Hyundai Motor Company: The Quality Revolution and The EV Moonshot

I. Introduction: The "Third Largest" Hook

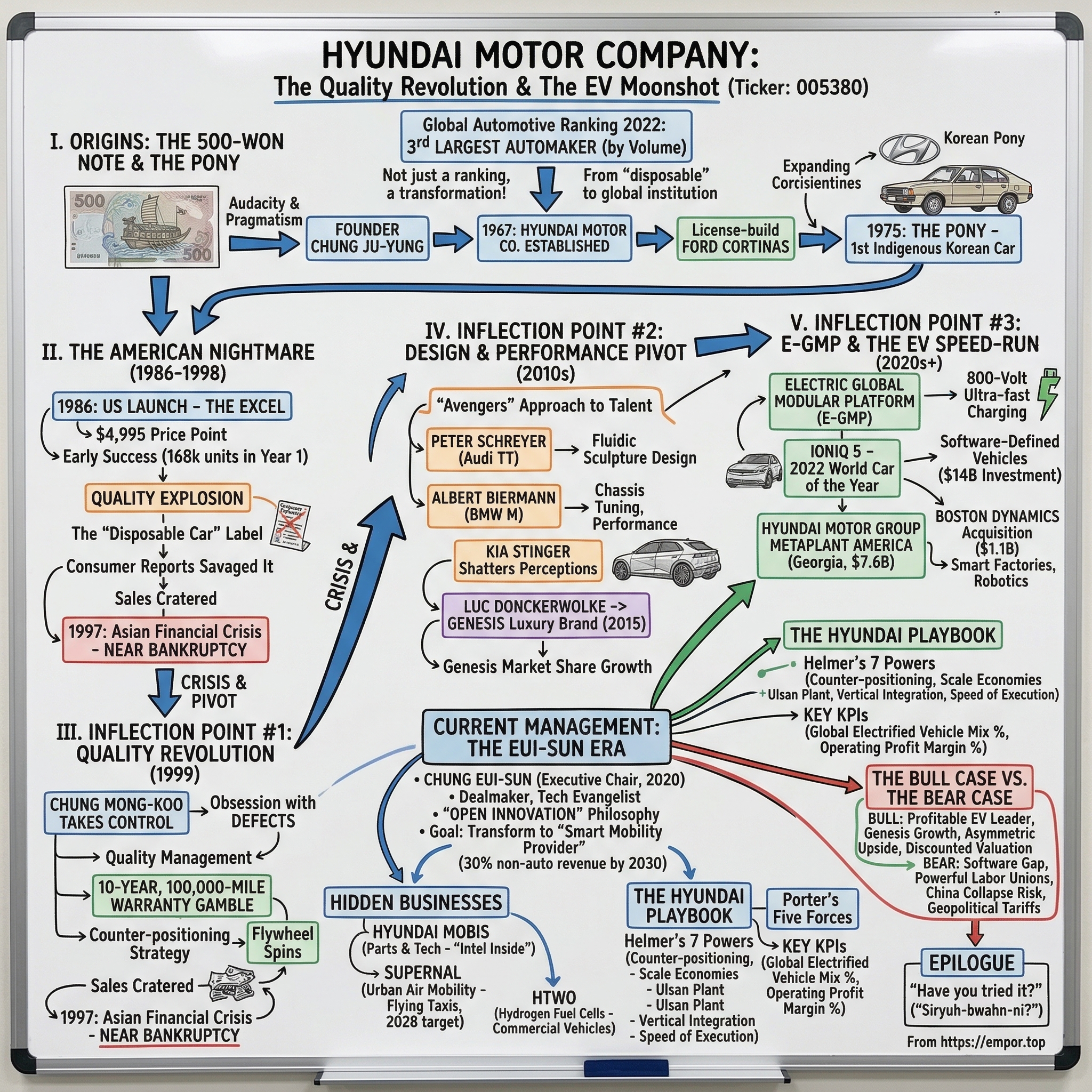

Somewhere around 2022, a number appeared in the global automotive rankings that made executives in Wolfsburg, Nagoya, and Detroit do a double-take. Hyundai Motor Group, the South Korean conglomerate encompassing Hyundai, Kia, and the luxury Genesis brand, had officially become the third-largest automaker in the world by volume. Trailing only Toyota and Volkswagen, this was no longer the plucky underdog story. This was a coronation.

But the real story is not the ranking itself. It is the sheer improbability of the journey. Hyundai Motor Company was, within living memory, the punchline of American late-night television. David Letterman cracked jokes about its cars. Consumer Reports treated them as barely worthy of review. The very name "Hyundai" was synonymous with "disposable." And yet, by 2025, the company posted record annual revenue of 186.3 trillion Korean won, roughly $128.4 billion, on global sales of 4.14 million vehicles. The stock, listed on the Korea Exchange under ticker 005380, traded at around 522,000 won per share in March 2026, giving the company a market capitalization of approximately 118 trillion won. That is the kind of transformation that deserves more than a footnote in automotive history. It deserves the full story.

The narrative arc here is not simply about making cars. It is about a "national champion" enterprise that survived near-bankruptcy, a catastrophic reputation crisis, a continental financial meltdown, and the wholesale disruption of its industry by electric vehicles and software. Along the way, it bought a robotics company famous for viral YouTube videos, launched a flying taxi division, bet billions on hydrogen fuel cells, and built the largest single automotive plant the world has ever seen. In South Korea, Hyundai commands roughly eighty percent of the domestic passenger vehicle market, a dominance so complete it borders on cultural infrastructure. The company is not just a carmaker. It is an institution.

The central question of this story is deceptively simple: How did a company that was building Ford Cortinas under license in the 1960s become the enterprise that Elon Musk recently acknowledged as "doing very well"? The answer involves a founder who showed up to a British bank with a banknote, a son who stopped assembly lines over door handles, a grandson who bought Boston Dynamics, and one of the most audacious warranty bets in the history of consumer marketing.

This is the Hyundai story.

II. The Origins: The 500-Won Note and The Pony

The story of Hyundai Motor Company cannot be understood without understanding its founder, and to understand its founder, you need to start with a banknote.

Chung Ju-yung was born in 1915 in what is now North Korea, the eldest son in a peasant farming family. He ran away from home multiple times as a teenager, eventually making his way to Seoul, where he worked as a day laborer, a rice delivery boy, and a construction hand. By the end of the Korean War, he had built Hyundai Engineering and Construction into one of the country's most formidable builders, winning contracts to rebuild a shattered nation. But Chung had a particular genius that transcended construction. He was a salesman of national identity.

The most famous illustration of this came when Chung traveled to London in the early 1970s to secure financing from Barclays Bank for a shipyard. Korea had never built a modern ocean-going vessel. Chung had no shipyard, no engineers with deepwater experience, and no orders. What he did have was a 500-won banknote. He pulled it from his pocket and showed the Barclays bankers the image printed on it: a geobukseon, a 16th-century Korean ironclad turtle ship, one of the most advanced naval vessels of its era. "You see," Chung reportedly told them, "Koreans have been building ships for centuries." He got the loan. And Hyundai Heavy Industries went on to become the largest shipbuilder on earth.

This story matters because it encapsulates the DNA that would later drive Hyundai Motor. It is audacity married to pragmatism, national pride weaponized as business strategy, and a willingness to leap before the net appears.

The pivot to automobiles came in 1967, when Chung established Hyundai Motor Company. Initially, the operation was straightforward: assemble Ford Cortinas under license for the Korean domestic market. But Chung quickly recognized that assembly was a dead end. If Hyundai did not own its own technology, it would forever be a vassal of foreign automakers. The goal became nothing less than building Korea's first indigenous automobile.

The result was the Hyundai Pony, launched in 1975. It was not, by any stretch, a purely Korean creation. Chung hired George Turnbull, a former managing director of British Leyland, to oversee engineering. The engine came from Mitsubishi. The styling was penned by Giorgetto Giugiaro at Italdesign, the legendary Italian studio. One observer called it "Lego-set engineering," snapping together the best available components from around the world. But what mattered was not the provenance of the parts. What mattered was that the Pony existed at all. It was the first mass-produced Korean car, and it sold well enough domestically and in export markets like Canada and the Middle East to prove that Korea could be more than a nation of shipbuilders and construction workers. The Pony was not a great car. But it was a proof of concept for something far more ambitious.

What makes the early Hyundai story so instructive for investors is the template it established. From the very beginning, the company operated on a principle of aggressive technology absorption followed by rapid indigenization. Hire the best foreign talent, license the best foreign technology, learn everything, and then do it yourself. This playbook would repeat itself, with increasing sophistication, for the next five decades.

III. The American Nightmare (1986-1998)

The Hyundai Excel arrived in the United States in 1986, and for a brief, dazzling moment, it looked like the most successful automotive import launch in American history. The numbers were staggering: 168,882 units sold in its first calendar year on sale, a record for any new import brand. The reason was brutally simple. The Excel started at $4,995. A Honda Civic cost $7,000. For first-time buyers, college students, and anyone on a tight budget, the Excel was an irresistible proposition. It was transportation, unadorned and unapologetic, at a price point that undercut everything else on the market.

Then the cars started breaking.

The Excel's quality problems became legendary. Engines failed prematurely. Transmissions shuddered and died. Interior trim pieces came loose in owners' hands. In the humid American South, dashboards warped and cracked. The car earned a grim nickname: "the disposable car." You drove it until it stopped, and then you bought something else. Consumer Reports savaged it. J.D. Power's initial quality surveys placed Hyundai at or near the bottom of every ranking.

The damage to the brand was catastrophic and compounding. Every broken Excel was a walking billboard for unreliability. Hyundai became the default punchline when anyone wanted to reference a bad car. David Letterman used it as shorthand for automotive failure. The stigma metastasized from the Excel to the entire brand. Even when Hyundai introduced improved models in the early 1990s, consumers simply did not believe the company was capable of building a decent car.

By the mid-1990s, annual U.S. sales had cratered to roughly 90,000 units, a fraction of the launch-year peak. Internally, the company was a mess. The chaebol structure that had served Hyundai well in its construction and shipbuilding days was ill-suited to the demands of modern automotive manufacturing. Decision-making was hierarchical to the point of paralysis. Quality control was treated as an afterthought, something that happened after production targets were met. And looming over everything was the structural fragility of the Korean economy itself.

When the Asian Financial Crisis struck in 1997, it nearly destroyed Hyundai along with the rest of Korea's corporate establishment. The won collapsed, credit markets froze, and chaebol after chaebol toppled into insolvency. Hyundai survived, but barely, and the crisis laid bare every weakness that had been papered over by years of breakneck growth. The company was selling fewer cars in America than it had a decade earlier, its reputation was in ruins, and the broader Hyundai Group was being forced into a painful restructuring that would eventually split the conglomerate into separate entities.

This was the nadir. Hyundai Motor at the end of the 1990s was a company that had bet big on America and lost, that had traded short-term volume for long-term brand destruction, and that was now facing an existential question: Could it survive, let alone compete, in the world's most demanding automotive markets? The answer would come from an unlikely source, the founder's son, armed with a stopwatch and an obsession with door handles.

IV. Inflection Point No. 1: The Quality Revolution and The Warranty Gamble

In 1999, Chung Mong-koo took control of Hyundai Motor Company. He was sixty years old, the second son of founder Chung Ju-yung, and he had spent most of his career running Hyundai's auto parts and service divisions. He was not a charismatic visionary in the mold of his father. He was an operations man, methodical, demanding, and possessed of an almost pathological intolerance for defects.

The stories from his first months in charge have become the stuff of Korean corporate legend. Chung Mong-koo would walk the factory floors at the Ulsan plant unannounced, running his hands along body panels, testing the fit of trim pieces, opening and closing doors to feel the weight and solidity of the mechanisms. If a door handle felt "off," if a panel gap was a millimeter too wide, he would stop the line. In the hierarchical culture of a Korean chaebol, where the chairman's word was absolute law, this was a seismic event. Assembly line workers and middle managers who had spent careers prioritizing volume over quality were suddenly being told that a single imperfect door handle mattered more than hitting the day's production target.

Chung institutionalized this obsession under the banner of "Quality Management." He restructured the company's engineering processes, hired quality consultants from around the world, and tied executive compensation to quality metrics rather than volume metrics. He personally reviewed J.D. Power survey data and demanded specific, measurable improvements on every deficiency identified. The message was unambiguous: Hyundai would either become a quality-first manufacturer, or it would die trying.

But quality improvements, no matter how real, mean nothing if consumers do not believe them. And in 1999, American consumers had absolutely no reason to believe that Hyundai had changed. The brand damage from the Excel era was too deep, too personal, and too reinforced by a decade of jokes and bad press. Hyundai needed a signal so dramatic, so costly, and so credible that it would force consumers to reconsider everything they thought they knew.

That signal was the 10-year, 100,000-mile powertrain warranty.

Launched in 1999, this was the longest and most comprehensive warranty in the mainstream automotive industry. It was not a marketing gimmick layered on top of fine print. It was a genuine promise: if your Hyundai's engine or transmission failed within ten years or a hundred thousand miles, the company would fix it for free. At a time when most competitors offered three-year, 36,000-mile bumper-to-bumper warranties, Hyundai was putting more than three times as much skin in the game.

The strategic brilliance of this move is best understood through Hamilton Helmer's "7 Powers" framework, specifically the concept of counter-positioning. The warranty worked because Hyundai's established competitors were structurally unable to respond. Toyota and Honda could not match a 10-year warranty without implicitly admitting that their customers might need one, which would undermine their carefully cultivated reputations for reliability. Moreover, matching the warranty would have exposed them to enormous potential liabilities across their much larger installed bases. Hyundai, with its small U.S. sales volume, was risking relatively little in absolute dollar terms. The incumbents, with millions of cars on the road, would have been risking billions.

The bet was binary. Either the quality improvements Chung Mong-koo was driving through the factories were real, in which case the warranty would cost relatively little to honor and would transform the brand. Or the improvements were not real, in which case the warranty claims would bankrupt the company. There was no middle ground.

The improvements were real. By 2004, Hyundai tied Honda for the top spot in J.D. Power's Initial Quality Study, a result so shocking that many in the industry assumed it was an anomaly. It was not. Hyundai's quality scores continued to climb throughout the 2000s, and warranty claim rates declined steadily. The "laughingstock" era was definitively over.

For investors, the warranty gamble illustrates a recurring pattern in the Hyundai story: the company's willingness to make asymmetric bets where the downside is survivable but the upside is transformational. The warranty did not just fix the brand. It gave Hyundai a structural advantage in consumer consideration that persisted for over a decade. When consumers cross-shopped a Hyundai against a Honda or Toyota in the 2000s, the warranty was the tiebreaker, a tangible, quantifiable reason to take the risk on the Korean brand. And once those consumers experienced the improved quality firsthand, they became repeat buyers. The flywheel had begun to spin.

V. Inflection Point No. 2: The Design and Performance Pivot (2010s)

By 2010, Hyundai had solved its quality problem. J.D. Power rankings confirmed it. Consumer Reports acknowledged it. Warranty claims data proved it. But the company's leadership recognized a deeper challenge: "reliable" was not the same as "desirable." Nobody dreamed about owning a Hyundai. Nobody posted Hyundai Sonatas on their bedroom walls. The cars were competent, affordable, and utterly forgettable. In the language of brand strategy, Hyundai had moved from "rejection" to "acceptance," but it had not yet achieved "aspiration."

The solution was one of the most aggressive talent acquisition campaigns in automotive history, a strategy that insiders began calling the "Avengers" approach.

The first and most consequential hire was Peter Schreyer, the German designer who had penned the original Audi TT, one of the most iconic automotive designs of the 1990s. When Hyundai announced in 2006 that Schreyer was joining as Chief Design Officer, the reaction in the industry ranged from disbelief to pity. Why would a designer of his stature join Hyundai? The answer, as Schreyer later explained, was creative freedom. At Audi, he was one voice among many in a vast Volkswagen Group bureaucracy. At Hyundai, he would have the chairman's ear and a blank canvas. Schreyer introduced the "Fluidic Sculpture" design language that transformed Hyundai's lineup from anonymous rental-car appliances into vehicles that people actually turned their heads to look at. The 2011 Sonata, with its swept-back silhouette and aggressive stance, was the first tangible proof that Hyundai could be a design-led brand.

But design only gets you to the showroom. The driving experience keeps you there. For that, Hyundai made what may have been an even more audacious hire: Albert Biermann, the head of BMW's legendary M Division. Biermann was the man responsible for some of the finest driving machines in automotive history, the M3, the M5, the cars that defined the phrase "ultimate driving machine." In 2015, he joined Hyundai as head of vehicle testing and high-performance development. If Schreyer's hire raised eyebrows, Biermann's raised entire foreheads.

The impact was profound and immediate. Biermann brought with him an entire philosophy of chassis tuning, suspension calibration, and dynamic refinement that Hyundai had never possessed. Within a few years, automotive journalists began noting that Hyundais and Kias were not just reliable and well-designed; they were genuinely enjoyable to drive. The Kia Stinger, a rear-wheel-drive sports sedan developed under Biermann's supervision, was the vehicle that definitively shattered the perception that Korean cars could not compete on driving dynamics. It was reviewed not just favorably, but rapturously, by publications that had historically treated Korean cars with polite condescension.

The third piece of the puzzle was Luc Donckerwolke, a Belgian designer whose resume included stints at Lamborghini, where he designed the Murciélago, and Bentley. Donckerwolke was brought in to help shape the identity of Genesis, Hyundai's audacious attempt at building a standalone luxury brand.

Genesis, launched as a separate marque in 2015, represented a calculated gamble. The automotive industry is littered with failed luxury brand extensions, from Volkswagen's Phaeton to various stillborn efforts by other mass-market manufacturers. The precedent that loomed largest was Toyota's Lexus, which had been launched in 1989 and had succeeded by creating a completely separate organization, a "monastic" approach that insulated the luxury brand from any association with its mass-market parent. Genesis took a different path. Rather than building everything from scratch, it leveraged the existing Hyundai Motor Group supply chain, particularly the engineering and components capabilities of Hyundai Mobis, while creating a distinct brand identity, dealer experience, and design language.

The initial investment in the Genesis program was approximately $500 million, a fraction of the billion-plus dollars that Lexus spent in the 1980s, adjusted for inflation. The bet was that by 2025, the luxury segment's purchase criteria had shifted. Buyers cared less about the prestige of the badge and more about the quality of the product, the technology on offer, and the ownership experience. Genesis was designed to win on those metrics.

By 2025, the bet appeared to be paying off. Genesis sold 221,482 vehicles globally, with the U.S. operation delivering 82,331 units, a ten percent increase over the prior year and a record for the brand. The GV80 Coupe recorded growth of 166 percent in its second year on the market. Perhaps more importantly, Genesis's luxury market share in the United States tripled to 3.5 percent over five years, powered by an expanding lineup that grew from three sedans to six models spanning sedans and SUVs. The brand is targeting 350,000 annual units by 2030, which would place it firmly in the competitive set with Lexus, BMW, and Mercedes-Benz.

The design and performance pivot of the 2010s was not just about making prettier, better-driving cars. It was about permanently changing the industry's mental model of what a Korean automaker could be. When Peter Schreyer and Albert Biermann and Luc Donckerwolke chose to stake their professional reputations on Hyundai, it sent a signal that no marketing campaign could replicate. Talent follows opportunity, and the world's best automotive talent was now flowing to Seoul.

VI. Inflection Point No. 3: The E-GMP and The EV Speed-Run

In the early months of 2020, as the world grappled with a global pandemic, Hyundai Motor was making a decision that would define its next decade. While Toyota hedged its bets on hybrids and hydrogen, while Volkswagen committed to its MEB platform but struggled with software integration, and while legacy Detroit automakers announced ambitious EV timelines they would later delay, Hyundai went all-in on what it called the Electric Global Modular Platform, or E-GMP.

The E-GMP was not simply an electric version of an existing platform. It was a purpose-built architecture designed from the ground up for battery-electric vehicles, with a specification sheet that read more like a Porsche engineering brief than anything from a mass-market automaker. The headline feature was 800-volt electrical architecture, a technology that enables ultra-fast charging. At the time of its announcement, 800-volt systems were essentially exclusive to the Porsche Taycan, a six-figure performance car. Hyundai was promising to deliver the same capability in a mid-market crossover priced under $45,000.

Think about what that means for a moment. The single biggest consumer objection to electric vehicles has always been charging time. Range anxiety is really charging-time anxiety. An 800-volt system can add roughly 200 miles of range in approximately eighteen minutes of fast charging, transforming EVs from "plan your life around charging stops" to "grab a coffee while the car fills up." By democratizing this technology, putting it in a vehicle that a middle-class family could actually afford, Hyundai was attempting to remove the single largest barrier to mass EV adoption.

The first product off the E-GMP platform was the Ioniq 5, launched in 2021, and it was a revelation. Styled as a retro-futuristic homage to the original 1975 Pony, the Ioniq 5 combined striking design with genuine technological leadership. It won World Car of the Year, World Electric Vehicle of the Year, and World Car Design of the Year in 2022, a clean sweep that no vehicle had previously achieved. More importantly, it sold. In the United States, Ioniq 5 retail sales climbed 151 percent year-over-year in September 2025, and the model recorded its highest-ever annual sales total for the year. The Ioniq 6 sedan and the larger Ioniq 9 followed, broadening the electric lineup across segments.

But the hardware platform was only half the story. Hyundai recognized that the real competitive battleground of the 2030s would be software, not sheet metal. The company announced plans to spend $14 billion through 2030 on software-defined vehicle development, an acknowledgment that the car of the future would be defined more by its code than by its combustion or even its battery. In his 2026 strategic vision address, Executive Chair Chung Eui-sun framed the stakes in existential terms, declaring that artificial intelligence was "not merely a tool but a transformative force capable of defining problems and creating new knowledge" and that Hyundai's future depended on whether it treated AI "as a tool or adopted it as the engine of organizational evolution."

The physical manifestation of this EV commitment is Hyundai Motor Group Metaplant America, a $7.6 billion facility in Ellabell, Georgia, about twenty-five miles west of Savannah. When total investments including battery joint ventures with LG Energy Solution and SK On are included, the figure rises to $12.6 billion, the largest single investment in Georgia's history. The facility, which began full production of the Ioniq 5 in October 2024, spans over sixteen million square feet and will eventually produce up to 500,000 electric and hybrid vehicles annually for Hyundai, Kia, and Genesis. Beyond the Metaplant itself, Hyundai committed an additional $21 billion in U.S. investment from 2025 to 2028, a figure that serves double duty as both a manufacturing strategy and a hedge against the trade policy uncertainty emanating from Washington.

The acquisition of Boston Dynamics in 2021 for approximately $1.1 billion fits into this broader transformation narrative. On the surface, buying a robotics company famous for videos of dogs and humanoids doing backflips seems like an odd move for an automaker. But the logic becomes clear when you understand Hyundai's vision of the factory of the future. Boston Dynamics' capabilities in autonomous mobility, manipulation, and sensor-driven navigation are directly applicable to automated manufacturing, warehouse logistics, and last-mile delivery. The integration is already happening. At the Singapore Innovation Center, Hyundai has been piloting Boston Dynamics' Stretch robot for logistics applications, and the Metaplant in Georgia incorporates advanced automation concepts informed by the acquisition. Whether Hyundai overpaid is debatable. SoftBank had acquired Boston Dynamics from Google's parent Alphabet for an estimated price between $100 million and $500 million. Hyundai paid $1.1 billion for an eighty percent stake. But the strategic value of robotics capabilities to a company betting its future on automated smart factories and autonomous mobility may well justify the premium. The more immediate financial question is the Boston Dynamics IPO timeline: Hyundai had committed to taking the unit public within four years of the acquisition, a deadline that lapsed in June 2025. SoftBank holds a put option exercisable through June 2026, adding a near-term financial overhang that investors should watch.

VII. Current Management: The Eui-sun Era

The boardroom at Hyundai Motor Group's headquarters in Seoul is a long way from the construction sites and shipyards where the Chung family built its empire. But the man who now sits at its head carries the weight of that history with him every day.

Chung Eui-sun became Executive Chair of Hyundai Motor Group in October 2020, succeeding his father Chung Mong-koo in what was widely viewed as the final step in a carefully orchestrated generational transition. He is the third generation of the founding family to lead the enterprise, the grandson of Chung Ju-yung and the son of the man who engineered the quality revolution. But Eui-sun is a fundamentally different kind of leader than either of his predecessors.

Where his grandfather was a construction baron who built through sheer force of will, and his father was an operations disciplinarian who built through quality obsession, Eui-sun is a dealmaker and a technology evangelist. He studied business at Korea University, spent time at the University of San Francisco, and cut his teeth running Kia Motors before ascending to the chairmanship of the broader group. Those who have worked with him describe a leader who is more comfortable in Silicon Valley than on a factory floor, more interested in partnerships than in command-and-control hierarchy.

The evidence is in the deals. Under Eui-sun's leadership, Hyundai formed a joint venture with Aptiv called Motional to develop autonomous driving technology. It invested in Rimac, the Croatian electric hypercar maker, through Kia. It partnered with Uber on air taxis. It acquired Boston Dynamics. Each of these moves represented a break from the traditional chaebol model of doing everything in-house. Eui-sun's philosophy, which he has articulated publicly as "Open Innovation," is that the pace of technological change in mobility has become too fast for any single company to master alone.

The governance structure, however, remains very much a chaebol affair. Eui-sun holds approximately 2.6 percent of Hyundai Motor Company directly, a seemingly small stake. But the real power lies in the web of cross-shareholdings that characterize the Hyundai Motor Group structure. Hyundai Mobis, the group's parts and technology arm, and Hyundai Glovis, the logistics subsidiary, are the key nodes in a circular ownership structure that gives the Chung family effective control far in excess of their direct economic interest. This structure is the perennial "bear case" for corporate governance at Hyundai. Critics argue that it allows the controlling family to extract value from minority shareholders and to pursue strategic priorities that may not align with shareholder return maximization.

The counterargument, and it is a powerful one, is that this structure enables a time horizon that publicly traded Western automakers simply cannot match. When Eui-sun commits $14 billion to software development over a decade, or $12.6 billion to a single manufacturing complex in Georgia, he is making bets that a CEO accountable to quarterly earnings calls might never make. The chaebol structure is the mechanism that allows Hyundai to think in decades while its competitors think in quarters. Whether the benefits of that long-termism outweigh the governance risks is one of the central analytical questions for any investor considering the stock.

The stated goal of the Eui-sun era is to transform Hyundai from a "Car Maker" to a "Smart Mobility Provider," with a target of deriving thirty percent of revenue from non-automobile sources by 2030. That is an extraordinarily ambitious target for a company that currently derives the vast majority of its revenue from selling cars and trucks. But it provides a framework for understanding the investments in robotics, air mobility, hydrogen, and software that might otherwise appear scattered.

Vice Chair Jaehoon Chang, who serves as CEO of Hyundai Motor Company, handles the operational execution of this vision. Chang has reaffirmed the company's commitment to becoming a "software-driven mobility company," a phrase that would have been unimaginable from a Hyundai executive even a decade ago. The division of labor between the visionary chairman and the operational CEO appears to be functioning well, though the ultimate test will come when the massive capital commitments of the current period need to translate into returns.

VIII. The Hidden Businesses and Segments

When most people think of Hyundai, they think of the cars in their neighbor's driveway. But the Hyundai Motor Group ecosystem extends far beyond the vehicles that carry the badge, and some of the most strategically important assets are the ones that consumers never see.

Hyundai Mobis is the one that matters most. Think of it as the "Intel Inside" of the Hyundai universe. Mobis is the group's parts and technology subsidiary, and it designs and manufactures many of the most sophisticated components that go into Hyundai, Kia, and Genesis vehicles: advanced driver-assistance systems, electrification modules, infotainment platforms, and sensor suites. In an industry where the value of a vehicle is increasingly defined by its electronics rather than its mechanical components, Mobis is where much of Hyundai's technological capability actually resides. For investors who want exposure to Hyundai's technology trajectory without the capital intensity and cyclicality of vehicle manufacturing, Mobis is the entity to watch. It trades separately on the Korea Exchange and has its own analyst following.

Supernal is the venture that sounds like science fiction but is staffed like a serious engineering program. Based in Washington, D.C., Supernal is Hyundai's Urban Air Mobility division, tasked with developing electric vertical takeoff and landing aircraft, essentially flying taxis. The company has over 600 engineers working on the program and has announced plans to introduce an unmanned aircraft system with a hybrid powertrain in 2026, followed by an all-electric model optimized for intra-city operations in 2028. The regulatory path for urban air mobility remains uncertain, and commercialization timelines in this sector have a long history of slipping. But Hyundai's commitment is real in terms of headcount and capital, and the potential market, if it materializes, is measured in trillions.

Then there is hydrogen. Hyundai's hydrogen brand, HTWO, represents more than two decades of accumulated expertise in fuel-cell technology. While the consumer hydrogen vehicle market has been disappointing globally, with limited refueling infrastructure constraining adoption, Hyundai has found a different angle: commercial vehicles. The company is the world leader in hydrogen fuel-cell trucks, a segment where the economics of hydrogen, high energy density, fast refueling, and no battery weight penalty, make considerably more sense than in passenger cars. Hyundai is building what it calls the "Hydrogen Value Chain" in both Georgia, USA, and South Korea, encompassing production, storage, distribution, and end-use in heavy transport. The thesis is that hydrogen will never power your sedan, but it may well power the truck that delivered the goods in your kitchen.

Each of these businesses, Mobis, Supernal, HTWO, represents an option on a different future. Mobis is the near-term value driver, a profitable technology company embedded within the group structure. Supernal and HTWO are longer-dated options, potentially very valuable if their respective markets develop, but contributing minimal revenue today. The sum-of-the-parts story is one that Hyundai's management is increasingly trying to articulate to investors, and it is a story that the current stock price may not fully reflect.

IX. Playbook: Business and Investing Lessons

The Hyundai story, spanning six decades and three generations of leadership, offers a masterclass in several dimensions of strategy that are worth examining through formal frameworks.

Start with Hamilton Helmer's 7 Powers. The most obvious power that Hyundai has demonstrated is counter-positioning, embodied by the 1999 warranty gamble. As discussed earlier, the genius of the ten-year warranty was not that it was generous. It was that incumbents could not rationally respond to it. This is the textbook definition of counter-positioning: a newcomer adopts a business model or strategy that is superior but which incumbents cannot copy because doing so would damage their existing business. Toyota matching a ten-year warranty would have implied that Toyotas might break within ten years, a concession antithetical to its entire brand positioning.

The second power is scale economies, and at Hyundai, this power is expressed in physical form at the Ulsan Complex. Situated on 1,225 acres on the southeastern coast of South Korea, Ulsan is the world's largest integrated automobile manufacturing facility. It encompasses five factories, employs approximately 34,000 workers, and produces roughly 1.54 million vehicles per year, or one car every ten seconds. But what makes Ulsan truly unique is not just its size. It is the degree of vertical integration. The complex includes its own dedicated port, through which seventy-five percent of its annual output is shipped directly to over two hundred countries. Hyundai owns its own steel production through Hyundai Steel. It owns its own shipping and logistics through Hyundai Glovis. From raw materials entering one end of the supply chain to finished vehicles sailing out the other, an extraordinary proportion of the value chain is controlled by the group. This level of integration drives unit costs down relentlessly and provides a buffer against the supply chain disruptions that hobbled less vertically integrated competitors during the pandemic.

The third power is what Helmer might classify as a cornered resource, though in Hyundai's case the resource is not a patent or a talent pool but something more cultural: speed of execution. The chaebol structure, for all its governance shortcomings, enables a velocity of decision-making and capital deployment that Western automakers cannot match. When the decision was made to build the Metaplant in Georgia, the facility went from announcement to producing vehicles in under three years. In the Western automotive industry, a timeline like that is almost unheard of. The centralized decision-making and vertically integrated supply chain mean that Hyundai can execute a five-year project in three years, a structural advantage that compounds over time as each project completed ahead of schedule frees up capital and organizational bandwidth for the next one.

Now apply Porter's Five Forces to Hyundai's competitive position. The threat of new entrants is genuinely high and rising. Xiaomi launched its SU7 electric sedan to enormous demand in China. Sony and Honda formed a joint venture. BYD is expanding globally with aggressive pricing. The barriers to entry in electric vehicles are structurally lower than in internal combustion, because EVs have far fewer mechanical components and the critical technology, the battery, is available from third-party suppliers. This is precisely why Hyundai is pivoting so aggressively toward software, because software capability, deeply integrated with vehicle hardware, is a barrier to entry that cannot be purchased from a supplier catalog.

Supplier power is unusually low for Hyundai, for the simple reason that Hyundai is, to a remarkable degree, its own supplier. Hyundai Mobis provides components, Hyundai Steel provides raw materials, Hyundai Glovis handles logistics. This vertical integration means that the company is far less exposed to supplier pricing power than competitors who rely on external supply chains.

Buyer power is moderate and segment-dependent. In the mass market, consumers are highly price-sensitive and have abundant alternatives. In the luxury segment through Genesis, buyers are less price-sensitive but more demanding of brand cachet, which Genesis is still building. The competitive rivalry is intense across all segments, with the EV transition adding new competitors even as legacy players consolidate.

For investors tracking Hyundai's ongoing performance, two key performance indicators matter above all others. The first is global electrified vehicle mix as a percentage of total sales. Electrified vehicles, encompassing battery-electric, plug-in hybrid, and hybrid models, approached one million units globally in 2025, representing roughly 38 percent of the retail sales mix in the United States. Hyundai's 2030 target of 3.3 million electrified vehicle sales implies this mix needs to rise dramatically. Tracking the quarterly trajectory of this metric reveals whether the company is executing on its most important strategic transition, or whether consumer demand, production constraints, or competitive pressure are slowing the shift. The second KPI is operating profit margin. In 2025, the consolidated operating margin came in at 6.2 percent, down from the prior year, with management guiding to 6.3 to 7.3 percent for 2026. The margin trajectory captures the tension at the heart of the Hyundai story: the company is simultaneously investing massive sums in EV platforms, software, robotics, and new manufacturing capacity while trying to maintain profitability in an increasingly competitive market. A sustained decline in operating margin would signal that the investment thesis is breaking; stable or improving margins amid heavy investment would confirm that the scale economies and vertical integration are working as intended.

X. The Bear Case vs. The Bull Case

Every great investment story has a shadow narrative, a version of events where the risks materialize and the thesis breaks. For Hyundai, the shadow narrative has several distinct chapters.

The software gap is the most existential concern. Hyundai has committed $14 billion to software development through 2030, and Executive Chair Chung has made AI and software-defined vehicles the centerpiece of his strategic vision. But the question remains: can a company whose core competency for sixty years has been bending metal and assembling physical objects transform itself into a software company? Tesla's advantage is not its cars; it is the integrated software stack that controls every aspect of the vehicle, from battery management to autonomous driving to over-the-air updates. In China, Huawei and Xiaomi bring the software DNA of consumer electronics giants to the automotive space. Hyundai's software capabilities, while improving, have not yet been tested at the scale and sophistication that these competitors demand. The $14 billion commitment is necessary, but spending money and building capability are not the same thing.

Labor relations represent a structural risk that is unique to Hyundai among major global automakers. The Korean automotive unions are among the most powerful and militant in the world. In 2025, following the Korean government's approval of the so-called "Yellow Envelope Law" that expanded protections for union activity, Hyundai's 42,000-member union launched its first partial strikes in seven years across three facilities including the flagship Ulsan plant. The union's demands extended beyond traditional wage and hours issues to include advance notification of new business ventures and overseas plant expansions, essentially seeking a veto over strategic decisions. Annual labor disputes have been a feature of Hyundai's operating environment for decades, and while they have never been fatal, they impose real costs in terms of lost production, elevated labor expenses, and management distraction.

The China collapse is a cautionary tale about geopolitical risk that no amount of product excellence can mitigate. At its peak in 2016, Hyundai sold over 1.6 million vehicles annually in China, commanding roughly ten percent of the market. Then the THAAD crisis hit. South Korea's deployment of a U.S. missile defense system provoked a Chinese government-orchestrated consumer boycott of Korean goods, and Hyundai's sales cratered almost overnight. By 2024, combined Hyundai and Kia market share in China had fallen to approximately one percent. In December 2025, the company sold its shares in its Chinese parts subsidiary, effectively acknowledging that the Chinese market was lost. The lesson for investors is that Hyundai's global footprint, while a strength, also exposes it to geopolitical risks that are inherently unpredictable and against which no warranty or design excellence provides protection.

The tariff environment adds another layer of uncertainty. The U.S. tariff regime has been in flux, and Hyundai's 2025 operating profit decline was attributed in part to tariff impacts and higher sales incentives needed to remain competitive. The Metaplant in Georgia and the $21 billion U.S. investment commitment are partly defensive moves, designed to ensure that Hyundai has sufficient domestic production capacity to navigate whatever trade policy emerges.

The bull case, however, is compelling on multiple fronts.

Hyundai is arguably the only legacy automaker that has proven it can build a profitable, high-performance electric vehicle platform today, not in 2027 or 2030, but now. The E-GMP platform's 800-volt architecture, the Ioniq lineup's commercial success, and the Metaplant's production ramp demonstrate execution capability that most competitors have yet to match. Ford has lost billions on its EV operations. General Motors has repeatedly delayed EV launches. Volkswagen's software subsidiary Cariad has been plagued by delays and leadership turnover. Against this competitive backdrop, Hyundai's EV execution looks genuinely differentiated.

Genesis is successfully penetrating the luxury segment with expanding market share, a broader product lineup, and plans for hybrid models beginning in 2026. The luxury segment carries structurally higher margins, and Genesis's growth trajectory toward 350,000 annual units by 2030 represents a meaningful margin accretion opportunity for the group.

The "moonshot" investments in hydrogen, robotics, and urban air mobility provide asymmetric upside that is not priced into the stock. If any one of these bets pays off at scale, the value creation could be transformational. If none of them work, the downside is manageable because these investments are sized appropriately relative to the group's cash generation.

And then there is the valuation itself. At a market capitalization of approximately 118 trillion won against revenue of 186 trillion won, Hyundai trades at a price-to-sales ratio that is modest by global automotive standards and deeply discounted relative to its EV-focused narrative. The "Korea discount," the structural undervaluation that the market applies to Korean equities due to governance concerns and chaebol complexity, has been a persistent feature of Hyundai's valuation. Whether that discount is justified or represents an opportunity is a judgment call that depends on one's assessment of the governance risks discussed earlier.

XI. Epilogue: Final Reflections

There is a phrase attributed to Chung Ju-yung, the patriarch who started it all, that has become something of a corporate motto within the Hyundai universe: "Siryuh-bwahn-ni?" Roughly translated, it means "Have you tried it?" It was reportedly his response whenever an engineer or manager told him that something could not be done. Have you actually tried, or are you just assuming it is impossible?

That phrase echoes across the entire arc of this story. A farmer's son who talked his way into a Barclays loan with a banknote. A quality revolution led by a man who stopped assembly lines over door handles. A warranty that bet the company on its own improvement. A mid-market crossover with Porsche-grade electrical architecture. A robotics acquisition that mystified analysts. A flying taxi division with six hundred engineers.

At every inflection point, the Hyundai playbook has been the same: absorb the best available knowledge, execute with chaebol speed, make the asymmetric bet, and dare the market to underestimate you again. The company that entered the United States in 1986 selling $4,995 throwaway sedans now operates the world's largest auto plant, builds vehicles that win global car-of-the-year awards, and is investing tens of billions in a future where cars drive themselves, robots roam factory floors, and air taxis shuttle commuters above gridlocked cities.

Whether that future materializes on the timeline Hyundai envisions, whether the software capabilities catch up to the hardware ambitions, whether the governance structure enables or constrains value creation, these remain open questions. But the pattern of the last sixty years suggests that betting against a company whose founding ethos is "Have you tried it?" has been a consistently losing proposition.

XII. Key Resources

- Made in Korea: Chung Ju Yung and the Rise of Hyundai by Richard M. Steers

- Hyundai's Ulsan Plant Virtual Tour (Hyundai Motor Global Newsroom)

- E-GMP Technical Deep-Dive (Hyundai Motor Group Technical Center)

- Boston Dynamics "Stretch" Logistics Robot Analysis

- Hyundai Motor 2025 Annual Report and CEO Investor Day Presentation

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube