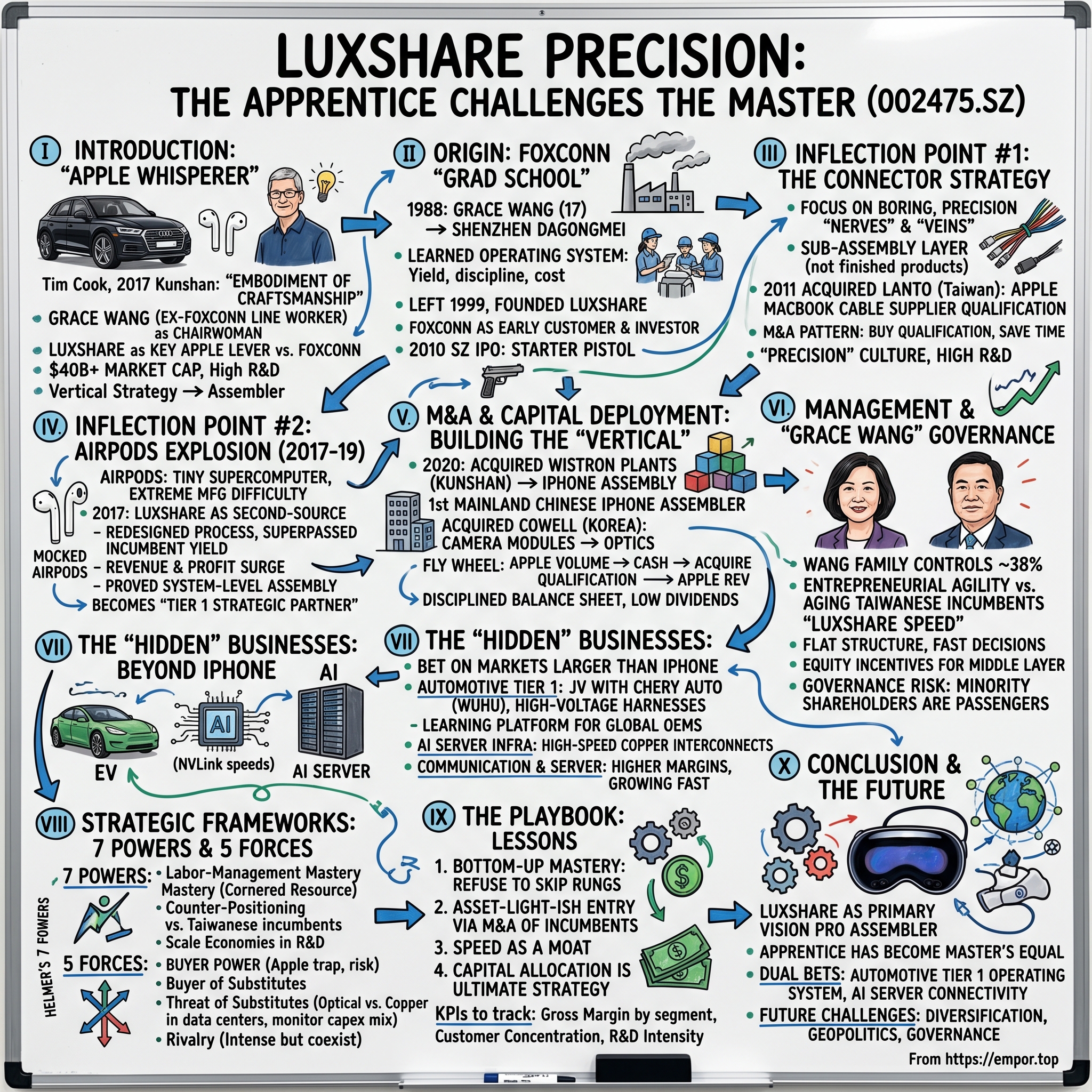

Luxshare Precision: The Apprentice Who Challenged the Master

I. Introduction & The "Apple Whisperer"

Picture the scene in late 2017. A black Audi pulls through the gates of an industrial park on the outskirts of Kunshan, a manufacturing city an hour's drive from Shanghai that most Westerners have never heard of. Tim Cook steps out in his trademark untucked shirt, squints through the autumnal haze, and walks into a cavernous factory floor where tens of thousands of workers in blue smocks are assembling something almost impossibly small and impossibly complex: the second-generation AirPods. Cook pauses at a workstation, picks up a half-finished unit, rotates it between his fingers, and turns to his hosts. The words he chose that day would later be reprinted in Chinese newspapers for years: what he saw was, in his phrasing, "the embodiment of craftsmanship."

It was an extraordinary moment for a company that, less than two decades earlier, had not existed. And more extraordinary still for the woman standing beside him—a former factory line worker named Grace Wang, who had once, as a teenager, clocked in at 7 a.m. on a Foxconn assembly line in Shenzhen making connectors for a few cents a piece. In 2017, she was the chairwoman of Luxshare Precision, a company Cook had come to personally inspect because it was rapidly becoming the single most important lever Apple possessed in its strategy to de-risk itself from its longtime manufacturing partner, Foxconn.

This is the thesis, and it is almost novelistic in its symmetry. Grace Wang's very first employer, the company that taught her how to organize labor, how to think about yield, and how to treat precision as a religion, was Foxconn. And three decades later, her company is the instrument Apple uses to hedge its dependence on that same Foxconn. The apprentice challenging the master is not a metaphor. It is the literal strategic reality of the world's most valuable consumer hardware supply chain.

And the numbers tell a story that Wall Street is only now beginning to fully price. Luxshare Precision, trading under the Shenzhen ticker 002475, crossed a market capitalization of around $40 billion over the past several years, with revenue that has compounded at a rate most hardware companies would consider a typographical error. The company has transformed itself from a maker of two-cent wire connectors to a system-level assembler of products that retail for $249 (AirPods Pro), $999 (iPhone Pro), and $3,500 (Vision Pro). It has done so while maintaining an R&D intensity nearly double its assembly peers, and while paying out remarkably little in dividends, plowing cash instead into the next bet, and the next, and the next.

What follows is the story of how a girl from Chenghai district in Shantou, Guangdong, built a company that now controls a meaningful share of the "nervous system" of the world's most important electronic devices—and why her next act, an ambitious pivot into the automotive and AI server markets, may be the most consequential chapter yet. It is a story about the compounding power of doing the boring things exceptionally well, about the patience to remain vertical when everyone else is going horizontal, and about what happens when the student decides that the master's way is not, in fact, the only way.

We begin where all great Asian manufacturing stories seem to begin: on a Foxconn assembly line.

II. The Origin: The Foxconn "Grad School"

In 1988, a seventeen-year-old Grace Wang—then known by her Chinese name Wang Laichun—boarded a crowded train headed south from her hometown in Guangdong province. She was one of the very first cohorts of what Chinese sociologists would later call the dagongmei, or "working sisters," the young women who flooded into Shenzhen's newly designated Special Economic Zone during the first real wave of Chinese industrialization. She was not trained. She was not educated beyond middle school. She had nothing, really, except a willingness to work and a quiet, almost pathological attention to detail.

She walked into a Foxconn factory that at the time had fewer than a hundred employees. The company had only recently relocated its operations from Taiwan to the mainland under the founder Terry Gou, who was himself only beginning to build the empire that would eventually employ more than a million people. It is difficult, from our vantage point today, to appreciate how unformed Foxconn was in 1988. There were no ten-story dormitories, no AI-controlled production lines, no iPhone. Just rows of plastic injection machines and young women making connectors and cables for the nascent personal computer industry.

Grace Wang would spend the next eleven years of her life inside that institution, and it is no exaggeration to call it her graduate school. She started on the line, was promoted to line leader, then to shift supervisor, then eventually into management of an entire connector business unit. She absorbed, by osmosis and by deliberate study, the entirety of the Foxconn operating system: the obsession with yield, the militaristic labor organization, the brutal cost discipline, the relentless compression of cycle times. She learned how Terry Gou thought. And crucially, she learned what Terry Gou did not do well—how his system's rigidity, its Taiwanese-family-firm bureaucracy, its reluctance to empower mainland Chinese engineers, created blind spots that a more agile competitor could one day exploit.

In 1999, Grace Wang did something that at the time looked foolish. She left. Together with her younger brother Wang Laisheng, who would become her closest business partner, she founded a small connector business in Shenzhen that would eventually be renamed Luxshare Precision. The company had essentially no capital, few customers, and no obvious path to scale. It was, in every measurable sense, a more primitive version of the Foxconn she had just departed.

But there was one extraordinary feature of those early years that tends to get glossed over in the hagiographies, and it is worth pausing on. Foxconn, her former employer, became one of Luxshare's largest early customers. Terry Gou recognized that the young woman who had left his company was not a threat but a potential supplier of the sub-components he himself needed. In fact, Foxconn's affiliated entities eventually took meaningful equity stakes in Luxshare during the years leading up to its 2010 IPO. The master, in other words, invested in the apprentice. It is one of the most structurally interesting business relationships of modern Asian industrial history, and it contains within it almost everything you need to know about how Chinese supply chains actually work: the lines between partner, customer, competitor, and investor are blurred to the point of invisibility.

By the time Luxshare listed on the Shenzhen Stock Exchange in September 2010, the company had already established itself as a serious player in the connector and cable assembly niche. The IPO was not a blockbuster; it was an efficient capital raise for a company that needed money to keep growing. And grow it did. But what would become clear only in retrospect was that the 2010 listing was not the culmination of anything. It was the starter pistol. The next decade would see Luxshare do something almost no other Chinese hardware company managed to do: it would climb, rung by rung, up Apple's supply chain ladder, and eventually stand eye-to-eye with the master itself.

To understand how that happened, we need to talk about a seemingly unremarkable acquisition in 2011—and about why, in hardware, the most boring products are often the most strategic.

III. Inflection Point #1: The Connector Strategy

There is a tendency in business journalism to tell the story of Chinese manufacturing through its most visible products—the iPhones, the Teslas, the solar panels. But anyone who has spent time inside a device factory knows that the most valuable real estate inside any consumer electronic is rarely the thing you see. It is the nerves. The veins. The tiny, precision-milled connectors and the flexible printed circuit cables that carry power and data between the visible components. These parts are boring. They are also the difference between a product that works and a product that does not, and the margin profile of a company that can make them reliably, at scale, with sub-micron tolerances, is quietly spectacular.

Grace Wang understood this in her bones. She had, after all, spent eleven years making exactly these parts at Foxconn. And so when Luxshare in the early 2010s had to make the single most important strategic choice of its corporate life, it did not chase glamour. It went deeper into the boring stuff.

The specific decision was this: rather than try to become an assembler of finished products—which would have put it into direct, brutal competition with Foxconn on Foxconn's strongest turf—Luxshare deliberately positioned itself horizontally across the "sub-assembly" layer. The company would become the most precise, most reliable supplier of connectors, cables, antennas, and interconnect modules to every major electronics brand in the world. If Foxconn was the general contractor assembling the house, Luxshare would be the wiring and plumbing specialist whose work was invisible but indispensable.

The defining move came in 2011 with the acquisition of Lanto Electronic, a Taiwan-based cable maker that had been struggling but that held something Luxshare desperately needed: a validated supplier relationship with Apple for MacBook internal cables. The acquisition was not especially large in absolute dollar terms, but it was a master key. By folding Lanto's engineering and qualification status into Luxshare, Grace Wang effectively leapfrogged years of the Apple supplier onboarding process. Overnight, Luxshare transformed from a regional connector vendor into a qualified Apple supplier, with the right to ship parts directly into Cupertino's approved vendor list.

This is a pattern worth pausing on, because it recurs throughout Luxshare's history and is one of the most underappreciated features of how the company compounds. Luxshare rarely greenfields a new capability. Instead, it identifies companies that already have a hard-won qualification—whether it is a supplier relationship, a process patent, or a specific manufacturing license—and it acquires them at moments of weakness. The premium it pays for the acquired capability is almost always less than the cost and time of building the capability from scratch. In a supply chain where qualification cycles with Apple can take three to five years, buying a qualified seat is often the single best use of capital a company can find.

The Lanto acquisition unlocked the MacBook cable business. From there, Luxshare's internal engineering team began a patient, methodical expansion of scope. Each year, the company would take on a slightly more complex sub-assembly for Apple. Internal antennas. USB-C cables. Lightning cables. The Apple Watch wristband connector. Each new SKU was another foothold, another opportunity to demonstrate that the company could hit Apple's terrifying yield and quality targets, another data point in the ledger that Cupertino's operations team maintained on supplier reliability.

And here the "Precision" in the company's name begins to do real work. Internally, Luxshare built a culture around the idea that the boring stuff was not boring at all—that making a connector that inserted correctly 999,999 times out of a million was an engineering discipline as rigorous as designing a chip. The company's R&D spend during this period climbed toward the 6-7% of revenue band, roughly double the 2-3% that traditional assembly peers allocated. For a sub-component supplier, that level of R&D intensity was almost unheard of. It signaled that Grace Wang was not running her company like a commodity cable maker. She was running it like a precision engineering firm that happened to be making cables.

By the mid-2010s, Luxshare had established itself as a trusted member of Apple's inner sanctum. But trust is a ladder, not a destination. The next rung required something harder. It required the company to prove that it could assemble a full product, end to end, and do so at yields that would have broken most of its peers. The product that would force that proof was something that did not yet exist: a pair of wireless earbuds that Apple was secretly developing in Cupertino.

IV. Inflection Point #2: The AirPods Explosion (2017–2019)

In the summer of 2016, Apple unveiled the original AirPods at the iPhone 7 launch. The product was mocked. Pundits called them "toothbrush heads." Twitter was full of cartoons showing the little white stems falling out of people's ears on subway platforms. What almost no one outside the supply chain understood at the time was that AirPods were, from a manufacturing standpoint, one of the most difficult consumer products ever attempted.

The challenge is not intuitive unless you have tried to build one. A wireless earbud is essentially a tiny supercomputer that must fit inside a volume smaller than a sugar cube, wirelessly pair with a phone in under two seconds, maintain audio synchronization between left and right units to within microseconds, survive sweat and moisture, last five hours on a battery the size of a grain of rice, and do all of this while being mass-manufactured at a scale of tens of millions of units per quarter. The original AirPods squeezed a custom W1 chip, a microphone array, multiple sensors, an antenna, and a battery into a form factor that left almost no tolerance for assembly error. Yield rates at the incumbent assembler—a Japanese firm that had been Apple's preferred partner for acoustic products—reportedly languished in ranges that would have been catastrophic for a product Apple was trying to ramp to hundreds of millions of units.

In 2017, Apple made a decision that would change Luxshare's trajectory forever. Cupertino invited Luxshare to become a second-source assembler for AirPods. Initially Luxshare took on a small share of volume, proving itself in a kind of supplier boot camp. But within eighteen months, the company had done something extraordinary: it had redesigned the assembly process itself. Luxshare's engineering team, many of them veterans of the connector business who understood sub-millimeter tolerances in their sleep, systematically reworked the jigs, fixtures, and automation cells that had been used by the original assembler. They attacked the yield problem as an engineering problem, not a labor problem.

The results were staggering. Luxshare's AirPods yield rates quickly surpassed those of the incumbent. Apple, which always seeks dual sourcing as a matter of both risk management and price discipline, rapidly shifted volume share. By 2019, Luxshare was widely reported to be assembling more than half of all AirPods units globally, and for certain generations and variants, the figure was substantially higher still.

What this did to Luxshare's financials was nothing short of transformative. The consumer electronics segment of the company—which is a polite euphemism for "Apple-related business"—climbed from roughly a third of revenue in the early 2010s to more than 80% by the late 2010s. Revenue compounded at rates north of 40% annually for several years running. Net income followed. But the real significance was not in the numbers. It was in what the numbers proved.

AirPods demonstrated that Luxshare could do system-level assembly, not just component manufacturing. This was a categorical leap, and it fundamentally changed Apple's view of the company. Before AirPods, Luxshare was one of several reliable connector vendors in Apple's ecosystem. After AirPods, Luxshare was a company that could take Apple's most difficult acoustic product and solve the yield problem that had stumped a well-respected Japanese incumbent. Every operations executive at Apple—and there are a lot of them—took note.

There is a moment in every supplier's life when the customer begins to see them differently. For Luxshare, that moment happened somewhere in the back half of 2018, when internal Apple documents reportedly began flagging the company as a "Tier 1 strategic partner" rather than a component vendor. The practical implication was that Luxshare now had a seat at the table for future product discussions. When Apple's operations team in Cupertino began sketching out the manufacturing plan for the Vision Pro—a product that would not launch for another five years—Luxshare was in the room.

This is the compounding magic of reputation in the Apple supply chain. Each proof point buys the right to bid on the next, harder, more lucrative product. And the next product, it turned out, was the one everyone said Luxshare could never make: the iPhone itself.

V. M&A & Capital Deployment: Building the "Vertical"

In July 2020, at the height of pandemic supply chain chaos, a short and almost unremarkable announcement appeared on the Shenzhen Stock Exchange. Luxshare Precision would acquire two plants from the Taiwanese contract manufacturer Wistron, one in Kunshan and one nearby, for a total consideration of roughly 3.3 billion Chinese yuan, or approximately $470 million at prevailing exchange rates. The acquired facilities were iPhone assembly lines.

The announcement, buried in disclosure filings, was one of the most consequential industrial transactions of the decade. With it, Luxshare graduated from being Apple's most important component and sub-assembly supplier to being a member of the small, exclusive club of companies that assemble the iPhone itself—a club that had, for two decades, been the near-exclusive domain of three Taiwanese giants: Foxconn, Pegatron, and Wistron. By taking Wistron's seat at that table, Luxshare became the first mainland-Chinese company ever admitted.

Analysts at the time debated whether Luxshare had overpaid. The answer, with six years of hindsight, is almost comically one-sided. Consider the alternative. To greenfield an iPhone assembly capability, a new entrant would need to spend years securing Apple's qualification, recruiting and training tens of thousands of specialized workers, purchasing and validating thousands of pieces of proprietary tooling, and building the engineering relationships with Apple's New Product Introduction team that are truly the moat of the business. The combined cost of doing that organically would have run into the billions of dollars and would have consumed half a decade. Luxshare bought it all, turnkey, for $470 million. It was one of the most surgical strategic acquisitions in the history of Chinese industrial capital.

The Wistron deal matters also for what it signaled. It signaled that the big Taiwanese contract manufacturers, who had dominated the Apple supply chain for a generation, were entering a phase of strategic retreat. Wistron had grown tired of the margin compression and political risk of being an Apple assembler in mainland China. Pegatron would eventually follow, divesting portions of its iPhone assembly capacity to Luxshare in subsequent years. Even Foxconn, though it remains the largest iPhone assembler by volume, began exploring a geographic diversification into India and Vietnam that diluted its focus on the mainland. Into this vacuum stepped Luxshare, younger, hungrier, and willing to accept the margin profile that the Taiwanese incumbents were unwilling to defend.

Parallel to the Wistron deal, in the same pandemic year, Luxshare executed another strategic acquisition: the purchase of Cowell Electronics, a Korean camera module supplier to Apple. Cowell had been a Tier 2 supplier of camera modules, squeezed between the giants LG Innotek and Sunny Optical. Luxshare's acquisition moved the company into smartphone camera modules—an adjacent, high-precision optics business that sat architecturally very close to what Luxshare already did well. The Cowell deal was smaller than the Wistron deal but followed the same logic: buy a qualified supplier at a moment of weakness, inherit the customer relationship and engineering capability, and accelerate the timeline to meaningful Apple revenue by several years.

Step back and the pattern becomes clear. Luxshare's M&A strategy is not a growth strategy in the conventional sense. It is a capability acquisition strategy. Each deal adds a specific process, a specific qualification, a specific foothold into a specific Apple product category. Cables and connectors first. Then acoustics, through AirPods assembly. Then iPhone assembly, through Wistron. Then optics, through Cowell. Then, later, mixed-reality assembly, through the Vision Pro relationship. Each rung of the ladder was climbed with capital that could be deployed quickly precisely because the company kept its balance sheet disciplined and its dividend payout modest. The free cash flow generated by the AirPods windfall was not returned to shareholders; it was redeployed into the next strategic foothold.

This is the "capital flywheel" that defines the company. Apple's demanding but enormous volume generates the cash. The cash is used to acquire the next qualified capability. The new capability becomes the foundation for the next round of Apple revenue. And so on. It is a flywheel that requires, above all, the discipline to avoid distraction—to not go chase the glamorous thing, the adjacent thing, the China-subsidized thing. It is the discipline of a management team that treats the Apple relationship not as a customer relationship but as a multi-decade marriage with an extraordinarily demanding partner.

To understand how that discipline is maintained at the top, we need to meet the two people whose family name is on the letterhead and whose personal wealth is almost entirely tied up in the fortunes of the enterprise.

VI. Management & The "Grace Wang" Governance

Grace Wang is, by most accounts of people who have met her, a remarkably understated executive. She does not grant many interviews. She is not on the global conference circuit. She does not have a biography or a business book in the way that Terry Gou, Jack Ma, or even William Ding have cultivated personal public profiles. When she speaks at investor meetings in Shenzhen, she does so quietly, in Mandarin, and usually with a notebook in front of her. Her voice has a flat, almost schoolteacher cadence, which some Western investors who have met her describe as deceptively matter-of-fact. Behind it is one of the most demanding operators in the Chinese industrial economy.

She is the Chairwoman of Luxshare Precision. Her younger brother Wang Laisheng serves as Vice Chairman and runs meaningful parts of the operational business. Together, the Wang family controls approximately 38% of the company through a holding entity called Luxshare Limited, which is the single largest shareholder. This concentration of control is deliberate and has been preserved through multiple capital raises and stock issuances. Grace Wang has consistently signaled, both in annual reports and in her capital allocation decisions, that maintaining family control is a non-negotiable feature of the corporate structure.

There is a cultural observation that is worth articulating here, because it matters for the investment thesis. The traditional Taiwanese contract manufacturers—Foxconn, Pegatron, Wistron, Quanta—are all run by founders or founder-adjacent executives who came of age in the 1980s Taiwanese tech industry. These men are now in their seventies, and many of their companies are going through generational transitions that are proving difficult. Foxconn's Terry Gou, now in his mid-seventies, has divided his time between political ambitions in Taiwan and the company. Pegatron and Wistron have both gone through phases of strategic retrenchment. Against this backdrop of aging leadership and creeping bureaucracy, Grace Wang and her brother Wang Laisheng are in their fifties, with decades of runway ahead and with the kind of entrepreneurial agility that characterizes first-generation founders at the peak of their powers.

This generational gap shows up in the operating metrics. Luxshare's decision cycles are notoriously fast. Executives describe a culture in which a supplier qualification question can be raised at 9 p.m. on a Sunday and answered with an engineering response team on site by Wednesday morning. Factories are retooled over long weekends. New product ramps are executed with what has become known in Shenzhen industry circles simply as "Luxshare Speed"—a phrase that has entered the vernacular as a competitive benchmark. The company's organizational structure is relatively flat, with Grace Wang and Wang Laisheng personally involved in major supplier and customer decisions in a way that would be impossible at the larger, more bureaucratic Taiwanese incumbents.

The incentive architecture is the other half of this story. Luxshare has consistently maintained one of the most aggressive stock-based compensation programs in the Chinese manufacturing sector, and critically, that compensation is not concentrated at the top. A significant portion of equity incentives flows to the "middle layer" of engineering leads, shift managers, and process engineers—the people whose work actually determines whether a production line hits its yield target. In an industry where Foxconn, BYD, and other deep-pocketed competitors are constantly attempting to poach talent, Luxshare's ability to retain its engineering middle class through equity participation has been a quiet but critical competitive advantage.

Coupled with this is the R&D intensity. Luxshare consistently spends 6-7% of revenue on research and development. For context, traditional assembly peers such as Foxconn have historically run in the 2-3% range. In absolute dollar terms, Luxshare's R&D budget now rivals or exceeds that of much larger Taiwanese peers. The company employs tens of thousands of engineers. That investment is what allows Luxshare to move upstream—to solve Apple's manufacturing problems before Apple itself has fully articulated them, to co-design tooling with Apple's NPI team, and to stay one process generation ahead of its nominal competitors.

A brief word on governance risk, because no discussion of a Chinese single-family-controlled enterprise is complete without acknowledging it. Investors should be clear-eyed that the Wang family's controlling stake means that minority shareholders are, in a meaningful sense, passengers. Related-party transactions, acquisitions of controlled entities, and decisions about dividend policy and capital allocation are effectively decided by the family. To date, the track record of those decisions has been excellent for minority shareholders. Whether that continues is a question of trust in the individuals rather than the legal structure.

With management and governance in place, the question becomes: where does the next decade of growth come from? The iPhone is mature. AirPods are mature. Even the Vision Pro is, for all its engineering glory, a small addressable market for the foreseeable future. The answer is that Luxshare is, right now, making two parallel bets on markets vastly larger than the iPhone. It is just that most public investors are only beginning to notice them.

VII. The "Hidden" Businesses: Beyond the iPhone

If you drive about forty minutes southeast from Luxshare's Kunshan headquarters, you arrive at a sprawling industrial park in Wuhu, Anhui province, where an entirely different future is being built. This is the home of Chery Automobile, China's largest automobile exporter, and it is also the epicenter of Luxshare's most ambitious strategic bet beyond Apple: the automotive Tier 1 business. Founded in 2022, the Luxshare-Chery joint venture, known formally as Luxshare Automotive Technology, is not trying to build a car with the Luxshare badge on it. Grace Wang is not interested in competing with Xiaomi or BYD for consumer mindshare. What she is interested in is something subtler and, arguably, more valuable: becoming the operating system of EV hardware.

Consider what a modern electric vehicle actually is. It is a rolling computer with a battery pack. The interior wiring harness of an EV is roughly three to four times the length of that in an internal combustion vehicle, because EVs need to route not only low-voltage signal wires but also high-voltage cables capable of carrying 400V or 800V from battery to motor. These high-voltage connectors must be engineered to survive vibration, heat, and electromagnetic interference in ways that make laptop connectors look trivial. The charging port itself—whether GB/T in China, CCS in Europe, or NACS in North America—is a high-precision piece of engineering that carries the full drive current of the vehicle. Every one of these elements is, spiritually and technically, exactly the kind of product Luxshare has spent three decades learning to make.

The Chery partnership gives Luxshare a trusted customer for its high-voltage automotive products, but more importantly, it gives the company a learning platform. Chery is one of the most aggressive EV exporters in the world, shipping vehicles to more than eighty countries. By partnering directly with Chery's chassis and powertrain engineering teams, Luxshare is learning the automotive qualification process—a notoriously slow and demanding process known as IATF 16949—from the inside. The goal is not to remain a Chery supplier. The goal is to become an automotive Tier 1 supplier globally, capable of shipping to Volkswagen, Ford, Stellantis, Hyundai, and the rest. The automotive segment, while only representing roughly 3-5% of current consolidated revenue, has been growing at rates comfortably north of 50% year-over-year, and internal targets reportedly call for it to reach a scale comparable to the consumer electronics segment within a decade.

The second "hidden" business is, if anything, even more interesting because it sits on top of the single most powerful technology trend of our era: artificial intelligence infrastructure. Inside every modern AI server—the kind that powers ChatGPT, Claude, or the training runs at OpenAI and Anthropic—are thousands of high-speed interconnects that shuttle data between CPUs, GPUs, memory, and networking silicon at extraordinary speeds. As Nvidia's chips move from PCIe Gen4 to Gen5 to Gen6, and as NVLink speeds double every generation, the physical wires that carry these signals become more challenging to manufacture than ever. The problem is that at these speeds, copper traces begin to lose fidelity across very short distances; the engineering required to maintain signal integrity through a copper interconnect at 224 Gbps is an order of magnitude more difficult than at 112 Gbps.

Luxshare has been quietly building out exactly this capability. The company has become one of the leading global suppliers of what are known as high-speed copper cables for data center applications, including the internal "cable cartridges" that replace PCB traces inside AI server racks. For a select list of hyperscaler customers, Luxshare's connectivity products are integral to the next-generation server architectures being deployed in 2025 and 2026. The communication and server segment—while representing only around 5-7% of revenue today—carries substantially higher gross margins than consumer electronics assembly, because the customer base is less concentrated and the engineering barriers to entry are higher.

It is useful to understand the economic mix this creates at the segment level. Consumer electronics, dominated by Apple, is roughly 80-85% of revenue but runs at the lowest gross margins—it is a high-volume, high-capex, precision-assembly business with a single customer who negotiates ferociously. Automotive is small in revenue terms but growing fast and carrying better margins, because high-voltage automotive connectors command pricing power that consumer connectors do not. Communication and server is the smallest segment but carries the highest margin per dollar of revenue, and it is the one most leveraged to the AI capex cycle that is reshaping the global semiconductor industry.

Translated into a five-year forward view, this means Luxshare is a company whose revenue mix is almost certainly going to look very different by 2030. If automotive and communication grow even close to management's ambition, the "Apple revenue" share will decline not because Apple shrinks but because the other two grow faster. That diversification is the single most important question investors need to track over the coming decade, and it is the reason the segment disclosures in Luxshare's annual reports are worth reading line by line.

And it is also why, to understand the durability of this business model, we need to step back and apply a more rigorous strategic framework to what we have observed.

VIII. Strategic Frameworks: 7 Powers & 5 Forces

In Hamilton Helmer's "7 Powers" framework, a business possesses durable competitive advantage only to the extent that it holds one or more of seven specific structural positions. Applying the framework to Luxshare is instructive because it reveals that the company's moat is not the obvious one—scale—but a cluster of three reinforcing powers that are harder to see and harder to replicate.

The most distinctive is what Helmer calls Cornered Resource, and in Luxshare's case the cornered resource is not a patent or a raw material but something more ephemeral: Labor-Management Mastery. Luxshare has developed, through three decades of iteration, an organizational capability to ramp up production lines with a hundred thousand or more seasonal workers for Apple's autumn launch cycle, and to do so while maintaining yield rates that its Taiwanese competitors cannot match. This sounds simple. It is not. The logistics of recruiting, housing, training, and deploying that many workers across multiple mega-facilities while meeting Apple's unforgiving quality standards is an operational competence built over years of iterative learning. It is, in a very real sense, uncopyable on any reasonable time horizon.

The second power is Counter-Positioning. Luxshare's rise was enabled by a specific structural feature of the Taiwanese contract manufacturers: their reluctance to compete aggressively on mainland Chinese engineering talent and their slow adaptation to mainland-specific supply chain dynamics. When Apple began, in the late 2010s, to actively seek mainland Chinese diversification of its Taiwanese supplier base—driven partly by geopolitical risk and partly by cost pressure—Luxshare was already positioned as the natural answer. Foxconn could not easily respond without cannibalizing its own Taiwanese-run plants. This is the essence of counter-positioning: the incumbent's structural advantages become liabilities when the game changes, and the entrant wins without the incumbent being able to effectively retaliate.

The third power is Scale Economies in R&D. While Luxshare is much smaller than Foxconn in revenue terms, its R&D spend is disproportionately high for its scale, and it is concentrated on the specific domains where Apple's next products require innovation. This allows Luxshare to co-design process technology with Apple in a way that smaller component makers simply cannot afford to do. The R&D flywheel, combined with Apple's preference to award pilot programs to suppliers that can self-fund process development, creates a virtuous cycle that is very difficult for smaller competitors to break into.

Now turn to Porter's Five Forces. The most immediately visible force, and the single most important risk to the entire thesis, is the Bargaining Power of Buyers—specifically, the power of Apple. Apple accounts for a majority of Luxshare's revenue. Apple negotiates hard on price every year. Apple has the option, at any point, to redirect volume to Foxconn, Pegatron, Goertek, or other suppliers. This is the "Apple Trap" that every Apple supplier lives with, and it has historically been the end of the line for companies that became too dependent on Cupertino's generosity. The question for Luxshare is whether the company's diversification into automotive and AI server is fast enough to reduce the Apple concentration to manageable levels before Apple's leverage is ever used against it. Management is clearly aware of this risk and is explicitly working against it. The financial data supports the diversification thesis, but it is an uncompleted journey.

The Threat of Substitutes is the second force worth interrogating seriously. Within data centers, the long-term trend is clearly toward optical interconnects in contexts where distance exceeds a few meters, which means that Luxshare's high-speed copper products have a ceiling on how far they can scale. The company has begun investing in optical transceiver capability precisely because the substitution risk is real. The near-term window for copper remains robust—copper is cheaper, better understood, and fully adequate for the intra-rack distances that dominate AI server architecture today—but investors should watch the capex mix carefully. Over the next five to ten years, the copper-to-optical transition will redefine the competitive landscape, and Luxshare's position in that transition will matter more than anything else about its server business.

Rivalry Among Existing Competitors is intense but, paradoxically, less threatening than it appears. The Apple supply chain has a small number of qualified competitors, and they tend to coexist rather than attack each other's core positions. Foxconn remains the dominant iPhone assembler; Luxshare is the fastest-growing but still secondary player. The two companies compete on the margin rather than in open warfare, and their customer—Apple—has no interest in seeing either of them weakened to the point of becoming a single source of failure.

Threat of New Entrants is low. The capital intensity, Apple qualification cycles, and labor-management complexity described above all function as structural barriers to new entry. India-based contract manufacturers and Vietnam-based operations have begun to matter at the assembly margin, but they lack the vertical integration and R&D depth of a Luxshare.

Bargaining Power of Suppliers is moderate but manageable. Luxshare sources raw materials, specialty chemicals, and specific high-precision tooling from a global supplier base. Material cost inflation is a margin concern in any given year, but the company's scale gives it meaningful negotiating power.

Taken together, the strategic framework suggests a business with genuine durable advantage, but with one concentrated and consequential risk. For the thesis to work over the long run, Luxshare must continue to execute on its diversification while maintaining its operational excellence in the Apple business. That is a narrow path, but it is a path the Wang family has been walking for a very long time without stumbling.

IX. The Playbook: Lessons for Investors & Builders

Stepping back from the specifics, the Luxshare story offers a handful of lessons that apply well beyond Chinese manufacturing. They are the lessons that make the company worth studying for any investor or operator trying to understand how durable industrial franchises actually get built.

The first lesson is the power of bottom-up mastery. Grace Wang did not start by trying to build the most visible product. She started by making the most boring, precision-dependent component possible, and she refused to move upmarket until her company was unequivocally the best in the world at that component. Only then did she acquire the capability for the next rung, and the next. The discipline of refusing to skip rungs—of proving mastery at each layer before attempting the next—is what distinguished Luxshare from the dozens of Chinese manufacturers who tried to leap directly into finished products and ended up with neither scale nor moat. In hardware, the boring stuff is the moat. The visible thing is just the marketing.

The second lesson is asset-light-ish entry through acquisition of tired incumbents. Rather than greenfielding iPhone assembly capability, Luxshare bought Wistron's plants. Rather than building a camera module capability from scratch, it bought Cowell. This pattern of acquiring capability at moments of incumbent weakness, rather than trying to build it organically, compressed timelines by five to ten years in each case. The premium paid for qualified, ready-to-run capability was always a bargain compared to the alternative. For any operator thinking about entering a regulated or qualification-heavy industry, the Luxshare playbook of buying your way into the tier above you is a genuine strategic tool.

The third lesson is speed as a moat. In the Shenzhen industrial ecosystem, where every supplier can access the same capital, the same real estate, and roughly the same labor pool, the only truly defensible advantage is execution speed. Luxshare's ability to retool a production line over a long weekend, to respond to an Apple engineering change order within 48 hours, and to ramp a new product from pilot to high-volume manufacturing in a quarter rather than a year is not a soft skill. It is a compounding institutional capability, baked into the company's culture and incentive structure, that actually shows up in financial outcomes every quarter.

The fourth lesson, and perhaps the most underappreciated, is that capital allocation is the ultimate expression of strategy. Grace Wang has consistently resisted the temptation to pay large dividends, pursue diversifying acquisitions outside her circle of competence, or overextend her balance sheet to chase growth for growth's sake. Every yuan of free cash flow has been deployed into either strategic M&A or R&D aimed at climbing the next rung of Apple's ladder. This is the unglamorous, patient work of compounding industrial capital, and it is rarer than it should be.

On the topic of KPIs, investors who want to track Luxshare's progress over time are best served by narrowing to a small number of indicators rather than drowning in segment detail. There are three that are, in practice, the most informative.

The first is gross margin by segment, and specifically the trend in consolidated gross margin as the mix shifts. If automotive and communication grow faster than consumer electronics, consolidated gross margin should drift upward. A stalled or declining consolidated gross margin would suggest that either pricing pressure from Apple is intensifying or that the diversification into higher-margin segments is not progressing as planned. This single metric captures much of what the thesis hinges on.

The second KPI is customer concentration, measured as the percentage of revenue coming from the single largest customer. Today, this number is high. The long-term question is whether it can be brought meaningfully lower without sacrificing growth. Investors should watch the annual report disclosure on major customer exposure as a direct indicator of diversification progress.

The third KPI is R&D intensity, expressed as R&D expense as a percentage of revenue. Luxshare's moat is meaningfully a function of its ability to out-invest its assembly peers in process engineering. If R&D intensity declines materially, the company is either harvesting rather than investing, or losing the scale economies that have defined its rise. Either would be a warning sign worth taking seriously.

There are a handful of second-layer diligence items that are worth a brief mention for completeness. Luxshare operates in a sector where climate-related regulation, particularly around scope 3 emissions for large OEM customers like Apple, has become a meaningful compliance overlay. The company has been advancing its renewable energy commitments in line with Apple's supplier code, and that compliance should be viewed as a cost of doing business rather than a competitive advantage. Geopolitical risk is real: any material escalation of U.S.-China trade friction that affects Apple's manufacturing strategy would ripple directly to Luxshare. The company's gradual build-out of capacity in Vietnam and India is a partial hedge, but only a partial one. Finally, the Wang family control structure, while to date beneficial, is a governance feature that deserves ongoing attention through the lens of related-party transactions and the quality of the independent directors on the board.

With the playbook articulated, we are left with one final question. Where does this company go from here?

X. Conclusion & The Future

Return, for a moment, to the scene in Kunshan with which this story began. Tim Cook walking through the factory, pausing at a workstation, complimenting the craftsmanship. In the years since that visit, the relationship between Luxshare and Apple has only deepened. When Apple chose to bet the future of the company's spatial computing narrative on the Vision Pro—a device whose manufacturing complexity makes AirPods look like a calculator—it chose Luxshare as the primary assembler. The Vision Pro, in all of its engineering audacity, is the most difficult product Apple has ever tried to build at scale. That Luxshare is the company trusted to bring it into the world is the single clearest piece of evidence that the apprentice has, indeed, become the master's equal.

What comes next depends on whether Grace Wang can do for the automotive industry what she has done for the consumer electronics industry. The thesis has a pleasing symmetry to it. EVs, like smartphones, are software-defined devices whose hardware value is concentrated in precision components, wiring, and system-level integration. The automotive Tier 1 supplier base is aging, Taiwanese-less, and less digitally native than the EV OEMs they serve. There is room for a new kind of automotive supplier: Chinese, hungry, digitally fluent, and operationally obsessive. Luxshare, through Chery and through its own organic investment, is building exactly that company.

The AI server bet is the wildcard. If the current AI capex cycle continues for another five to ten years—which most credible forecasts suggest it will—the global spending on high-speed interconnects will increase by at least an order of magnitude over current levels. Luxshare's position in that spend is already meaningful and is growing. Whether copper or optical wins the next architecture battle is less important than the fact that Luxshare is investing in both and will participate in whichever the market chooses.

There is a poetic irony in where this story ends, or rather, where it pauses. Grace Wang boarded a train to Shenzhen in 1988 as one of the first working girls of the reform era. Forty years later, she runs a company that Cupertino's supply chain team treats as one of its two most strategically important partners. The apprentice learned from the master, left the master, became a supplier to the master, then a competitor to the master, and finally—by the judgment of the master's own largest customer—an equal to the master. That arc is not just a business story. It is a parable of what forty years of Chinese industrial capitalism has made possible, and it is a parable that still has chapters left to be written.

The next decade will answer the harder questions. Can Luxshare manage the transition away from Apple concentration without fumbling the core business? Can it build the automotive franchise into something globally significant? Can it navigate the inevitable geopolitical frictions that will affect every Chinese supplier to Western customers over the coming years? Can the Wang family's governance model survive the transition from founder-led entrepreneurship to professionalized global enterprise?

None of these questions have obvious answers. What is clear is that the company that will try to answer them is, in the unshowy, relentless style that Grace Wang has cultivated for three decades, among the most formidable industrial franchises in the world. And somewhere, in a factory in Kunshan that most Western investors have never visited, the work of precision continues, one connector at a time, toward whatever the next product happens to be.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube