Samsung Electronics: The Vertical Integration Superpower

I. Introduction: The Everything Company

Picture this: you wake up in the morning, and before your feet even touch the floor, you have already interacted with Samsung three times. The alarm on your Galaxy phone went off — its OLED screen, manufactured by Samsung Display, lit up with notifications processed by a Samsung-designed chip, stored on Samsung-made NAND flash memory. You shuffle to the kitchen and open a Samsung refrigerator. You glance at the Samsung television in the living room.

On the drive to work, the infotainment system in your car — powered by Harman, a Samsung subsidiary — streams your morning podcast. At the office, the server handling your emails runs on Samsung DRAM. The solid-state drive in your laptop? Samsung. The screen on your colleague's iPhone? Also Samsung.

No other company on Earth touches human life at this many points. Samsung Electronics is not a consumer electronics company. It is not a semiconductor company. It is not a display company. It is all of these things simultaneously, and that is what makes it one of the most extraordinary corporate stories ever told.

As of the mid-2020s, Samsung Electronics generates annual revenues in the range of 250 to 300 trillion Korean won — roughly $190 to $230 billion — making it one of the largest technology companies on the planet by revenue. But raw revenue only hints at the real story. Samsung and its affiliated companies represent roughly 20 percent of South Korea's total GDP. One corporate group, one family's vision, accounts for a fifth of the economic output of the world's tenth-largest economy.

The thesis of this deep dive is simple but powerful: Samsung mastered "The Hard Way." While Silicon Valley celebrated asset-light software models and platform economics, Samsung chose the opposite path. It poured tens of billions of dollars every single year into the most capital-intensive, cyclical, and brutally competitive industries on the planet — DRAM memory, NAND flash, OLED displays, and semiconductor foundry services. The company's competitive advantage was not born from a brilliant algorithm or a viral app. It was forged in the furnace of multi-billion-dollar fabrication plants, relentless process engineering, and a willingness to invest through downturns when every rational actor was running for cover.

But here is the modern inflection point that makes Samsung's story urgent right now. For the first time in three decades, the "Fast Follower" playbook — watch what others invent, then manufacture it better and cheaper at massive scale — is being stress-tested by the AI revolution.

The explosion of generative AI created an overnight mega-demand for High Bandwidth Memory, or HBM, the specialized memory chips that power Nvidia's data center GPUs. And Samsung, the perennial memory champion, found itself in the unfamiliar position of playing catch-up to its smaller Korean rival, SK Hynix. The company that defined the memory industry for forty years stumbled at the most important technological inflection since the smartphone.

How Samsung responds to this challenge will determine whether it remains the undisputed king of technology hardware or cedes ground to hungrier, more focused competitors. That tension — between Samsung's extraordinary legacy and its uncertain AI future — is the thread running through everything that follows.

II. From Noodles to Semiconductors: The Strategic Foundation

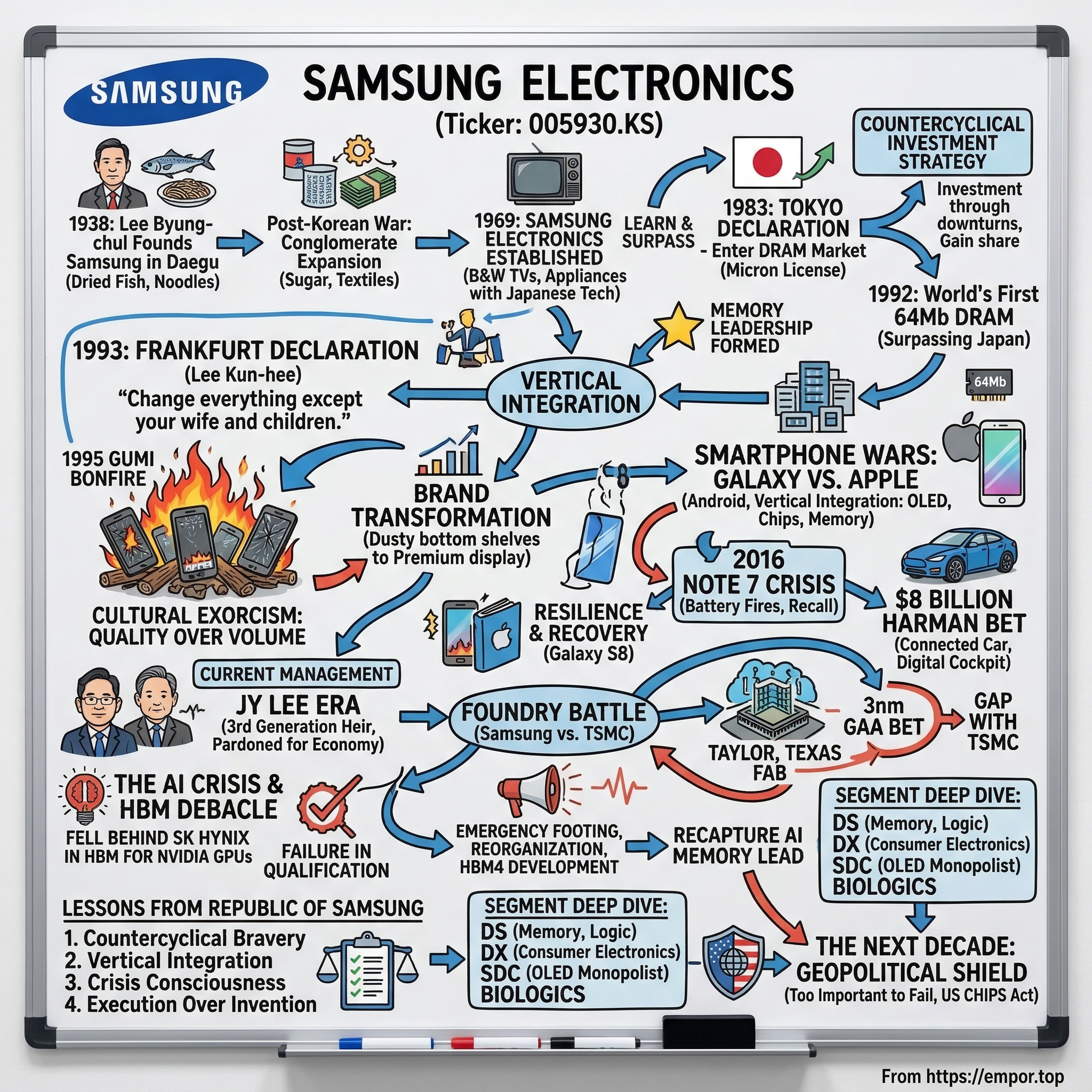

In March 1938, a 28-year-old man named Lee Byung-chul opened a small trading company in Daegu, a provincial city in southeastern Korea. The company's initial products were dried fish, vegetables, and noodles, exported to Manchuria and Beijing. He called it Samsung — "Three Stars" in Korean — a name meant to evoke something large, numerous, and eternal. The three stars represented his ambition for the business to be big, strong, and everlasting. It was, by any measure, a modest beginning.

Lee Byung-chul was the son of a wealthy landowner, educated in Japan at Waseda University, where he studied political science and economics. He returned to Korea with an understanding of Japanese industrial conglomerates — the zaibatsu — and a conviction that Korea's future lay in industrialization, not agriculture. Over the next two decades, Samsung evolved from a trading company into a conglomerate spanning sugar refining, textiles, insurance, and retail.

Lee Byung-chul watched Japan and the United States with the eye of a strategist, identifying which industries were ascending and positioning Samsung to enter them, always a step behind the technological frontier but with a determination to close the gap.

The pivotal shift came in 1969 when Samsung Electronics was formally established. South Korea was still a developing nation, its per capita GDP lower than many African countries at the time. President Park Chung-hee was pushing an aggressive export-led industrialization strategy, and Lee Byung-chul positioned Samsung to ride that wave.

The initial products were basic — black-and-white televisions assembled with Japanese technology, washing machines, and refrigerators. Samsung was essentially a Japanese knock-off operation, licensing technology from companies like Sanyo and NEC.

But every license agreement was treated as a classroom. Samsung engineers disassembled every component, studied every process, and slowly built indigenous capability. Korean engineers would travel to Japanese factories, take meticulous notes, and return home to replicate what they had learned — often sleeping on factory floors to maximize their time learning production techniques. The goal was never to remain a licensee forever. The goal was to learn and then surpass.

Then came the gamble that changed everything. In February 1983, Lee Byung-chul stood before a group of executives and engineers in Tokyo and made what became known as the "Tokyo Declaration." Samsung would enter the DRAM semiconductor market.

At the time, this was borderline insane. DRAM — Dynamic Random-Access Memory — was the domain of Japanese giants like NEC, Toshiba, Hitachi, and Fujitsu. Intel, the American inventor of DRAM, had recently been routed by the Japanese and was in the process of exiting the business entirely. And here was a Korean noodle-trader-turned-TV-assembler announcing he would compete against the most technologically advanced manufacturers in the world.

The skeptics were everywhere, including inside Samsung. DRAM fabrication required clean rooms thousands of times more sterile than a hospital operating theater, manufacturing tolerances measured in microns, and capital investments that could bankrupt the entire company if they failed. Samsung had zero experience in semiconductor manufacturing. Lee Byung-chul did not care.

He understood something that the market did not: DRAM was not just a product, it was a commodity with economies of scale so steep that the lowest-cost, highest-volume producer would eventually destroy everyone else. And Samsung intended to be that producer.

The company licensed 64K DRAM technology from Micron Technology in the United States — at the time a small startup itself — and began building its first fab in Giheung, south of Seoul. The pace was staggering. Engineers worked around the clock, sometimes in shifts of 18 hours or more, sleeping in dormitories adjacent to the construction site. Samsung went from licensing the 64K design to producing functional chips in roughly six months, a timeline that stunned the industry. The yields were terrible at first — far more chips came off the line dead than alive — but they were in the game. And in semiconductors, being in the game is the prerequisite for everything that follows.

And this is where the playbook that would define Samsung for the next four decades was born: countercyclical investment.

The semiconductor industry is violently cyclical. Demand booms, companies build capacity, supply floods the market, prices crash, and everyone cuts spending. The rational response during a downturn is to reduce capital expenditure and wait for recovery. Samsung did the exact opposite.

When DRAM prices collapsed in the mid-1980s, Samsung accelerated its investment. When Japanese and American competitors closed fabs and laid off engineers, Samsung opened new production lines and hired aggressively. The logic was cold and brilliant: by investing through the trough, Samsung would emerge from every downturn with more capacity, newer technology, and lower costs than competitors who had retrenched. When prices recovered, Samsung would capture disproportionate share of the upswing profits. Rinse and repeat, cycle after cycle, for decades.

By the late 1980s, Samsung had closed the technology gap to within a year of the Japanese leaders. The 1990s brought vindication. In 1992, Samsung developed the world's first 64-megabit DRAM chip, leapfrogging Japanese competitors for the first time. The timing was poetic — the Japanese semiconductor industry, once seemingly invincible, was entering a long structural decline driven by the burst of Japan's bubble economy and the rising costs of staying at the technological frontier.

The student had surpassed the masters. It took less than a decade from the Tokyo Declaration to technological leadership — a feat that shocked the global semiconductor industry and established a pattern of breathtaking catch-up that Samsung would attempt to repeat in displays, smartphones, and foundry services.

The deeper legacy of this era was cultural. The early semiconductor years at Samsung were marked by a near-paranoid fear of failure. Engineers worked in a pressure cooker environment where missing a technology node by even a few months could mean billions in lost revenue and existential threat to the company.

This "crisis consciousness" — the deeply ingrained belief that Samsung is always one bad cycle away from disaster — became the company's defining cultural trait. It is the reason Samsung's workforce operates with a military-like discipline that startles Western observers. It is the reason the company runs "emergency mode" drills even during boom years. And it is the reason that, even as Samsung grew into a revenue behemoth, its leadership never stopped behaving as if the company's survival was in question.

III. The Frankfurt Declaration and The Quality Fire

In early 1993, Lee Kun-hee — the third son of Lee Byung-chul, who had assumed the chairmanship after his father's death in 1987 — was on a world tour, visiting Samsung's overseas operations and retail partners. What he found disturbed him deeply.

In a Los Angeles electronics store, Samsung products were literally gathering dust on the bottom shelves, positioned as bargain-bin alternatives to Sony, Panasonic, and Philips. The brand carried no prestige, no aspiration. Samsung was seen globally as the cheap Korean option — functional but forgettable.

Lee Kun-hee was a complicated figure: reclusive, intense, a man who preferred small meetings to grand stages, and who was known to watch the same movie dozens of times to study its craft. He was obsessed with quality in all its forms — in cars, in watches, in film — and seeing Samsung's products treated as disposable commodities wounded him personally.

On June 7, 1993, at the Falkenstein Grand Kempinski Hotel in Frankfurt, Germany, Lee Kun-hee gathered approximately two hundred senior Samsung executives and delivered a speech that lasted three days. That is not a typo. Three days.

The speech, known afterward as the "Frankfurt Declaration" or the "New Management" initiative, was a blistering indictment of Samsung's culture. Lee Kun-hee told his executives that Samsung was a "second-rate" company producing "second-rate" products. He said the company had become complacent, addicted to volume over quality, and that unless it fundamentally transformed, it would be swept away by global competition within a decade.

His most famous line from the address became corporate legend: "Change everything except your wife and children."

This was not mere rhetoric. Lee Kun-hee was declaring war on the organizational culture that had built Samsung into a successful but unremarkable mass manufacturer. He demanded that every division, every factory, every product line undergo a complete quality revolution. Employees were ordered to start their workday two hours earlier — a change from the traditional 8:30 AM start to 7 AM — to signal that the old way of doing things was dead. The "7-4" system (arrive at 7, leave at 4) replaced the old schedule overnight across the entire company.

The most visceral demonstration of this new philosophy came in 1995 at the Gumi manufacturing complex in southeastern South Korea. Samsung had discovered that a batch of mobile phones and fax machines rolling off the production line had significant quality defects.

In most companies, the response would be a quiet recall, an internal quality review, some process adjustments. Lee Kun-hee ordered something different entirely.

He had approximately 150,000 defective devices — phones, fax machines, and other consumer products worth an estimated $50 million — piled into a massive heap in the factory yard. Then, in front of 2,000 Samsung employees, he set the pile on fire.

Workers wept as they watched months of their labor go up in flames. The message was not subtle. Lee Kun-hee was conducting a cultural exorcism, burning away the mentality that tolerated defects, that prioritized meeting production quotas over meeting quality standards. He wanted every Samsung employee to understand in their bones that shipping a defective product was no longer acceptable under any circumstances.

The Gumi bonfire became Samsung's foundational myth — its equivalent of Steve Jobs returning to Apple or Howard Schultz closing every Starbucks for retraining. It was the moment Samsung decided it would rather destroy value than ship mediocrity.

The transformation did not happen overnight, but its trajectory was unmistakable. In the late 1990s, Samsung began pouring money into industrial design, hiring hundreds of designers and sending them to study at art schools in London, Milan, and New York. The company established its own design centers in major cities worldwide. Products began winning awards. The brand started climbing.

Samsung televisions moved from the bottom shelf at Walmart to the premium shelf at Best Buy. Mobile phones went from anonymous slabs to objects of genuine design aspiration. By the early 2000s, Samsung's brand value — as measured by Interbrand's annual ranking — was on a steep upward curve, eventually surpassing Sony in 2005.

Think about that: the cheap Korean knock-off brand had overtaken the most iconic consumer electronics brand in history. Samsung had gone from dusty bottom shelves in Los Angeles to premium displays in every major electronics retailer on the planet. The Frankfurt Declaration had taken twelve years to fully manifest, but it remade Samsung from a volume manufacturer into a genuine premium brand.

The Frankfurt Declaration is the single most important strategic event in Samsung's history because it unlocked pricing power. Before 1993, Samsung competed primarily on cost — make it cheaper than the Japanese, win on price. After the quality revolution, Samsung could charge premium prices for premium products while still maintaining its cost advantages from manufacturing scale.

That combination — premium pricing and low-cost manufacturing — is the holy grail of industrial competition, and Samsung achieved it in multiple product categories simultaneously. The company was now ready for the battle that would define the next two decades.

IV. The Smartphone Wars: Galaxy vs. The World

In January 2007, Steve Jobs unveiled the iPhone, and the mobile phone industry as it existed was instantly rendered obsolete. Nokia, Motorola, BlackBerry, Sony Ericsson — all of them were caught flatfooted.

Samsung, however, was in a peculiar position. It was already one of the world's largest mobile phone manufacturers, selling hundreds of millions of handsets annually, mostly mid-range devices. But unlike Nokia, which was deeply invested in its own Symbian operating system, Samsung had no religious attachment to any particular software platform. The company was a hardware pragmatist, willing to adopt whatever operating system gave it the best path to market.

When Google launched Android in late 2008 as an open-source mobile operating system, Samsung saw its opportunity with unusual clarity. Rather than build its own OS from scratch — as it attempted half-heartedly with Bada and later Tizen — Samsung went all-in on Android.

The bet was strategic and asymmetric. Google needed a hardware champion to make Android credible against the iPhone. Samsung needed a software platform to power its hardware. The marriage was imperfect but extraordinarily productive — Google and Samsung would later clash over Samsung's attempts to customize Android with its own TouchWiz interface and app ecosystem, a tension that persists to this day. But in those early critical years, Samsung became the "Default" Android partner, the company that Google pointed to when it needed to show that Android could match the iPhone's hardware polish.

The Galaxy S series, launched in 2010, was Samsung's direct answer to the iPhone. But the secret weapon was not marketing, and it was not software. It was vertical integration — the accumulated infrastructure of decades of component manufacturing, all turned inward to serve Samsung's own products.

Consider what Samsung could do that no other Android manufacturer could: it made its own OLED displays, giving Galaxy phones the most vibrant, energy-efficient screens in the industry. It manufactured its own DRAM and NAND flash memory, guaranteeing supply and optimizing cost. It designed its own application processors through its Exynos line, giving it partial independence from Qualcomm. It even manufactured its own camera sensors and battery cells.

Every other Android manufacturer — HTC, LG, Motorola, Xiaomi — had to buy most of these components on the open market, often from Samsung itself. Samsung was competing against its own customers, and it had a structural cost advantage that was nearly impossible to replicate.

This vertical integration advantage manifested in a specific and measurable way: Samsung could launch new products faster, in greater volume, and at lower unit cost than any competitor. When a new generation of OLED technology became available, Samsung's phone division got first access because the display division was a sister operation. When memory prices spiked, Samsung's phone division was insulated because it sourced internally.

And then there was the Apple paradox — perhaps the most fascinating competitive dynamic in modern business history.

Samsung was simultaneously Apple's fiercest smartphone competitor and Apple's most critical component supplier. For years, Samsung manufactured the application processors inside iPhones, supplied OLED displays for iPhone screens, and provided NAND flash and DRAM for Apple's devices. Apple was, at various points, Samsung's single largest customer.

The "frenemy" relationship was extraordinary: Apple would sue Samsung for patent infringement — the legendary "thermonuclear war" that Steve Jobs declared — while simultaneously signing multi-billion-dollar supply contracts with Samsung's component divisions. The profits Samsung earned from selling components to Apple effectively subsidized Samsung's R&D to build better Galaxy phones to compete against Apple. It was a strategic loop that drove both companies to extraordinary heights.

The Galaxy series climbed relentlessly. The Galaxy S3 in 2012 was the first Android phone to genuinely threaten the iPhone's cultural dominance. The Galaxy Note series, with its oversized screen and stylus, created an entirely new category — the "phablet" — that Apple eventually copied with the iPhone 6 Plus. By the mid-2010s, Samsung was shipping over 300 million smartphones annually, commanding roughly 20 to 25 percent of the global smartphone market.

Then disaster struck. In August 2016, Samsung launched the Galaxy Note 7, and within weeks, reports began surfacing of devices catching fire. The culprit was a battery defect — Samsung had pushed for higher energy density in a thinner form factor, and the battery cells from two different suppliers both had manufacturing flaws that could cause short circuits.

Samsung initially issued a recall and offered replacement devices, but in a devastating twist, the replacements also caught fire. Airlines banned the Note 7 from flights entirely — flight attendants made announcements specifically naming the Samsung device. Memes flooded social media. News footage of smoking phones in airport terminals became a global spectacle.

Samsung ultimately recalled every single unit — approximately 2.5 million devices — and discontinued the product entirely, an almost unprecedented move for a flagship product from a major manufacturer. The financial cost was estimated at over $5 billion in direct expenses, with additional billions in market value evaporated. The reputational damage was incalculable.

But here is where the story gets interesting. Samsung's response to the Note 7 crisis became a case study in crisis management. The company launched an unprecedented investigation, hiring independent testing firms and publishing the full results publicly. It created an eight-point battery safety check that became the industry gold standard. And it did not shy away from the next product launch.

The Galaxy S8, released in April 2017, was widely praised as one of the best smartphones ever made — featuring a stunning "Infinity Display" edge-to-edge screen that set a new design standard. Within a year of the worst product failure in smartphone history, Samsung had fully recovered its market position.

The Note 7 crisis, paradoxically, proved the resilience of Samsung's brand and supply chain. Any other company might have been destroyed. Samsung barely blinked.

The smartphone division today is a study in the power and limitations of market share in a maturing industry. Samsung sells more smartphones than anyone, but the profit pool has increasingly concentrated at the top — where Apple captures the vast majority of industry profits — and the bottom — where Chinese manufacturers like Xiaomi and Oppo compete on razor-thin margins.

Samsung occupies the uncomfortable middle, selling premium flagships that compete with Apple and mid-range devices that compete with Chinese brands. The strategic question is whether the smartphone division's primary value is as a profit center or as a demand driver for Samsung's component empire — a captive customer that guarantees volume for the display, memory, and processor divisions.

V. M&A and Capital Deployment: The $8 Billion Harman Bet

Samsung Electronics has historically been one of the most disciplined — critics might say timid — acquirers among global technology giants. While Apple, Google, Microsoft, and Meta spent the 2010s on headline-grabbing acquisitions, Samsung largely sat on a massive cash pile that exceeded $100 billion at various points, preferring organic growth and internal R&D over transformative deals.

The cultural explanation is rooted in Samsung's DNA: the company trusts what it builds more than what it buys, and its success in semiconductors and displays was achieved through patient, grinding internal development rather than acquisition-driven shortcuts.

That restraint made the November 2016 announcement all the more striking. Samsung agreed to acquire Harman International Industries — the parent company of JBL, AKG, Harman Kardon, and Mark Levinson audio brands — for approximately $8 billion in cash. It was Samsung's largest acquisition ever, and it caught the market off guard.

Samsung, the memory chip and smartphone colossus, was buying an audio and automotive electronics company? The immediate reaction was skepticism. At roughly 12 times EBITDA, critics argued Samsung was overpaying for a mature business with limited synergies to Samsung's core operations.

But the strategic logic revealed itself over time. Samsung was not buying speakers. It was buying the cockpit of the future automobile.

Harman was — and remains — one of the world's largest automotive electronics suppliers, providing infotainment systems, connected car platforms, and digital cockpit solutions to virtually every major automaker. BMW, Mercedes-Benz, Toyota, and dozens of others relied on Harman's systems for navigation, audio, driver assistance interfaces, and over-the-air update capabilities.

Samsung's insight was prescient: the car of the future is essentially a smartphone on wheels. As vehicles become increasingly software-defined, the company that controls the cockpit electronics controls the relationship with the driver. Samsung was positioning itself to own the interior of the next generation of vehicles.

The deal closed in March 2017, and Harman was operated with significant autonomy — Samsung did not attempt to forcibly integrate it into its Korean corporate structure, a wise decision given the cultural differences. By the mid-2020s, Harman's automotive division had grown meaningfully, with its order backlog expanding as automakers accelerated the shift to digital cockpits and software-defined vehicles. The acquisition looked increasingly smart, though the full payoff remained a long-term play.

The broader question of Samsung's capital allocation is one that perennially frustrates outside investors. Samsung has historically returned relatively modest amounts of capital to shareholders compared to US technology peers. The company sits on enormous cash reserves and generates massive free cash flow — particularly during memory upcycles — yet its dividend yield and buyback activity have been conservative by global standards.

Part of this reflects the Korean corporate governance environment, where chaebol families have historically prioritized corporate stability and reinvestment over shareholder returns. Part of it reflects the genuine capital demands of Samsung's business: when you are building new memory fabs that cost $15 to $20 billion each, maintaining a large cash buffer is not mere conservatism, it is survival strategy.

Samsung did announce enhanced shareholder return programs in recent years, committing to return a significant portion of free cash flow to shareholders through dividends and buybacks. But the tension remains. Foreign investors, who hold a substantial portion of Samsung's outstanding shares, consistently push for more aggressive capital returns. The Lee family and Korean institutional investors tend to favor reinvestment.

This governance dynamic is a critical variable for any investor evaluating Samsung — the question of "who does Samsung serve?" does not have a simple answer.

For a company generating revenue north of $200 billion annually, the relative absence of large-scale M&A is itself a strategic statement. Samsung believes it can build most things better than it can buy them. The Harman deal was the exception that proved the rule — an acquisition of capability in an adjacent market where Samsung had no organic presence. Whether Samsung will need to make similar bets in AI infrastructure, cloud services, or software platforms remains one of the most important open questions about the company's future.

VI. Current Management: The JY Lee Era

The story of Samsung's current leadership is inseparable from the story of South Korea's relationship with its most powerful corporate dynasty. Lee Jae-yong — known internationally as "JY Lee" or "Jay Y. Lee" — is the only son of Lee Kun-hee and the third-generation heir to the Samsung empire. His path to the chairmanship was neither smooth nor guaranteed. It wound through some of the most dramatic corporate governance scandals in Asian business history.

JY Lee was groomed for leadership from an early age. He studied at Seoul National University, earned a master's degree at Keio University in Japan, and attended Harvard Business School, though he did not complete his doctorate there. He joined Samsung in the early 1990s and rose through various positions, gaining experience across the conglomerate's divisions.

But his ascension was complicated by the byzantine corporate structure through which the Lee family maintained control of Samsung — a web of circular shareholdings, cross-investments, and holding companies that even experienced Korea analysts struggle to diagram.

The critical — and controversial — event was the 2015 merger of Samsung C&T (the group's de facto holding company) with Cheil Industries (another Lee family-linked entity). The merger was widely seen as a restructuring designed to consolidate JY Lee's control over the Samsung empire. It was bitterly contested by Elliott Management, the American activist hedge fund, which argued the merger terms were unfair to Samsung C&T minority shareholders.

Samsung prevailed in the shareholder vote, but the fallout was explosive. The South Korean government's National Pension Service voted in favor of the merger under political pressure, and this decision became a central element of the corruption scandal that brought down President Park Geun-hye.

JY Lee was arrested in February 2017 on charges of bribery, embezzlement, and perjury — accused of making payments to entities connected to President Park in exchange for government support for the Samsung C&T merger. He was convicted, sentenced to prison, released on a suspended sentence, re-arrested, and ultimately pardoned by President Yoon Suk-yeol in August 2022.

The pardon was explicitly justified on economic grounds: the Korean government stated that JY Lee's leadership was essential for Samsung's competitiveness and, by extension, for the South Korean economy. The business community had lobbied hard for the decision, arguing that Samsung needed its chairman to negotiate major investments and partnerships — particularly the CHIPS Act commitments in the United States — that required top-level decision-making authority.

It was a remarkable acknowledgment that Samsung and South Korea are so deeply intertwined that the nation's economic interests required the company's leader to be free. No Western democracy would pardon a corporate executive on the grounds that their company was too important to the economy — but in South Korea, where Samsung's tentacles reach into nearly every sector, the calculus was different.

Since his pardon, JY Lee has formally assumed the role of Executive Chairman — a title his father held for decades. His management style differs meaningfully from his father's. Where Lee Kun-hee was the imperial chairman — a figure of almost mythological authority who ruled through fear, vision, and dramatic gestures — JY Lee is more reserved, more globally oriented, and more comfortable delegating to professional managers.

He has pushed Samsung toward a more decentralized structure with empowered divisional CEOs, while retaining the ability to make big strategic calls himself. His strategic priorities have centered on three areas: winning in semiconductor foundry services against TSMC, catching up in AI-related technologies including HBM, and expanding Samsung's presence in next-generation areas like biotechnology and automotive electronics.

The shareholding structure remains a source of both fascination and frustration for investors. The Lee family's direct stake in Samsung Electronics is relatively modest — in the low single digits of outstanding shares. Control is exercised through a cascade of cross-shareholdings: the family holds a significant stake in Samsung Life Insurance, which holds shares in Samsung Electronics, which holds stakes in other Samsung affiliates, creating a web of mutual ownership that amplifies the family's effective control far beyond its direct economic interest.

This structure is common among Korean chaebols but is viewed with suspicion by international corporate governance advocates who argue it allows the family to extract private benefits of control at the expense of minority shareholders.

The generational transition also created a massive inheritance tax bill. When Lee Kun-hee passed away in October 2020, the family faced an estimated 12 trillion won (roughly $10 billion) in inheritance taxes — one of the largest tax bills in history. The family has been paying this obligation over several years, partly through the sale of shares and partly through the donation of significant art collections and other assets to the Korean government.

This tax burden has had real implications for the family's shareholding percentage and, by extension, for the corporate governance dynamics of the entire Samsung group. Some analysts speculate that the inheritance tax pressure could eventually force a more fundamental restructuring of the Samsung group — potentially including a simplification of the cross-shareholding structure that has long been a source of governance concerns.

The management question boils down to execution risk and governance discount. JY Lee is widely regarded as competent but faces the challenge of leading through what may be the most disruptive technological transition since the smartphone — the AI revolution. The governance structure creates a persistent discount in Samsung's valuation relative to what it might trade at under a more transparent, Western-style ownership model. Whether that discount represents an opportunity or a trap depends on whether one believes the Lee family's interests are sufficiently aligned with minority shareholders — a question that Samsung's history answers with a complicated "mostly, but not always."

VII. Segment Deep Dive: The Four Pillars

To understand Samsung Electronics, you have to stop thinking of it as a single company and start thinking of it as four distinct businesses lashed together by shared ownership, shared technology infrastructure, and a shared culture of relentless execution. Each pillar operates at a scale that would make it a Fortune 500 company in its own right.

DS (Device Solutions): The Crown Jewel

The Device Solutions division — encompassing memory semiconductors (DRAM and NAND flash) and the Logic/Foundry business — is the engine room of Samsung Electronics. It is where the company's most enduring competitive advantages reside, where the deepest technical moats are built, and where the most dramatic profit swings occur.

Start with memory. Samsung has been the world's largest memory semiconductor manufacturer for over three decades. In DRAM, it holds roughly 40 percent of global market share in a consolidated oligopoly — Samsung, SK Hynix, and Micron collectively control over 95 percent of the world's DRAM supply. In NAND flash, the market is somewhat more fragmented, but Samsung remains the leader with approximately 30 to 35 percent share, competing against SK Hynix (and its Solidigm subsidiary), Kioxia, Western Digital, and Micron.

The economics of memory semiconductors are fascinating and brutal. Memory is a commodity — a Samsung DRAM chip is functionally interchangeable with an SK Hynix DRAM chip — which means pricing is set by supply and demand, not brand or differentiation.

This creates violent cyclicality: during shortages, memory prices spike and manufacturers earn extraordinary margins (Samsung's DS division has produced operating margins above 50 percent during peak upcycles). During oversupply, prices collapse and the entire industry can swing to losses. Samsung's countercyclical investment strategy — spending aggressively during downturns to gain share and push down the cost curve — has been the key to its dominance. Weaker competitors either exit or fall further behind, while Samsung emerges from each cycle stronger.

During an upcycle, the memory division can generate 60 to 70 percent of Samsung Electronics' total operating profit, despite representing a much smaller share of total revenue. During a downturn, it can drag the entire company into near-breakeven territory. This cyclicality is the single most important dynamic for investors to understand about Samsung.

The foundry business — manufacturing chips designed by other companies — is Samsung's strategic moonshot. Samsung is the world's second-largest foundry operator after TSMC, but the gap is enormous. TSMC commands over 60 percent of global foundry revenue; Samsung holds roughly 12 to 15 percent. Samsung's foundry ambitions are central to its long-term strategy, as the logic semiconductor market is growing faster than memory and carries more stable margins.

DX (Device eXperience): The Brand in Every Home

The Device eXperience division encompasses Samsung's consumer-facing businesses: mobile phones, tablets, wearables, televisions, monitors, and home appliances. This is the division that makes Samsung a household name, that puts the Samsung logo in billions of pockets and living rooms worldwide.

The mobile business remains the anchor, with Samsung consistently shipping more smartphones than any other manufacturer globally. But the profit dynamics of smartphones have shifted. Samsung generates healthy but not exceptional margins on its flagship Galaxy S and Galaxy Z (foldable) lines, while its mid-range A-series competes in an increasingly cutthroat segment against Chinese manufacturers.

The television business is another area of long-standing dominance — Samsung has been the world's number one TV brand by revenue for nearly two decades — but televisions are a mature, low-growth category.

What DX provides, beyond direct profit, is brand equity and ecosystem stickiness. Samsung has been building out its SmartThings platform to connect phones, TVs, appliances, wearables, and home automation devices into an integrated ecosystem — the Samsung equivalent of Apple's ecosystem lock-in. This strategy is still in its early innings compared to Apple, but the installed base of Samsung devices is so large that even modest success in ecosystem integration creates meaningful switching costs.

SDC (Samsung Display): The Hidden Monopolist

Samsung Display Corporation is technically a subsidiary of Samsung Electronics, but it operates with significant independence and deserves recognition as one of the most strategically important display companies in the world. Samsung Display dominates the global small-to-medium OLED market with a share that has exceeded 90 percent at various points.

If you are reading this on a high-end smartphone — whether it is a Galaxy S, an iPhone Pro, or a Google Pixel — you are very likely looking at a Samsung-manufactured OLED panel.

OLED — Organic Light-Emitting Diode — technology was Samsung's second great "brute force" technology bet after DRAM. Samsung poured billions into OLED manufacturing capacity starting in the late 2000s, years before the market demanded it.

When Apple finally adopted OLED for the iPhone X in 2017, Samsung was the only manufacturer with the capacity and yield rates to supply Apple's enormous volume requirements. This gave Samsung Display an effective monopoly on high-end mobile OLED panels that persisted for years, though Chinese display makers like BOE and CSOT have been gradually gaining share in lower-tier OLED products.

The display business is strategically critical for two reasons. First, it generates substantial revenue from external customers — Apple being the most important — providing a steady income stream. Second, it gives Samsung's own device divisions preferential access to the best display technology, perpetuating the vertical integration advantage in smartphones and other consumer products.

The Hidden Growth Engine: Samsung Biologics

While technically a separate listed entity and not a division of Samsung Electronics, Samsung Biologics deserves mention because it represents the Samsung model applied to an entirely new industry: biopharmaceutical contract manufacturing.

Samsung Biologics operates as a CMO (Contract Manufacturing Organization), building and operating massive biologic drug manufacturing facilities — essentially applying the semiconductor clean room expertise and capital-intensive scaling playbook to pharmaceutical production. Think of it as the TSMC model for medicine: invest heavily in manufacturing capacity, offer it to pharmaceutical companies that lack their own production capability, and earn stable contract revenues.

Samsung Biologics has grown explosively since its founding in 2011, becoming the world's largest biopharmaceutical CMO by capacity. The company's plants in Incheon, South Korea, boast combined capacity exceeding 600,000 liters — the largest in the world.

For Samsung group investors, Biologics represents optionality — a proof of concept that the Samsung playbook of capital-intensive, brute-force manufacturing excellence can be applied beyond electronics. If the model works in pharmaceuticals, where could it work next? Materials science? Energy storage? The implications extend well beyond one subsidiary's revenue line.

VIII. The Foundry Battle: Samsung vs. TSMC

In a brightly lit conference room in Hwaseong, South Korea, Samsung's semiconductor engineers face a whiteboard covered in yield curve charts and node transition timelines. On the other side of the Taiwan Strait, in Hsinchu, TSMC's engineers stare at similar charts. These two companies are locked in what may be the most consequential industrial competition of the twenty-first century: the race to manufacture the world's most advanced semiconductor chips.

To understand this battle, start with what a foundry does. A semiconductor foundry manufactures chips that other companies design. TSMC pioneered this "pure-play" model in 1987 — the insight was that many companies could design great chips but could not afford to build and operate the multi-billion-dollar fabrication plants needed to produce them. TSMC would be the factory for the fabless world. The model worked spectacularly. Today, TSMC manufactures chips for Apple, Nvidia, AMD, Qualcomm, Broadcom, and virtually every other major chip designer on earth.

Samsung entered the foundry business as an extension of its existing semiconductor manufacturing operations. The logic was straightforward: Samsung already had cutting-edge fabs for making its own Exynos processors and memory chips; why not sell excess capacity to outside customers? Over time, the foundry ambition grew from a side business into a strategic priority.

Samsung invested tens of billions of dollars in dedicated foundry capacity, including the massive $17 billion fab under construction in Taylor, Texas — part of Samsung's commitment to expand semiconductor manufacturing in the United States, supported by incentives from the US CHIPS Act.

The competition is centered on the most advanced manufacturing nodes — currently the 3-nanometer and sub-3-nanometer processes. A "nanometer" in this context refers to the transistor gate length, though at these scales the number is more of a marketing designation than a literal measurement. What matters is that smaller nodes enable more transistors per chip, which means more computing power in less space with lower energy consumption. For AI chips, which demand enormous computational density, leading-edge nodes are not optional — they are essential.

Samsung made a bold technological bet with its 3nm node: it was the first to deploy GAA (Gate-All-Around) transistor architecture in mass production, which Samsung brands as MBCFET (Multi-Bridge Channel FET).

GAA represents a fundamental shift in transistor design. In traditional FinFET transistors — the architecture used since the 14nm node — the gate wraps around three sides of the channel. Imagine holding a garden hose with your hand — your fingers cover three sides but leave a gap. In GAA, the gate wraps around all four sides completely, like sliding a ring over the hose, providing better electrostatic control. This translates to improved performance and power efficiency. Samsung began shipping 3nm GAA chips in 2022, ahead of TSMC, which continued with an advanced FinFET approach for its initial 3nm node.

But being first to announce and first to ship is not the same as winning. The foundry business is ultimately judged on three metrics: yield (what percentage of chips coming off the production line actually work), performance (how fast the chips run and how little power they consume), and trust (whether customers believe the foundry will deliver on time, in volume, and without compromising their intellectual property). On all three metrics, TSMC has maintained a significant lead.

Samsung's foundry yields have been a persistent challenge. Industry reports have consistently indicated that Samsung's leading-edge yields lag TSMC's by meaningful margins. Lower yields mean higher effective cost per working chip, which makes Samsung a less attractive option for cost-sensitive, high-volume customers.

Then there is the "neutrality" problem — perhaps Samsung's most fundamental structural disadvantage in the foundry market.

TSMC is a pure-play foundry. It does not design or sell its own chips. It does not compete with its customers. Samsung, by contrast, designs its own Exynos application processors, its own image sensors, and its own consumer electronics products.

When Qualcomm considers whether to manufacture its next Snapdragon processor at Samsung's foundry, it must weigh the risk that Samsung — which competes against Qualcomm in the mobile processor market — might gain insight into Qualcomm's designs. This conflict of interest is real and has cost Samsung foundry contracts. Apple, which once used Samsung as its primary processor manufacturer, shifted entirely to TSMC in part because of competitive concerns.

Samsung has attempted to address the neutrality issue by creating organizational firewalls between its foundry and product divisions. It physically separated foundry operations, created independent management structures, and invested heavily in information security protocols. These measures have helped, but the perception issue persists. TSMC's purity of focus — its singular commitment to being the world's best contract manufacturer, with no competing product interests — remains a powerful competitive advantage.

The Taylor, Texas fab represents Samsung's biggest geographic bet on the foundry business. Originally announced in 2021, the plant is designed to produce advanced-node chips and is a direct response to the global "chip war" — the geopolitical push by the United States to bring leading-edge semiconductor manufacturing back onshore. Samsung secured substantial incentives under the CHIPS Act, but the timeline has faced delays and cost overruns that have tested investor patience.

The foundry battle matters immensely for Samsung's long-term trajectory. Memory semiconductors will remain cyclical regardless of Samsung's dominance. Consumer electronics face margin pressure from Chinese competition. The foundry business, if Samsung can crack the code on yields and customer trust, offers something different: secular growth driven by the world's insatiable demand for more computing power.

But closing the gap with TSMC is perhaps the hardest strategic challenge Samsung has ever faced — harder even than catching the Japanese in DRAM in the 1980s, because TSMC is a focused, superbly managed competitor that has been refining its model for nearly four decades.

IX. Hamilton's 7 Powers and Porter's 5 Forces

Step back from the operational details and examine Samsung through the lens of competitive strategy. Hamilton Helmer's 7 Powers framework asks a simple question: what durable advantages does a business possess that competitors cannot easily replicate? For Samsung, the answer is layered and, in some cases, surprisingly fragile.

Scale Economies are Samsung's most obvious power. In memory semiconductors, Samsung's scale advantage is self-reinforcing. Its enormous production volume drives down unit costs, which generates profits that fund the next generation of capacity investment, which further increases scale. Annual capital expenditure regularly exceeds $40 billion — a sum that only a handful of companies on earth can match.

This spending level creates a barrier to entry that is essentially insurmountable for new competitors and slowly grinds down existing rivals who cannot keep pace. In display manufacturing, a similar scale dynamic prevails: Samsung's OLED capacity was built through years of cumulative investment that no competitor can replicate quickly.

Cornered Resource manifests in Samsung's manufacturing know-how — specifically, the accumulated yield engineering expertise in sub-5nm semiconductor manufacturing and OLED production. This knowledge is embedded in thousands of engineers, in proprietary process recipes, and in institutional learning that took decades to build. You cannot hire it away in bulk. You cannot license it.

However, this cornered resource is less dominant in foundry services, where TSMC's yield expertise is superior, and increasingly contested in memory, where SK Hynix demonstrated that Samsung's knowledge advantage is not absolute.

Switching Costs are an area where Samsung has been building but has not yet achieved the moat depth of competitors like Apple. The SmartThings ecosystem creates some switching friction for consumers who invest in multiple Samsung devices and home automation products. But honestly, Samsung's ecosystem lock-in pales compared to Apple's. Most Samsung phone users could switch to another Android manufacturer with minimal disruption.

Where switching costs are more meaningful is in Samsung's B2B relationships — semiconductor foundry customers who have invested months of design work optimizing for Samsung's process nodes face significant switching costs if they want to move to TSMC, and vice versa.

Process Power — the ability to do something with lower cost or higher quality through organizational improvements embedded deep in the company — is arguably Samsung's strongest long-term advantage. The relentless countercyclical investment discipline, the crisis consciousness culture, the Gumi bonfire mentality — these are not strategies that can be copied by reading a case study. They are deeply embedded organizational processes that produce consistent outputs across cycles and decades.

Counter-Positioning is where Samsung's story gets complicated. In the foundry business, Samsung is counter-positioned poorly relative to TSMC. Samsung's integrated model creates a structural conflict that TSMC's pure-play model does not face. In the smartphone market, Samsung's Android-based approach is counter-positioned against Apple's vertically integrated hardware-software model, but not in a way that clearly favors Samsung.

Now apply Porter's Five Forces to Samsung's competitive landscape.

Rivalry is intense on every front. In memory, SK Hynix and Micron are formidable competitors — SK Hynix in particular has demonstrated the ability to out-innovate Samsung in HBM. In smartphones, Apple dominates the profit pool while Chinese manufacturers squeeze Samsung from below. In foundry, TSMC is a near-monopolist at the leading edge. In displays, Chinese manufacturers backed by state subsidies are steadily gaining share.

Threat of New Entrants is low in Samsung's core businesses due to the enormous capital requirements — building a cutting-edge semiconductor fab costs $20 billion or more. But the threat of Chinese state-subsidized entry is real and growing. Chinese memory manufacturers like CXMT and YMTC have made meaningful progress in legacy and mid-range chips, and while they remain far behind Samsung at the leading edge, their trajectory and the scale of Chinese government support represent a long-term competitive threat.

Supplier Power is moderate. Samsung manufactures most of its own critical components, reducing dependency on external suppliers. However, the company relies on equipment manufacturers like ASML for the tools needed to build and operate its fabs. ASML has significant supplier power — it is the sole manufacturer of EUV lithography systems, and Samsung must compete with TSMC, Intel, and others for ASML's limited production output.

Buyer Power varies by segment. In memory, buyers have limited power because the market is an oligopoly — there are only three major DRAM suppliers. In consumer electronics, buyer power is high because consumers can easily switch between brands. In foundry, major customers like Qualcomm and Nvidia have significant bargaining power because TSMC offers a credible alternative.

Threat of Substitutes is generally low for Samsung's core products. There is no substitute for DRAM or NAND flash in computing. OLED faces competition from mini-LED, but OLED's advantages in contrast, flexibility, and thinness make it the preferred technology for premium devices. The most meaningful substitution threat may be architectural: if future AI chips move toward fundamentally different memory architectures that reduce reliance on traditional DRAM, Samsung's memory dominance could face long-term disruption.

X. The AI Crisis: Why Samsung Fell Behind in HBM

In the pantheon of Samsung's competitive challenges, nothing in recent memory stung quite like the HBM debacle. For a company that built its identity on being the undisputed king of memory semiconductors, losing the technology lead in the most important memory category of the AI era was not just a business setback — it was an existential narrative shock.

HBM — High Bandwidth Memory — is a specialized type of DRAM that stacks multiple memory dies vertically, connected by thousands of microscopic pathways called TSVs (Through-Silicon Vias), and packages them on an interposer alongside a processor die.

Think of it like building a multi-story apartment building instead of a sprawling suburban home — you get vastly more capacity and bandwidth in a much smaller footprint. HBM is the memory technology that enables modern AI accelerators to function. Nvidia's A100 and H100 GPUs, the workhorses of the generative AI revolution, require enormous amounts of HBM to feed their processing cores with data fast enough. Without HBM, large language models simply could not be trained or run at practical speeds.

SK Hynix saw the HBM opportunity earlier and moved faster. While Samsung was focused on maintaining its leadership in conventional DRAM — where it held the largest market share and the best cost position — SK Hynix placed a concentrated bet on HBM, investing heavily in advanced packaging technology and working closely with Nvidia to co-develop HBM solutions optimized for Nvidia's GPU architectures.

The payoff was spectacular. SK Hynix's HBM3 and subsequently HBM3E products became the preferred choice for Nvidia, which commanded the vast majority of the AI accelerator market. SK Hynix secured the lion's share of Nvidia's HBM orders, earning extraordinary margins on a product category that was growing exponentially.

Samsung's HBM products, by contrast, struggled with qualification. Reports in 2024 indicated that Samsung's HBM3E chips had difficulty passing Nvidia's stringent quality and thermal testing requirements.

The issue was not that Samsung lacked the underlying DRAM technology — it remained the world's largest and most technically capable DRAM manufacturer. The problem was in the advanced packaging — the precision stacking, bonding, and thermal management of multiple memory dies — where SK Hynix had invested more aggressively and built up superior process expertise. Samsung's "fast follower" approach, which had served it brilliantly for decades, was too slow for a market that was exploding in real time.

The financial implications were significant. HBM commanded dramatically higher prices per bit than conventional DRAM, and the market was growing at triple-digit percentage rates year-over-year. Every quarter that Samsung was underrepresented in HBM shipments to Nvidia represented billions of dollars in foregone revenue and profit.

Meanwhile, SK Hynix — historically the smaller, less profitable sibling in the Korean memory duopoly — saw its stock price and profitability surge, momentarily challenging Samsung's long-standing dominance of the memory industry's value chain.

Samsung's response was characteristically aggressive. The company reorganized its memory division leadership, reportedly placing its semiconductor business on "emergency footing" — invoking the crisis mode that is embedded in Samsung's corporate DNA. Engineering teams were surged to address the packaging yield issues. Samsung accelerated development of its next-generation HBM products and expanded its advanced packaging capacity.

The company also pursued diversification of its HBM customer base beyond Nvidia, seeking qualification with other AI chip developers and hyperscale cloud providers.

By late 2024 and into 2025, reports indicated that Samsung had made meaningful progress on HBM qualification, with some products reportedly passing Nvidia's tests. Samsung also began shipping its own branded HBM solutions and investing in next-generation HBM4 development. The race was far from over — SK Hynix retained a significant lead in market share and customer trust — but Samsung's history of catching up from behind gave the market some confidence that the company would eventually close the gap.

The deeper strategic lesson of the HBM episode is that Samsung's "fast follower" model may need to evolve. In markets where technology transitions happen gradually and predictably — like the progression from one DRAM node to the next — Samsung's approach of watching first movers, learning from their mistakes, and then executing at superior scale works brilliantly.

But the AI revolution created a discontinuity: demand for HBM exploded so rapidly that being even six to twelve months behind the technology leader meant missing the most lucrative window of the cycle. In an AI-driven future where the pace of hardware innovation is accelerating, Samsung may need to shift from "fast follower" to "first mover" in critical categories — a profound cultural shift for a company whose DNA is built on disciplined pursuit rather than speculative leaps.

The three KPIs that matter most for tracking Samsung going forward are: first, HBM market share — Samsung's portion of total HBM shipments to AI customers, which directly measures whether the company is closing the gap with SK Hynix in the highest-value memory category. Second, memory division operating margin, which captures both pricing power and yield efficiency and serves as the clearest signal of where the company sits in the memory cycle. Third, foundry customer win rate — specifically, new design wins from major fabless customers — which signals whether Samsung is making credible progress against TSMC in the logic semiconductor market.

XI. Playbook: Lessons from the Republic of Samsung

Distill eight decades of Samsung's history into strategic principles, and four lessons emerge that transcend the specifics of semiconductors and smartphones — lessons applicable to any capital-intensive, globally competitive industry.

Countercyclical Bravery: Invest When Others Are Afraid

This is Samsung's master principle, the strategic insight that built a dynasty. When DRAM prices crashed in the 1980s, Samsung built fabs. When the Asian financial crisis devastated the Korean economy in 1997-1998, Samsung accelerated its LCD investment. When the global financial crisis hit in 2008-2009, Samsung doubled down on OLED capacity. Each time, the calculus was the same: downturns are when competitors retrench, when equipment suppliers offer discounts, when the best engineers become available, and when the foundations of the next upcycle are laid.

Samsung understood that in capital-intensive industries, the companies that invest through the trough emerge from it with structural advantages that persist for years. This requires two things that most companies lack: the financial resources to sustain investment during periods of negative returns, and the institutional courage to bet billions on a recovery that has no guaranteed timeline.

Samsung had both — the cash reserves generated during upcycles provided the resources, and the Lee family's long-term ownership provided the courage to accept short-term pain for long-term dominance. When Samsung is spending aggressively during a downturn, that is typically a signal that the next upcycle will be disproportionately profitable for the company.

Vertical Integration Is the Ultimate Margin Protector

Samsung's ability to make its own screens, its own memory, its own processors, and its own packaging for its own devices creates a compounding cost advantage that pure assemblers cannot replicate. Vertical integration insulates Samsung from supply chain disruptions, guarantees access to the latest technology for its own products, and captures margin at every stage of the value chain.

When Apple buys an OLED screen from Samsung, Samsung earns a component margin. When Samsung puts that same screen in a Galaxy phone, it captures the full retail margin. This dual-capture model — selling components to competitors while using the same components in your own products — is an extraordinarily powerful economic engine.

The risk of vertical integration, of course, is complexity. Managing a semiconductor fab, a display factory, a smartphone assembly line, and a television manufacturing operation simultaneously requires organizational capabilities that most companies cannot sustain. Samsung manages it through a combination of Korean corporate culture, scale, and the connective tissue of shared manufacturing expertise that transfers across divisions.

Crisis Consciousness: Always Be in Danger

Even at the peak of its power — when Samsung was simultaneously the world's largest smartphone manufacturer, the world's largest memory company, and the world's largest OLED producer — the internal culture operated as though the company was on the verge of extinction. This is not neurosis; it is a deliberate management philosophy rooted in the memory industry's cyclicality and the trauma of Samsung's near-death experiences during the 1990s Asian financial crisis.

The practical manifestation is a company that never coasts. Samsung's R&D spending consistently ranks among the highest in the world — typically $20 billion or more annually. Its capital expenditure is relentless. Its organizational structure features regular "emergency mode" activations where divisions are restructured and leadership is shuffled to address competitive threats. The HBM challenge triggered exactly this kind of response: leadership changes, engineering surges, and accelerated investment — the corporate immune system activating at full force.

Execution Over Invention: You Don't Have to Be First, You Have to Be the First to Scale

Samsung did not invent DRAM. Intel did. Samsung did not invent OLED. Kodak did. Samsung did not invent the smartphone. Apple did. Samsung did not invent foldable displays. The concept existed in research labs for years.

But Samsung was the first to manufacture DRAM at global scale and the lowest cost. Samsung was the first to mass-produce OLED displays at billions of units. Samsung was the first to ship foldable phones in commercial volumes. The consistent pattern is not invention but industrialization — taking a technology that exists in the laboratory or in limited production and scaling it to planetary volume with reliable quality and declining costs.

This execution-over-invention philosophy reflects a deep understanding of where value is created in technology hardware. The idea is necessary but not sufficient. The prototype proves the concept but does not capture the market. The factory — the multi-billion-dollar, thousands-of-engineers, years-of-yield-optimization factory — is where the value is realized. Samsung's genius is the factory, and its strategic question for the next decade is whether factory genius is enough in an age when software, algorithms, and AI architectures are becoming the primary locus of value creation.

XII. Conclusion: The Next Decade and The Geopolitical Shield

Stand back and look at Samsung Electronics as it exists in early 2026, and the picture is one of immense power, meaningful vulnerability, and pivotal strategic choices.

The power is undeniable. Samsung remains one of the most diversified and vertically integrated technology companies ever built. Its memory semiconductor business generates cash flows that fund investment across every other division. Its display business supplies the screens for the world's most popular devices, including those of its competitors. Its consumer electronics brands have global recognition. Its manufacturing expertise — the accumulated knowledge of millions of production runs, billions of chips, and trillions of pixels — is a competitive asset that cannot be replicated in any short timeframe.

The vulnerability is equally real. The HBM miss exposed the limitations of the fast-follower model in a world where AI is compressing innovation cycles. The foundry business remains a distant second to TSMC, and closing that gap requires not just investment but a fundamental shift in how potential customers perceive Samsung's neutrality and reliability. The smartphone business faces relentless margin pressure from both ends of the market. And the governance structure — the chaebol ownership web, the family succession dynamics, the persistent governance discount — creates a valuation ceiling that may limit shareholder returns even as the underlying businesses perform.

The strategic choices ahead will define Samsung's next era. Can Samsung become a genuine foundry alternative to TSMC for the most advanced chips? Can it catch SK Hynix in HBM and recapture the memory technology lead at the moment when memory matters most? Will the company's investments in automotive electronics through Harman, biotechnology through Samsung Biologics, and next-generation computing bear fruit?

And then there is the geopolitical dimension — the most powerful tailwind Samsung has ever enjoyed. In a world where the United States and China are competing for semiconductor supremacy, where Taiwan's status creates existential risk for TSMC's operations, and where every major nation is desperate to secure domestic chip manufacturing capacity, Samsung occupies a unique position.

It is the only company other than TSMC capable of manufacturing leading-edge logic semiconductors. It is the largest memory manufacturer. It has fabs in South Korea, the United States, and other locations. For Western governments seeking to diversify semiconductor supply chains away from geographic concentration in Taiwan, Samsung is not just a company — it is a strategic asset.

This geopolitical reality creates a "too important to fail" dynamic that is unusual for a private company. The South Korean government's decision to pardon JY Lee on economic grounds made the implicit explicit: Samsung's health is a matter of national security. The US CHIPS Act incentives flowing to Samsung's Texas operations reflect a similar calculation by American policymakers. In a world of great-power competition, Samsung's factories are not just industrial assets — they are infrastructure of geopolitical significance.

The story of Samsung is ultimately the story of a nation that built a company to save itself, and a company that became indistinguishable from the nation. Lee Byung-chul started with dried fish and noodles in 1938. His son set 150,000 phones on fire to demand excellence. His grandson navigated prison, pardon, and the AI revolution. Through it all, the core Samsung formula — invest more than anyone else, manufacture better than anyone else, and never stop being afraid — has endured. Whether that formula is sufficient for the AI age is the question that will define Samsung's next chapter. The answer will matter not just for Samsung's shareholders, but for the global technology supply chain that depends on Samsung's continued excellence.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube