GEM Co., Ltd.: The Sovereignty of the Urban Mine

I. Introduction & The "Urban Mining" Thesis

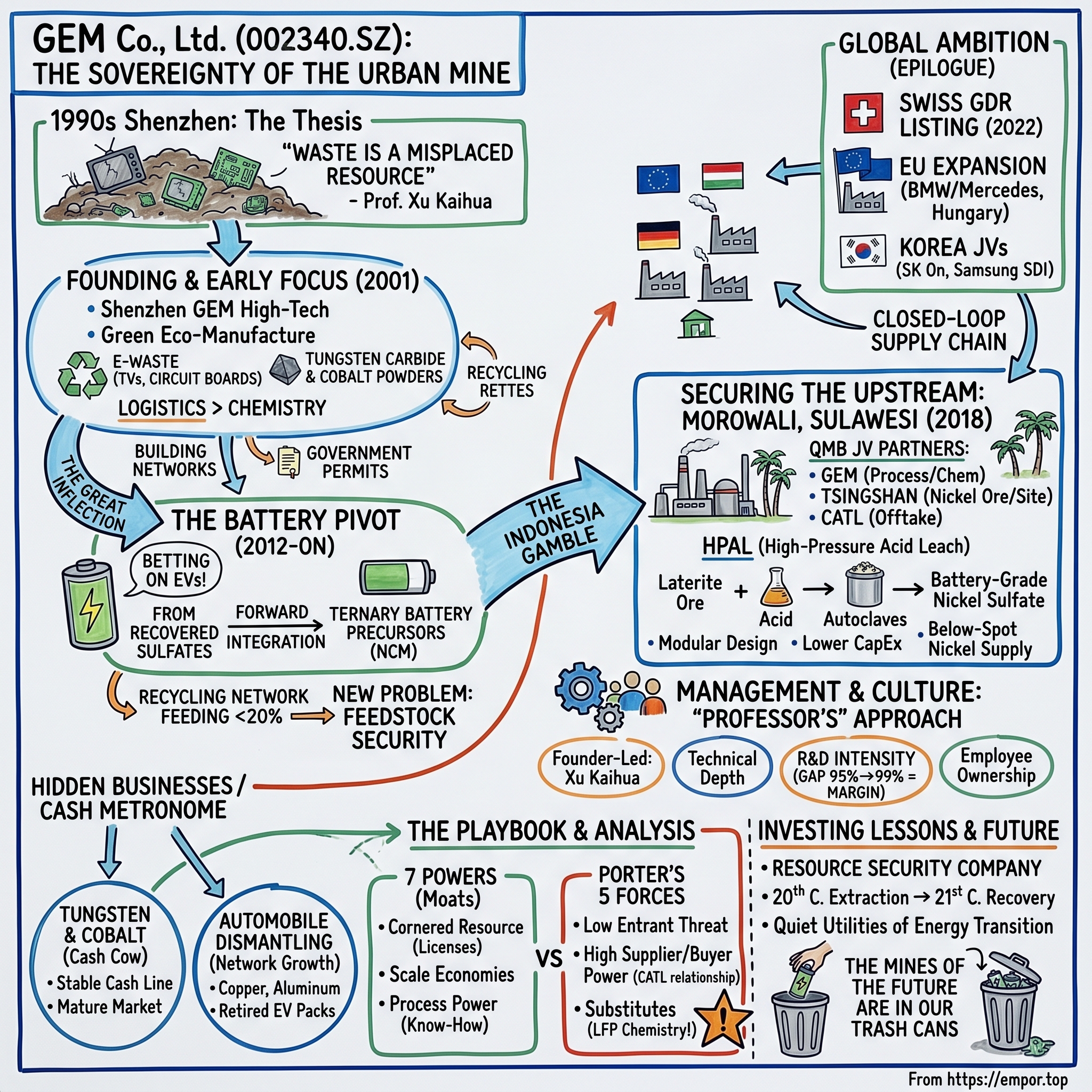

Picture a landfill on the outskirts of Shenzhen in the late 1990s. Mounds of dead televisions, their cathode ray tubes cracked and leaching phosphor into the red Guangdong soil. Pile upon pile of stripped-out printer boards, their gold-plated contacts oxidizing in the humid subtropical air. Children pick through the debris with bare hands, looking for copper wiring to sell by the kilo. A young metallurgical professor named Xu Kaihua walks past one of these informal salvage sites and does the math in his head. The concentration of cobalt in a discarded lithium-ion laptop battery is roughly a hundred times higher than the grade found in a typical cobalt mine in Congo. The concentration of gold in a ton of circuit boards beats the world's richest hard-rock gold mines by a factor of thirty or forty. And yet humanity keeps digging holes in the ground while the richest ore body in the world sits in the trash.

That asymmetry—between what we throw away and what we extract—is the entire thesis of GEM Co., Ltd., a Shenzhen-listed industrial company that has spent the last quarter-century methodically turning garbage into a strategic resource base for the electric vehicle revolution. Today, GEM is a top-three global producer of ternary battery precursors, the chemical building blocks that go into the cathodes of nickel-manganese-cobalt (NCM) lithium-ion batteries powering everything from Teslas to BMW iX SUVs to the Volvos coming off assembly lines in Ghent. It is also, by tonnage, one of the largest battery and electronics recyclers on earth.

The scale is easy to miss because GEM does not have a consumer-facing brand. You will not see its logo on your smartphone or your vehicle. But the nickel sulfate inside a 2025-model-year CATL battery pack has a very real probability of having passed through a GEM high-pressure acid leach autoclave in Morowali, Indonesia, or through a shredder line at a GEM recycling facility in Jingmen, Hubei. The company operates as infrastructure: invisible, critical, and stubbornly profitable in a business where most competitors fail.

This episode is the story of how a college professor with an obsession about waste became the architect of China's "closed-loop" battery supply chain. It is a story about contrarian thinking—betting on EVs a decade before most industrial investors had heard of Tesla. It is a story about vertical integration pushed downward, toward the garbage, rather than upward, toward the customer. And it is a story about what the 21st-century mining industry actually looks like: less pit and more process, less geology and more chemistry, less sovereign concession and more municipal waste collection contract.

By the end, a single question frames the investment case. Is GEM a recycler? A chemical company? A miner? The answer, as the company's Chairman likes to say, is "none of the above and all of the above." GEM is a resource security company, and in a world where the US Inflation Reduction Act, the EU Critical Raw Materials Act, and China's own industrial policy have all converged on the same conclusion—that batteries are the new oil—resource security is about as good a business as there is.

Let's start where the story actually begins, in a university laboratory in central China, with a professor who refused to accept that garbage was garbage.

II. Founding & The "Waste as Wealth" Origin

Xu Kaihua was not supposed to be a businessman. Born in 1963 in Hubei province, he came of age in the aftermath of the Cultural Revolution, when university seats were rationed and scientific careers were rebuilding from a lost decade. He trained as a metallurgist at the Central South University of Technology in Changsha—one of the handful of Chinese institutions that had continued to do serious work in non-ferrous metals throughout the tumult of the 1960s and 1970s. By the mid-1990s he was a tenured professor and a respected expert on cobalt and nickel recovery chemistry, publishing papers on hydrometallurgical extraction that nobody outside a few specialist journals was reading.

What changed Xu's life was a sabbatical observation. In the late 1990s, as China's consumer electronics boom was cresting—every coastal family suddenly owned a color television, a refrigerator, a washing machine—a parallel phenomenon was emerging. Old appliances were not going anywhere. They piled up in courtyards, in alleys, at the edges of cities. Informal scrappers burned the plastics off wires in open fires. Acid baths used to strip gold from connectors were dumped into drainage ditches. The environmental cost was catastrophic. And yet the economic logic was real. There was genuine value in the waste.

Xu's insight was that this informal, polluting, economically irrational activity was signaling something important. If uneducated migrants with hand tools could make a living pulling metals out of trash, then a proper industrial-chemical operation with real engineering could make an enormous business out of the same input stream. The phrase he coined, and that became GEM's philosophical foundation, was deceptively simple: "Waste is not garbage, but a misplaced resource." In Chinese it rhymes and has a kind of classical cadence. In English it reads like a slogan. But behind it sits a real metallurgical argument. The concentration of valuable metals in modern electronics is genuinely higher, sometimes by orders of magnitude, than in natural ore bodies. The entire cost structure of mining—drilling, blasting, hauling overburden, processing low-grade ore—could be leapfrogged if you started with the right kind of feedstock.

In 2001, Xu left his academic post and founded Shenzhen GEM High-Tech Co., Ltd. The "GEM" stood for Green Eco-Manufacture, which was both corporate branding and genuine ideology. The initial capital was modest, the technology was crude by later standards, and the first product lines were completely unsexy. GEM started by recycling old televisions and circuit boards, recovering copper, precious metals, and assorted non-ferrous materials. A parallel business line focused on tungsten carbide and cobalt powders, the feedstock for industrial cutting tools. This was not a glamorous business. It was dusty, chemical-intensive, and served a mature industrial customer base. But it taught the young company two things that would define it forever.

The first was that the feedstock problem—getting a reliable, regular, quality-controlled stream of waste material—was the hard part. Chemistry was solvable. Logistics and relationships were not. GEM had to build recycling networks with municipal authorities, with waste haulers, with informal scrappers that it gradually formalized. Over the first decade, the company methodically secured operating permits and collection agreements across eleven Chinese provinces. This network became the moat. Anyone could theoretically build a hydrometallurgical plant. Almost no one could replicate the permit stack, the government relationships, and the collector network that fed it.

The second lesson was that Chinese regulators, once they decided to care about environmental compliance, would care with a vengeance. Starting in the mid-2000s, Beijing began systematically cracking down on informal e-waste processing. The acid-dumping, wire-burning, backyard-smelting ecosystem was steadily criminalized. For GEM, which had been investing in proper effluent treatment and closed-loop chemistry from day one, this was a windfall. Competitors were shut down. Collection streams consolidated toward licensed operators. The company that had built the expensive, regulated way suddenly had a structurally advantaged business.

In January 2010, GEM listed on the Shenzhen Stock Exchange under the ticker 002340.SZ. The prospectus described it as China's first "circular economy" public company. The IPO raised modest capital by later standards but achieved something more important: it announced to a generation of Chinese policymakers and industrialists that turning waste into metal was a legitimate, investable, scalable business. The prospectus language—closed loops, urban mining, resource recycling—would within a decade become central planning vocabulary.

What nobody reading that 2010 prospectus could fully appreciate was how perfectly the company was positioned for the next wave. Xu had built an infrastructure for cobalt and nickel recovery just as the world was about to demand those two metals in quantities that no existing mining industry could meet. The pivot was coming.

III. The Great Inflection: The Battery Pivot

In 2012, if you asked a room full of commodity analysts what the next big demand shock for nickel and cobalt would be, almost none of them would have said electric vehicles. The Chevy Volt had just launched to mixed reviews. Tesla's Model S was still shipping its first units. BYD was mostly known as a conventional carmaker with a weird sideline in lithium iron phosphate buses. Lithium-ion batteries were understood primarily as a laptop and cellphone technology, and the entire global market for battery-grade cobalt was measured in low tens of thousands of tons per year.

Inside GEM, however, Xu Kaihua was looking at a different set of signals. China's central government had begun issuing subsidies for new energy vehicles. The Ministry of Industry and Information Technology was drafting the battery industry development plan that would become the backbone of the country's EV strategy. Domestic cell makers—CATL had only been founded in 2011, but it was already winning tenders—were scaling their ambitions. And the chemistry that all of them were betting on, for automotive applications, was ternary: nickel-cobalt-manganese cathodes, abbreviated NCM, offering the energy density required for passenger vehicle range. Every one of those cathodes required a precursor, a specific crystalline powder of mixed nickel-cobalt-manganese hydroxide, manufactured to demanding specifications. And that precursor was made from exactly the two metals that GEM had spent a decade learning how to extract from waste.

The pivot, in retrospect, looks obvious. At the time it was bold. GEM reorganized around a new thesis: rather than selling recovered cobalt sulfate and nickel sulfate as commodity intermediates to anonymous trading desks, the company would integrate forward, manufacturing the value-added precursor powders directly. This was the difference between selling flour and selling cake mix. The margin structure was fundamentally better, the customer relationships were longer-lived, and the technical barriers—precursor manufacturing requires tight particle-size control, consistent morphology, and demanding impurity tolerances—meant that price-based competition would be blunted by qualification hurdles.

To execute the pivot, GEM invested heavily in precursor capacity during the middle of the decade, first at its Jingmen complex in Hubei and then at additional sites in Jiangsu and Fujian. By the late 2010s the company had lined up supply agreements with essentially every major Chinese ternary cathode producer and, through them, with the big cell makers. The strategic logic extended beyond chemistry. Because GEM simultaneously operated the upstream recycling network, it could feed a meaningful portion of its precursor output with metal units recovered from scrap rather than sourced from newly mined ore. That "closed loop" was not just an ESG narrative. It was a real cost and geopolitical hedge.

But pivoting into battery precursors created a new problem, one that Xu had underestimated. As GEM's precursor volumes scaled, the company found that its recycling network—already the largest in China—could only supply a fraction of the nickel and cobalt it needed. The rest had to be purchased on the open market, exposing GEM to the same commodity volatility that every non-integrated precursor maker faced. The Shanghai cobalt price could double in a year. Nickel could swing forty percent in a quarter. For a company whose moat was supposed to be feedstock security, being a price-taker on fifty-plus percent of its input was an uncomfortable position.

There was only one durable solution: go upstream to where the metal came out of the ground. And by the late 2010s, for nickel specifically, every serious analyst knew that only one country really mattered. Indonesia had emerged as the decisive marginal producer of nickel in the world, sitting on vast laterite deposits of relatively low-grade but enormously abundant ore, and the Jakarta government had banned raw ore exports in an explicit industrial-policy bid to force downstream processing on Indonesian soil. For GEM, following the metal to its source meant following it to Sulawesi. The company that had begun by picking through Chinese trash heaps was about to become a tropical miner.

IV. Securing the Upstream: The Indonesia Gamble

The Morowali Industrial Park sits on the eastern coast of the Indonesian island of Sulawesi, a muddy, humid, tropical expanse of reclaimed coastline, coal-fired power plants, dormitory blocks, and steaming metallurgical complexes. If you visit, what strikes you first is the sheer industrial density of it. In the space of a single bay, dozens of nickel smelters and chemical plants operate twenty-four hours a day, producing a meaningful share of the world's stainless steel feedstock and, increasingly, the battery-grade nickel that powers the global EV fleet. The man who built Morowali was Xiang Guangda, founder of Tsingshan Holding Group, and the phrase that describes his operating philosophy inside Chinese industrial circles is, roughly translated, "speed over perfection." Tsingshan is China's nickel king. It does things bigger, faster, and cheaper than any Western competitor believes is possible.

In 2018, GEM announced a joint venture at Morowali that would define its next decade. The QMB New Energy project paired GEM with Tsingshan and with CATL, China's dominant battery cell maker. The three-way structure was elegant. Tsingshan brought the nickel ore, the site, the permitting relationships with Jakarta, and the operational speed. GEM brought the hydrometallurgical process design, the precursor-grade chemistry expertise, and the end-product demand profile. CATL brought the ultimate downstream pull, committing to offtake the battery-grade nickel that the joint venture would produce. It was one of the first genuinely integrated "mine to cathode" partnerships in the global battery industry, and it was struck years before most Western automakers had even begun to think about sourcing raw materials directly.

The technology at the center of the bet was High-Pressure Acid Leach, or HPAL. This is the critical explanation to understand, so let's slow down. Indonesian laterite nickel ore is not like the sulfide ore that most traditional nickel miners process. It is a weathered, relatively low-grade material that cannot simply be smelted for battery-grade output. To get battery-grade nickel sulfate from laterite, you have to dissolve the ore in sulfuric acid under high pressure and temperature inside massive autoclaves, precipitate the nickel selectively, and clean it to extremely tight purity specifications. HPAL is a notoriously difficult process. Western majors, including BHP and Vale, had tried and largely failed to operate HPAL plants profitably over the preceding two decades, racking up billions of dollars in cost overruns and missed production targets at projects in Australia, New Caledonia, and the Philippines. HPAL had a reputation as a technology that could not be done cheaply.

GEM's bet, alongside Tsingshan, was that this reputation was a legacy of Western capital cost structures and project management habits rather than an inherent technological limit. The Chinese consortium built Morowali HPAL plants using modular design principles, Chinese engineering and construction services, and aggressive schedule compression. The reported capital intensity, measured in dollars of investment per annual ton of nickel capacity, came in well below the benchmarks set by the best Western HPAL projects. Whether that delta was sustainable through full ramp-up, environmental remediation, and long-cycle maintenance remained a question. But in the short and medium term, the cost advantage translated directly into margin headroom in the nickel sulfate business.

For GEM specifically, the Indonesia initiative did three things simultaneously. It secured a long-term supply of battery-grade nickel at below-spot-market effective costs, shielding the precursor business from input volatility. It transformed the company's business profile from a pure recycler-processor into a hybrid miner-recycler, with the attendant benefits and risks of an upstream exposure. And it sent a clear signal to GEM's downstream customers—the cell makers and, behind them, the automakers—that the company intended to control its destiny at every stage of the supply chain.

The risks were equally clear. Jakarta's export policy could shift with the political winds. Environmental controversy around HPAL tailings disposal, particularly the deep-sea tailings placement methods used at some Indonesian projects, carried reputational risk in European and North American markets where battery buyers increasingly cared about supply chain provenance. And the nickel price itself, notoriously volatile, could swing dramatically enough to render integration economics temporarily unfavorable. The 2022 nickel short squeeze on the London Metal Exchange, which caused Tsingshan itself to take multi-billion-dollar trading losses, was a reminder of how treacherous this commodity could be.

But on balance, through the end of the 2024 and into 2025 operating period, the QMB bet had paid off. Capacity ramped, offtake flowed, and GEM's precursor business was increasingly supplied by captive metal units rather than open-market purchases. For a company whose founding thesis was feedstock sovereignty, Indonesia had delivered exactly what it was supposed to deliver.

The question now is whether the people at the top of the company can steward this integrated platform through the next stage of its evolution. That depends, as it always does in a founder-led Chinese industrial, on the founder.

V. Management & The "Professor's" Culture

Walk into GEM's Shenzhen headquarters and the first impression is not that of a typical Chinese industrial conglomerate. There are no marble lobbies, no oversized portrait walls, no ostentatious displays of political connections. The decor leans toward the functional-academic: whiteboards filled with reaction equations, framed patents, a small museum display of recovered metal samples ranging from silver to palladium to neodymium, each labeled with the waste stream it came from. The aesthetic matches the founder. Xu Kaihua, now in his early sixties, still carries himself like the metallurgical professor he once was, more comfortable discussing extraction kinetics than stock-market narratives, known inside the company for personally reviewing technical papers produced by the R&D division and occasionally authoring them.

Xu's shareholding is channeled primarily through Shenzhen Zhongjin Industrial Co., his holding vehicle, which controls a large block of GEM shares sufficient to keep him firmly in the driver's seat on any strategic decision. He has not done what many Chinese industrial founders did during the boom years of the 2010s and 2020s, which is to cash out heavily at peak valuations and pivot to family-office mode. He remains visibly operational, still attending major plant commissioning ceremonies, still signing off on multi-billion-yuan capital expenditure decisions, still traveling to Indonesia for site reviews. In a peer group populated by flashier entrepreneurs, his personal brand is the absence of a personal brand.

Alongside Xu, the most important executive figure at GEM over the past decade has been Wang Min, who has served in senior executive roles overseeing the battery materials business and corporate development. The partnership between Xu and his senior operating team reflects the deliberately engineered culture of GEM: long tenures, technical depth, and personal continuity. In an industry where mid-career chemical engineers are routinely poached by cell makers and precursor competitors willing to pay salary premiums of fifty percent or more, GEM has kept its core technical leadership largely intact. The retention mechanism is partly cultural—Xu's personal recruitment and mentoring of young researchers from his alma mater network—and partly structural, through a series of employee stock ownership plans and partnership-equity arrangements that have given middle-management engineers meaningful long-term economic participation in the business.

The R&D intensity tells its own story. GEM has consistently reinvested a share of revenue into research and development that runs several multiples above what a commodity recycler would typically spend. This is not a one-year marketing number. It is a sustained, decade-plus pattern, and it has produced a substantial patent portfolio in hydrometallurgical extraction, precursor synthesis, and process engineering. Xu, to the amusement and occasional exasperation of his CFO, insists on treating R&D as the company's long-term capital base. When asked why a recycling company needs the R&D profile of a pharmaceutical, his answer tends to be some version of: the gap between 95% recovery and 99% recovery is the entire margin of the business. That gap is a research problem.

The governance picture is not entirely without blemishes. GEM has, over the years, executed capital markets transactions—secondary equity issuances, convertible bonds, the 2022 GDR listing on the Swiss exchange—that have occasionally diluted minority shareholders. Related-party transactions with the founder's holding vehicles and with supply-chain partners require careful reading of the annual report footnotes. Some analysts have flagged episodes of aggressive revenue recognition or working-capital management that deserve scrutiny. None of this is uncommon in Chinese industrials and none of it rises to the level of a red flag in the forensic-accounting sense, but it is the kind of governance texture that long-term fundamental investors need to track rather than ignore.

The cultural tone at the top is what drives the strategic decisions. Xu's worldview is what he calls "technological idealism"—a conviction that the right technology, pursued patiently enough, will eventually out-compete business models built on financial engineering or regulatory arbitrage. That idealism has made GEM bet on unglamorous businesses, recycled streams, and circular-economy narratives for years longer than the market was willing to reward. It also means that when the market did turn, in the EV supercycle of the early 2020s, GEM was already positioned where a dozen newer competitors were only beginning to arrive.

That long-term patience has produced a portfolio of businesses that, individually, range from obvious to surprising. The battery materials business gets the headlines. But underneath it sit several other lines of activity that, while less prominent, do a meaningful share of the financial work.

VI. The Hidden Businesses: Tungsten & Scrapped Cars

If the battery precursor business is GEM's narrative engine, the tungsten carbide and ultra-fine cobalt powder business is its cash metronome. Tungsten carbide is the material used to make the cutting tips of industrial drill bits, lathe tools, and machining inserts. It sits quietly inside every machine shop in the world. The market is mature, the customer base is fragmented, and the chemistry is mostly stable. GEM's entry into this business traces back to the company's original non-ferrous metals focus, and the firm has steadily accumulated a position as one of the largest global producers of the ultra-fine cobalt powders that go into premium tungsten carbide grades. This is a business that does not grow at EV-industry rates. But it also does not collapse when nickel prices wobble. It is what finance textbooks call a cash cow, and in a company whose growth capex is heavy and whose battery-business revenues are correlated with a small number of end markets, having a stable, uncorrelated cash line is structurally valuable.

The second quiet business that merits attention is the automobile dismantling initiative. China retired something on the order of two million-plus end-of-life vehicles annually through the early 2020s, and that number is trending sharply upward as the first wave of mass-motorization vehicles from the 2000s reach their scrap date. Every one of those vehicles contains copper, aluminum, platinum-group metals in the catalytic converter, lead in the battery, various electronics, and increasingly, in the case of retired EVs, lithium-ion battery packs. GEM has spent the last several years building a network of formal automobile dismantling facilities, engineered from the ground up with automation, component-level recovery, and environmental controls that no informal scrapper can match. The business is still small relative to battery materials, but the long-term logic is identical to the company's founding thesis: as regulation forces scrap volumes toward licensed operators, the players with scale and process expertise capture the economics.

A third and smaller line focuses on waste plastics, targeting the growing European and increasingly North American demand for recycled-content polymers in consumer and industrial goods. The economics of plastic recycling are chronically difficult because virgin plastic is cheap and the sorting challenges are real, but for downstream buyers with ESG mandates—particularly large consumer brands under shareholder and regulatory pressure to reduce virgin plastic usage—the ability to buy certified recycled polymer carries a meaningful price premium. GEM has positioned its plastics business to serve exactly this premium tier, and while the financial contribution is modest, the strategic signaling value to global customers evaluating GEM's overall sustainability credentials is not.

Lastly, the company operates a collection of smaller, specialized recycling and materials lines—printed circuit boards, cobalt-nickel waste from cemented carbide operations, certain rare-earth recovery streams—that collectively add up to a meaningful contribution but individually do not move the needle. These matter mostly because they represent optionality. If, in the late 2020s, rare earth processing becomes the next geopolitical flashpoint in the U.S.–China trade relationship (it arguably already has), GEM has a quiet, technical foothold in parts of that supply chain that would be non-trivial to replicate from scratch.

The segment picture that emerges is of a company whose headline exposure is ternary battery precursor and nickel, but whose underlying business mix is considerably more diverse than the sell-side reports typically capture. This is consequential. A pure-play battery-materials company is a pure-play cyclical. GEM is a cyclical core with several semi-counter-cyclical appendages, and those appendages matter most in the years when the main cycle turns against the business.

Understanding the cycle, the moats, and the way the competitive landscape shapes GEM's long-term economics is the next question. This is where the analytical frameworks start earning their keep.

VII. The Playbook: 7 Powers & 5 Forces Analysis

Hamilton Helmer's Seven Powers framework is a useful scalpel for dissecting durable competitive advantage, and GEM is one of those rare industrial businesses where at least three of the seven powers show up clearly rather than as narrative stretches.

The first and most important is what Helmer calls Cornered Resource. In GEM's case, the cornered resource is not a mine, a patent, or a contract. It is the recycling network itself: the licenses, the collection agreements, the municipal relationships, and the informal local ties that together allow the company to aggregate end-of-life batteries and electronics at scale. In China, this network has real teeth. Chinese environmental regulations, progressively tightened through the 2010s and enforced with increasing seriousness through the 2020s, have effectively barred informal operators from handling hazardous e-waste. Licensed operators with proper permits across the disassembly, hydrometallurgical processing, and chemical engineering stages are scarce, and GEM's footprint across eleven-plus provinces puts it in a small peer group. Replicating this network would require not only capital but years of government relationship building, something that a new entrant cannot simply write a check for.

The second power is Scale Economies. Hydrometallurgical processing is a fixed-cost-heavy, batch-and-continuous flow business where unit costs decline materially with throughput. A plant processing one hundred thousand tons of battery scrap annually has dramatically lower per-ton economics than a plant processing ten thousand tons. GEM's investment over the past decade has concentrated volumes at a small number of large, technically sophisticated sites, and the resulting cost curve puts the company in the lowest tier of the industry by processing cost per ton of recovered metal unit. Scale economics in a commodity-adjacent business are not a glamorous moat, but they are a durable one.

The third power is Process Power—the accumulated know-how, operational tuning, and tacit engineering knowledge that makes a complex industrial process run reliably at scale. Battery recycling, at the black-mass-to-refined-metal stage, is a genuinely hard chemistry problem. Recovery rates of 98% versus 95% are the difference between profit and loss for a given ton of input. GEM has spent two decades optimizing its process flow, to a degree that internal recovery rates reportedly approach the high-nineties across nickel, cobalt, and increasingly lithium. A new entrant can buy the same process equipment, but it cannot buy twenty years of operational learning.

The other four powers in Helmer's framework—switching costs, counter-positioning, branding, and network economies—do not really apply to GEM in the classical sense. Precursor buyers can qualify multiple suppliers and do. Brand is essentially irrelevant in B2B industrial chemistry. Network economies don't operate in a materials business. The company is therefore a three-power franchise: cornered resource, scale economies, and process power. By industrial standards, that is a strong profile.

Applying Porter's Five Forces as a cross-check surfaces the other side of the picture. The threat of new entrants in GEM's core businesses is genuinely low, for the reasons just described: permits, scale, and process learning all take years to accumulate. The bargaining power of suppliers is mixed. On the recycling side, GEM is effectively the consolidator, with leverage over fragmented scrap supply. On the newly mined nickel side, GEM's Indonesian positioning has materially reduced the leverage of third-party sellers. The bargaining power of buyers is more of a live issue. GEM's downstream customers are concentrated—a relatively small number of cathode and cell makers account for the bulk of precursor demand—and these customers have their own captive recycling initiatives (notably Brunp, which is CATL's recycling arm). This matters. CATL is simultaneously GEM's largest customer category, its joint-venture partner in Indonesia, and, through Brunp, its most formidable competitor. Competitive rivalry within Chinese precursor manufacturing is intense, with multiple players of real scale competing on cost, quality, and customer relationships. Margins in precursor are decent but compressed relative to the gold-rush years of the late 2010s. Finally, threat of substitutes is the one genuinely important swing variable, and it deserves its own paragraph.

The substitute threat in GEM's case is not a competing technology in the precursor space. It is a different battery chemistry altogether. Lithium iron phosphate, the LFP chemistry pioneered in China by BYD and now adopted by much of the cost-sensitive EV and stationary storage market, contains no nickel and no cobalt. As LFP penetration rises in the global EV market—and through 2024 and 2025 it has been rising faster than almost any forecaster expected—the addressable market for nickel-cobalt-based precursors becomes relatively smaller. This does not eliminate ternary. Long-range premium EVs, much of the U.S. market, and most European applications continue to favor higher-nickel chemistries for their superior energy density. But the bull case for GEM is materially softer if LFP ends up claiming seventy percent of the global battery market rather than, say, fifty percent.

The substitute threat is thus the single most important variable in the long-term valuation story, and it is the natural gateway to the bull-bear debate.

VIII. The Bear vs. Bull Case & Investing Lessons

The bear case for GEM is built primarily on chemistry and geopolitics. The chemistry argument is simple: if the global battery mix shifts decisively toward LFP, sodium-ion, or other post-ternary architectures, the economic value of GEM's recycled nickel-cobalt stream compresses. There is still value in recycling lithium and other common elements, but the margin structure of a lithium-iron-phosphate recycling business is a shadow of the margin structure of a nickel-cobalt recycling business, for the straightforward reason that iron and phosphate are cheap whereas nickel and cobalt are not. Even in a world where ternary retains a meaningful share of the premium segment, the price trajectory for battery-grade nickel sulfate and cobalt sulfate has been volatile and not uniformly upward. Analysts who built models assuming steady-state nickel prices in the high teens of thousands of dollars per ton have repeatedly watched those prices collapse back toward cost-curve levels as Indonesian supply came online.

The geopolitical argument is more nuanced. GEM's Indonesian exposure is a double-edged sword. On one hand, Morowali and the QMB complex are the reason GEM has a cost-advantaged nickel position in the first place. On the other hand, Indonesia has shown itself willing to reshape policy around extractive industries with very little notice. The mineral export ban that forced downstream processing onshore in the first place is the positive expression of this policy activism. Potential future policy actions—royalty changes, environmental enforcement, domestic-ownership rules—are the risk side of the same coin. Additionally, Chinese-operated HPAL facilities in Indonesia face growing scrutiny from Western automakers and European regulators over environmental practices, particularly deep-sea tailings disposal. If end buyers start meaningfully penalizing Indonesian-Chinese nickel on sustainability grounds, GEM's cost advantage could be partially eroded by a provenance discount.

Layered on top of these two core bear arguments are the standard governance and accounting concerns that attach to Chinese industrial equities. Related-party transactions, aggressive capex accounting, complex subsidiary structures, and the general opacity of certain Chinese reporting disclosures are all genuine risks. None of these issues, as of the 2024 annual reporting cycle, have escalated into a material restatement or auditor action at GEM, but they are the kind of overhang that serious allocators have to spend time on.

The bull case starts from a different observation. Ternary chemistry is not going away. The performance envelope of high-nickel cells, measured in energy density per kilogram and per liter, remains meaningfully ahead of LFP at the cell level. For applications where weight and range matter—premium passenger EVs, long-haul commercial vehicles, much of the aerospace and defense envelope, and essentially all current-generation BMW, Mercedes, and higher-end Tesla products—ternary continues to win on engineering merit. The battle between ternary and LFP is not a technology-replacement story in the way that flat-panel televisions replaced cathode-ray tubes. It is a market-segmentation story, and ternary's segment is the high-value, high-margin one.

Within that segment, GEM's closed-loop business model, in which the company takes end-of-life battery packs from automakers and supplies back precursor materials for new battery production, creates a remarkably sticky customer relationship. GEM's partnerships with European automakers like BMW and Mercedes—formalized through long-term cooperation agreements beginning in the late 2010s and expanding subsequently—are genuinely differentiated. For a premium automaker trying to build a sustainability narrative around its EV lineup, being able to credibly claim that end-of-life battery packs are returning to the supply chain as new battery materials is a real marketing and compliance asset. That asset is not easy to replicate, because it requires a recycler with proven process economics, sufficient scale to handle automotive-size volumes, and credible environmental compliance across multiple jurisdictions. GEM has each of those three attributes.

The bull case also leans on the "integrated across the stack" argument that is the through-line of this whole episode. GEM is simultaneously upstream (Indonesian nickel), midstream (hydrometallurgical processing and precursor manufacturing), and downstream-facing through its closed-loop partnerships. Pure-play recyclers, pure-play precursor makers, and pure-play miners all face the structural problem that somewhere in their value chain, they are a price-taker. GEM is a price-taker at fewer nodes than almost any peer. That integrated position produces a mid-cycle margin profile that the unintegrated competitors cannot match, and it means that GEM's earnings, while cyclical, should bottom less painfully and peak more sustainably through a full commodity cycle.

What are the KPIs that matter for tracking GEM's ongoing performance? Three variables deserve the bulk of the attention. First, ternary precursor shipment volumes, which measure the company's participation in the battery materials market and its share of a competitive category. Second, recovered metal volumes from recycling—particularly nickel, cobalt, and lithium—which measure the utilization of the cornered-resource network and the gradual scaling of the closed-loop proposition. Third, Indonesian nickel sulfate output and cash-cost positioning, which measure the payoff of the QMB bet and the company's raw-material self-sufficiency. Revenue and reported earnings are consequences of these three underlying operational variables. If the three move in the right direction, the P&L follows. If they stall, the P&L stalls.

The investing lesson beneath all of this is perhaps the most important takeaway of the GEM story. In an age obsessed with software platforms and network effects, capital-intensive industrial businesses can still build durable franchises—but they do it by being the low-cost, high-process-skill provider and by integrating vertically in the unsexy direction, toward the feedstock, rather than the sexy direction, toward the customer. GEM did not build a brand. It built a permit stack, a recycling network, a chemical process, and a tropical HPAL position. The result is a business that looks like infrastructure rather than a product, and that is a business model with staying power.

The final question is what comes next, and here the story opens up geographically in ways that the founding professor probably could not have imagined when he first sketched out a waste-recovery business plan in 2001.

IX. Epilogue: The Global Ambition

In July 2022, GEM completed the issuance of global depositary receipts on the SIX Swiss Exchange, making it one of the first wave of Chinese A-share companies to pursue a dual listing in Zurich under the cross-border scheme negotiated between Beijing and Bern. The GDR listing raised international capital and, more importantly, put the company's balance sheet and narrative in front of European institutional allocators in a way that a Shenzhen-only listing never could. The capital was earmarked for international expansion, and specifically for Europe and Korea.

The European expansion made strategic sense for reasons that go beyond capital structure. European automakers—BMW, Mercedes, Stellantis, Volkswagen—have been among GEM's most important long-term customer relationships. The European Union's Critical Raw Materials Act, the U.S. Inflation Reduction Act, and the broader geopolitical tilt away from dependence on Chinese supply chains have all created a regulatory environment in which battery materials produced inside Europe, or at least outside China, carry a premium in automotive procurement contracts. For GEM, building out plants in Europe—Hungary has been a particular focus, alongside evaluation of additional sites—is less about winning new customers and more about preserving the right to keep serving existing ones under the new rules of the game.

The Korean expansion is complementary. Korea is home to LG Energy Solution, Samsung SDI, and SK On, three of the world's most important battery cell manufacturers, and historically the Korean cell industry has sourced substantial amounts of precursor material from Chinese suppliers. As the geopolitical map has shifted and as Korean cell makers have scaled their North American operations in response to IRA-driven incentives, they have needed precursor suppliers with non-Chinese production footprints. GEM's Korean joint venture initiatives, entered into with several partners starting in the early 2020s, position the company to continue serving those customers from politically acceptable production sites.

The larger pattern is unmistakable. A company that spent its first two decades building the densest battery-materials infrastructure inside China is now methodically replicating pieces of that infrastructure outside China, not because the domestic market is shrinking, but because the global market is bifurcating and the company needs production footprints on both sides of the bifurcation to preserve its role in the supply chain. This is the inverse of the geographic expansion patterns that defined Western multinationals in the 1990s and 2000s, when U.S. and European companies built production capacity in China because China was the low-cost manufacturing base. Now, Chinese industrial leaders are building production capacity in Europe and Korea because politics requires them to.

What the global expansion does not do is fundamentally alter the identity of the company. At its core, GEM remains what Xu Kaihua designed it to be. It is not primarily a chemicals company, although it runs sophisticated chemistry. It is not primarily a mining company, although it now owns equity in Indonesian nickel operations. It is not primarily a recycler, although it operates the largest battery recycling network in China. It is a resource security company. Its product is not any particular output of its factories. Its product is the continued availability, at stable cost, of the specific material inputs that its customers need to build the batteries that power the energy transition.

In the 20th century, the wealth of nations was shaped by the ability to extract hydrocarbons and metals from the ground. The companies that won the 20th century—Standard Oil, Rio Tinto, BHP, Alcoa—were fundamentally extractive enterprises whose competitive moats were land, concessions, and geological luck. In the 21st century, the geography of resources is being rewritten. The most valuable cobalt deposit in the world may not be in the Congo. It may be in a warehouse in Jingmen, Hubei, filled with retired battery packs from 2018-vintage electric buses. The most valuable nickel operation may not be a legacy mine in Canada. It may be an HPAL plant in Morowali whose raw material came off a barge from a few kilometers away. The most valuable platinum stream may not be a smelter in South Africa. It may be an automobile dismantling line in eastern China.

GEM, in other words, is proving that the next generation of resource companies will be defined not by what they pull out of the earth but by what they pull back out of our past. The metals that the 20th century spent mining did not disappear when they were used. They were embedded in products that we are only now learning how to take apart. And the companies that learn how to take them apart, at scale, under regulatory cover, with the right chemistry, will be the quiet utilities of the energy transition.

Whether GEM's specific equity trajectory rewards long-term investors is a question that depends on battery chemistry choices, commodity price cycles, Chinese regulatory evolution, Indonesian political stability, European permitting timelines, and the founder's ability to keep building an unusual company in an increasingly normal industry. None of these variables is easy to forecast. But the underlying thesis—that waste is a misplaced resource, and that the company which figures out how to put those resources back in the right place captures a durable economic position—has held up for a quarter century. It is not obvious why it should suddenly fail to hold up now.

The professor was right. The mines of the future are in our trash cans. GEM is the company that noticed first.

Top 5 "Long-Form" Links for Further Research

- GEM's 2023 Annual Report: the detailed breakdown of the Indonesia HPAL ramp-up, segment economics, and capital expenditure schedule.

- "Urban Mining in China": the academic literature on metal recovery from e-waste, including papers authored or co-authored by Xu Kaihua.

- The QMB New Energy joint venture disclosures: partnership economics between GEM, Tsingshan, and CATL, including offtake and governance structures.

- S&P Global Commodity Insights: benchmarking nickel-cobalt-manganese precursor margins, Chinese vs. Korean vs. Western pricing structures.

- Tungsten Carbide Industry Review: understanding the "hidden" cash cow business that funds GEM's riskier bets in battery materials.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube