BDStar: The Silicon Heart of the Beidou Dream

I. The "Sputnik" Moment: Introduction & Roadmap (0:00 – 0:10)

Picture a foggy morning at the Xichang Satellite Launch Center in Sichuan Province. It was June 23, 2020, and a Long March-3B rocket was preparing to punch through the clouds carrying the final satellite of China's Beidou-3 global navigation constellation. When that rocket lit up the sky, something quietly seismic happened in global technology. After more than a quarter century of incremental work, China became only the third power—after the United States and Russia—to operate its own global satellite navigation system. The Americans had GPS. The Russians had GLONASS. Now China had Beidou.

But here's the thing nobody outside China's technology ministries quite grasped at the time. A satellite constellation is, in a way, the easy part. You launch a rocket. You park a satellite in geostationary or medium-earth orbit. You broadcast a signal. The hard part—the truly generational, civilization-level hard part—is the tiny piece of silicon inside a farmer's tractor in Hebei, or a DJI drone floating over a wedding in Shenzhen, or the automotive ADAS stack helping a Nio sedan hold its lane on the G4 expressway. That silicon listens to the constellation. It takes a shower of faint radio signals from twenty thousand kilometers away, performs mathematical miracles, and tells the machine where it is on the planet to within a centimeter.

The company that makes more of that silicon than anyone else in China—and increasingly, outside of it—is a firm most Western investors have barely heard of. Its name is Beijing BDStar Navigation Co., Ltd., ticker 002151 on the Shenzhen Stock Exchange. The "BD" in BDStar stands for Beidou. The star is literal.

Today on Acquired, we tell the story of how a small trading outfit founded in the year 2000—a company that started its life selling Canadian GPS receivers to Chinese surveyors out of a modest Beijing office—transformed itself into what is essentially the Qualcomm of China's satellite navigation stack. This is the story of Zhou Ruxin, a former state-enterprise engineer who walked away from a secure government-adjacent career to build a private company just as China was first gambling on its own sovereign space program. It is also the story of a uniquely Chinese corporate form: the "national champion" that exists simultaneously as a profit-maximizing public company and as a load-bearing pillar of national industrial policy.

The scope of this episode is enormous. We're not just talking about GPS. We're talking about the positioning chips inside DJI's Mavic drone line. We're talking about the high-precision antennas that allow John Deere-style autonomous tractors to plant corn in perfectly straight rows across Heilongjiang's black soil. We're talking about the centimeter-level correction services that are beginning to underwrite China's entire autonomous driving narrative. And we're talking about 22-nanometer system-on-chip designs being taped out at a Beijing-headquartered firm with a market capitalization somewhere between a mid-cap industrial and a large-cap specialty semiconductor name.

Three themes will anchor our narrative. First: the tension between national strategic imperatives and commercial survival. BDStar has had to serve two masters for its entire corporate life—Beijing's industrial policy planners on one hand, and public market shareholders on the other. Second: the "buy-to-build" M&A playbook. BDStar grew not by organic R&D alone but by aggressively acquiring Chinese antenna leaders, German automotive electronics firms, and domestic chip design houses, stitching them together into something resembling a vertically integrated positioning stack. Third: the quiet shift from selling boxes to selling bits—the transition from hardware volumes to what we will call "Positioning-as-a-Service," the nascent but potentially enormous cloud business that sits on top of the silicon.

Let's begin at the beginning, in a very different Beijing than the one that launched a global constellation in 2020.

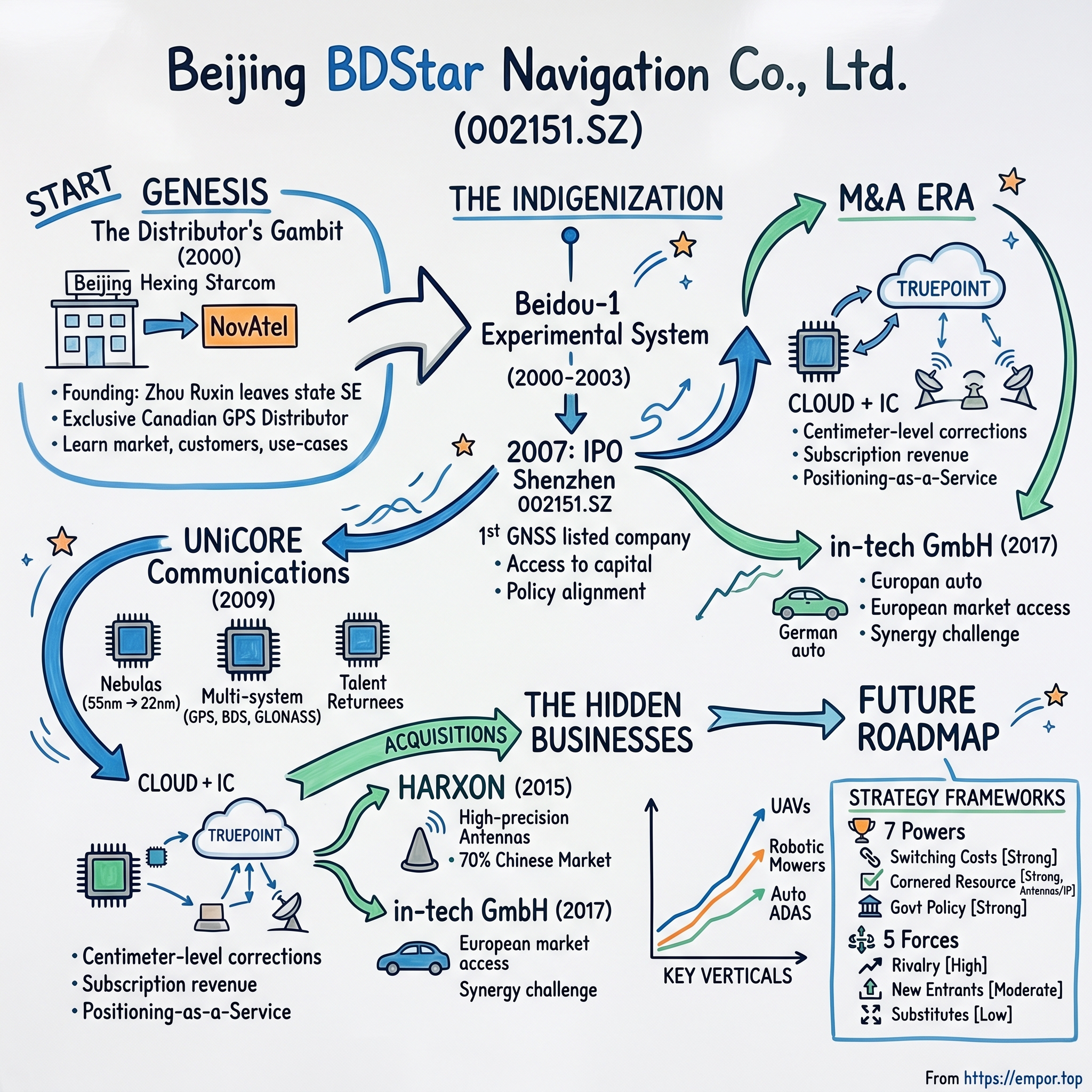

II. Genesis: The Distributor's Gambit (0:10 – 0:30)

The year was 2000. Beijing was preparing for a bid to host the Olympics. The Chinese internet sector was still figuring out what a portal was. And inside a state-linked electronics research institute, a mid-career engineer named Zhou Ruxin was making one of those decisions that sound pedestrian on a resume but rewire a human life. He was leaving. A stable position, a danwei, a career track that in the late 1990s still came with an apartment and medical benefits and the quiet social cushion of a ministry affiliation. He was walking away to start a private company.

To appreciate how unusual that was, you have to understand the texture of the Chinese technology scene in 2000. Lenovo had only recently emerged from Legend Group. Huawei was still largely a domestic telecom equipment supplier. ZTE was state-owned. The idea of a private, professionally managed technology company—especially in anything adjacent to defense or national infrastructure—was an exotic and slightly suspicious proposition. Zhou's bet was that a sliver of the satellite navigation industry, a sliver too specialized and too small for the big state-owned enterprises to bother with, could be privately owned, privately run, and eventually privately listed. He was right, but the path was nothing like linear.

The company Zhou founded with a handful of colleagues—initially called Beijing Hexing Starcom, later consolidated under the Beijing BDStar Navigation name—did not design chips. It did not make antennas. It did not build satellites. It distributed other people's products. Specifically, for most of its first decade, BDStar was the exclusive mainland Chinese distributor of high-precision GNSS receivers from NovAtel, a Calgary, Canada–based firm considered one of the global gold standards in survey-grade positioning hardware. If you were a geodesist surveying a hydroelectric dam site in Yunnan in 2004, or a seismologist instrumenting a fault line near Chengdu, the odds were non-trivial that the orange-and-black NovAtel receiver in your field kit had crossed a BDStar invoice.

This is the classic Acquired playbook writ Chinese: before you try to build, become the most knowledgeable distributor in the market. Sell somebody else's superior product. Learn who the customers are, how they buy, what they complain about, what margins they bear, and what the use-case boundaries really are. Zhou was not trying to build a distribution empire—he was doing what Masayoshi Son did with early Japanese PC software distribution, what Michael Dell did with direct-sales PCs before he vertically integrated, and what countless Chinese entrepreneurs have done in the semiconductor and medical device spaces since. The distribution business was the tuition payment for a later, more ambitious act.

That later act was made possible by a specific and peculiar piece of Chinese industrial policy: the launch of the Beidou-1 experimental satellite system. Beidou-1, deployed between 2000 and 2003, was a regional two-satellite demonstrator that proved China could do something GPS could not—two-way messaging through the constellation itself. For fishermen in the South China Sea, Beidou-1 was a satellite text-message service that happened to also do positioning. It was not yet a serious competitor to GPS, but it was a technological flag planted firmly in geostationary orbit, and more importantly, it was a signal to any Chinese entrepreneur reading the tea leaves that the state intended to invest in satellite navigation for decades. Industrial policy in China has historically been a very long instrument. You can build a company on a five-year plan. You can build a dynasty on a fifteen-year plan.

BDStar read that tea correctly. By 2007, the company was ready for its next step: an IPO on the Shenzhen Stock Exchange. Listing in February 2007, BDStar became the first GNSS-focused company publicly listed in China, a "first mover" designation that carried both practical benefits and narrative weight. Practical benefits: access to equity capital at a moment when Chinese domestic investors were feverishly bidding up anything with a defense or technology narrative. Narrative weight: the implicit endorsement, through the listing process itself, that BDStar was a company the state wanted to see flourish.

Why IPO so early, long before the commercially meaningful Beidou-2 or Beidou-3 phases? Two reasons. First, Zhou needed growth capital to transition from distribution margins into design margins, and equity was cheap. Second, listing locked in a valuation frame and a governance structure at a moment when the state's industrial policy winds were blowing favorably. Get your paperwork done while the weather is good. The 2007 IPO gave BDStar roughly half a billion yuan in growth capital—modest by today's standards, generous by 2007 semiconductor startup standards in China, and just enough runway to begin the expensive pivot from reseller to builder.

The distribution business had done its job. It had taught BDStar the customer stack, given it a brand in the Chinese surveying and precision industrial markets, and thrown off enough cash and enough public-markets credibility to fund the next decade. But by the end of the 2000s, a harder question was looming in Beijing's ministries, and Zhou could see it coming. The question was: how long could China tolerate having its critical positioning infrastructure depend on foreign silicon?

III. Inflection Point 1: The Great "Indigenization" (0:30 – 0:55)

In a Beijing government office sometime around 2010—and we are generalizing a long series of meetings into a single narrative moment for clarity—senior technology policy planners were reviewing a document that had quietly become one of the most important industrial policy questions of the coming decade. The Beidou-2 regional constellation was nearing completion. By 2012 it would cover the Asia-Pacific with positioning, navigation, and timing services at accuracies rivaling GPS for most civilian use cases. A triumph. But there was a problem that nobody outside a small community of engineers fully appreciated.

The silicon inside Chinese positioning products was overwhelmingly foreign. U-blox of Switzerland. Trimble and Garmin of the United States. SiRF, before its absorption into CSR and then Qualcomm. NovAtel of Canada, BDStar's own supplier. If you opened up a Chinese vehicle tracking unit, or a Chinese surveying receiver, or a Chinese telecom time server, odds were better than even that the positioning engine was a chip designed somewhere in the West. This was a national security vulnerability that had been tolerable while Beidou was a prestige project. It would become intolerable the moment Beidou became real infrastructure.

Imagine explaining to a Politburo Standing Committee member that China's sovereign navigation system—funded with billions of yuan of rocket launches—was being read by Chinese military and civilian users through chips designed in Thalwil, Switzerland or Sunnyvale, California. Imagine explaining that in a scenario of diplomatic friction with either nation. The political calculus became obvious. Beidou had to have Beidou-native silicon, and it had to have it fast.

For BDStar, this was the moment of strategic truth. The company's distribution business was profitable. NovAtel receivers were excellent. Reselling them was a comfortable life. But comfort is the enemy of transformation, and Zhou had built this company precisely for a moment like this. The answer was a new entity: Unicore Communications, founded in 2009 as a BDStar subsidiary with the specific charter of designing domestic GNSS chips.

The founding of Unicore is worth pausing on because it illustrates the distinctly Chinese concept of a "designed champion." Unicore was not a skunkworks. It was not organic growth. It was an intentional, capitalized, staffed, and state-supported project to build a national chip design house inside a publicly listed commercial company. Early leadership came from returnees—engineers who had worked at companies like SiRF, Qualcomm, and other Silicon Valley RF and baseband firms and who could be enticed back to Beijing by some combination of patriotism, rising compensation packages, and the intoxicating prospect of building a national champion from scratch. If you've followed the trajectory of Chinese semiconductors in general—companies like HiSilicon, GigaDevice, Will Semiconductor—this pattern is familiar. Return-the-diaspora recruiting is one of China's most consistent semiconductor playbooks.

The chip Unicore needed to build was technically ferocious. A GNSS baseband has to track signals from four and eventually seven constellations: GPS, GLONASS, Beidou, Galileo, and regional systems like Japan's QZSS and India's NavIC. Each broadcasts on multiple frequency bands. The receiver needs to perform code correlation, Doppler tracking, ephemeris decoding, and ionospheric correction across dozens of simultaneous channels, while consuming milliwatts of power in a mobile device. It is not the hardest chip in the world—that honor goes to the bleeding-edge mobile processors—but it is a serious RF and DSP design, and by 2010 no Chinese firm had done it well.

Unicore's early chips—starting with a multi-system baseband around 2010-2011 and then a series of increasingly integrated SoCs through the mid-2010s—were not immediately competitive with u-blox on every dimension. What they were, critically, was Chinese. And "Chinese" in this context meant qualified to enter the supply chain for Chinese government procurement, Chinese military-civil fusion programs, Chinese state-owned enterprise infrastructure, and, over time, Chinese commercial electronics. The moat was not performance. The moat was regulatory and political, and it was immensely profitable for the firm that moved first.

By the time Beidou-2 reached full regional operational capability in 2012, BDStar through Unicore had Beidou-native silicon in the field. By the time Beidou-3 began launching satellites in 2017 and reached global operational capability in 2020, Unicore had moved from 100-nanometer geometry to 55-nanometer, with the 22-nanometer "Nebulas" generation on the roadmap. This was not merely technology progress. This was BDStar converting itself from a distributor into the primary domestic silicon architect of a sovereign navigation stack, in perfect rhythm with the state's own constellation roadmap.

What does this teach us as investors? That in China, the most valuable kind of moat is not always a patent or a brand or a switching cost. Sometimes the most valuable moat is temporal alignment. Be the first domestic provider of a critical capability at the exact moment national policy decides that capability must be domestic. BDStar built that alignment deliberately, over a decade, before the policy tailwind arrived. And when the wind finally blew, the company was the logical vendor.

With indigenization underway and Unicore producing silicon, the next question became simple and enormous. Chips are one piece of a positioning system. Antennas are another. Correction services are a third. Automotive integration is a fourth. Could BDStar buy its way into the rest of the stack?

IV. Capital Deployment: The M&A "Benchmarking" Era (0:55 – 1:25)

There is a specific kind of M&A decision that defines acquisitive companies, and BDStar faced one in 2015 with the acquisition of Harxon Corporation. Harxon was, and remains, the dominant Chinese designer and manufacturer of high-precision GNSS antennas—the ceramic and patch-array antennas that sit on top of surveying rovers, agricultural tractors, marine vessels, and increasingly, autonomous mobile robots. By various industry estimates, Harxon controlled somewhere in the neighborhood of 70% of the Chinese high-precision antenna market at the time of acquisition. That is a classic "Cornered Resource" situation in Hamilton Helmer's framework. If you want centimeter-accuracy antennas in China at industrial scale, you go to Harxon, or you deal with significantly less desirable alternatives.

BDStar paid what industry observers at the time considered a premium multiple for Harxon. The specific transaction consideration has been disclosed in various company filings. The more interesting question is not the price tag but the strategic logic. BDStar was buying a complementary, not a redundant, asset. Chips and antennas are the two halves of the GNSS front-end. Own both, and you can sell an integrated module to customers who previously had to integrate across vendors. The bundle economics can be meaningful. More importantly, you capture the design-in decision at a deeper level of the customer's bill of materials. Once a surveying equipment OEM standardizes on a BDStar chip paired with a Harxon antenna, the switching cost to pick apart that pairing and introduce a different vendor for either half becomes a real engineering exercise.

The Harxon deal made strategic sense on two levels. First, it entrenched BDStar at the top of the Chinese high-precision positioning stack. Second, it hedged the chip business. If Unicore's silicon stumbled against foreign competition, the antenna business could still carry the company. Diversification, in the vertical rather than horizontal sense.

Then came the more controversial move. In 2017, BDStar announced the acquisition of in-tech GmbH, a Munich-area German automotive electronics and engineering services firm, for a reported sum of roughly €60 million. in-tech was not an antenna maker. It was not a chip designer. It was a services business—a firm that provided automotive electronics development, testing, and validation services primarily to German Tier-1 suppliers and OEMs. Think of it as a specialized engineering consultancy embedded in the Munich-Stuttgart-Ingolstadt automotive supply chain. A small but real player in the deeply competitive European automotive electronics services market.

Why would a Chinese GNSS chip and antenna company buy a German automotive engineering services firm? The stated rationale was access. The European automotive supply chain is famously difficult for outsiders to penetrate. Volkswagen, BMW, Daimler, Audi, and their Tier-1 suppliers like Bosch, Continental, and ZF operate through long-standing relationships and rigorous supplier qualification regimes. A Chinese chip company walking in cold has essentially no chance of getting a GNSS receiver designed into a BMW ADAS stack. A Chinese company that owned a Munich engineering services firm embedded in BMW's development projects, however, might have a plausible path.

Was this logic sound? Let's do the Acquired benchmarking exercise. in-tech at acquisition had revenues roughly in the low hundreds of millions of euros and operating margins modest by software company standards but reasonable by engineering services standards. Public comps for automotive engineering services—firms like Bertrandt or EDAG in Germany—were trading at enterprise value multiples of revenue in the 0.5 to 1.2x range and P/E multiples in the low-to-mid teens. Against those benchmarks, BDStar's price tag was defensible as a purely financial transaction, though certainly not cheap.

The harder question is whether the strategic synergy materialized. Cross-border M&A, especially Chinese acquisitions of German industrial assets during the 2015-2018 wave, has a spotty track record. Cultural integration friction is real. German mittelstand firms operate on a social contract between labor, works councils, management, and local communities that is structurally incompatible with the more top-down approach of many Chinese acquirers. Retention of key engineering staff post-acquisition is a constant challenge. Getting the German subsidiary to meaningfully route business to the Chinese parent's products—the actual synergy thesis—requires a degree of integration that many cross-border deals never achieve.

BDStar's approach with in-tech has been, by most reports, relatively hands-off. in-tech continued to operate largely as a standalone German entity, its management mostly retained, its customer relationships preserved. The good news: the acquired business did not implode. The more honest news: the hoped-for synergy of BDStar silicon flowing into German automotive ADAS stacks has been slower and more modest than the 2017 investor presentations implied. Some integration has happened, particularly in commercial vehicle and specialized automotive applications, but the vision of BDStar as a major GNSS vendor to German luxury brand ADAS has not materialized at scale through this channel. This is a recurring theme in Chinese-European industrial M&A, and in-tech is neither the worst nor the best example.

Here is where capital efficiency analysis gets interesting. BDStar has, for most of its life as a public company, traded at a P/E ratio meaningfully higher than global peers like Trimble or Garmin. Trimble, an American positioning technology company with a global customer base, has historically traded at forward P/E multiples in the teens to low twenties depending on the cycle. BDStar has frequently traded at multiples in the thirties, forties, or higher, reflecting a combination of domestic growth narrative premium, "national champion" policy support, and the structurally higher multiples common in Chinese A-share technology names.

This valuation gap is strategically powerful. BDStar's equity is, effectively, a cheaper currency than its Western peers' equity. Issuing BDStar shares to acquire a German services firm, or a Chinese antenna maker, or a domestic chip house, costs BDStar's existing shareholders less dilution than it would cost a Trimble shareholder to do the equivalent deal using Trimble's shares. This is how a public-market premium becomes a corporate development weapon. You use expensive paper to buy cheaper, cash-flowing industrial assets, and over time you convert those assets into consolidated growth that justifies, at least partially, the premium you paid with.

For investors, the second-layer diligence question is whether the premium is self-reinforcing or self-consuming. If BDStar's acquisitions generate sufficient return on invested capital to justify the multiple, the flywheel spins. If they don't—if in-tech-style deals end up being mostly defensive rather than accretive—then the premium is eventually arbitraged away as the growth narrative fails to materialize in the numbers. So far, blended ROIC on the consolidated BDStar portfolio has been respectable but not extraordinary, which makes the ongoing story partly about execution and partly about continued macro alignment with Chinese industrial policy.

With a chip engine, an antenna franchise, and a European automotive foothold all assembled, the next question was whether BDStar's leadership could manage the resulting complexity. And the answer depended heavily on one man.

V. Management Spotlight: Zhou Ruxin & The New Guard (1:25 – 1:45)

There is a common archetype in Chinese technology entrepreneurship, and Zhou Ruxin does not quite fit any of them. He is not a flamboyant founder in the Jack Ma mold. He is not a secretive military-industrial technocrat of the Huawei-Ren Zhengfei variety. He is not a foreign-educated returnee evangelist. He is, in many ways, a Beijing engineer of a specific generation—technically trained, patiently ambitious, politically literate, and comfortable operating inside the narrow channel between private enterprise and state industrial policy. The quality that distinguishes him is an almost monastic willingness to sit inside a single industry for decades.

Born in the mid-1960s, Zhou came up through China's technical education and state electronics research system. His early career was spent at state-linked institutes working on navigation and communications, and it was there that he absorbed both the technical substance and the political rhythm of Chinese industrial policy. He understood, before many in the domestic electronics industry, that satellite navigation was going to be a generational Chinese priority. And he understood, perhaps more importantly, that being privately organized—free from the bureaucratic drag of a state-owned enterprise but still aligned with state priorities—was going to be the optimal corporate form for capturing the resulting economic opportunity.

Zhou still controls roughly 28% of BDStar's outstanding shares directly and through affiliated entities. That is a meaningful owner-operator stake for a company of BDStar's market capitalization, and it is considerably higher than the typical founder stake at most Chinese public technology companies of comparable age. He has not sold down aggressively, he has not taken meaningful secondary liquidity, and he has not diluted himself out of control through successive financing rounds. For a founder-CEO now well into his corporate life, this is a meaningful signal about alignment with public shareholders.

The more interesting lens on Zhou's leadership is not the share ownership—which is static—but the incentive architecture he has built around the next generation of management. BDStar's employee stock ownership plans, rolled out in multiple tranches during 2022 and 2023, are unusually interesting. The vesting and strike-price structures are tied not just to profit or revenue but to highly specific technical and commercial milestones. Shipment volumes for the Nebulas generation chip. Penetration of high-precision modules into automotive Tier-1 bills of materials. Revenue growth rates in specific verticals like unmanned aerial vehicles and autonomous mobile robots.

This is a choice. It is a choice to bias the management team toward aggressive growth in specific, strategic segments, even at the possible expense of near-term margin optimization. It says, in effect, that the board and the founder believe the most valuable thing management can do right now is drive volume and design-in penetration for the company's next-generation silicon, not harvest cash from the existing business. It is a "growth at an attractive cost" incentive, not a "profit maximization" incentive, and it is the kind of explicit prioritization that reveals a company's actual strategic posture far more clearly than any investor presentation.

The professionalization of BDStar's management has been a quiet but deliberate process. In its earliest years, the company was structured around Zhou personally—the classic founder-does-everything Chinese private company. Over the 2010s, particularly after the Harxon and in-tech acquisitions, that structure became untenable. A distributor you can run with a founder at the center. A vertically integrated, internationally operating, multi-segment GNSS technology platform with operations in Beijing, Shenzhen, Munich, and the United States you cannot. BDStar is now organized around division-level leadership, with Unicore Communications, Harxon, the cloud services business, and various system integration units operating with substantial operational autonomy under a group holding structure.

Zhou's evolution has been the most interesting personal transformation in the story. He started as what he once reportedly described as "essentially a salesman"—a distributor learning a market. He became, over the course of two decades, a silicon strategist. The skill set that lets you close a distribution contract is very different from the skill set that lets you commission a 22-nanometer SoC tape-out and allocate capital between a German automotive subsidiary, a domestic antenna franchise, and a cloud correction services platform. That Zhou has apparently made that transition without imploding the company is, by any reasonable standard, a managerial achievement. Not every founder makes that passage. The Chinese technology landscape is littered with founders who were excellent at the first act and structurally incapable of the second.

The second-layer diligence question that every long-term investor should be asking about BDStar is succession. Zhou is now approaching the stage of a founder's career at which succession planning becomes material. There is no disclosed succession announcement, but the professionalization of the divisional leadership bench, the depth of the ESOP-aligned senior management team, and the expansion of external director representation on the board all suggest that the founder understands the question. The answer will play out over the next five to ten years.

For now, under Zhou's continued leadership, the company has quietly built a portfolio of businesses that most outside observers have not fully inventoried. Which brings us to the hidden businesses inside BDStar.

VI. The Hidden Businesses: "Cloud + IC" (1:45 – 2:05)

There is a specific kind of pleasure in the research process where you open up a company that markets itself as one thing and discover, underneath, that it is actually several things stacked on top of each other. BDStar presents as a positioning hardware company. Open it up, and you find roughly four distinct businesses, each with its own economics, and the most interesting two are the ones that get the least airtime in conventional brokerage reports.

The first and most important is the integrated circuit division, operating through Unicore Communications. This is where Nebulas lives. Nebulas is BDStar's multi-generational high-precision GNSS SoC family, and the fourth-generation Nebulas-IV chip moved the family to 22-nanometer process geometry. To understand why this matters, consider the following simple mental model. A GNSS chip does three things: it listens to faint satellite signals across multiple constellations and frequency bands, it performs enormous amounts of signal processing math to pull position from those signals, and it does both while consuming as little power and occupying as little board space as possible. Each process node shrink—from 100nm to 55nm to 40nm to 22nm—reduces power consumption, reduces die area, and improves integration capacity. A 22nm Nebulas-IV chip can do things in a drone or a smartphone that a 55nm Nebulas-II chip simply cannot, because the older chip would drain the battery or take up too much real estate.

The IC division's gross margins have historically been above 50% in periods of healthy mix and decent volume. Semiconductor design businesses at scale can achieve this kind of margin structure because the marginal cost of an additional chip is the wafer and test cost, while the design, IP, and validation costs are fixed. Nebulas-IV, once designed, can be fabricated at TSMC or a qualified domestic foundry partner at commodity foundry economics, and the difference between the fabrication cost and the price at which the chip is sold to a drone OEM or an automotive Tier-1 is mostly gross profit. This is the kind of business model investors have paid through the nose for at companies like Nvidia and Qualcomm for years. Inside BDStar, the IC division is a structural gross margin machine that most of the Chinese investor community still views as a commodity hardware business. There is a perception gap here.

The second hidden business is the cloud platform. BDStar operates a correction services network, branded at various points under names including TruePoint, that provides high-precision GNSS corrections via ground reference stations distributed across China and increasingly along Belt and Road corridors. Here's the concept in simple terms. Raw GNSS signals from a constellation, decoded by a receiver, yield positioning accuracy at the meter level in ideal conditions. For applications like autonomous driving, precision agriculture, surveying, and drone inspection, meter accuracy is useless. You need centimeter accuracy, and to get it, you need real-time correction data that accounts for ionospheric delays, satellite orbit variations, and other error sources. That correction data is generated by a network of reference stations and delivered to receivers via cellular or satellite links, typically as a subscription service.

Think of this as Azure for location. A hardware user pays a recurring fee—monthly or annual—to subscribe to correction services, and in return gets centimeter-level positioning accuracy in real time. Unlike the chip itself, which is sold once at a hardware margin, the correction service is a high-gross-margin recurring revenue stream that, once built out, scales at software-like economics. BDStar has been quietly building this correction services footprint for years, seeding ground reference stations across China and expanding into selected international markets. The revenue contribution today is still modest in the context of the overall P&L, but the trajectory matters enormously. A recurring services business hidden inside a hardware company is exactly the kind of structural story that long-term investors pay to discover.

The third business is the traditional system integration franchise: industrial positioning products, telecom timing systems, marine and aviation navigation systems, and related high-specification equipment. This is a solid, slow-growing, decent-margin cash generator. It is not the exciting part of the story, but it pays the bills and funds the R&D for the exciting parts.

The fourth business is the German automotive subsidiary and associated automotive electronics activities. This is the piece that has most tested the patience of investors. The logic remains sound, the execution has been mixed, and the contribution to consolidated growth has been real but not transformative.

Across these four businesses, the segment with the most interesting growth rate is what BDStar has labeled internally and in various disclosures as the "low-speed autonomous" segment. This includes robotic lawn mowers for the European and North American residential market, warehouse automated guided vehicles, last-mile delivery robots, and autonomous cleaning and inspection platforms. This segment has been growing at approximately 40% compound annually over recent years while the broader company growth rate has been considerably slower. The economics are attractive: these platforms typically require high-precision positioning modules that command premium ASPs, and the addressable market is expanding as robotic automation penetrates new use cases.

For investors looking for a single illustrative KPI, low-speed autonomous module shipments is one of the most leveraged indicators of BDStar's future growth trajectory. If that line continues to compound at 30-40% through the late 2020s, it will eventually become the largest single segment. If it decelerates, one of the key bull case pillars weakens.

With four businesses, multiple geographic footprints, and several competitive dynamics in play, the next question is how we think about BDStar's structural position in its markets. Time for the frameworks.

VII. Strategy Frameworks: 7 Powers & 5 Forces (2:05 – 2:25)

Let's run BDStar through Hamilton Helmer's 7 Powers framework, because the exercise is illuminating and the answers are not uniformly bullish.

Scale economies. BDStar has scale advantages in antenna manufacturing through Harxon and increasing scale advantages in chip design through the amortization of Nebulas development costs across growing unit volumes. But these scale advantages are not dramatic relative to global peers; Trimble, u-blox, and Broadcom all operate at comparable or greater scale. Score: modest.

Network economies. Limited. GNSS hardware does not benefit from traditional two-sided network effects in the way marketplaces or social networks do. However, the correction services business does exhibit a mild network effect: more subscribers generate more telemetry data, which can improve correction model quality, which modestly attracts more subscribers. Score: weak but emerging.

Counter-positioning. BDStar's emergence as a low-cost, government-aligned domestic alternative to U-blox and NovAtel put those incumbents in a difficult position. They could not cut prices aggressively in China without cannibalizing their global pricing, and they could not easily replicate BDStar's political positioning. This is a textbook counter-positioning story, but it is largely historical. The counter-positioning advantage has been mostly realized at this point. Score: strong historically, diminishing prospectively.

Switching costs. This is one of BDStar's strongest powers, and it is especially strong in automotive. Once a Tier-1 automotive supplier integrates a specific GNSS chip into an ADAS stack and qualifies that chip through the multi-year safety and reliability validation cycles that automotive requires, switching to a competing chip is a five-to-seven-year project minimum. The qualification costs, the re-validation costs, the software porting costs, and the customer approval costs are enormous. The same logic applies in industrial positioning, surveying, and telecom timing, though with somewhat shorter cycles. Score: strong.

Cornered resource. BDStar has two cornered resources worth noting. First, its patent portfolio in Beidou-3 signal processing, particularly around the specific modulation schemes and authentication mechanisms of the Chinese constellation, is unusually deep and technically difficult to engineer around. Second, Harxon's dominance in high-precision antenna designs represents a specific cornered resource in a narrow but lucrative market. Score: strong.

Process power. Modest. Chip design and antenna design both benefit from accumulated process know-how, but neither represents a truly differentiated process power of the Toyota Production System variety. Score: modest.

Branding. Limited as a consumer brand. Meaningful as a B2B reputation asset in the Chinese positioning industry. Score: modest.

To Helmer's seven, we need to add what might fairly be called an eighth power when analyzing Chinese companies: government policy alignment. This is a power that Western strategic frameworks often underweight or ignore, because in most Western economies the pace and intensity of industrial policy intervention does not rise to the level of a structural competitive advantage. In China, it does. BDStar's status as the de facto national champion of Beidou-native silicon gives it preferential access to government procurement, favored status in military-civil fusion programs, implicit underwriting in banking and capital markets, and moral hazard protection during moments of industrial stress. This is not a moat in the traditional sense—it does not stop a competitor from entering the market—but it is a structural advantage in capturing specific flows of revenue, capital, and talent. Score: strong.

Now Michael Porter's 5 Forces.

Threat of new entrants. Moderate. The technical barriers to entering high-precision GNSS are real but not insurmountable. Several well-funded Chinese startups and established semiconductor firms have mounted entries over the past decade. However, the combination of capital requirements, qualification cycles, and government policy alignment creates meaningful barriers that have so far prevented any new entrant from becoming a top-three competitor.

Threat of substitutes. Low for the core positioning function. GPS-family positioning is essential to many applications, and the substitutes—inertial navigation, vision-based positioning, wheel odometry—are complementary rather than replacement technologies for most use cases. Cellular positioning is an emerging partial substitute in some urban contexts but does not threaten the precision markets BDStar serves.

Bargaining power of suppliers. Moderate. The most important suppliers are semiconductor foundries (TSMC historically, with increasing SMIC dependency for certain products) and specialty component manufacturers. Geopolitical pressure on leading-edge foundry access is a real concern and a structural risk that BDStar shares with most Chinese fabless semiconductor firms.

Bargaining power of buyers. Moderate. In mass-market consumer hardware like smartphones, buyers are large and price-sensitive. In automotive, buyers are large but switching costs are high, creating a more balanced relationship. In industrial and government buyers, BDStar often has the upper hand due to its qualified-domestic-supplier status.

Intensity of rivalry. High. The most significant domestic competitors are companies like Hwa Create, Mengsheng Electronic, ComNav Technology, and several other Chinese firms. Internationally, u-blox remains a significant competitor in global markets, and Trimble dominates in certain precision agriculture and surveying segments outside China. The competitive lesson is that BDStar's "silicon-first" approach—integrating from chip design upward—has structurally advantaged it over "system-first" rivals that source chips and build systems. Owning the silicon lets you own the roadmap.

Pull this together, and the investor takeaway is that BDStar's position is defended by a combination of moderate-to-strong switching costs, a strong cornered resource in Chinese-system-specific IP and antenna dominance, a structurally important government policy alignment, and a credible counter-positioning legacy that has evolved into a market-leadership incumbency. The vulnerabilities are geopolitical supplier risk, moderate rivalry, and the challenge of translating domestic dominance into international scale.

With the frameworks applied, let's pull out the investor playbook.

VIII. The Playbook: Lessons for Investors (2:25 – 2:40)

If you zoom out on the BDStar story, three reusable investment frameworks fall out that apply well beyond this single company and this single industry.

First, the "National Alignment" playbook. The most powerful structural tailwind in modern Chinese industrial investing is alignment between a company's R&D roadmap and the state's multi-year technology priorities. BDStar's roadmap—from Beidou-1 in the early 2000s through regional Beidou-2 to global Beidou-3 and now the emerging Beidou-4 plans for the 2030s—has been a near-perfect mirror of the Chinese government's satellite navigation roadmap. This is not coincidence; it is deliberate. Companies that can credibly position themselves as the commercial execution arm of a national strategic priority enjoy capital access, procurement preference, regulatory support, and talent draw that pure private-market competitors cannot match.

The investor lesson is to look for this alignment as a primary screen in Chinese industrial and technology names. Not every sector has such an alignment. Sectors where it exists include semiconductors, electric vehicles, biotechnology, renewable energy, satellite infrastructure, advanced materials, and quantum computing. Sectors where it does not exist include most consumer internet categories, which have actually faced the opposite direction of policy wind in recent years. BDStar is a case study in how to identify and invest behind the positive version of this dynamic.

Second, the "Component to System" trap. BDStar's in-tech acquisition is the cautionary tale in this area. Moving from high-margin, structurally defensible components (chips, antennas) into lower-margin, more competitive systems (automotive electronics services, integration) is a path that consumes capital and attention without necessarily generating returns. The logic is usually one of strategic positioning—we need a foothold with this customer base, or we need to own more of the value chain—but the economics often don't support the strategic story. High-margin component businesses are high-margin precisely because they are structurally defended. Low-margin system businesses are low-margin precisely because they are commodity. Owning both does not automatically make either better; it often just dilutes the consolidated margin profile while adding integration complexity.

This is a generalized industrial strategy trap. Companies like ASML have resisted this trap by staying fanatically focused on high-end lithography components. Companies that have fallen into it, selectively, have diluted their return profiles. The investor lesson is to be skeptical of "vertical integration" stories that move downstream into lower-margin businesses, and to probe carefully whether the strategic logic actually translates into synergy economics in the consolidated P&L. BDStar has not been catastrophically damaged by the in-tech experience, but it is clear in retrospect that the synergy thesis was ambitious relative to the realized outcome.

Third, patience in hardware. Moving from 100nm to 22nm at Unicore took approximately fifteen years. Building the Harxon antenna franchise to market dominance took more than a decade. Building the correction services network to meaningful regional coverage has taken similar time. Success in deep-technology businesses—semiconductor design, RF systems, precision mechanical engineering—is measured in decades, not quarters. Companies that have tried to compress these development cycles with aggressive capital deployment have often produced weaker technical outcomes than those that have compounded capability slowly.

This has direct implications for the time horizon appropriate to BDStar as an investment. If you are trading the quarterly print, BDStar will disappoint you on the days when a large customer pushes out an order or when Nebulas chip yields hit a temporary hiccup at the foundry. If you are compounding over a five-to-ten-year horizon in alignment with the Chinese satellite navigation industry and its broader positioning technology ecosystem, the question is less about the next quarter's number and more about whether the strategic position continues to strengthen. Those are very different investment conversations, and BDStar is better suited to the second than to the first.

A related discipline: when looking at BDStar's KPIs, focus on a very small number of indicators that actually matter for the long-term thesis. We'd argue the three most important are:

One, Unicore high-precision chip shipment volumes, particularly in the latest Nebulas generation. This measures whether the company's silicon strategy is winning design-ins at the rate required for the growth narrative.

Two, correction services subscription revenue and subscriber count. This measures whether the nascent Positioning-as-a-Service business is becoming meaningful or remaining a rounding error.

Three, automotive revenue as a percentage of consolidated revenue, with particular attention to the margin profile of that segment. This measures whether the "component to system" transition is accretive or dilutive, and it will ultimately determine whether the in-tech and related automotive plays are validated or written down.

The reader can track these directly from BDStar's semi-annual and annual disclosures. They are the small number of dials that actually move the long-term investment case. Everything else is noise.

IX. Conclusion & Final Grade (2:40 – 2:45)

Let's return to the image that opened this episode. A Long March rocket punching through Sichuan clouds in the summer of 2020, carrying the final satellite of China's Beidou-3 global constellation. The photograph of that launch is, in a certain sense, the visual summary of a quarter-century of Chinese industrial policy made real in orbit. It is also, more quietly, the backdrop against which BDStar completed its own transformation from a small Beijing distributor of Canadian GPS receivers into what can fairly be called the Qualcomm of Beidou.

That transformation has several acts. The distribution act of the early 2000s, when Zhou Ruxin learned the market by selling NovAtel gear. The public listing of 2007, when BDStar became the first GNSS company on a Chinese exchange and pocketed the growth capital for the next phase. The indigenization act beginning around 2009, when Unicore Communications was founded to design Beidou-native silicon in anticipation of a policy shift that everyone in the industry could see coming but few acted on early. The M&A acquisition sequence of the mid-2010s, when Harxon and in-tech stitched together a vertically integrated positioning portfolio spanning chips, antennas, and automotive electronics. The services layering of recent years, as the correction services network and the low-speed autonomous segment added recurring revenue and high-growth new verticals on top of the established hardware core. And the ongoing professionalization of management and incentives, aligning the next generation of leadership with the aggressive shipment and penetration targets that the next decade will require.

The bull case is simple to state. BDStar is positioned at the commercial apex of a global Chinese satellite navigation infrastructure that is continuing to expand geographically through Belt and Road alignments, growing in economic relevance as autonomous mobility and precision industrial applications scale, and enjoying the structural policy tailwind of Chinese industrial priorities. If BDStar captures even a meaningful share of the global IoT-scale positioning market as Beidou gains international acceptance, the financial trajectory implied by the Nebulas chip roadmap, the correction services build-out, and the low-speed autonomous segment growth is material over a five-to-ten-year horizon. This is a national-champion compounding story in one of the most strategically protected corners of Chinese technology.

The bear case is also simple to state. Geopolitical friction may erect "silicon curtains" that prevent BDStar's high-margin chips from ever entering U.S. and European markets at scale, capping the international TAM. Foundry access for the most advanced process nodes may be constrained by export control dynamics. Domestic competition will intensify as other Chinese firms target the same segments. The in-tech pattern—buying your way into a segment only to discover the synergies don't materialize—could repeat in other acquisitions. And the fundamental correlation between the company and Chinese industrial policy is a double-edged sword; if that policy shifts, so does the tailwind.

Between those two cases sits a company whose fundamental characteristics—Cornered Resource dominance in Chinese high-precision antennas, strong Switching Costs in automotive and industrial customers, emerging network economics in correction services, and a structurally powerful government policy alignment—are unusually favorable by the standards of most industrial technology businesses globally. The execution risks are real. The competition is real. The geopolitical overhang is real. But the strategic position is genuinely rare, and rare strategic positions tend to command, over long periods, rare economic outcomes, if management continues to execute at the level Zhou and his team have demonstrated over the past quarter century.

For long-term fundamental investors, the BDStar question is not whether the company is good—it plainly is—but whether the price at any given moment reflects a reasonable probability-weighted view of the outcomes we have discussed. That is a judgment for each investor to make with their own framework and discount rate. The purpose of this episode has been to equip you to make that judgment with a complete picture of the company's history, strategy, competitive position, management, and the industrial dynamics in which it operates.

From a small Beijing office reselling Canadian GPS receivers, to the primary commercial architect of China's satellite navigation silicon stack, in twenty-six years. Whatever else one says about BDStar, the arc of the story is genuinely remarkable, and the next decade of satellite navigation is going to be written, in substantial part, at the intersection of Chinese national policy and the specific corporate vehicle that Zhou Ruxin built to capture it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube