Rongsheng Petrochemical: The Private Giant & The Saudi Alliance

I. Introduction: The $3.4 Billion Handshake

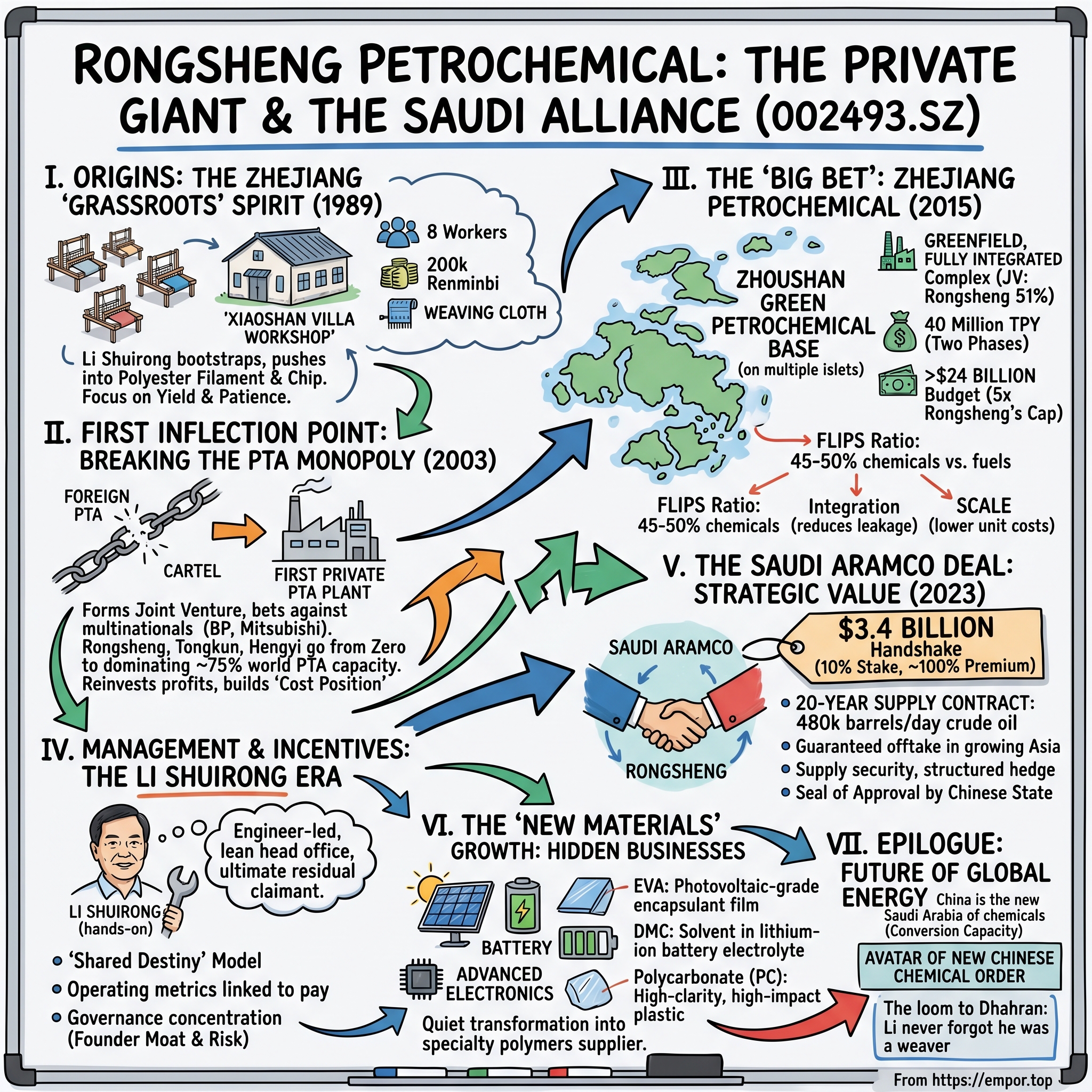

On a humid afternoon in late March 2023, in a tastefully understated conference room in Dhahran, a signature was scratched onto a piece of paper that, if you squinted, looked like the opening shot of a new global order. On one side of the table sat representatives of Saudi Aramco, the most profitable company in the history of capitalism, custodian of the kingdom's subterranean sea of hydrocarbons. On the other side sat Li Shuirong, a soft-spoken engineer from a village outside Hangzhou who, thirty-four years earlier, had scraped together 200,000 renminbi—about $40,000 at the time—to buy a dozen second-hand textile looms and weave cloth by hand.

The contract they signed transferred a 10% stake in Rongsheng Petrochemical to Aramco for 24.6 billion renminbi, roughly $3.4 billion in cash. At the time of announcement, Rongsheng's A-shares traded on the Shenzhen Stock Exchange at a price that valued the whole company at a fraction of what Aramco agreed to pay. The implied premium to market was close to 100%. Investors squinted at the headlines. Sell-side analysts wrote notes with tentative titles like "Strategic Premium or Overpayment?" Energy wonks pointed out the symmetry: just a few months earlier, Aramco had paid an even fatter premium for a slightly smaller stake in Rongsheng's sister company, but this was the largest single foreign direct investment ever made in China's petrochemical sector. Not industry—sector. Not year—ever.

Why would the Saudis—a company that could in theory build its own refinery anywhere in the world—pay a twelve-figure number to buy into a Chinese chemical company that most Americans had never heard of? And more to the point, how did a private weaving shop in Zhejiang become the junior partner of the House of Saud?

That is the thesis of this episode. Rongsheng Petrochemical, trading as 002493 on the Shenzhen exchange, is the ultimate "integration play" in modern industrial history. The company spent three decades climbing the petrochemical value chain from the very bottom—raw woven fabric—to the very top: crude oil. Along the way it did something that very few companies anywhere in the world have ever pulled off. It went backwards up a vertical so long and so technically complex that it passed state-owned behemoths like Sinopec and CNPC in specific product lines, and it did so as a private, family-controlled firm.

The road map for today's conversation runs in three arcs. First, the unlikely origin story: a village workshop in Xiaoshan with eight workers, a bootstrapped climb into polyester, and then a contrarian bet on PTA—a precursor chemical—against a cartel of foreign giants. Second, "The Big Bet": the construction of the Zhoushan Green Petrochemical Base through the joint venture Zhejiang Petrochemical, which at full build became one of the largest single-site refineries on planet earth. Third, the pivot that the headlines missed: the quiet transformation of Rongsheng from a "refinery company" into a supplier of the specialty polymers that encapsulate your rooftop solar panels and shuttle lithium ions inside your EV battery.

The "hidden" chemicals business, as we will argue, is the real prize. Gasoline is the loss leader. The magic is what they do with the molecules on the way there.

II. Origins: The Zhejiang "Grassroots" Spirit

Xiaoshan is not a place that appears on many world maps. A flat, canal-laced district on the southern bank of the Qiantang River, it had for centuries been a farming and weaving region in Zhejiang province, famous for a kind of white-striped cotton fabric and for its tradition of peasant-entrepreneurs who, if they could not grow out of poverty, would weave or trade their way out. In 1989, Li Shuirong was twenty-six years old. He had trained as a textile technician, spent time supervising work at a collective weaving workshop, and he had saved, borrowed, and coaxed together 200,000 renminbi—a fortune in that context, and a rounding error by any modern standard.

With that money, he founded what was then called Rongsheng Chemical Fibre Weaving, a name so deliberately mundane it almost parodied itself. The initial factory occupied a few hundred square meters. There were eight workers. The looms were used. The product was chemical fibre cloth, a woven polyester textile that would be sold on to garment makers and, for the lucky lots, to export traders in Shanghai and Ningbo. Three decades later, when asked to describe those years, Li would tell interviewers that the hardest part was not the work—it was the uncertainty. There was no manual for starting a private manufacturing company in late-1980s China. There were no venture capitalists. There were, effectively, no private banks. There was only the loom, the bolt of cloth, and the next order.

It is worth stopping on this moment because the DNA of modern Rongsheng is all here. First, the obsession with yield: a weaver who survives in commodity cloth learns, the hard way, that every percentage point of waste is the difference between profit and bankruptcy. Second, the patience. Li did not pivot into property development, which was the standard get-rich-quick move of the 1990s among Zhejiang entrepreneurs. He stayed in the fibre business. Third, the method: climb the chain. Weaving is the bottom of the textile ladder. The real margin sits one rung up, in the yarn. The still-better margin sits two rungs up, in the polyester chip from which the yarn is spun. The generational margin sits three rungs up, in the chemical feedstock from which the chip is made.

So Rongsheng did what its peers did not. Through the late 1990s and into the early 2000s, it pushed into polyester filament—the shiny, strong synthetic thread that was then flooding Chinese garment factories as the middle class's appetite for cheap, durable clothing exploded. By 2003, Li and his partners had built one of the largest private polyester producers in the Hangzhou Bay region. By 2007, the operation had grown into a diversified textile-chemical group with its own sister entity, Rongsheng Holding, and a reputation among Zhejiang industrialists as a company that reinvested profits instead of distributing them.

To understand why this mattered, you have to understand the "Zhejiang model." In the 1990s, Chinese industrial development was split along an ideological seam. In the north and west, the state-owned enterprises dominated—disciplined, funded, politically protected, but slow. In the south and east, especially along the coastal strip from Shanghai to Wenzhou, an army of small private firms emerged in the shadows of the SOEs, each run by a founder-operator, each obsessive about cost, each willing to bet the whole balance sheet on a single machine, a single product, a single shipment. Rongsheng was not the biggest of these. Not initially. But it had, and has, the purest version of that operating culture: lean head office, engineers running the plants, and a chairman who for years kept his personal office in Xiaoshan even as his industrial footprint grew to span half the country.

From this small grassroots beginning, Rongsheng would soon discover that the real competitors up the chain were not fellow weavers. They were multinationals and state champions—and they had no intention of letting a village workshop break into their profit pool.

III. The First Inflection Point: Breaking the PTA Monopoly

If you want to understand how Rongsheng became the partner of Saudi Aramco, you need to understand a three-letter acronym that has changed more Chinese fortunes than any other in the last twenty years: PTA. Purified Terephthalic Acid. It is a white crystalline powder, refined from a chemical called para-xylene, and it is the most important single ingredient in the polyester universe. A rough rule of thumb: about 85% of a polyester chip is PTA. No PTA, no polyester. No polyester, no filament, no polyester cloth.

In the early 2000s, the market for PTA inside China was a near-textbook cartel. A handful of multinationals—BP, Mitsubishi, and a few others—together with a small circle of Chinese state-owned producers controlled essentially all domestic supply. China was by then the world's largest consumer of PTA, because China was by then the world's largest weaver. Yet its domestic industry was dependent on imports. The pricing power sat overseas. The margin sat overseas. And on the ground in Xiaoshan, polyester makers like Rongsheng watched helplessly as a molecule they could not make absorbed the best economics in their own value chain.

This is the point at which most companies would have tried to lobby for protection, or diversify into real estate, or simply accept the squeeze. Rongsheng did the opposite. In 2003, Li Shuirong joined with several other private Zhejiang polyester firms to form a new joint venture to build PTA capacity of their own. The first plant came on line in 2005. The scale was an eye-watering departure from anything Rongsheng had built before: a single unit larger than any single private chemical plant then operating in China. It required financing that stretched the group's banking relationships to their limit and a licensed chemical technology package imported from abroad. In the internal telling, Li stood on the construction site during the commissioning phase and did not leave for three weeks.

The result of that bet was, frankly, quiet at first. PTA prices were volatile. The plant's initial years were lean. Margins tightened when imports surged and fattened when they receded. But the real impact was structural. Rongsheng, together with its Zhejiang partners, had broken the foreign monopoly. Over the following decade, private Chinese producers—Rongsheng, Tongkun, Hengyi, Hengli—would go from zero to dominating roughly three-quarters of the world's PTA capacity. The multinationals retreated. Several shuttered Chinese plants. BP sold out of key Asian assets. Mitsubishi gradually wound down exposure. What had looked like an impregnable moat turned out to be, in the face of committed private Chinese capital operating at scale, a sandbank.

Here is the part of the story that investors who look only at the income statement miss. Rongsheng's peers in the same era enjoyed similar opportunities, but they played them very differently. Some diversified aggressively into property and finance, chasing the leverage-fueled real-estate boom that dominated Chinese headlines in the 2010s. A few of them, in retrospect, are now case studies in distress. Rongsheng did not. Every yuan of cash flow that came out of its weaving, polyester, and PTA businesses was ploughed back into the chemical chain. A fourth PTA line. A fifth. Improvements in catalyst efficiency that shaved kilograms of raw material per tonne of output. A tweak that recovered a bit more steam from a cooling tower. Unglamorous, deeply unsexy, compounding engineering decisions that meant that when the PTA cycle turned, Rongsheng's units were usually running closer to the low end of the global cost curve while its competitors were sweating.

The strategic logic underneath this capital discipline can be summarised in one idea: Rongsheng was not buying capacity. It was buying cost position. That distinction is the single most important thing to remember about how this company thinks. In a commodity chemical, the winner is not the largest producer or even the most modern producer. It is the lowest-cost producer, because cycles always come, and when they come, the high-cost producers shut down while the low-cost producers accumulate share and gorge on the eventual upswing. For a decade, Rongsheng treated every spare yuan as a chip to bet on cost position. It would turn out to be exactly the right preparation for the largest bet of its life.

Because by the middle of the 2010s, the Chinese state had quietly begun to open a door that had been shut for forty years. And Rongsheng was standing right next to it.

IV. The "Big Bet": Zhejiang Petrochemical

Take a boat from the Ningbo waterfront out into Hangzhou Bay, and after an hour or so of brown, estuary-coloured water, the Zhoushan archipelago rises out of the sea—more than a thousand islands, most uninhabited, a few dotted with fishing villages, one or two with container ports. In 2015, on a pair of adjacent islets connected by a new-built causeway, the Chinese government designated a site for what would become one of the most audacious industrial projects of the decade: a greenfield, fully integrated refining and petrochemical complex built by private enterprise, for private enterprise, at a scale previously reserved for state champions.

The context matters. For forty years, crude oil refining in China had been effectively the exclusive preserve of three entities: Sinopec, CNPC, and CNOOC. These were the national oil companies, created to secure China's energy supply and, not incidentally, to collect the best profit margins in the petrochemical chain. Private firms had been permitted to build downstream businesses—polyester plants, PTA plants, plastics plants—but the upstream refinery gate had been closed. In 2015, under pressure from overcapacity, slowing domestic demand growth, and a strategic rethink of how the chemical industry should evolve, Beijing quietly reopened that gate. A small number of private, domestically owned companies were invited to apply for licences to build large-scale integrated refineries, on the condition that the resulting complexes would be focused on producing chemicals rather than fuels.

Rongsheng, together with three partners—Juhua Group (a local state-owned chemical company), Tongkun Group (a fellow polyester private), and Zhoushan Haitou (a local state investment vehicle)—formed Zhejiang Petrochemical Company, universally known by the initials ZPC. Rongsheng was and is the controlling partner, holding 51% of the equity. ZPC was given the green light to build a 40-million-tonne-per-year refining and chemical integration project at Zhoushan, to be delivered in two 20-million-tonne phases. To appreciate what 40 million tonnes per year means, consider that this single facility, when built, would refine more crude oil than the entire United Kingdom consumes in a year. It would be among the three or four largest refining sites on planet earth.

The total capital budget for ZPC Phases I and II exceeded 170 billion renminbi, which at then-prevailing exchange rates translated to roughly $24 billion. By way of context, that is a number larger than the market capitalisation of most listed refining companies in the world at the time. It was roughly five times the market capitalisation of Rongsheng itself at the moment the project was approved. This was, in the most literal sense the phrase permits, a bet-the-company moment.

What makes the ZPC story an Acquired-worthy case study is not the money, however. Other companies have committed larger dollar amounts to worse-reasoned megaprojects. What is remarkable is the execution. Phase I, at 20 million tonnes of annual crude processing capacity, broke ground in mid-2017 and achieved first oil through the main unit in late 2019—roughly two and a half years from first piling to commissioning, for a facility that included a 20-million-tonne atmospheric and vacuum distillation unit, multiple cracking units, a para-xylene complex large enough to supply a continent, ethylene crackers, and downstream polymer trains. Western megaprojects of comparable scope have routinely run seven to ten years. Phase II was added within three further years, bringing total on-site crude processing capacity to 40 million tonnes by the early 2020s. A third phase, at a further 20 million tonnes, has been under negotiation and partial development, though the exact pace of approval has not been fully disclosed.

Three features distinguish ZPC's engineering design from the plants of its state-owned peers, and together they explain why the complex has produced outsized margins since startup. First, chemical yield. A traditional Chinese refinery converts around 60% of a barrel of crude into transportation fuels and only a fraction into chemical feedstocks. ZPC's design flips this ratio. Somewhere between 45% and 50% of every barrel of crude it processes is ultimately directed into chemical products rather than gasoline or diesel, a proportion more than double the industry average. The implication: ZPC is effectively a chemical plant that happens to make gasoline as a by-product, not a refinery that happens to make some chemicals.

Second, integration. Inputs that would be sold as intermediate products in a standalone refinery are instead piped directly into adjoining chemical units, eliminating storage, handling, and intermediate margin leakage. The economic benefit of this on-site handoff is subtle but compounding: ZPC consistently captures 3–5 percentage points of additional gross margin compared to a non-integrated peer, simply because the molecules never leave the fence.

Third, scale. A 20-million-tonne single-train atmospheric-vacuum unit is not merely "bigger" than two 10-million-tonne units; it is a structurally different machine, with lower unit capital cost, lower unit labour cost, and lower unit energy cost. In commodity chemical economics, scale advantages of this kind are the difference between a 15% return on capital and a 25% return on capital across a cycle.

By the early 2020s, ZPC was contributing the overwhelming majority of Rongsheng's consolidated net profit. In peak years, it produced the bulk of the group's earnings in a single site, turning the rest of the company—textiles, standalone PTA, polyester—into a legacy footnote in the financial statements. Rongsheng had, in a span of less than five years, transformed from a polyester-and-PTA company into a crude-to-chemicals powerhouse. The old identity had not been abandoned so much as quietly subsumed.

It was, in retrospect, exactly this new identity that made Rongsheng a target for the most important strategic investment in its history.

V. Management & Incentives: The Li Shuirong Era

Pictures of Li Shuirong are rare. Profile interviews are rarer. Unlike the tech-era Chinese billionaires whose personal brands became as valuable as their equity stakes, Li has spent his career cultivating a deliberate low profile. He is, by reliable accounts of people who have worked with him, an introvert in a kingdom of extroverts, an engineer in a world of dealmakers, and a Zhejiang operator in a country increasingly dominated by Beijing politics. He remains chairman of Rongsheng Petrochemical and the ultimate controlling shareholder of its parent, Rongsheng Holding Group, through which he holds roughly 60% of the listed company's equity.

That ownership concentration is the single most important fact about how this company is governed. In a country where the median large listed firm is either controlled by the state or diluted by successive rounds of private placement, Rongsheng is a founder-controlled, cash-reinvesting, engineer-run enterprise in which the ultimate decision maker and the ultimate residual claimant are the same person. This is the structural reason why the company has been able to sustain its multi-decade pattern of aggressive capital reinvestment. There is no quarterly dividend-hungry institutional shareholder base to placate. There is no activist pushing for buybacks. The controlling shareholder has, for thirty-odd years, consistently chosen to plough cash into the next unit, the next integration step, the next margin. The alignment between capital allocation and the long-term economic interests of the controlling family is nearly total.

What is Li's operating style? Inside the company, the word most often used by former employees and by bankers who have worked with the group is "hands-on." Li is known for walking the plants, asking specific technical questions, and for a level of comfort with engineering detail that is genuinely unusual at the chairman level. He has, according to people familiar with the project, personally reviewed specification decisions on ZPC units that in a typical large industrial group would be signed off three or four layers below the CEO. The cultural consequence is a management team dominated by engineers and plant operators rather than by finance lifers or consultants. Head office headcount at Rongsheng is strikingly small for a company of its asset base.

Incentives are aligned through a model that the Chinese business press has described as "shared destiny." Senior managers at both the listed company and at the key operating entities, including ZPC itself, have been given equity or equity-linked exposure to the performance of the specific assets they run. Plant managers' compensation is heavily variable and heavily linked to operating metrics—uptime, yield, unit cost, specific energy consumption. The result is a culture in which the incremental margin on a tonne of paraxylene is a board-level conversation as much as a floor-level conversation.

There is a broader point here about why being private, family-controlled, and engineer-led gave Rongsheng what amounts to a multi-year head start over its larger state-owned competitors. The state-owned refiners were constrained, in the 2010s, by bureaucratic capital allocation processes, by political imperatives around employment in legacy refineries, and by the inertia of very large organisations. Rongsheng was constrained by none of these. When the refining licence window opened in 2015, the company was able to move from decision to commitment in months rather than years, and the advantage compounded from there. ZPC came online at a moment when the Chinese state-owned refiners were still debating whether and how to modernise their own facilities. That five-year head start has, more than anything else, driven the earnings power of the modern company.

It is also worth acknowledging the governance risk that sits alongside this structure. Concentrated ownership by a founder is an advantage when the founder is making good decisions; it is a cliff-edge when the founder is making bad decisions or when succession becomes a question. Rongsheng is not there yet—Li is, at time of writing, in his early sixties and by all accounts fully engaged—but any fundamental investor thinking about this company for the long run has to reckon with the fact that the governance moat is also, potentially, the governance single point of failure.

Aramco, interestingly, seemed to view that concentrated control as a feature rather than a bug. The ability to sign a twenty-year supply agreement with a counterparty whose founder-owner could, in effect, make and keep a decision of that magnitude was itself part of what made Rongsheng worth the premium.

VI. The Saudi Aramco Deal: Benchmarking & Strategic Value

Return to the scene in Dhahran. By the time the 2023 stake purchase was signed, Saudi Aramco and Rongsheng had been talking, in one form or another, for several years. The Saudi engagement with Chinese downstream was not a single deal but a campaign. In prior years, Aramco had taken equity in a partner petrochemical venture in northeastern China and had signed long-term crude supply agreements with multiple Chinese independent refiners. The Rongsheng transaction was, however, the headline piece, and the one that drew the widest attention.

The numbers: Aramco's subsidiary acquired 10% of Rongsheng's listed A-share equity for 24.6 billion renminbi. The agreed per-share price of 24.3 renminbi was approximately double the 30-trading-day volume-weighted average at the time of the transaction announcement. The obvious question—and the one most Western analysts asked on day one—was whether Aramco had overpaid.

The better question is what Aramco actually bought. Read strictly as an equity purchase of 10% of a cyclical Chinese chemical company, the deal does look expensive. Read as a package that includes a multi-decade crude supply arrangement, it looks entirely different. As part of the transaction framework, Aramco contracted to supply Rongsheng with 480,000 barrels per day of crude oil on long-term terms. That is a staggering number. To put it in context, 480,000 barrels per day is more oil than the entire United Kingdom produces. Over a twenty-year contract life, at prevailing prices, that supply agreement channels hundreds of billions of dollars of Saudi crude into Chinese refineries—most of it destined for ZPC.

For Aramco, the strategic logic is straightforward and, frankly, elegant. The long-term oil demand thesis is clearest in Asia generally and in China specifically. Chinese refining and petrochemical demand continues to grow even as Western gasoline demand plateaus. A 480,000-barrel-per-day guaranteed offtake into the largest, most modern integrated complex in East Asia is, from Aramco's perspective, a structural hedge against any medium-term deterioration in Chinese spot demand. It guarantees a buyer at scale for the most valuable single segment of the Saudi barrel. The 10% equity is, in a sense, the price of admission—and the alignment mechanism that ensures the offtake is real, not paper.

For Rongsheng, the benefits are symmetric. The company secured a "cornered resource"—a guaranteed, long-term supply of high-quality Saudi crude at pre-negotiated terms, at scale. In an industry where supply disruptions and geopolitical volatility can annihilate quarterly earnings, this transforms the risk profile of ZPC from a spot-price taker into a structurally advantaged buyer. Saudi crude is the preferred diet of many complex refineries, well matched to ZPC's unit configurations, and the deal effectively ensures that ZPC will run at design specification through geopolitical cycles that might force less-advantaged competitors to reduce rates or blend inferior substitutes.

The cash proceeds are equally important. The 24.6 billion renminbi was, in practical terms, a strategic capital injection in a form that Rongsheng did not have to repay. Crucially, the cash was earmarked not for further gasoline production—the market for Chinese transport fuels is mature and in certain sub-segments already contracting—but for the next phase of the company's strategy: a further build-out of high-end "new materials" capacity. Which is the piece of the story most casual observers continue to miss.

The transaction also carried an unspoken signal. For decades, the strategic question surrounding any large Chinese private firm has been whether its independence could survive encounters with national policy priorities. The Aramco deal was, in effect, a validation that the Chinese state viewed Rongsheng as a national strategic asset—important enough to anchor the largest foreign direct investment in the Chinese chemical sector, and trusted enough to be the counterparty to a multi-decade supply arrangement with the Saudi national oil company. That implicit seal of approval is not tradable, but it is material.

With fresh capital, guaranteed feedstock, and a strategic partner on the register, Rongsheng turned its attention to the part of the business that is least well understood by the market.

VII. Hidden Businesses & Segments: The "New Materials" Growth

If you read only the headlines—"China approves 40 million tonne refinery," "Aramco buys stake in Chinese refiner"—you would be forgiven for assuming that Rongsheng is in the business of making gasoline, diesel, and jet fuel. It isn't. Or rather, it is, but those products are the low-margin by-products of a set of chemical processes whose highest-margin outputs barely register in the mass media.

The mental model worth holding in your head is this: ZPC is not a refinery that makes chemicals on the side. ZPC is a giant integrated chemicals complex that cracks crude oil as its upstream feed because doing so is cheaper than buying intermediate feedstocks on the market. Every molecule of crude that enters the fence is being processed with the ultimate aim of producing the highest-value product the configuration will allow. Gasoline and diesel are, in this framing, a kind of collateral yield. The magic is elsewhere.

Consider three of the "hidden" product lines that have, over the past few years, become an increasingly important part of the Rongsheng earnings mix.

Ethylene vinyl acetate, known universally as EVA, is a flexible polymer whose most important modern application is as the encapsulant film that sandwiches the photovoltaic cells in a solar panel. EVA film holds the glass, the cells, and the backsheet together, and it has to be optically transparent, UV-stable, and chemically inert over decades of exposure. High-quality photovoltaic-grade EVA is a surprisingly specialised product. For years, the world's capacity was dominated by a handful of petrochemical incumbents, most of them non-Chinese. As Chinese solar module manufacturing scaled into global dominance in the 2010s, domestic demand for EVA outran domestic supply, and China became a net importer of a product it ultimately wanted to make at home. ZPC's EVA units have, by the mid-2020s, become among the largest producers of solar-grade EVA in the Asia-Pacific region, supplying directly into the Chinese solar module supply chain. Margins on photovoltaic-grade EVA are materially above those of bulk commodity polyethylene and have been, through certain periods, multiples above.

Dimethyl carbonate, or DMC, is a small-molecule chemical whose main modern use is as a solvent in the electrolyte formulations of lithium-ion batteries. Every EV battery you have ever ridden on top of contains DMC. As the Chinese EV industry exploded in the late 2010s and 2020s, demand for DMC and related carbonates followed. ZPC and its associated entities have built substantial battery-grade DMC capacity, backwards-integrated from the cracker's own ethylene stream. Again, margins on battery-grade DMC materially exceed those of bulk commodity products, and the downstream customer—the Chinese battery industry—has been among the fastest-growing buyers of anything on earth for a decade.

Polycarbonate, or PC, is a high-clarity, high-impact-strength engineering plastic used in electronics, automotive components, medical devices, and, increasingly, the housings of consumer electronics. The production process is technically challenging, with a historically consolidated global supply base dominated by a few Western and Japanese chemical majors. ZPC's polycarbonate capacity, running on on-site-sourced bisphenol A, has made Rongsheng one of the largest PC producers in China and, by extension, in the world.

These three lines—EVA, DMC, PC—are illustrative, not exhaustive. The full list of Rongsheng's higher-value product portfolio includes styrenics, ABS, specialty polyolefins, aromatics derivatives, and a lengthening tail of engineering plastics. The common pattern across this portfolio is that each product sits downstream of a molecule that ZPC already produces in abundance from its crude slate, and each serves a downstream Chinese demand base tied to a structurally growing end-market: renewables, electrification, advanced electronics, or high-end automotive.

The segment implications show up in the margin mix. The bulk fuel barrel is low-margin, volatile, and cyclical. The specialty chemical barrel is materially higher-margin, less volatile, and tied to structural growth themes that are, if anything, gathering pace. As Rongsheng has ramped its new-materials capacity, the share of group profit attributable to these higher-value outputs has risen, and the sensitivity of the consolidated P&L to short-term gasoline cracks has declined. None of this shows up in the stock ticker, because the market continues to price Rongsheng as a refining company. But for fundamental investors willing to do the segment work, the real economic engine of the modern company is increasingly the new-materials portfolio, not the fuel yield.

One more layer of second-layer diligence is worth noting. The global trade and tariff environment around chemicals and new materials has become materially more complicated in the 2020s. Solar-grade EVA and certain battery chemicals have attracted trade-policy attention in Western markets. Rongsheng's customer base, heavily weighted toward Chinese downstream manufacturers, is somewhat insulated from direct Western tariff exposure, but any deterioration in global demand for Chinese solar modules or EVs would eventually reach the chemical suppliers. On the other hand, Chinese industrial policy—particularly the 14th Five-Year Plan's emphasis on domestic self-sufficiency in high-end chemicals—has been a tailwind for precisely this class of business.

Which brings us to the playbook.

VIII. The Playbook: 7 Powers & 5 Forces

Let's put Rongsheng through the two analytical frameworks that this kind of episode deserves: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces. The two frameworks are complementary. Helmer's powers are about the sources of durable competitive advantage; Porter's forces are about the structure of the industry in which that advantage operates.

On Scale Economies, Rongsheng's position at ZPC is as clear-cut as it gets in modern industry. The single-site 40-million-tonne footprint, with integrated aromatics, olefins, and polymer trains, is among the largest on earth. Unit capital costs, unit labour costs, and unit energy costs are structurally below those of sub-scale competitors. In a commodity chemicals business, scale economies are not a marketing phrase—they translate directly into a lower breakeven oil price, which determines who runs and who idles in the troughs. Rongsheng's breakeven has historically sat comfortably in the lower tier of the global cost curve for the products where it competes.

On Cornered Resource, the Saudi Aramco supply agreement is, by any reasonable definition, exactly that. A twenty-year, 480,000-barrel-per-day guaranteed offtake of high-quality Saudi crude, on pre-negotiated terms, is not a commodity relationship. It is a structural asymmetry relative to competitors that must buy crude on the spot market in a world where Middle Eastern supply is a subject of serial geopolitical anxiety. It is worth noting, however, that "cornered resource" in Helmer's strict sense requires preferential access at a price that cannot be replicated. The Aramco contract is not disclosed in granular pricing terms, and the degree to which Rongsheng's purchase cost is structurally advantaged versus a marginal Chinese buyer is not publicly known. What is known is that supply security, rather than per-barrel price, is the primary advantage.

On Process Power, Rongsheng's proprietary integration of refining, aromatics, and downstream polymer production is the third leg. The specific configuration of ZPC—particularly its very high ratio of chemical yield to fuel yield and its in-fence handoffs between units—is not easily replicable, because replicating it requires not just the design but the decade of cumulative operating experience that allows these units to be run at design specification. A competitor starting from scratch today could in theory build the same facility, but would face many years of learning-curve losses before reaching ZPC's operating parameters.

Two of Helmer's remaining powers—Counter-Positioning and Switching Costs—are less directly relevant. Rongsheng's commodity chemical customers, by and large, can source equivalent products elsewhere. Brand and Network Economies do not meaningfully apply.

On Porter's 5 Forces, the analysis runs as follows. Bargaining power of suppliers is, for most chemical companies, a perpetual problem; the supplier is OPEC. In Rongsheng's case, the Aramco partnership largely neutralises this force. Bargaining power of customers is moderate—Chinese downstream polymer buyers are numerous and somewhat fragmented, though certain specialty products serve a concentrated customer base and command accordingly firmer pricing.

Threat of substitutes in the core product mix is real but limited. Bioplastics and recycled polymers exist at the margin, but for the foreseeable future the scale of global demand for petrochemical-derived materials far exceeds what alternative sources can supply. Threat of new entrants, however, is where the moat is deepest. The entry ticket to match ZPC's position is, conservatively, north of 20 billion US dollars. The regulatory permits required to build an integrated refining-chemical complex of this scale in China are functionally impossible to obtain de novo today; the licensing window that opened for Rongsheng and a handful of peers in 2015 is, for all practical purposes, closed. Industry rivalry is the remaining force, and it is intense: Rongsheng shares its segment with Hengli Petrochemical, Shenghong Petrochemical, and the state-owned giants, all of whom are formidable in their own right. Rivalry inside the "private refining chemical" cohort is a real headwind to margins in downturns, but it also keeps the cohort disciplined.

Put differently, Rongsheng sits behind a very deep moat at the asset level, in an industry with no meaningful new entrant risk, with supplier power neutralised by the Aramco deal, and with a small circle of rivals who are collectively investing behind the same structural themes.

What, then, of the bull and bear cases?

The bear case is relatively straightforward and, at moments of cyclical weakness, can feel very compelling. Global chemicals are cyclical. Chinese property demand, which has historically pulled through a meaningful share of polymer consumption, has been weak for several years and shows no imminent sign of structural recovery. Global oversupply in commodity chemicals, particularly in the ethylene chain, has pressured margins. Chinese macro growth has decelerated. Geopolitical risk between China and Western markets, especially in the context of EVs and solar modules, introduces tail risks to segments of the demand base. The stock is inherently a cyclical, and within cyclicals, it is levered—the capital structure required to build ZPC has left Rongsheng with significant debt.

The bull case runs to the opposite side of the ledger. The pivot to renewables and electrification materials—EVA, DMC, PC, engineering plastics—means that even in a decarbonising world, Rongsheng is supplying the chemicals for the decarbonisation, not fighting against it. The Aramco alliance structurally de-risks the feedstock side. The cost curve position at ZPC means that Rongsheng will remain profitable in cycles where marginal competitors will not. The global restructuring of chemical capacity, in which older and sub-scale Western and Asian plants have been closing, creates room for the largest and most efficient producers to gain share. The next phase of capex is increasingly tilted toward higher-margin specialty products, which over time should lift consolidated margin structurally.

KPIs worth watching: first, the gross margin of the ZPC integrated complex, reported through segment or subsidiary disclosures, as the cleanest single indicator of how the crown jewel is performing. Second, the product mix shift, measured as the share of revenue or gross profit coming from new-materials segments—EVA, carbonates, polycarbonate, engineering plastics—versus traditional fuels and bulk polymers. Third, the leverage ratio and interest coverage, because the debt stack carried from the ZPC build is the most immediate risk factor in a prolonged down-cycle.

Comparatively, Rongsheng's closest peer is Hengli Petrochemical, which built a comparable private integrated complex in the northeast. The two companies are structurally similar and financially not dissimilar, and a fundamental investor comparing them would focus on site-specific yields, product mix, and leverage.

Myth versus reality deserves a brief interlude. The consensus narrative, especially in Western press, often portrays Rongsheng as "just another Chinese refiner" and reads the Aramco deal as a simple premium buy. The reality is that Rongsheng is a private family-controlled specialty chemicals company that happens to own one of the world's largest refineries as its upstream feedstock unit. The Aramco stake is best understood as a bundled arrangement in which a multi-decade crude offtake was the primary asset traded, and the 10% equity was the alignment mechanism. Miss this, and you misread both the deal and the company.

IX. Epilogue: The Future of Global Energy

There is a phrase that has been circulating in energy-policy circles in recent years: "China is the new Saudi Arabia of chemicals." The meaning is specific. Saudi Arabia's dominance of the global oil system has been built on the possession of the lowest-cost, largest-reserve hydrocarbon basin on earth. China's emerging dominance of the global chemical system is being built on something slightly different—not reserves, but conversion capacity. The world's crude oil is still Saudi. The world's refined and chemicalised crude oil is increasingly Chinese.

In that picture, Rongsheng occupies a specific and, arguably, defining position. It is not the only Chinese private integrated chemical producer, but it is the largest and the most fully integrated. The combination of scale, cost position, product breadth, and strategic alignment with the most important crude supplier in the world makes it, in a very real sense, the avatar of the new Chinese chemical order. The Aramco alliance is, in this reading, not a one-off transaction but an emblem. The two largest petrochemical systems on earth—Saudi upstream and Chinese downstream—have been formally bound at the single most important processing node.

What does this mean for the person who started it all? Li Shuirong began his career at a loom in Xiaoshan, earning margins measured in cents per metre of cloth. Thirty-seven years later, he sits on the board of a company that processes a meaningful fraction of the world's crude oil and that counts the Saudi national oil company as a strategic shareholder. The arc is implausible enough that if it were offered as the plot of a novel, the novel would be rejected on the grounds of lack of credibility. The best single-sentence summary of the company's trajectory is that Li never forgot he was a weaver. He just kept climbing.

For investors thinking about Rongsheng as a long-term fundamental position, the key observation is that the company's competitive advantages are rooted in physical assets, contractual relationships, and operating culture that are very difficult to replicate. The industry around it is consolidating toward the largest and most efficient producers. The end-market demand mix is evolving in ways that favour the products Rongsheng has chosen to expand into. The principal risks are macro—Chinese growth, global chemical cyclicality, leverage, governance concentration—rather than idiosyncratic.

And the larger story, the one that this episode has really tried to tell, is about how a company can, over decades, climb a value chain that almost nobody else has climbed, by combining patience with engineering discipline and refusing the shortcuts that looked easier at the time. In a world in which the temptation to diversify, to financialize, and to chase the market has taken down many of its peers, Rongsheng stayed in its lane. The lane, it turned out, ran all the way from a loom in a Zhejiang village to a handshake in Dhahran.

Whether the next decade proves as kind as the last three is a question that sits firmly in the domain of things no podcast can tell you. What can be told is the shape of the bet Rongsheng has made. It has bet that the molecules underneath modern electrification—the EVA in the solar panel, the DMC in the EV battery, the polycarbonate in the smartphone housing—will be produced at scale by whoever can produce them cheapest, cleanest, and most reliably. It has bet that its own integrated configuration, cost position, and Saudi-anchored feedstock make it the most likely such producer in Asia. And it has bet, as it has always bet, that reinvesting today's cash flow into tomorrow's unit is the only game worth playing.

That, in the end, is the Rongsheng story. A weaving shop that became a refinery. A refinery that is, quietly, a chemicals lab. A chemicals lab that is, less quietly, building the physical infrastructure of the energy transition.

The handshake in Dhahran was not the end of that journey. It was the beginning of its next chapter.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube