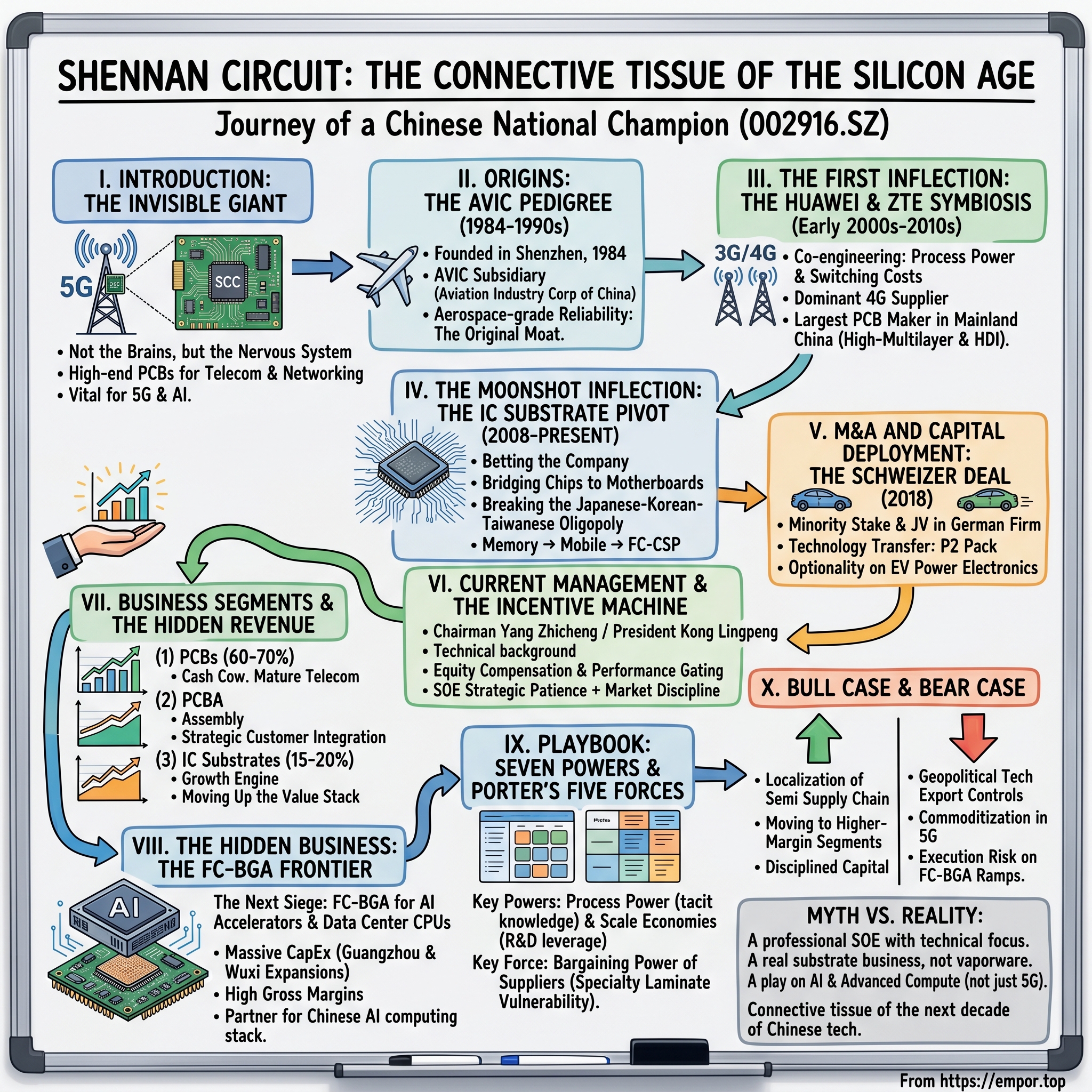

Shennan Circuit: The Connective Tissue of the Silicon Age

I. Introduction: The Invisible Giant

Walk into any teardown lab in Shenzhen, Hsinchu, or San Jose, and you will witness the same quiet ritual. An engineer pries open a 5G base station, a high-end networking switch, or an AI server motherboard, and what greets them first is not the silicon. It is not the Nvidia H-series chip glinting under the fluorescent light, nor the Intel Xeon with its dull metallic heatspreader. What greets them first is a slab of greenish-tan laminated material, perforated with thousands of precision-drilled holes, carrying copper traces thinner than a human hair across fourteen, eighteen, sometimes twenty-four stacked layers. That slab is a high-end printed circuit board. And in a shockingly high percentage of the world's most demanding telecom and networking hardware, the logo stamped discreetly in the corner reads "SCC"—Shennan Circuit.

This is the industry's dirty secret. Everyone obsesses over the "brains"—Nvidia's GPUs, Intel's CPUs, AMD's Epycs. Everyone genuflects before the "foundry"—TSMC's 3nm lines in Tainan, Samsung's fab in Pyeongtaek. But almost nobody outside the supply chain talks about the nervous system. The PCB and the IC substrate are the connective tissue that lets a chip talk to the world. Without them, the most advanced silicon is an inert block of sand. A 5G Massive MIMO antenna cannot beamform without a 20+ layer high-frequency PCB beneath it. An H100 GPU cannot route 80 billion transistors' worth of signals off-die without an ABF substrate pulling each electrical path out to the motherboard. The nervous system is not glamorous. But it is the physical precondition for the entire silicon age.

Shennan Circuit Company Limited, listed on the Shenzhen Stock Exchange as 002916.SZ, is the Chinese national champion in that nervous system. It is a company with a market capitalization north of $6 billion USD, revenue that crossed 17 billion RMB in recent years, and the rare distinction of being both an entrenched state-owned enterprise—a subsidiary of the AVIC aviation conglomerate—and a genuinely world-class tech manufacturer. It is the largest PCB maker in mainland China by revenue in the high-multilayer and HDI segments. It is the dominant supplier to Huawei's and ZTE's wireless base stations. And it is, at the time of this writing in April 2026, China's most credible shot at cracking the Japanese-Korean-Taiwanese oligopoly in IC packaging substrates, the most technically demanding segment in the entire PCB universe.

The roadmap ahead traces a forty-two-year arc. From a small workshop founded in 1984 inside a Shenzhen that was still mostly rice paddies and fishing villages, to a military-adjacent AVIC subsidiary quietly building aerospace-grade circuitry, to a strategic pivot into high-density interconnect boards just as Huawei and ZTE needed a local champion for 3G rollout, to a bet-the-company moonshot into IC substrates during the 2008 financial crisis, to today's high-stakes push into FC-BGA substrates—the packaging technology that sits underneath every hyperscaler's AI accelerator. It is a story of patience, state capital, process obsession, and one very large, very expensive, very multi-decade engineering siege. Let us begin where all good Chinese tech stories begin: with a parent company that almost no outsider understands.

II. Origins: The AVIC Pedigree

Picture Shenzhen in 1984. The Special Economic Zone was four years old. The population had not yet tripled. Deng Xiaoping had not yet made his famous Southern Tour. The whole city was a construction site, a policy experiment, a punt that Beijing had made on the idea that Chinese capitalism might work if you walled it off in one corner and gave it a running start. It was in this environment—part frontier, part laboratory—that a state-owned aviation conglomerate decided it needed a printed circuit board company.

The parent in question was AVIC, the Aviation Industry Corporation of China. To a Western reader, AVIC is usually filed mentally next to Boeing or Airbus—a maker of commercial and military aircraft. That framing is dangerously incomplete. AVIC is one of the half-dozen "backbone" central SOEs that function as vertically integrated industrial policy organs for the Chinese state. It builds fighter jets. It builds helicopters. It builds engines, avionics, landing gear, radar, and—critically for our story—every single electronic component that goes into those systems. When Beijing decided in the early 1980s that it needed indigenous capability across the entire aerospace electronics stack, it did not issue an RFP to third parties. It stood up subsidiaries.

Shennan Circuit was one of those subsidiaries. The logic was elemental. Aerospace-grade PCBs are not the cheap double-sided boards that go into a toaster. They must survive vibration, thermal cycling between minus-fifty and plus-one-hundred-fifty Celsius, electromagnetic interference from radar systems, and decades of operational life with near-zero field failure rates. IPC Class 3, the American specification for high-reliability military and aerospace electronics, is an order of magnitude more demanding than IPC Class 2, the standard for consumer goods. If you can build a PCB that can ride in a J-10 fighter jet, you can build anything.

That aerospace pedigree became the original moat. While the rest of the Shenzhen electronics boom was racing to the bottom of the cost curve—churning out low-layer-count boards for toys, calculators, and cheap consumer gadgets—Shennan was over in its own quiet corner, perfecting multilayer lamination, high-temperature solder mask formulations, and the kind of process controls that come from a QC culture where a single defect could, in theory, cause a pilot to die. That culture became an identity. When Huawei and ZTE came knocking in the mid-1990s looking for a reliable local partner, they found a company that already thought about reliability the way a cardiac surgeon thinks about sterility.

The 1980s and 1990s can be compressed for our purposes. Shennan was not, during those decades, a revenue giant. It was the steady hand in the corner—a technically serious outfit that accumulated quietly, bought equipment slowly, trained engineers patiently, and laid the groundwork for what would later become a three-pillar strategy: PCBs, PCB assembly (PCBA), and eventually IC substrates. Industry insiders came to refer to this as the "three-in-one" playbook, a phrase that would anchor every subsequent investor presentation. But in the 1990s, that future was not obvious. What was obvious was that Shenzhen was about to explode, and Shennan was positioned at the intersection of aerospace-grade discipline and commercial-grade ambition.

The real story begins when the dial-up modem generation ended and the mobile era began. Because the single most important fact about Shennan Circuit—the fact that explains almost everything else—is that its destiny was welded, beginning in the early 2000s, to a rising force on the other side of Shenzhen: a company called Huawei.

III. The First Inflection: The Huawei and ZTE Symbiosis

The story of Shennan's transformation from a respectable AVIC subsidiary into a national champion is, at its core, the story of two phone numbers on a Rolodex in the early 2000s. One belonged to Huawei, headquartered a twenty-minute drive away in Longgang District. The other belonged to ZTE, just up the road in Nanshan. Both companies were building the equipment that would, over the following two decades, underpin nearly every 3G, 4G, and 5G network across China and the developing world. And both companies had a problem: the PCBs they needed were getting fiendishly difficult to build.

Here is the technical reality that made this symbiosis inevitable. When a wireless carrier moves from 2G to 3G to 4G to 5G, the base station electronics do not merely get faster. They get denser, higher-frequency, and much more thermally hostile. A 2G base station's PCB might have six to eight copper layers stacked together, carrying signals at a few hundred megahertz, with trace spacing measured in comfortable fractions of a millimeter. A 5G Massive MIMO radio unit's PCB can have more than twenty layers, carrying millimeter-wave signals at tens of gigahertz, with trace spacing measured in micrometers, and doing so in a sealed enclosure mounted on a cellphone tower in the middle of the Gobi Desert at 45 degrees Celsius. The board has to work. For ten years. With no maintenance. The physics is brutal.

This is where the term "High-Density Interconnect," or HDI, enters the story. HDI is the PCB industry's answer to Moore's Law. Instead of fattening up traces and pads, HDI boards use microvias, laser-drilled holes only 75 to 100 micrometers in diameter, to stack connections vertically between layers. The result is a board that packs three times the routing density of conventional multilayer construction. HDI was a Japanese specialty in the 1990s. By the 2000s, Shennan had decided it was going to become a Chinese specialty too. They poured CapEx into laser drills, automatic optical inspection, and new lamination presses. They hired engineers out of AVIC's aerospace divisions who already understood the kind of tight-tolerance process control that HDI demanded.

The timing was providential. Huawei's first big 3G contracts—the European WCDMA deployments and the massive Chinese TD-SCDMA rollout—were coming online in the mid-2000s. ZTE was right behind, winning carrier business in emerging markets. Both companies needed HDI boards at volumes that the Japanese incumbents like CMK and Ibiden were either unwilling to meet or priced at a premium that would have eaten into Huawei's famous cost advantage. Shennan walked into the room with a value proposition that was almost impossible to refuse: aerospace-grade quality, Chinese pricing, and—this is the part that matters—co-engineering.

That word, co-engineering, is the key to understanding Shennan's strategic position. Shennan did not merely take blueprints from Huawei and manufacture to spec. Their engineers sat inside Huawei's R&D buildings during the critical early design phases, working out the stack-up—the specific sequence of dielectric and copper layers—that would allow a given radio unit to hit its signal integrity targets. They argued about laminate materials. They modeled thermal behavior. They fought over whether a particular high-speed differential pair could be routed on layer 8 or needed to move to layer 6. By the time the board went into production, Shennan's engineers often understood the RF physics of the final product better than Huawei's own PCB design team did.

This is what Hamilton Helmer, in his classic taxonomy of competitive advantages, calls "Process Power" intertwined with "Switching Costs." Once a telecom OEM has designed its next-generation base station around Shennan's specific stack-up capabilities, swapping to an alternative supplier is not a procurement decision. It is an engineering project that might take eighteen months and put the product's launch schedule at risk. That is not a relationship a rational purchasing department wants to disturb.

By the early 2010s, as the 4G rollout hit its stride, Shennan's communications PCB business had become one of the largest of its kind in the world. Huawei was reportedly a customer that, at various points, accounted for more than a quarter of Shennan's total revenue—a dangerous concentration on paper, but one that reflected genuine technical lock-in rather than mere commercial dependence. ZTE, Ericsson, Nokia, and Samsung Networks rounded out the top-tier customer list. Shennan had effectively become the global go-to supplier for the densest, most demanding telecom backplane and radio-unit boards in the industry.

But success in one technology cycle is the setup for a strategic problem in the next. By 2008, the smartest people inside Shennan were already asking themselves an uncomfortable question: what happens when 4G matures and the world moves on? That question led to the single most consequential capital allocation decision in the company's history.

IV. The Moonshot Inflection: The IC Substrate Pivot

Every truly great industrial company has a moment where a handful of leaders sit in a conference room, look at each other, and decide to bet the company on something that does not yet work. For Intel, it was the decision to abandon memory and become a microprocessor company. For TSMC, it was Morris Chang's decision to be a pure-play foundry. For Shennan Circuit, it was a series of decisions that began in 2008 and did not fully pay off for more than a decade. The bet had a name: IC substrates.

To appreciate what this meant, one has to understand a piece of electronics the non-specialist never thinks about. When a chip—a piece of silicon fabbed by TSMC or SMIC—leaves the fab, it is a tiny die, perhaps a few millimeters on a side, with hundreds or thousands of electrical contacts on its bottom surface spaced a few tens of micrometers apart. That spacing, in industry jargon "pitch," is far, far too fine to mate directly with a conventional PCB, which operates at a pitch ten to a hundred times coarser. You cannot solder a chip directly to a motherboard. Something has to bridge the two worlds. That something is the IC substrate.

Think of it as a miniaturized, ultra-high-precision PCB that lives underneath the silicon. On its top side, it accepts the microscopic contacts of the die. On its bottom side, it presents a grid of larger solder balls that can mate to a conventional motherboard. In between, it routes thousands of signals through layers so thin and so precisely aligned that the manufacturing process more closely resembles semiconductor fabrication than circuit board production. The best way to explain it to a layman: if a PCB is a highway system, an IC substrate is the interchange ramp that lets a bullet train merge into it. Without that ramp, the train is stranded.

In 2008, the global IC substrate market was effectively an oligopoly. Japan's Ibiden and Shinko Electric dominated high-end applications, particularly ABF (Ajinomoto Build-up Film) substrates for CPUs. South Korea's Samsung Electro-Mechanics and LG Innotek held the mid-tier. Taiwan's Unimicron and Kinsus rounded out the global top five. The Chinese mainland had essentially zero share of the advanced substrate market. Every IC substrate underneath every Chinese-designed chip was imported.

Shennan's leadership saw two things clearly. First, the global financial crisis had temporarily depressed CapEx spending across the semiconductor supply chain, which meant equipment could be bought on better terms. Second, if Shennan could become the first credible Chinese player in substrates, it would be positioned to ride whatever wave came next, whether that wave was smartphones, data centers, or something nobody had yet imagined. The board approved the initial investment. It was, by any measure, a bet.

The technical barrier turned out to be even steeper than anyone had feared. IC substrates are manufactured with line widths and spacings measured in fractions of the wavelengths used in advanced PCB production. The dielectric materials—ABF film, specialty resins, low-loss laminates—are sourced from a tiny handful of Japanese chemical companies and require deep process expertise to handle. Yield curves in substrate manufacturing are brutal: a single particle of dust in the wrong place, a single micrometer of misregistration between layers, and an entire panel is scrap. The industry lore, repeated at every substrate conference, is that it takes ten years from the first production line being installed to the first profitable, high-yield operation. That lore turned out to be accurate.

For most of the late 2000s and early 2010s, Shennan's substrate operation was, by the company's own admission in its annual reports, a drag on profitability. Memory substrates—the relatively simpler kind used for DRAM and NAND packages—came online first. Then modem and processor substrates for consumer applications. Then, slowly, the higher-end FC-CSP (flip-chip chip-scale package) substrates used in mobile processors. Each step required new equipment, new chemistry, new trained engineers, and another multi-year yield ramp. The capital expenditures were enormous. Investors, particularly in the run-up to Shennan's 2017 IPO on the Shenzhen exchange, sometimes questioned whether the substrate business would ever earn a respectable return on the billions of renminbi that had been plowed into it.

The breakthrough came in the mid-2010s and really consolidated only after the 2017 IPO gave the company access to a deeper pool of public capital. By then, Shennan had cracked FC-CSP at commercial yields. Chinese fabless chip designers—companies like HiSilicon, Unisoc, and eventually a crop of AI chip startups—were desperate for a domestic substrate supplier that could service their ramps without the geopolitical fragility of relying on Japanese, Korean, or Taiwanese sources. The 2019 US-China trade tensions, and particularly the export controls that began to throttle China's access to advanced semiconductor equipment, suddenly gave the substrate business a second kind of value: strategic insurance.

By the early 2020s, what had looked like an expensive distraction had become Shennan's most exciting growth engine. The company had succeeded in doing what almost no other player on the mainland had managed—building a genuinely world-class IC substrate business from scratch. The revenue contribution was still modest as a percentage of the whole. But the strategic significance, and the multi-year CAGR of that segment, was enormous. And it set the stage for an even more ambitious technical push that would define the late 2020s: the bet on FC-BGA.

Before we get to that, though, there is a deal from the tail end of this period worth examining in its own right. Because Shennan's pivot was not just organic. It was also, in one notable case, inorganic.

V. M&A and Capital Deployment: The Schweizer Deal

In December 2018, an announcement appeared on the Schweizer Electronic AG website in Schramberg, Germany—a small Black Forest town that has been synonymous with precision engineering for well over a century. Schweizer, a family-rooted PCB manufacturer specializing in power electronics for the European automotive industry, had agreed to sell a strategic stake to a Chinese partner. That partner was Shennan Circuit. Over the following months, the deal was structured in two parts: a direct equity investment that would give Shennan a large minority stake in the German parent, and a joint venture in China that would license Schweizer's core power-electronics technology for the Chinese market.

To understand why this deal mattered, you have to think about the PCB industry the way a chess player thinks about a middlegame. By 2018, Shennan had essentially checkmated the high-end Chinese telecom PCB market. Growth in that segment would track 5G CapEx, which everyone knew was going to be enormous but also cyclical. The smartest move was to diversify into an adjacent, secular-growth PCB vertical that would not rise and fall with base station orders. The obvious candidate was automotive electronics, and within automotive, the hot subsegment was the electrification transition: power PCBs for inverters, battery management systems, on-board chargers, and the whole stack of components that separate an electric vehicle from a combustion one.

Schweizer's crown-jewel technology was something called "P2 Pack," an embedded die package for power semiconductors. In plain language: instead of soldering a power transistor onto a PCB's surface, P2 Pack embeds the bare silicon die directly inside the PCB's copper layers. This approach dramatically reduces parasitic inductance, improves thermal dissipation, and allows for much higher power densities in automotive inverters. It was, by 2018, considered one of the most promising packaging architectures for next-generation EV powertrains. And Schweizer, for all its technical brilliance, lacked the scale and the customer base to deploy it at the volumes that would justify its ongoing R&D.

Enter Shennan. The deal that emerged was, in retrospect, a textbook example of capital-efficient technology transfer. Shennan took a meaningful minority stake in the German parent—reportedly around the 20-plus percent level, enough to get a seat at the table but not enough to trigger the kind of political blowback that full acquisitions of German "Mittelstand" champions had increasingly attracted in the late 2010s. The Chinese JV gave Shennan the ability to manufacture P2 Pack and related embedded-die PCBs at scale inside China, targeting Chinese EV OEMs that were, at that moment, entering their own hockey-stick growth phase.

Did Shennan overpay? The question has been debated inside industry circles ever since. On a pure multiples basis, the valuation Shennan paid for its Schweizer stake was, by most accounts, above the prevailing PCB industry multiple. But that comparison misses the point. Shennan was not buying a PCB company. It was buying optionality on a specific technology platform that could plausibly become the dominant power-electronics packaging architecture of the 2030s. If you benchmark against what Unimicron, the Taiwanese peer, had spent on organic capacity expansions in the same window, or against what Japanese peers were paying for minority stakes in battery-component suppliers, the Schweizer price looks defensible. If P2 Pack wins out over competing architectures, Shennan will have bought a foothold in the EV power-electronics value chain at a bargain. If it loses, Shennan will have paid for an expensive hedge.

The deal also illustrated something important about Shennan's broader playbook on capital deployment. The company has consistently preferred minority stakes, joint ventures, and licensed manufacturing rights over full acquisitions of Western companies. This is partly pragmatic—full acquisitions trigger CFIUS-style regulatory reviews, management integration headaches, and the inevitable cultural friction of a Chinese SOE trying to digest a European Mittelstand firm. But it is also philosophically consistent with how Shennan has always thought about its role: as a bridge, not a conqueror. Import the IP, pair it with Chinese scale, build the domestic franchise, and let the Western partner keep doing what it does best in its home market.

It is a classic capital-light approach to technology acquisition, and it sits in striking contrast to the splashier cross-border deals that dominated Chinese outbound M&A headlines in the mid-2010s. You can argue about whether the strategy maximizes upside. You cannot argue that it has been capital-efficient. The Schweizer deal, more than five years after its announcement, remains one of the cleanest case studies of how a Chinese industrial champion has used minority stakes to accelerate its technical roadmap without overextending its balance sheet.

This strategic patience bears the fingerprint of a specific kind of leadership. Which brings us to the people currently running the company.

VI. Current Management and the Incentive Machine

The stereotype of a Chinese state-owned enterprise executive, deeply embedded in Western business literature, is an unflattering one. The caricature is of a Party-appointed apparatchik, more concerned with internal politics than with operational excellence, rotated in and out on three-to-five-year cycles, with minimal personal financial stake in the company's long-term performance. That stereotype is, in many SOEs, painfully accurate. It is also, as applied to Shennan Circuit, quite badly wrong.

Chairman Yang Zhicheng and President Kong Lingpeng are the current custodians of the "professional SOE" paradox that Shennan has come to embody. Yang, who assumed the chairmanship in the late 2010s, has a background that reads more like a semiconductor industry resume than a typical SOE career path. He came up through AVIC's electronics divisions, spent years running operations rather than finance or HR, and is known within the industry as someone who can walk a fab floor and actually talk intelligently about wet-process chemistry. Kong Lingpeng, as president and chief operating force, has a similar pedigree: deep technical grounding, long tenure inside the company, and a reputation for being obsessed with yield and capacity planning rather than with the corporate politics that often consume SOE executives.

The more important signal, though, is not the biographies. It is the incentive structure. In 2021, Shennan launched its first major stock option incentive plan, granting options to several hundred core technical and management employees. Then in 2023, the company launched a second, larger round, extending the program to more employees and at more aggressive performance vesting thresholds. The vesting triggers were tied to specific revenue and profit growth targets, year over year, across multiple years, with a particular emphasis on the high-end product mix shift—meaning executives could only fully vest if the company demonstrably migrated revenue up the technology stack into IC substrates and FC-BGA, not just by growing commodity PCB volume.

This kind of performance-gated equity compensation is not unusual in Western tech firms. It is quite unusual in Chinese SOEs, where state-ownership regulations have historically made large equity grants to professional managers both legally complex and politically sensitive. Shennan's willingness to push through two rounds of such programs—and to structure them with genuine operational teeth rather than as soft-target rubber stamps—tells you something important about how the company is being governed. Skin in the game, in the phrase that Nassim Taleb made famous, actually exists here.

The ownership structure reinforces the point. AVIC International, the direct parent, holds something in the neighborhood of a 60-percent controlling stake. That is the floor of state control, the part that is not going anywhere. But the remaining float is disproportionately owned not by retail investors or speculative hot money, but by a deep bench of institutional investors—public mutual funds, insurance companies, the "national team" sovereign funds, and a rotating cast of QFII and Northbound Connect foreign institutional accounts that flows through the Shenzhen-Hong Kong Stock Connect. The presence of this "smart money" float is not decorative. It means management faces real scrutiny at every quarterly earnings call, every annual general meeting, every analyst day. The public funds that dominate A-share institutional ownership in the semiconductor supply chain—firms like E Fund, China AMC, and the specialist tech funds—have been known to dump positions rapidly when SOE management disappoints on execution.

What you end up with, then, is an unusual hybrid. A state-owned majority owner who provides strategic patience and access to policy tailwinds. A professional management team with technical credibility and performance-vesting equity. A sophisticated institutional minority shareholder base that keeps quarterly discipline honest. And a board that has been willing to approve the kind of multi-decade CapEx commitments—substrate lines cost hundreds of millions of dollars each—that would be impossible in a pure private-equity-funded competitor operating on a shorter time horizon.

It is, in short, a governance structure that is almost custom-built for the kind of patient, capital-intensive, multi-generational technology build-out that an IC substrate business requires. Which is convenient, because the next chapter of Shennan's story requires even more of that patience and capital than anything that has come before.

VII. The Hidden Business: The FC-BGA Frontier

Let us slow down and really break apart how this company makes money today, because the reported segment mix tells a deliberately simple story that can obscure the much more interesting strategic dynamics underneath.

The first and largest segment is printed circuit boards, the core PCB business. By revenue, this accounts for somewhere between 60 and 70 percent of the total. Within that, the largest subsegment is still communications infrastructure—the backplanes, radio units, and switching boards for 5G base stations and high-end networking equipment. That subsegment is, bluntly, mature. Chinese 5G build-out has passed its peak-CapEx year. Global 5G CapEx has peaked and is working through the digestion phase. Growth in this bucket, over the next few years, will be more about mix enrichment—moving into higher-layer-count, higher-frequency, higher-ASP boards for 5G-Advanced and eventual 6G programs—than about unit volume. The PCB business is, in Acquired-speak, the Cash Cow. It generates stable, high-absolute-profit cash that funds everything else.

The second segment is PCBA, or printed circuit board assembly. This is the business of taking a bare PCB, loading it up with components—the ICs, the capacitors, the connectors—and delivering a finished functional module to the customer. Margins in PCBA are structurally lower than in bare-board manufacturing, but the business is strategically valuable because it deepens customer integration. An OEM that buys both the PCB and the assembled module from the same supplier is much less likely to switch, because doing so would require unpicking two tightly coupled manufacturing flows rather than just one. Think of PCBA as the service layer wrapped around the product.

The third segment, and the one that ought to command the most attention from long-term investors, is IC substrates. As of the most recent public disclosures, this segment accounted for roughly 15 to 20 percent of total revenue, but it has been compounding at a growth rate that is multiples of the overall company growth rate. Inside the substrate bucket, the mix has been moving aggressively from simpler memory substrates toward more complex FC-CSP products used in mobile application processors, and now toward the next frontier, which is FC-BGA.

FC-BGA—Flip Chip Ball Grid Array—is the most technically demanding class of packaging substrate in the industry. It is what sits underneath a high-end CPU, GPU, or AI accelerator. An Nvidia H100 data-center GPU has an FC-BGA substrate. An Intel Xeon CPU has an FC-BGA substrate. The AMD Epyc that powers a hyperscaler's database tier has an FC-BGA substrate. The industry is currently in the middle of a multi-year capacity shortage in FC-BGA, driven by the explosion in AI accelerator demand and compounded by the fact that only a tiny handful of global players—Ibiden, Shinko, Samsung Electro-Mechanics, AT&S, and Unimicron—have the process expertise and installed capacity to supply it.

Shennan has publicly announced, and begun executing, a large-scale capital investment plan to enter FC-BGA at commercial scale. The Guangzhou and Wuxi expansions together represent the biggest single CapEx commitment in the company's history. Pilot lines were running. Customer qualification with domestic Chinese fabless chip designers—particularly those working on AI accelerators, switch ASICs, and data-center CPUs—has been in progress. The company's stated ambition, and the thing that makes this story so interesting, is that Shennan is trying to become the first viable mainland Chinese supplier of FC-BGA substrates for the domestic AI chip ecosystem.

The narrative implication here is massive. For the first three decades of its existence, Shennan's pitch was: we are the best Chinese PCB supplier for Chinese telecom equipment. In the late 2010s, the pitch evolved to: we are the first viable Chinese substrate supplier. Now, with the FC-BGA push, the pitch has become: we are the foundational infrastructure partner for the Chinese AI computing stack. That is a different kind of company. It is a company that, if it executes, will be on the critical path for every Chinese hyperscaler and every Chinese AI chip startup for the next decade and beyond.

The execution risk is real. FC-BGA yield ramps are famously painful. Established competitors have multi-decade head starts. The equipment supply chain for the most advanced FC-BGA production flows through Japanese and European vendors who are themselves subject to increasingly complex export-control regimes. Customer qualification timelines run eighteen to thirty-six months from first pilot production to full-volume ramp. None of this will be fast. None of this is guaranteed. But the prize—a seat at the table of the global substrate oligopoly, with the backing of a Chinese state apparatus that has identified semiconductor localization as a top-tier strategic priority—is roughly as big as any prize that exists in this industry.

The economic model is also worth pausing on. FC-BGA substrates carry gross margins that are typically two to three times those of high-end PCBs. If Shennan successfully ramps FC-BGA volume while its cash-cow PCB business remains stable, the mix-shift effect on overall company profitability could be substantial. That is the key KPI frame through which investors should think about the next several years.

With the segmentation laid out, it is worth stepping back and asking the structural question: why is any of this defensible?

VIII. Playbook: Seven Powers and Five Forces

Hamilton Helmer's Seven Powers framework is, for good reason, the lens that Acquired listeners reach for when analyzing a durable business. Applied to Shennan, two of the seven powers stand out as genuinely load-bearing.

The first is what Helmer calls Process Power—the tacit knowledge embedded in how the organization actually does its work, knowledge that cannot be replicated by pouring capital into the problem. In IC substrate manufacturing, this power is not an abstraction. It is chemistry, metallurgy, microfabrication, and defectivity control wrapped into a body of operational know-how that accumulates one failed yield ramp at a time. The Japanese incumbents have been refining this process knowledge since the 1980s. Shennan has been at it for nearly two decades now. Every one of those years adds another incremental understanding of how to tune a specific chemical bath, how to register successive build-up layers with submicrometer precision, how to manage thermal stress during cure cycles. A new entrant cannot buy this. They have to live it.

The second is Scale Economies—not in the commodity sense of "we are bigger and therefore cheaper per unit," but in the more interesting R&D-leverage sense. The Wuxi and Nantong smart-factory complexes give Shennan something that almost no other Chinese peer can match: enough high-end PCB and substrate production volume to spread a very large, very specialized R&D organization across a cost-per-board that remains competitive. When Shennan's engineers solve a signal-integrity problem on a 24-layer Huawei backplane, the learning can be propagated across hundreds of thousands of boards annually. A smaller competitor making ten thousand of the same board has to amortize equivalent R&D against a tenth the revenue. Compounded over a decade, that gap becomes unbridgeable.

The other Seven Powers apply in muted form. Switching Costs exist for Shennan's deeply-integrated telecom customers, as we discussed, but they are somewhat lower for commodity PCB customers. Network Economies do not really apply in manufacturing. Counter-Positioning is probably not the right frame—Shennan is the incumbent, not the disruptor. Cornered Resource arguably applies in the sense that Shennan has exclusive access to certain advanced Japanese and European laminate and equipment suppliers under long-term agreements, but this is closer to Process Power than to a clean Cornered Resource. Brand is essentially irrelevant in an industrial-components market. So the real answer is: Process Power and Scale Economies, stacked on top of each other.

Porter's Five Forces add another layer of analytical clarity. Consider each in turn.

Bargaining Power of Buyers is high, at least in theory. Shennan's largest customers—Huawei, ZTE, Ericsson, Samsung Networks, and the emerging Chinese AI chip designers—are themselves enormous, technically sophisticated organizations with the ability to dual-source and to pressure on price. But the counterweight is that on the most advanced specs, Shennan is often the only qualified supplier at the required volume, or one of only two. Sole-sourcing or dual-sourcing relationships on critical boards attenuate buyer power substantially. A purchasing manager at Huawei cannot, realistically, tell Shennan to cut prices by 15 percent and find an alternative next month for a 22-layer 5G massive MIMO board.

Bargaining Power of Suppliers is more concerning. The specialty laminates used in high-end PCBs and substrates—particularly ABF film from Ajinomoto and low-loss materials from Japanese chemical majors—come from a tiny number of global suppliers. Copper foil for high-frequency applications is similarly concentrated. This is a real input-cost vulnerability that investors should monitor, especially in years where geopolitical friction raises the risk of export controls flowing the other direction—Japanese chemical suppliers constrained in what they can ship to Chinese buyers. Shennan has been working to localize some of this input supply chain, but progress is uneven.

Threat of New Entrants is near zero for IC substrates and FC-BGA. The entry ticket, in pure capital terms, exceeds 500 million dollars for a production-capable substrate facility. The yield-ramp clock is measured in years. The equipment is export-controlled. The customer qualification gauntlet takes eighteen to thirty-six months minimum. For standard multilayer PCBs, new entrants are a constant factor, but Shennan's product mix has deliberately shifted away from the segments where that threat is live.

Threat of Substitutes is intriguing. In theory, advanced packaging technologies—chiplet architectures, silicon interposers, fan-out wafer-level packaging—could cannibalize parts of the traditional substrate market. In practice, these technologies have so far expanded the packaging substrate TAM rather than contracted it, because high-performance chiplet designs actually require more substrate area, not less. But this is a five-to-ten-year watch item.

Industry Rivalry is intense at the commodity end of PCBs and more rational at the substrate end, where the oligopoly of five or six global players keeps competition disciplined. Shennan's strategic migration up the value stack is, in large part, a migration from high-rivalry commodity competition into more consolidated, higher-margin oligopoly dynamics.

Stack these two frameworks on top of each other and the picture is: a defensible franchise in high-end PCBs, a genuinely world-class emerging franchise in IC substrates, some input-cost vulnerability that is manageable but worth monitoring, and a multi-year runway into FC-BGA that, if executed, reinforces every one of these competitive advantages. It is not a perfect business. But it is a business with real, durable, understandable economic power.

Which does not mean there are no risks. There are big ones, and they deserve their own accounting.

IX. The Bull Case and the Bear Case

Start with the bear case, because the bear case for Shennan is genuinely serious and not a caricature.

The first bear argument is geopolitical. Shennan's whole strategic premise—that it will become the indispensable substrate supplier to the Chinese AI and advanced computing stack—depends on there being a Chinese AI and advanced computing stack worth supplying. If US export controls successfully throttle the flow of advanced semiconductor manufacturing equipment, EDA software, and high-end chip designs into China to the point where the domestic ecosystem cannot produce competitive AI accelerators, then the addressable market for Shennan's FC-BGA substrates collapses. You can have the best substrate in China, but if nobody in China is designing a chip that needs a world-class FC-BGA, you are stuck selling it to a much smaller, much slower-growing customer base. This risk is real, and it has tightened rather than loosened over the past several years.

The second bear argument is commoditization at the base of the stack. 5G infrastructure CapEx has peaked globally. Telecom equipment OEMs are entering a digestion phase. The next wireless generation, whatever it turns out to be, will not likely hit significant CapEx deployment until the end of the decade. In the interim, Shennan's large, high-margin telecom PCB business faces a period of single-digit volume growth and potentially compressing margins as competitors chase share. The cash cow may, for a period, produce less cash than it has historically.

The third bear argument is execution risk on FC-BGA itself. This story has been told too many times before in too many industries—a challenger spends tens of billions of renminbi trying to enter a complex, yield-driven oligopoly, only to find that the incumbents' decade-plus process advantage cannot be closed with capital alone. The graveyard of Chinese semiconductor ambitions is populated with companies that raised huge sums, built impressive-looking fabs, and then stalled at subscale yields. Shennan's track record in IC substrates generally gives confidence that they know how to grind through these ramps. But FC-BGA is genuinely harder than anything they have done before, and the timeline from pilot to competitive full-volume production is still a multi-year road with real cliffs.

The fourth bear argument is input dependency. The specialty chemistry and equipment that underpin advanced substrate production flow through Japanese, Korean, Taiwanese, and European suppliers. If those supply lines are constrained by future export controls running the other direction—restrictions on high-end laminate shipments to Chinese substrate makers, for example—Shennan's ramp could be bottlenecked by factors outside its control.

Now the bull case. The bull case is, in the largest sense, a thesis about Chinese semiconductor localization. For more than two decades, China has been the world's largest end consumer of PCBs and a massive consumer of IC substrates. Until very recently, the advanced end of that supply chain was dominated by non-Chinese players, and China's own contribution was concentrated at the lower-value tail. Both economic policy and geopolitical pressure have converged on the same verdict: this has to change. And Shennan is, unambiguously, the national champion positioned to capture that shift.

If even half of the advanced PCB and substrate demand currently flowing through non-Chinese suppliers to Chinese end customers were to shift domestically over the coming decade, the revenue opportunity for a company like Shennan would be enormous. Even more importantly, a fragmenting world in which the US, EU, Japanese, and Chinese supply chains increasingly decouple does not mean Shennan has no market. It means Shennan has the Chinese market, which is the biggest market. And that market, via its domestic AI chip designers, its EV power-electronics OEMs, its 5G and emerging 6G telecom equipment makers, and its data-center hyperscalers, is one of the great secular growth opportunities of the era.

A second leg of the bull case is the product mix shift. Each renminbi of revenue that migrates from commodity PCB to IC substrate to FC-BGA carries structurally higher gross margin. If Shennan successfully grows the high-margin segments while the commodity segments remain stable, the earnings geared effect over a five-year horizon is substantial. This is not a trick of financial engineering. It is the natural consequence of moving up a technology curve where the incumbent margins are real and defensible.

A third leg is capital discipline. Unlike some of its Chinese semiconductor peers that have grown via aggressive, state-subsidized, debt-financed expansions, Shennan has generally run a more conservative balance sheet. Internally generated cash flow, supplemented by the 2017 IPO proceeds and measured use of private placements, has funded the bulk of the CapEx. This disciplined profile means Shennan can weather the inevitable cyclical downturns without facing the kind of refinancing crises that have bedeviled less well-capitalized competitors.

Weighing these, the bull and bear cases really turn on one question: how much of the grand Chinese semiconductor localization story is real, and how much is wishful thinking colliding with export controls? Reasonable analysts can disagree. But one thing is not really in dispute: if the localization thesis plays out, Shennan is positioned as well as any company on the mainland to capture the resulting value.

A quick aside on the diligence overlays worth keeping an ear open for. Accounting-wise, watch capitalized versus expensed R&D treatment as substrate capacity ramps—aggressive capitalization can flatter near-term earnings. Watch the depreciation schedules on the new FC-BGA lines, which carry very long useful-life assumptions that can create lumpy gross-margin dynamics. Watch related-party transactions through the AVIC parent ecosystem, which are modest in scale but non-trivial. On regulatory, watch for any tightening of Japanese or European laminate and equipment export license approvals, which would surface first as capacity-ramp guidance revisions rather than as a headline event. On institutional ownership, Northbound Connect holdings have been a decent leading indicator of foreign-institutional sentiment shifts; meaningful outflows or inflows in that channel often precede re-ratings. None of these by itself rewrites the investment story, but each is worth a glance at each quarterly result.

For a long-term investor trying to keep a single scorecard, three KPIs arguably matter most. The first is IC substrate revenue growth rate, quarter over quarter and year over year, because that segment is the center of gravity for any bull thesis. The second is the ratio of high-end product mix within the core PCB segment—specifically, the revenue contribution from sub-segments like 5G backplane and high-speed networking boards versus lower-layer-count commodity work, because that mix governs the PCB cash cow's margin trajectory. The third is the gross margin trajectory at the consolidated level, because if the mix shift story is real and well-executed, it will show up first and cleanest in consolidated gross margin line. Everything else—CapEx cadence, customer announcements, incentive plan vestings—is colorful context that ultimately validates or invalidates those three numbers.

X. Myth Versus Reality and Final Thoughts

Every company accumulates a cloud of consensus narratives, and the ones around Shennan are worth checking against reality.

The first common myth: "Shennan is just another opaque Chinese SOE, with governance that can't be trusted." Reality: Shennan is a majority state-owned company, yes, but its governance profile—two major employee stock option rounds, institutionally-heavy minority ownership, professional management with deep technical backgrounds, disclosure quality that generally meets or exceeds Chinese A-share norms—is closer to a Western industrial manufacturer than to the stereotypical SOE. That does not eliminate SOE risk. It does mean the company should not be automatically lumped into that bucket without a look at the specifics.

The second common myth: "Shennan's IC substrate business is just a marketing story; they haven't really cracked the technology." Reality: the substrate business has been shipping in commercial volumes for years, at yields and margins that generate meaningful profit contribution. The question about FC-BGA specifically is still open, but the memory and FC-CSP business is a done deal. This is a real operating business, not a vaporware pivot.

The third common myth: "Shennan is a play on 5G CapEx." Reality: it was, historically, and that remains an important revenue contributor. But the incremental dollar of value being created in the business is increasingly in IC substrates and EV power electronics. Analyzing Shennan purely through the lens of 5G spending cycles misses most of the interesting dynamics.

The fourth common myth: "The Schweizer deal was a desperate grab for German technology." Reality: it was a carefully structured minority-stake-plus-JV transaction that represents the company's broader philosophy on technology acquisition—import IP via minority positions, scale it through Chinese JVs, avoid the geopolitical flak that comes with full acquisitions.

So what to take away from all this.

Shennan Circuit's story is, at its heart, the story of a company that used a boring, high-reliability, commodity-adjacent business—printed circuit boards for telecom equipment—to fund a decade-long, capital-intensive R&D siege on the hardest problem in its industry. The siege was IC substrates. The siege mostly succeeded. And now that success is being used to fund the next, even more ambitious siege: FC-BGA for the Chinese AI and advanced computing stack.

In the language of Acquired, this is a company that married Scale Economies and Process Power to build a durable franchise in one industry, then used the cash flow from that franchise to tunnel into a second, higher-margin, higher-defensibility adjacent industry. It is the industrial-manufacturing equivalent of what semiconductor companies did when they went from memory to logic, or what media companies did when they went from linear broadcast to streaming. The move is expensive, slow, uncertain, and when it works it creates enormously more value than the original business ever could have on its own.

The legacy of this forty-two-year arc is that Shennan is no longer primarily an aviation-conglomerate electronics subsidiary, whatever its ownership structure formally says. It is the connective tissue, the nervous system, the physical substrate upon which the next decade of Chinese AI computing, Chinese electric vehicle power electronics, and Chinese advanced telecom infrastructure will be built. For long-term fundamental investors trying to understand what the Chinese semiconductor supply chain will look like in 2030, Shennan Circuit is not a name you can afford to skip past. Whether the story plays out as the bulls hope or stumbles under the weight of the bears' concerns, it will be told in every earnings call, every capacity announcement, and every yield milestone at Wuxi, Nantong, and Guangzhou over the coming years.

The silicon age has always had its famous names—the designers and the foundries that dominate magazine covers and earnings headlines. The nervous system that lets all of that silicon do useful work has always been, and probably always will be, unfamous. But unfamous is not the same as unimportant. And Shennan Circuit, for anyone willing to look past the familiar names, is quietly becoming one of the more important industrial stories of its generation.

XI. Top 5 Further Reading Links

- Prismark PCB Industry Reports — the gold-standard global benchmark on PCB and substrate market sizing, end-market segmentation, and competitive positioning.

- Shennan Circuit Annual Report (most recent fiscal year) — the essential primary-source read on FC-BGA capacity plans, segment contribution breakdowns, and management's own stated roadmap.

- History of AVIC International Technology Spin-offs — broader context on how the AVIC conglomerate structures its relationships with listed subsidiaries and what that implies for governance.

- IPC Standard 6012 — the industry specification that defines the reliability classes Shennan's boards are built to, and a useful technical grounding in what makes high-reliability PCB manufacturing genuinely difficult.

- Case Studies on the Schweizer-Shennan Partnership — industry analyst write-ups of the P2 Pack embedded-die technology transfer and its implications for the global EV power-electronics value chain.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube