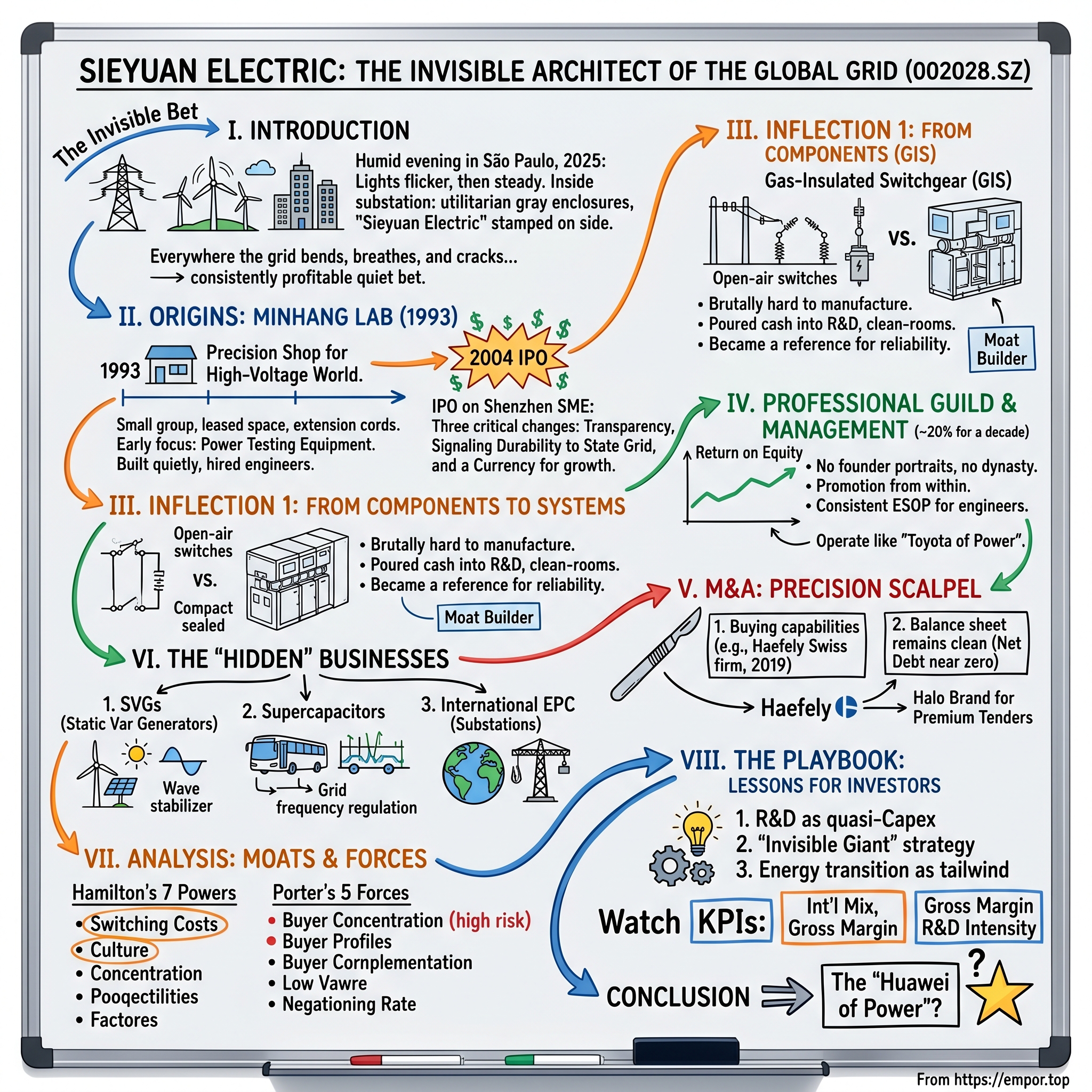

Sieyuan Electric: The Invisible Architect of the Global Grid

I. Introduction: The "Swiss Army Knife" of the Grid

Picture a humid evening in São Paulo in late 2025. The lights flicker across a sprawling industrial park, then steady themselves as the local utility's voltage regulators silently absorb a surge from a distant wind farm. Nobody notices. That is the entire point. Inside the substation, behind a cyclone fence and a faded warning sign in Portuguese, sits a row of metal-clad enclosures painted a utilitarian gray. Stamped on the side, in modest white lettering, is a name almost no Brazilian engineer would have recognized a decade ago: Sieyuan Electric.

Half a world away, the same name sits on switchgear humming inside a data center outside Frankfurt, on capacitor banks balancing a Saudi solar field, and on a transformer test rig in a Swiss laboratory founded the year Karl Marx died. The company is everywhere the modern grid bends, breathes, and cracks under the weight of the energy transition. And yet, ask the average investor, even a thoughtful one focused on industrials, to name the most consistently profitable Chinese power equipment company of the past decade, and Sieyuan rarely makes the list.

That is the story.

While the financial press lavished attention on Tesla's Megapacks, BYD's blade batteries, and CATL's gigafactories, the unglamorous middle of the energy stack, the gear that actually moves electrons from where they are generated to where they are consumed, became one of the most lucrative quiet bets on the planet. And inside that middle layer, a Shanghai-based, founder-led-but-professionally-managed enterprise compounded book value at a rate that would make most asset-light software firms blush.

By April 2026, Sieyuan Electric carried a market capitalization north of six billion U.S. dollars on the Shenzhen exchange. It had delivered a return on equity around twenty percent for nearly a decade running, a feat its much larger Western peers, ABB, Siemens Energy, Hitachi Energy, had managed only sporadically and only with financial engineering. It had grown international revenue from a rounding error to roughly a fifth of the top line in less than ten years, and along the way it had become the preferred non-state alternative to China's grid-equipment incumbents.

The thesis is simple to state and harder to internalize. In an industry dominated by sprawling state-owned giants with effectively unlimited balance sheets, a privately founded, professionally managed Chinese firm carved out a defensible position by being faster on R&D, more disciplined on capital, and more honest with its shareholders than the institutions it was competing against. In a sector where bureaucratic tempo is measured in five-year plans, Sieyuan moved at the cadence of a Silicon Valley product team and protected its margins like a Swiss watchmaker.

This is the story of how that happened, who built it, what they bought along the way, and why a quiet equipment maker in Minhang District matters far more to the 2030 net-zero math than its share register suggests. It is, in the language Acquired listeners know well, a study in scale economies, switching costs, and the kind of cornered resource that does not show up on any balance sheet: a culture.

Let us go back to where it began, in a Shanghai laboratory that, at the time, almost nobody believed would amount to much.

II. Origins: The Minhang Lab

Minhang in 1993 was not yet the polished suburb it would become. It was a patchwork of rice paddies and rusting state factories, the southwestern frontier of a Shanghai still figuring out what reform-era capitalism actually meant. Deng Xiaoping's "Southern Tour" was barely a year in the rearview mirror, the air still electric with the idea that a Chinese citizen could, lawfully, start a private company and own its profits. Down a side road off Jianchuan Lu, in a cluster of buildings that looked more like a vocational school than a future industrial champion, a small group of engineers leased space, ran extension cords across the floor, and started building power testing equipment.

Sieyuan was, in its earliest incarnation, a precision shop for the high-voltage world. Its founders were technically trained, several with ties to local research institutes, and they noticed something specific. China's electricity grid was about to undergo the largest expansion any country had ever attempted. Every kilometer of new transmission line, every substation, every transformer, would need to be tested before it was energized and after every fault. The instruments to do that testing, calibrated to brutal accuracy, were almost entirely imported. They were expensive, slow to service, and built for European and American grid frequencies and voltages that did not always map cleanly onto Chinese practice.

So the early Sieyuan made test sets. Then, because the testing customers also bought passive components and the engineers understood the physics intimately, the company added capacitors and reactors. These are the unglamorous workhorses of any high-voltage system, the equivalent of shock absorbers and tension cables in a suspension bridge. They smooth and stabilize. They are not what the public photographs. They are what the chief engineer specifies before the photographers arrive.

For a decade, the company built quietly. It hired engineers from the nearby Shanghai Jiao Tong University, paid them better than the state institutes did, and gave them something the state could not: equity, or at least the prospect of it. By the early 2000s, Sieyuan had become a recognizable mid-tier supplier to State Grid Corporation of China, the colossal monopsony that purchased nearly everything that moved an electron in the country.

The inflection arrived in 2004, when Sieyuan listed on the Shenzhen Stock Exchange's Small and Medium Enterprise Board. Stock code 002028. The IPO raised a relatively modest sum by today's standards, but the cash itself was almost beside the point. The listing did three things that mattered far more than the proceeds.

First, it forced transparency. A privately held supplier could fudge its margins, smooth its receivables, hide its inventory write-downs. A listed one in Shenzhen, even on the SME board with its lighter governance regime, had to publish audited statements that customers, competitors, and most importantly, future hires could read. Engineers considering a move from a state-owned enterprise could now see, in black and white, that this Minhang outfit was profitable, growing, and not about to disappear.

Second, it signaled durability to State Grid's procurement officers. Buying mission-critical equipment from a young private firm carried career risk for any utility manager. If a transformer failed, the manager would have to explain why he or she chose the upstart. A public listing, with its quarterly reports and required disclosures, was the closest thing China had at the time to a Good Housekeeping Seal of Approval.

Third, and most consequentially, it gave Sieyuan a currency. The shares could be used to retain talent, to acquire technology, to bolt on adjacent businesses without leveraging the balance sheet. The company would put that currency to work patiently, deliberately, and almost never wastefully, for the next two decades.

There is a deeper structural advantage worth lingering on. China's power equipment industry was, and largely still is, dominated by firms whose ultimate parent is the state. NARI Technology traces back to the State Grid research institute. Pinggao Electric and Xuchang XJ are part of the State Grid group itself. TBEA carries deep regional government roots. These firms have privileged access to design specifications, early visibility into procurement plans, and the soft assurance that the buyer is, in some sense, themselves.

Sieyuan had none of that. It was a private enterprise selling into the captive customer of a state-owned monopoly. To survive, it had to be measurably better. To grow, it had to be roughly twice as efficient as its state-affiliated rivals. Every yuan of R&D had to land. Every product launch had to displace someone with a stronger relationship.

Constraint, as it so often does, became the company's most valuable asset. The discipline forced by being on the outside of the family business eventually became Sieyuan's competitive moat. By the time the next decade arrived, that discipline would have to be applied to a much bigger ambition: moving from making the components to selling the systems.

III. Inflection Point 1: From Components to Systems

By 2009 and 2010, the contours of China's energy buildout had become impossible to miss. The country had committed to a continental-scale ultra-high-voltage transmission program, lines operating at 800 kilovolts direct current and one million volts alternating current, that would carry electricity from coal and hydro plants in the country's far west to the manufacturing sprawl of the eastern seaboard. The numbers involved were almost cartoonish. Tens of thousands of kilometers of new transmission. Hundreds of new substations. Equipment orders that would shape the entire industry's capacity for a generation.

For a component maker like Sieyuan, this was both opportunity and existential threat. Opportunity, because every UHV substation contained capacitors and reactors and would be tested with high-voltage gear. Threat, because the contracts were being structured around system suppliers, firms that could deliver an entire bay of switchgear, not just the parts inside it. Sit still as a component vendor and you become a price-taking subcontractor to a primary supplier. Move up the stack and you keep your margin and your relationship with the utility.

Sieyuan moved.

The vehicle for that move was gas-insulated switchgear, known throughout the industry as GIS. To explain why GIS mattered so much, it is worth pausing on what it actually does. A high-voltage substation is, at its essence, a series of giant switches. Switches that connect transmission lines to step-down transformers. Switches that isolate faults so that a lightning strike on one line does not cascade into a city-wide blackout. Switches that permit maintenance crews to work safely on de-energized equipment.

In the old world, those switches were open-air affairs, vast steel lattices the size of football fields holding ceramic insulators and arcing horns. They worked, but they consumed enormous land area and were vulnerable to dust, salt, fog, and pollution. GIS encloses the same switching function inside a sealed metal housing filled with sulfur hexafluoride gas. The gas is an extraordinary insulator, allowing the switchgear to be a fraction of the size, enabling substations to be tucked into urban basements, mountain caves, and offshore platforms.

GIS is also brutally hard to manufacture. Tolerances are measured in microns. A single pinhole leak in a weld can render an entire bay non-compliant. The product is sold to customers for whom failure is not an inconvenience but a televised disaster. For a Chinese newcomer to break into the GIS market against Siemens, ABB, Mitsubishi, and the captive state-owned suppliers required not just engineering competence but a willingness to wear the reputational risk of being new.

Sieyuan's bet was the engineering equivalent of a startup deciding to compete with Boeing on commercial aircraft. The company poured cash into a dedicated GIS research line, hired metallurgists and gas-handling specialists, built clean-room assembly bays, and most critically, partnered with a handful of forward-leaning provincial utilities willing to pilot its early units. There were failures. There were rework cycles. There were nights when senior engineers slept on cots beside test rigs because a high-pressure leak could only be diagnosed in the small hours when the lab was thermally stable.

What emerged from that period, roughly 2010 to 2015, was a credible 252 kilovolt and then 550 kilovolt GIS product family. Not the world's best, not initially. But good enough, at significantly lower price points than the European incumbents, with delivery times that the imports could not match. State Grid procurement, ever sensitive to import substitution and ever pleased to play foreign and domestic suppliers against each other, started awarding Sieyuan meaningful tonnage. Each successful installation became a reference. Each reference made the next sale easier.

The strategic consequence cannot be overstated. By moving into GIS, Sieyuan transformed itself from a vendor whose products were specified line-by-line on a bill of materials into a supplier whose products defined the substation layout itself. Once an engineering institute drew a substation around Sieyuan GIS dimensions, the company's capacitors, reactors, and increasingly its instrument transformers came along almost automatically. The component business became the pull-through. The system business became the moat.

There was a quieter, branding-level shift happening in parallel. For its first fifteen years, Sieyuan had been categorized in the Chinese power industry as a "cheaper alternative." By the mid-2010s, that label began to peel away. The company started winning bids not because it was the lowest price but because its mean time between failures, the brutal quantitative metric on which utility engineers actually live and die, had become competitive with the imports. In the grid business, a failure is not a bug. It is, quite literally, a blackout. Sieyuan had earned the right to be specified on reliability, not just on price.

That earned reputation would soon meet a much larger test as the company began contemplating something Chinese industrial firms have historically struggled with: the methodical institutionalization of management beyond the founder.

IV. Current Management: The Professional Guild

Walk into Sieyuan's Shanghai headquarters in 2026 and the first thing that strikes a visitor familiar with Chinese industrial firms is what is missing. There are no oversized portraits of the founder in the lobby. No reception desk perched beside a wall of philanthropic plaques bearing the chairman's name. The conference rooms are named after technical concepts, not family members. The senior executives, when they walk past, do so in the small clusters of people who have worked together for fifteen or twenty years, finishing each other's sentences in technical shorthand.

This is, by Chinese standards, deeply unusual.

The dominant pattern in Chinese private industry has been the founder-as-emperor. The first-generation entrepreneur retains controlling shares well past the age at which Western counterparts would have transitioned to a professional CEO. Family members occupy critical posts. Succession is handled either dynastically or, more often, not at all, becoming an investor anxiety that compresses valuation multiples for years before the founder finally either retires or dies.

Sieyuan's chairman, Dong Zenghuan, broke that mold deliberately and early. His ownership stake, around thirteen percent according to recent filings, is meaningful enough to align his economic interests with public shareholders without giving him the autocratic latitude of a controlling founder. He cannot, by the simple math of the share register, override his own board. He chose that.

Dong is, by background and temperament, an engineer-administrator rather than a charismatic visionary. Public appearances are sparse. Media interviews are rationed. When he does speak publicly, the content is overwhelmingly technical and operational, not aspirational. There are no manifestos about disrupting the global energy order, no Bezos-style annual letters laying out grand strategic frameworks. The message, repeated year after year, is mundane and powerful: invest in R&D, treat the engineers well, do not over-leverage, do not chase fashionable acquisitions, expand internationally with patience.

Below Dong sits an executive team that has the texture of a guild. The senior leadership in operations, technology, finance, and international business have, in many cases, spent their entire careers at the company. Promotion is from within. Outside hires for senior roles are rare and usually targeted at specific technical capabilities the company does not have. The implicit deal offered to a new graduate engineer joining Sieyuan is unromantic and credible: stay, do good work, become a meaningful owner of the company over time.

That last clause is operationalized through one of the most consistent employee stock ownership programs in Chinese industry. Sieyuan has rolled out repeated ESOP tranches over the past decade, broadly distributed across mid-level and senior engineers, not concentrated at the top. The plans are funded through market purchases and structured with multi-year vesting. The cumulative effect is that a meaningful fraction of the company's float is held by the people who actually design, build, and ship its products.

The financial signature of this culture shows up in places that are easy to miss. Engineer turnover at Sieyuan, in an industry where talented power engineers are recruited aggressively by larger state firms and by foreign multinationals, runs significantly below the industry average. Each retained senior engineer is worth, by industry rule of thumb, several years of salary in avoided ramp-up costs and preserved tacit knowledge. Across thousands of engineers and decades, the compounding effect is enormous and almost never appears as a discrete line item in any presentation.

Operationally, the philosophy is best captured by an analogy that internal documents have used for years. The company aspires to be, in its niche, something like the Toyota of power equipment. Not the highest gross margin player. Not the flashiest in any single product category. But the most consistent, the most reliable on delivery dates, the most disciplined on warranty costs, the firm whose order book is least likely to surprise anyone in a bad way.

That consistency translates into a return on equity that has, year after year, hovered around twenty percent. To put that in context, the global heavy electrical equipment majors, ABB, Siemens Energy, Hitachi Energy, Schneider Electric, have over the past decade typically generated returns on equity in the high single to low teens, with substantial volatility around restructuring charges, currency swings, and project losses. Sieyuan's number is both higher and dramatically smoother. That smoothness is the management culture made visible.

There is one risk in this model worth naming honestly. A guild culture that prizes internal promotion, technical depth, and consensus can, at scale and over time, struggle with the kind of discontinuous strategic pivot that an outsider CEO sometimes drives. Sieyuan has avoided this trap so far by making its bigger bets, GIS, ultra-high voltage, supercapacitors, international expansion, sequentially rather than simultaneously, and by importing capabilities through targeted acquisitions rather than reorganizations.

Which brings us to the company's M&A history, an arena in which Chinese industrial firms have collectively destroyed staggering amounts of shareholder value, and in which Sieyuan has, against the run of play, behaved with notable surgical restraint.

V. M&A & Capital Deployment: The Precision Scalpel

The history of Chinese outbound industrial M&A since 2010 reads, in aggregate, as a cautionary tale. State-owned and private firms alike paid premium prices for European brands, German Mittelstand machine tool companies, Italian industrial conglomerates, French technology houses, only to discover that integration was harder than the deal slides suggested, that European labor laws bit harder than expected, and that the synergies projected by investment bankers existed mostly on PowerPoint. Goodwill impairments littered the years that followed.

Sieyuan watched this carnage and chose a different path. Its M&A philosophy, articulated implicitly through behavior rather than explicitly through doctrine, has three rules. First, never bet the balance sheet. Second, buy capabilities, not revenue. Third, keep the acquired brand intact while quietly importing manufacturing efficiency.

The most instructive case study is the 2019 acquisition of Haefely, a Swiss firm founded in 1904 that had become one of the world's premier makers of high-voltage testing equipment. Haefely's gear sits in the most prestigious laboratories on the planet. Its name on a test certificate carries the kind of weight that takes a century to accumulate and cannot be manufactured. For a company that had begun its own life in the testing equipment business, acquiring Haefely was a strategic homecoming with a strong industrial logic: Sieyuan's volume-driven Chinese manufacturing meeting Haefely's reference-quality Swiss engineering and customer book.

The price, while not disclosed in granular detail, was modest by the standards of Chinese outbound deals of the period. Industry reconstructions place the multiple paid at something on the order of one and a half to two times Haefely's revenue, well within the range of comparable precision-instrument transactions and a fraction of what some Chinese acquirers had paid for German Mittelstand targets earlier in the decade.

The integration playbook was equally restrained. Haefely kept its name, its Basel headquarters, its senior management, and its engineering culture. What changed was less visible. Component sourcing, where it made sense, shifted toward Sieyuan's Chinese supply base. Manufacturing of certain volume product lines was duplicated or migrated to Chinese facilities with Haefely engineering oversight, while the high-precision custom work stayed in Switzerland. The combined entity could now compete for projects in price-sensitive emerging markets that Haefely alone would have lost on cost, while Sieyuan's domestic test equipment business inherited a halo brand for premium tenders.

The supercapacitor strategy provides another lens. Through investments and a controlling stake in Shanghai Aowei, which trades as a separate entity but operates inside Sieyuan's strategic orbit, the company moved into ultracapacitor technology, a niche cousin of lithium-ion batteries. Where lithium cells store a great deal of energy and release it slowly, supercapacitors store less energy but release it almost instantly and survive millions of charge-discharge cycles. They are, in essence, the energy world's sprinters to lithium's marathoners.

Sieyuan saw two end markets where that profile mattered. The first was urban electric transit, particularly buses, where supercapacitor-equipped vehicles can recharge in seconds at each stop and never carry the weight or fire risk of a large battery pack. The second was grid stabilization, where the millisecond-scale power swings caused by clouds passing over solar farms or sudden wind gusts can be smoothed by short-duration supercapacitor banks, sparing the much more expensive lithium systems from premature wear. The Tesla acquisition of Maxwell Technologies in 2019 had briefly put supercapacitors on the front pages, but the technology's commercial trajectory has been quieter and slower than the headlines implied. Sieyuan's bet has been patient: build a credible domestic supplier, integrate the capability into its broader grid offering, and wait for the energy transition to make the use case unavoidable.

Across these and other smaller deals, Sieyuan's balance sheet has remained almost defiantly clean. Net debt has hovered near zero or, in some years, comfortably negative. Cash reserves have been substantial relative to annual capital expenditure. In an industry where major projects can be delayed, customers can demand extended payment terms, and a single cancelled order can leave a competitor scrambling, Sieyuan has built what amounts to an antifragile structure. When rivals stretch on a downturn, Sieyuan can keep investing. When rivals retrench on R&D in a bad year, Sieyuan does not.

The frugal fortress, as one analyst report described it, is not an accident of conservative finance. It is the deliberate choice of a management team that watched, learned, and decided to be the firm that buys quality assets when the cycle hands them out cheap, rather than the firm fire-selling its prized asset when the cycle turns against it.

The capabilities accumulated through this disciplined deployment, GIS, ultra-high voltage, supercapacitors, precision testing, were the platform for the next chapter, which took Sieyuan well beyond the transformer business that had initially defined it.

VI. The "Hidden" Businesses: Beyond the Transformer

Walk into a wind farm operations center in Inner Mongolia at three in the morning and watch the screens. Wind speeds rise and fall in unpredictable bursts. Each gust shoves more current onto the local distribution feeder. Each lull pulls it back. The voltage, instead of holding the steady sine wave that industrial loads expect, wobbles and bounces. Without intervention, every motor, every variable-speed drive, every sensitive controller on that feeder would degrade or fail prematurely. The intervention, in modern wind and solar installations, comes from a class of devices known as Static Var Generators.

SVGs, in their simplest description, are electronic shock absorbers for the grid. They sit beside renewable generation and inject or absorb reactive power on a millisecond cycle, smoothing the voltage waveform back to something close to ideal. They are, in effect, the power-quality immune system that allows wind and solar, the world's two cheapest sources of new generation but also the two most variable, to be integrated into modern grids at the scale that the energy transition requires.

The SVG market did not really exist in commercial volumes a decade ago. Today, by 2026, it is one of the fastest-growing segments in the entire power equipment industry, with multi-year compound growth rates in the high twenties to low thirties, and Sieyuan sits as one of a small handful of top-tier global players. The company's SVG business grew out of its longstanding capacitor and reactor competence, leveraging deep knowledge of how reactive power actually behaves in real grids rather than how it appears in the textbook.

The business has a beautiful underlying structure. Every new utility-scale wind project needs SVG capacity, generally a fraction of nameplate generation. Every new solar farm above a certain size needs the same. Every long high-voltage direct current line needs reactive support at its terminals. The customer is typically a renewable developer or a utility, both of which buy on technical specification and increasingly on local-content rules. Sieyuan, with deep manufacturing presence in China and growing assembly capability internationally, is positioned to serve both.

Then there is the supercapacitor business, the patient bet introduced earlier. By 2026, the ultracapacitor business had moved beyond proof-of-concept into commercial reality across two main vectors. The first was urban transit, where cities across China and increasingly in Eastern Europe and Latin America had begun specifying supercapacitor-equipped buses for routes where the route geometry, frequent stops, dedicated charging at terminals, made the technology economically superior to battery-electric. The second was the grid-scale ancillary services market, where supercapacitor banks sized in the megawatts provided sub-second frequency response, the kind of fast intervention that lithium batteries can technically perform but that abuses their cycle life.

The third hidden business, and the one with perhaps the largest long-term option value, is international engineering, procurement, and construction. Sieyuan does not just sell pieces of equipment overseas. Increasingly, it builds entire substations turnkey. A utility in Kenya, a mining company in Chile, a transmission operator in the Philippines can contract Sieyuan to design, source, ship, install, and commission a complete substation on a fixed-price, fixed-timeline basis. The Chinese Belt and Road Initiative, with all its geopolitical baggage, opened the door to many of these markets. Sieyuan walked through that door but also, importantly, kept walking after the initial wave receded, building local relationships, training local engineers, and qualifying its products for the diverse technical standards of dozens of countries.

The financial result has been a steady internationalization of the revenue mix. Where overseas revenue once accounted for low single digits of the top line, it has by 2026 grown to roughly twenty percent and, critically, has been growing meaningfully faster than the domestic business. International gross margins, contrary to what an outside observer might expect, have generally been higher than domestic, reflecting both the value-added nature of EPC work and the absence of the grinding price pressure exerted by State Grid's centralized procurement.

The geographic diversification is also a strategic insurance policy. The single largest concentration risk in Sieyuan's business has always been its dependence on State Grid and China Southern Power Grid, the two near-monopsony buyers of high-voltage equipment in China. Every percentage point of revenue that comes from a Latin American utility, an African transmission operator, or a Southeast Asian industrial customer is a percentage point less hostage to the procurement policies and capital expenditure cycles of those two giant Chinese institutions.

There is a more subtle benefit. Selling internationally forces a level of product and service refinement that domestic sales, where the customer is large, sophisticated, and tightly integrated with the supplier ecosystem, does not always require. International tenders demand documentation in multiple languages, third-party type tests, compliance with IEC and IEEE standards rather than just GB Chinese national standards, and warranty performance under climates ranging from Saudi summers to Mongolian winters. Each of these forcing functions ratchets the underlying engineering capability of the firm upward, and that ratchet, once moved, does not easily slip back.

These hidden businesses, SVGs, supercapacitors, and international EPC, have collectively shifted the gravitational center of Sieyuan from a domestic Chinese transformer parts supplier to something more like a diversified global power technology platform. Which sets up a more analytical question: in the rigorous frameworks that long-term investors actually use to think about competitive position, how does Sieyuan actually score?

VII. Analysis: Hamilton's 7 Powers and Porter's 5 Forces

The temptation with a company that has compounded as smoothly as Sieyuan is to assume that the moat is obvious and inevitable. It is neither. The competitive position has been earned, in specific identifiable ways that map onto the formal frameworks long-term investors use to separate durable businesses from cyclical ones.

Begin with Hamilton Helmer's seven powers framework. Of the seven, three apply meaningfully to Sieyuan, one applies in a degraded form, and three do not really apply at all. That is, in fact, a more honest scoring than most company write-ups produce.

Scale economies in distribution and service are real. Sieyuan operates a service network that touches every Chinese province and a growing number of overseas markets. For a utility customer, the calculus is simple: when a piece of switchgear fails at three in the morning, can a qualified technician be on site within hours? Sieyuan's domestic answer is yes, almost everywhere, and that yes is the product of years of deliberate field-engineer hiring and spare-parts inventory. A new entrant, even one with a technically superior product, would need years and substantial capital to replicate that footprint. The same logic increasingly applies to overseas markets where Sieyuan has built local presence.

Switching costs are perhaps the strongest of the seven powers in Sieyuan's case, and the least appreciated. When a utility standardizes on a particular vendor's GIS at a given voltage class, the consequences ripple through the organization for decades. Spare parts inventory is bought to fit that vendor's bays. Maintenance crews are trained on that vendor's interlocks, gas-handling procedures, and diagnostic software. Engineering institutes design future substations around that vendor's standard footprint. Replacing the incumbent vendor on the next project means absorbing the cost of new spares, retraining, redesign, and the operational risk of a heterogeneous fleet. Most utilities, given the choice between a marginally better competitor and the standardization advantage of the incumbent, choose the incumbent. Sieyuan has been on the winning side of that math for over a decade in China and is increasingly on the winning side abroad.

The cornered resource power, in the Helmer framework, is something a competitor cannot replicate even if it sees and understands the resource. For Sieyuan, the closest thing to a cornered resource is the management culture itself. Specifically, the combination of professional, non-dynastic governance, broad employee ownership, low engineer turnover, and patient capital allocation. A competitor can read about this culture in the annual report. A competitor cannot transplant it. Cultures are downstream of decades of decisions, hires, and small daily reinforcements, and they can be eroded much faster than they can be built. This is, structurally, the most valuable thing Sieyuan owns.

Counter-positioning, network economies, branding, and process power apply in various weaker forms but are not the load-bearing elements of the moat. The brand matters at the margins, particularly internationally where the Haefely halo helps, but Sieyuan is not a brand-driven business in the way that, say, ABB or Schneider can claim. Process power exists in manufacturing efficiency but is not a unique structural advantage.

Now turn to Porter's five forces, which speak more directly to industry structure than to firm-specific moats. The picture here is more mixed and more honest about the risks.

Rivalry within the Chinese power equipment industry is genuinely intense. The state-affiliated giants, NARI, Pinggao, Xuji, TBEA, China XD, and a long tail of regional players, all compete for the same State Grid procurement awards, often on price-led tenders. Margins on standard products have been pressured for years and will continue to be. Sieyuan's defense has been to compete on product cycles rather than on commodity tonnage, to win the next-generation specifications before they become the previous generation's race to the bottom.

Threat of new entrants is moderate. The capital requirements, type-test certifications, and reference-installation track records required to enter the high-voltage equipment market constitute a real barrier. New entrants have appeared in adjacent areas like SVGs and battery-grid integration, and Sieyuan has had to compete with newer firms there. But in core high-voltage GIS, transformers, and reactors, the credible challenger list is short and slow-moving.

Threat of substitutes is largely absent in the conventional equipment lines. Electricity has to be transformed, switched, and metered, and the physics of those operations has not fundamentally changed since the early twentieth century. Where substitution risk exists, it is at the periphery: solid-state transformers eventually displacing conventional units in specific applications, software-defined grid management reducing the need for some hardware redundancy. These are real but distant.

Bargaining power of buyers is the single largest structural risk Sieyuan faces. State Grid and China Southern Power Grid are, between them, by far the largest customers for power equipment in the world's largest power equipment market. Their procurement policies, their technical specifications, and their pricing decisions can move an entire industry's profitability in a single quarter. A decision by State Grid to favor a particular subsidiary on a major UHV award can mean billions of yuan of revenue migrating from one supplier to another. Sieyuan has lived inside this monopsony for its entire existence. Its strategic answer has been the deliberate, patient internationalization described earlier, plus the broadening into adjacent customer categories like industrial and renewable developers. Each step away from concentrated buyer dependence is, in five-forces language, a step toward better long-term unit economics.

Bargaining power of suppliers is generally manageable. Inputs are commodity-grade copper, electrical steel, switchgear components, and increasingly some specialty electronics for SVG and supercapacitor applications. Sieyuan's scale gives it reasonable negotiating leverage, and its geographic diversification reduces single-source exposure.

Synthesizing all of this, the picture that emerges is a company with two robust moat sources, switching costs and management culture, operating in an industry with genuinely intense rivalry and a single dominant structural risk in buyer concentration. The strategy has been, for years, to invest in deepening the moats and to systematically diversify away from the structural risk. Both efforts have been working.

VIII. The Playbook: Lessons for Investors

There is a body of unwritten wisdom that emerges from spending real time inside any genuinely well-run company. Sieyuan, for all its quietness, has assembled a playbook that is worth extracting because it is both unusual and potentially generalizable to other industrial bets.

The first lesson is the treatment of research and development as quasi-capital expenditure. Sieyuan has, for over a decade, spent in the neighborhood of seven percent of revenue annually on R&D. That figure does not move materially with the cycle. In good years, when revenue is growing fast, the absolute R&D dollars grow accordingly. In leaner years, when peers are cutting research budgets to defend margins, Sieyuan holds the line. The reasoning is straightforward. Power equipment product cycles are long, eight to twelve years from concept to volume production for a new GIS family, and the customers reward visible innovation pipelines. A competitor that pulses R&D spending up and down based on quarterly results ends up perpetually arriving at the new specification two years late. Two years, in a fifty-year-life infrastructure asset, is the difference between being the standard and being the alternative.

The second lesson is what might be called the "invisible giant" strategy for thriving in a state-dominated industry. The temptation, for a private firm operating beside state-owned giants, is either to lobby aggressively for policy carve-outs or to flee to international markets where the state's hand is lighter. Sieyuan has done neither. Instead, it has worked to become the supplier the state-owned customer cannot afford to discriminate against. By being demonstrably more cost-effective on specific product lines, by being faster on new product introduction, by being more reliable in field performance, the company has positioned itself such that excluding it from a major procurement actually costs the buying institution money and reputation. Being too good to ignore is a more durable strategy than being too connected to be excluded.

The third lesson is the energy transition tailwind, and here it is worth being precise rather than hand-wavy. The investment case for Sieyuan does not depend on any single forecast about renewable capacity additions or net-zero policy. It depends on a more robust observation: regardless of whether the world hits its 2030 climate targets, the world is going to install vastly more grid infrastructure over the next two decades than it did over the past two. Every megawatt of variable renewable generation requires more grid investment per megawatt of capacity than thermal generation did. Every electric vehicle on the road, every heat pump replacing a gas boiler, every electrified industrial process pulls more current through transmission and distribution networks that were originally designed for a different load profile.

This is the "shovels in a gold mine" framing. The end markets for the power equipment industry, the utilities, the renewable developers, the electrified industrial customers, will spend astonishing sums of capital over the coming two decades regardless of which generation technologies win, which countries hit their targets first, and which policy frameworks survive political rotation. Sieyuan, as a high-quality global supplier of the gear that all of those end markets need, captures a slice of that spending without having to bet on any single horse.

For investors who want to track the company's actual performance over time rather than just its narrative, three KPIs cut through the noise more cleanly than the dozens of metrics in any quarterly release.

The first is international revenue mix. Watching the percentage of total revenue generated outside China, and more specifically the year-over-year growth rate of that overseas segment, captures both the diversification away from the State Grid monopsony and the company's global competitive position. A stalling international growth rate would signal either competitive pressure or strategic retreat, both of which would be material.

The second is gross margin consistency, particularly within the GIS and switchgear product lines. Sieyuan's competitive position rests on the ability to hold pricing in a structurally competitive industry. Eroding gross margins would be the earliest visible sign of either commoditization or a loss of technical edge. Holding margins through a pricing-pressure cycle is the visible signature of the moat working.

The third is research and development intensity, measured both as a percentage of revenue and as absolute spend. The seven percent figure is a statement of strategic identity. A meaningful drop, particularly during a downturn, would suggest that the management discipline is weakening. A sustained increase, particularly directed at the segments where the energy transition is creating new demand, would suggest the company is leaning into the wave rather than coasting on it.

These three metrics, internationalization, margin stability, and R&D intensity, together capture more about the underlying health of the franchise than almost any other combination of disclosed numbers. Watch them.

IX. Conclusion & Bear/Bull Case

Stand back from the details and the company resolves into a simpler shape. A mid-sized Chinese industrial firm, founded in the tail of the country's reform era, that chose discipline over flash, professional management over founder cult, gradual capability building over transformative bets. A firm that exists at the meeting point of two of the most powerful long-duration trends of the next two decades, the global electrification of energy demand and the industrialization of clean generation, and that has positioned itself to sell critical hardware to almost everyone participating in those trends.

The bull case writes itself once the structural pieces are in place. Sieyuan continues its international expansion at its current pace, gradually shifting from a roughly twenty percent overseas revenue mix toward something closer to forty or fifty percent over the coming decade. The management culture and ESOP-driven engineer retention continue to throw off compounding R&D output, keeping the company on the leading edge of GIS, SVG, and supercapacitor product cycles. The Haefely brand and similar future bolt-on acquisitions provide premium positioning in markets where Chinese-origin firms have historically struggled. The underlying market for grid infrastructure expands at a pace that comfortably absorbs all the supply Sieyuan can profitably build.

If the bull case unfolds in full, the comparable to keep in mind is not actually any of the other power equipment companies. It is Huawei, in its trajectory through the telecommunications equipment industry. Huawei rose from a domestic Chinese supplier to the dominant global provider of carrier-grade telecom equipment by combining aggressive R&D, intense customer service, and a willingness to compete in markets that Western firms had under-invested in. Sieyuan, in its quieter and more capital-disciplined way, is following a structurally similar arc in power equipment. The "Huawei of power" framing is not a guarantee, but it is the right reference for the upside scenario.

The bear case is also coherent and worth taking seriously. The single largest external risk is geopolitics. As Western governments increasingly scrutinize Chinese-origin equipment in critical infrastructure, citing supply chain security and cybersecurity concerns, the addressable market for Sieyuan in North America, Western Europe, and Japan has narrowed and could narrow further. Tariffs, screening regimes, and outright bans on Chinese equipment in certain grid applications have already affected related industries and could affect Sieyuan's high-end international ambitions. The company can still grow rapidly in emerging markets and the Global South, but the premium-priced developed-market opportunity may remain partially closed.

The second risk is domestic. State Grid Corporation of China, while currently a relatively even-handed buyer that procures meaningfully from private suppliers like Sieyuan, could shift policy toward favoring its internal subsidiaries more aggressively. This has happened before in other sectors of the Chinese industrial economy and would compress Sieyuan's domestic revenue growth and margins simultaneously. The company's diversification efforts mitigate this risk but do not eliminate it.

The third risk is execution. The company has been remarkable for a long time, but the next decade involves bigger international footprint, larger turnkey projects, more complex integrations, and a deeper reliance on the same management team to scale without losing the disciplined culture that got them here. Founder transitions, even gradual ones, in companies with strong founder-shaped cultures sometimes go badly. Sieyuan's professional management ethos reduces this risk but does not negate it.

Hovering above all of this is a more philosophical observation. The company's distinctive feature, the thing that makes it interesting to long-term investors, is not any single product or market position. It is the consistency of judgment across decades. A management team that did not take the easy money on real estate during China's property bubble. That did not stretch the balance sheet during the post-2015 leverage boom. That did not chase European trophy assets at the peak. That did not abandon R&D during the pandemic-era cost compression. That did not hype itself during the 2021 EV-adjacent rerating.

That kind of judgment is uncommon in any market and rarer still in Chinese industrial firms. It is also, structurally, the hardest single thing for a competitor to replicate, the easiest thing to lose, and the thing most worth watching for any sign of erosion.

There is one final myth-versus-reality observation worth leaving with. The consensus narrative on Chinese industrial firms among many international investors is that they win on cost and lose on quality, that their financial reporting is suspect, and that their governance is opaque to the point of investability. Sieyuan, viewed honestly, is a counterexample on each count. It increasingly competes on technical merit rather than just price. Its financial reporting has been clean and consistent across multiple economic cycles. Its governance, while not perfect by Western institutional standards, is meaningfully more shareholder-friendly than the average Chinese industrial peer. Reality, in this case, is more interesting than the consensus story.

The invisible architect keeps building. Most of the world's investors will keep not noticing. That, more than any single financial metric, is the situation worth understanding before drawing conclusions.

X. Top Links & Further Reading

-

Sieyuan Electric annual reports, 2014 through 2024, with particular attention to the segment evolution from components to integrated solutions and the growth of international revenue disclosures.

-

State Grid Corporation of China ultra-high voltage transmission whitepapers, providing essential context for the procurement environment in which Sieyuan operates and the multi-decade buildout that has shaped industry capacity.

-

Public materials and trade press coverage of the 2019 Haefely acquisition, illustrating how a disciplined Chinese industrial acquirer can integrate a century-old European brand without destroying the underlying value.

-

Analytical work on China's electricity market reform, often referred to as Power Reform 2.0, which outlines how the gradual introduction of market-based pricing, ancillary service markets, and provincial spot markets favors operationally efficient suppliers and creates new demand categories for products like SVGs and supercapacitors.

-

International Energy Agency annual world energy investment reports, providing the macro context for grid infrastructure spending against which Sieyuan's growth needs to be judged.

-

Comparative financial analyses of global power equipment majors, ABB, Siemens Energy, Hitachi Energy, Schneider Electric, against Chinese peers, useful for benchmarking return on equity, R&D intensity, and international revenue mix.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube