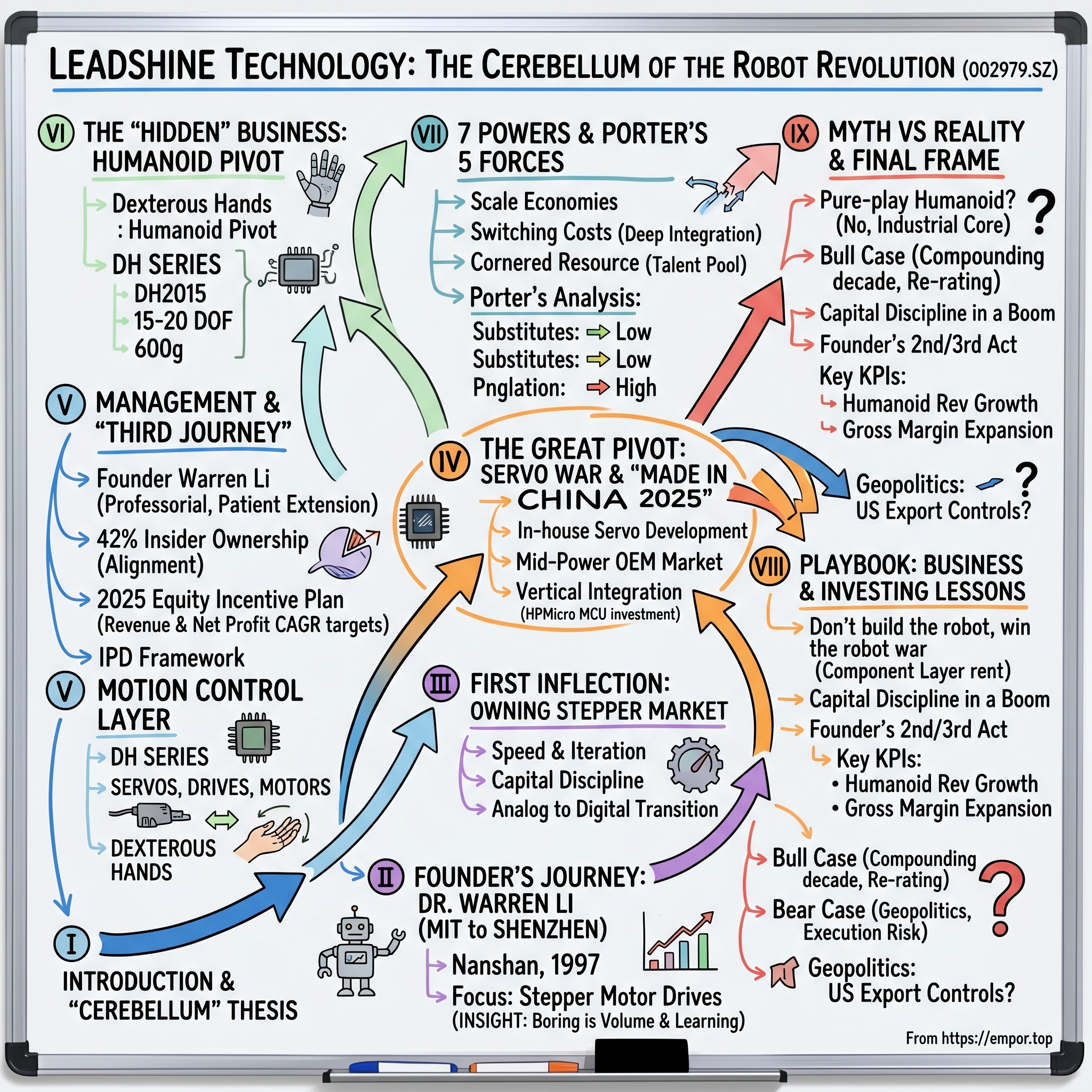

Leadshine Technology: The Cerebellum of the Robot Revolution

I. Introduction & The "Cerebellum" Thesis

Picture a humanoid robot picking up an egg. Not smashing it. Not dropping it. Just picking it up with the same gentle, almost absent-minded precision a toddler uses after their first hundred attempts. Every time that hand closes around the shell without cracking it, something miraculous has happened at the motor level. A tiny current has been modulated thousands of times per second. A rotor has spun, stopped, and reversed with torque calibrated to the weight of a chicken embryo. The "brain" of the robot may be a large language model trained on a billion YouTube videos, and the "body" may be a gleaming exoskeleton stamped out in Dongguan. But what sits between them—what translates intent into a movement so delicate it could hold a human heart—is a piece of technology the industry, almost without irony, calls the cerebellum.

In 2026, the global technology conversation has been thoroughly consumed by two ends of the humanoid robotics supply chain. On one side stand the brain makers: Tesla with Optimus Gen-3, Figure AI with its 03 production line, Boston Dynamics and Agility, all racing to turn robotics into the next iPhone moment. On the other side sit the body builders: the cast-aluminum frame suppliers, the harmonic reducer specialists, the lithium-ion pack integrators. Between them, largely invisible to the retail investor and barely discussed on Twitter, lies the most under-appreciated layer of the stack: the motion control layer. The servos, the stepper motors, the drives, the controllers, and—crucially—the dexterous hands with their twenty axes of independently controlled torque. This is the cerebellum. And the company that has quietly, methodically, almost monastically built itself into a primary contender to supply this layer to the humanoid economy is a mid-cap industrial listed on the Shenzhen Stock Exchange under the ticker 002979.SZ.

Its name is Leadshine Technology Co., Ltd. It began in a Nanshan dormitory in 1997 with a founder who had just traded an MIT robotics lab for a Shenzhen industrial park. For two decades it made its money a few dollars at a time, selling stepper motor drives to printer manufacturers, textile looms, and the low-end CNC machines that populate the back alleys of Chinese light industry. It was, by any honest reckoning, unsexy. And yet by 2026 this same company operates a dedicated humanoid robotics R&D base in Dongguan, ships multi-fingered dexterous hands to Tier-1 embodied AI startups, and commands the attention of a global investor class that only eighteen months earlier could not have pronounced "Leadshine."

This is the story of how that happened. It is a story of reverse brain drain, of a founder's second and third acts, of the slow accretion of competence in the unglamorous middle of an industrial stack. It is also a story about China's twenty-year march from copycat component shop to systems integrator, and about what happens when you spend three decades obsessed with a single word: precision.

II. The Founder's Journey: From MIT to the "Silicon Valley of Hardware"

The grainy 1990s photograph—still framed in Leadshine's corporate museum, according to interviews with long-tenured employees—shows a slender young Chinese engineer in a flannel shirt standing next to a hulking robotic arm at an MIT lab. The engineer's hair is a little too long, his smile a little too hesitant. He is Dr. Warren Li (Li Weiping in Mandarin), and at the moment the shutter clicked he was finishing his doctorate in robotics and control systems at a time when the phrase "Chinese engineer with an MIT Ph.D." was rare enough to be nearly exotic.

To understand why Warren Li decided to leave Cambridge, Massachusetts and move to a half-built district of Shenzhen in 1997, you have to understand the era. In the mid-1990s, China was the world's factory in a very specific and somewhat humiliating sense: it made things, but it did not design them. Motion control—the quiet discipline of making motors turn exactly the right number of degrees at exactly the right speed—was dominated by Japanese and German firms. Names like Yaskawa, Panasonic, Mitsubishi, Sanyo Denki, Oriental Motor, Siemens, and Bosch Rexroth. A Chinese CNC factory stamping out bicycle parts might use Chinese steel, Chinese plastic, and Chinese labor, but the brain and cerebellum inside its machines were almost certainly imported. The margin went home to Osaka or Munich.

Li had grown up in this environment, gone abroad, and absorbed the other side of the trade. He had seen how much of the "black box" in American robotics was simply software riding on top of carefully tuned analog electronics. And he had watched the rise of Shenzhen from afar—a former fishing village that by 1997 was on its way to becoming the densest hardware supply chain on earth, a city where a prototype that took six weeks in California could be iterated in six days if you knew the right shop on the right block. The returnee thesis, for him, was not patriotic posturing. It was simple arbitrage: take world-class control theory, pair it with world-class manufacturing density, and you had a business.

He founded Leadshine in Nanshan District, Shenzhen, in 1997 with a handful of engineers and a focus that, to anyone coming from an MIT lab, would have looked almost insultingly narrow. Stepper motor drives. Not robotic arms. Not vision systems. Not anything you would brag about at a reunion dinner. Stepper drives were the workhorses of cheap automation—the little circuit boards that took a digital pulse from a microcontroller and translated it into a discrete rotation. Every desktop printer, every vinyl cutter, every budget CNC router, every semi-automatic textile loom on the Pearl River Delta needed one. They sold for tens of dollars apiece, not thousands. They were, by the standards of the industry, boring.

But here is the founder's insight, and it is the kind of insight that only someone with a doctorate and a factory nearby tends to have: boring is where the volume lives. And wherever volume lives, the learning curve runs fastest. Li bet that if he spent a decade doing the unglamorous work of making the best, cheapest, most reliable stepper drives in China, he would accumulate two assets that money could not easily buy: manufacturing muscle and algorithmic intuition. The first would throw off cash. The second would, eventually, let him move up the value chain to servos, to integrated controllers, and someday to whatever new motion problem came next. The "someday" took almost thirty years to arrive. When it did, it took the form of a humanoid robot.

The Warren Li of 2026 is in his early sixties, having held the chairman and general manager roles at Leadshine for the entire three-decade arc. Colleagues describe him as more professor than CEO—soft-spoken, fond of whiteboard derivations, allergic to the kind of conference-circuit showmanship that defines so many Chinese tech founders. The throughline from 1997 to today is not a pivot. It is a patient extension. The obsession with precision that made him leave MIT is the same obsession that now drives Leadshine's push into twenty-degree-of-freedom dexterous hands.

That patience would be tested almost immediately. By the early 2000s, every coastal Chinese city had its own stepper drive workshop, and the race to the bottom was on.

III. The First Inflection Point: Owning the Stepper Market

If you want to understand Chinese industrial capitalism in the 2000s, study a stepper drive catalog from around 2005. The same generic board would appear under a dozen brand names, each one priced a few renminbi lower than the last, each one claiming marginally better torque at marginally lower cost. Most of these companies are now forgotten, absorbed, or reduced to no-name parts on Alibaba listings. Leadshine was one of the few that survived with its name, its margins, and its engineering culture intact. The question worth asking is how.

The first part of the answer was speed. Shenzhen in 2005 was already the most iterative hardware city in the world. If a customer called Leadshine on a Monday complaining that their drive hummed at a certain frequency on a specific Hitachi printer, Warren Li's team could source a modified capacitor from a supplier three blocks over by Tuesday afternoon, respin a board by Wednesday, and ship a revised sample by Friday. The Japanese competitors—Sanyo Denki, Oriental Motor—were technically superior. They built drives that could run for a decade without a failure. But their engineering cycles ran in quarters, not days. For a Japanese firm, a minor specification change required three meetings in Tokyo and a sign-off from a plant manager who had never visited the customer. For Leadshine, it required a phone call and a taxi. In the low end of the market, where the customer was a small Shenzhen OEM who needed a drive that worked "well enough" at half the price, speed beat perfection every time.

The second part of the answer was capital discipline. Leadshine did not chase foreign venture capital. It did not grow by pouring money into a money-losing land grab. Instead, it reinvested the thin but real margins from each generation of stepper drives into the next generation. Profit-driven R&D, in the language of Chinese manufacturing. Every dollar earned went back into either a marginally better driver chip, a marginally better heat-dissipation design, or a marginally better assembly line. Over a decade, those margins compounded into a moat. By the time Leadshine reached its tenth anniversary in 2007, it was selling more stepper drives per year than any other company in China. The company would go on to claim, and industry reports would repeatedly confirm, a domestic market share of roughly one-third in the mainstream stepper drive segment—a share it has defended into the mid-2020s.

The third part, and the most consequential, was the transition from analog to digital. In the mid-2000s, most stepper drives were analog affairs: discrete components, tuned by hand, subject to drift. The cutting edge was digital stepper drives, where a small microcontroller ran the commutation algorithm in software, opening the door to features like micro-stepping, current shaping, and real-time fault detection. This was the technological transition that killed off most of Leadshine's low-end Chinese competition. A workshop in Dongguan could still build analog drives and sell them cheap. It could not build a digital drive with embedded software. That required the kind of in-house firmware team that Warren Li had been quietly assembling for a decade.

By around 2010, Leadshine was no longer just the cheapest option. It was holding its own patents on current-control algorithms, shipping digital drives that matched Japanese quality at a Chinese price, and beginning to appear in export markets—shipped out of Shenzhen to Southeast Asia, Eastern Europe, and eventually to a niche but growing base of American and European customers who cared more about cost than brand. The stepper business had become, for the company, an annuity. A cash cow that threw off enough margin to fund something much more ambitious.

What came next was the pivot that would define the company's second act: the move into servo motors. Servos were to steppers what sports cars were to tractors—same basic idea, vastly more difficult engineering. And the servo market was not populated by Dongguan workshops. It was populated by giants.

IV. The Great Pivot: The Servo War and "Made in China 2025"

In 2015, Chinese Premier Li Keqiang unveiled a policy document with a title that would become globally infamous: "Made in China 2025." The plan listed ten industries in which China intended to achieve technological self-sufficiency, and motion control—servos, drives, CNC systems—sat near the top. To foreign competitors it read as a threat. To Chinese industrial companies it read as something closer to a starter's pistol.

By the time "Made in China 2025" was announced, Leadshine had already been circling the servo business for nearly five years. The motivation was straightforward. A stepper motor moves in discrete steps, which limits its precision at high speed and makes it prone to a failure mode engineers call "losing steps"—the motor skips a pulse under load, the position drifts, and suddenly your CNC machine is cutting a part a millimeter off. A servo motor, by contrast, runs closed loop. An encoder reports position back to the drive in real time, and the drive corrects. The result is smoother motion, higher torque at speed, and the kind of precision required for anything more demanding than a vinyl printer. As Chinese industry moved up-market—into 3C electronics assembly, into lithium-ion battery production, into solar panel fabrication, and eventually into medical and semiconductor manufacturing—the stepper market plateaued while the servo market compounded.

The problem was that servos belonged to the Japanese and Germans. Yaskawa alone commanded roughly a quarter of the global market. Add Mitsubishi, Panasonic, Fanuc, Siemens, and Bosch Rexroth, and the combined foreign share was punishingly high. Chinese domestic competitors—Inovance, Estun, Hollysys, Shanghai Step—were attacking from below. A company like Leadshine, which had been selling stepper drives for fifteen years, had to answer a basic question: where exactly could it win?

The answer, articulated by Warren Li and his senior engineering team in the early 2010s and refined through painful trial and error, was the mid-power OEM market. Think of the servo universe as a pyramid. At the top sit high-power, high-precision applications: machine tools used in aerospace, semiconductor wafer steppers, injection-molding machines for automotive components. That market was owned by Yaskawa and Siemens, and no Chinese company would crack it in this cycle. At the bottom sit commodity applications—cheap conveyors, simple pick-and-place machines—where margins had collapsed. In the middle sat the OEM market: the companies that designed and built automation equipment for the new Chinese growth industries. 3C electronics assembly for smartphone factories. Lithium battery winding and coating machines. Solar cell stringers. These OEMs needed servos that were 80 percent as good as a Yaskawa at 60 percent of the price, integrated tightly with drives and controllers and shipped with responsive local support. Inovance, now the largest Chinese motion control company, had focused its energy on massive factory automation systems. That left the dedicated mid-power OEM niche wide open.

Leadshine attacked it systematically. It built servo motors in-house rather than rebadging someone else's. It developed its own drives, its own controllers, and—critically—its own firmware stack so that an OEM customer could drop in a Leadshine motion system as a single integrated solution. The pitch was simple: one supplier, one tech support line, one software environment, all tuned specifically to the customer's industry. A lithium battery winding machine builder could plug in a Leadshine EL8 servo, tune it in the company's proprietary software, and ship product. The total cost of ownership was lower not because the parts were cheaper but because the integration was easier.

The second strategic decision was vertical integration upstream into silicon. In the mid-2010s, Chinese motion control companies faced a common problem: they did not control their own chips. A servo drive's performance is dictated in large part by the microcontroller at its heart. For years, Chinese drive makers bought their MCUs from Texas Instruments, STMicroelectronics, or Renesas. If any of those suppliers raised prices, extended lead times, or—in an increasingly plausible geopolitical scenario—restricted exports, the drive maker's gross margin evaporated overnight. Leadshine's answer was an equity investment in Shanghai HPMicro, a specialist MCU design house focused on motor control chips. The bet was classic capital-light vertical integration: rather than buy a chip company outright, Leadshine took a stake large enough to secure preferential access, influence the roadmap, and hedge its gross margins, without taking on the balance-sheet risk of owning a fab-light semiconductor company in an industry notorious for cycle pain. Contrast this with the fashion among Chinese industrial peers in the same period. Estun, a servo and robotics competitor, paid a rumored premium to acquire Germany's Cloos robotics business, a storied but aging welding brand, stretching its balance sheet in a move many analysts later described as vanity M&A. Leadshine, by refusing to play that game, preserved the capital discipline that had kept it alive through the stepper wars.

The financial footprint of this strategic restraint is visible in one number worth dwelling on. Leadshine's R&D spending has consistently run at roughly ten to twelve percent of revenue for the last several years—a level that would be unremarkable at a software company but is almost unheard of for a mid-cap Chinese industrial firm its size. For context, many of its low-end competitors run at three to five percent. That multi-year over-investment in research, funded out of the stepper business's cash flow, is what made the company's next move possible. Without it, the humanoid pivot would have been impossible.

V. Management and the "Third Entrepreneurial Journey"

To sit across from Warren Li in 2026 is to meet a founder who carries himself more like a university department head than the chairman of a publicly listed industrial company with a market capitalization measured in tens of billions of renminbi. He wears plain collared shirts, speaks in the mildly didactic cadence of a lifelong engineer, and—according to former employees—still occasionally corrects whiteboard derivations at internal R&D reviews. He is, in the language of corporate governance, an owner-operator of the purest kind. Public filings disclose that Dr. Li and his immediate family control roughly forty-two percent of the company's outstanding shares, a level of insider ownership that puts him firmly in the founder-aligned camp and rules out any quick hostile-takeover scenario. When Warren Li speaks about a ten-year humanoid robotics roadmap, he is speaking about his own money, his own reputation, and, implicitly, his own legacy.

That last point matters, because Leadshine's current chapter is not a typical Chinese industrial story of generational succession. It is a story of a founder in his early sixties deliberately choosing to commit the company to a third entrepreneurial journey rather than coast on the first two. The first was the stepper business. The second was the servo pivot. The third—humanoid components—required him to throw the weight of a mature, profitable, cash-generative industrial firm behind a market that in 2022 barely existed and in 2026 is still burning cash at the customer level. Boards of many listed Chinese companies would have balked. A non-founder CEO, thinking about his next quarterly bonus, certainly would have balked. The forty-two percent ownership stake is what makes a bet of this scale possible.

The 2025 Equity Incentive Plan, disclosed through the company's filings in the summer of 2025, is the clearest window into management's ambition. Rather than the soft performance targets that characterize many Chinese corporate stock plans, Leadshine's plan tied executive equity vesting to a set of targets that internal observers described as "brutal" when the document circulated. The headline numbers: a revenue compound annual growth rate of roughly twenty percent measured against a 2024 baseline, and a net profit compound annual growth rate of roughly twenty-three percent over the same vesting window. In a global industrial context, where low-double-digit growth is considered excellent, these targets were aggressive bordering on aspirational. They were also, importantly, a signal to the market. Warren Li and his management team were telling investors, in effect, that they expected the robotics business to compound hard enough to re-rate the entire company. If they miss, executives' own equity vests partially or not at all. If they hit, the value creation flows through to the shareholder base as a whole.

Beneath the financial incentives sits an organizational transformation that is harder to see but arguably more important. Starting in the early 2020s, Leadshine began migrating its product development process toward the "Integrated Product Development" (IPD) framework famously adopted by Huawei in the late 1990s and refined into a near-religion by consultants across Shenzhen since. IPD, in plain language, is an attempt to break down the silos between R&D, marketing, manufacturing, and sales so that a product is designed from day one with a complete view of customer needs, cost targets, and supply chain realities. For a founder-engineer-led firm like Leadshine, the risk of stagnation was always that the company would optimize for technical elegance at the expense of time-to-market and customer fit. IPD is management's antidote. It is also the machinery that allowed Leadshine to stand up an entirely new humanoid robotics division in less than three years without cannibalizing its core business.

The second layer of diligence worth flagging here is concentration and succession. The family's forty-two percent stake is a strategic asset, but it is also a concentration risk. Any health event or governance shock involving Warren Li would reverberate through the share price. Filings as of the most recent disclosure cycle show no obvious heir-apparent or co-CEO, and the company has not publicly articulated a succession plan. For long-term investors in a founder-dominated industrial firm, that is an open question worth monitoring rather than resolving in advance.

With the culture and capital structure understood, the interesting question becomes what exactly management decided to build with all this optionality. The answer lives in a factory campus on the outskirts of Dongguan and inside a product line that, until very recently, almost no one outside the company's engineering staff knew existed.

VI. The "Hidden" Business: The Humanoid Pivot

Walk into a lab at Figure AI, or 1X, or one of the roughly thirty Chinese humanoid startups that emerged after 2023, and the robots on the workbench look impressively human-shaped. They stand on two legs, balance, walk, even do the occasional halting dance. They impress because they look like us. But to a robotics engineer, the truly interesting parts of these machines are not the legs, which are the easy problem. They are the hands. The hands are where the money is, the hands are where the IP is, and the hands are where the next decade of progress will be fought and won. And it is exactly there, in the hands, that Leadshine has placed the largest capital bet in its history.

The short version of why hands are hard goes like this. A human hand has twenty-seven bones, thirty-four muscles, and around twenty-seven degrees of freedom. To approximate it mechanically, a dexterous robotic hand needs something on the order of twenty individually actuated joints, each one driven by a motor small enough to fit in a fingertip, powerful enough to generate useful force, and precise enough to distinguish between holding a grape and crushing it. The electronics that drive each of those motors must sit within the hand itself—routing cables up through a thick wrist and forearm is not practical at this degree of miniaturization. The firmware must process sensor feedback from force and tactile sensors at kilohertz frequencies to enable behaviors like adjusting grip strength when an object starts to slip. And the entire assembly must weigh on the order of half a kilogram, so that a humanoid robot can hold up its own arm without dramatically increasing the shoulder actuator's torque burden. It is, in short, a problem that combines electric motor design, miniaturized drive electronics, firmware, sensor integration, mechanical engineering, and materials science. Almost no one in the world is set up to solve all of those simultaneously. Leadshine has spent thirty years building precisely the capabilities needed to do so.

The product line that crystallized this bet was unveiled publicly in 2024 under the name of the DH Series dexterous hand. The flagship variant, the DH2015, offered fifteen-to-twenty degrees of freedom in a hand weighing roughly six hundred grams—comparable to a small adult human hand. It used a combination of coreless brushless motors, planetary gearboxes, and tendon-driven linkages to deliver fingertip force in the neighborhood of ten newtons per finger, sufficient to grip a water bottle firmly or pinch a pen between thumb and forefinger. Demonstrations at robotics conferences in 2024 and 2025 showed the hand pouring water from a bottle, picking up a coin from a table, pressing the buttons on an elevator panel, and—the set-piece demonstration—pinching a quail's egg between thumb and index finger without cracking the shell. The hand was not a research prototype. It shipped in production quantities to humanoid robotics OEMs, and by the second half of 2025 had become the reference platform for several domestic Chinese humanoid startups and at least one North American embodied-AI company whose identity has not been publicly disclosed.

To back the DH Series and related products, the company announced in 2024 and began executing in 2025 a dedicated humanoid robotics component production base in Dongguan, with total planned investment of roughly five hundred million renminbi—on the order of seventy million U.S. dollars. By the standards of the semiconductor industry, that is a rounding error. By the standards of Leadshine, which had historically expanded through small, self-funded facility upgrades, it was the single largest capital deployment in the company's twenty-seven-year history. The Dongguan base is designed to produce not just dexterous hands but the full stack of humanoid motion components: joint modules, frameless torque motors, integrated drives, and the hollow-shaft servo assemblies that sit inside a humanoid's shoulders, hips, and knees. When fully operational, it will give Leadshine the ability to be a single-vendor supplier for the entire motion control layer of a humanoid robot—from the ankle servo to the fingertip actuator—with internally developed silicon, firmware, and mechanics.

The segment-level economics, to the extent they have been disclosed, tell the investor story in miniature. As of the most recent reporting period, humanoid and robotics-related revenue represented a modest share of total company revenue—small enough that it did not move the consolidated top line dramatically. But the year-over-year growth rate of the segment was multiples higher than the core stepper and servo business. More importantly, the order book—disclosed partially in public communications and elaborated in analyst briefings—suggested that humanoid component revenue could scale to a meaningful double-digit share of total revenue over the next cycle if current commercial discussions with Tier-1 humanoid OEMs convert. In financial language, the humanoid business is a call option on the stock. Investors are paying a modest premium today for a binary outcome in the 2027–2030 window.

The element of the pivot that is easiest to miss, and most important, is that Leadshine does not need the humanoid business to succeed for the company to succeed. The core business—industrial steppers, servos, motion controllers sold into lithium battery, solar, 3C electronics, and general automation—generates cash and continues to compound at mid-teens rates. The humanoid bet is, in Warren Li's own framing, the company's third entrepreneurial journey. If it works, it transforms Leadshine from a Chinese industrial mid-cap into a global motion standard. If it does not work, the company continues to be a well-run, cash-generative motion control franchise. The asymmetry is what makes the story interesting.

With the strategic and operational picture in view, the question for a sophisticated investor is why this moat is defensible against both Chinese and global competition. The answer is a structural one.

VII. The 7 Powers and Porter's Five Forces Analysis

Hamilton Helmer's Seven Powers framework asks a deceptively simple question about any business: why can this company earn durably above its cost of capital? In Leadshine's case, three of the seven powers apply in ways that are worth walking through carefully, because they speak directly to the durability of the humanoid thesis.

Scale economies are the first and most obvious. Leadshine's dominance of the Chinese stepper motor drive market—roughly a third of domestic share by most industry counts—throws off the kind of cash flow that allows the company to fund ten-to-twelve percent of revenue on R&D year after year. A smaller player cannot afford to staff a dedicated humanoid robotics R&D team in Dongguan while also maintaining a competitive servo roadmap. A larger player, like Inovance, can afford it but has its strategic attention divided across large-format factory automation, industrial robotics, and electric vehicle powertrains. Leadshine occupies an unusual sweet spot: large enough to afford the R&D, focused enough to deploy it against a specific moonshot. Scale economies, in this sense, are less about unit cost advantages on any single product and more about R&D amortization across a growing portfolio of motion products that all share underlying motor and drive technology.

Switching costs are the second power, and they are deeper in motion control than many observers realize. The standard mental model of an industrial component supplier is that switching is easy—if Yaskawa raises prices, the OEM just buys the next motor from Panasonic. The reality is almost the opposite. Once an OEM—say, a lithium battery electrode coating machine builder—has integrated Leadshine's servo into its machine, the integration is rarely just mechanical. It includes tuning parameters captured in the company's configuration software, firmware hooks into the machine's HMI, support for specific communication protocols used in the customer's factories, and a set of service relationships built up over years of warranty claims and field support. To swap Leadshine for Yaskawa is not a component purchase; it is a multi-month engineering project involving redesigned brackets, reissued wiring diagrams, retrained service technicians, and requalification of every machine at every customer site. In practice, OEMs simply do not do it unless the incumbent supplier fails catastrophically. The higher up the value chain a supplier moves—from stepper to servo to integrated motion solution to humanoid joint module—the deeper those switching costs become. For a humanoid OEM, where the motion control layer is tightly integrated with the robot's real-time control stack, the switching cost is arguably as high as it gets in industrial components.

Cornered resource is the third and perhaps most under-appreciated power. The specific resource in question is talent. Motion control, and especially small-format high-torque motor design of the kind required for dexterous hands, is one of those niche disciplines where the relevant human capital is measured in hundreds of people globally, not thousands. Warren Li's MIT-to-Shenzhen pipeline, built over three decades of direct recruiting from Chinese top-tier universities and select overseas returnees, has aggregated a disproportionate share of that domestic talent inside a single company. Coreless brushless motor design specialists, firmware engineers who can hand-tune current loops in the low microsecond range, tactile sensor integration specialists—these are not people a competitor can simply hire by posting a job on LinkedIn. The cornered resource is not a patent portfolio, though the company has those. It is a multi-hundred-person engineering organization with a shared language, a shared tooling stack, and a shared set of unwritten problem-solving heuristics that took a generation to build.

Porter's Five Forces frames the same picture from the outside in. Bargaining power of buyers is high at the individual customer level—a major humanoid robotics OEM buys in volumes large enough to negotiate aggressively—but is muted by the systems-integration approach that transforms any component sale into a multi-year partnership. Bargaining power of suppliers has been partially neutralized by the HPMicro investment, which secured internal access to motor control silicon; the remaining raw material exposures (rare-earth magnets, copper) are commodity risks shared by the entire industry rather than company-specific vulnerabilities. Threat of new entrants is bifurcated: in low-end stepper drives, entrants are frequent but irrelevant, because the lower tier of the market does not compete for the humanoid customer. In the humanoid-capable tier, the combination of capital requirements, talent scarcity, and integration complexity creates an entry barrier that has, so far, kept the field of serious credible suppliers small. Rivalry among existing competitors is intense in servos, where Inovance and Estun fight for share every quarter, but much thinner in the humanoid motion component category where the credible domestic Chinese players can be counted on one hand and the global players (Maxon in Switzerland, Harmonic Drive in Japan) have historically been reluctant to move aggressively downstream into integrated dexterous-hand solutions. Substitutes—the fifth force—are essentially nonexistent at the dexterous-hand level; there is no alternative technology that replaces a multi-actuator robotic hand.

Pulling the two frameworks together yields a simple conclusion. The moat is not any single product. It is the interlocking combination of R&D-funded scale economies, deep customer-level switching costs, and a concentrated pool of motion control talent, operating in a market segment where credible substitutes and credible new entrants are both thin. That is the structural argument for why Leadshine is interesting. The question is what an investor does with it.

VIII. Playbook: Business and Investing Lessons

Step back from the company and three broader lessons emerge—lessons that apply not only to motion control and humanoid robotics but to the entire next decade of industrial technology investing.

The first lesson is that you do not have to build the robot to win the robot war. The technology industry has a persistent cognitive bias toward end-product companies. In every major platform shift, the retail investor gravitates toward the shiniest device maker—Apple in personal computing, Tesla in electric vehicles, OpenAI in large language models—and only belatedly discovers that most of the durable economic rent accrues to the component layer. Nvidia earned a trillion dollars of market capitalization not by building computers but by making the GPUs inside them. TSMC earned comparable wealth not by designing chips but by fabricating them. ASML earned its own not by making chips or computers but by making the lithography machines that make the machines. In each case the component vendor benefited from a structural advantage: as the end market fragments across competing product companies, the component vendor sells to all of them, capturing the aggregate growth of the category rather than the idiosyncratic fortunes of any single brand. Leadshine's positioning in motion control is an early-stage version of this pattern. Whether Tesla's Optimus, Figure's 03, or any of the Chinese humanoid platforms wins the end-product race, the underlying hand actuators, servo joints, and control electronics are coming from a small set of suppliers. Owning the "Nvidia of Motion" is a different trade than owning the "Tesla of Robots," and arguably a better one for an investor who is not certain which end product will dominate.

The second lesson is the quiet power of capital discipline in a boom market. It is almost axiomatic in industrial history that when a new technological wave arrives—internet, mobile, electric vehicles, now humanoid robotics—a flood of capital pours in, companies overbuild, and a brutal shakeout follows. The survivors are rarely the companies that grew fastest. They are the companies that grew sustainably, financed by reinvested profits rather than debt-fueled acquisitions. Leadshine's choice in the mid-2010s to invest upstream in chip design through a minority stake in HPMicro rather than paying a headline-grabbing premium for a foreign brand—as several Chinese industrial peers did in the same period—was a small decision that compounded into a large one. The company entered the 2020s with a clean balance sheet, meaningful cash reserves, and the ability to self-fund a five-hundred-million-renminbi capital expansion into humanoid components without stressing its capital structure. Capital discipline is the unsexy counterpart of R&D intensity. Both have to be present for a mid-cap industrial to make the leap into a new platform category. Either alone is insufficient.

The third lesson is the one that is hardest to observe from the outside: the founder's second act. The statistical base rate for a founder successfully leading a company through two complete platform transitions is low. The base rate for three transitions is vanishingly low. The vast majority of founder CEOs either exit, get replaced, or preside over gradual irrelevance as the technology they understood gives way to the technology they do not. Warren Li's trajectory—from stepper drives in the 1990s, to servos in the 2010s, to humanoid components in the 2020s—is rare, and it is worth asking why it worked. The honest answer appears to involve three factors. First, the founder's technical depth. A Ph.D. in robotics from the 1990s remains relevant to modern humanoid motion control in a way that, say, a marketing background would not. Li understands the math. He can evaluate a young engineer's current-loop tuning strategy on its merits, not on secondhand report. Second, the ownership structure. A forty-two percent family stake in a listed industrial company means no board is going to force a strategy change on time-series considerations. The company can take a decade to make a transition work. Third, the deliberate adoption of IPD and the recruitment of a younger generation of division-level leadership, which has allowed Li to shift from operational execution to strategic allocation without losing the company's technical identity. The founder's second (and third) act is not a matter of personal heroism. It is a matter of institutional architecture.

The KPIs worth watching for a long-term investor in Leadshine are fewer than one might expect. There are really only two that matter. The first is the humanoid segment revenue and its growth rate—whether disclosed explicitly or inferred from channel checks and order-book commentary. The segment going from a few percent of revenue to a double-digit share, on a company that is itself still growing, would validate the thesis. The second is gross margin, both at the consolidated level and, to the extent disclosed, in the robotics segment. Motion control companies that move up the value chain should see gross margins expand; those that fail to move up the stack see margins compress. If Leadshine's gross margin trends up over the next several reporting cycles, the strategic narrative is working. If it trends sideways or down, something is wrong. Beyond those two metrics—segment growth and gross margin—most other numbers are noise in the near term.

IX. Myth vs Reality and the Final Frame

Before closing, two myths worth dispelling.

The first myth is that Leadshine is a pure-play humanoid robotics company. It is not. The humanoid robotics division is the most interesting part of the company, and the one that is likely to determine investor returns at the margin, but the bulk of current revenue still comes from the industrial motion control business. Steppers, servos, and controllers sold into lithium-battery manufacturing, solar panel fabrication, 3C electronics assembly, textile machinery, packaging lines, and general CNC. This is a mature, cyclical, respectable business that grows in the mid-teens in good years and flat in bad years. Investors who enter the stock expecting humanoid purity will be disappointed by how much of the quarterly story is driven by Chinese capital expenditure cycles in battery and solar. The humanoid segment is the call option, not the underlying.

The second myth is that the dexterous hand category is wide-open greenfield. It is not. Global competitors are real and serious. Shadow Robot in the United Kingdom, Wonik Robotics in South Korea, and a handful of well-funded Chinese startups are all shipping dexterous hands. Harmonic Drive and Maxon supply high-end components to the same customers Leadshine serves. The moat is not that Leadshine is alone; the moat is that it has a larger integrated portfolio than any single specialist competitor, with upstream silicon access and downstream servo integration that most competitors lack. That is a different and more defensible claim than pure technical leadership.

With those caveats, the bull case resolves to something straightforward. Over a five-to-seven-year horizon, humanoid robotics transitions from a venture-funded curiosity to a meaningful industrial category, with shipments measured in the hundreds of thousands of units annually rather than thousands. The motion control layer of each robot—hands, joint modules, integrated drives—contains tens of thousands of renminbi of content. Leadshine, as one of a handful of credible Tier-1 suppliers globally, captures a meaningful share of that aggregate spend. Its humanoid segment scales from its current small base to a double-digit share of revenue, dragging the consolidated growth rate up and expanding gross margins as higher-value-added content displaces commodity drives. The company re-rates from a Chinese industrial mid-cap trading on mid-single-digit revenue multiples to something closer to a global technology franchise. In that world, the patient investor who bought in the mid-2020s is looking at a decade of compounding.

The bear case is, regrettably, equally straightforward. Geopolitics is the central risk. U.S. export control regimes have expanded steadily since 2018, and there is no structural reason they will not continue to expand into new categories of dual-use technology. Humanoid robotics sits uncomfortably at the intersection of industrial automation (which is largely unregulated), military robotics (which is heavily regulated), and advanced AI-adjacent hardware (which is increasingly scrutinized). If Western humanoid OEMs are restricted from sourcing critical motion components from Chinese suppliers, whether by executive order in Washington, by customer self-policing in California, or by supply-chain localization mandates in Europe, Leadshine's addressable market shrinks to the Chinese domestic humanoid ecosystem plus a handful of permissive export destinations. That is still a large market—China is likely to be the largest single humanoid market globally over the next decade—but it is not the global standard the bull case requires. A secondary bear case concerns execution risk. Humanoid OEMs could delay their commercial ramps, leaving Leadshine with an expensive Dongguan production base running well below capacity. Competition from global specialists could intensify. Rare-earth magnet costs could spike. Any of these would compress margins and extend the payback on the capital already deployed.

The cerebellum thesis, in the end, is a structural statement about where durable economic rent is likely to accrue in the humanoid economy, layered on top of a specific company's claim to occupy that position. Warren Li's bet, placed over thirty years and most heavily concentrated in the last three, is that motion control is hard enough, integrated enough, and talent-constrained enough to support a small number of highly profitable suppliers for a very long time. If he is right, Leadshine is exactly the kind of quiet, under-followed industrial franchise that compounding investors spend careers searching for. If he is wrong, the company remains a well-run Chinese motion control business. The asymmetry is the reason the story is worth telling. What happens next will be written one shipment of dexterous hands at a time, at a factory in Dongguan, by engineers whose names most investors will never learn.

X. Outro and Further Reading

For those who want to go deeper, several sources reward the time. Dr. Warren Li's academic publications from his MIT period and early Leadshine years, collected in various IEEE transactions on industrial electronics, remain the clearest statement of his technical philosophy on current-loop control. Leadshine's investor presentations from 2024 and 2025, available through the Shenzhen Stock Exchange disclosure portal, provide the most detailed publicly available view of the humanoid robotics segment strategy. Demonstration videos of the DH Series dexterous hand, circulated at Chinese robotics industry conferences and embedded in the company's corporate communications, offer a visceral sense of why the product is interesting in a way no analyst report can fully convey.

For context on the broader industrial backdrop, the "Made in China 2025" policy documents, while officially deprecated from Chinese government communications in the late 2010s, remain the clearest articulation of the industrial upgrading agenda that shaped two decades of capital formation in companies like Leadshine. Sinocism and Gavekal research have published extensively on the Chinese industrial technology stack. Hamilton Helmer's Seven Powers, long a reference point for strategic investors, provides the analytical vocabulary for thinking about durability in component-layer businesses. And for the pure-play humanoid robotics industry view, the ongoing coverage by Bernstein's industrial automation team and the specialist robotics trade press rewards attention.

The story of Leadshine is, in the end, a story of patience. A founder who spent a decade making stepper drives before anyone cared, another decade making servos before anyone noticed, and who is now, in his sixties, placing the largest bet of his career on a technology that may define the next generation of embodied intelligence. Whether that bet pays off in the form the bulls hope for, or falls victim to the geopolitical and execution risks the bears fear, the journey from a Nanshan dormitory to a Dongguan humanoid components base is one of the most interesting industrial biographies of the Chinese reform era. Whatever happens to the stock, the history is worth telling.

The cerebellum of the robot revolution may not have a household name yet. Give it a cycle or two.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube