Samsung Electronics: The Memory Chip Empire That Conquered Consumer Tech

I. Introduction & Episode Setup

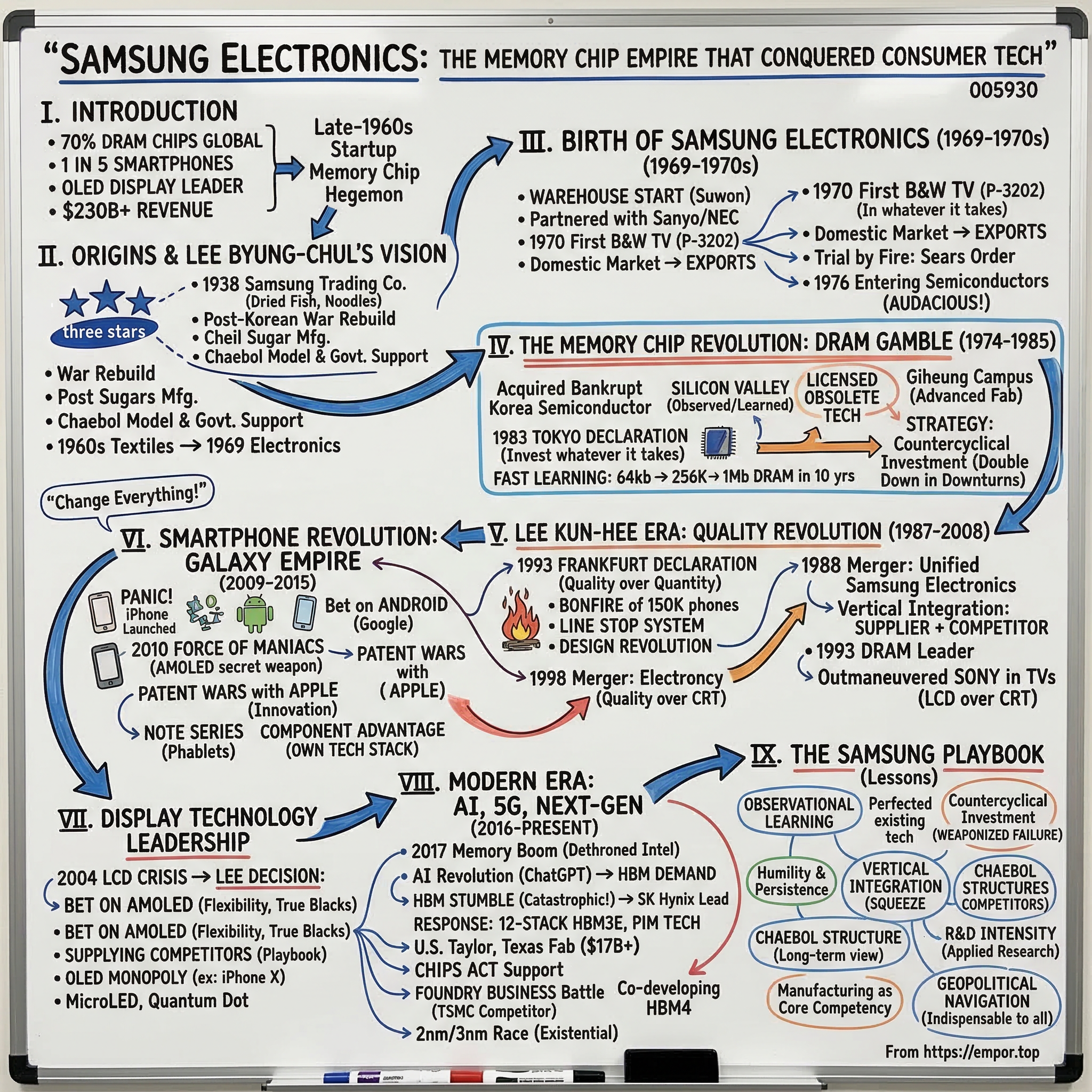

Picture this: A single company manufactures 70% of the world's DRAM memory chips, powers one in every five smartphones sold globally, and produces virtually every OLED display worth having. That company isn't American, Japanese, or Chinese—it's South Korean. Samsung Electronics, the crown jewel of the Samsung Group, generates more revenue than the entire GDP of countries like Morocco or Ecuador, clocking in at over $230 billion annually as the world's second-largest technology company by revenue.

How did a late-1960s electronics startup, born in a war-torn nation with virtually no technological infrastructure, become the memory chip hegemon that would humble Intel, outmaneuver Sony, and battle Apple for smartphone supremacy? The answer lies in a uniquely Korean blend of government-backed ambition, countercyclical investment strategy, and a willingness to bet the company on technologies that others deemed impossible.

This is the story of three transformations: from trading company to electronics manufacturer, from copycat to innovator, and from component supplier to consumer technology titan. It's about the Lee family's multi-generational vision, where a grocery trader's son would build black-and-white televisions, and his grandson would wage patent wars with Steve Jobs. Along the way, we'll discover how Samsung mastered the art of being both supplier and competitor—selling iPhone displays to Apple while simultaneously trying to destroy them in the smartphone market.

The Samsung playbook has become the blueprint for Asian tech companies looking to catch and surpass the West. It's a strategy built on massive capital expenditure during industry downturns, vertical integration that would make Andrew Carnegie jealous, and a manufacturing excellence that turned commodity chips into a strategic weapon. Today, as artificial intelligence drives unprecedented demand for high-bandwidth memory and advanced semiconductors, Samsung's decades-long bet on memory technology positions them at the center of the next computing revolution.

II. Samsung Group Origins & Lee Byung-chul's Vision

March 1, 1938. A 28-year-old named Lee Byung-chul stood in front of a modest storefront in Taegu, Korea, watching workers unload sacks of rice and dried fish. The sign above read "Samsung Sangwhoe"—Samsung Trading Company. The name meant "three stars," which Lee hoped would shine forever, bright and eternal. He had scraped together 30,000 won (about $2,000 in today's money) to start this grocery trading business, with dreams far bigger than the Japanese colonial authorities would have imagined.

Lee wasn't born into wealth, but his family owned enough land to afford him an education at Waseda University in Tokyo—though he never graduated, returning home with ideas about modern business practices but no degree. What he did possess was timing and an understanding of arbitrage. Korea's infrastructure was fragmented; goods abundant in one region were scarce in another. Lee's Samsung Trading Company would bridge these gaps, initially focusing on exporting dried fish, vegetables, and noodles to Manchuria and Beijing.

The business thrived until World War II and Korea's subsequent liberation created chaos. Lee, demonstrating a resilience that would define Samsung's DNA, relocated to Seoul in 1947 and rebuilt. But the real transformation came after the Korean War's devastation in 1953. President Syngman Rhee's government faced a nation where 80% of industrial facilities lay in ruins. The solution? Partner with ambitious entrepreneurs to rebuild the economy. Lee Byung-chul saw opportunity where others saw only rubble.

In 1953, Lee established Cheil Sugar Manufacturing, Korea's first sugar refinery—a masterstroke of timing. As American aid poured in and the economy began recovering, demand for processed foods skyrocketed. Sugar wasn't just a commodity; it represented modernization, Western influence, and economic progress. Within three years, Cheil Sugar dominated the domestic market, generating cash flows that would fund Lee's greater ambitions.

The chaebol model was taking shape—large, family-controlled conglomerates working hand-in-glove with government planners. It wasn't quite capitalism, wasn't quite state control, but something uniquely Korean. The government provided cheap loans, protected domestic markets, and guaranteed export credits. In return, chaebols like Samsung would industrialize the nation, create jobs, and earn foreign currency through exports. Critics called it crony capitalism; Lee called it nation-building.

By the 1960s, Samsung had expanded into textiles, opening Korea's largest woolen mill in 1954. Lee's strategy was clear: enter industries essential for economic development, achieve scale through government support, then use profits to fund the next expansion. He studied the Japanese zaibatsu model but added Korean characteristics—more family control, closer government ties, and an almost messianic belief in size and scope. "A company is a person," Lee would say, "and a person must grow to survive."

The textile business taught Samsung crucial lessons about manufacturing, quality control, and export markets. By 1969, Samsung was Korea's largest exporter of textiles, shipping to buyers from New York to Tokyo. But Lee Byung-chul, now 59, knew textiles were yesterday's business. The future belonged to electronics. Japan's post-war miracle had been built on transistor radios and televisions. Taiwan was emerging as an electronics assembler. Korea, Lee decided, would not be left behind. The three stars would shine in the electronic age.

III. Birth of Samsung Electronics (1969–1970s)

January 13, 1969. In a converted warehouse in Suwon, 45 workers gathered around makeshift assembly lines, their breath visible in the frigid air. Samsung Electric Industries had just been incorporated, and these employees—most with no electronics experience—would attempt something audacious: build televisions to compete with Japanese giants like Sony and Panasonic. The initial capital was a mere $250,000, the workforce inexperienced, and the technology nonexistent. Lee Byung-chul's electronics dream seemed destined for failure.

The public reaction was hostile. Samsung had built its reputation on trading, sugar, and textiles—solid, traditional businesses. Now Lee wanted to make electronics? Worse, he planned to do it by partnering with Japanese companies, the former colonizers who still evoked painful memories. When news leaked that Samsung was negotiating technology transfers with Sanyo and NEC, protesters gathered outside Samsung buildings. "Japanese collaborator!" they shouted. Lee, characteristically, was unmoved. "Emotion is luxury," he told his board. "Technology is survival."

The partnership with Sanyo proved transformative. Toshio Iue, Sanyo's founder, became an unlikely mentor to Lee Byung-chul. Where Lee was a novice in electronics, Iue was a veteran who had built Sanyo from nothing. He taught Lee the importance of yield rates in manufacturing, the complexity of supply chains for electronic components, and most importantly, the art of reverse engineering. "Copy exactly first," Iue advised, "improve later." It was advice Samsung would follow religiously for the next decade.

By 1970, Samsung Electronics had produced its first product: a 12-inch black-and-white television. The model, designated P-3202, rolled off the production line in May. It was crude by Japanese standards—the picture occasionally flickered, the sound crackled, and the plastic casing felt cheap. But it worked, and more importantly, it cost 30% less than imported Japanese sets. The domestic market, protected by high tariffs, had no choice but to buy Korean. Samsung sold 10,000 units in the first year.

The real ambition, however, was exports. Lee Byung-chul understood that Korea's domestic market of 30 million people could never support world-class scale. Samsung needed to sell internationally, which meant competing on quality, not just price. Throughout the early 1970s, Samsung engineers—many trained in Japan under technology transfer agreements—systematically improved their televisions. They studied Sony models down to the last capacitor, learned about signal processing from NEC, and gradually closed the quality gap.

The breakthrough came in 1974 when Samsung received its first major export order: 50,000 black-and-white televisions for Sears Roebuck in the United States. The TVs would be sold under the Sears brand—Samsung's name appeared nowhere—but Lee didn't care about recognition yet. He cared about scale, learning, and cash flow. The Sears order required Samsung to drastically expand production, improve quality control, and master international logistics. It was trial by fire, and Samsung emerged stronger.

By 1976, Samsung was producing color televisions, refrigerators, washing machines, and air conditioners. The company had grown from 45 to 3,000 employees. Revenue exceeded $100 million. But Lee Byung-chul, now 66, knew consumer electronics was just the beginning. At a management retreat in 1976, he shocked his executives with a new directive: Samsung would enter the semiconductor business. When someone pointed out that even established electronics companies like RCA and Fairchild were struggling with semiconductors, Lee responded with what became a famous quote: "If we don't do it now, we'll be assembling other people's products forever."

The electronics division had proven Samsung could master complex manufacturing. Now came the ultimate test: could a Korean company, with no semiconductor experience, challenge Silicon Valley and Japan in the most capital-intensive, technically demanding industry on earth? The answer would transform not just Samsung, but the entire global technology landscape.

IV. The Memory Chip Revolution: DRAM Gamble (1974–1985)

The Korea Semiconductor Company was dying. In December 1974, its American parent had abandoned the operation, leaving behind obsolete equipment and unpaid workers in a facility outside Seoul. The company specialized in transistors and simple integrated circuits—technology already a generation behind. Most saw a worthless heap of machinery and debt. Lee Byung-chul saw Samsung's future. He acquired the bankrupt operation for a fraction of its book value, renamed it Samsung Semiconductor, and began planning something audacious: Samsung would become a major player in memory chips.

The semiconductor industry in 1974 was dominated by American inventors and Japanese manufacturers. Intel had created the DRAM (Dynamic Random Access Memory) chip in 1971. Texas Instruments and Motorola led in logic chips. Meanwhile, Japanese companies like NEC and Toshiba were rapidly improving manufacturing yields. For Samsung—lacking experience, technology, or talent—entering this arena seemed suicidal. Industry analysts calculated that catching up would require at least $1 billion in investment and a decade of losses. Lee Byung-chul authorized the investment anyway.

Samsung's initial semiconductor operation was almost comically primitive. Engineers worked in a converted warehouse where temperature fluctuations ruined entire batches of chips. The clean rooms leaked. The yield rate—the percentage of functioning chips—was below 10%, compared to 50-60% at Japanese facilities. An American consultant visiting in 1975 wrote: "This is not a semiconductor facility. It's a very expensive way to make sand."

But Samsung had one advantage: the ability to learn faster than anyone expected. The company sent hundreds of engineers to Silicon Valley, paying them to work for free at American companies just to observe. They licensed obsolete technology from Micron Technology for DRAM and Sharp Corporation for SRAM, then reverse-engineered newer designs. They hired retired Japanese engineers who brought knowledge of manufacturing processes. It was industrial espionage conducted in broad daylight, all perfectly legal, driven by an almost desperate hunger to catch up.

February 1983 marked the turning point. At the Okura Hotel in Tokyo, Lee Byung-chul made what became known as the "Tokyo Declaration." Standing before assembled press, the 73-year-old patriarch announced: "Samsung will become a major DRAM vendor. We will invest whatever it takes. We will not retreat." The Japanese executives in attendance reportedly laughed. Samsung was still years behind in technology. Their newest chip was 16 kilobits while Japanese companies were shipping 64 kilobit DRAMs. How could they possibly catch up?

The answer was speed and capital. Within one year of the Tokyo Declaration, Samsung developed its own 64kb DRAM, reducing the technology gap from over a decade to approximately four years. The achievement stunned the industry. How had they moved so fast? The secret was Samsung's willingness to run multiple development teams in parallel, burning through cash to compress timelines. While Japanese companies ran sequential development—design, test, refine, produce—Samsung ran everything simultaneously, accepting massive waste in exchange for speed.

Seven months after announcing the 64K DRAM, Samsung achieved something even more remarkable: mass production of 256K DRAM began, leapfrogging several competitors. This wasn't just catching up anymore—this was joining the leaders. The memory chip industry operates on a brutal principle: each new generation (measured in increasing memory capacity) resets the competitive landscape. Miss one generation and you might never recover. Samsung had just proven it could play at the frontier.

The Giheung campus, constructed in 1984, embodied Samsung's semiconductor ambitions. Built at a cost of $1.5 billion—more than Samsung's entire revenue just five years earlier—it was the most advanced semiconductor facility outside Japan or the United States. The complex featured Class 10 clean rooms (no more than 10 particles per cubic foot of air), automated wafer handling systems, and redundant power supplies to prevent any interruption. Lee Byung-chul personally inspected the facility monthly, sometimes arriving at 3 AM to check on night shift operations.

The strategy that would make Samsung the world's largest memory manufacturer was taking shape: countercyclical investment. When memory prices collapsed in 1984-1985, sending several American manufacturers into bankruptcy, Samsung doubled down. While competitors cut capacity, Samsung expanded. While others reduced R&D, Samsung increased spending to 10% of revenue. The logic was simple but required nerves of steel: oversupply would eventually clear, demand would return, and Samsung would have the newest facilities and highest yields when it did.

By 1985, Samsung was shipping 1 megabit DRAMs, fully catching up with world leaders. The technology gap had been eliminated in less than ten years—not the decades experts predicted. The memory chip division was still losing money, but orders were growing exponentially. Major computer manufacturers like IBM and Compaq, initially skeptical of Korean semiconductors, were qualifying Samsung as a supplier. The three stars that Lee Byung-chul had named his company after were about to shine in silicon.

V. Lee Kun-hee Era: Quality Revolution & Global Ambitions (1987–2008)

November 19, 1987. Lee Byung-chul drew his last breath, leaving behind a business empire worth $20 billion and a succession plan that broke tradition. Instead of the eldest son, the chairmanship of Samsung Group passed to his third son, Lee Kun-hee, a quiet, contemplative man who had spent most of his career in the shadows. The Korean business community wondered: Could this soft-spoken introvert, known more for his love of movies and cars than business acumen, fill his father's enormous shoes?

Lee Kun-hee's first years seemed to confirm the doubters. He maintained his father's strategies, avoided major changes, and rarely appeared in public. Samsung continued growing through momentum alone—electronics revenue surpassed $10 billion in 1988 following the merger of Samsung Electronics and Samsung Semiconductor. But internally, Lee Kun-hee was observing, analyzing, and planning a revolution. He spent months visiting Samsung facilities incognito, sometimes posing as a customer. What he discovered horrified him.

In 1993, Lee Kun-hee summoned Samsung's top 200 executives to Frankfurt, Germany. For three days, he led them through electronics stores, showing them Samsung products gathering dust while Sony and Philips flew off shelves. At the Falkenstein Grand Kempinski Hotel, he delivered a now-legendary eight-hour speech. "Change everything except your wife and children," he declared. "Samsung makes second-rate products. We compete on price alone. This ends now." The Frankfurt Declaration, as it became known, marked Samsung's transformation from fast follower to innovation leader.

The quality revolution was brutal. Lee Kun-hee ordered a bonfire of 150,000 defective phones worth $50 million—employees watched their work burn. He introduced the "Line Stop" system: any worker could halt production if they spotted a defect, revolutionary in Korea's hierarchical culture. He hired Western designers, paying them multiples of Korean salaries, scandalizing traditional executives. In 1996, he declared the "Year of Design Revolution," insisting that Samsung products must be beautiful, not just functional.

But the real genius of Lee Kun-hee's era was recognizing that consumer products and components weren't separate businesses—they were a synergistic ecosystem. The 1988 merger creating unified Samsung Electronics wasn't just administrative; it was strategic. Memory chips developed for internal products could be sold externally. Display technology created for Samsung TVs could supply other manufacturers. This vertical integration would become Samsung's ultimate competitive weapon.

The memory business exploded under this strategy. In 1992, Samsung introduced SDRAM (Synchronous DRAM), becoming the first to commercialize this faster, more efficient memory standard. By 1993, Samsung had captured 13% of global DRAM market share. When memory prices crashed in 1996, Samsung again employed countercyclical investment, expanding capacity while competitors retreated. The Asian Financial Crisis of 1997-1998 provided another opportunity. As Korean competitors like LG Semicon faltered, Samsung acquired talent, facilities, and market share.

In 1998, Samsung made another leap, introducing both DDR SDRAM and GDDR SGRAM—specialized graphics memory. These weren't just incremental improvements but architectural changes that would define computing for the next decade. DDR (Double Data Rate) doubled memory bandwidth without increasing clock speed. GDDR enabled the 3D graphics revolution in gaming and eventually cryptocurrency mining. By controlling these standards early, Samsung locked in customer relationships that persist today.

Lee Kun-hee's 10-year plan to challenge Sony showed remarkable results by 2000. Samsung's televisions, once dismissed as cheap knockoffs, now competed directly with Sony Trinitrons. The company pioneered large-screen LCD TVs when Sony remained committed to CRTs. Samsung's design revolution paid off—products won international awards, and the brand shed its discount image. Revenue reached $100 billion in 2005, surpassing Sony's $66 billion.

The transformation's crown jewel was memory dominance. By 2010, Samsung controlled 35% of the global DRAM market, double its nearest competitor. The company had survived four major industry downturns by investing when others retreated. Each cycle eliminated competitors and increased Samsung's share. What started as Lee Byung-chul's impossible dream had become Lee Kun-hee's reality: Samsung was the undisputed memory king.

Yet Lee Kun-hee understood that hardware excellence wasn't enough for the digital age. In 2008, as Apple's iPhone redefined mobile computing, he recognized an inflection point. At a management meeting, he pointed to an iPhone and said, "Our enemies have changed. We must change faster." The smartphone wars were about to begin, and Samsung's component advantage would either be its greatest weapon or its Achilles heel.

VI. The Smartphone Revolution: Galaxy Empire (2009–2015)

June 2009. Inside Samsung's mobile division in Suwon, panic was setting in. The iPhone, launched two years earlier, had redefined what a phone could be. Nokia was stumbling. BlackBerry was vulnerable. Android had just emerged as a potential alternative to iOS. J.K. Shin, head of Samsung's mobile business, faced a career-defining decision: Should Samsung stick with its own Bada operating system, license Windows Mobile, or bet everything on Google's unproven Android platform? He chose Android, and with that decision, the Galaxy empire was born.

The first Samsung Galaxy, launched June 2009, was forgettable—a modest device that sold poorly. But Samsung learned fast. The company assembled a "task force of maniacs" (as one engineer described it) who worked 100-hour weeks dissecting the iPhone, analyzing Android's capabilities, and designing something that could compete. They had one massive advantage: Samsung made its own displays, memory, and processors. While other Android manufacturers waited for component suppliers, Samsung could prototype new features in weeks, not months.

March 2010. At CTIA Wireless in Las Vegas, Samsung unveiled the Galaxy S. The device featured a 4-inch Super AMOLED display—larger and more vibrant than the iPhone's 3.5-inch LCD. The screen was Samsung's secret weapon, manufactured in-house using organic LED technology that Samsung had been perfecting since 2007. Colors popped with an intensity that made the iPhone look washed out. The 5-megapixel camera, using Samsung's own image sensors, matched the iPhone 4's quality. Most importantly, it ran Android 2.1, offering customization and openness that iOS couldn't match.

The Galaxy S exceeded all expectations, selling over 20 million units globally. But success brought conflict. In April 2011, Apple sued Samsung for patent infringement, claiming the Galaxy S copied the iPhone's design. Steve Jobs was reportedly furious, telling his biographer Walter Isaacson: "I will spend my last dying breath if I need to... to destroy Android." The lawsuit was more than legal maneuvering—it was personal. Samsung supplied crucial components for the iPhone, including displays and memory. Now they were using that insider knowledge to compete.

Samsung's response was brilliantly cynical. While fighting Apple in court, they continued supplying iPhone components, generating billions in revenue that funded Galaxy development. They counter-sued Apple for wireless technology patents. They hired an army of designers to ensure future products looked nothing like iPhones while maintaining appeal. Most cleverly, they launched marketing campaigns that mocked Apple users as sheep waiting in lines, positioning Galaxy as the choice for independent thinkers.

The Galaxy S2, launched May 2011, proved Samsung could innovate, not just imitate. With a 4.3-inch display, dual-core processor, and just 8.5mm thickness, it was technically superior to the iPhone 4S in almost every dimension. It sold over 10 million units in the first five months. Samsung's TouchWiz interface, while criticized by purists, added features that iOS lacked: widgets, customizable home screens, and true multitasking. The message was clear: Galaxy phones did more.

By 2012, the student had become the master. The Galaxy S3, with its 4.8-inch display and intelligent features like Smart Stay (keeping the screen on while you're looking at it), outsold the iPhone in several quarters. Samsung became the world's largest smartphone manufacturer, a position it maintains today. The company was shipping over 200 million smartphones annually by 2013, capturing nearly 32% of global market share compared to Apple's 15%.

The component advantage proved decisive. Samsung's vertical integration meant they could introduce new technologies faster and cheaper than competitors. The Galaxy Note series, launched in 2011 with a then-enormous 5.3-inch screen, created the "phablet" category that Apple wouldn't enter until 2014. AMOLED displays gave Samsung devices superior battery life and outdoor visibility. The company's memory fabs meant Galaxy phones could offer more storage at lower costs.

The Apple lawsuits dragged on, generating headlines but little change. In 2012, a US jury awarded Apple $1 billion in damages, later reduced to $548 million. Samsung paid while earning billions supplying iPhone components. It was corporate warfare at its most sophisticated—fighting in court while profiting from your enemy's success. By 2015, Samsung was supplying the majority of iPhone OLED displays, the processor fabrication for Apple's A9 chip, and significant portions of iPhone memory.

The Galaxy empire peaked with the S6 and S6 Edge in 2015, featuring curved displays that no competitor could match because no competitor could manufacture them. Samsung had turned its component capabilities into a consumer moat. While other Android manufacturers competed on price, Samsung competed on features only they could deliver. The smartphone revolution had proven that owning the technology stack—from memory to display to processor—was the ultimate competitive advantage in consumer electronics.

VII. Display Technology Leadership & Vertical Integration

The year was 2004, and Samsung's display division faced an existential crisis. LCD panel prices had crashed 40% in twelve months. Chinese manufacturers were entering the market with government subsidies. Japanese competitors like Sharp and Sony were forming alliances. Inside Samsung's boardroom, executives debated whether to retreat from displays entirely. Lee Kun-hee ended the discussion with a characteristic decision: "We don't retreat. We dominate." Samsung would invest $21 billion in next-generation display technology over the next five years—the largest single technology bet in the company's history.

The display business exemplified Samsung's vertical integration philosophy. The company didn't just make screens; they controlled the entire value chain. Samsung produced the specialty glass, manufactured the liquid crystals, designed the driver chips, and assembled the final panels. When LED backlighting emerged, Samsung made those too. This integration provided cost advantages, but more importantly, it enabled innovation at the intersection of technologies. Samsung could optimize displays for their own memory chips, tune them for specific processors, and prototype new concepts without waiting for suppliers.

AMOLED (Active-Matrix Organic Light-Emitting Diode) became Samsung's display breakthrough. While competitors focused on improving LCD technology, Samsung bet on OLED's fundamental advantages: self-illuminating pixels that didn't need backlighting, true blacks from pixels that could turn completely off, and flexibility that would eventually enable foldable screens. The technology was fiendishly difficult to manufacture—early yields were below 30%, meaning 70% of panels were defective. Each failed batch cost millions. Several board members privately questioned whether OLED was "Lee Kun-hee's folly."

By 2007, Samsung had solved the yield problems through a combination of materials science and manufacturing precision. They developed new encapsulation techniques to prevent moisture damage, created more stable organic compounds, and designed equipment that could deposit materials with nanometer accuracy. The first Samsung AMOLED displays appeared in digital cameras and MP3 players—small screens where the technology's advantages were obvious but manufacturing volumes were forgiving.

The smartphone revolution transformed AMOLED from an interesting technology to a strategic weapon. As we saw in the Galaxy story, Super AMOLED displays became Samsung's key differentiator. But the real power came from Samsung's willingness to supply competitors while competing with them. By 2010, Samsung was selling AMOLED panels to Nokia, HTC, and Motorola—funding expansion through their competitors' purchases. It was the memory playbook applied to displays: achieve scale through external sales, use that scale to drive down costs, then leverage those costs in your own products.

The relationship with Apple epitomized this strategy's complexity. In 2010, Apple needed OLED displays for potential future iPhones but didn't trust Samsung completely. They invested in LG Display and Sharp, trying to create alternative suppliers. But Samsung's manufacturing lead was insurmountable. When Apple finally adopted OLED for the iPhone X in 2017, Samsung was the only supplier capable of meeting Apple's volume and quality requirements. The initial order was worth $9 billion—revenue that Samsung could theoretically use to compete with the iPhone.

Samsung's display dominance extended beyond mobile. In televisions, the company pioneered Quantum Dot technology, enhancing LCD displays with nanocrystals that produced more accurate colors. They developed MicroLED, positioning for a future beyond OLED. In 2021, Samsung controlled 41% of the global display panel market by revenue. More remarkably, they controlled over 90% of the mobile OLED market—a near monopoly in the most profitable segment.

The vertical integration model created compounding advantages. Samsung's display division could work with the memory division to optimize frame buffer requirements. They collaborated with the processor team to reduce power consumption. The TV division provided volume for new technologies before they were ready for mobile. This internal ecosystem meant Samsung could move from concept to mass production faster than any competitor. A display technology that might take LG or Sharp three years to commercialize, Samsung could deliver in eighteen months.

Critics argued this integration made Samsung too complex, too capital-intensive. The display business alone required annual investments exceeding $10 billion just to maintain competitiveness. But supporters pointed to the strategic value: Samsung could squeeze competitors from multiple angles. They could raise component prices to external customers while keeping costs low internally. They could prioritize their own products for new technologies. They could use component relationships to gather intelligence on competitors' plans.

By 2015, Samsung's vertical integration had created an almost unassailable position. The company was simultaneously the world's largest manufacturer of memory chips, displays, and smartphones. Each business reinforced the others in a virtuous cycle of scale, innovation, and profit. The model that Lee Byung-chul had imagined—controlling critical technologies rather than just assembling products—had reached its apotheosis. Samsung wasn't just participating in the electronics industry; in many ways, they were the electronics industry.

VIII. Modern Era: AI, 5G, and Next-Gen Tech (2016–Present)

The year 2016 marked an inflection point. Memory chip prices began their historic surge, driven by insatiable demand for data center capacity and smartphone storage. Samsung's semiconductor division posted revenues of $69.8 billion in 2017, compared to Intel's $62.7 billion, with operating profit of $7.21 billion in the second quarter alone. The student had officially surpassed the master. Samsung became the largest semiconductor company in the world from 2017 to 2018, briefly dethroning Intel, the decades-long champion.

The memory boom was unprecedented. DRAM prices rose 44% from 2016 to 2017, and NAND flash prices went up 17% year-over-year for the first time, with memory accounting for more than two-thirds of all semiconductor revenue growth in 2017. Samsung's countercyclical investment strategy—building capacity during downturns—had positioned them perfectly for this upswing. While competitors struggled to meet demand, Samsung had the newest fabs and highest yields. The memory market surged nearly $50 billion to reach $130 billion in 2017, with Samsung's memory revenue alone increasing nearly $20 billion.

But the modern era brought new challenges alongside triumphs. The artificial intelligence revolution, sparked by ChatGPT's launch in late 2022, created unprecedented demand for a specialized type of memory: High-Bandwidth Memory (HBM). HBM solves the bandwidth bottleneck by stacking memory chips vertically, creating an ultra-wide, multi-lane superhighway for data to travel between memory and AI accelerators like Nvidia's GPUs. This was supposed to be Samsung's moment—another memory transition where their manufacturing excellence would dominate.

Instead, Samsung stumbled catastrophically. While they focused on traditional DRAM and NAND, rival SK Hynix made an aggressive bet on HBM, partnering closely with Nvidia. SK Hynix now commands a dominant 57% of the HBM market, with Samsung falling to 27%, having focused resources on developing HBM3 and HBM3E specifically for Nvidia's wildly successful H100 and Blackwell AI accelerators. The consequences were devastating: Samsung's operating profit plummeted by 56%, with the company forced to take a one-time inventory writedown on unsold AI chips due to failure to get its latest 12-layer HBM3E chips certified by Nvidia.

Samsung's response demonstrated both determination and innovation. In February 2024, Samsung announced the development of the 36GB HBM3E 12H, the industry's first 12-stack HBM3E DRAM, using Through-Silicon Via technology to stack 12 layers of 24Gb DRAM chips. They also pioneered Processing-in-Memory (PIM) technology, integrating AI-dedicated semiconductors into HBM, allowing processors to be implemented right into DRAM, with potential for doubling GPU accelerator performance while reducing energy consumption.

The semiconductor landscape was also shifting geopolitically. Recognizing the strategic importance of domestic chip production, Samsung made its largest-ever U.S. investment. In November 2021, Samsung announced a $17 billion semiconductor facility in Taylor, Texas, with groundbreaking in the first half of 2022 and operations targeted for the second half of 2024, spanning more than 5 million square meters. The facility would boost production of semiconductor solutions for next-generation technologies in 5G, artificial intelligence, and high-performance computing.

The Texas investment evolved dramatically with government support. In December 2024, the U.S. Department of Commerce awarded Samsung up to $4.745 billion under the CHIPS Act, with Samsung expected to invest more than $37 billion in the region, supporting creation of over 15,000 jobs. This transformed Samsung's Texas presence into a comprehensive ecosystem for development and production of leading-edge logic chips, including two new fabs and R&D in Taylor, plus expansion of the existing Austin facility.

Beyond memory, Samsung pushed boundaries in chip manufacturing technology. The company had mastered the progression from 20nm to 10nm to 7nm nodes, each requiring exponentially greater precision and investment. By 2021, they were producing 5nm chips using Extreme Ultraviolet (EUV) lithography—technology so complex that only three companies worldwide could execute it. The race to sub-3nm manufacturing became existential, with each generation doubling transistor density and enabling new computing paradigms.

The foundry business—manufacturing chips designed by others—emerged as Samsung's next battlefield. While TSMC dominated with over 50% market share, Samsung invested aggressively to compete, offering integrated solutions that leveraged their memory and display capabilities. The Taylor fab secured major AI chip orders, with Groq contracting Samsung for 4-nanometer production and Canadian startup Tenstorrent partnering for chiplet manufacturing.

Looking forward, Samsung faces both unprecedented opportunities and existential challenges. The AI revolution demands more memory than ever before—not just quantity but specialized types like HBM for training large language models. Samsung is co-developing bufferless HBM4 chips with TSMC, the sixth-generation HBM that major makers plan to mass-produce as early as 2025. Success would restore Samsung's memory leadership; failure could permanently relegate them to second place.

The 5G rollout presents another massive opportunity. Every 5G base station requires 16 times more memory than 4G equivalents. Autonomous vehicles need high-reliability memory for real-time processing. Edge computing demands low-power, high-density solutions. Samsung's ability to provide integrated solutions—memory, processors, displays—positions them uniquely for these converging markets.

Yet challenges loom large. Chinese memory manufacturers, backed by unlimited government funding, threaten Samsung's pricing power. Geopolitical tensions force Samsung to navigate between U.S. technology restrictions and Chinese market access. The cyclical nature of memory—boom followed by bust—means Samsung must maintain massive R&D spending even during downturns. Most critically, the HBM failure exposed Samsung's vulnerability when technology transitions occur faster than expected.

The modern Samsung Electronics stands at a crossroads. They remain the world's largest memory manufacturer, but that crown sits uneasily. They've invested billions in next-generation fabs, but success depends on regaining Nvidia's trust for HBM certification. They're pushing toward 2nm manufacturing, but TSMC maintains a process lead. The company that Lee Byung-chul founded to trade groceries, that his son transformed into a technology giant, now faces its greatest test: Can Samsung adapt quickly enough to lead the AI revolution, or will they become another incumbent disrupted by the very changes they helped create?

IX. Playbook: Business & Technology Lessons

The Samsung playbook reads like a masterclass in industrial transformation, but with footnotes written in blood, sweat, and silicon. When business school professors discuss Samsung's strategy, they often focus on the successes—the market dominance, the vertical integration, the innovation. What they miss is that Samsung's real genius lies not in avoiding failure but in weaponizing it. Every setback became a setup for a larger victory, every crisis an opportunity to fundamentally restructure the competitive landscape.

The fast-follower-to-leader strategy defined Samsung's first four decades. The company never invented the television, the memory chip, or the smartphone. Instead, they perfected the art of observational learning—studying pioneers' mistakes, identifying inefficiencies, then entering markets with superior execution. When Sony spent billions developing Trinitron CRT technology, Samsung learned from their R&D, then leapfrogged directly to LCD. When Intel created DRAM, Samsung didn't try to out-innovate; they out-manufactured, driving costs so low that inventors couldn't compete with their own invention.

This approach required humility that most Western companies couldn't stomach. Samsung engineers worked for free at American semiconductor companies just to observe. They licensed obsolete technology, then reverse-engineered current generation products. They endured being called copycats, knowing that today's imitator could become tomorrow's innovator. The strategy worked because Samsung understood a fundamental truth: in technology, being first matters less than being best at scale.

The countercyclical investment philosophy transformed Samsung from participant to predator. While competitors followed traditional business cycles—investing during booms, retrenching during busts—Samsung did the opposite. The 1985 memory crash that bankrupted American manufacturers? Samsung doubled capacity. The 1997 Asian Financial Crisis? Samsung acquired talent and equipment at fire-sale prices. The 2008 global recession? Samsung invested $21 billion in displays while Sharp and Sony formed defensive alliances.

This strategy required extraordinary financial discipline and nerve. During the 2008 crisis, Samsung was burning $1 billion quarterly in their display division while simultaneously expanding capacity. Board members privately questioned whether Lee Kun-hee had lost his mind. But Samsung understood that downturns were when competitive positions shifted. Weak competitors exited, prices for equipment plummeted, and talented engineers became available. By the upturn, Samsung would have the newest facilities, best talent, and lowest costs—a combination that proved insurmountable.

Vertical integration became Samsung's ultimate moat, but it started as necessity, not strategy. In the 1970s, Korean component suppliers couldn't meet Samsung's quality requirements, so they made their own. No one would license current technology, so they developed it internally. What began as workarounds for isolation became competitive advantages. By 2010, Samsung didn't just assemble products; they controlled the entire stack from raw materials to retail.

Consider the Galaxy smartphone. Samsung manufactured the AMOLED display, the memory chips, the application processor, the image sensors, even the battery. When Apple needed to build an iPhone, they had to coordinate dozens of suppliers. Samsung had internal meetings. This integration provided cost advantages, but more importantly, it enabled innovation at the intersections. Samsung could optimize displays for their specific processors, tune memory controllers for their applications, design batteries that perfectly fit their industrial design.

The chaebol structure—family control, government partnership, cross-shareholdings—drew criticism from Western governance experts but proved remarkably effective for Samsung's needs. Family control enabled multi-decade planning horizons. When Lee Kun-hee decided to enter semiconductors, he could commit billions over decades without activist investors demanding quarterly returns. Government partnership provided patient capital and protected markets during the learning phase. Cross-shareholdings created internal ecosystems where divisions supported each other through downturns.

Yet the chaebol model also created vulnerabilities. Decision-making concentrated in the Lee family meant one bad leader could destroy decades of progress. Government partnership worked when interests aligned but became a liability when political winds shifted. The opacity of cross-shareholdings made true profitability difficult to assess. Samsung succeeded not because of the chaebol structure but in spite of its limitations, constantly adapting the model to changing circumstances.

R&D intensity separated Samsung from other fast followers. While Chinese manufacturers competed on labor costs, Samsung competed on technology. R&D spending consistently exceeded 6% of revenue, reaching above 8% during critical transitions. But Samsung's R&D philosophy differed from Western approaches. Instead of pure research seeking breakthrough innovations, Samsung focused on applied research—taking existing technologies and making them manufacturable at scale.

The development of 64-layer 3D NAND exemplified this approach. The concept wasn't Samsung's invention, but they solved the manufacturing challenges that others couldn't. They developed new deposition techniques, created proprietary etching processes, designed custom equipment. When competitors were struggling with 32-layer products, Samsung was shipping 64-layer at higher yields. Innovation through manufacturing excellence became Samsung's signature.

Manufacturing itself became a core competency that transcended products. Samsung's fabs achieved yield rates that seemed impossible—producing memory chips with 95% success rates when competitors managed 70%. They accomplished this through obsessive attention to detail: clean rooms with air 1000 times purer than hospital operating rooms, proprietary statistical process control systems, and workers trained like Swiss watchmakers. A Samsung fab technician once told me they tracked over 1,000 variables for each wafer. When you control that many variables, what looks like luck becomes probability.

The geopolitical navigation required skills no MBA program teaches. Samsung operated in a country technically still at war, dependent on American technology and security guarantees, while selling to Chinese customers who represented 40% of revenue. They manufactured in China while maintaining technology leadership that the U.S. wanted to protect. They competed with Japanese companies while depending on Japanese equipment. Every decision had diplomatic implications.

Samsung's solution was strategic ambiguity—being indispensable to all sides while fully controlled by none. They manufactured chips for the U.S. military while selling memory to Huawei. They accepted American CHIPS Act funding while expanding in China. They shared enough technology to maintain partnerships but kept critical knowledge in Korea. It was a high-wire act that required constant rebalancing.

The component supplier and competitor paradox reached its apex with Apple. Samsung sold Apple displays, memory, and processors worth billions annually while competing viciously in smartphones. During patent trials where the companies sought billions in damages, Samsung continued shipping components to Apple, and Apple continued buying. Both understood a profound truth: in modern technology, pure competition was impossible. Value chains were too intertwined, technologies too interdependent.

This paradox required organizational gymnastics. Samsung created information firewalls between divisions, with component sales teams forbidden from sharing Apple's plans with the mobile division. They priced components to Apple at market rates, avoiding the temptation to squeeze a competitor. The strategy worked because Samsung understood that component revenue was more stable and profitable than finished products. Let Apple take the market risk; Samsung would take the guaranteed margins.

Scale economics underpinned everything. Samsung's fabs cost $20 billion each, but once built, the marginal cost of chips approached zero. This created winner-take-all dynamics—the largest manufacturer had the lowest costs, could offer the best prices, won the most customers, funded the next generation of investment. Samsung understood this virtuous cycle and did everything to maintain it, including selling below cost to prevent competitors from achieving scale.

The playbook's lessons seem straightforward: invest countercyclically, integrate vertically, achieve scale, control critical technologies. But execution required capabilities most companies lack: patient capital measured in decades, willingness to absorb massive losses, ability to coordinate tens of thousands of engineers, nerve to bet the company repeatedly. Samsung's strategy wasn't hidden; it was just too difficult for others to copy.

Looking forward, the playbook faces its greatest test. The technologies Samsung must master—artificial intelligence, quantum computing, biotechnology—don't necessarily favor their manufacturing-centric approach. Software and algorithms matter more than scale. Innovation cycles measured in months, not years. Network effects, not production costs, determine winners. Samsung must evolve from a company that perfects hardware to one that creates ecosystems, from fast follower to first mover, from manufacturer to platform. Whether the playbook that built Samsung can transform it remains the billion-dollar question—or rather, the trillion-dollar one.

X. Analysis & Investment Case

From an investor's perspective, Samsung Electronics presents a fascinating paradox: a company that simultaneously embodies both the bull and bear case for technology investing in the 2020s. The numbers tell a story of dominance— Samsung led the semiconductor market in 2024 with a 10.6% share, controlling markets from memory to smartphones to displays. Yet beneath these headlines lurk fundamental questions about sustainability, technological disruption, and geopolitical risk that make Samsung perhaps the most complex large-cap technology investment available today.

Let's start with the market position, which remains formidable despite recent stumbles. In memory chips, Samsung maintains approximately 40% share in DRAM and 35% in NAND flash—markets worth a combined $160 billion annually. In smartphones, they've held the global crown since 2012, shipping over 250 million units annually. In displays, they control over 90% of mobile OLED production, essentially a monopoly in the highest-margin segment. This isn't just market share; it's market power, the ability to influence pricing, set standards, and extract economic rents that would make a 19th-century railroad baron envious.

The financial metrics reflect this dominance but also reveal vulnerabilities. Revenue exceeded $230 billion in recent years, placing Samsung among the world's largest technology companies. Operating margins in the semiconductor division can exceed 40% during upcycles—extraordinary for manufacturing. But these margins prove volatile, sometimes turning negative during downturns. Capital expenditure runs at $30-40 billion annually, a crushing burden that few companies could sustain. Return on invested capital varies wildly, from over 20% in boom years to single digits in busts.

The memory business exemplifies both Samsung's strength and weakness. During upcycles, it's a money-printing machine. When AI-driven demand exploded in 2017-2018, Samsung generated more profit from memory than most Fortune 500 companies' total revenue. But memory remains stubbornly cyclical. Supply/demand imbalances create price swings of 50% or more. Chinese competitors, backed by state funding, threaten to structurally oversupply markets. The HBM failure shows that even in memory, technological transitions can upset established hierarchies overnight.

The AI transition presents the starkest near-term challenge and opportunity. Samsung received delayed approval for 8-layer HBM3E from Nvidia for Chinese market processors, but remains behind SK Hynix and Micron in the AI arena, with executives warning of Q1 constraints on HBM sales. The miss isn't just about one product cycle; it's about positioning for a potentially decades-long AI infrastructure buildout. If Samsung can't crack the HBM market, they risk being relegated to commodity DRAM while competitors capture AI-driven superprofits.

Yet Samsung's response demonstrates resilience. Samsung plans to use cutting-edge 4-nanometer foundry process for HBM4 logic dies, seeking optimization from the design stage with their system LSI division to maximize performance. The vertical integration that enabled past successes could prove decisive again. Samsung remains the only company that can design, manufacture, and package all components of an AI system—a capability that becomes more valuable as systems grow more complex.

The foundry business represents another pivot point. Samsung invested billions trying to challenge TSMC's dominance in contract chip manufacturing. Results have been mixed—they've won some contracts but remain a distant second with roughly 15% market share versus TSMC's 55%. The Taylor facility and CHIPS Act funding provide new resources, but success requires more than capacity. Samsung must convince fabless designers to trust them with critical designs while Samsung simultaneously competes with those same customers in end markets.

Technology transitions beyond AI loom large. Quantum computing threatens to obsolete traditional semiconductors for certain applications. Silicon photonics could replace electronic interconnects. New memory technologies like MRAM or ReRAM might disrupt DRAM/NAND duopoly. Samsung invests in all these areas but lacks the focus of pure-play competitors. They must bet on everything while excelling at something—a difficult balance even for a company of Samsung's resources.

The China dependency creates unique risks. China represents approximately 40% of Samsung's revenue—their largest market for both components and finished products. Yet U.S. technology restrictions increasingly limit what Samsung can sell to Chinese customers. U.S. export restrictions on AI chips will likely weigh on first-quarter earnings. Samsung must navigate between losing Chinese revenue and losing American technology access—a balance that grows more precarious as tensions escalate.

Competition intensifies across all segments. In memory, SK Hynix proved more agile in HBM while Micron leverages U.S. government support. In foundry, TSMC's technology lead seems insurmountable while Intel's resurgence threatens from below. In smartphones, Chinese brands like Xiaomi and Oppo offer comparable features at lower prices. In displays, Chinese manufacturers backed by subsidies rapidly close the technology gap. Samsung faces competent competitors in every business, often with structural advantages Samsung lacks.

The succession question adds governance uncertainty. The Lee family's control enabled long-term thinking but also created vulnerabilities. Legal challenges to the family's ownership structure continue. The next generation of leadership lacks the founder's charisma or his son's strategic vision. Professional management might improve governance but could lose the entrepreneurial spirit that enabled bold bets like semiconductors. The transition from family to professional control—if it occurs—will be delicate.

Bear Case: The pessimist sees multiple threats converging. Memory enters a structural oversupply as Chinese capacity comes online. The HBM failure proves Samsung can't adapt quickly to technological discontinuities. Foundry remains subscale despite massive investments. Smartphones commoditize as innovation slows. U.S.-China tensions force Samsung to choose sides, losing either technology or markets. The company becomes the IBM of Asia—a former champion unable to navigate platform shifts.

Financial projections support concern. If memory margins normalize to historical averages, operating profit could fall 40%. Continued foundry losses drain resources from profitable divisions. Smartphone market saturation limits growth. The stock, trading at elevated multiples based on AI optimism, could face significant multiple compression. A realistic bear case sees 30-50% downside as reality replaces hope.

Bull Case: The optimist sees unparalleled positioning for the AI age. Samsung's HBM challenges prove temporary as their manufacturing excellence ultimately prevails. Customized HBM solutions across 20+ variants and partnerships with foundries for HBM4 demonstrate strategic adaptation. Memory demand from AI training, inference, and edge computing drives a supercycle lasting years, not quarters. The foundry business reaches critical scale, benefiting from customers' desire to diversify from TSMC. Vertical integration provides unique advantages in heterogeneous computing architectures.

The numbers support optimism too. AI could drive memory content per server up 10x over five years. Samsung's 40% share of a $500 billion memory market would generate $200 billion in high-margin revenue. Foundry could reach 25% share of a $200 billion market. Display technology leadership extends to AR/VR, automotive, and foldables. The company's generating $300+ billion revenue with 25% operating margins isn't fantasy—it's achievable if AI demand materializes as predicted.

The investment case ultimately depends on time horizon and risk tolerance. Short-term investors face a binary bet on HBM qualification and memory pricing. Long-term investors must weigh Samsung's structural advantages against technological and geopolitical uncertainties. The company trades at approximately 12x forward earnings—cheap for a technology leader but expensive for a cyclical manufacturer.

The sophisticated investor recognizes Samsung as a complex option on multiple technology trends. The memory business provides exposure to AI infrastructure buildout. The foundry offers leverage to semiconductor reshoring. The component businesses benefit from 5G, automotive electrification, and IoT proliferation. The portfolio approach—multiple bets across related technologies—reduces single-point-of-failure risk while limiting pure-play upside.

Risk management becomes crucial. Samsung's volatility exceeds most large-cap technology stocks. Revenue can swing 20% year-over-year. Operating margins range from negative to 40%+. The won's movement against major currencies adds another variable. Geopolitical events—a Taiwan crisis, technology embargo, trade war escalation—could devastate the investment case overnight. Position sizing must reflect these risks.

In conclusion, Samsung Electronics represents either exceptional value or a value trap, depending on your views on memory cycles, AI adoption, and geopolitical stability. The company possesses unique capabilities—vertical integration, manufacturing excellence, scale—that remain valuable regardless of technology trends. But these advantages must overcome significant challenges—technological disruption, fierce competition, political uncertainty—that threaten the business model.

For the fundamental investor, Samsung offers rare exposure to critical technology infrastructure at reasonable valuations. The memory oligopoly, display monopoly, and growing foundry presence provide multiple ways to win. Patient capital willing to endure volatility could be rewarded as AI demand materializes and geopolitical tensions stabilize. But this isn't a comfortable investment—it requires conviction that Samsung's playbook, refined over five decades, can adapt once more to a changing world.

XI. Epilogue & Recent Developments

The boardroom on the 42nd floor of Samsung's Seoul headquarters feels heavy with history. Portraits of Lee Byung-chul and Lee Kun-hee gaze down at the current leadership, their expressions inscrutable. What would the founders think of Samsung today—a company that generates more revenue than the entire Korean economy when they started, yet struggles with challenges they could never have imagined?

Lee Byung-chul, who began with dried fish and noodles, would marvel at the technological empire bearing his three-star logo. The man who begged Japanese companies for obsolete technology would be astounded that Samsung now decides which technologies reach market and which die in laboratories. But he might also recognize the current struggles. The HBM failure echoes his early semiconductor losses—painful but necessary learning. The geopolitical balancing recalls his navigation between Japanese colonizers and American occupiers. The fundamental challenge remains unchanged: How does a Korean company compete globally while remaining Korean?

Lee Kun-hee would likely be less surprised by today's challenges. His Frankfurt Declaration—"change everything"—anticipated a world where past success guarantees nothing. He understood that Samsung's greatest enemy wasn't competitors but complacency. The HBM stumble vindicated his paranoia about technological disruption. Yet he might question whether professional managers possess the entrepreneurial hunger that built Samsung. Can spreadsheet analysis replace the gut instinct that led to betting billions on unproven technologies?

The Lee family succession saga continues evolving. Lee Jae-yong (Jay Y. Lee), the heir apparent, faces a different challenge than his predecessors. He must lead not through absolute authority but through consensus, not by founder's prerogative but by professional competence. His legal troubles—conviction for bribery, pardons, ongoing investigations—weakened family control just as Samsung faces its greatest strategic challenges. The transition from family dynasty to professional management, inevitable but fraught, occurs against the backdrop of technological and geopolitical upheaval.

Corporate governance evolution accelerates under pressure. Independent directors now comprise the board majority. Compliance programs, once perfunctory, gained real teeth. Transparency improved, though Samsung remains opaque by Western standards. The company struggles to balance Korean corporate culture—hierarchical, consensual, relationship-based—with global investor demands for accountability. This cultural tension manifests in everything from R&D decisions to capital allocation.

The semiconductor industry's transformation continues accelerating. The race to 2nm, then 1nm, then whatever comes after silicon's physical limits, demands investments that strain even Samsung's resources. The company spent KRW 35 trillion ($24 billion) on R&D throughout 2024, yet still fell behind in critical areas. The industry's consolidation—through both mergers and technological barriers—creates an oligopoly where a single mistake can prove fatal. Samsung must run faster just to maintain position.

U.S.-China tensions reshape every strategic decision. The CHIPS Act funding comes with strings—restrictions on Chinese expansion, technology sharing limitations, effective alliance with U.S. interests. Yet China remains Samsung's largest market and manufacturing base. Every advanced chip Samsung produces potentially becomes a weapon in great power competition. The company that survived by being neutral increasingly must choose sides, with existential implications for either choice.

The automotive transformation presents both opportunity and challenge. Electric vehicles require 5x more semiconductor content than traditional cars. Autonomous driving demands advanced processors, specialized memory, sophisticated displays. Samsung supplies all these components but lacks the automotive expertise of traditional suppliers. They must learn new reliability standards, qualification processes, supply chain requirements. Success could open a $100+ billion market; failure could cede another industry to competitors.

Recent AI developments with DeepSeek raised fundamental questions about the semiconductor industry's assumptions. If AI models can achieve similar performance with 10x less computing power through better algorithms, what happens to demand for high-end chips? Samsung's massive investments assume ever-growing appetite for computational power. Efficiency improvements that reduce hardware requirements could devastate the business model. Yet Samsung has survived multiple technological disruptions by adapting faster than competitors.

SK Hynix shares dropped 9.9% on concerns that DeepSeek's low-cost AI would upend the premise of big spending on data centers and powerful chips. This volatility reflects deeper uncertainty about AI's trajectory. Will it follow the PC pattern—explosive growth, then commoditization? Or the internet model—continuous expansion over decades? Samsung's strategy assumes the latter, but the former could leave them with massive stranded investments.

Sustainability pressures add complexity. Semiconductor manufacturing consumes enormous resources—a single fab uses as much water as a small city, electricity as much as 100,000 homes. Governments demand cleaner production just as technological requirements grow more stringent. Samsung must innovate not just in chip design but in manufacturing processes, materials science, and waste management. Environmental compliance could become either competitive advantage or crushing burden.

The talent war intensifies globally. Samsung competes for the same engineers sought by TSMC, Intel, Apple, and countless startups. Korean demographics—aging population, declining births—limit domestic talent supply. The rigid corporate culture that enabled past success may repel the creative individuals needed for future innovation. Samsung experiments with Silicon Valley-style campuses and Western management practices, but cultural change comes slowly.

Looking ahead, Samsung faces three potential paths. The optimistic scenario sees them navigating current challenges as they have past ones—through superior execution, massive investment, and strategic patience. They regain HBM leadership, achieve foundry scale, and ride the AI wave to unprecedented prosperity. The company Lee Byung-chul founded for 30,000 won becomes the world's first trillion-dollar Asian technology company.

The pessimistic path leads to gradual decline. Unable to match TSMC's process leadership or overcome HBM failures, Samsung becomes a commodity producer in increasingly commoditized markets. Chinese competitors destroy memory profitability. The company fragments, selling divisions to focus on remaining strengths. The three stars dim to historical footnote, another former champion unable to maintain relevance.

The realistic path likely lies between extremes. Samsung muddles through—profitable but not dominant, innovative but not revolutionary, global but constrained by geography and geopolitics. They remain critical to technology infrastructure but never quite achieve the ambitions that drove the founders. Success becomes about optimization rather than transformation, efficiency rather than breakthrough, survival rather than conquest.

What would the founders make of these choices? Lee Byung-chul, the trader, might counsel pragmatism—take profits where available, avoid existential risks, preserve the enterprise for future generations. Lee Kun-hee, the revolutionary, would likely demand bolder action—bet everything on technological leadership, accept no compromise with mediocrity, change everything except core values.

Perhaps the answer lies in synthesizing both visions. Samsung succeeded by being simultaneously conservative and radical—conservative in financial management, radical in technological ambition. They were patient with investments but impatient with execution. They copied until they could create. This paradoxical approach—disciplined audacity—enabled a grocery trader's son to build semiconductors and his grandson to battle Silicon Valley.

The epilogue remains unwritten. Samsung stands at an inflection point where past strategies may not ensure future success. The playbook that built an empire needs revision for an age of artificial intelligence, quantum computing, and great power competition. Whether Samsung can transform once more—from manufacturer to innovator, from follower to leader, from national champion to global platform—will determine not just one company's fate but potentially the trajectory of Asian technology leadership.

The three stars that Lee Byung-chul named his company after still shine in Samsung's logo, but their meaning has evolved. Once representing eternal prosperity, they now symbolize the three transformations Samsung must navigate: from hardware to software, from products to platforms, from Korean company to global enterprise. Whether these stars will shine forever, as the founder hoped, or fade like so many corporate constellations before them, only time will reveal.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube