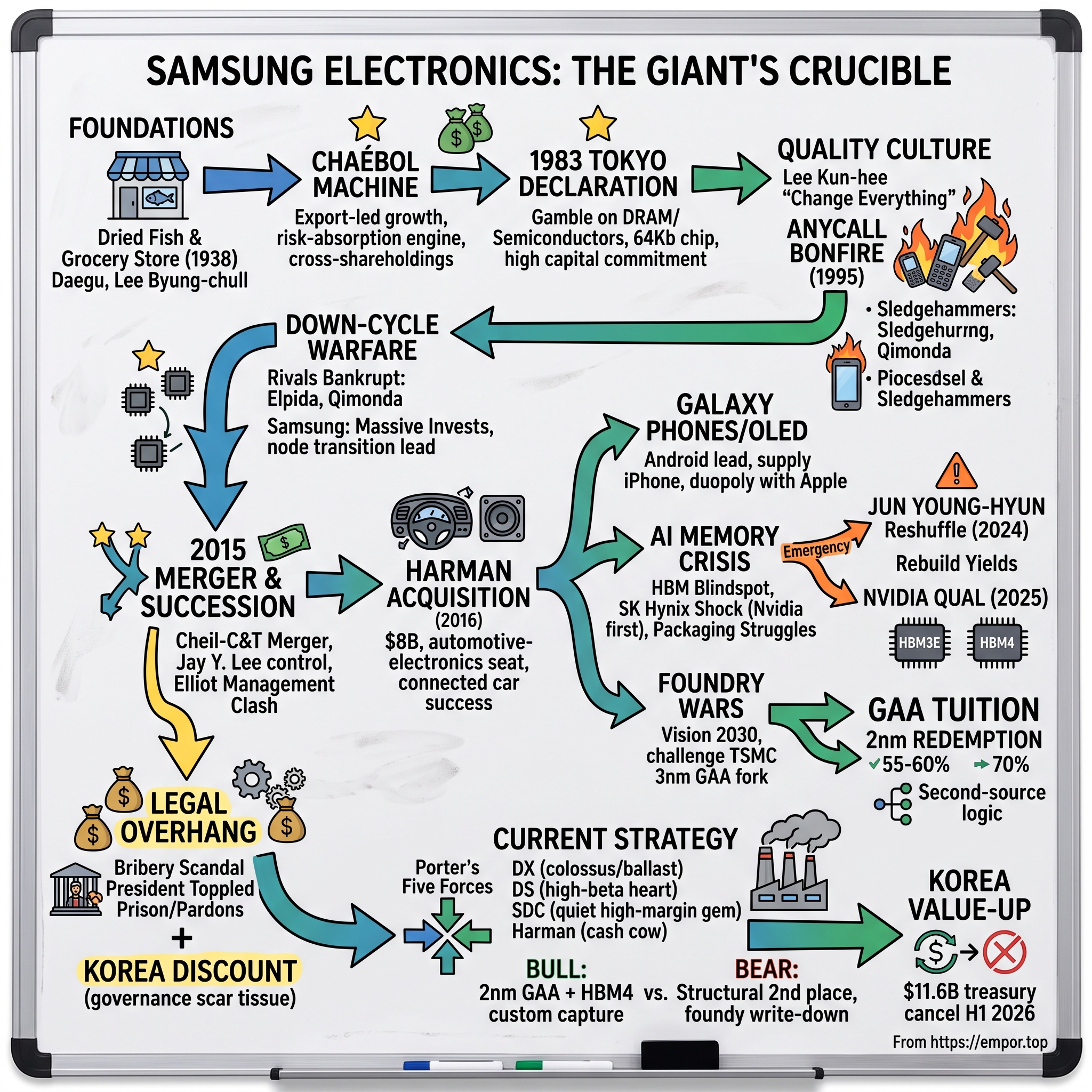

Samsung Electronics: The Giant's Crucible

I. Introduction & Episode Roadmap

Picture the single most valuable company in Asia's fourth-largest economy — a firm that stamps its logo on roughly one in five smartphones sold on Earth, that fabricates the memory chips inside data centers on every continent, that supplies the very OLED screen glowing on the front of an Apple iPhone. Now picture that same company, in the spring of 2024, quietly convening an emergency reshuffle of its semiconductor leadership because it had missed — badly, and in public — the defining technology wave of the decade.

That is the paradox of 삼성전자 Samsung Electronics Co., Ltd. In its 2024 fiscal year the group generated KRW 300.9 trillion in revenue, and by 2025 it had climbed to KRW 333.6 trillion — roughly $240 billion — with group operating profit of KRW 43.6 trillion.12 Samsung had spent four decades as the undisputed king of commodity memory, the company that other memory makers priced against and, one by one, went bankrupt fighting. And yet when generative artificial intelligence detonated demand for a specialized product called high-bandwidth memory (HBM), Samsung was not the beneficiary. Its smaller domestic rival, SK하이닉스 SK Hynix, was.

The core conflict of this story is the collision between two Samsungs. There is the historical Samsung: a machine of brutal scale, ruthless capital deployment, and process engineering so relentless it drove unit costs below what any competitor could survive. And there is the vulnerable Samsung: a company that, at the exact moment the industry pivoted from selling memory by the ton to selling memory as a bespoke, co-engineered component, found its once-untouchable "process power" had quietly cracked — in HBM packaging, and again in the yield struggles of its advanced foundry.

Here is the road we will travel. We begin in a dried-fish and grocery store in Daegu in 1938, and the audacious 1983 "Tokyo Declaration" that took Samsung into DRAM with, essentially, zero expertise. We move to 이건희 Lee Kun-hee and the near-religious quality culture he forged by literally setting fire to his own products. We enter the succession crucible — the 2015 merger, Paul Singer's Elliott Management, a bribery scandal that toppled a president, and the long legal ordeal of 이재용 Jay Y. Lee. We benchmark the $8 billion Harman bet. We dissect the HBM defeat and the scramble to recover. We walk the advanced foundry battlefield where Samsung and 台積電 TSMC diverged at the 3nm node. And finally we size the segment economics, weigh management's credibility against its own past promises, and stress-test the whole edifice against South Korea's 기업 밸류업 corporate value-up program.

Why does this story matter beyond the drama? Because Samsung Electronics is not merely a company; it is a load-bearing pillar of an entire national economy, accounting for a share of South Korea's exports and market capitalization that would be unthinkable for any single firm in the United States or Europe. When Samsung stumbles, Seoul's benchmark index stumbles, foreign fund flows into Korea wobble, and the national conversation about chaebol reform reignites. For a global investor, Samsung is simultaneously the cleanest way to own the memory cycle, a leveraged bet on the AI hardware buildout, a call option on a foundry challenger, and a wager on whether Korean corporate governance can genuinely change. Few large-cap equities bundle so many distinct theses under one ticker — which is exactly what makes it both compelling and confusing.

This is not an investor-relations brochure. Samsung says it will reclaim its crown. The job here is to ask what evidence actually supports that — and what would prove it wrong.

II. Foundational Legacy & The "Tokyo Declaration" (1938–1983)

The origin is almost comically modest. In 1938, a young entrepreneur named 이병철 Lee Byung-chull opened a trading company in Daegu that dealt in dried fish, locally grown produce, and noodles — exporting to Manchuria and Beijing.[^4] The name he chose, Samsung, means "three stars." There was nothing in that storefront to suggest that within two generations the firm would be etching circuits measured in billionths of a meter.

What came next was the classic arc of a country rebuilding from catastrophe. South Korea in 1953, in the wake of the Korean War, was one of the poorest places on the planet — its per-capita income trailing much of sub-Saharan Africa. Lee rode the reconstruction: sugar refining, textiles, insurance, retail, fertilizer. Each business threw off cash that funded the next. By the 1970s Samsung had become a sprawling 재벌 chaebol — one of the family-controlled industrial conglomerates that the Korean state deliberately cultivated as instruments of national development.

The chaebol machine

To understand Samsung you must understand the chaebol bargain. Park Chung-hee's government pursued export-led industrialization with an iron hand: it directed cheap credit, protected home markets, and rewarded conglomerates that could win abroad. The chaebol, in turn, diversified across wildly unrelated industries — shipbuilding, chemicals, electronics, construction, life insurance — held together by cross-shareholdings and a founding family's absolute authority. Critics would later call this structure opaque and self-dealing. But in the early, capital-hungry decades it did something valuable: it let a single group absorb enormous, sustained losses in one venture using the steady profits of another.

That cushion is the whole reason the next chapter was even possible.

The Tokyo gamble

On February 8, 1983, Lee Byung-chull, then in his seventies, phoned a newspaper chairman from Tokyo and asked him to tell the readers of Korea: Samsung was entering the semiconductor business, no matter what it took.3 This became known as the 도쿄 선언 Tokyo Declaration, and by any rational assessment of the time it was reckless.

Consider what DRAM manufacturing actually demanded. It is one of the most capital-intensive, technically unforgiving industries ever created — a business where you spend billions to build a fabrication plant, where a speck of dust can ruin a wafer, and where the product is a commodity whose price collapses on a brutal cycle. Samsung had tried and failed to make chips before; it had bought a struggling firm called Korea Semiconductor in 1974 and produced nothing of note.3 The Japanese giants — NEC, Hitachi, Toshiba — were a decade ahead and defended their lead ferociously. Lee committed roughly $400 million of the group's reserves against the near-unanimous objection of his own senior executives.3

His logic was not about the memory chip itself. It was that semiconductors would become the foundational input of every future electronic product — that whoever controlled the chip controlled the value chain above it. It was, in other words, a bet on where the world was going, financed by where the group already was.

The early results validated the skeptics before they validated Lee. Samsung built its first fab in about six months, a task that normally took a year and a half, and developed a 64-kilobit DRAM — becoming, remarkably, only the third country in the world to do so.3 But developing a chip and profiting from a chip are different things. The semiconductor division bled cash for years. Those losses did not sink the company for one reason: the textiles, the sugar, the paper, the insurance — the boring, stable businesses — paid the bills while the chip engineers learned.

The strategic lesson embedded here would echo through everything Samsung later did. In the earliest, money-losing phase of a capital-intensive industry, a diversified conglomerate is not a governance embarrassment — it is a risk-absorption engine. Samsung could afford to lose money learning DRAM precisely because it was not only a DRAM company. Hold that thought; decades later, the same structure that funded the gamble would become the thing activist investors attacked.

By the time Lee Byung-chull died in 1987, the foundation was laid. But it took his son to turn a fast-follower into a hegemon — and he did it by burning things.

III. The "New Management" Doctrine & Rise of the DRAM Hegemon (1983–2010s)

In 1993, on a business trip to Los Angeles, Lee Kun-hee walked into an electronics store and found Samsung televisions shoved to the back, gathering dust, ignored by shoppers reaching for Sony and Panasonic. Samsung was, by then, a large and growing manufacturer. But large and cheap is not the same as good, and Lee Kun-hee — who had inherited the chairmanship in 1987 — was viscerally offended by the gap.

"Change everything except your wife and children"

On June 7, 1993, he summoned roughly 200 senior executives to Frankfurt and delivered what became Samsung's founding scripture of the modern era. Over days of marathon meetings he demanded a total reversal of the company's DNA — from quantity to quality, from fast-follower to leader. His line has been quoted ever since: "Change everything except your wife and children."5 He warned that in an era of globalization, a company that refused to change would remain "forever a second-rate player."5

This was not a slogan; it was a cultural detonation. And Lee Kun-hee understood that culture is changed by spectacle, not by memo. He got his spectacle in 1995.

The Anycall bonfire

Samsung's mobile phone division, racing to get products out the door, had let its defect rate climb toward 12%. Lee ordered every faulty unit recalled. In March 1995, at the Gumi factory, workers piled roughly 150,000 phones, fax machines, and other devices — worth an estimated $15 million — into a heap in front of 2,000 assembled employees.[^7] Ten workers wearing "Quality First" headbands smashed the pile with sledgehammers, and then it was set on fire while employees reportedly wept.[^7]

The theater was the point. Lee was making an unforgettable, physical statement that Samsung would rather burn its own inventory than ship something second-rate. Whether one reads this as inspired leadership or authoritarian corporate ritual, the effect on Samsung's manufacturing discipline was real and lasting — it became the origin myth of the company's obsession with yield and quality control, the same obsession that would later define its memory dominance.

Down-cycle warfare

Now comes the part that made Samsung genuinely feared. Memory is cyclical in a way that is hard to overstate: when demand softens, prices don't just dip, they crater, because the product is a commodity and every producer is dumping supply at once. In these downturns, most companies do the sane thing — they cut capital spending, mothball capacity, and wait for the storm to pass.

Samsung did the opposite. In the deepest troughs, when rivals were slashing investment to survive, Samsung poured capital into new capacity and faster node transitions.[^5] The logic was cold and correct: by adding the most advanced, lowest-cost supply exactly when everyone else retreated, Samsung drove the market price below its competitors' cost of production. It could bleed in a downturn longer than anyone else could, and it used that endurance as a weapon.

The body count tells the story. Germany's Qimonda went bankrupt in 2009. Japan's Elpida — エルピーダ, the last independent Japanese DRAM maker, itself a merger of survivors — collapsed into bankruptcy in 2012 and was absorbed by Micron. What had been a fragmented field of a dozen memory makers consolidated into a three-player oligopoly: Samsung, SK Hynix, and Micron. Today those three control well over 90% of the world's DRAM. That structure — an oligopoly forged in the fire of Samsung's counter-cyclical aggression — is the single most important fact about memory economics, and we will return to it when we weigh the investment case.

The "golden copy"

The final pillar of the DRAM hegemony was operational: Samsung's ability to move to each new manufacturing node faster than rivals while holding yields high. In memory, the company that shrinks its transistors first at good yield produces more bits per wafer at lower cost — and captures a disproportionate share of profit when prices recover in the upcycle.[^5] Samsung's engineers turned node transitions into a repeatable, replicable process — an internal "golden copy" they could stamp out across fabs. For most of two decades this process advantage looked permanent, a structural moat that no competitor could cross.

From chips to Galaxy

The memory war was invisible to consumers, but the same quality doctrine reshaped the businesses they could see. Through the 2000s Samsung parlayed its manufacturing muscle into two consumer conquests. First came flat panels: as the world abandoned bulky cathode-ray televisions for LCD and later OLED, Samsung's willingness to sink billions into panel fabs made it the world's top television maker by the late 2000s, a position it has held for well over a decade. Second, and more consequentially, came the phone. When Apple's iPhone redefined the smartphone in 2007, Samsung — unlike Nokia and BlackBerry — did not freeze. It embraced Google's Android, launched the Galaxy S line in 2010, and threw its entire vertically integrated arsenal at the problem: it made the processor, the memory, the display, and the battery, and it out-marketed every other Android maker on Earth.

The result was a genuine duopoly at the top of the phone market and, for a stretch, the largest smartphone shipment volume in the world. But the phone business also taught Samsung the limit of its own model. Hardware, however excellent, is commoditizing; Apple captured the lion's share of industry profit through software, services, and brand, while Samsung captured volume at thinner margins. That asymmetry — Samsung as the supreme manufacturer, Apple as the supreme monetizer — is the enduring shape of the rivalry, and it is why Samsung's most profitable relationship with Apple is not as a competitor but as its supplier, selling Apple the very OLED panels and memory that go inside the iPhone. Few rivalries in business are as intimate.

It was not permanent, this untouchability. But before the moat cracked, the family that owned it faced a crisis that had nothing to do with chips and everything to do with mortality, taxes, and control.

IV. The Succession Crucible: The 2015 Merger & The Elliott Management Clash

In May 2014, Lee Kun-hee suffered a heart attack. He would never recover, lingering in a hospital bed for six years until his death in October 2020. His incapacitation set off a silent, high-stakes race inside the House of Lee: how to transfer control of one of the world's largest industrial empires to his son, Jay Y. Lee, before the patriarch died — and before the tax bill came due.

The inheritance trap

South Korea imposes one of the highest inheritance taxes on Earth — an effective rate that can approach 50% or more on large estates and controlling stakes. For a founding family whose entire power rests on holding just enough equity at the top of a cross-shareholding pyramid, that tax is existential. Sell shares to pay it, and you risk losing control of the empire the shares represent. The Lee family needed to tighten Jay Y. Lee's grip on the group's crown jewel — Samsung Electronics — without triggering a fire sale.

The problem was the org chart. Jay Y. Lee held a large personal stake in an affiliate called 제일모직 Cheil Industries. But the affiliate that actually held a critical 4.1% block of Samsung Electronics was 삼성물산 Samsung C&T, the group's construction and trading arm — and there, Lee's direct stake was thin. Control of the electronics business ran through Samsung C&T. So the family needed Jay Y. Lee's Cheil ownership to translate into control of Samsung C&T.

The merger formula

The solution, announced in 2015, was an all-stock merger of Cheil Industries and Samsung C&T at a fixed ratio — one that valued Cheil richly and Samsung C&T cheaply. Because Lee owned far more of Cheil, the exchange ratio handed him an outsized share of the combined entity, and with it, a firmer grip on the Samsung Electronics stake buried inside. It was, in effect, a mechanism to pass control down a generation using other shareholders' equity as the fulcrum.

To minority owners of Samsung C&T, this looked like value being transferred out of their pockets and into the founding family's. Enter the activist.

Paul Singer comes to Seoul

Elliott Management, the famously combative fund run by Paul Singer, disclosed a 7.12% stake in Samsung C&T and launched a public campaign to block the deal.6 Elliott's argument was straightforward and, to many independent observers, compelling: the merger ratio undervalued Samsung C&T — some analyses put the gap at more than 30% — for the benefit of the Lee family at the expense of ordinary shareholders.6 The influential proxy adviser ISS recommended shareholders reject it.7

What followed exposed the machinery of Korean corporate power in a way foreign investors never forgot. The swing vote belonged to the 국민연금공단 National Pension Service (NPS) — the government-controlled pension fund and one of Samsung C&T's largest shareholders. In July 2015, over the objections of independent advisers, the NPS voted for the merger, and it narrowly passed.6[^10]

The scandal that toppled a president

The story did not end at the ballot. A criminal investigation later revealed that the NPS's decisive support had been secured through corruption: Samsung had funneled bribes to a confidante of President Park Geun-hye — 박근혜 — to win the government's backing. The scandal metastasized into a national crisis. Park was impeached and removed from office in 2017. Jay Y. Lee was convicted of bribery, embezzlement, and related crimes, sentenced to five years, and imprisoned; his sentence was reduced on appeal, he was released, re-imprisoned in January 2021, released again on parole, and finally pardoned by President Yoon Suk Yeol in August 2022 on the argument that Samsung was too important to the economy to leave leaderless.20

A separate case — accusations of stock manipulation and accounting fraud tied to the merger itself — dragged on for years. Lee was acquitted at trial in early 2024, and in July 2025 South Korea's Supreme Court upheld that acquittal, finally closing the criminal chapter.8 Elliott, for its part, pursued Seoul through an investor-state arbitration; in 2023 an international tribunal partially accepted Elliott's claims and ordered the Korean government to pay damages over the NPS's role.[^10]

The Korea Discount, made concrete

Step back from the legal thicket and the investment meaning is stark. This episode did not merely embarrass Samsung; it codified, in the minds of global investors, the "코리아 디스카운트" Korea Discount — the persistent valuation gap by which Korean companies trade below international peers. The mechanism is trust: when minority shareholders learn that the controlling family may engineer transactions to entrench itself, and that the state may help, they demand a higher risk premium — which is just another way of saying they pay less for the same earnings. Samsung's governance scar tissue became a permanent line item in its cost of capital, and undoing it is the central question of the value-up debate we will reach at the end.

There is a subtler cost, too, one that outlasted the headlines. The merger locked in a control structure — a pyramid running from the family through Samsung Life Insurance and the merged Samsung C&T down to Samsung Electronics — that constrains what the group can do with its own crown jewel. Insurance regulation, cross-shareholding rules, and the ever-present risk that unwinding any link could trigger a tax event or a loss of control mean that Samsung Electronics is, in a sense, held hostage by the architecture built to keep it in the family. An activist would put it bluntly: the world's premier memory maker has a suboptimal owner structure bolted on top of it, and every debate about dividends, buybacks, and reinvestment is refracted through the family's need to defend that structure. This is not a historical footnote; it is a live variable in 2026, and it is why governance sits at the center of the bull-bear divide rather than at its margins.

For now, note the irony: even as the family fought for control, it was also sitting on one of the largest corporate cash piles in the world. What it chose to do with a slice of that cash, in 2016, became one of the more quietly successful acquisitions in modern tech.

V. The $8 Billion Masterstroke: Benchmarking the Harman Acquisition

When Samsung announced in November 2016 that it would pay $8 billion — $112 per share, all cash — for a US audio and automotive-electronics company called Harman International, the reaction ranged from puzzled to dismissive.9 Samsung made phones and chips and TVs. Harman made premium car speakers and infotainment systems. Analysts asked the obvious question: what was the world's biggest consumer-electronics maker doing paying a rich premium to enter the slow-moving, relationship-driven automotive supply business, years after the connected-car theme was already fashionable?

Buying a seat in the dashboard

The strategic thesis, in fairness, was coherent. Roughly two-thirds of Harman's revenue at acquisition was automotive-related, and it came with something Samsung could not build quickly: decades-deep design-win relationships with the world's premium automakers, and audio brands — Harman Kardon, JBL, Bang & Olufsen licensing, Mark Levinson — embedded in millions of cars.9 Harman's audio and telematics systems were already installed in tens of millions of vehicles. Samsung was not buying a product; it was buying a credentialed seat inside the automobile at the exact moment the car was becoming a computer on wheels.

The skepticism was not unreasonable either. Big tech's history of large acquisitions is littered with write-downs, and "we'll find the synergies later" is the epitaph on many of them. So the honest way to judge Harman is not by the press release but by the arithmetic, years on.

The numbers, years later

Here the results speak for themselves. In fiscal 2024, Harman generated KRW 14.27 trillion in revenue and KRW 1.31 trillion in operating profit — a record, and up from roughly KRW 559 billion in 2021, KRW 880 billion in 2022, and KRW 1.17 trillion in 2023.1[^13] That operating profit of about $900 million on an $8 billion purchase price is a mid-single-digit-percent annual operating yield on the original outlay — and that is before crediting any strategic value from the technology and relationships. Measured against the graveyard of overpriced big-tech deals, Harman turned into an unusually clean win: a business Samsung bought at a fair price that compounded into a stable, growing cash generator.[^13]

What made it work was integration few outsiders anticipated: Samsung Display's premium OLED panels feeding Harman's digital cockpits, paired with Harman's audio and telematics, let the combined unit win multi-billion-dollar "digital cockpit" contracts with premium marques including BMW and Mercedes-Benz.[^13] The evidence suggests the deal delivered not because of a flashy thesis but because Samsung largely left a well-run business alone, fed it components it uniquely made, and let the automotive cycle work in its favor.

The analytical lesson is subtler than "Harman was a good deal." It is that Samsung's best capital deployment came from buying an adjacent business it understood how to feed, at a reasonable price, and then exercising restraint — not from a transformational moonshot. That is a flattering data point for capital discipline, but it is also a narrow template. Harman is a stable, mid-margin cash cow; it is not the kind of asset that moves the needle for a group whose profits are dominated by the memory cycle. In a year when DS alone can swing by tens of trillions of won, Harman's roughly KRW 1.3 trillion of operating profit is real money but rounding-error material to the equity story. The deal proves Samsung can allocate capital well; it does not prove Samsung can allocate capital at the scale its balance sheet permits. That gap — between demonstrated competence on a $8 billion deal and a decade of inaction on a far larger cash pile — is the thread that runs into every capital-allocation debate that follows.

The M&A drought

And yet Harman's success poses an awkward question that cuts against management. It was Samsung's last mega-acquisition. In the nearly ten years since, the company has not closed another deal of remotely comparable scale — despite a balance sheet that could fund almost anything.

Why? Part of the answer is the legal paralysis of the chairman during his years of trials and imprisonment, which froze bold capital allocation at the top. Part is regulatory reality: at Samsung's scale, the most logical targets — a merchant chip or IP giant — invite antitrust and national-security vetoes, as the collapse of NXP's and Arm's respective sale processes to other suitors demonstrated the risk. And part is cultural: post-crisis Samsung is run by consensus-driven professional managers who are structurally cautious. A skeptical investor would frame it plainly — Samsung proved it could deploy $8 billion brilliantly, then spent a decade sitting on a cash pile it could not, or would not, similarly deploy. That tension between capacity and action is a recurring theme, and nowhere did inaction cost more than in the product Samsung should have owned outright: the memory chip that powers AI.

VI. The AI Memory Crisis: High Bandwidth Memory (HBM) & The SK Hynix Shock

For thirty years there was one rule in memory that everyone knew: nobody beats Samsung on a memory chip. Samsung had the scale, the yields, the golden copy. Then, sometime around 2023, the rule broke — and it broke against a smaller Korean rival that Samsung had spent decades looking down on.

What HBM actually is

Start with the technology, because the whole drama turns on it. An AI accelerator — an Nvidia GPU — is a ferociously fast calculator that is perpetually starving for data. The bottleneck is not compute; it is feeding the compute. High-bandwidth memory solves this by stacking DRAM chips vertically, like a high-rise instead of a subdivision, and wiring them to the processor through thousands of microscopic connections so data flows in a torrent rather than a trickle. The catch: stacking a dozen wafer-thin chips into a tower, without warping them or trapping heat, is monstrously hard. HBM is less a commodity and more a feat of 3D packaging and thermal engineering.

And that is precisely where Samsung's traditional advantage — being the best at making a single flat memory chip cheaply — mattered less than being the best at gluing a tower of them together.

The blindspot

In the late 2010s, Samsung's management looked at HBM and saw a niche. AI memory, the thinking went, would remain a small, specialized, low-volume product — not worth prioritizing over the vast commodity DRAM and NAND business that paid the bills. Reporting and subsequent accounts indicate the company pulled back on HBM development at the very moment it should have been pressing the accelerator. It was a classic incumbent's error: the market that looks like a rounding error today is the market that eats you tomorrow.

Meanwhile, SK Hynix — the perennial number two, forged from the wreckage of Hyundai's semiconductor unit — made the opposite bet. It partnered closely with Nvidia and poured effort into HBM, and crucially it pioneered a packaging method called Mass Reflow Molded Underfill, or MR-MUF. In plain terms: instead of stacking chips and pressing thin films between each layer one at a time (Samsung's thermal-compression, non-conductive-film approach, TC-NCF), SK Hynix flowed a protective material around the whole stack at once, which dissipated heat better and yielded more good units. When you are building thermal high-rises, the company with the better method for keeping them cool and intact wins.

The Nvidia lockout

The consequence was the most painful kind for a proud company: exclusion. As the generative-AI boom exploded in 2023 and 2024, Nvidia's rigorous qualification process — the multi-month gauntlet a supplier must pass before its chips are allowed into a GPU — became the gate to the fastest-growing, highest-margin memory market in history. SK Hynix walked through first and captured near-monopoly economics during the early, most lucrative phase. Samsung got stuck at the gate. Its HBM3 and then its HBM3E chips repeatedly failed or lagged in Nvidia's validation, quarter after quarter, in a public and humiliating slow-motion failure. By mid-2025, market trackers put SK Hynix at roughly 62% of the HBM market, with Micron having overtaken Samsung for second place and Samsung down around 17%.11 The king of memory was running third in memory's most important product.

The emergency turnaround

Samsung's response revealed how seriously it took the crisis. In May 2024 — not at the usual year-end reshuffle, but mid-year, an almost unheard-of signal of urgency — the company replaced the head of its Device Solutions (semiconductor) division. Out went 경계현 Kyung Kye-hyun, reassigned to lead the group's advanced research institute and future-business planning; in came 전영현 Jun Young-hyun, a memory veteran who had run the business years earlier and had since led Samsung SDI, the battery affiliate.10 In November 2024, Samsung deepened the shake-up, elevating Jun and restructuring the chip leadership further as the stock languished.17

Jun's playbook was less about slogans than about engineering fundamentals. He consolidated fragmented HBM development teams that had been working at cross-purposes, and drove the organization back to first-principles problem-solving on packaging and yield.10 Whether this was visionary or simply overdue, the market gave him credit for stabilizing quality and rebuilding institutional confidence.

The validation milestones followed, and this is where an independent read matters — because management's narrative and the proven facts must be separated. What is proven: in September 2025, Samsung cleared Nvidia's qualification for its 12-layer HBM3E, ending the long lockout on the prior-generation product.[^15] Under new leadership the DS division rebounded to record memory revenue as the 2025 memory cycle turned sharply upward.217 What remains a claim to be tested: Samsung's assertion that it is positioned to lead in the next generation. The company has aligned with Nvidia — whose CEO 黃仁勳 Jensen Huang has publicly courted all three memory makers — on next-generation HBM4 and custom silicon, and in 2026 Samsung and SK Hynix were both reported as suppliers for Nvidia's Rubin platform, with SK Hynix still slated to take the larger share.15 In May 2026 Samsung said it had shipped industry-first 12-layer HBM4E samples, claiming a lead of several months over SK Hynix.16

That last claim is exactly the kind of assertion an investor should hold at arm's length. Samsung shipping the first sample is not the same as Samsung winning the first volume qualification — the exact distinction that cost it the Blackwell cycle. The honest scorecard reads: Samsung has clawed back onto the field, its recovery is real and reflected in the 2025 numbers, but it has not yet proven it can retake the technological lead it lost.

Myth versus reality

Two consensus narratives are worth puncturing here. The first myth is that Samsung was simply asleep and out-engineered — a lumbering incumbent beaten by a nimbler rival. The reality is more specific and more damning: Samsung made a deliberate resource-allocation choice to deprioritize HBM because it misjudged the size of the market, and it compounded that with a packaging-technology bet (TC-NCF) that scaled worse than SK Hynix's MR-MUF. This was not inattention; it was a wrong forecast executed competently. The distinction matters because forecasting errors are recoverable in a way that structural incompetence is not — and Samsung's rapid organizational response supports the "wrong bet, not broken company" reading.

The second myth runs the other way — the bullish claim, heard on Samsung's own earnings calls through 2025, that the company is now "fully back" in HBM. Here the numbers demand caution. Passing qualification on a prior-generation product (12-layer HBM3E) in late 2025, well after SK Hynix had banked the fattest margins of the cycle, is recovery, not restoration. Management's framing on recent calls has emphasized HBM4 momentum and sampling leadership; a skeptical listener notices that "sampling first" has been Samsung's talking point before, and that the metric that actually pays — locked-in volume allocation from Nvidia — still tilts to SK Hynix into 2026.15 The truthful middle position is that Samsung is a credible, improving number-two-or-three in AI memory, no longer at risk of irrelevance, but not yet the price-setter it was in commodity DRAM.

The company that once made rivals go bankrupt is now the challenger, and it is playing the same catch-up game in another arena entirely — the foundry.

VII. The Advanced Foundry Wars: GAA Node Struggles & The TSMC Moat

If memory was the crown Samsung lost and is fighting to regain, the foundry is the crown it has never worn — and has spent tens of billions of dollars, and a great deal of pride, trying to seize.

Vision 2030 and the moat it charged

The contract chip-manufacturing business — the "foundry," where you fabricate chips designed by other companies like Apple, Nvidia, and Qualcomm — is dominated by one firm to a degree that has no parallel in modern industry: TSMC, which manufactures the overwhelming majority of the world's most advanced logic chips. In 2019 Samsung declared "Vision 2030," a pledge to invest well over $100 billion to challenge TSMC's dominance in the leading-edge foundry.

Why is TSMC so hard to dislodge? Because a foundry's moat is trust plus yield. A fabless designer bets its entire product — hundreds of millions of dollars and a market window — on the foundry delivering working chips at high yield, on time. TSMC has earned that trust over decades of not fumbling. Switching to a cheaper, less-proven foundry is a career-ending risk for a chip designer if it goes wrong. That is a switching cost measured not in dollars but in fear.

The fork at 3nm

The most consequential decision in this war came at the 3-nanometer node, and it was a genuine architectural fork. Both companies needed a new transistor design, because the old "FinFET" structure was running out of room to shrink. TSMC played it safe: it stayed with proven FinFET for its 3nm generation and squeezed one more cycle out of a mature architecture. Samsung gambled: in 2022 it became the first company in the world to ship a 3nm chip using an entirely new transistor structure called Gate-All-Around (GAA), which it branded MBCFET.12

The analogy: imagine a garden hose with a single pinch valve to control water (FinFET). GAA wraps the control around the entire hose on all four sides (gate-all-around), giving far finer command of the flow — better performance, less leakage. It is genuinely superior architecture. Samsung's bet was that leapfrogging to it early would let it vault ahead of TSMC on performance and win marquee customers.

The yield nightmare

The bet backfired in the short run, and the reason is the most important word in chipmaking: yield. Being first to a hard new architecture means being first to all its unsolved problems. Samsung's early 3nm GAA yields — the percentage of usable chips per wafer — were reported to have languished well below 30%. At that yield, the economics are ruinous: you scrap more than two-thirds of what you make. Predictably, the customers who matter — Nvidia, Qualcomm, and even Samsung's own Exynos mobile-chip division — kept sending their flagship business to TSMC, whose boring, reliable FinFET 3nm simply worked. Samsung had the more advanced technology and still lost the customers, because in the foundry business reliability beats novelty every time.

The 2nm redemption — real optionality, still unproven

Here is where the story turns genuinely interesting, and where the bull case lives. There is a version of events in which Samsung's painful early GAA experience was not a debacle but tuition — expensive schooling in a technology the whole industry must eventually adopt. Because at 2nm, everyone has to move to GAA. TSMC's own transition to GAA at 2nm, underway in 2025–2026, is its first, and it is a difficult one. Samsung, having already bled through the learning curve, has a head start on the architecture that now becomes universal.

The data offer partial support. Samsung's 2nm GAA yields were reported climbing from the low ranges early in 2025 into a 55–60% band by late 2025, with reports of its second-generation SF2P process reaching a 70% milestone in early 2026.1219 To win back hyperscalers and custom-silicon designers, Samsung has reportedly been willing to undercut TSMC's advanced-node pricing by a meaningful margin — the classic challenger's wedge: if you can't beat them on trust yet, compete on price and prove yourself on a second-source basis.

But sobriety is warranted. A 55–70% yield, if accurate, is competitive but not yet clearly at parity with TSMC's mature output, and yield reports on unannounced processes are notoriously soft, often sourced from the supply chain rather than confirmed by the company. Samsung has been here before — leading on paper, trailing in the customer's purchase order. The foundry thesis is real optionality, not a realized advantage. It will be proven or falsified by one thing only: whether a marquee external customer commits a flagship, high-volume design to Samsung's 2nm line and it ships at good yield. Until then, the multi-billion-dollar foundry buildout remains simultaneously Samsung's most exciting call option and its largest write-down risk.

Why the second-source logic cuts both ways

There is a structural reason the foundry battle may never resolve as cleanly as the bull case hopes, and it is worth sitting with. The entire semiconductor industry has a vested interest in there being a credible alternative to TSMC — a single point of failure that concentrated in Taiwan makes every fabless designer and every government nervous. That collective anxiety is Samsung's biggest tailwind: customers want a second source to exist. But wanting a second source to exist is not the same as being willing to put your flagship product on it. A designer will happily route a low-margin, forgiving chip to Samsung to keep the option alive, while reserving the part that defines its product for the foundry it trusts. That dynamic can keep Samsung's foundry perpetually busy and perpetually second-tier — profitable enough to justify continued investment, never dominant enough to earn TSMC's margins. Intel's parallel struggle to build a competitive foundry with far deeper losses underscores how brutally hard the trust-plus-yield moat is to storm. Samsung's advantage over Intel is that it already runs high-volume leading-edge silicon for its own memory and mobile chips; its disadvantage against TSMC is that being second-best in a business defined by reliability is a structurally thin place to stand.

The blunt investor's summary: the foundry is where Samsung is spending the most and where the outcome is least knowable. Treat it as a binary that has not yet resolved.

Which brings us to the ledger — what all of this actually earns, and who is steering it.

VIII. Current Strategy: Segment Economics & Management Credibility

Strip away the drama and Samsung is, at bottom, four very different businesses stapled together under one ticker. Understanding the company as an investment means understanding that each has its own margin structure, its own cycle, and its own competitive reality. The 2024 segment figures — drawn from the company's own interim report — lay it out cleanly.4

The four engines

The Device eXperience (DX) division — phones, TVs, home appliances, networks — is the revenue colossus: KRW 174.89 trillion in 2024 revenue but only KRW 12.44 trillion in operating profit.4 That is the tell. DX is a high-volume, low-to-moderate-margin business. Its crown is the Mobile eXperience unit, which fights Apple at the premium end of smartphones, increasingly leaning on "Galaxy AI" features to justify high-end pricing and defend share. But a mid-single-digit operating margin is the honest signature of a hardware business with real competition and limited pricing power; DX keeps the lights on and the factories full, it does not mint the profits.

The Device Solutions (DS) semiconductor division is where the money is actually made — and lost. In 2024 it posted KRW 111.07 trillion in revenue and KRW 15.09 trillion in operating profit, more than the far-larger DX division.4 DS is the high-beta heart of Samsung: in a memory upcycle it can generate the majority of corporate profit, and in a downturn it can swing to outright losses (as memory did in 2023). Owning Samsung is, more than anything, owning the memory cycle with a foundry option attached.

Samsung Display (SDC) is the quiet high-margin gem: KRW 29.16 trillion revenue and KRW 3.73 trillion operating profit in 2024 — a mid-teens margin.4 Its power comes from a dominant, technologically entrenched position in premium small-panel OLED, most notably as the leading supplier of the OLED screens on Apple's iPhones. That Apple relationship is the definition of a high-switching-cost customer: designing a phone around a specific display supplier is not a decision changed lightly.

Harman, already dissected, rounds out the group as a stable KRW 14.27 trillion automotive cash cow.4

The analytical point is that these four do not rise and fall together. DX and SDC provide ballast; DS provides the beta. When commentators cheer or mourn "Samsung's earnings," they are almost always really talking about the memory cycle inside DS. In 2025, as memory prices surged and HBM sales scaled, DS drove group operating profit to KRW 43.6 trillion and quarterly profit to record highs, including an all-time-high quarterly operating profit of KRW 20.1 trillion in the December 2025 quarter — a vivid reminder of how much of the equity story rides on that one volatile segment.2

It also complicates the way outsiders should read a single year's results. A record 2025 is not evidence that Samsung has "fixed" anything structural; it is substantially evidence that the memory cycle turned, as it always eventually does, and that a company with Samsung's scale prints enormous profits when it does. The harder question — the one the cycle obscures — is whether Samsung is gaining or losing share of the profit pool within the upcycle. On that measure the 2023–2025 stretch is sobering: Samsung participated in the AI-memory boom, but SK Hynix captured a disproportionate slice of it. A rising tide that lifts a rival's boat faster than your own is not the vindication the headline profit number implies. This is the discipline the reader must impose on Samsung's own upbeat framing: separate the cyclical tailwind from the competitive scorecard.

There is a second-order diligence note worth flagging here. Samsung's capital intensity is extreme and lumpy — the KRW 53.6 trillion of 2024 capex, overwhelmingly in chips, is a bet placed years before the payoff is known.1 In memory and foundry, that spending is committed at the top of enthusiasm and harvested (or written down) much later, which means Samsung's balance sheet carries a permanent execution risk that a software business never faces. The company's fortress net-cash position cushions this, but "diworsification" — spreading capital across memory, foundry, phones, displays, appliances, and automotive — is precisely the complexity an activist would probe: is the conglomerate discount Samsung trades at partly self-inflicted by a portfolio too sprawling for any single management team to run at peak efficiency?

Who actually runs it — and for whom

Now the governance question, which for Samsung is inseparable from the investment case. Executive Chairman Jay Y. Lee controls this entire apparatus while holding less than 2% direct equity in Samsung Electronics. His control flows indirectly, through the post-merger Samsung C&T and through 삼성생명 Samsung Life Insurance, in the cross-shareholding chain the 2015 merger was designed to secure.

This is where an activist's eyebrow should rise. The controlling shareholder's personal financial incentive is not perfectly aligned with the minority's. The Lee family carries a multi-billion-dollar inheritance-tax liability — reportedly among the largest such bills in the country's history — and servicing it favors steady, predictable dividends flowing up the chain. A minority investor might prefer the company retain and reinvest cash, or return it through buybacks and cancellations that boost per-share value. When a controlling family needs dividend cash to pay a tax bill, there is a structural tension between what suits the family and what suits per-share value. That tension sits underneath every capital-allocation decision Samsung makes, and it is the crux of the value-up debate.

On operational credibility, the picture is more favorable but should be judged by behavior, not titles. DS chief Jun Young-hyun has earned genuine institutional credibility for the HBM recovery and quality stabilization — a case of a specific leader given a specific mandate who delivered measurable progress against it.10[^15] On the DX side, longtime executive 한종희 Han Jong-hee steered the consumer business toward ecosystem lock-in, connected home, and premium TV share, defending margins in a maturing smartphone market against both Apple at the top and aggressive Chinese vendors below. The broader management record cuts both ways: the HBM miss was a genuine, self-inflicted strategic error that the company was slow to acknowledge, and the mid-year firing of a division head was itself an admission of failure. But the response — urgent, structural, and so far effective — is the kind of concrete "when things go wrong, here is the specific plan" behavior that separates credible management from evasive management. The company named the problem, changed the person, and showed results within roughly a year and a half. That is a data point in management's favor, even as the underlying miss is a data point against.

The deeper credibility test, though, is consistency of narrative over time, and here Samsung's professional-management era earns a mixed grade. Through 2022 and 2023, management publicly downplayed the HBM gap even as the evidence mounted, before pivoting sharply to a "we are catching up fast" message in 2024–2025. Analysts on recent earnings calls have pressed precisely on this — asking, in effect, why they should trust the current optimism when the prior confidence proved misplaced. Management's answers have grown more concrete and engineering-specific under Jun, which is the right direction, but the episode is a reminder that Samsung's leadership, like any, narrates from a position of interest. The independent posture is to weight demonstrated milestones (a passed qualification, a shipped part, a booked contract) far more heavily than forward assurances, no matter how confidently delivered.

The question that remains is whether this professional, consensus-driven, family-controlled machine can do the one thing the market is now demanding of it: aggressively return capital. To frame that, we need the powers behind the business.

IX. Playbook: Hamilton Helmer's 7 Powers of Samsung

Strip the narrative down to its strategic skeleton and ask the question that matters for durability: what, exactly, protects Samsung's profits from competition? Hamilton Helmer's framework of durable "powers" is a useful scalpel here — not every power applies, and the honest exercise is naming which are real, which are broken, and which never existed.

Scale Economies — real, and the foundation. This is Samsung's bedrock power. Annual capital expenditure that has run north of $50 trillion won in peak years — KRW 53.6 trillion in 2024, with KRW 46.3 trillion in the chip division alone — buys a scale few can match.1 In DRAM and NAND, that scale translates into a lower cash cost per bit than most rivals, and in mobile OLED it underwrites a dominant panel position. Scale economies are what let Samsung wage the down-cycle warfare that built the memory oligopoly in the first place. This power is intact.

Process Power — historically the crown jewel, recently cracked. For two decades, Samsung's ability to transition nodes faster at higher yield — the golden copy — was a genuine process power that competitors could not replicate. The HBM defeat and the 3nm GAA yield debacle proved that this power is not automatic; it can be lost through misjudgment and organizational sprawl. It is currently being rebuilt under Jun Young-hyun's engineering-first regime, but "being rebuilt" is not "restored." An investor should treat Samsung's process power as impaired and on probation, not as a given.

Switching Costs — bifurcated. In commodity memory, switching costs are low by design: a DDR5 module from Samsung, Micron, or SK Hynix is largely interchangeable, and buyers multi-source deliberately. This is why commodity memory is a price-taking, cyclical business with no pricing power in a downturn. But at the high end the picture inverts. In advanced foundry and in custom HBM4 — where the customer co-designs the physical silicon and packaging with the supplier — switching costs become enormous, because you cannot casually move a co-engineered design to a rival. Samsung's strategic race is precisely to migrate its business from the low-switching-cost commodity zone into the high-switching-cost custom zone. That migration is the whole game.

Cornered Resource — the oligopoly itself. The tightest structural advantage in the entire Samsung story is not something Samsung owns but something it belongs to: a global DRAM market where three players control well over 90% of supply. That oligopoly, forged by the bankruptcies of Qimonda and Elpida and effectively protected by the astronomical capital and know-how required to enter, is the closest thing memory has to a cornered resource. It is why memory, for all its cyclicality, is far more profitable across a full cycle than its commodity nature would suggest. The risk to this power is not a new entrant — that is nearly impossible — but a demand collapse or a shift, like the early HBM phase, where one incumbent captures disproportionate share within the oligopoly.

Brand — real in phones, irrelevant in chips. Samsung does hold a genuine consumer brand, ranked among the most valuable in the world, which supports pricing at the premium end of Galaxy phones and TVs. But brand power is confined to the DX consumer businesses; it does nothing for a DRAM module or a foundry contract, where buyers are engineers running qualification tests, not shoppers responding to a logo. Since DS is where the profit swings live, Samsung's brand is a real but ring-fenced asset — worth noting, easy to over-weight.

Notably absent from Samsung's arsenal are the powers that define software and platform companies — there is little in the way of network economies or counter-positioning here. Samsung is, at its core, a capital-and-process business, and its powers are the powers of manufacturing at scale. The synthesis is this: Samsung's durable advantages (scale, the oligopoly) are strongest exactly where the profits are most cyclical and least differentiated, while the advantages it most needs for the AI era (process power, high-end switching costs) are the ones currently impaired or unproven. A company does not get re-rated for the powers it already had; it gets re-rated for the powers it can rebuild. That shapes everything about how Samsung can and cannot win from here — which is exactly what the final section stress-tests.

X. The Investment Spine: Bull vs. Bear & The Value-Up Stress Test

Every investment case has a spine — the one or two questions on which the whole thesis pivots. For Samsung, the spine has two vertebrae: can it convert its foundry and HBM optionality into realized, high-margin AI-chain share, and can its family-controlled governance finally reward shareholders the way Korea's regulators are now pushing every chaebol to do?

The value-up stress test

South Korea launched its 기업 밸류업 corporate value-up program to attack the Korea Discount head-on — pressuring companies to improve capital efficiency, boost shareholder returns, and cancel treasury shares rather than hoard them. The program is the government effectively conceding that decades of chaebol governance destroyed valuation, and asking companies to voluntarily fix it, with tax incentives as the carrot and mandated treasury-share cancellation floated as the stick.14

Samsung has, to its credit, begun to respond in ways that are more than rhetoric. In November 2024, with its stock depressed, it announced a KRW 10 trillion (roughly $7.2 billion) share buyback — the first tranche, about KRW 3 trillion, to be repurchased and cancelled outright rather than parked as treasury stock.13 In 2026 it moved to cancel further large blocks of treasury shares, with reports of roughly $11.6 billion in cancellations planned.18 Cancellation matters more than a buyback that sits idle: retiring shares permanently shrinks the count and lifts per-share value, and — not incidentally — reduces the taxable value of the family's holdings, one of the rare places where the family's tax interest and minority interest genuinely align.18

But the stress test is unresolved. The bear's rejoinder is that these programs are reactive, sized modestly against Samsung's cash generation, and could stall the moment the family's dividend-versus-cancellation calculus shifts. Whether value-up marks a permanent regime change in Samsung's capital allocation or a cyclical gesture at a low stock price is, as of mid-2026, genuinely not yet answerable. It is the single most important governance variable to watch.

The bull case

The bull case is a story of vertical capture. In it, Samsung does something no rival can structurally attempt: it integrates custom HBM4 memory with its own advanced 2nm GAA logic foundry, offering AI customers a single-vendor, co-designed memory-plus-logic package and capturing margin across the entire high-value AI chain rather than ceding the logic half to TSMC. Simultaneously, TSMC's pricing power peaks and its own GAA transition stumbles just enough that cost-conscious hyperscalers, desperate for a credible second source, qualify Samsung's 2nm line — validating the "GAA tuition" thesis. Underneath, SDC and Harman keep compounding on premium OLED and automotive cockpits. In this world, the process power is restored, the oligopoly holds, and Samsung re-rates as the market stops pricing it as a broken incumbent.

The strongest evidence for this case is that Samsung is the only company on Earth that owns world-class memory, leading-edge foundry, and premium displays under one roof — a genuinely unique integration, if it can be made to work.

The bear case

The bear case is a story of structural second place. SK Hynix's lead in advanced HBM packaging proves durable rather than temporary, and Samsung remains a lower-margin, catch-up supplier in the one memory product that matters most — always shipping the "first sample" but rarely winning the first volume qualification. The foundry never crosses the yield-and-trust threshold with a marquee external customer, turning the enormous capex into a chronic write-down drag rather than a growth engine. And governance stays frozen — legal overhangs give way to family-tax rigidity and chaebol consensus-paralysis, keeping capital returns suboptimal and the Korea Discount firmly in place. In this world, Samsung is a cyclical hardware conglomerate that periodically prints big memory profits and periodically gives them back, with no durable re-rating.

The strongest evidence for this case is the recent past: Samsung genuinely lost the opening, highest-margin phase of the AI memory boom to a smaller rival, and its foundry has yet to win a single flagship external design at the leading edge. Those are facts, not fears.

The activist stress test and the risk radar

Put on the hat of a skeptical long/short investor and the challenges write themselves. Capital allocation: Samsung sat on one of the world's largest corporate cash hoards for years while under-returning it, then began buybacks only after the stock had de-rated and regulators applied pressure — reactive, not disciplined. Portfolio complexity: six or more unrelated businesses under one roof invite a conglomerate discount that clean-focus rivals (SK Hynix in memory, TSMC in foundry) do not carry. Governance and related-party risk: control flows through an insurance affiliate and a merged trading company whose 2015 combination was litigated for a decade, and the controlling family's tax needs shape payout policy. Disclosure: Samsung reports at a segment altitude that lets a blockbuster memory quarter mask softness in phones or appliances. Accountability: the HBM miss went uncorrected for years before a leadership change forced the issue. None of these is fatal, but together they are the anatomy of the Korea Discount expressed at the company level.

On the risk radar, the material threats are specific rather than generic. Demand and technology risk are two sides of one coin: Samsung's fate is tethered to the AI capex cycle, and if hyperscaler spending on accelerators cools, the HBM and foundry theses deflate together. Buyer-concentration risk is acute — a handful of customers, Nvidia foremost, hold qualification power over the highest-margin products. Geopolitical exposure is real and rising: Samsung manufactures at enormous scale in South Korea and operates fabs in China and the United States, leaving it exposed to US-China export controls, tariff regimes, and the security politics of the semiconductor supply chain. And execution risk in the 2nm foundry ramp is the single largest self-controllable variable — the one place where Samsung's own hands, not the market's, will determine whether tens of billions of capex become an asset or an impairment.

Porter, briefly, and the KPIs that decide it

Through a Porter lens, the memory oligopoly means low threat of new entrants and manageable rivalry among three disciplined players — favorable. But buyer power is rising fast: when a handful of hyperscalers and Nvidia account for the bulk of AI-memory demand, those buyers can dictate qualification terms and play suppliers against each other, which is exactly how Samsung got locked out. Supplier power (chip equipment makers like ASML) is high but symmetric across all memory makers. The competitive squeeze, in other words, is coming from concentrated, powerful buyers — and Samsung's answer must be to make itself indispensable through co-design, the high-switching-cost path.

For an investor tracking this story, three KPIs cut through everything else. First, HBM4 validation timelines with Nvidia and AMD — the single cleanest proof of whether the process power is truly restored or merely narrated. Second, 2nm GAA production yield, with something like a sustained 70% at a named external customer as the threshold that converts foundry from option to asset. Third, the mix and pace of cash returned to shareholders — specifically dividend growth versus share cancellation rates — as the live readout on whether value-up is real. Watch those three, and the rest of the noise resolves into signal.

Samsung entered the AI era as the giant that got caught off guard. Whether the crucible of the last two years forged a sharper company or merely exposed a slower one is the question every number from here will answer.

References

-

Samsung Electronics Announces Fourth Quarter and FY 2024 Results — Samsung Global Newsroom, 2025-01-31 ↩↩↩↩

-

Samsung Electronics Announces Fourth Quarter and FY 2025 Results — Samsung Global Newsroom, 2026-01-29 ↩↩↩

-

Samsung Marks 40th Anniversary of 'Tokyo Declaration' — BusinessKorea, 2023-02 ↩↩↩↩

-

Samsung Electronics 2024 4Q Interim Report (segment revenue and operating profit) — Samsung Electronics IR ↩↩↩↩↩

-

Samsung's iconic Frankfurt declaration marks 30th anniversary — The Korea Herald, 2023-06-06 ↩↩

-

Shareholders approve Samsung C&T, Cheil merger despite pension fund opposition — Pensions & Investments, 2015-07-17 ↩↩↩

-

Investors approve fraught Samsung C&T-Cheil deal — CNBC, 2015-07-16 ↩

-

South Korea's top court acquits Samsung chief of fraud charges — UPI, 2025-07-17 ↩

-

Samsung Electronics to Acquire HARMAN, Accelerating Growth in Automotive and Connected Technologies — Samsung Global Newsroom, 2016-11-14 ↩↩

-

Samsung Electronics Names Young Hyun Jun as New Head of Device Solutions Division — Samsung Global Newsroom, 2024-05-21 ↩↩↩

-

SK hynix holds 62% of HBM, Micron overtakes Samsung, 2026 battle pivots to HBM4 — Astute Group, 2025 ↩

-

Samsung Reportedly Hits 55–60% 2nm Yields, Eyeing an Edge Through Early GAA Deployment — TrendForce, 2025-11-25 ↩↩

-

Samsung Electronics to Buy Back KRW 10 Trillion in Stock — Samsung Global Newsroom, 2024-11-15 ↩

-

Samsung Electronics to cancel W16tr in treasury shares — The Korea Herald, 2025 ↩

-

SK hynix Reportedly to Supply About Two-Thirds of NVIDIA HBM4; Samsung Targets Early Delivery — TrendForce, 2026-01-28 ↩↩

-

Samsung Ships Industry-First HBM4E Samples — TechTimes, 2026-05-30 ↩

-

Samsung Electronics appoints co-CEO in leadership shuffle focused on chip divisions — CNBC, 2024-11-27 ↩↩

-

Samsung Electronics to Cancel $11.6B in Treasury Stock in H1 — Seoul Economic Daily, 2026-03-10 ↩↩

-

Samsung Cracks the 2nm Code: 70% Yield Milestone for SF2P — FinancialContent, 2026-02-05 ↩

-

South Korean president to pardon Samsung leader Lee Jae-yong — PBS NewsHour, 2022-08-12 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube