BYD: The Vertical Integration Superpower

I. Introduction: The 2024 Crossover

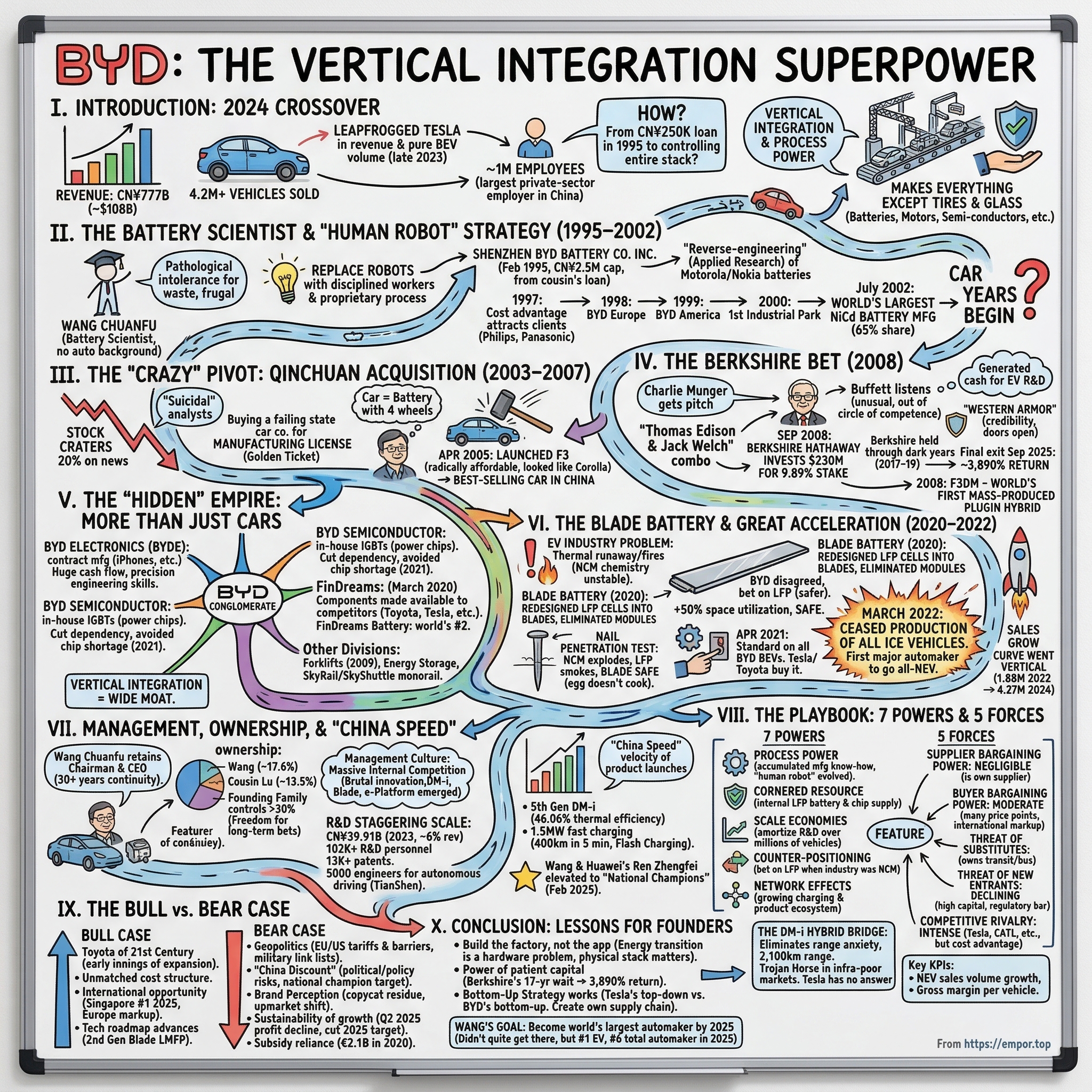

Somewhere in late 2023, a quiet threshold was crossed. A company that most Americans could not identify on a highway — whose name, "Build Your Dreams," sounds like a motivational poster — officially leapfrogged Tesla in both revenue and pure battery electric vehicle volume. By the time the final 2024 numbers landed, BYD had posted CN¥777 billion in revenue (roughly $108 billion), sold over 4.2 million vehicles, and employed nearly a million people. That last figure alone makes BYD the largest private-sector employer in China and nearly triple the headcount of Toyota.

The question this article sets out to answer is deceptively simple: How did a chemistry professor with no automotive background, starting with a CN¥250,000 loan from his cousin in 1995, build a company that now controls the entire stack of the modern energy economy — from the lithium in the battery cell to the semiconductor chips on the circuit board, from the monoblock transit system overhead to the electric bus in the depot below?

The answer is not a car story. It is a story about the ultimate application of process power and vertical integration — two concepts that the business strategy world talks about in abstract terms but that Wang Chuanfu turned into a living, breathing industrial machine. BYD makes everything except the tires and the glass. They make the batteries, the motors, the semiconductors, the power electronics, the body panels, the interior lighting, the software, and even the transit systems that compete with their own cars for passengers. When the global chip shortage of 2021 brought Tesla and Ford to their knees, BYD accelerated. They had their own chip fabs.

The arc of this story runs from "shameless" reverse-engineering of Motorola cell phone batteries in a Shenzhen workshop to the Blade Battery — a piece of technology so good that Tesla, BYD's greatest rival, now buys it for their own vehicles. Along the way, we will encounter Charlie Munger calling Wang Chuanfu "a combination of Thomas Edison and Jack Welch," a stock-price collapse that nearly killed the company, a sledgehammer taken to a prototype car, and a single strategic decision in March 2022 that may prove to be the most consequential bet in modern automotive history.

This is the story of BYD.

II. The Battery Scientist and the "Human Robot" Strategy (1995–2002)

Wang Chuanfu was born on April 8, 1966, in Wuwei County, Anhui Province — deep in rural China, the kind of place where farming was not a lifestyle choice but an economic sentence. He was one of eight children. Both of his parents died during his youth. His elder brother and sister essentially raised him, scraping together enough to keep him in school. That biographical detail matters because it explains something fundamental about the man: an almost pathological intolerance for waste, a frugality that persists to this day even as his net worth hovers in the tens of billions of dollars. He still wears a $15 company uniform. He still flies economy class. He still eats in the factory cafeteria.

Wang earned his bachelor's degree in metallurgical physical chemistry from Central South University in 1987 and a master's from the Beijing Non-Ferrous Metal General Research Institute (GRINM) in 1990. By 1993, at the age of twenty-seven, he had been appointed general manager of BAK Battery, a subsidiary established by his research institute in Shenzhen. It was a good job. It was a government-affiliated position with stability and prestige. And Wang left it two years later to start his own company with borrowed money.

The insight that drove him out the door was breathtakingly simple. In the mid-1990s, Japanese giants — Sony, Sanyo, Matsushita — dominated the global rechargeable battery market. Their manufacturing process relied on multi-million-dollar automated clean rooms, robotic assembly lines, and capital expenditures that no Chinese startup could dream of matching. The conventional wisdom was clear: you needed expensive robots to make batteries. Wang looked at the problem differently. He realized he could replace a $10 million robot with fifty highly disciplined workers and a proprietary chemical process. The workers would perform the same repetitive tasks, but in a semi-automated environment that cost a fraction of the Japanese setup. He called this the "human robot" strategy, and it was not a euphemism for exploitation — it was a genuine manufacturing innovation. By combining cheap labor with clever process engineering, Wang could undercut Japanese battery prices by eighty percent while maintaining comparable quality.

On November 18, 1994, Wang gathered twenty people in Buji Town, Longgang District, Shenzhen. On February 10, 1995, Shenzhen BYD Battery Company Limited was formally incorporated with CN¥2.5 million in capital — most of it the CN¥250,000 loan from his cousin Lu Xiangyang, who would become one of the wealthiest people in China on the strength of that bet. The company started with nickel-cadmium batteries and a single, consuming ambition: take market share from the Japanese.

What happened next was pure execution. BYD took apart Motorola and Nokia batteries — literally disassembling them, analyzing the chemistry, studying the form factor. Critics called it reverse engineering. Wang preferred to think of it as applied research. His famous quote on the subject was characteristically blunt: "In developing a new product, sixty percent comes from existing literature, thirty percent from sample analysis, and another five percent from raw materials and other external factors. Our own original research accounts for only about five percent." The genius was not in the chemistry — it was in the manufacturing process that made the chemistry commercially viable at scale.

By 1996, BYD had secured its first order from Sanyo — selling batteries to one of the very companies it was trying to displace. When the 1997 Asian financial crisis cratered the global electronics supply chain, BYD's cost advantage became irresistible. Philips, Panasonic, and Motorola all became major clients. The crisis that destroyed competitors became BYD's accelerant.

In 1998, BYD opened its first overseas branch — BYD Europe B.V. in the Netherlands. In 1999, BYD America Corporation was established. By 2000, the company had opened its first industrial park in Kuichong, Shenzhen. And by July 2002, BYD had become the world's largest nickel-cadmium battery manufacturer, controlling sixty-five percent of global production and surpassing Sanyo — the same company that had placed BYD's first order six years earlier.

That same month, in July 2002, BYD listed on the Hong Kong Stock Exchange. The IPO was a validation of everything Wang had built: a world-leading battery company, profitable, growing, and sitting on a war chest. Nobody outside the company had any idea what Wang planned to do with the money. But inside BYD's Shenzhen headquarters, a plan was already forming — one so audacious that it would cause the stock to crater and prompt analysts to use the word "suicidal."

The battery years were over. The car years were about to begin.

III. The "Crazy" Pivot: The Qinchuan Acquisition (2003–2007)

In January 2003, less than six months after the Hong Kong IPO, BYD announced the acquisition of Xi'an Qinchuan Automobile Co., Ltd. from Norinco, the Chinese state-owned defense conglomerate. The price was HK$269 million — roughly $35 million at the time.

The reaction from the market was immediate and savage. BYD's stock dropped twenty percent in days. Shareholders were furious. Analysts called it suicidal. The logic was obvious: why would the world's largest rechargeable battery manufacturer, a company printing money in consumer electronics, buy a failing state-owned car company in Xi'an — a city known for its terracotta warriors, not its automobiles? Qinchuan was a marginal player producing low-quality sedans that nobody wanted. Its factories were antiquated. Its brand was worthless.

But Wang Chuanfu was not buying a brand, and he was not buying a car company. He was buying a license. In China, you cannot manufacture automobiles without government approval, and those approvals are extraordinarily difficult to obtain. By acquiring Qinchuan, BYD inherited its manufacturing license — a golden ticket into the automotive industry. Wang's strategic logic was elegant in its simplicity: a car is nothing more than a battery with four wheels. If you control the battery, you can control the car. And if you can control the car, you can control the entire energy transition.

The first attempt was a disaster. BYD's initial car — a vehicle so forgettable that it has been largely scrubbed from official histories — was, by all accounts, ugly. Dealers refused to sign up. The design was poor, the build quality was worse, and the market response was devastating. There is a story, likely embellished but widely circulated in Chinese business circles, that Wang personally took a sledgehammer to the prototype in front of his engineering team — a "burn the boats" moment designed to communicate that mediocrity was not an option.

What came next changed everything. In April 2005, BYD launched the F3 — and the company's trajectory pivoted permanently. The F3 was, to put it diplomatically, heavily inspired by the Toyota Corolla. To put it less diplomatically, it looked almost identical. But here was the thing: it cost CN¥73,000, roughly $10,000 — about half the price of the Corolla it resembled. The F3 became the best-selling car in China, not because it was beautiful or innovative or prestigious, but because it was radically affordable and reasonably reliable. Wang had applied the same playbook that worked in batteries: study the best product on the market, understand its manufacturing process, and then figure out how to make something comparable at a fraction of the cost.

The F3 was not the electric dream. It was a gasoline-powered sedan that had nothing to do with batteries or clean energy. But it served a crucial strategic purpose: it generated the cash flow and the manufacturing expertise that BYD needed to fund its real ambition. Every F3 sold was essentially a subsidy for the electric vehicle R&D lab. Wang was playing a longer game than anyone realized.

The years between 2005 and 2007 were a masterclass in using a cash cow to fund a moonshot. BYD scaled its automotive operations in Xi'an, learned the brutal economics of car manufacturing — supply chains, dealer networks, warranty claims, crash testing — and quietly built an electric vehicle program that would soon attract the attention of the most famous investor in the world.

The battery company had become a car company. But the car company was about to become something much more interesting.

IV. The Berkshire Bet: "The Guy Who Doesn't Give Up" (2008)

The story of how Warren Buffett's Berkshire Hathaway came to invest in BYD is one of the great business discovery narratives of the twenty-first century, and it starts not with Buffett but with two other members of the Berkshire constellation.

David Sokol was then the chairman of MidAmerican Energy, Berkshire's utility subsidiary. In 2008, Sokol traveled to Shenzhen to visit BYD's operations. What he found was not a polished corporate campus with manicured lawns and executive dining rooms. He found Wang Chuanfu working twelve-hour days, eating on the factory floor alongside his workers, personally reviewing battery chemistry data, and running engineering meetings with the intensity of a man who slept four hours a night. Sokol came back and told Charlie Munger about what he had seen.

Munger's reaction was immediate and emphatic. After his own due diligence, Munger delivered what became one of his most quoted assessments: Wang Chuanfu was "a combination of Thomas Edison and Jack Welch." Edison for the relentless invention — Wang claims to spend sixty to seventy percent of his time on technology and product development. Welch for the operational execution — the ability to run a sprawling industrial conglomerate with military discipline.

Munger pitched the investment to Buffett. By all accounts, Buffett was skeptical. He knew nothing about Chinese battery companies. He knew nothing about electric vehicles. He was, as he has often said, a man who likes to stay within his circle of competence. But Munger was insistent, and when Charlie Munger is insistent, Warren Buffett listens.

In September 2008 — the same month that Lehman Brothers collapsed and the global financial system teetered on the edge of oblivion — Berkshire Hathaway, through MidAmerican Energy, invested $230 million for a 9.89% stake in BYD at HK$8 per share. The timing was extraordinary. The world was panicking, and Berkshire was writing a quarter-billion-dollar check to a Chinese company that most Americans had never heard of, run by a man who had pivoted from batteries to cars in a move that his own shareholders had called suicidal.

The investment was more than capital. It was what might be called "Western Armor." In 2008, BYD was still being sued by Foxconn over allegations of trade secret theft — cases that would drag on for years and result in criminal convictions of former BYD employees. The company was criticized for copycat designs. Its brand outside China was essentially nonexistent. The Berkshire imprimatur changed the calculus. When the Oracle of Omaha's firm backs you, doors open. Institutional investors take a second look. Suppliers extend better terms. Potential partners pick up the phone.

There was a second story unfolding in 2008, one that tends to get less attention but matters enormously for understanding BYD's strategic arc. In that same year, BYD launched the F3DM at the Geneva Motor Show — the world's first mass-produced plug-in hybrid electric vehicle. It beat General Motors' much-hyped Chevrolet Volt to market. The F3DM was not a commercial blockbuster. Its technology was crude by later standards. But it proved something critical: BYD could integrate its battery technology with its automotive platform in a way that no other company — not Toyota, not GM, not any of the established automakers — had yet achieved. The vertical integration thesis was beginning to manifest.

The Berkshire investment transformed Wang Chuanfu's personal wealth almost overnight. BYD's share price surged roughly fivefold from the investment price. By late 2009, Wang was crowned China's richest man by the Hurun Report, with an estimated net worth of $5.1 billion — up from $3.4 billion earlier that year. For a man who still wore a company uniform and ate in the cafeteria, the distinction was almost absurdly incongruent.

But the Berkshire relationship was not just a one-time capital event. It was a seventeen-year partnership. Berkshire held its BYD stake through the dark years of 2017-2019 — when BYD's net profit collapsed from CN¥5 billion to CN¥1.6 billion as Chinese EV subsidies were cut — and through the explosive growth years of 2022-2024. When Berkshire finally completed its exit in September 2025, the investment had generated a return of approximately 3,890%. Charlie Munger, who passed away in November 2023, never saw the final exit, but his judgment on Wang Chuanfu — the Edison-Welch hybrid — had been vindicated spectacularly.

The Berkshire years taught BYD something important: patient capital, deployed at moments of maximum skepticism, can be transformative. Wang would remember this lesson when the darkest years came.

V. The "Hidden" Empire: More Than Just Cars

To understand BYD, you have to understand that the car business — as dominant as it is — sits atop a hidden empire of industrial subsidiaries that would each be significant companies in their own right. Most analysis of BYD focuses on vehicle sales, which accounted for seventy-nine percent of revenue in 2024. But the remaining twenty-one percent tells the deeper story of why BYD's competitive moat is so wide.

BYD Electronics (BYDE): This is the silent giant. Listed separately on the Hong Kong Stock Exchange and 65.76% owned by the parent company, BYD Electronics is one of the world's largest contract manufacturers of electronic components. It manufactures parts for iPhones, iPads, Huawei phones, and Xiaomi devices. In 2023, BYD Electronics generated CN¥129.95 billion in revenue and employed over 150,000 people, with factories spanning China, Romania, Hungary, India, and Vietnam. When Apple needed suppliers for the iPhone 16 supply chain, BYD Electronics was on the list. This business serves two purposes: it generates massive cash flow that funds EV R&D, and it keeps BYD's manufacturing expertise at the cutting edge of precision engineering. The skills required to make iPhone components — micro-tolerances, surface finishing, high-volume quality control — are directly transferable to automotive manufacturing.

BYD Semiconductor: This subsidiary was born out of frustration. When BYD's automotive ambitions grew, the company found itself dependent on external suppliers for IGBTs — insulated-gate bipolar transistors, the power semiconductor chips that control the flow of electricity in an electric vehicle's drivetrain. Think of an IGBT as the traffic cop of an EV: it manages how electricity flows from the battery to the motor, controlling speed, torque, and energy recovery. Every electric vehicle needs them, and in the late 2010s, the global supply was dominated by a handful of European and Japanese companies. Wang, true to form, decided to make his own. BYD Semiconductor was formally established in 2020, producing IGBTs, integrated circuits, and LED components. When the global chip shortage hit in 2021, the strategic brilliance of this decision became apparent. Tesla halted production lines. Ford idled factories. BYD accelerated, because it had its own supply. An IPO for BYD Semiconductor was planned but cancelled in November 2022 — a decision that, in retrospect, looks like Wang choosing to keep his most strategically valuable asset fully integrated rather than spinning it off for a quick valuation pop.

FinDreams: In March 2020, BYD carved out its component divisions into four separate entities under the FinDreams umbrella: FinDreams Battery, FinDreams Powertrain, FinDreams Technology, and FinDreams Precision. The strategic logic was counterintuitive: BYD was taking its crown jewels — the battery technology, the powertrain systems, the automotive electronics — and making them available to competitors. Toyota buys FinDreams batteries. Tesla uses them in Megapack energy storage systems. Kia, Ford, Suzuki, Xiaomi, XPeng, Nio, and a dozen other automakers are customers. FinDreams Battery is now the world's second-largest EV battery producer, controlling approximately seventeen percent of the global market — behind only CATL, China's other battery giant. The logic here mirrors what Intel attempted with its foundry model: if you can sell your components to competitors, you achieve scale economies that further reduce your own costs, creating a virtuous cycle where even your rivals fund your cost advantage.

Beyond these three pillars, BYD operates a forklift division (established in 2009, with thirty thousand units of annual capacity), an energy storage business (which landed a 12.5 GWh contract with the Saudi Electricity Company in February 2025), and the SkyRail/SkyShuttle monorail system — a fully in-house transit solution with over $1.5 billion in development costs, operational in Shenzhen, Chongqing, and Jinan, with projects underway in São Paulo, Bahia in Brazil, and even a bid for the Sepulveda Pass transit corridor in Los Angeles.

The strategic implication is profound. BYD is not an automaker that buys batteries. It is not a battery company that also makes cars. It is a vertically integrated energy and transportation conglomerate that happens to sell most of its output in the form of automobiles. When analysts try to find comparable companies, they struggle. Is BYD the next Toyota? The next Samsung? The next General Electric in its prime? None of these comparisons quite work, because no company in history has simultaneously manufactured batteries, semiconductors, consumer electronics, automobiles, buses, monorail systems, and energy storage at this scale.

The hidden empire is the moat. And it is getting wider every year.

VI. The Blade Battery and The Great Acceleration (2020–2022)

By the late 2010s, the electric vehicle industry had a problem that was becoming impossible to ignore: the cars kept catching fire. Lithium-ion batteries, packed with volatile chemistry and squeezed into ever-tighter spaces to maximize range, were experiencing thermal runaway — a cascading failure where one cell overheats, ignites its neighbors, and the entire battery pack becomes an inferno. The industry had largely moved toward NCM chemistry (nickel cobalt manganese) because it offered superior energy density and range. But NCM was inherently unstable. Every few months, a headline would appear: an EV consumed by flames in a parking garage, a recall of tens of thousands of vehicles, a consumer confidence crisis that threatened to stall the entire transition.

The alternative chemistry — LFP, or lithium iron phosphate — was safer but had been dismissed by most of the industry as a dead end. LFP batteries were heavier, less energy-dense, and offered shorter range. The consensus was clear: the future belonged to NCM, and the safety problems would be engineered away through better thermal management systems. BYD disagreed.

Wang Chuanfu's team had been working on LFP for years, and in 2020, they unveiled the Blade Battery — a piece of engineering that may ultimately prove to be BYD's single most important innovation. The concept was elegant: instead of packaging LFP cells into conventional block-shaped modules, BYD redesigned the cells themselves into long, thin blades — typically ninety-six centimeters long and nine centimeters wide. These blades were arranged in an array and inserted directly into the battery pack, eliminating the intermediate module layer entirely. The result was a dramatic increase in space utilization — over fifty percent compared to conventional LFP block batteries — which partially closed the energy density gap with NCM while maintaining LFP's inherent safety advantages.

The marketing masterstroke was the nail penetration test. In a video that went viral across Chinese social media and later globally, BYD demonstrated what happens when you drive a steel nail through three different battery types. The NCM battery exploded in flames, reaching temperatures above 500°C. A conventional LFP battery produced smoke and heat. The Blade Battery? Its surface temperature rose to just 30-60°C. No smoke. No fire. You could hold an egg against it and the egg would not cook. It was a devastatingly effective piece of comparative marketing that reframed the entire industry conversation: maybe range was not the only thing that mattered. Maybe not dying in a fire mattered too.

The Blade Battery debuted in the BYD Han sedan in July 2020, and by April 2021, it was standard on every BYD battery electric vehicle. The technology did not just solve BYD's product problem — it solved the industry's trust problem. Automakers who had been reluctant to adopt LFP because of its range limitations now had a version that was structurally integrated, space-efficient, and demonstrably safer than the NCM alternative. Tesla began using BYD's LFP batteries. Toyota signed supply agreements. The customer list grew to include Kia, Ford, Suzuki, Xiaomi, XPeng, Nio, and more than a dozen other manufacturers.

But the Blade Battery was only half of the 2020-2022 story. The other half was a decision so bold that it stunned the automotive world.

In March 2022, BYD announced that it would cease production of all internal combustion engine vehicles — effective immediately. Not a gradual phase-out. Not a target date a decade in the future. An immediate, total stop. BYD became the first major automaker in history to kill the ICE entirely, going all-in on new energy vehicles — a category that includes both pure battery electric vehicles and plug-in hybrids.

To appreciate the magnitude of this bet, consider the context. In early 2022, electric vehicles still represented a small minority of global auto sales. Most major automakers were hedging, maintaining parallel ICE and EV production lines, investing in hydrogen fuel cells as a backup, and quietly lobbying against aggressive emissions regulations. BYD's decision to abandon ICE was not a hedge — it was a declaration that the internal combustion engine was already dead, and that any resources spent maintaining it were wasted resources.

The results were immediate and dramatic. In the years leading up to the decision, BYD's annual sales had stagnated in the range of 400,000-500,000 vehicles. After the pivot, the growth curve went vertical. In 2022, BYD sold 1.88 million vehicles. In 2023, it sold 3.02 million. In 2024, it crossed 4.27 million. Revenue doubled, then doubled again: CN¥216 billion in 2021, CN¥424 billion in 2022, CN¥602 billion in 2023, CN¥777 billion in 2024. Net income followed: CN¥3 billion in 2021, CN¥16.6 billion in 2022, CN¥30 billion in 2023, CN¥40.3 billion in 2024.

The "Great Acceleration" was not just about volume — it was about proving that vertical integration, applied with extreme discipline over two decades, could create a cost structure that no competitor could match. BYD made its own batteries, its own chips, its own motors, its own power electronics, and its own software. Every component it produced in-house was a cost it did not pay to a supplier. And in a business where margins are thin and scale is everything, that cost advantage was the difference between profit and loss at price points that competitors could not touch.

The company that the market had called suicidal in 2003 was now the fastest-growing automaker on earth. The chemistry professor who had borrowed money from his cousin to make phone batteries was sitting atop a $108 billion revenue empire. And the Blade Battery — born from a chemistry that the industry had dismissed as a dead end — had become the foundation on which it all rested.

VII. Management, Ownership, and The Culture of "China Speed"

Wang Chuanfu remains chairman and CEO of BYD as of early 2026, an extraordinary span of continuity for a company of this scale. He has led BYD for over thirty years, from its founding in 1995 through every strategic pivot, every crisis, and every period of hypergrowth. In an industry characterized by revolving-door C-suites and professional management rotations, Wang's tenure is remarkable — and his continued operational involvement is even more so.

Wang holds approximately 17.6% of BYD's equity. His cousin Lu Xiangyang — the man who lent CN¥250,000 to start the company — holds 13.5%. Together, the founding family controls over thirty percent of the company, a concentration that gives Wang the freedom to make long-term bets without the quarterly earnings pressure that constrains Western automaker CEOs. When Wang decided to kill the ICE in March 2022, he did not need to convince a dispersed shareholder base or negotiate with activist investors. He made the call and executed.

The management culture at BYD is distinctive in ways that do not translate neatly into Western corporate frameworks. The company uses what might be called a "massive internal competition" model. Different engineering teams are assigned to work on the same project simultaneously — competing against each other for the right to take their design into production. The winning team gets the production line; the losing teams go back to the lab. It is brutal, inefficient by conventional metrics, and extraordinarily effective at producing rapid innovation. The DM-i hybrid system, the Blade Battery, and the e-Platform architecture all emerged from this competitive hothouse.

Stella Li, BYD's executive vice president and the face of the company's international expansion, has been with BYD for over two decades. Wolfgang Egger, the former Alfa Romeo and Audi design chief hired in November 2016, transformed BYD's design language from the copycat aesthetics of the F3 era into something genuinely distinctive — the Dragon Face design language of the Dynasty Series and the marine-inspired Ocean Series.

The R&D operation is staggering in scale. In 2023, BYD spent CN¥39.91 billion on research and development — roughly six percent of revenue — and employed 102,000 R&D personnel, sixty percent of whom were under the age of thirty. The company filed over 13,000 patents between 2003 and 2023. In 2022 alone, BYD hired 280,000 new employees. By December 2024, total headcount had reached 968,900, including over 104,000 in R&D. With 5,000 engineers dedicated solely to autonomous driving systems, BYD's TianShen ("God's Eye") driver assistance technology has been fitted as standard on twenty-one of thirty models as of February 2025 — including the cheapest Seagull.

Wang's personal philosophy remains anchored in the extreme frugality of his upbringing. In February 2025, he sat in the Great Hall of the People alongside Ren Zhengfei of Huawei, in seats directly in front of Xi Jinping — a positioning that Chinese observers interpreted as a deliberate signal that BYD and Huawei had been elevated to the status of "national champions." For a man who grew up an orphan in rural Anhui, the symbolism could not have been more dramatic.

The culture of "China Speed" — a phrase used within BYD to describe the velocity at which the company develops and launches new products — is not just rhetoric. BYD's fifth-generation DM-i hybrid system, launched in May 2024, achieved 46.06% brake thermal efficiency (a measure of how efficiently an engine converts fuel energy into useful work — the higher, the better), which the company claimed was the world's highest. Its 1MW fast-charging system, rolled out in March 2025, adds approximately 400 kilometers of range in five minutes. And in early March 2026, BYD unveiled its second-generation Blade Battery using LMFP (lithium manganese iron phosphate) chemistry, achieving 190-210 Wh/kg energy density and supporting "Flash Charging" — 10 to 70% state of charge in five minutes, even in sub-zero temperatures.

The speed is relentless. The question for investors is whether this pace can be sustained as the company scales toward five million vehicles per year and expands into dozens of international markets simultaneously. The culture that produces "China Speed" is deeply intertwined with Wang Chuanfu's personal intensity — and the company has never operated without him at the helm.

VIII. The Playbook: 7 Powers and 5 Forces Analysis

Understanding BYD through the lens of business strategy frameworks reveals why the company's competitive position is so difficult to replicate.

Hamilton Helmer's 7 Powers

BYD's most formidable power is Process Power — the accumulated manufacturing know-how that Wang Chuanfu has built over three decades. This is not a single patent or a single factory; it is the institutional knowledge of how to design, engineer, and produce at enormous scale while maintaining cost discipline. The "human robot" strategy of the battery years evolved into the hyper-integrated manufacturing systems of the automotive years, and that evolution represents decades of learning that cannot be purchased or reverse-engineered. When BYD achieves a landed cost for the Seagull EV that allows it to retail for under CN¥90,000 (approximately $12,000) while still generating profit, that is process power in action — the result of thousands of small manufacturing optimizations accumulated over years.

Cornered Resource manifests in two forms. First, BYD's internal supply of LFP batteries through FinDreams Battery — the world's second-largest EV battery producer — means the company is never at the mercy of external suppliers for its most critical component. Second, BYD Semiconductor's in-house IGBT and power chip production eliminates dependence on the European and Japanese chipmakers that gatekeep this technology for most automakers. These are not resources that competitors can easily acquire. CATL can sell batteries to anyone, but it cannot replicate BYD's integration of batteries, chips, motors, and vehicles within a single corporate structure.

Scale Economies are the third and perhaps most visible power. Selling over four million vehicles per year allows BYD to amortize its R&D spending (CN¥39.91 billion in 2023) across a volume base that dwarfs most competitors. When you spend forty billion yuan on R&D and sell four million cars, the R&D cost per vehicle is roughly CN¥10,000. When a rival spends similar amounts but sells 500,000 cars, their per-vehicle R&D cost is eight times higher. This arithmetic is why BYD can price the Seagull at $12,000 and still fund one of the largest automotive R&D operations on earth.

Counter-Positioning also applies. BYD's decision to bet on LFP chemistry when the industry consensus favored NCM was a classic counter-positioning move. Established battery makers and automakers had invested billions in NCM supply chains and production processes. Switching to LFP would have meant writing off those investments. BYD, which had been working on LFP from the start, faced no such switching costs. The Blade Battery was the product that made counter-positioning pay.

Porter's Five Forces

The forces analysis reveals BYD's structural advantages with unusual clarity:

Supplier Bargaining Power: Negligible. This is the single most important structural advantage BYD possesses. In a normal automotive company, suppliers of batteries, chips, motors, and power electronics hold enormous leverage — they can raise prices, constrain supply, or prioritize other customers. BYD is its own supplier for virtually every critical component. When the industry talks about "supply chain resilience," BYD does not need the conversation. It is the supply chain.

Buyer Bargaining Power: Moderate but manageable. In China, BYD's home market (seventy-seven percent of 2025 sales), the sheer breadth of the product lineup — from the sub-$12,000 Seagull to the $140,000+ Yangwang U8 — means BYD competes across virtually every price segment. Buyers have choices within the BYD ecosystem, which reduces the risk that a single model's failure could imperil the company. Internationally, BYD enjoys significant pricing power: in Europe, the company marks up vehicles by 92-112% versus China prices, earning approximately €14,300 profit per Seal U EV in the EU compared to €1,300 in China.

Threat of Substitutes: Present but mitigated. Public transportation, ride-sharing, and micro-mobility are all substitutes for personal vehicle ownership. But BYD has hedged this risk by operating its own transit division — the SkyRail monorail system and its electric bus business. The company sells the substitute, too.

Threat of New Entrants: Declining. The capital requirements for automotive manufacturing, the complexity of battery technology, and the regulatory barriers (especially in China, where manufacturing licenses are tightly controlled) create significant entry barriers. The dozens of Chinese EV startups that launched in the 2018-2020 period are now consolidating rapidly, with many failing or being absorbed.

Competitive Rivalry: Intense. BYD faces fierce competition from CATL in batteries, from Tesla globally in premium EVs, from Volkswagen and Toyota in mainstream vehicles, and from Chinese rivals like Geely, SAIC, and the remaining EV startups. The rivalry is real, but BYD's cost advantage — rooted in its vertical integration — provides a durable edge that pure-play competitors struggle to match.

The DM-i Hybrid Bridge

One strategic asset deserves special attention: BYD's plug-in hybrid technology, particularly the DM-i system. Tesla sells only pure battery electric vehicles. BYD sells both — and in markets where charging infrastructure is underdeveloped, range anxiety is real, and consumers are not ready to go fully electric, the plug-in hybrid is a "Trojan Horse" that Tesla simply does not have. A BYD DM-i vehicle can run fifty to one hundred kilometers on pure electric power for daily commuting, then switch to gasoline for long trips. It eliminates range anxiety while delivering dramatically lower fuel consumption than a conventional car. The fifth-generation DM-i system claims a combined range of 2,100 kilometers — enough to drive from Beijing to Shanghai and back without refueling. For consumers in Brazil, Mexico, Thailand, and Southeast Asia — markets where BYD is expanding aggressively — the plug-in hybrid is often a more practical purchase than a pure EV. Tesla has no answer for this segment.

The KPIs That Matter

For investors tracking BYD's ongoing performance, two metrics stand above all others. First, NEV sales volume growth — the monthly and quarterly vehicle delivery numbers that serve as the most immediate indicator of demand trajectory, market share gains, and the effectiveness of new model launches. This single number captures whether BYD's growth engine is accelerating, plateauing, or decelerating. Second, gross margin per vehicle — the indicator of whether BYD's vertical integration advantage is translating into sustainable profitability or being competed away through pricing pressure. When BYD reported its first quarterly profit decline in over three years during Q2 2025 (net profit down 29.9% year-over-year), it was the gross margin compression, not the volume growth, that concerned analysts. Volume without margin is a treadmill. Margin with volume is a compounding machine.

IX. The Bull vs. Bear Case

The Bull Case

The bullish thesis for BYD rests on a simple proposition: this is the Toyota of the twenty-first century, and we are still in the early innings of its global expansion.

Toyota's dominance of the late twentieth-century automotive industry was built on a manufacturing system — the Toyota Production System — that competitors could study but never fully replicate, because the advantage was embedded in decades of institutional learning, supplier relationships, and cultural norms. BYD's advantage is structurally analogous but even more comprehensive: it is not just a manufacturing system but an entire supply chain, from raw materials to finished vehicles, controlled by a single company.

The unmatched cost structure is the foundation. BYD can profitably sell the Seagull at price points that would destroy the margins of every Western automaker. The $12,000 Seagull is not a loss leader — it is a profitable product that creates volume, drives scale economies, and funds R&D for premium models like the Yangwang U9 supercar (priced above $140,000). No other automaker can operate profitably across this price range because no other automaker controls its own supply chain to the same degree.

The international expansion opportunity is enormous and still in its early stages. In 2024, BYD's overseas sales reached 417,204 vehicles — impressive growth but still less than ten percent of total volume. The company has manufacturing facilities operational or under construction in Thailand, Brazil, Hungary, Turkey, Indonesia, Cambodia, and India. In markets where Tesla is too expensive for the mass market — Brazil, Mexico, Southeast Asia, the Middle East, Africa — BYD's price-competitive lineup has no peer. By April 2025, BYD's EV sales in Europe had surpassed Tesla's. In 2025, BYD dominated Singapore's car market with a 21.2% share — the single most popular car brand in the country.

The technology roadmap continues to advance at remarkable speed. The second-generation Blade Battery, unveiled in early March 2026, uses LMFP chemistry to achieve higher energy density and supports Flash Charging that adds meaningful range in single-digit minutes. The 1.5MW Flash Charging system enables 10 to 97% charge in nine minutes. The TianShen autonomous driving system, developed partly in-house and partly with Momenta, has been integrated with DeepSeek's large language model and fitted as standard equipment across most of the lineup. BYD is not just a car company — it is increasingly a technology company that happens to deliver its technology in the form of vehicles.

The Bear Case

The bearish thesis centers on three interconnected risks: geopolitics, the "China discount," and brand perception.

Geopolitics is the most immediate threat. The European Union imposed a 17.4% additional import duty on BYD vehicles in July 2024, on top of the existing 15% tariff — bringing the effective tariff to over 32%. The United States is effectively closed to BYD passenger vehicles through a combination of tariffs and regulatory barriers. The NDAA for fiscal year 2024 prohibits the U.S. Department of Defense from procuring BYD batteries. In October 2025, the U.S. Department of Defense stated that BYD merits inclusion on a list of companies linked to China's military. These are not abstract policy risks — they are active, escalating barriers to BYD's most profitable potential markets. The European markup of 92-112% over China prices is enormously profitable, but it also means that tariff increases directly threaten BYD's highest-margin revenue stream. If the EU follows the U.S. in effectively closing its market, BYD's international growth story narrows significantly.

The "China Discount" is a broader phenomenon that affects all Chinese companies listed on domestic or Hong Kong exchanges. Political risk — the possibility of regulatory intervention, geopolitical escalation over Taiwan, or sudden policy shifts that prioritize state objectives over shareholder returns — creates a persistent valuation discount relative to comparable Western companies. BYD's elevation to "national champion" status, symbolized by Wang Chuanfu's prominent seating alongside Ren Zhengfei at Xi Jinping's feet in February 2025, is both a blessing and a curse. It provides state support and political cover domestically, but it also paints a target internationally. The closer BYD is perceived to be to the Chinese state, the harder it becomes to enter Western markets on purely commercial terms.

Brand perception remains a work in progress. BYD's origins as a "copycat" manufacturer — the F3 that looked like a Corolla, the battery-reverse-engineering era — left a reputational residue that the company is still working to scrub. The Yangwang brand, with its $140,000+ U8 amphibious SUV and U9 electric supercar, is an explicit effort to move upmarket and establish BYD as a luxury competitor. But brand elevation takes decades, not years. Hyundai spent thirty years transforming its image from cheap Korean econobox to legitimate premium competitor with the Genesis brand. BYD is attempting the same transition at compressed timescales, and the outcome is not guaranteed.

There is also the question of whether BYD's growth rate is sustainable. Q2 2025 delivered the company's first quarterly profit decline in over three years, with net profit falling 29.9% year-over-year. In September 2025, BYD cut its annual sales target by up to sixteen percent — from 5.5 million units to 4.6 million. The Chinese EV market is increasingly crowded, with fierce price competition eroding margins for all players. BYD's vertical integration provides a cost floor that competitors cannot match, but even the most efficient manufacturer cannot defy margin gravity indefinitely in a commoditizing market.

Finally, there are subsidy and regulatory considerations. BYD received the equivalent of approximately €2.1 billion in Chinese state subsidies in 2020 alone. The Rhodium Group estimates that BYD received $4.3 billion in state support between 2015 and 2020. As China's subsidy regime evolves and Western governments scrutinize Chinese industrial policy, the question of how much of BYD's cost advantage is structural versus policy-dependent remains an open one. The company's darkest period — 2017-2019, when net profit collapsed from CN¥5 billion to CN¥1.6 billion — was directly triggered by subsidy cuts. BYD survived and ultimately thrived, but the episode demonstrated that government policy can move the needle on profitability in material ways.

X. Conclusion: Lessons for Founders

The BYD story inverts almost every assumption of the 2010s technology playbook. The dominant narrative of that era held that the future belonged to "asset-light" companies — software platforms with minimal physical infrastructure, outsourced manufacturing, and negative working capital cycles. Build the app, not the factory. Own the customer relationship, not the supply chain. Move fast and break things.

Wang Chuanfu built the factory. He built the supply chain. He built the battery factory, the chip fab, the motor plant, the vehicle assembly line, the bus depot, and the monorail track. BYD is the anti-thesis of asset-light — it is the most asset-heavy major technology company in the world, with nearly a million employees and manufacturing facilities on four continents.

And it works. It works because the energy transition — unlike social media or e-commerce — is fundamentally a hardware problem. You cannot disrupt lithium-ion chemistry with a software update. You cannot 3D-print a semiconductor. You cannot outsource battery safety to a contract manufacturer in a different country and maintain quality control at the level required when your product carries human beings at highway speeds. The 2020s belong to companies that control the physical stack, and no company controls more of the physical stack than BYD.

The second lesson is the power of patient capital. Berkshire Hathaway held its BYD investment for seventeen years, through a period when the stock declined over seventy percent from its 2009 highs and the company's profitability collapsed. Berkshire did not sell during the dark years. It waited. And it was rewarded with a 3,890% return. The investors who abandoned BYD during the 2017-2019 subsidy crisis — when it genuinely looked like the company might be a failed experiment — missed the greatest automotive growth story of the twenty-first century.

The third lesson is the most counterintuitive. Tesla's approach to the EV market was top-down: start with the $100,000 Roadster, use it to fund the $70,000 Model S, use that to fund the $35,000 Model 3, and eventually build a mass-market vehicle that everyone can afford. It is a brilliant strategy, and it worked. BYD's approach was bottom-up: start with the $1 battery cell, use it to win contracts from Motorola and Nokia, use the profits to buy a car company, use the car company to build a $10,000 gasoline sedan, use the sedan's cash flow to fund electric vehicle R&D, and eventually build a complete energy ecosystem from the atom to the automobile. Both strategies produced trillion-dollar outcomes. But BYD's bottom-up approach created something that Tesla's top-down approach did not: a vertically integrated supply chain that makes the company its own most important supplier.

Wang Chuanfu once set a goal for BYD to become the world's largest automaker by 2025. He did not quite get there — Toyota and Volkswagen Group still sell more total vehicles. But BYD overtook Ford to become the sixth-largest automaker globally in 2025, and it became the world's largest electric vehicle manufacturer, surpassing Tesla. For a company founded thirty-one years ago with borrowed money in a Shenzhen apartment, built by an orphan from Anhui who taught himself battery chemistry and then taught himself how to build cars, the trajectory defies every conventional model of corporate development.

The dream, it turns out, was never about building cars. It was about building everything.

XI. Top 10 Resources for Further Reading

-

"Build Your Dreams: The BYD Story" — Corporate biography covering Wang Chuanfu's founding vision and BYD's evolution from battery startup to automotive giant.

-

Snowball: Warren Buffett and the Business of Life by Alice Schroeder — Essential context for the Berkshire Hathaway-BYD relationship and Charlie Munger's role in the investment decision.

-

The 2002 BYD HKSE Prospectus — The original IPO filing that documents BYD's battery business at the moment of its public listing, before the automotive pivot.

-

Charlie Munger's 2009 Daily Journal Annual Meeting Transcript — Contains Munger's famous "combination of Thomas Edison and Jack Welch" assessment of Wang Chuanfu.

-

CSIS Report: "Overcapacity or Comparative Advantage?" — A rigorous analysis of China's EV subsidy regime and its role in shaping BYD's competitive position.

-

FinDreams Battery Technical Whitepapers — Primary source material on the Blade Battery engineering, LFP cell design, and the nail penetration test methodology.

-

"The Li-ion War" — Nikkei Asia deep dive on the competitive dynamics between BYD and CATL, the two Chinese battery giants battling for global market share.

-

BYD 2024 Annual Report — Segment-level financial data for BYD Electronics, FinDreams, and the automotive division, essential for understanding the hidden empire.

-

"The 10,000 Mile Test" — Car and Driver's long-term review of the BYD Atto 3, one of the first comprehensive Western assessments of BYD's vehicle quality.

-

Wired Magazine: "The Man Who Beat Tesla" — Profile of Wang Chuanfu that explores the personal philosophy and management style behind BYD's rise.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube